The Effects of Agricultural Price Instability on Vertical Price Transmission: A Study of the Wheat Chain in Italy

Abstract

1. Introduction

2. Background and Literature Review

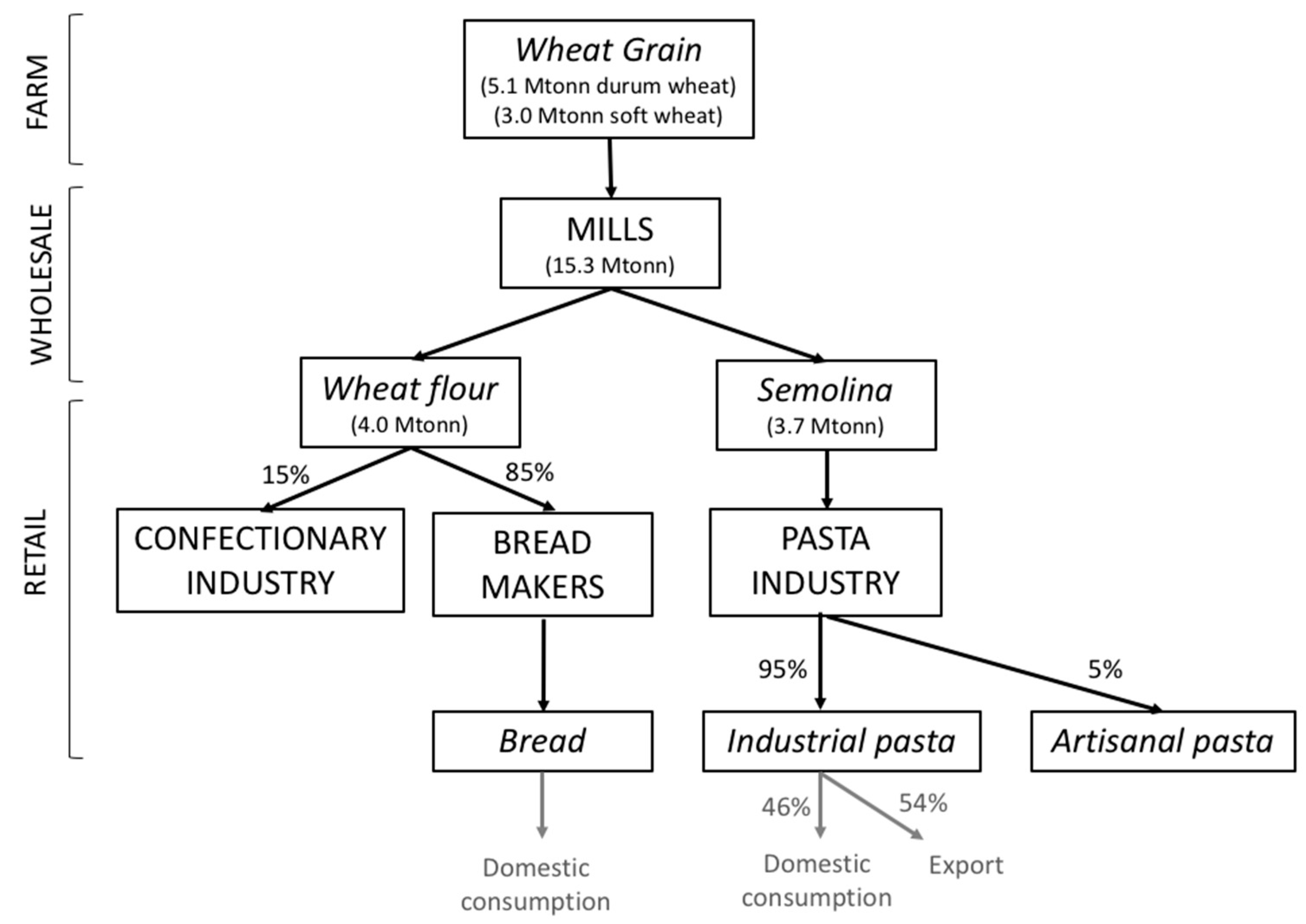

3. The Italian Wheat Value Chain

4. Materials and Methods

5. Empirical Results

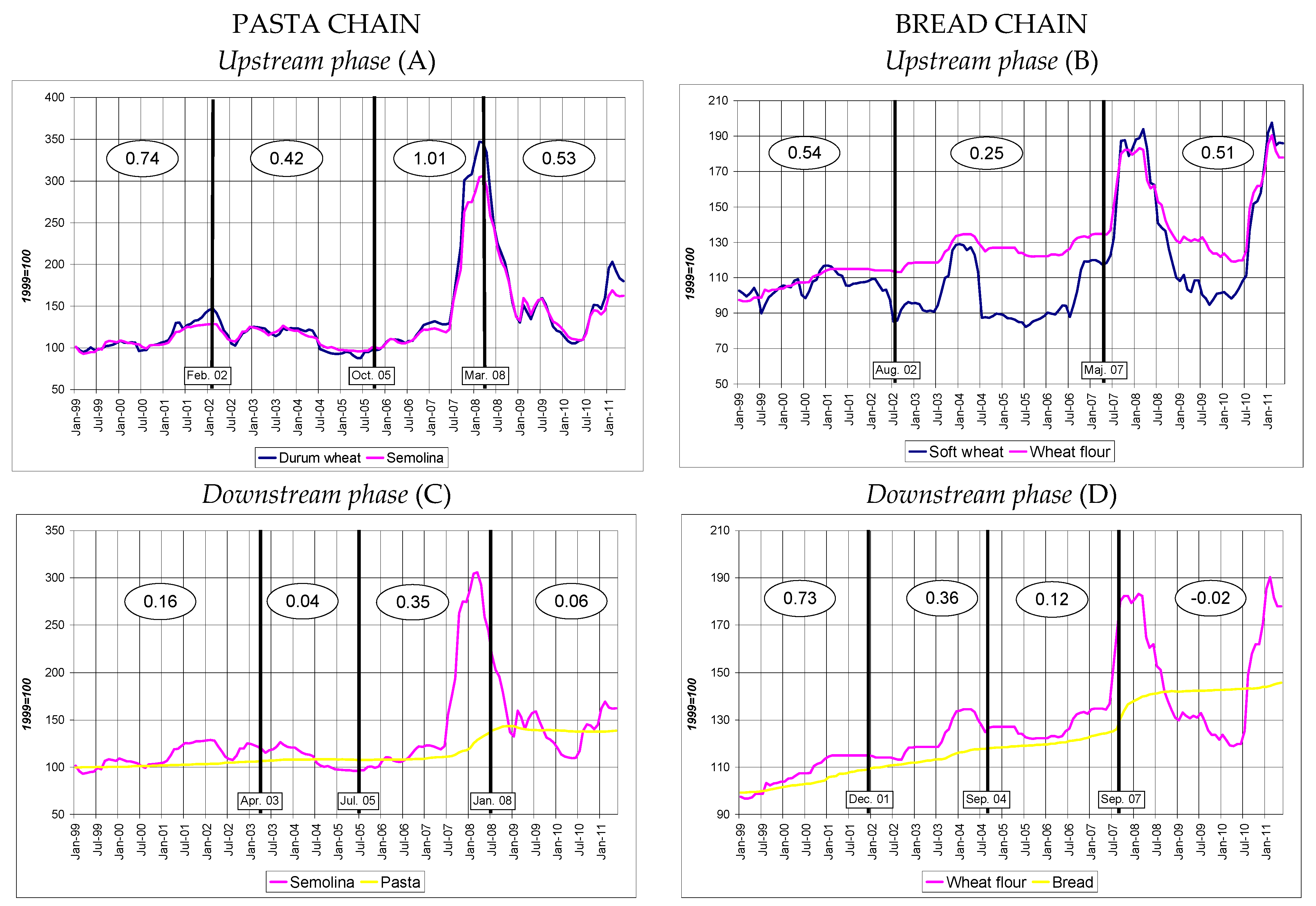

5.1. Price Transmission in the Pasta Chain

5.2. Price Transmission in the Bread Chain

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Castellini, C.; Boggia, A.; Cortina, C.; Dal Bosco, A.; Paolotti, L.; Novelli, E.; Mugnai, C. A multicriteria approach for measuring the sustainability of different poultry production systems. J. Clean. Prod. 2012, 37, 192–201. [Google Scholar] [CrossRef]

- Ciliberti, S.; Frascarelli, A. L’obbligo dei contratti di cessione dei prodotti agricoli e alimentari: Una valutazione degli effetti dell’articolo 62 della legge n. 27/2012. Econ. Agro-Aliment. 2014. (In Italic) [Google Scholar] [CrossRef]

