DebtG: A Graph Model for Debt Relationship

Abstract

:1. Introduction

- It presents a graph model of debt relationship between entities including individuals, enterprises, governments, etc.;

- It defines three basic debt structures, namely debt path, debt tree, and debt circuit;

- It proposes two algorithms to detect the three debt structures and possible methods to solve the debt clearing problem based on these structures;

- It carries out a profit analysis of the third-party platform and presents a case analysis using real-life debt data.

2. Related Works

- The entities involved in debt relationships have many attributes that affect debt clearing. For example, the due date of debt is more important than the amount of debt in determining the order of debt settlement. However, the current models only focus on the debt amount in order to clear the largest amount of debt;

- There is often more than one debt between a pair of entities, and these debts also have different attributes. An entity may prefer to settle earlier debts with higher discounts or vice versa. However, the current models only contain at most one debt between a pair of entities;

- It may be impossible to solve the debt clearing problem by constructing cycles with the help of the Ministry of Finance (see [3]) or subsidy center (see [4]). When the series of entities formed a debt path (see Section 3), refs. [3,4] added a third-party platform to the path to construct a cycle, and the platform paid the first debtor to clear the debts. However, the last creditor had no obligation to pay the platform because it did not owe the platform.

3. DebtG Model and Its Application

3.1. Formal Definitions

- is the set of vertices, and each vertex represents an entity (for example, enterprise, government, individual, bank, etc.). Each vertex has a unique ID;

- is the set of directed arcs, and each arc represents the corresponding entities have debt relationship. Specifically, denotes that the corresponding entity of owes that of . There may exist more than one arc between a pair of entities;

- is the attribute sets of vertices, and is the attribute set of . The attribute sets of vertices contain the name, address, assets, and other information of corresponding entities;

- is the attribute sets of arcs, and is the attribute set of . The attribute sets of arcs should contain the amount of debt, and it may also contain the debt arising/due date, priority, and other information of debt.

- Out-degree denotes is the debtor of entities;

- In-degree denotes is the creditor of entities.

