Drivers of Mobile Payment Acceptance in China: An Empirical Investigation

Abstract

1. Introduction

2. Materials and Methods

2.1. Facilitating Factors

2.1.1. Perceived Transaction Convenience (PTC)

2.1.2. Compatibility

2.1.3. Relative Advantages

2.1.4. Social Influence

2.2. Environment Factors

2.2.1. Government Support

2.2.2. Additional Value

2.3. Inhibiting Factors: Perceived Risk

2.4. Personal Factors

2.4.1. Absorptive Capacity

2.4.2. Affinity

2.4.3. Personal Innovativeness in Information Technology (PIIT)

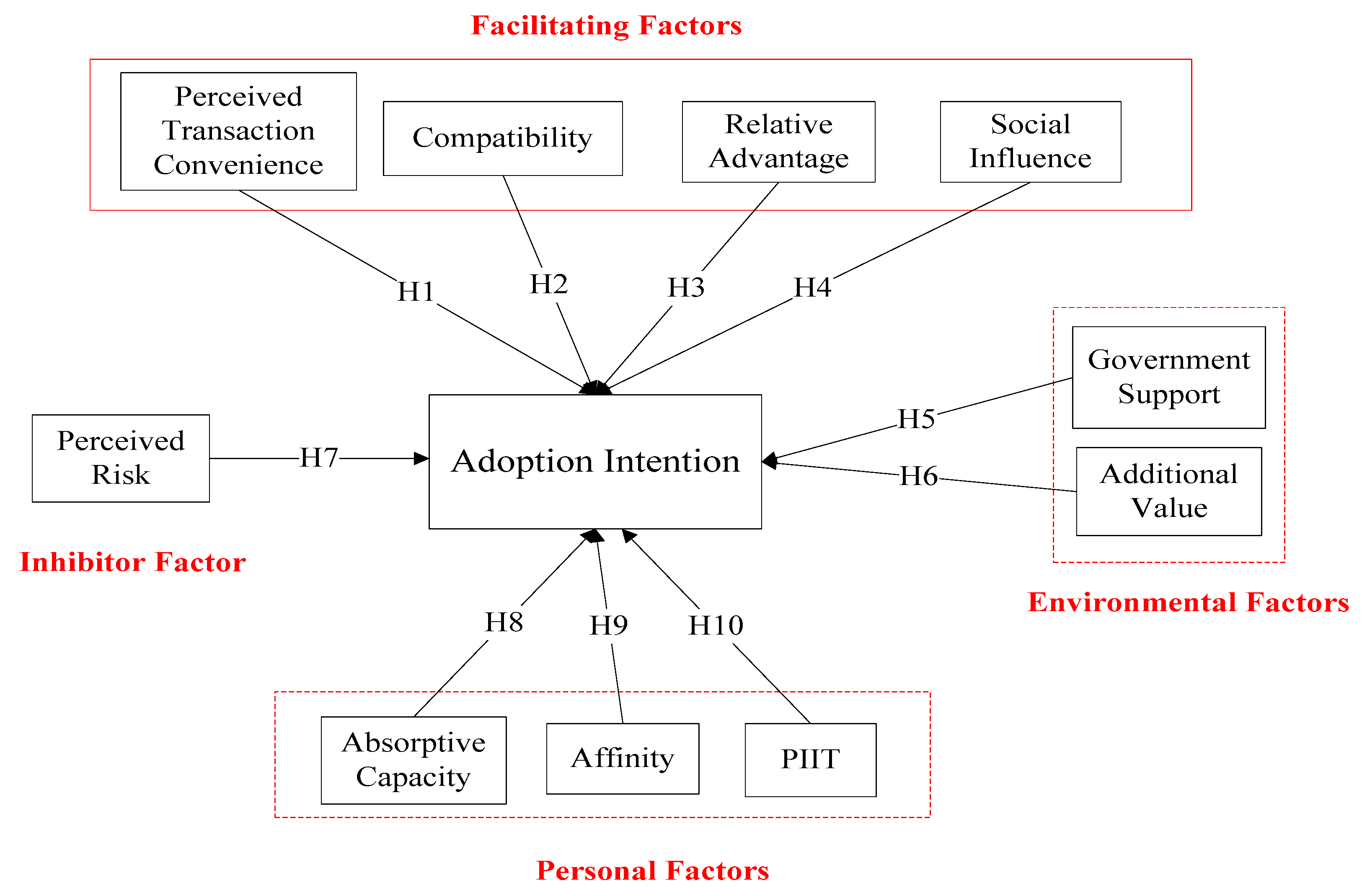

3. Research Model and Hypotheses

3.1. Facilitating Factors and Adoption Intention

3.1.1. Perceived Transaction Convenience and Adoption Intention

3.1.2. Compatibility and Adoption Intention

3.1.3. Relative Advantage and Adoption Intention

3.1.4. Social Influence and Adoption Intention

3.2. Environmental Factors and Adoption Intention

3.2.1. Government Support and Adoption Intention

3.2.2. Additional Value and Adoption Intention

3.3. Inhibitor Factor (Perceived Risk) and Adoption Intention

3.4. Personal Factors and Adoption Intention

3.4.1. Absorptive Capacity and Adoption Intention

3.4.2. Affinity and Adoption Intention

3.4.3. Personal Innovation in IT (PIIT) and Adoption Intention

4. Results

4.1. Data Collection

4.2. Measurement Items

4.3. Measurement Model Testing

4.4. PLS Analysis

5. Discussion

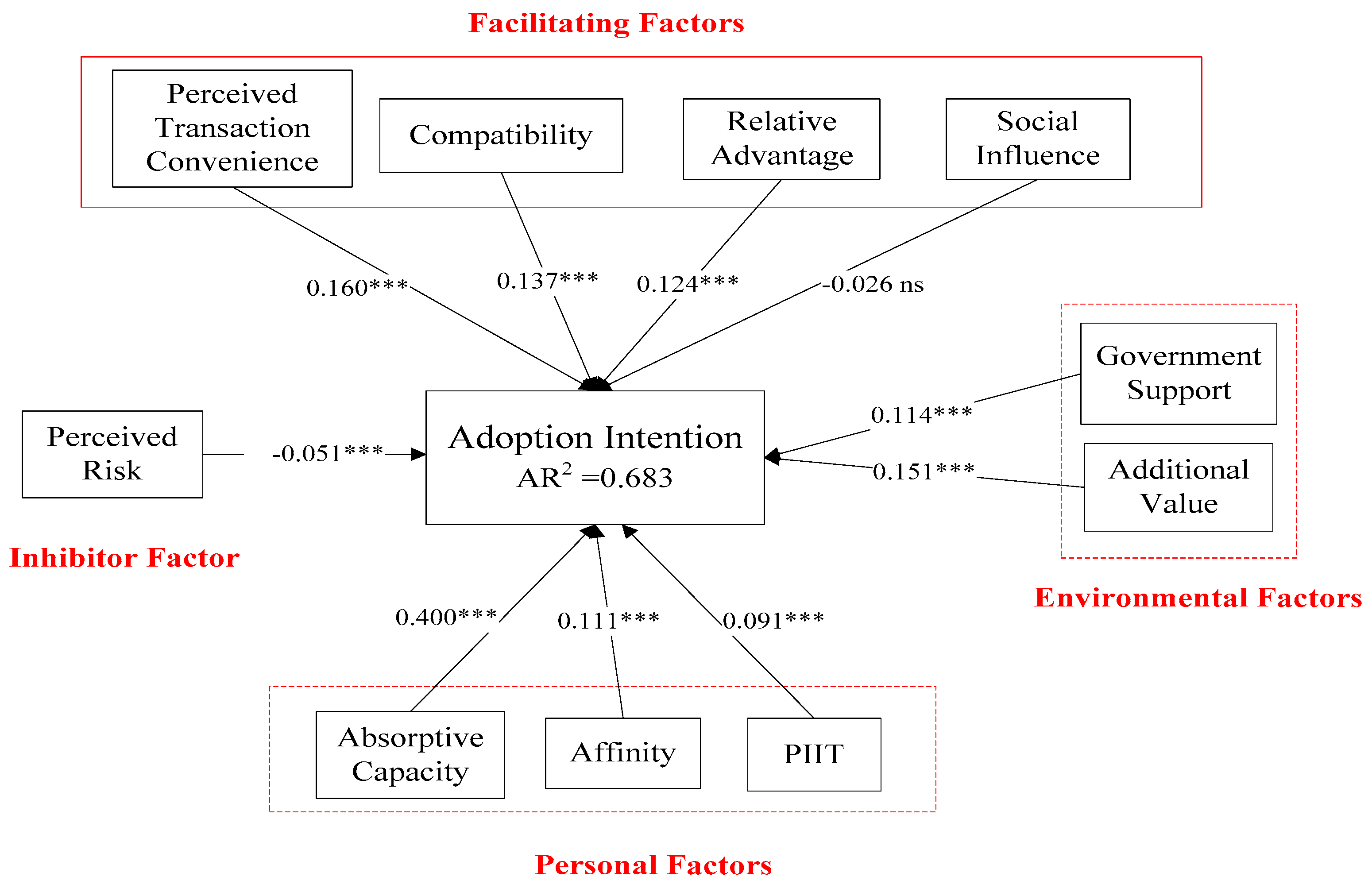

5.1. Summary of Results

5.1.1. Facilitating Factors

5.1.2. Environment Factors

5.1.3. Inhibiting Factor

5.1.4. Personal Factors

5.2. Theoretical Implication

5.3. Managerial Implication

5.4. Limitations and Future Research

- Even though statistical results support generalizability when the sample size is greater than 100, larger samples guard for many biases and strengthen the explanation power of this study [85].

- The results of this study show that social influence does not have a significant impact on Chinese users’ adoption of mobile payment. As this result is inconsistent with previous studies, it is suggested that further discussion can be conducted regarding whether social influence has a significant impact on users in different demographics variables (e.g., gender, education, usage experience, etc.) adopting mobile payment services.

- Although the age structure of the questionnaire is relatively evenly distributed among users aged 16–25, 26–35, and 36–45 years old, China has a large population and many elderly people. Therefore, it is suggested that more questionnaires be completed by older respondents to render such research results more comprehensive, in order to better understand the influence on users in China by the factors regarding mobile payment.

- China has a vast territory and a large urban–rural gap, thus the results cannot fully reveal the situation of consumers in various areas. Therefore, it is suggested that interviewees from more areas may be added in order to gain a more comprehensive understanding of the situation of using mobile payment in China, as well as the differences in the factors regarding the use of mobile payment in different Chinese regions (e.g., urban and rural areas).

- According to an eMarketer [2] report, 81.4% of smart phone users use mobile payment services; in the future, we also plan to examine the applicability of the research model in different categories of user groups (use and nonuse of mobile payment services). We would like to investigate our research model in different user groups and make comparisons of users’ willingness to adopt mobile payment services.

