On Alternative Algorithms for Computing Dynamic Mode Decomposition

Abstract

1. Introduction

1.1. Description of the Standard DMD Algorithm

| Algorithm 1 Exact DMD |

Input: Data matrices X and Y, and rank r. Output: DMD modes and eigenvalues 1: Procedure DMD(X,Y,r). 2: (Reduced r-rank SVD of X) 3: (Low-rank approximation of A) 4: (Eigen-decomposition of ) 5: (DMD modes of A) 6: End Procedure |

1.2. Matrix Similarity

2. New DMD Algorithms

2.1. An Alternative of Exact DMD Algorithm

| Algorithm 2 Alternative exact DMD |

Input: Data matrices X and Y, and rank r. Output: DMD modes and eigenvalues 1: Procedure DMD(X,Y,r). 2: (Reduced r-rank SVD of X) 3: (Low-rank approximation of A) 4: (Eigen-decomposition of ) 5: (DMD modes of A) 6: End Procedure |

2.2. A New DMD Algorithm for Full Rank Dataset

| Algorithm 3 DMD Algorithm for full rank dataset |

Input: Data matrices X and Y. Output: DMD modes and eigenvalues 1: Procedure DMD(X,Y). 2: (Low-rank approximation of A) 3: (Eigen-decomposition of ) 4: (DMD modes of A) 5: End Procedure |