3.2. Debt Structures of DebtG

3.3. Detection and Elimination of Debt Circuit

| Algorithm 1 Detect and Eliminate Debt Circuits | |

| Required: A DebtG | |

| Ensure: A set of debt circuits | |

| 1. | for each do |

| 2. | |

| 3. | |

| 4. | end for |

| 5. | |

| 6. | for each do |

| 7. | if then |

| 8. | |

| 9. | else if then |

| 10. | |

| 11. | end if |

| 12. | if or then |

| 13. | |

| 14. | end if |

| 15. | delete and its associate arcs from |

| 16. | |

| 17. | end for |

| 18. | while do |

| 19. | Sort according to a certain criterion |

| 20. | the first vertex in |

| 21. | detect a debt circuit starting with |

| 22. | if exists then |

| 23. | |

| 24. | subtract from all attributes of all arcs of |

| 25. | else |

| 26. | |

| 27. | end if |

| 28. | end while |

| 29. | return all debt circuits |

3.4. Detection and Clearing of Debt Tree and Debt Path

| Algorithm 2 Detect and Clear Debt Trees and Debt Paths | |

| Required: An acyclic DebtG | |

| Ensure: A set of debt trees and debt paths | |

| 1. | Sort according to a certain criterion |

| 2. | candidate tree roots and path heads |

| 3. | for each do |

| 4. | is a queue |

| 5. | is the list of vertices of a debt tree or debt path |

| 6. | while is not empty do |