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Dahlberg, T.; Mallat, N.; Ondrus, J.; Zmijewska, A. Past, present and future of mobile payments research: A literature review. Electron. Commer. Res. Appl. 2008, 7, 165–181. [Google Scholar] [CrossRef]

- eMarketer. Global Proximity Mobile Payment Users. Available online: https://www.emarketer.com/content/global-proximity-mobile-payment-users. (accessed on 8 April 2019).

- Bigdata Research, 2018 China Third Party Mobile Payment Market Development Report. Available online: http://www.bigdata-research.cn/content/201903/930.html. (accessed on 28 March 2019).

- Leong, L.Y.; Hew, T.S.; Tan, G.W.H.; Ooi, K.B. Predicting the determinants of the NFC-enabled mobile credit card acceptance: A neural networks approach. Expert Syst. Appl. 2013, 40, 5604–5620. [Google Scholar] [CrossRef]

- Tan, G.W.H.; Ooi, K.B.; Chong, S.C.; Hew, T.S. NFC mobile credit card: The next frontier of mobile payment? Telemat. Inform. 2014, 31, 292–307. [Google Scholar] [CrossRef]

- Bailey, A.A.; Pentina, I.; Mishra, A.S.; Ben Mimoun, M.S. Mobile payments adoption by US consumers: An extended TAM. Int. J. Retail Distrib. Manag. 2017, 45, 626–640. [Google Scholar] [CrossRef]

- Liébana-Cabanillas, F.; Muñoz-Leiva, F.; Sánchez-Fernández, J. A global approach to the analysis of user behavior in mobile payment systems in the new electronic environment. Serv. Bus. 2018, 12, 25–64. [Google Scholar] [CrossRef]

- Teo, A.C.; Tan, G.W.H.; Ooi, K.B.; Hew, T.S.; Yew, K.T. The effects of convenience and speed in m-payment. Ind. Manag. Data Syst. 2015, 115, 311–331. [Google Scholar] [CrossRef]

- Morosan, C.; DeFranco, A. It′s about time: Revisiting UTAUT2 to examine consumers′ intentions to use NFC mobile payments in hotels. Int. J. Hosp. Manag. 2016, 53, 17–29. [Google Scholar] [CrossRef]

- Koenig-Lewis, N.; Marquet, M.; Palmer, A.; Zhao, A.L. Enjoyment and social influence: Predicting mobile payment adoption. Serv. Ind. J. 2015, 35, 537–554. [Google Scholar] [CrossRef]

- Khalilzadeh, J.; Ozturk, A.B.; Bilgihan, A. Security-related factors in extended UTAUT model for NFC based mobile payment in the restaurant industry. Comput. Hum. Behav. 2017, 70, 460–474. [Google Scholar] [CrossRef]

- Yang, S.; Lu, Y.; Gupta, S.; Cao, Y.; Zhang, R. Mobile payment services adoption across time: An empirical study of the effects of behavioral beliefs, social influences, and personal traits. Comput. Hum. Behav. 2012, 28, 129–142. [Google Scholar] [CrossRef]

- Pham, T.T.T.; Ho, J.C. The effects of product-related, personal-related factors and attractiveness of alternatives on consumer adoption of NFC-based mobile payments. Technol. Soc. 2015, 43, 159–172. [Google Scholar] [CrossRef]

- Ozturk, A.B.; Bilgihan, A.; Salehi-Esfahani, S.; Hua, N. Understanding the mobile payment technology acceptance based on valence theory: A case of restaurant transactions. Int. J. Contemp. Hosp. Manag. 2017, 29, 2027–2049. [Google Scholar] [CrossRef]

- Mbogo, M. The impact of mobile payments on the success and growth of micro-business: The case of M-Pesa in Kenya. J. Lang. Technol. Entrep. Afr. 2010, 2, 182–203. [Google Scholar] [CrossRef]

- Yoon, C.; Kim, S. Convenience and TAM in a ubiquitous computing environment: The case of wireless LAN. Electron. Commer. Res. Appl. 2007, 6, 102–112. [Google Scholar] [CrossRef]

- Schierz, P.G.; Schilke, O.; Wirtz, B.W. Understanding consumer acceptance of mobile payment services: An empirical analysis. Electron. Commer. Res. Appl. 2010, 9, 209–216. [Google Scholar] [CrossRef]

- Ramos-de-Luna, I.; Montoro-Ríos, F.; Liébana-Cabanillas, F. Determinants of the intention to use NFC technology as a payment system: An acceptance model approach. Inf. Syst. E-Bus. Manag. 2016, 14, 293–314. [Google Scholar] [CrossRef]

- Oliveira, T.; Thomas, M.; Baptista, G.; Campos, F. Mobile payment: Understanding the determinants of customer adoption and intention to recommend the technology. Comput. Hum. Behav. 2016, 61, 404–414. [Google Scholar] [CrossRef]

- Ooi, K.B.; Tan, G.W.H. Mobile technology acceptance model: An investigation using mobile users to explore smartphone credit card. Expert Syst. Appl. 2016, 59, 33–46. [Google Scholar] [CrossRef]

- Kim, C.; Mirusmonov, M.; Lee, I. An empirical examination of factors influencing the intention to use mobile payment. Comput. Hum. Behav. 2010, 26, 310–322. [Google Scholar] [CrossRef]

- Rogers, E. Diffusion of Innovation, 4th ed.; Free Press: New York, NY, USA, 1995. [Google Scholar]