2.3. In Terms of Companion Matrix

2.4. Computational Cost and Memory Requirement

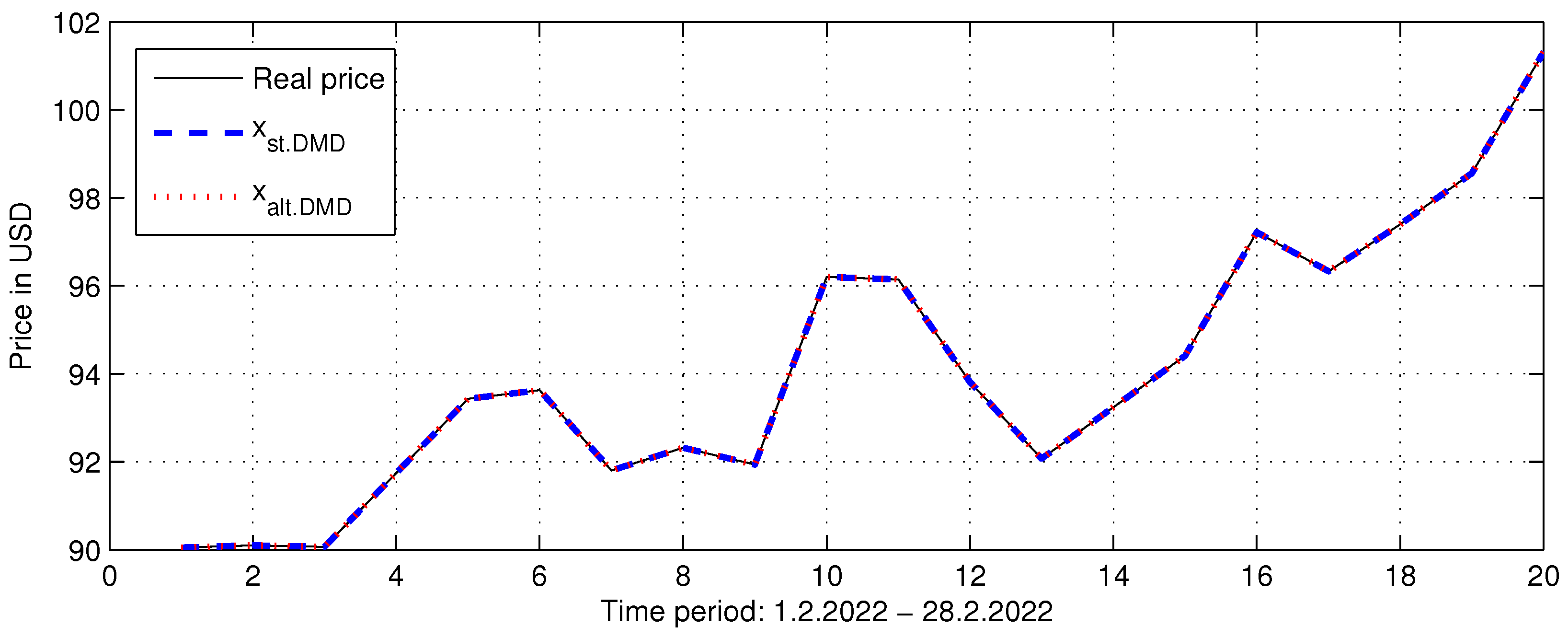

3. Numerical Illustrative Examples

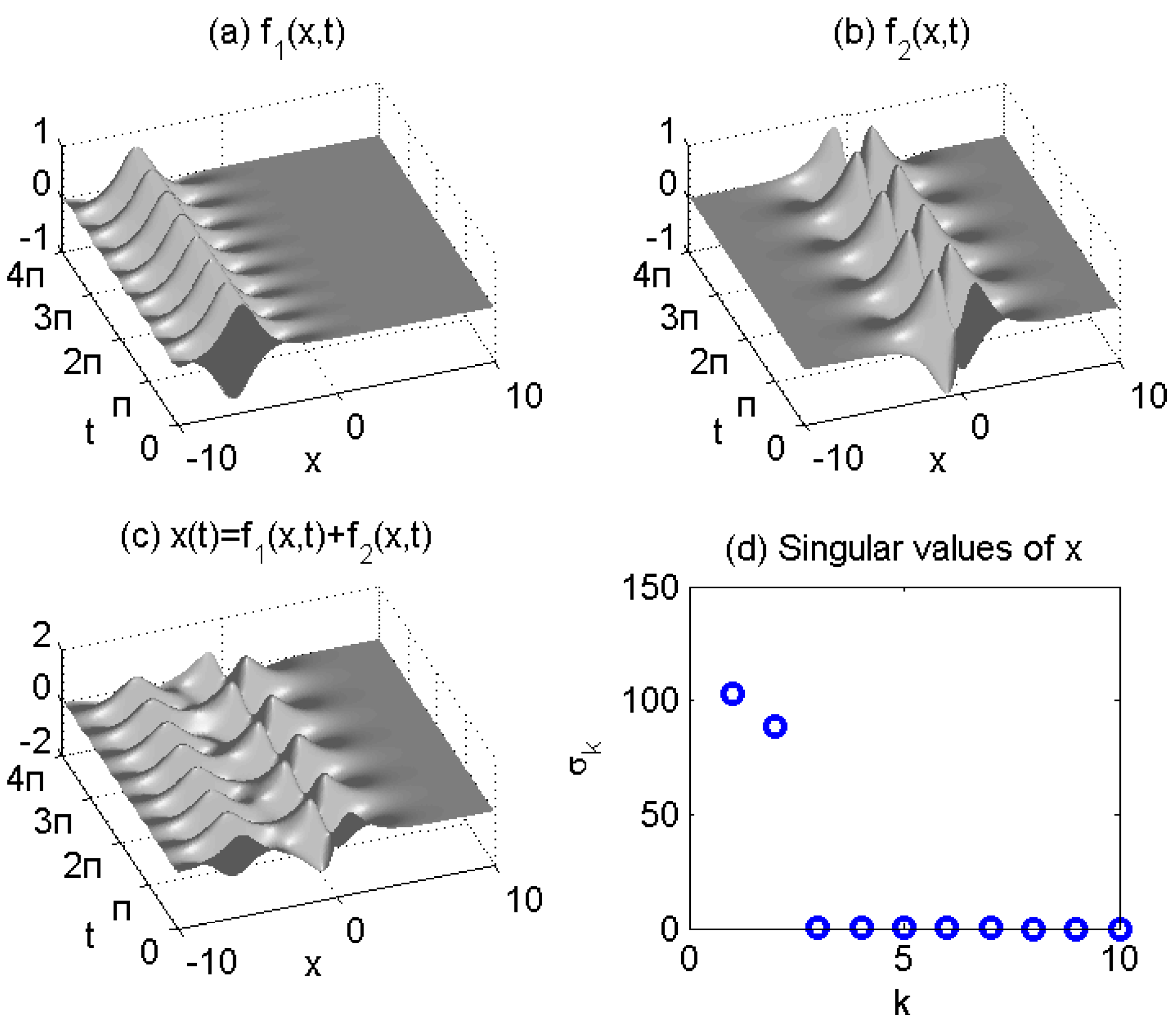