- Bakucs, Z.; Falkowski, J.; Fertö, I. Does market structure influence price transmission in the agro-food sector? A meta-analysis perspective. J. Agric. Econ. 2014, 65, 1–25. [Google Scholar] [CrossRef]

- Lloyd, T. Forty years of price transmission research in the food industry: Insights, challenges and prospects. J. Agric. Econ. 2017, 68, 3–21. [Google Scholar] [CrossRef]

- Kinnucan, H.W.; Tadjion, O. Theoretical restrictions on farm-retail price transmission elasticities: A note. Agribusiness 2014, 30, 278–289. [Google Scholar] [CrossRef]

- Peltzman, S. Prices rise faster than they fall. J. Polit. Econ. 2000, 108, 466–502. [Google Scholar] [CrossRef]

- Sexton, R.J.; Lavoie, N. Food processing and distribution: An industrial organization approach. Handb. Agric. Econ. 2001, 1, 863–932. [Google Scholar]

- Ball, L.; Mankiw, N.G. Asymmetric price adjustment and economic fluctuations. Econ. J. 1994, 104, 247–261. [Google Scholar] [CrossRef]

- Meyer, J.; Von Cramon-Taubadel, S. Asymmetric price transmission: A survey. J. Agric. Econ. 2004, 55, 581–611. [Google Scholar] [CrossRef]

- Frey, G.; Manera, M. Econometric Models of Asymmetric Price Transmission. J. Econ. Surv. 2007, 21, 349–415. [Google Scholar] [CrossRef]

- Peri, M.; Baldi, L. Nonlinear price dynamics between CO2 futures and Brent. Appl. Econ. Lett. 2011, 18, 1207–1211. [Google Scholar] [CrossRef]

- Cavicchioli, D. Detecting Market Power Along Food Supply Chains: Evidence and Methodological Insights from the Fluid Milk Sector in Italy. Agriculture 2018, 8, 191. [Google Scholar] [CrossRef]

- Brümmer, B.; Von Cramon-Taubadel, S.; Zorya, S. The impact of market and policy instability on price transmission between wheat and flour in Ukraine. Eur. Rev. Agric. Econ. 2009, 36, 203–230. [Google Scholar] [CrossRef]

- Levy, D.; Bergen, M.; Dutta, S.; Venable, R. The magnitude of menu costs: Direct evidence from large US supermarket chains. Q. J. Econ. 1997, 112, 791–824. [Google Scholar] [CrossRef]

- Richards, T.J.; Gómez, M.I.; Lee, J. Pass-through and consumer search: An empirical analysis. Am. J. Agric. Econ. 2014, 96, 1049–1069. [Google Scholar] [CrossRef]

- Kinnucan, H.W.; Forker, O.D. Asymmetry in farm-retail price transmission for major dairy products. Am. J. Agric. Econ. 1987, 69, 285–292. [Google Scholar] [CrossRef]

- Oladosu, G.; Msangi, S. Biofuel-Food Market Interactions: A Review of Modeling Approaches and Findings. Agriculture 2013, 3, 53–71. [Google Scholar] [CrossRef]

- OECD Food Price Formation, OECD Trade and Agriculture Directorate 2015. Available online: http://www.oecd.org/site/agrfcn/meetings/agrfcn-7-food-price-formation-paper-october-2015.pdf (accessed on 1 December 2018).

- Cacchiarelli, L.; Lass, D.; Sorrentino, A. CAP reform and price transmission in the Italian pasta chain. Agribusiness 2016, 32, 482–497. [Google Scholar] [CrossRef]

- Kejriwal, M.; Perron, P. Testing for multiple structural changes in cointegrated regression models. J. Bus. Econ. Stat. 2010, 28, 503–522. [Google Scholar] [CrossRef]

- Gregory, A.W.; Hansen, B.E. Residual-based tests for cointegration in models with regime shifts. J. Econ. 1996, 70, 99–126. [Google Scholar] [CrossRef]

- Kejriwal, M. Cointegration with structural breaks: An application to the Feldstein-Horioka puzzle. Stud. Nonlinear Dyn. Econ. 2008, 12. [Google Scholar] [CrossRef]

- Boetel, B.L.; Liu, D.J. