An Agent-Based Approach to Interbank Market Lending Decisions and Risk Implications

Abstract

1. Introduction

- Can a multi-agent system with learning agents reconstruct the dynamics of an interbank network?

- Does the change of agent’s risk preference cause the system to become less prone to contagion?

2. Background and Related Literature

2.1. Interbank Network Topology

2.2. Multi-Agent Systems in Interbank Networks

2.3. Multi-Agent Learning Systems

3. Methodology

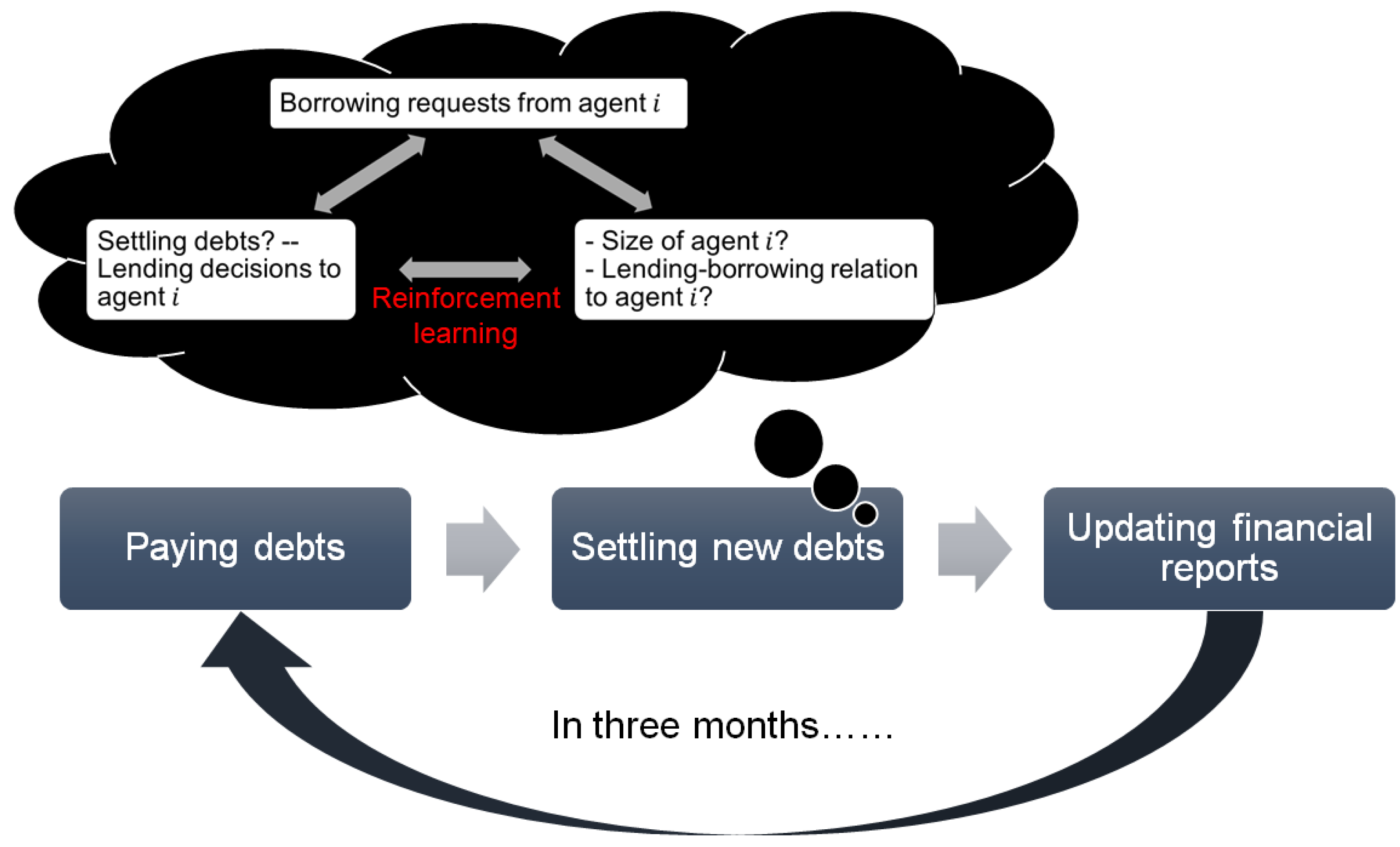

3.1. Multi-Agent Interbank Market Framework

3.1.1. Paying Debts

3.1.2. Settling New Debts

3.1.3. Updating Financial Reports

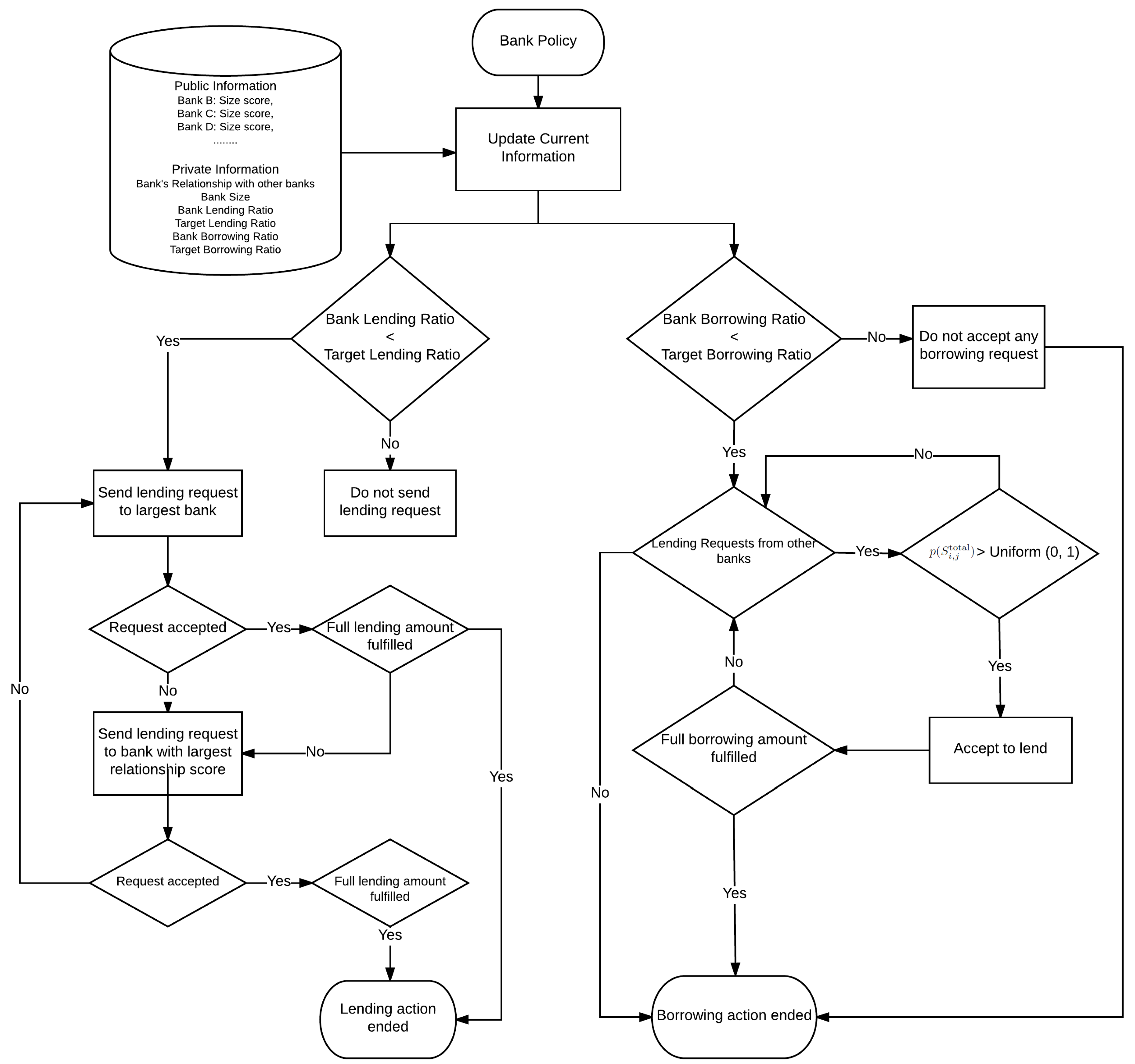

3.2. Bank Lending-Borrowing with Reinforcement Learning

3.2.1. Banking System States

3.2.2. Actions—Bank’s Lending and Borrowing Decisions

3.2.3. Temporal Difference Learning Update

4. Data

5. Model Validation

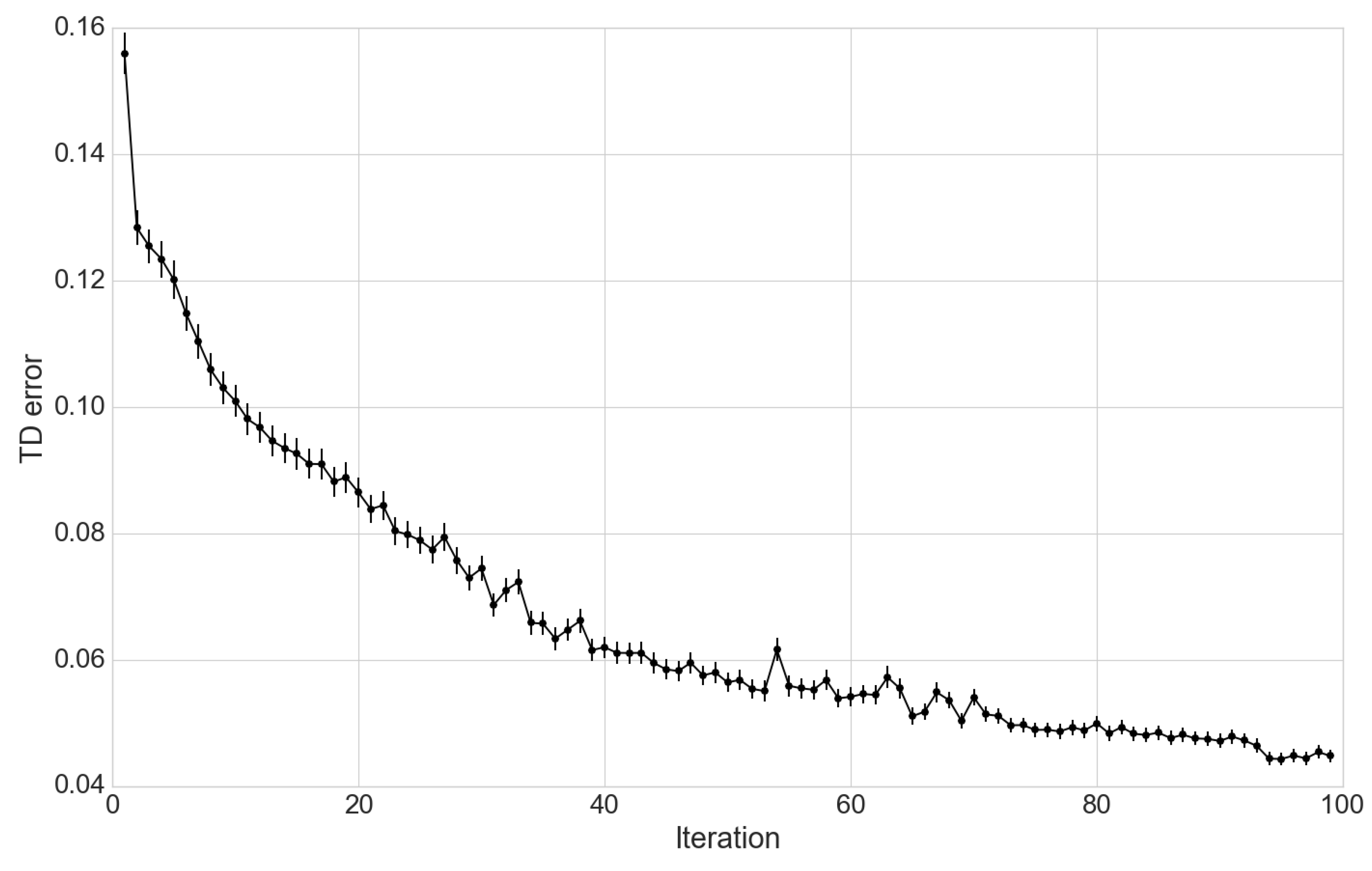

5.1. Convergence of Relationship Score Learning