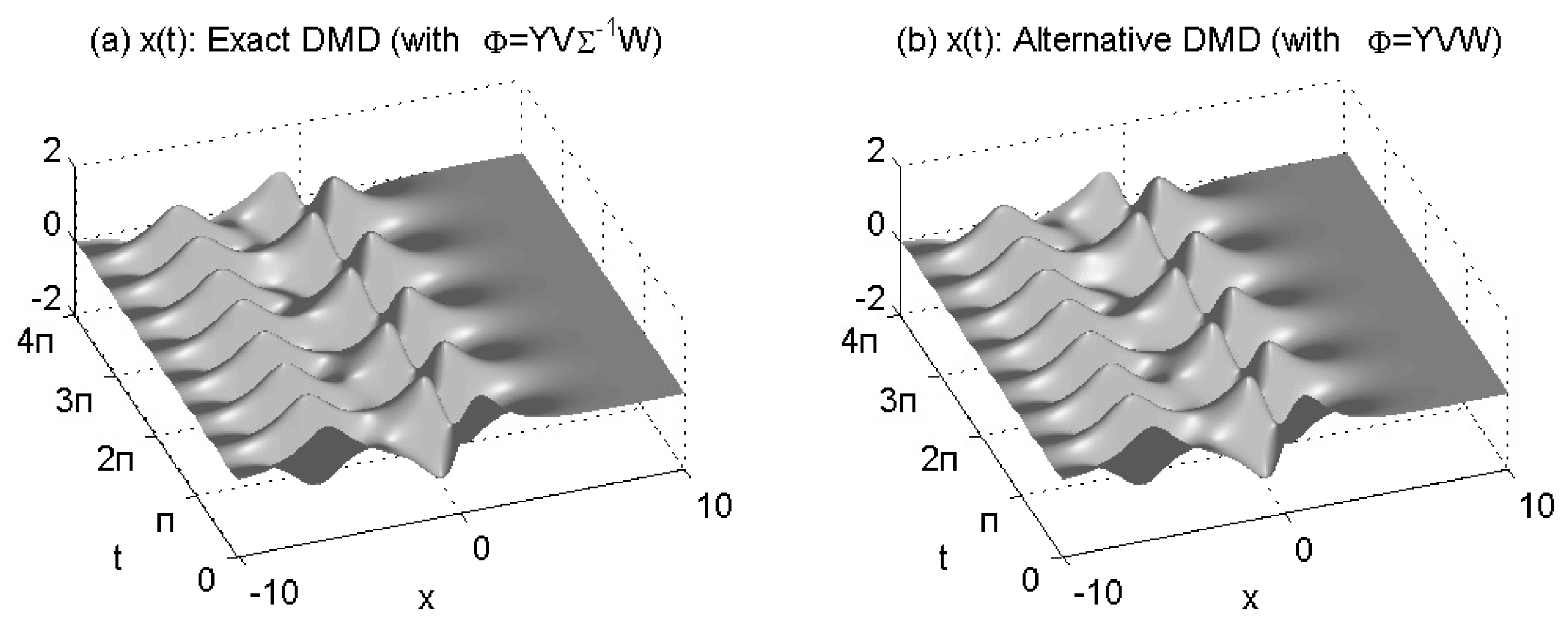

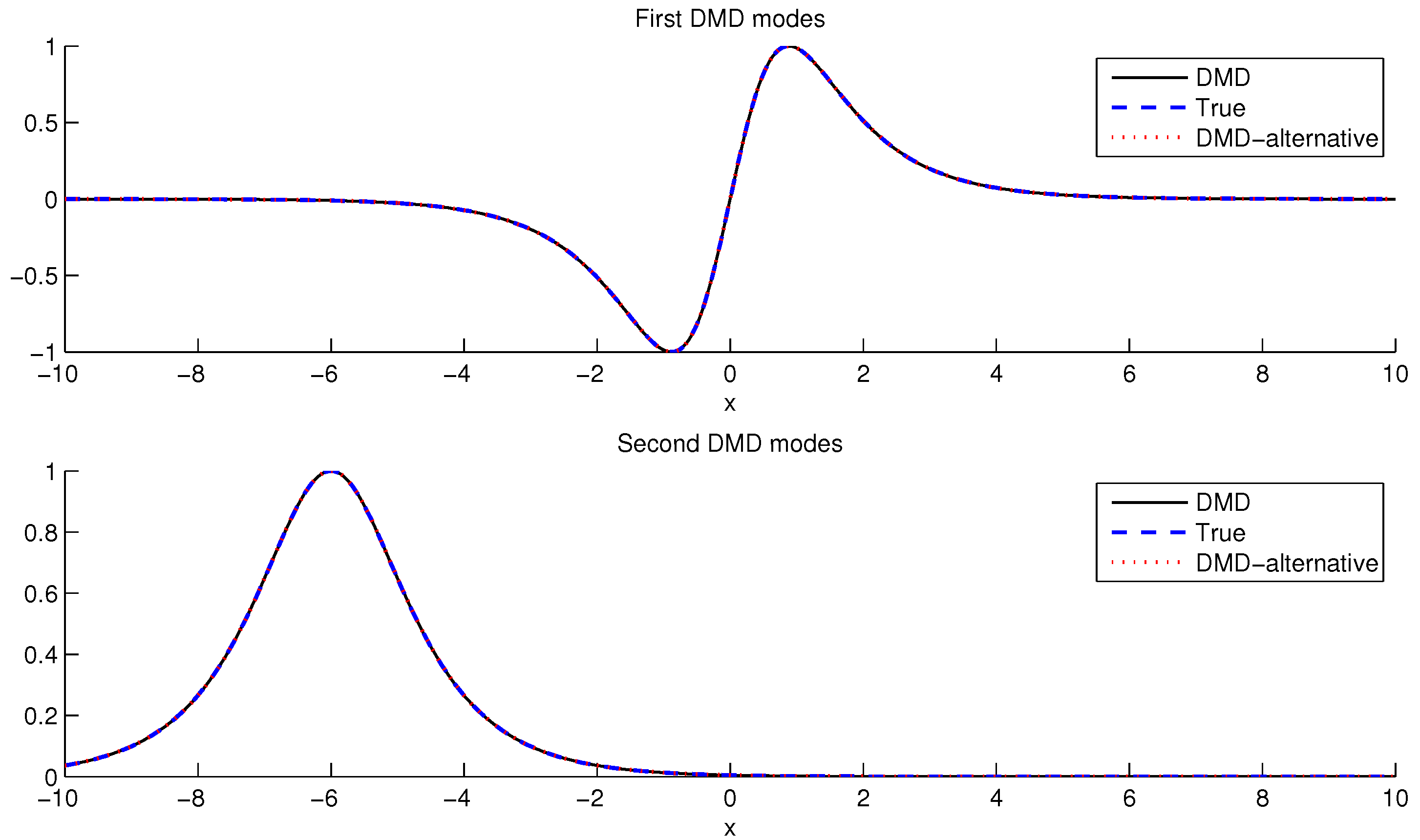

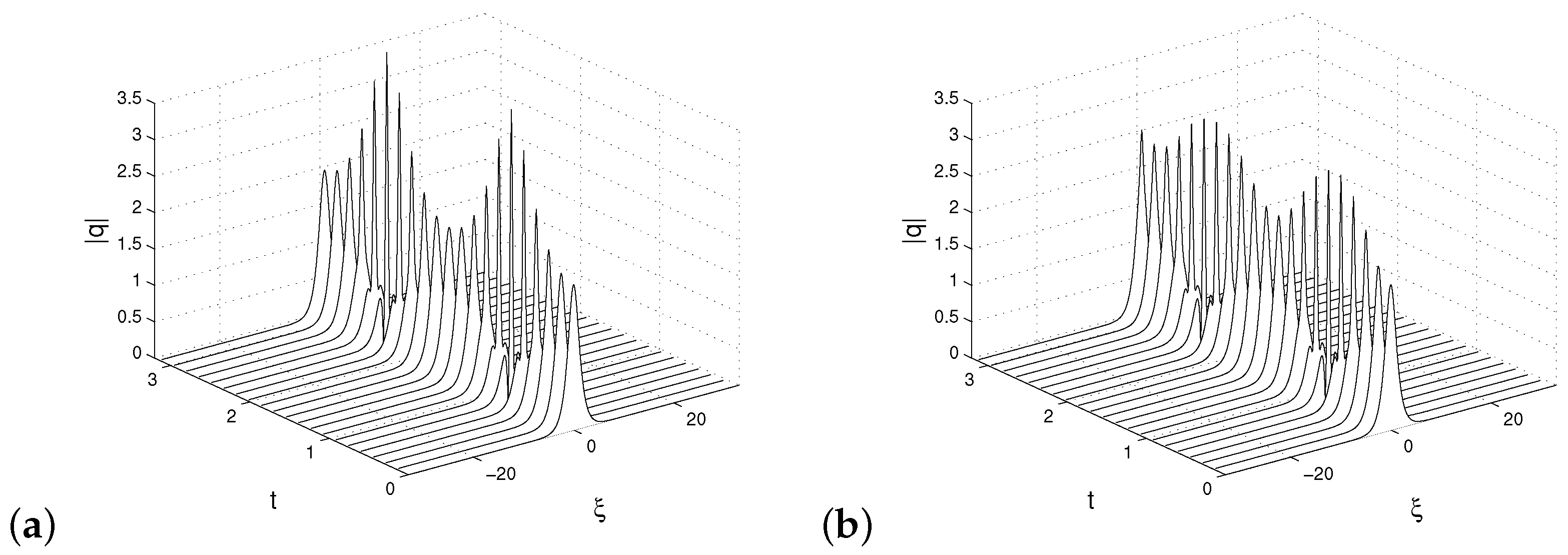

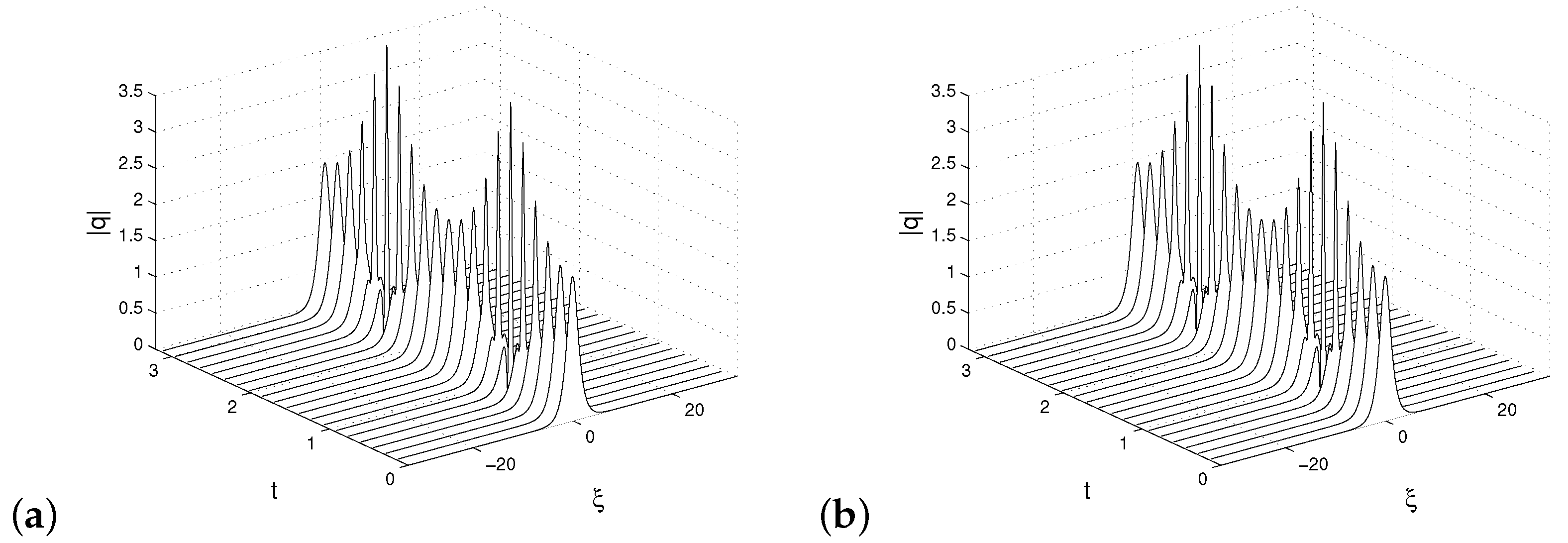

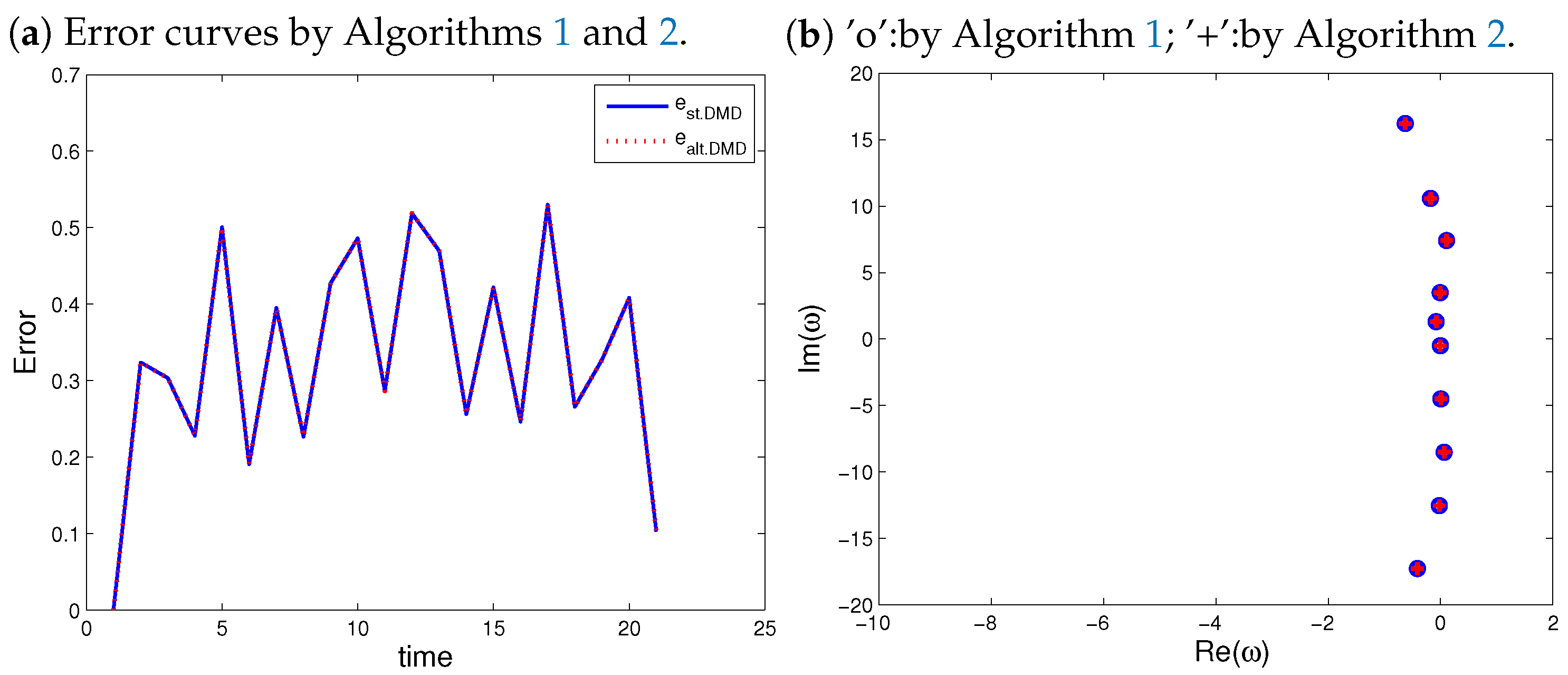

3.1. Example 1: Spatiotemporal Dynamics of Two Signals

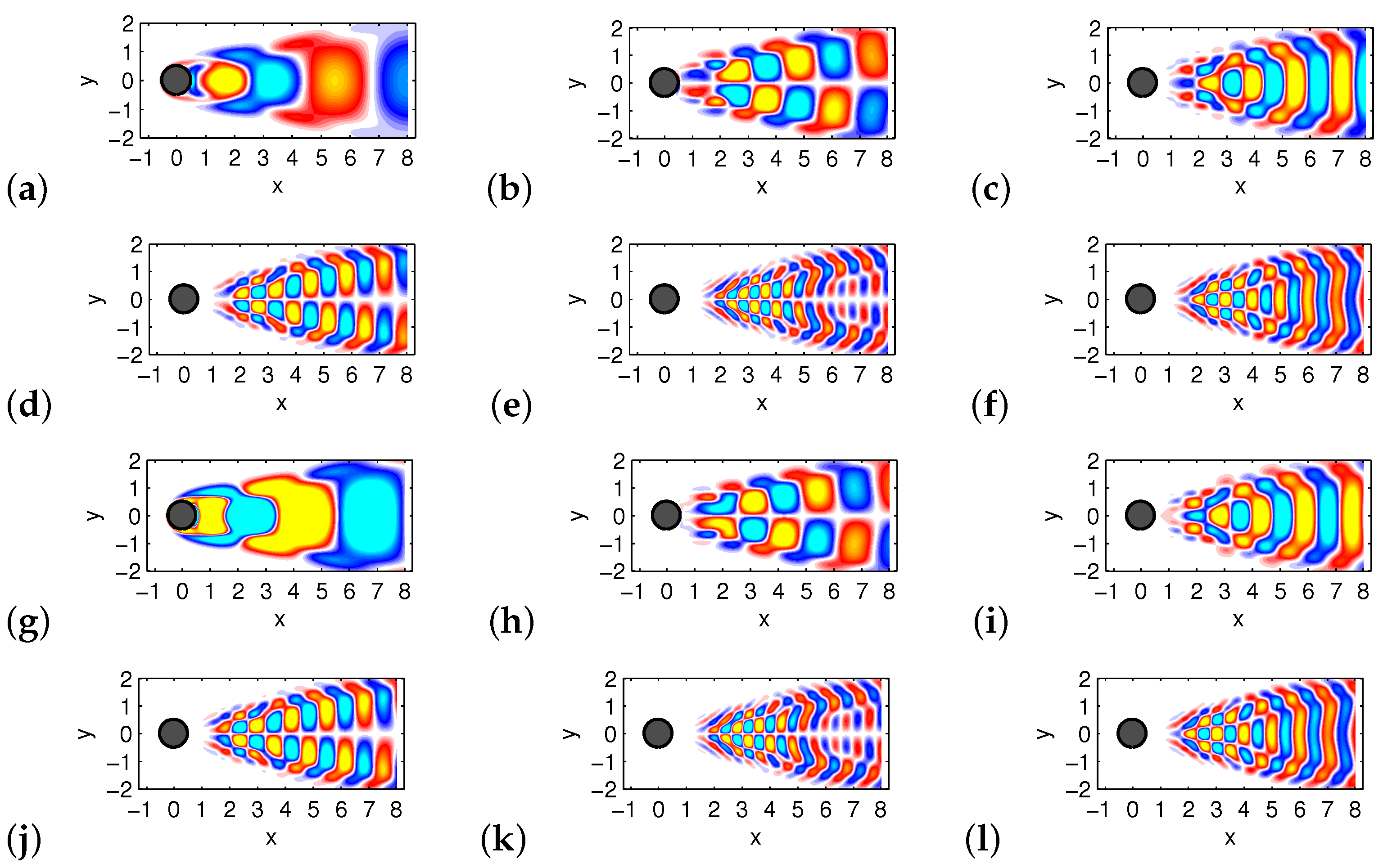

3.2. Example 2: Re = 100 Flow around a Cylinder Wake

3.3. Example 3: DMD with Different Koopman Observables

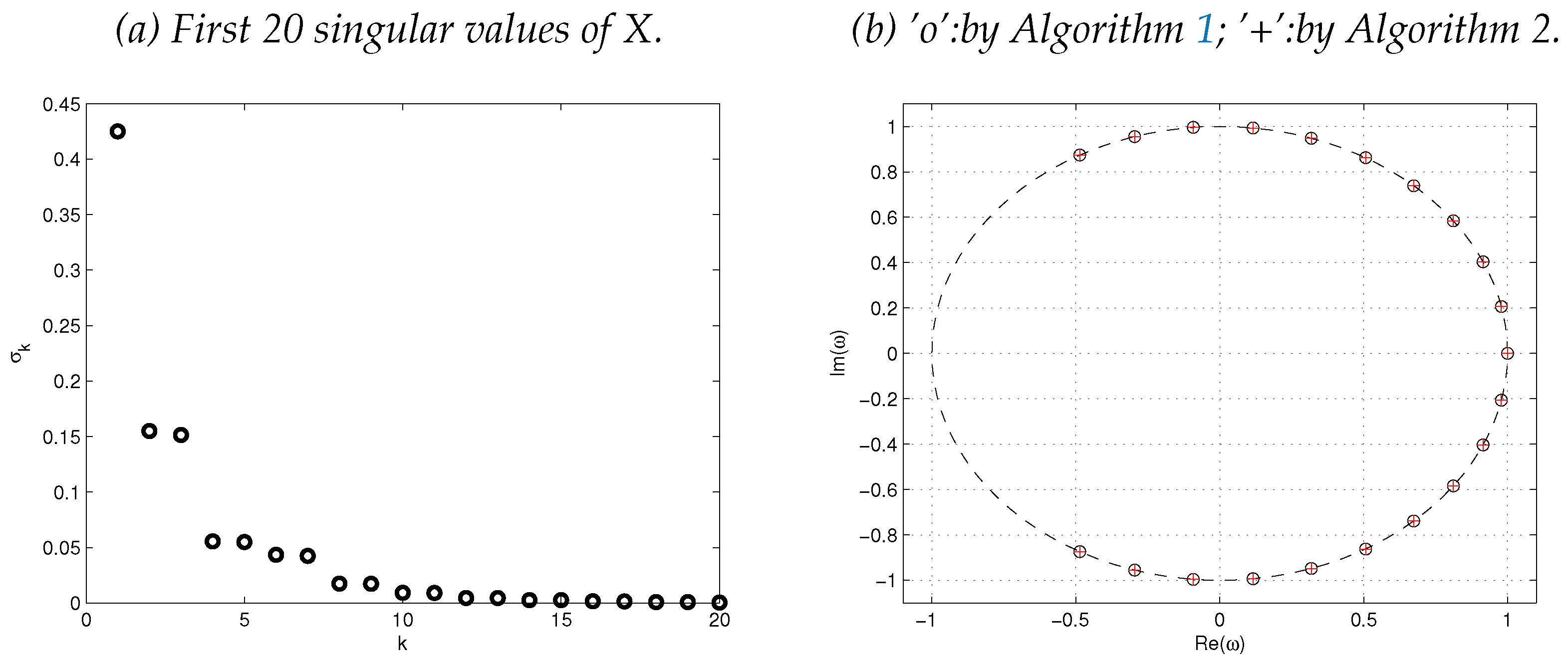

3.4. Example 4: Standing Wave

4. Conclusions

Funding

Conflicts of Interest

References

- Schmid, P.J.; Sesterhenn, J. Dynamic mode decomposition of numerical and experimental data. In Proceedings of the 61st Annual Meeting of the APS Division of Fluid Dynamics, San Antonio, TX, USA, 23–25 November 2008; American Physical Society: Washington, DC, USA, 2008. [Google Scholar]