- Liébana-Cabanillas, F.; Ramos de Luna, I.; Montoro-Ríos, F.J. User behaviour in QR mobile payment system: The QR Payment Acceptance Model. Technol. Anal. Strateg. Manag. 2015, 27, 1031–1049. [Google Scholar] [CrossRef]

- Aydin, G.; Burnaz, S. Adoption of mobile payment systems: A study on mobile wallets. J. Bus. Econ. Financ. 2016, 5, 73–92. [Google Scholar] [CrossRef]

- Nasri, W.; Charfeddine, L. Factors affecting the adoption of Internet banking in Tunisia: An integration theory of acceptance model and theory of planned behavior. J. High Technol. Manag. Res. 2012, 23, 1–14. [Google Scholar] [CrossRef]

- Raza, S.A.; Hanif, N. Factors affecting internet banking adoption among internal and external customers: A case of Pakistan. Int. J. Electron. Financ. 2013, 7, 82–96. [Google Scholar] [CrossRef]

- Ramanathan, R.; Ramanathan, U.; Ko, L.W.L. Adoption of RFID technologies in UK logistics: Moderating roles of size, barcode experience and government support. Expert Syst. Appl. 2014, 41, 230–236. [Google Scholar] [CrossRef]

- Kim, Y.J.; Han, J. Why smartphone advertising attracts customers: A model of Web advertising, flow, and personalization. Comput. Hum. Behav. 2014, 33, 256–269. [Google Scholar] [CrossRef]

- Payment and Clearing Association of China, 2018 Mobile Payment Survey Report. Available online: http://www.pcac.org.cn/index.php/focus/list_details/ids/654/id/50/t. (accessed on 26 March 2019).

- Liébana-Cabanillas, F.; Sánchez-Fernández, J.; Muñoz-Leiva, F. The moderating effect of experience in the adoption of mobile payment tools in Virtual Social Networks: The m-Payment Acceptance Model in Virtual Social Networks (MPAM-VSN). Int. J. Inf. Manag. 2014, 34, 151–166. [Google Scholar] [CrossRef]

- Kim, D.J.; Ferrin, D.L.; Rao, H.R. A trust-based consumer decision-making model in electronic commerce: The role of trust, perceived risk, and their antecedents. Decis. Support Syst. 2008, 44, 544–564. [Google Scholar] [CrossRef]

- Shin, D.H. Towards an understanding of the consumer acceptance of mobile wallet. Comput. Hum. Behav. 2009, 25, 1343–1354. [Google Scholar] [CrossRef]

- Wu, J.; Liu, L.; Huang, L. Consumer acceptance of mobile payment across time: Antecedents and moderating role of diffusion stages. Ind. Manag. Data Syst. 2017, 117, 1761–1776. [Google Scholar] [CrossRef]

- Lee, Y.K.; Park, J.H.; Chung, N.; Blakeney, A. A unified perspective on the factors influencing usage intention toward mobile financial services. J. Bus. Res. 2012, 65, 1590–1599. [Google Scholar] [CrossRef]

- Aldás-Manzano, J.; Ruiz-Mafé, C.; Sanz-Blas, S. Exploring individual personality factors as drivers of M-shopping acceptance. Ind. Manag. Data Syst. 2009, 109, 739–757. [Google Scholar] [CrossRef]

- Park, S.T.; Im, H.; Noh, K.S. A study on factors affecting the adoption of LTE mobile communication service: The case of South Korea. Wirel. Pers. Commun. 2016, 86, 217–237. [Google Scholar] [CrossRef]

- Zeng, Z.; Cleon, C.B. Factors affecting the adoption of a land information system: An empirical analysis in Liberia. Land Use Policy 2018, 73, 353–362. [Google Scholar] [CrossRef]

- Lwoga, E.T.; Lwoga, N.B. User Acceptance of Mobile Payment: The Effects of User-Centric Security, System Characteristics and Gender. Electron. J. Inf. Syst. Dev. Ctries. 2017, 81, 1–24. [Google Scholar] [CrossRef]

- Berry, L.L.; Seiders, K.; Grewal, D. Understanding service convenience. J. Mark. 2002, 66, 1–17. [Google Scholar] [CrossRef]

- Hayashi, F. Mobile Payments: What′s in It for Consumers? Economic Review-Federal Reserve Bank of Kansas City: Kansas City, KS, USA, 2012. [Google Scholar]

- Liu, F.; Zhao, X.; Chau, P.Y.; Tang, Q. Roles of perceived value and individual differences in the acceptance of mobile coupon applications. Internet Res. 2015, 25, 471–495. [Google Scholar] [CrossRef]

- Chen, L.D. A model of consumer acceptance of mobile payment. Int. J. Mob. Commun. 2008, 6, 32–52. [Google Scholar] [CrossRef]

- Di Pietro, L.; Mugion, R.G.; Mattia, G.; Renzi, M.F.; Toni, M. The integrated model on mobile payment acceptance (IMMPA): An empirical application to public transport. Transp. Res. Part C Emerg. Technol. 2015, 56, 463–479. [Google Scholar] [CrossRef]

- Chen, L.D.; Gillenson, M.L.; Sherrell, D.L. Consumer acceptance of virtual stores: A theoretical model and critical success factors for virtual stores. ACM Sigmis Database Database Adv. Inf. Syst. 2004, 35, 8–31. [Google Scholar] [CrossRef]

- Su, P.; Wang, L.; Yan, J. How users′ Internet experience affects the adoption of mobile payment: A mediation model. Technol. Anal. Strateg. Manag. 2018, 30, 186–197. [Google Scholar] [CrossRef]

- Lou, L.; Tian, Z.; Koh, J. Tourist satisfaction enhancement using mobile QR code payment: An empirical investigation. Sustainability 2017, 9, 1186. [Google Scholar] [CrossRef]

- Dang, Y.M.; Zhang, Y.G.; Morgan, J. Integrating switching costs to information systems adoption: An empirical study on learning management systems. Inf. Syst. Front. 2017, 19, 625–644. [Google Scholar] [CrossRef]

- Tan, M.; Teo, T.S. Factors influencing the adoption of Internet banking. J. AIS 2000, 1, 1–42. [Google Scholar] [CrossRef]

- Lin, C.Y.; Ho, Y.H. An empirical study on the adoption of RFID technology for logistics service providers in China. Int. Bus. Res. 2009, 2, 23–36. [Google Scholar] [CrossRef]

- Sánchez-Torres, J.A.; Canada, F.J.A.; Sandoval, A.V.; Alzate, J.A.S. E-banking in Colombia: Factors favouring its acceptance, online trust and government support. Int. J. Bank Mark. 2018, 36, 170–183. [Google Scholar] [CrossRef]

- Chaouali, W.; Yahia, I.B.; Charfeddine, L.; Triki, A. Understanding citizens′ adoption of e-filing in developing countries: An empirical investigation. J. High Technol. Manag. Res. 2016, 27, 161–176. [Google Scholar] [CrossRef]

- Hung, S.Y.; Chen, C.C.; Yeh, R.K.J.; Huang, L.C. Enhancing the use of e-learning systems in the public sector: A behavioural intention perspective. Electron. Gov. Int. J. 2016, 12, 1–26. [Google Scholar] [CrossRef]

- Featherman, M.S.; Pavlou, P.A. Predicting e-services adoption: A perceived risk facets perspective. Int. J. Hum. Comput. Stud. 2003, 59, 451–474. [Google Scholar] [CrossRef]

- Baganzi, R.; Lau, A. Examining trust and risk in mobile money acceptance in Uganda. Sustainability 2017, 9, 2233. [Google Scholar] [CrossRef]

- Chen, X.; Cheah, S.; Shen, A. Empirical Study on Behavioral Intentions of Short-Term Rental Tenants—The Moderating Role of Past Experience. Sustainability 2019, 11, 3404. [Google Scholar] [CrossRef]

- Merhi, M.; Hone, K.; Tarhini, A. A cross-cultural study of the intention to use mobile banking between Lebanese and British consumers: Extending UTAUT2 with security, privacy and trust. Technol. Soc. 2019, 59, 101151. [Google Scholar] [CrossRef]

- Phonthanukitithaworn, C.; Sellitto, C.; Fong, M.W. A comparative study of current and potential users of mobile payment services. Sage Open 2016, 6, 2158244016675397. [Google Scholar] [CrossRef]

- Thakur, R.; Srivastava, M. Adoption readiness, personal innovativeness, perceived risk and usage intention across customer groups for mobile payment services in India. Internet Res. 2014, 24, 369–392. [Google Scholar] [CrossRef]

- Hindawi: What Makes People Actually Embrace or Shun Mobile Payment: A Cross-Culture Study. Mob. Inf. Syst. 2018, 2018, 7497545. [CrossRef]

- Agarwal, R.; Prasad, J. A conceptual and operational definition of personal innovativeness in the domain of information technology. Inf. Syst. Res. 1998, 9, 204–215. [Google Scholar] [CrossRef]

- Gao, L.; Waechter, K.A. Examining the role of initial trust in user adoption of mobile payment services: An empirical investigation. Inf. Syst. Front. 2017, 19, 525–548. [Google Scholar] [CrossRef]

- Teh, P.L.; Ahmed, P.K.; Cheong, S.N.; Yap, W.J. Age-group differences in Near Field Communication smartphone. Ind. Manag. Data Syst. 2014, 114, 484–502. [Google Scholar] [CrossRef]

- Kuo, Y.-F.; Yen, S.-N. Towards an understanding of the behavioral intention to use 3G mobile value-added services. Comput. Hum. Behav. 2009, 25, 103–110. [Google Scholar] [CrossRef]

- Liébana-Cabanillas, F.; Marinkovic, V.; de Luna, I.R.; Kalinic, Z. Predicting the determinants of mobile payment acceptance: A hybrid SEM-neural network approach. Technol. Forecast. Soc. Chang. 2018, 129, 117–130. [Google Scholar] [CrossRef]

- Agag, G.; El-Masry, A.A. Understanding consumer intention to participate in online travel community and effects on consumer intention to purchase travel online and WOM: An integration of innovation diffusion theory and TAM with trust. Comput. Hum. Behav. 2016, 60, 97–111. [Google Scholar] [CrossRef]

- Maduku, D.K.; Mpinganjira, M.; Duh, H. Understanding mobile marketing adoption intention by South African SMEs: A multi-perspective framework. Int. J. Inf. Manag. 2016, 36, 711–723. [Google Scholar] [CrossRef]

- Chen, C. Perceived risk, usage frequency of mobile banking services. Manag. Serv. Qual. Int. J. 2013, 23, 410–436. [Google Scholar] [CrossRef]

- Kapoor, K.K.; Dwivedi, Y.K.; Williams, M.D. Examining the role of three sets of innovation attributes for determining adoption of the interbank mobile payment service. Inf. Syst. Front. 2015, 17, 1039–1056. [Google Scholar] [CrossRef]

- López-Nicolás, C.; Molina-Castillo, F.J.; Bouwman, H. An assessment of advanced mobile services acceptance: Contributions from TAM and diffusion theory models. Inf. Manag. 2008, 45, 359–364. [Google Scholar] [CrossRef]

- Lee, S.W.; Sung, H.J.; Jeon, H.M. Determinants of Continuous Intention on Food Delivery Apps: Extending UTAUT2 with Information Quality. Sustainability 2019, 11, 3141. [Google Scholar] [CrossRef]

- Palau-Saumell, R.; Forgas-Coll, S.; Sánchez-García, J.; Robres, E. User acceptance of mobile apps for restaurants: An expanded and extended UTAUT-2. Sustainability 2019, 11, 1210. [Google Scholar] [CrossRef]

- Shaw, N.; Sergueeva, K. The non-monetary benefits of mobile commerce: Extending UTAUT2 with perceived value. Int. J. Inf. Manag. 2019, 45, 44–55. [Google Scholar] [CrossRef]

- Rawashdeh, A.; Al-namlah, L. Factors influencing electronic data interchange adoption among small and medium enterprises in Saudi Arabia. Asian J. Bus. Account. 2017, 10, 253–280. [Google Scholar]

- Hasani, T.; Bojei, J.; Dehghantanha, A. Investigating the antecedents to the adoption of SCRM technologies by start-up companies. Telemat. Inform. 2017, 34, 655–675. [Google Scholar] [CrossRef]

- Tan, E.; Leby Lau, J. Behavioural intention to adopt mobile banking among the millennial generation. Young Consum. 2016, 17, 18–31. [Google Scholar] [CrossRef]

- Duane, A.; O′Reilly, P.; Andreev, P. Realising M-Payments: Modelling consumers′ willingness to M-pay using Smart Phones. Behav. Inf. Technol. 2014, 33, 318–334. [Google Scholar] [CrossRef]

- Ozturk, A.B. Customer acceptance of cashless payment systems in the hospitality industry. Int. J. Contemp. Hosp. Manag. 2016, 28, 801–817. [Google Scholar] [CrossRef]

- Lin, H.F. Understanding the determinants of electronic supply chain management system adoption: Using the technology–organization–environment framework. Technol. Forecast. Soc. Chang. 2014, 86, 80–92. [Google Scholar] [CrossRef]

- Mohammadi, H. Social and individual antecedents of m-learning adoption in Iran. Comput. Hum. Behav. 2015, 49, 191–207. [Google Scholar] [CrossRef]

- Ooi, K.B.; Lee, V.H.; Tan, G.W.H.; Hew, T.S.; Hew, J.J. Cloud computing in manufacturing: The next industrial revolution in Malaysia? Expert Syst. Appl. 2018, 93, 376–394. [Google Scholar] [CrossRef]

- Upadhyay, P.; Jahanyan, S. Analyzing user perspective on the factors affecting use intention of mobile based transfer payment. Internet Res. 2016, 26, 38–56. [Google Scholar] [CrossRef]

- Zha, X.; Zhang, J.; Yan, Y.; Xiao, Z. Does affinity matter? Slow effects of e-quality on information seeking in virtual communities. Libr. Inf. Sci. Res. 2015, 37, 68–76. [Google Scholar] [CrossRef]

- Leung, L.; Chen, C. Extending the theory of planned behavior: A study of lifestyles, contextual factors, mobile viewing habits, TV content interest, and intention to adopt mobile TV. Telemat. Inform. 2017, 34, 1638–1649. [Google Scholar] [CrossRef]

- Gbongli, K.; Xu, Y.; Amedjonekou, K.M. Extended Technology Acceptance Model to Predict Mobile-Based Money Acceptance and Sustainability: A Multi-Analytical Structural Equation Modeling and Neural Network Approach. Sustainability 2019, 11, 3639. [Google Scholar] [CrossRef]

- Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E. Multivariate Data Analysis: A Global Perspective 2010; Pearson Education: London, UK, 2010. [Google Scholar]

- Fornell, C.; Larcker, D.F. Evaluating structural equation models with unobservable variables and measurement error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Cohen, P.; West, S.G.; Aiken, L.S. Applied Multiple Regression/Correlation Analysis for the Behavioral Sciences; Psychology Press: London, UK, 2014. [Google Scholar]

- Lu, Y.; Yang, S.; Chau, P.Y.; Cao, Y. Dynamics between the trust transfer process and intention to use mobile payment services: A cross-environment perspective. Inf. Manag. 2011, 48, 393–403. [Google Scholar] [CrossRef]

- Alalwan, A.A.; Dwivedi, Y.K.; Rana, N.P. Factors influencing adoption of mobile banking by Jordanian bank customers: Extending UTAUT2 with trust. Int. J. Inf. Manag. 2017, 37, 99–110. [Google Scholar] [CrossRef]

- Zolait, A.H.S. The nature and components of perceived behavioural control as an element of theory of planned behaviour. Behav. Inf. Technol. 2014, 33, 65–85. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Measure | Items | Frequency | Percentage |

|---|---|---|---|

| Gender | Male | 109 | 42.4 |

| Female | 148 | 57.6 | |

| Age | 16–25 | 89 | 34.6 |

| 26–35 | 66 | 25.7 | |

| 36–45 | 55 | 21.4 | |

| 46–55 | 38 | 14.8 | |

| Over 55 | 9 | 3.5 | |

| Education | High school or less | 85 | 33.1 |

| University | 148 | 57.6 | |

| Graduate school | 24 | 9.3 | |

| Occupation | Full-time student | 93 | 36.2 |

| Military, public service, and education | 26 | 10.1 | |

| Finance | 5 | 1.9 | |

| Communication worker | 3 | 1.2 | |

| Freelancer | 39 | 15.2 | |

| Service industry | 21 | 8.2 | |

| Manufacturing | 28 | 10.9 | |

| Construction industry | 5 | 1.9 | |

| Specialist | 10 | 3.9 | |

| Information industry | 5 | 1.9 | |

| Agricultural/forestry/fishing/herding | 4 | 1.6 | |

| Housewife | 14 | 5.4 | |

| Other | 4 | 1.6 | |

| Mobile payment application used (multiple selection) | ALIPAY | 236 | 41.8 |

| WeChat pay | 244 | 43.2 | |

| UNION pay | 49 | 8.7 | |

| Apple pay | 15 | 2.7 | |

| JD PAY | 12 | 2.0 | |

| Bestpay | 4 | 0.7 | |

| Others | 5 | 0.9 | |

| Length of usage | <3 months | 15 | 5.8 |

| Between 3 and 6 months | 5 | 2.0 | |

| Between 6 months and 12 months | 8 | 3.1 | |

| Between 1 year and 3 years | 88 | 34.2 | |

| Above 3 years | 141 | 54.9 | |

| Frequencies of usage | Everyday | 185 | 72.0 |

| Once per every week | 47 | 18.3 | |

| Once per month | 18 | 7.0 | |

| Others | 7 | 2.7 | |

| Money for average per consumption (RMB) | <100 | 156 | 60.7 |

| 100–500 | 71 | 27.6 | |

| 500–1000 | 12 | 4.7 | |

| More than 1000 | 18 | 7.0 |

| Construct | Measure | Factor Loading | Adapted Source |

|---|---|---|---|

| Perceived Transaction Convenience (PTC) Cronbach’s α = 0.890 Composite Reliability = 0.924 | [20,22,31,61] | ||

| PCT1 | I believe that using mobile payment will be convenient. | 0.853 | |

| PCT2 | I think that it is easy to use mobile payment to accomplish my payment tasks. | 0.851 | |

| PCT3 | Mobile payment saves me time. | 0.880 | |

| PTC4 | Compared to traditional payment methods, I believe that mobile payment methods are more convenient. | 0.883 | |

| Compatibility (COM) Cronbach’s α = 0.818 Composite Reliability = 0.878 | [19,23,25,31,64] | ||

| COM1 | Using mobile payment fits into my lifestyle. | 0.756 | |

| COM2 | I believe that using mobile payment fits well with the way I like to buy. | 0.904 | |

| COM3 | Using mobile payment is compatible with the way I like to shop. | 0.743 | |

| COM4 | I would use the mobile payment over other kinds payment services (e.g., cash or traditional credit cards). | 0.797 | |

| Relative Advantage (RA) Cronbach’s α = 0.852 Composite Reliability = 0.901 | [23,33,68] | ||

| RA1 | Mobile payment is more efficient than Internet or off-line payment. | 0.843 | |

| RA2 | Mobile payment provides greater flexibility. | 0.753 | |

| RA3 | Mobile payment provides quicker access to the transactions that I need to make. | 0.820 | |

| RA4 | Mobile payment is more convenient than Internet or off-line payment | 0.912 | |

| Social interaction (SI) Cronbach’s α = 0.880 Composite Reliability = 0.901 | [11,56,70,71,72] | ||

| SI1 | People who are important to me expect me to use mobile payment. | 0.921 | |

| SI2 | Those people that influence my behavior think that I should use mobile payment. | 0.876 | |

| SI3 | I will use mobile payment if the service is widely used by people in my community | 0.889 | |

| Government Support (GS) Cronbach’s α = 0.897 Composite Reliability = 0.925 | [50,51,52] | ||

| GS1 | The government is active in setting up the facilities to enable mobile payment. | 0.773 | |

| GS2 | For me, the government supporting mobile payment is important. | 0.913 | |

| GS3 | The government promotes the use of the mobile payment. | 0.902 | |

| GS4 | The government has good laws and regulations for mobile payment. | 0.857 | |

| GS5 | For me, the government promoting the use of the mobile payment is important. | 0.761 | |

| Additional Value (AV) Cronbach’s α = 0.924 Composite Reliability = 0.942 | [16,23,27] | ||

| AV1 | I will use mobile payment if I receive an incentive. | 0.879 | |

| AV2 | Using mobile payment would obtain additional value when performing transactions. | 0.809 | |

| AV3 | I will use mobile payment if I receive a discount. | 0.914 | |

| AV4 | I think that using mobile payment would help me to keep up to date with the promotion of e-coupons. | 0.867 | |

| AV5 | I would like to benefit from a discount offered by a mobile payment transaction. | 0.900 | |

| Absorptive Capacity (AC) Cronbach’s α = 0.925 Composite Reliability = 0.943 | [23,34,81] | ||

| AC1 | I have the necessary knowledge to understand mobile payment services. | 0.849 | |

| AC2 | I understand clearly about the goals, tasks and responsibilities of mobile payment services. | 0.838 | |

| AC3 | I have the technical capability to absorb mobile payment knowledge. | 0.869 | |

| AC4 | I have information on state-of-the-art mobile payment services. | 0.920 | |

| AC5 | I have superior skills and capabilities to perform tasks using mobile payment compared to other colleagues. | 0.792 | |