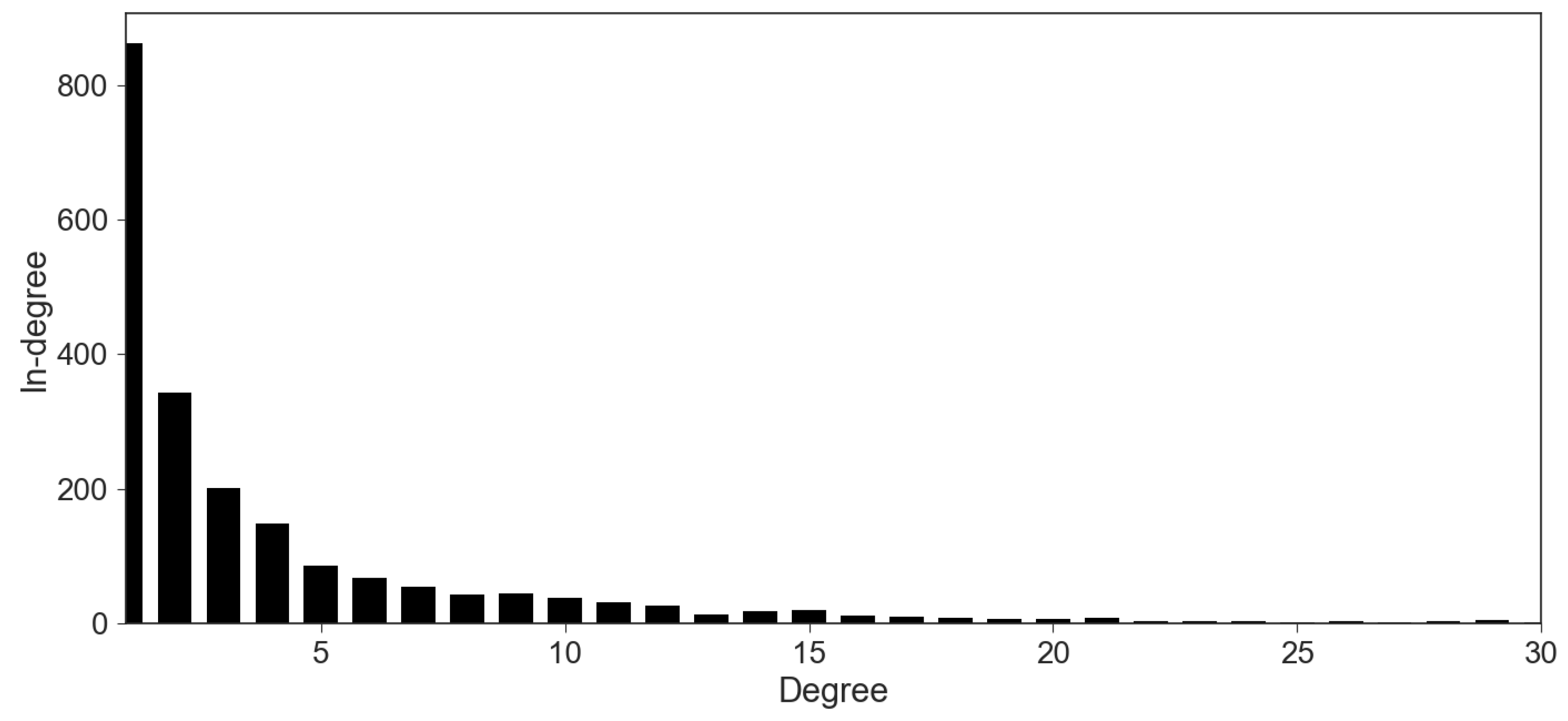

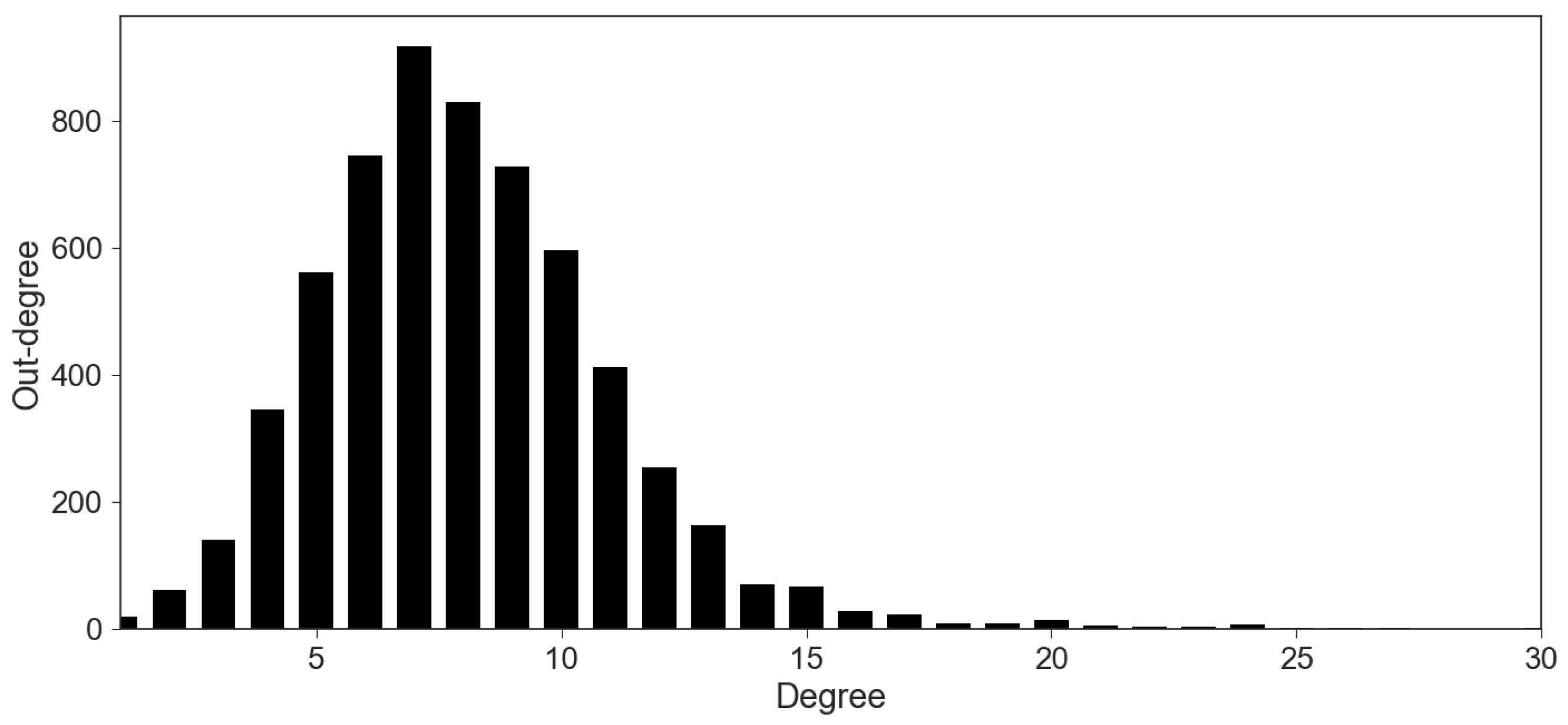

5.2. Network Properties Validation

- Degree: For each node in a network, the number of links directing to the node is called its in-degree, and the number of links directing out from the node is its out-degree. Average values are taken to measure the degree from the network-based perspective. As the “zero degree” nodes are not counted in the average, in-degree and out-degree values are different.