- Rowley, C.W.; Mezić, I.; Bagheri, S.; Schlatter, P.; Henningson, D.S. Spectral analysis of nonlinear flows. J. Fluid Mech. 2009, 641, 115–127. [Google Scholar] [CrossRef]

- Mezić, I. Spectral properties of dynamical systems, model reduction and decompositions. Nonlinear Dyn. 2005, 41, 309–325. [Google Scholar] [CrossRef]

- Chen, K.K.; Tu, J.H.; Rowley, C.W. Variants of dynamic mode decomposition: Boundary condition, Koopman, and Fourier analyses. J. Nonlinear Sci. 2012, 22, 887–915. [Google Scholar] [CrossRef]

- Grosek, J.; Nathan Kutz, J. Dynamic Mode Decomposition for Real-Time Background/Foreground Separation in Video. arXiv 2014, arXiv:1404.7592. [Google Scholar]

- Proctor, J.L.; Eckhoff, P.A. Discovering dynamic patterns from infectious disease data using dynamic mode decomposition. Int. Health 2015, 7, 139–145. [Google Scholar] [CrossRef]

- Brunton, B.W.; Johnson, L.A.; Ojemann, J.G.; Kutz, J.N. Extracting spatial–temporal coherent patterns in large-scale neural recordings using dynamic mode decomposition. J. Neurosci. Methods 2016, 258, 1–15. [Google Scholar] [CrossRef]

- Mann, J.; Kutz, J.N. Dynamic mode decomposition for financial trading strategies. Quant. Financ. 2016, 16, 1643–1655. [Google Scholar] [CrossRef]

- Cui, L.X.; Long, W. Trading Strategy Based on Dynamic Mode Decomposition: Tested in Chinese Stock Market. Phys. A Stat. Mech. Its Appl. 2016, 461, 498–508. [Google Scholar]

- Kuttichira, D.P.; Gopalakrishnan, E.A.; Menon, V.K.; Soman, K.P. Stock price prediction using dynamic mode decomposition. In Proceedings of the 2017 International Conference on Advances in Computing, Communications and Informatics (ICACCI), Udupi, India, 13–16 September 2017; pp. 55–60. [Google Scholar] [CrossRef]

- Berger, E.; Sastuba, M.; Vogt, D.; Jung, B.; Ben Amor, H. Estimation of perturbations in robotic behavior using dynamic mode decomposition. J. Adv. Robot. 2015, 29, 331–343. [Google Scholar] [CrossRef]

- Schmid, P.J. Dynamic mode decomposition of numerical and experimental data. J. Fluid Mech. 2010, 656, 5–28. [Google Scholar] [CrossRef]

- Seena, A.; Sung, H.J. Dynamic mode decomposition of turbulent cavity flows for self-sustained oscillations. Int. J. Heat Fluid Flow 2011, 32, 1098–1110. [Google Scholar] [CrossRef]

- Schmid, P.J. Application of the dynamic mode decomposition to experimental data. Exp. Fluids 2011, 50, 1123–1130. [Google Scholar] [CrossRef]

- Mezić, I. Analysis of fluid flows via spectral properties of the Koopman operator. Annu. Rev. Fluid Mech. 2013, 45, 357–378. [Google Scholar] [CrossRef]

- Tu, J.H.; Rowley, C.W.; Luchtenburg, D.M.; Brunton, S.L.; Kutz, J.N. On dynamic mode decomposition: Theory and applications. J. Comput. Dyn. 2014, 1, 391–421. [Google Scholar] [CrossRef]

- Kutz, J.N.; Brunton, S.L.; Brunton, B.W.; Proctor, J.L. Dynamic Mode Decomposition: Data-Driven Modeling of Complex Systems; Society for Industrial and Applied Mathematics: Philadelphia, PL, USA, 2016; pp. 1–234. ISBN 978-1-611-97449-2. [Google Scholar]

- Bai, Z.; Kaiser, E.; Proctor, J.L.; Kutz, J.N.; Brunton, S.L. Dynamic Mode Decomposition for CompressiveSystem Identification. AIAA J. 2020, 58, 561–574. [Google Scholar] [CrossRef]

- Le Clainche, S.; Vega, J.M.; Soria, J. Higher order dynamic mode decomposition of noisy experimental data: The flow structure of a zero-net-mass-flux jet. Exp. Therm. Fluid Sci. 2017, 88, 336–353. [Google Scholar] [CrossRef]

- Anantharamu, S.; Mahesh, K. A parallel and streaming Dynamic Mode Decomposition algorithm with finite precision error analysis for large data. J. Comput. Phys. 2013, 380, 355–377. [Google Scholar] [CrossRef]

- Sayadi, T.; Schmid, P.J. Parallel data-driven decomposition algorithm for large-scale datasets: With application to transitional boundary layers. Theor. Comput. Fluid Dyn. 2016, 30, 415–428. [Google Scholar] [CrossRef]

- Maryada, K.R.; Norris, S.E. Reduced-communication parallel dynamic mode decomposition. J. Comput. Sci. 2020, 61, 101599. [Google Scholar] [CrossRef]

- Li, B.; Garicano-Mena, J.; Valero, E. A dynamic mode decomposition technique for the analysis of non–uniformly sampled flow data. J. Comput. Phys. 2022, 468, 111495. [Google Scholar] [CrossRef]

- Smith, E.; Variansyah, I.; McClarren, R. Variable Dynamic Mode Decomposition for Estimating Time Eigenvalues in Nuclear Systems. arXiv 2022, arXiv:2208.10942. [Google Scholar]