| 7. | |

| 8. | for each and do |

| 9. | |

| 10. | |

| 11. | end for |

| 12. | end while |

| 13. | for each do |

| 14. | |

| 15. | end for |

| 16. | |

| 17. | |

| 18. | while is not empty do |

| 19. | |

| 20. | for each or do |

| 21. | if then |

| 22. | |

| 23. | end if |

| 24. | end while |

| 25. | resolve the debt tree or debt path according to values of all vertices |

| 26. | end for |

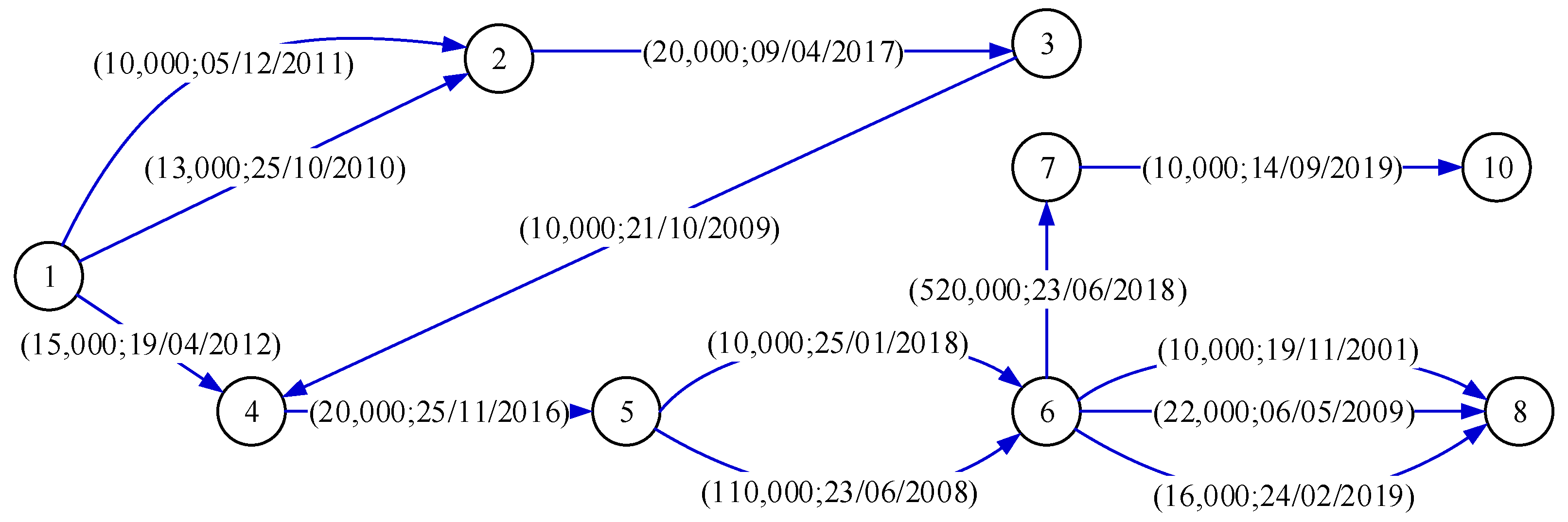

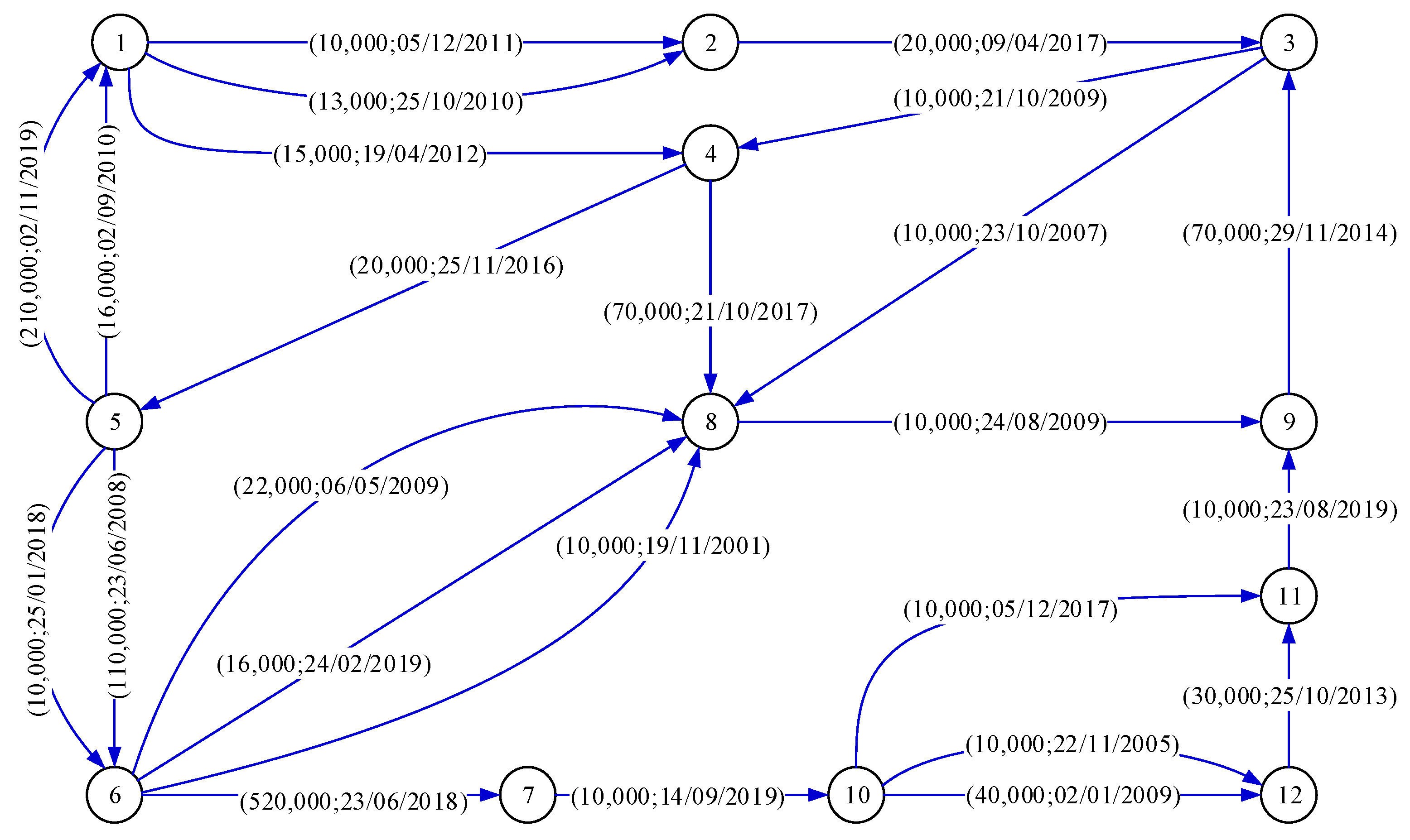

- If the tree root or path head pays enough money, this money can flow along the debt tree or debt path according to the topological orders of vertices. Taking Figure 4 as an example, suppose vertex 1, respectively, pays 15,000 to its creditors, vertices 2 and 4. Next, vertex 2 pays 15,000 to vertex 3, and vertex 3 pays 10,000 to vertex 4, so vertex 4 has 25,000. Vertex 4 pays 20,000 to vertex 6 through vertex 5, and vertex 6, respectively, pays 10,000 to vertex 8 and vertex 10 (through vertex 7) finally. During the above procedure, if a vertex in the debt tree can afford additional money, the successive users can receive more money. Because the topological order of vertex 4 is larger than that of vertex 3, vertex 4 should pay vertex 5 after it receives from vertex 3;