- Clustering coefficient: It is a closeness measure. A node’s clustering coefficient is the number of links between the node within its neighbors divided by the total number of links that could be formed between them. The in-clustering counts the links to the node, and the out-clustering counts the links from the node. Similar to network degree measures, network in-clustering and out-clustering are also average values across all nodes.

- Power law: A power law distribution is defined as . In network analysis, “power law” parameter is calibrated by fitting the degree histogram to the power law distribution. A detailed calibration methodology is introduced by [38]. In this paper, we regard the network as an indirected network when calibrating the power law.

6. Experiments and Discussion

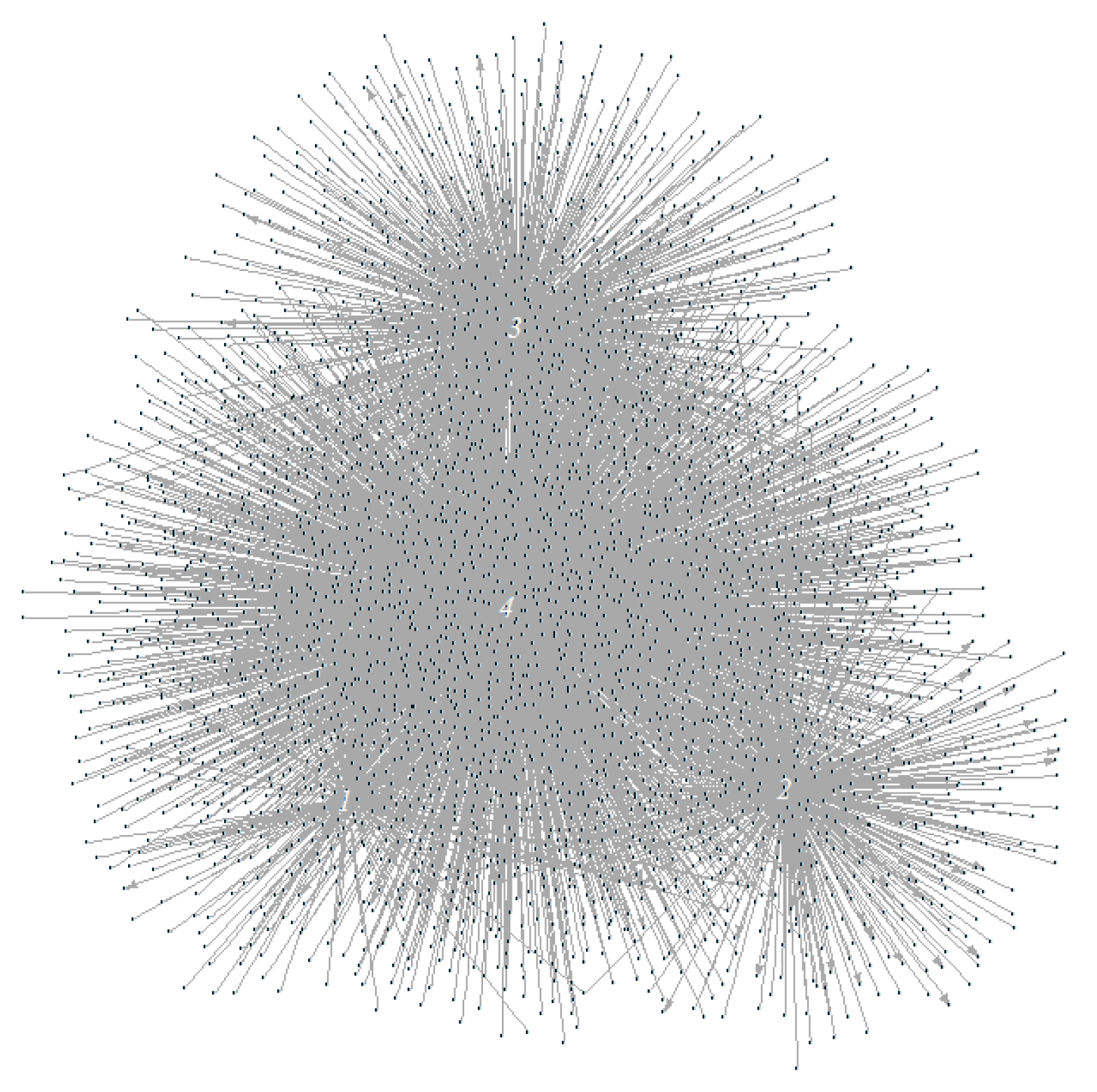

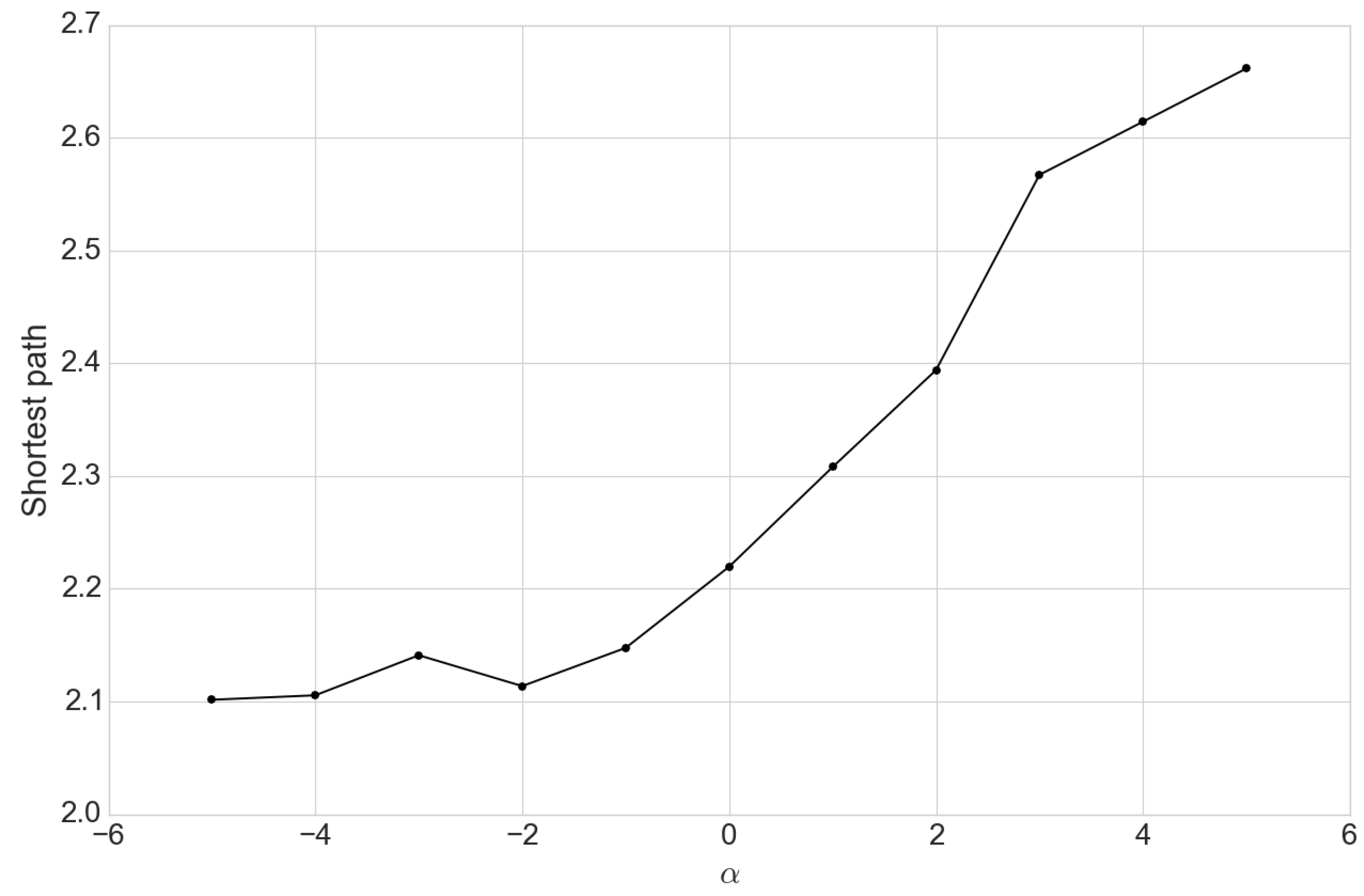

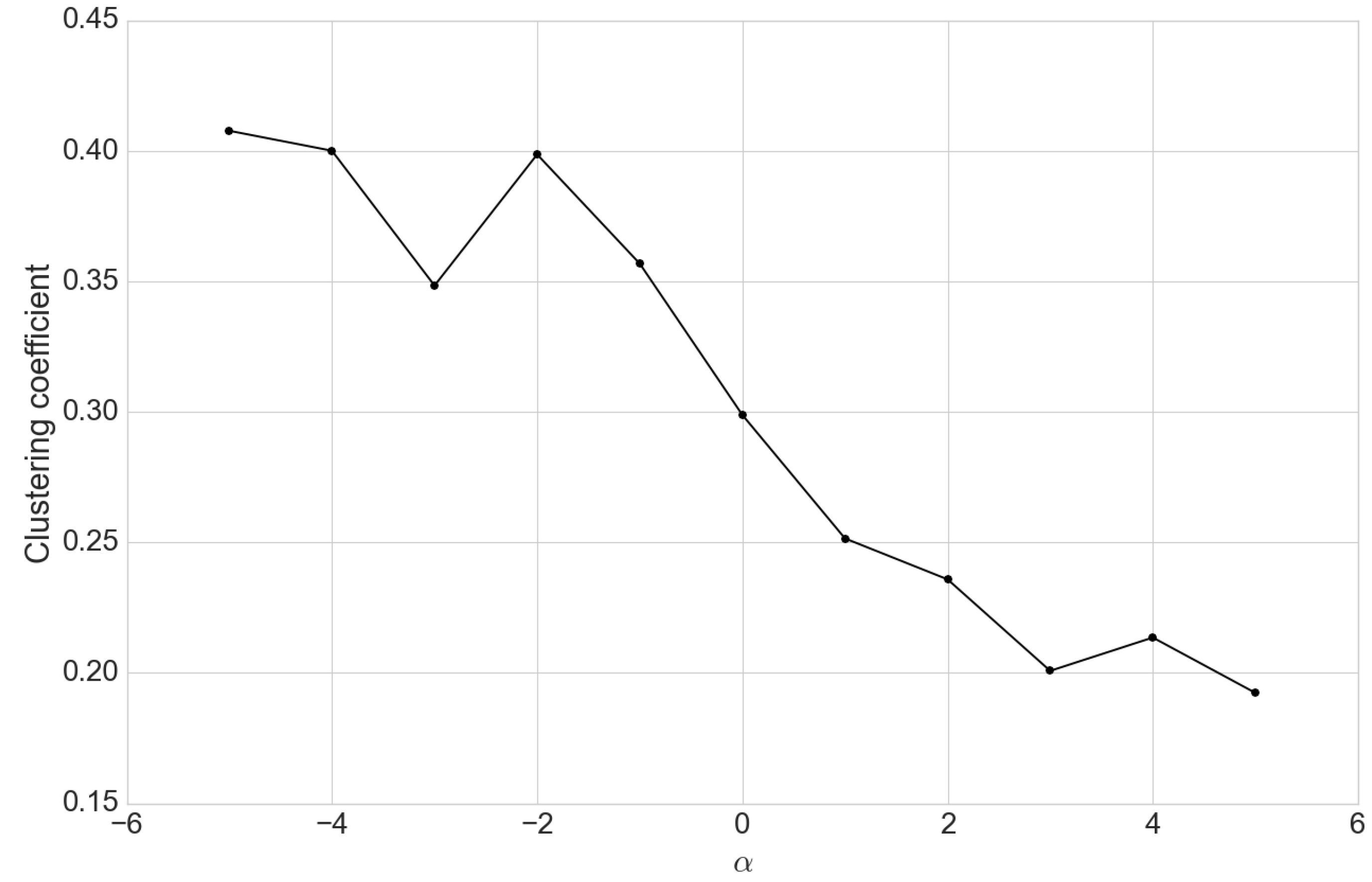

6.1. Interbank Network Topologies

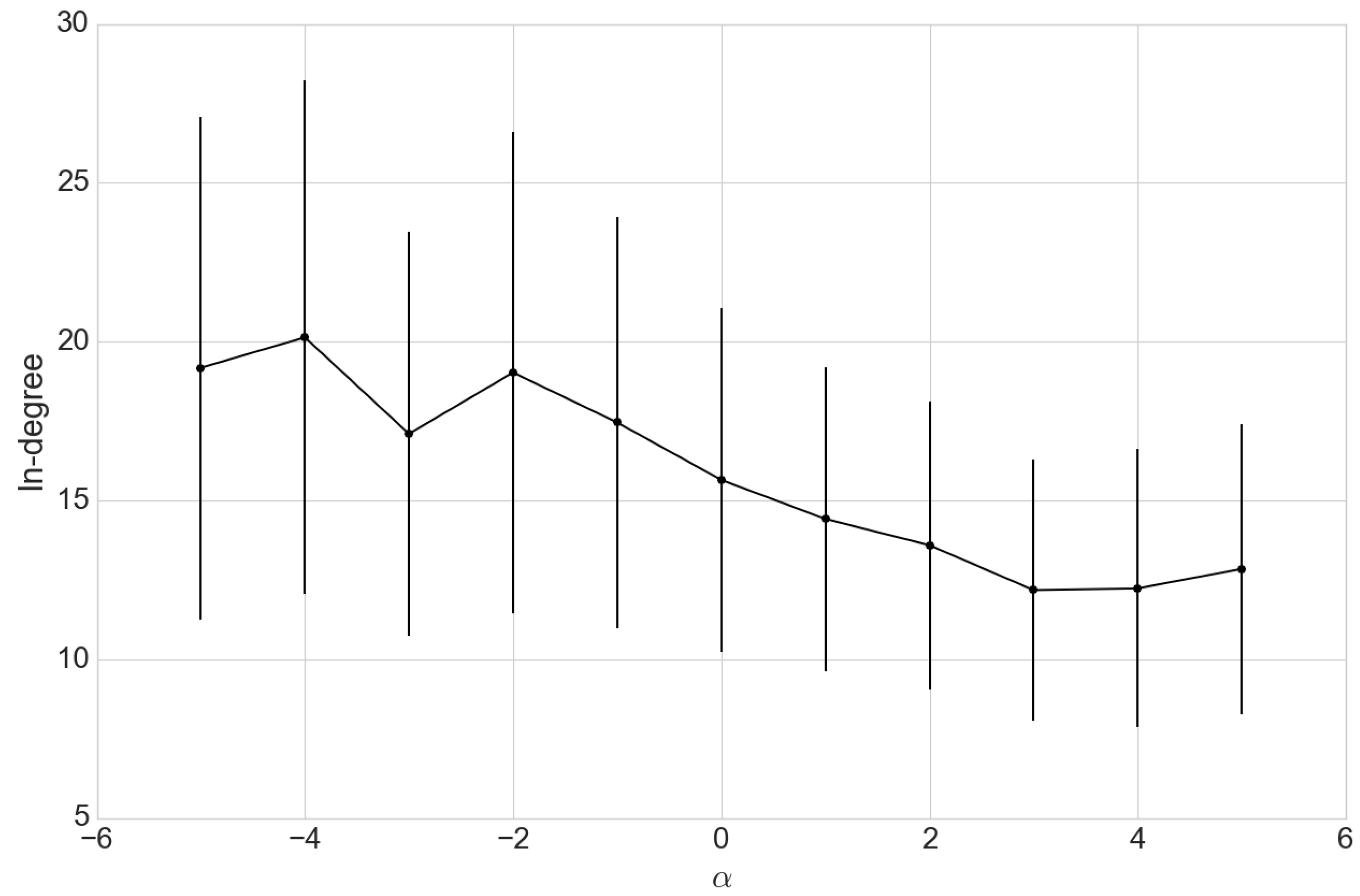

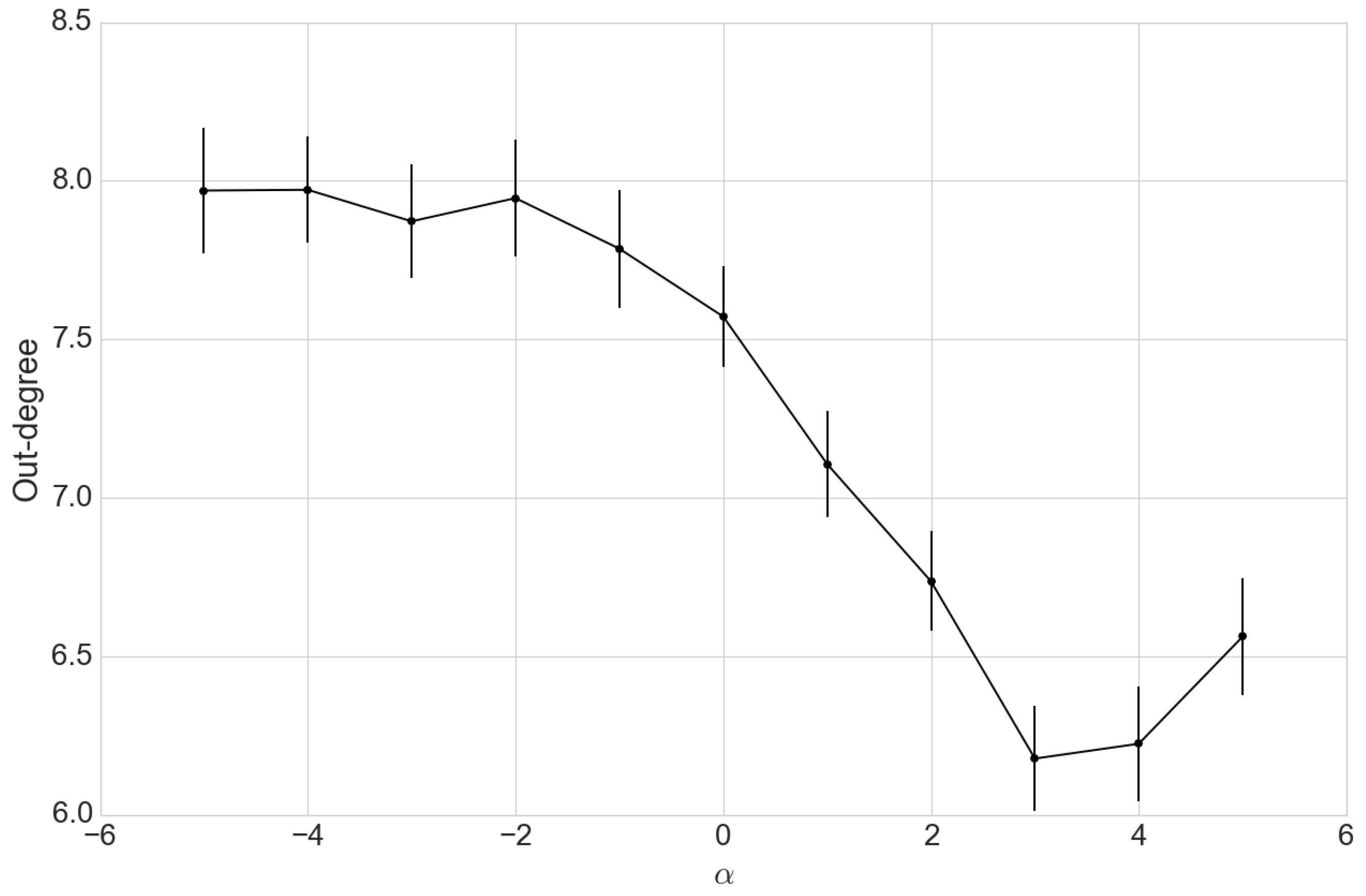

6.2. Network Adaptation and Risk Preferences

7. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Diamond, D.W.; Dybvig, P.H. Bank runs, deposit insurance, and liquidity. J. Polit. Econ. 1983, 91, 401–419. [Google Scholar] [CrossRef]

- Bhattacharya, S.; Gale, D.; Barnett, W.; Singleton, K. PRef. shocks, liquidity, and central bank policy. In Liquidity and Crises; Oxford University Press: New York, NY, USA, 2011. [Google Scholar]

- Brunnermeier, M.K. Deciphering the liquidity and credit crunch 2007–2008. J. Econ. Perspect. 2009, 23, 77–100. [Google Scholar] [CrossRef]

- Afonso, G.; Kovner, A.; Schoar, A. Stressed, not frozen: The federal funds market in the financial crisis. J. Financ. 2011, 66, 1109–1139. [Google Scholar] [CrossRef]

- Berrospide, J.M. Bank Liquidity Hoarding and the Financial Crisis: An Empirical Evaluation 2012; FEDS Working Paper No. 2013-03; Board of Governors of the Federal Reserve System (U.S.): Washington, DC, USA, 2013.

- Battiston, S.; Puliga, M.; Kaushik, R.; Tasca, P.; Caldarelli, G. Debtrank: Too central to fail? financial networks, the fed and systemic risk. Sci. Rep. 2012, 2, 541. [Google Scholar] [CrossRef] [PubMed]

- Eisenberg, L.; Noe, T.H. Systemic risk in financial systems. Manag. Sci. 2001, 47, 236–249. [Google Scholar] [CrossRef]

- Gai, P.; Kapadia, S. Contagion in financial networks. In Proceedings of the Royal Society of London A: Mathematical, Physical and Engineering Sciences; The Royal Society: London, UK, 2010; p. rspa20090410. [Google Scholar]

- Elliott, M.; Golub, B.; Jackson, M.O. Financial Networks and Contagion. Am. Econ. Rev. 2014, 104, 3115–3153. [Google Scholar] [CrossRef]