| Affinity (AFFI) Cronbach’s α = 0.906 Composite Reliability = 0.929 | [31,35,82] | ||

| AFFI1 | Using mobile payment is one of my major daily activities. | 0.849 | |

| AFFI2 | I cannot go without using mobile payment for several days. | 0.838 | |

| AFFI3 | I would have a sense of loss without mobile payment. | 0.869 | |

| AFFI4 | Mobile payment is important in my life. | 0.920 | |

| AFFI5 | If my mobile payment is down, I really miss it. | 0.792 | |

| Personal Innovation in IT (PIIT) Cronbach’s α = 0.878 Composite Reliability = 0.914 | [23,37,58,64] | ||

| PIIT1 | I like to try new information technologies. | 0.871 | |

| PIIT2 | I am willing to try new information technologies. | 0.889 | |

| PIIT3 | If I heard about a new information technology, I would look for ways to experiment with it. | 0.897 | |

| PIIT4 | I am usually one of the first among my peers to explore new information technologies. | 0.746 | |

| Perceived Risk (PSR) Cronbach’s α = 0.885 Composite Reliability = 0.918 | [56,57,58] | ||

| PSR1 | I am concerned that the mobile payment system collects too much personal information from my transactions. | 0.884 | |

| PSR2 | I would feel secure sending sensitive information through mobile payment. | 0.869 | |

| PSR3 | Overall mobile payment is a safe place to send sensitive information. | 0.916 | |

| PSR4 | I am not worried about using mobile payment because other people may be able to access my account. | 0.804 | |

| Adoption Intention (AI) Cronbach’s α = 0.950 Composite Reliability = 0.962 | [8,10,25,58] | ||

| AI1 | I intend to use mobile payment in the future. | 0.892 | |

| AI2 | I predict I would use mobile payment in the future. | 0.849 | |

| AI3 | I intend to use mobile payment services when the opportunity arises. | 0.937 | |

| AI4 | I am willing to use mobile payment services in the future. | 0.945 | |

| AI5 | I will always try to use mobile payment in my daily life. | 0.941 | |

| AVE | AC | AFFI | AI | AV | COM | GS | PIIT | PSR | PTC | RA | SI | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| AC | 0.835 | 0.914 | ||||||||||

| AFFI | 0.724 | 0.641 | 0.851 | |||||||||

| AI | 0.752 | 0.701 | 0.614 | 0.867 | ||||||||

| AV | 0.729 | 0.636 | 0.524 | 0.623 | 0.853 | |||||||

| COM | 0.769 | 0.408 | 0.481 | 0.425 | 0.379 | 0.877 | ||||||

| GS | 0.712 | 0.698 | 0.532 | 0.660 | 0.615 | 0.381 | 0.844 | |||||

| PIIT | 0.644 | 0.698 | 0.596 | 0.632 | 0.478 | 0.377 | 0.558 | 0.803 | ||||

| PSR | 0.695 | −0.084 | −0.095 | −0.172 | −0.257 | −0.056 | −0.216 | −0.126 | 0.834 | |||

| PTC | 0.802 | 0.408 | 0.385 | 0.469 | 0.305 | 0.753 | 0.385 | 0.369 | −0.052 | 0.895 | ||

| RA | 0.765 | 0.437 | 0.494 | 0.486 | 0.325 | 0.757 | 0.373 | 0.448 | −0.011 | 0.703 | 0.875 | |

| SI | 0.738 | 0.253 | 0.343 | 0.229 | 0.158 | 0.256 | 0.090 | 0.336 | −0.021 | 0.272 | 0.356 | 0.859 |

| Hypothesis | Path Coefficient | t-Value | Decision |

|---|---|---|---|

| H1: Perceived Transaction Convenience → Adoption Intention | 0.160 *** | 6.771 | supported |

| H2: Compatibility → Adoption Intention | 0.137 *** | 6.585 | supported |

| H3: Relative Advantage → Adoption Intention | 0.124 *** | 4.936 | supported |

| H4: Social Influence → Adoption Intention | −0.026 ns | −1.841 | non-supported |

| H5: Government Support → Adoption Intention | 0.114 *** | 4.573 | supported |

| H6: Additional Value → Adoption Intention | 0.151 *** | 7.032 | supported |

| H7: Perceived Risk → Adoption Intention | −0.051 *** | −4.350 | supported |

| H8: Absorptive Capacity → Adoption Intention | 0.400 *** | 14.735 | supported |

| H9: Affinity → Adoption Intention | 0.111 *** | 3.400 | supported |

| H10: Personal Innovation in IT → Adoption Intention | 0.091 *** | 4.573 | supported |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chen, W.-C.; Chen, C.-W.; Chen, W.-K. Drivers of Mobile Payment Acceptance in China: An Empirical Investigation. Information 2019, 10, 384. https://doi.org/10.3390/info10120384

Chen W-C, Chen C-W, Chen W-K. Drivers of Mobile Payment Acceptance in China: An Empirical Investigation. Information. 2019; 10(12):384. https://doi.org/10.3390/info10120384

Chicago/Turabian StyleChen, Wei-Chuan, Chien-Wen Chen, and Wen-Kuo Chen. 2019. "Drivers of Mobile Payment Acceptance in China: An Empirical Investigation" Information 10, no. 12: 384. https://doi.org/10.3390/info10120384

APA StyleChen, W.-C., Chen, C.-W., & Chen, W.-K. (2019). Drivers of Mobile Payment Acceptance in China: An Empirical Investigation. Information, 10(12), 384. https://doi.org/10.3390/info10120384