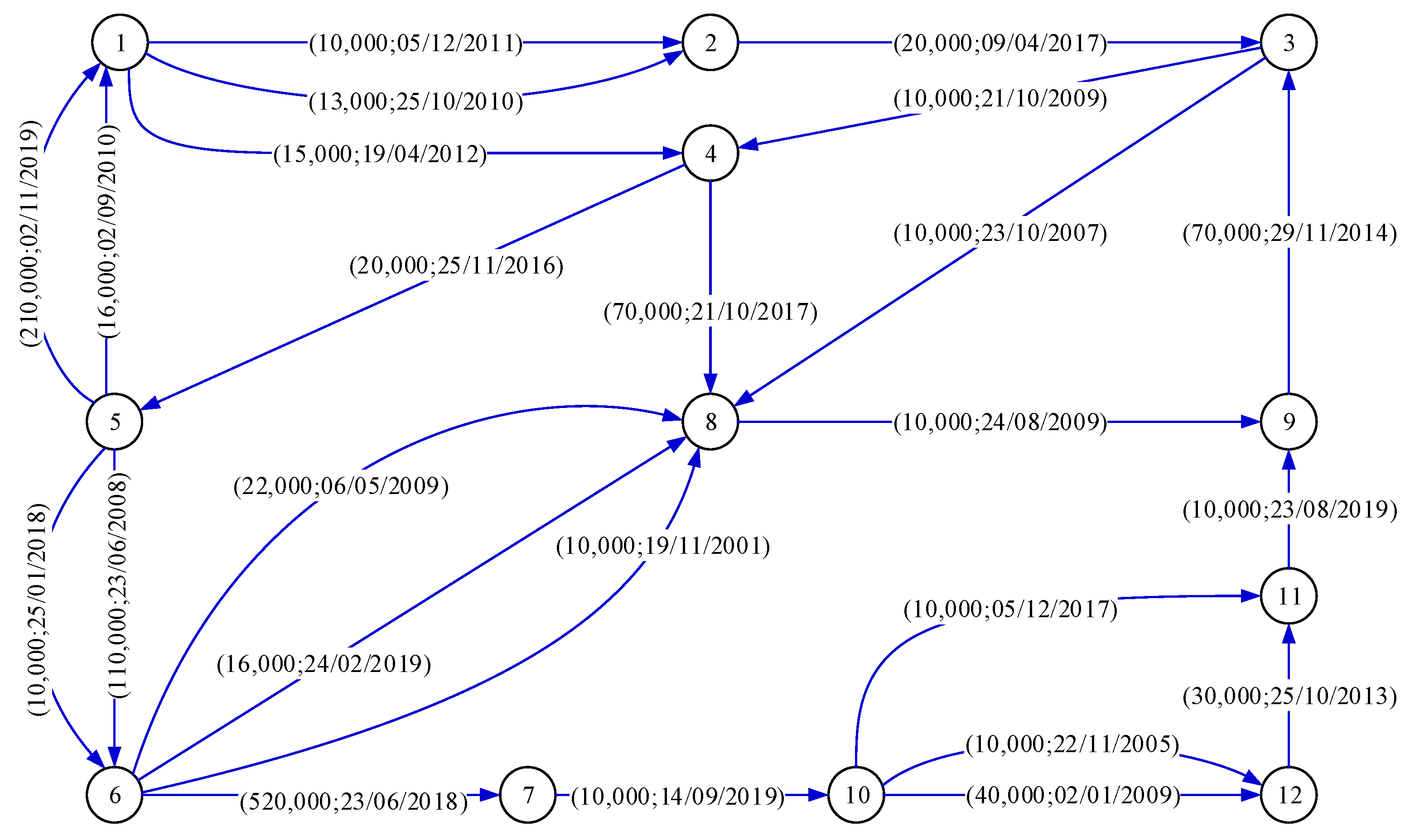

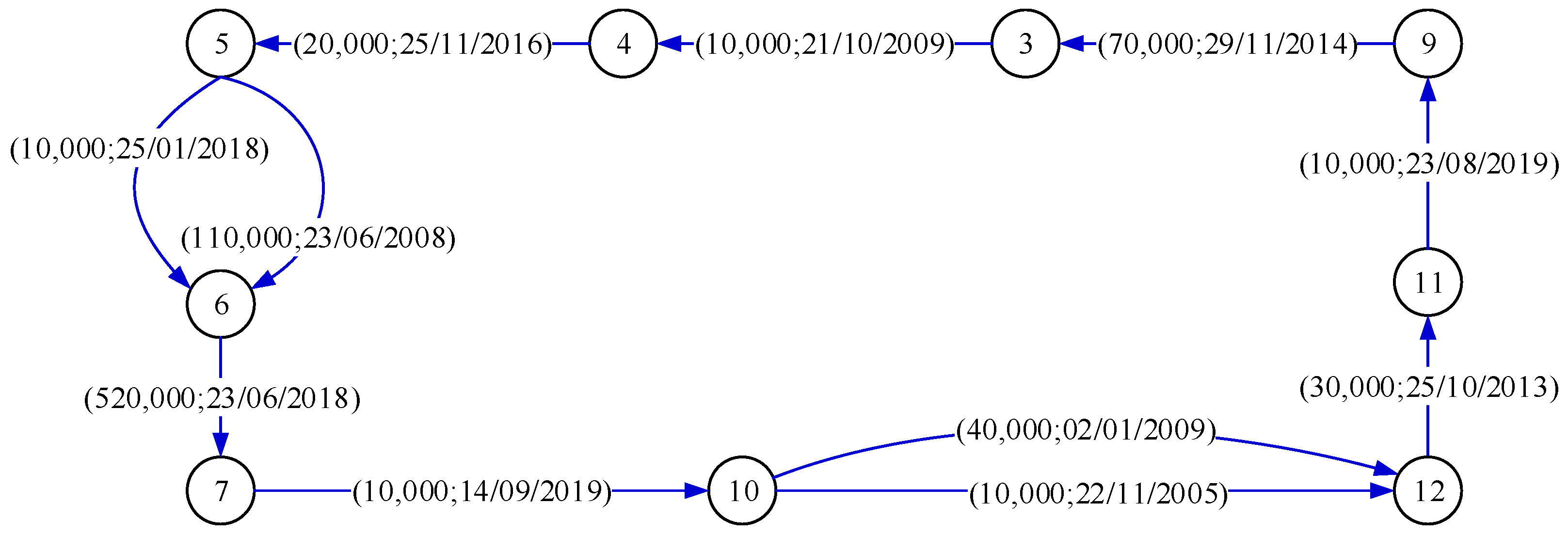

- Each vertex of the debt tree or debt path contributes some money to the third-party platform to aggregate enough money, and the platform pays it to the tree root or path head. The subsequent solution is the same as the above procedure. Taking Figure 2 as an example, vertices 1, 2, 3, and 9, respectively, contribute 2000, vertices 4 and 8, respectively, contribute 1000. Finally, these vertices gather 10,000 and pay to the platform, and then the platform pays 10,000 to vertex 1. This method is similar to crowdfunding.

4. Profit and Case Analysis

4.1. Profit Analysis

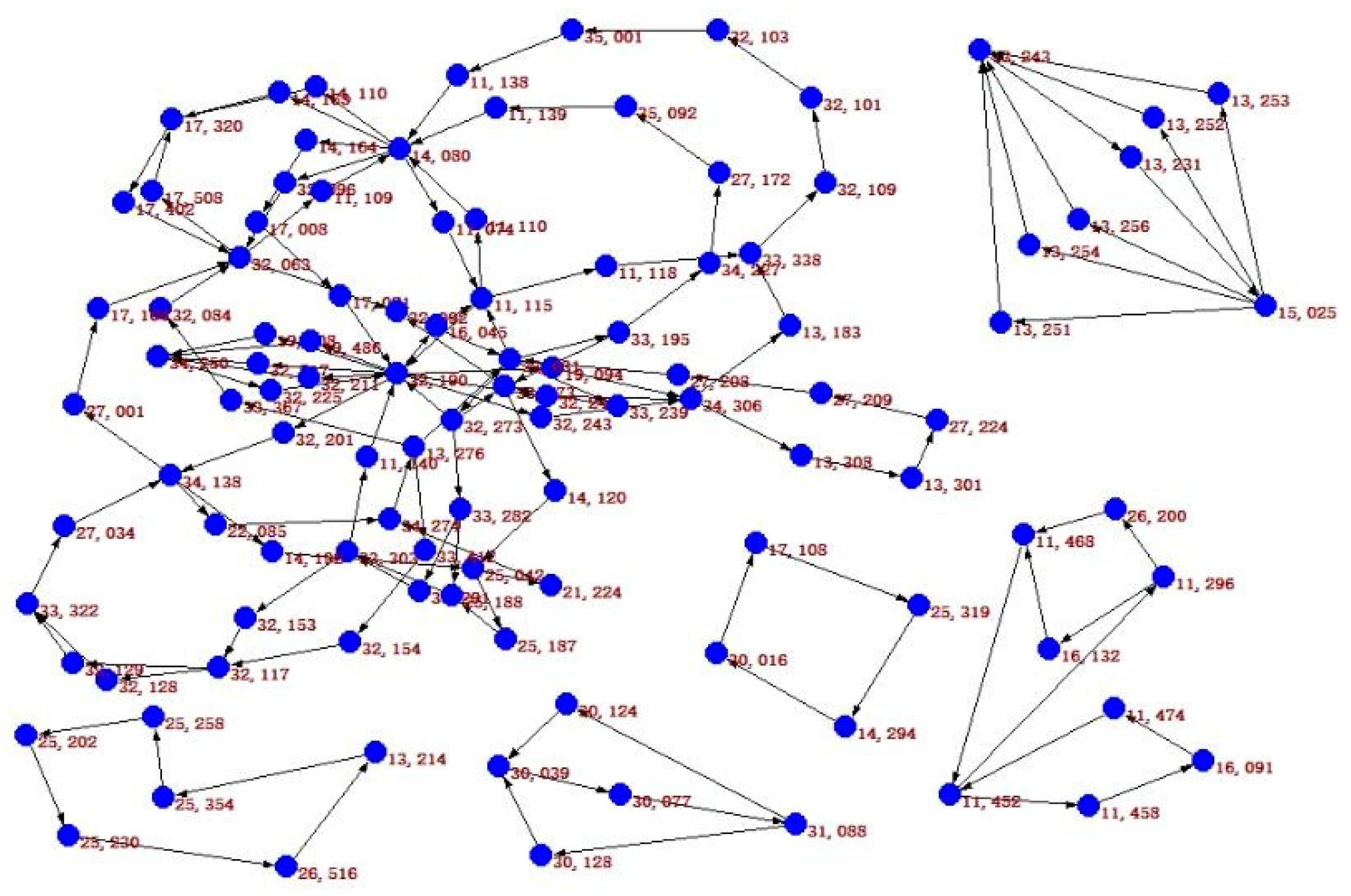

4.2. Case Analysis

5. Conclusions and Discussions

- The sorting criterion of entities (also the vertices of DebtG). Each entity wants to clear its debts first, but the debt structures are conflicting, as shown in the case analysis, so priority should be decided to guide the detection of debt structures;

- Privacy-preserving strategies during debt data collection. Debt is entities’ privacy, so it is very important to provide extremely privacy-preserving strategies;

- Methods to ensure that money flow only in the debt structure. The money provided by the third-party platform and/or tree root or path head aims to clear a series of debts of a debt structure, so it is very important to ensure that this money only flows between neighboring entities (also the vertices of DebtG) in a given debt structure;

- Algorithms to deal with large-scale graphs. Obviously, the more debt information is collected, the larger the DebtG is constructed, and the more debt are cleared. The large-scale graph needs effective distributed algorithms running on distributed systems.

Funding

Data Availability Statement

Conflicts of Interest

References

- Almenberg, J.; Lusardi, A.; Säve-Söderbergh, J.; Vestman, R. Attitudes towards Debt and Debt Behavior. Scand. J. Econ. 2020, 123, 780–809. [Google Scholar] [CrossRef]

- Drehmann, M.; Illes, A.; Juselius, M.; Santos, M. How much income is used for debt payments? A new database for debt ser-vice ratios. BIS Q. Rev. 2015. Available online: https://ssrn.com/abstract=2661611 (accessed on 6 May 2021).

- Gazda, V. Mutual Debts Compensation as Graph Theory Problem. In Topics in Numerical Partial Differential Equations and Scientific Computing; Springer: Berlin, Germany, 2001; pp. 162–167. [Google Scholar]

- Gazda, V.; Horváth, D.; Rešovský, M. An application of graph theory in the process of mutual debt compensation. Acta Poly-Tech. Hung. 2015, 12, 7–24. [Google Scholar]

- The Effect of National Culture on Debt Risk: An Empirical Analysis of “Belt and Road” Countries. In Proceedings of the 2020 International Conference on Big Data Application & Economic Management (ICBDEM 2020), Guiyang, China, 18 September 2020; Francis Academic Press: London, UK, 2020; pp. 470–481.

- Ye, Q.; Chen, M. Research on the Risk of Local Government Debt in China in the New Era. In Proceedings of the 2nd International Conference on Economy, Management and Entrepreneurship (ICOEME 2019), Voronezh, Russia, 14–15 May 2019; Atlantis Press: Dordrecht, The Netherlands, 2019; pp. 197–202. [Google Scholar]

- Wang, C.-W.; Chiu, W.-C. Effect of short-term debt on default risk: Evidence from Pacific Basin countries. Pac.-Basin Financ. J. 2019, 57, 101026. [Google Scholar] [CrossRef]

- Majeed, A.; Rauf, I. Graph Theory: A Comprehensive Survey about Graph Theory Applications in Computer Science and Social Networks. Inventions 2020, 5, 10. [Google Scholar] [CrossRef] [Green Version]

- O’Halloran, S.; Nowaczyk, N.; Gallagher, D. Big Data and Graph Theoretic Models. In Proceedings of the 2017 IEEE/ACM International Conference on Advances in Social Networks Analysis and Mining 2017, Sydney, Australia, 31 July–3 August 2017; Association for Computing Machinery (ACM): New York, NY, USA, 2017; pp. 1056–1064. [Google Scholar]

- Zhan, Q.; Yin, H. A loan application fraud detection method based on knowledge graph and neural network. In Proceedings of the 2nd International Conference on Cryptography, Security and Privacy, Guiyang, China, 16–19 March 2018; Association for Computing Machinery (ACM): New York, NY, USA, 2018; pp. 111–115. [Google Scholar]

- Gogoglou, A.; Nguyen, B.; Salimov, A.; Rider, J.; Bayan Bruss, C. Navigating the dynamics of financial embeddings over time. arXiv 2020, arXiv:2007.00591. [Google Scholar]

- Ren, Y.; Zhu, H.; Zhang, J.; Dai, P.; Bo, L. EnsemFDet an Ensemble: Approach to Fraud Detection based on Bipartite Graph. In Proceedings of the 2021 IEEE 37th International Conference on Data Engineering (ICDE) 2021, Chania, Greece, 19–22 April 2021. [Google Scholar]

- Yang, S.; Zhang, Z.; Zhou, J.; Wang, Y.; Sun, W.; Zhong, X.; Fang, Y.; Yu, Q.; Qi, Y. Financial Risk Analysis for SMEs with Graph-based Supply Chain Mining. In Proceedings of the Twenty-Ninth International Joint Conference on Artificial Intelligence, Yokohama, Japan, 11–17 July 2020; pp. 4661–4667. [Google Scholar]