- Haldane, A.G.; May, R.M. Systemic risk in banking ecosystems. Nature 2011, 469, 351–355. [Google Scholar] [CrossRef] [PubMed]

- Boss, M.; Elsinger, H.; Summer, M.; Thurner, S. Network topology of the interbank market. Quant. Financ. 2004, 4, 677–684. [Google Scholar] [CrossRef]

- Upper, C.; Worms, A. Estimating bilateral exposures in the German interbank market: Is there a danger of contagion? Eur. Econ. Rev. 2004, 48, 827–849. [Google Scholar] [CrossRef]

- Cont, R.; Moussa, A.; Santos, E.B. Network structure and systemic risk in banking systems. In Handbook on Systemic Risk; Cambridge University Press: Cambridge, UK, 2013; pp. 327–368. [Google Scholar]

- Angelini, P.; Nobili, A.; Picillo, C. The interbank market after August 2007: what has changed, and why? J. Money Credit Bank. 2011, 43, 923–958. [Google Scholar] [CrossRef]

- Mistrulli, P.E. Assessing financial contagion in the interbank market: Maximum entropy versus observed interbank lending patterns. J. Bank. Financ. 2011, 35, 1114–1127. [Google Scholar] [CrossRef]

- Acharya, V.V. A theory of systemic risk and design of prudential bank regulation. J. Financ. Stab. 2009, 5, 224–255. [Google Scholar] [CrossRef]

- Georg, C.P. The effect of the interbank network structure on contagion and common shocks. J. Bank. Financ. 2013, 37, 2216–2228. [Google Scholar] [CrossRef]