- Jovanović, M.R.; Schmid, P.J.; Nichols, J.W. Sparsity-promoting dynamic mode decomposition. Phys. Fluids 2014, 26, 024103. [Google Scholar] [CrossRef]

- Guéniat, F.; Mathelin, L.; Pastur, L.R. A dynamic mode decomposition approach for large and arbitrarily sampled systems. Phys. Fluids 2014, 27, 025113. [Google Scholar] [CrossRef]

- Cassamo, N.; van Wingerden, J.W. On the Potential of Reduced Order Models for Wind Farm Control: A Koopman Dynamic Mode Decomposition Approach. Energies 2020, 13, 6513. [Google Scholar] [CrossRef]

- Ngo, T.T.; Nguyen, V.; Pham, X.Q.; Hossain, M.A.; Huh, E.N. Motion Saliency Detection for Surveillance Systems Using Streaming Dynamic Mode Decomposition. Symmetry 2020, 12, 1397. [Google Scholar] [CrossRef]

- Babalola, O.P.; Balyan, V. WiFi Fingerprinting Indoor Localization Based on Dynamic Mode Decomposition Feature Selection with Hidden Markov Model. Sensors 2021, 21, 6778. [Google Scholar] [CrossRef]

- Lopez-Martin, M.; Sanchez-Esguevillas, A.; Hernandez-Callejo, L.; Arribas, J.I.; Carro, B. Novel Data-Driven Models Applied to Short-Term Electric Load Forecasting. Appl. Sci. 2021, 11, 5708. [Google Scholar] [CrossRef]

- Surasinghe, S.; Bollt, E.M. Randomized Projection Learning Method for Dynamic Mode Decomposition. Mathematics 2021, 9, 2803. [Google Scholar] [CrossRef]

- Li, C.Y.; Chen, Z.; Tse, T.K.; Weerasuriya, A.U.; Zhang, X.; Fu, Y.; Lin, X. A parametric and feasibility study for data sampling of the dynamic mode decomposition: Range, resolution, and universal convergence states. Nonlinear Dyn. 2022, 107, 3683–3707. [Google Scholar] [CrossRef]

- Mezic, I. On Numerical Approximations of the Koopman Operator. Mathematics 2022, 10, 1180. [Google Scholar] [CrossRef]

- Trefethen, L.; Bau, D. Numerical Linear Algebra; Society for Industrial and Applied Mathematics: Philadelphia, PL, USA, 1997. [Google Scholar]

- Golub, G.H.; Van Loan, C.F. Matrix Computations, 3rd ed.; The Johns Hopkins University Press: Baltimore, ML, USA, 1996. [Google Scholar]

- Lancaster, P.; Tismenetsky, M. The Theory of Matrices; Academic Press Inc.: San Diego, CA, USA, 1985. [Google Scholar]

- Nedzhibov, G. Dynamic Mode Decomposition: A new approach for computing the DMD modes and eigenvalues. Ann. Acad. Rom. Sci. Ser. Math. Appl. 2022, 14, 5–16. [Google Scholar] [CrossRef]

- Golub, G.H.; Van Loan, C.F. Matrix Computations; JHU Press: Baltimore, MD, USA, 2012; Volume 3. [Google Scholar]

- Bagheri, S. Koopman-mode decomposition of the cylinder wake. J. Fluid Mech. 2013, 726, 596–623. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Algorithm 1 | Algorithm 2 | Algorithm 3 | |

|---|---|---|---|

| () | () | () | |

| Reduced matrix | |||

| DMD modes |

| Cost of | Algorithm 1 | Algorithm 2 | Algorithm 3 |

|---|---|---|---|

| SVD ofX | − | ||

| Reduced matrix | |||

| DMD modes | |||

| Total cost |

| Matrix | Algorithm 1 | Algorithm 2 | Algorithm 3 |

|---|---|---|---|

| Y | |||

| − | |||

| r | − | − | |

| Total memory |

| Standard DMD | Alternative DMD | |

|---|---|---|

| Number of Cycles (k) | (Algorithm 1) | (Algorithm 2) |

| Standard DMD | Alternative DMD | |

|---|---|---|

| Relative errors |

| Standard DMD | Alternative DMD | |

|---|---|---|

| Number of Cycles (k) | (Algorithm 1) | (Algorithm 2) |

| Standard DMD | Alternative DMD | |

|---|---|---|

| Number of Cycles (k) | (Algorithm 1) | (Algorithm 2) |

| Standard DMD | Alternative DMD | |

|---|---|---|

| Number of Cycles (k) | (Algorithm 1) | (Algorithm 3) |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nedzhibov, G. On Alternative Algorithms for Computing Dynamic Mode Decomposition. Computation 2022, 10, 210. https://doi.org/10.3390/computation10120210

Nedzhibov G. On Alternative Algorithms for Computing Dynamic Mode Decomposition. Computation. 2022; 10(12):210. https://doi.org/10.3390/computation10120210

Chicago/Turabian StyleNedzhibov, Gyurhan. 2022. "On Alternative Algorithms for Computing Dynamic Mode Decomposition" Computation 10, no. 12: 210. https://doi.org/10.3390/computation10120210

APA StyleNedzhibov, G. (2022). On Alternative Algorithms for Computing Dynamic Mode Decomposition. Computation, 10(12), 210. https://doi.org/10.3390/computation10120210