- Păatcaş, C.; Bartha, A. Evolutionary solving of the debts’ clearing problem. Acta Univ. Sapientiae Inform. 2019, 11, 142–158. [Google Scholar] [CrossRef] [Green Version]

- Liang, L.; Chen, S.; Wu, D.D. A Decision Support Approach to Liquidate a Distressed Debt Network. IEEE Trans. Syst. Man Cybern. Syst. 2017, 50, 1242–1251. [Google Scholar] [CrossRef]

- Deo, N. Graph theory with applications to engineering and computer science. Networks 1975, 5, 299–300. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

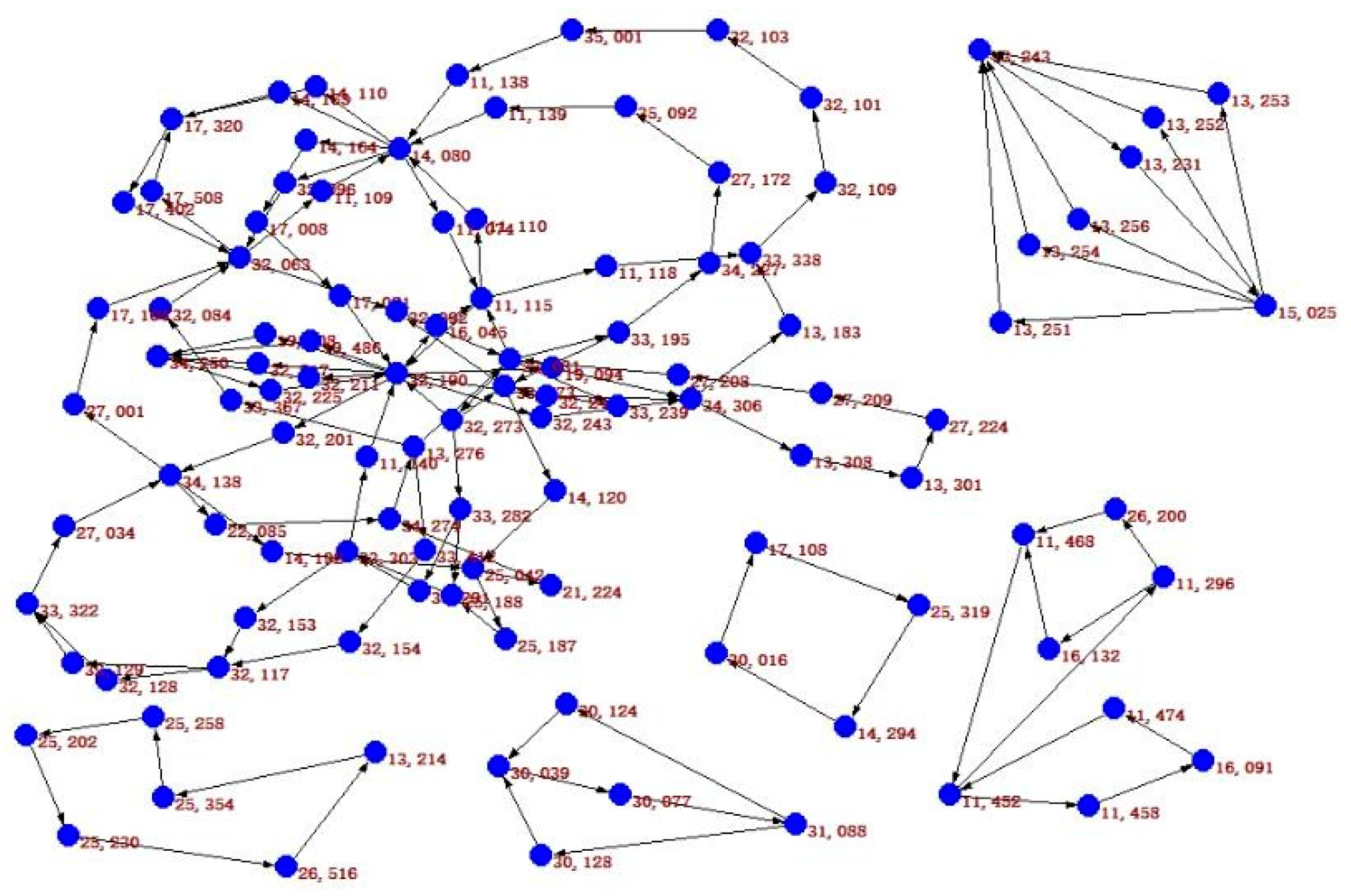

| Sequence of Vertices | Settle Amount |

|---|---|

| 33,338–32,109–32,101–32,103–35,001–11,138–14,080–14,164–17,008–17,021–32,190–19,094–34,306–13,183 | 0.9 |