- Ladley, D. Contagion and risk-sharing on the inter-bank market. J. Econ. Dyn. Control 2013, 37, 1384–1400. [Google Scholar] [CrossRef]

- Lux, T. Emergence of a core-periphery structure in a simple dynamic model of the interbank market. J. Econ. Dyn .Control 2015, 52, A11–A23. [Google Scholar] [CrossRef]

- Krause, J. The Purpose of Interbank Markets; Said Business School Working Paper 2016-17; Said Business School: Oxford, UK, 2016. [Google Scholar]

- Heider, F.; Hoerova, M.; Holthausen, C. Liquidity Hoarding and Interbank Market Spreads: The Role of Counterparty Risk; ECB Working Paper No. 1126; European Central Bank: Frankfurt, Germany, 2009. [Google Scholar]

- Iori, G.; Gabbi, G. A Network Analysis of the Italian Overnight Money Market. J. Econ. Dyn. Control 2008, 32, 259–278. [Google Scholar] [CrossRef]

- Roukny, T.; Georg, C.P.; Battiston, S. A Network Analysis of the Evolution of the German Interbank Market; Discussion Paper; Deutsche Bundesbank: Frankfurt, Germany, 2014. [Google Scholar]

- Cocco, J.F.; Gomes, F.J.; Martins, N.C. Lending relationships in the interbank market. J. Financ. Intermed. 2009, 18, 24–48. [Google Scholar] [CrossRef]

- Iyer, R.; Peydro, J.L. Interbank contagion at work: Evidence from a natural experiment. Rev. Financ. Stud. 2011, 24, 1337–1377. [Google Scholar] [CrossRef]

- Gilbert, N.; Terna, P. How to build and use agent-based models in social science. Mind Soc. 2000, 1, 57–72. [Google Scholar] [CrossRef]

- Macy, M.W.; Willer, R. From Factors to Factors: Computational Sociology and Agent-Based Modeling. Annu. Rev. Sociol. 2002, 28, 143–166. [Google Scholar] [CrossRef]

- Macal, C.M.; North, M.J. Tutorial on agent-based modelling and simulation. J. Simul. 2010, 4, 151–162. [Google Scholar] [CrossRef]

- Kok, C.; Montagna, M. Multi-Layered Interbank Model for Assessing Systemic Risk; ECB Working Paper No. 1944; European Central Bank: Frankfurt, Germany, 2016. [Google Scholar]

- Iori, G.; Mantegna, R.N.; Marotta, L.; Miccichè, S.; Porter, J.; Tumminello, M. Networked relationships in the e-MID Interbank market: A trading model with memory. J. Econ. Dyn. Control 2015, 50, 98–116. [Google Scholar] [CrossRef]

- Gobe, D.; Sunder, S. Allocative Efficiency of Markets with Zero-Intelligence Traders: Market as a Partial Substitute for Individual Rationality. J. Polit. Econ. 1993, 101, 119–137. [Google Scholar]

- Othman, A. Zero-intelligence agents in prediction markets. In Proceedings of the Seventh International Conference on Autonomous Agents and Multiagent Systems (AAMAS 2008), Estoril, Portugal, 12–16 May 2008; pp. 879–886. [Google Scholar]

- Sutton, R.S.; Barto, A.G. Reinforcement Learning: An Introduction; The MIT Press: Cambridge, MA, USA; London, UK, 1988. [Google Scholar]

- Liu, A.; Paddrik, M.; Yang, S.Y.; Zhang, X. Interbank contagion: An agent-based model approach to endogenously formed networks. J. Bank. Financ. 2017. [Google Scholar] [CrossRef]

- Anand, K.; Craig, B.; Von Peter, G. Filling in the blanks: Network structure and interbank contagion. Quant. Financ. 2015, 15, 625–636. [Google Scholar] [CrossRef]

- Tesauro, G. Practical Issues in Temporal Difference Learning. Mach. Learn. 1992, 277, 257–277. [Google Scholar] [CrossRef]

- Bech, M.L.; Atalay, E. The topology of the federal funds market. Phys. A Stat. Mech. Appl. 2010, 389, 5223–5246. [Google Scholar] [CrossRef]

- Clauset, A.; Shalizi, C.R.; Newman, M.E. Power-law distributions in empirical data. SIAM Rev. 2009, 51, 661–703. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Node Types: Banks’ size type is based on assets from 2001 to 2014, detailed approach is documented in [34] | |

| Large Banks | Bank of America, Citibank, J.P. Morgan Chase Banks, and Wells Fargo Bank |

| Small Banks | Other Banks |

| Link Types: | |

| Overnight debts | Federal funds, usually expire overnight |

| Short-term debts | Federal securities, usually expire within three months |

| Long-term debts | Loans expire less than one year |

| Asset: A | Liability: L |

|---|---|

| Overnight lending: | Overnight borrowing: |

| Short-term lending: | Short-term lending: |

| Long-term lending: | Long-term borrowing: |

| Cash and balance due: C | Other liabilities: OL |

| Other assets: OA | Equity: E |

| Equity Multiplier | E/A |

|---|---|

| Overnight lending, borrowing ratio | , |

| Short-term lending, borrowing ratio | , |

| Long-term lending, borrowing ratio | , |

| Min. | Median | Mean | Max. | |

|---|---|---|---|---|

| 0.00% | 1.29% | 2.49% | 94.82% | |

| 0.00% | 0.00% | 0.55% | 84.11% | |

| 0.00% | 0.00% | 0.23% | 36.18% | |

| 0.00% | 0.66% | 2.15% | 41.99% | |

| 0.00% | 0.00% | 0.25% | 76.43% | |

| 0.00% | 0.15% | 1.11% | 81.79% | |

| 4.20% | 9.20% | 11.38% | 99.24% |

| Parameter | Value |

|---|---|

| Large banks −1.0; small banks 0.0 | |

| 1.0 | |

| 0.5 | |

| 0.5 |

| Average In-Degree | Average Out-Degree | Average In-Clustering | Average Out-Clustering | Power Law | |

|---|---|---|---|---|---|

| U.S. Fed. Funds Market | 9.30 | 19.10 | 0.10 | 0.28 | 2.00 |

| Model | 10.51 | 17.17 | 0.03 | 0.31 | 2.00 |

| (0.14) | (0.09) | (0.00) | (0.02) | (0.00) |

| Overnight | Average Degree | Clustering Coefficient | Power Law | Average Path |

|---|---|---|---|---|

| Risk-Seeking Policy | 15.12 | 0.35 | 2.39 | 2.34 |

| Risk-Averse Policy | 11.51 | 0.19 | 2.42 | 2.66 |

| Short-term | Average Degree | Clustering Coefficient | Power Law | Average Path |

| Risk-Seeking Policy | 1.04 | 0.43 | 2.44 | 2.30 |

| Risk-Averse Policy | 1.04 | 0.53 | 2.29 | 2.21 |

| Long-term | Average Degree | Clustering Coefficient | Power Law | Average Path |

| Risk-Seeking Policy | 2.42 | 0.40 | 2.14 | 2.44 |

| Risk-Averse Policy | 2.42 | 0.57 | 2.15 | 2.28 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Liu, A.; Mo, C.Y.J.; Paddrik, M.E.; Yang, S.Y. An Agent-Based Approach to Interbank Market Lending Decisions and Risk Implications. Information 2018, 9, 132. https://doi.org/10.3390/info9060132

Liu A, Mo CYJ, Paddrik ME, Yang SY. An Agent-Based Approach to Interbank Market Lending Decisions and Risk Implications. Information. 2018; 9(6):132. https://doi.org/10.3390/info9060132

Chicago/Turabian StyleLiu, Anqi, Cheuk Yin Jeffrey Mo, Mark E. Paddrik, and Steve Y. Yang. 2018. "An Agent-Based Approach to Interbank Market Lending Decisions and Risk Implications" Information 9, no. 6: 132. https://doi.org/10.3390/info9060132

APA StyleLiu, A., Mo, C. Y. J., Paddrik, M. E., & Yang, S. Y. (2018). An Agent-Based Approach to Interbank Market Lending Decisions and Risk Implications. Information, 9(6), 132. https://doi.org/10.3390/info9060132