| 15,025–13,256–13,243–13,231 | 33.0 |

| 15,025–13,251–13,243–13,231 | 23.0 |

| 15,025–13,254–13,243–13,231 | 18.0 |

| 15,025–13,253–13,243–13,231 | 11.0 |

| 15,025–13,252–13,243–13,231 | 12.0 |

| 11,452–11,458–16,091–11,474 | 10.0 |

| 11,468–11,452–11,296–26,200 | 5.0 |

| 16,132–11,468–11,452–11,296 | 7.0 |

| 25,230–26,516–13,214–25,354–25,258–25,202 | 10.0 |

| 32,063–17,508–17,320–17,402 | 6.28 |

| 33,031–33,195–33,473–14,120–25,042–21,224–34,274–13,276–33,367–32,084–32,063–32,092 | 8.0 |

| 33,031–33,195–33,473–14,120–25,042–21,224–34,274–13,276 | 12.0 |

| 14,080–14,164–17,008–17,021–32,190–19,094–34,306–13,308–13,301–27,224–27,209–27,208–33,031–33,195–34,227–27,172–35,092–11,139 | 3.0 |

| 32,190–19,094–34,306–13,308–13,301–27,224–27,209–27,208–33,031–32,273 | 5.0 |

| 32,190–19,094–34,306–13,308–13,301–27,224–27,209–27,208–33,031–32,273–33,282–33,291–33,303–11,140 | 0.4 |

| 32,190–19,094–34,306–13,308–13,301–27,224–27,209–27,208–33,031–32,273–33,282–25,188–33,303–11,140 | 1.9 |

| 33,031–32,273–33,473–32,092 | 0.9 |

| 32,190–19,094–34,306–13,308–13,301–27,224–27,209–27,208–33,031–11,115 | 5.3 |

| 32,190–32,217–34,250–32,225 | 9.0 |

| 32,190–32,243–34,306–13,308–13,301–27,224–27,209–27,208–33,031–11,115 | 3.0 |

| 32,190–32,211–34,250–32,225 | 3.0 |

| 32,190–32,201–34,138–27,001–17,104–32,063–32,092–33,031–11,115 | 9.0 |

| 32,190–32,245–34,306–13,308–13,301–27,224–27,209–27,208–33,031–11,115 | 7.0 |

| 32,190–19,508–34,250–32,225 | 9.0 |

| 32,190–19,486–34,250–32,225 | 5.0 |

| 32,190–16,045–11,115 | 1.0 |

| 33,338–32,109–32,101–32,103–35,001–11,138–14,080–14,110–17,320–17,402–32,063–32,092–33,031–11,115–11,118 | 3.0 |

| 11,115–11,110–14,080–14,110–17,320–17,402–32,063–32,092–33,031 | 3.02 |

| 11,115–11,110–14,080–14,163–17,320–17,402–32,063–32,092–33,031 | 6.28 |

| 11,115–11,110–14,080–32,096–32,063–32,092–33,031 | 9.1 |

| 32,092–33,031–33,239–33,473 | 1.9 |

| 14,080–32,096–32,063–11,109 | 4.0 |

| 11,115–11,110–14,080–11,074 | 13.0 |

| 34,274–13,276–33,412–32,154–32,117–32,128–33,322–27,034–34,138–22,085 | 1.2 |

| 34,274–13,276–33,412–32,154–32,117–32,129–33,322–27,034–34,138–22,085 | 2.7 |

| 25,042–25,187–25,188–33,303–32,153–32,117–32,129–33,322–27,034–34,138–14,192 | 3.0 |

| 30,016–17,108–25,319–14,294 | 1.0 |

| 31,088–30,124–30,039–30,077 | 3.95 |

| 31,088–30,128–30,039–30,077 | 3.07 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Cui, H. DebtG: A Graph Model for Debt Relationship. Information 2021, 12, 347. https://doi.org/10.3390/info12090347

Cui H. DebtG: A Graph Model for Debt Relationship. Information. 2021; 12(9):347. https://doi.org/10.3390/info12090347

Chicago/Turabian StyleCui, Huanqing. 2021. "DebtG: A Graph Model for Debt Relationship" Information 12, no. 9: 347. https://doi.org/10.3390/info12090347

APA StyleCui, H. (2021). DebtG: A Graph Model for Debt Relationship. Information, 12(9), 347. https://doi.org/10.3390/info12090347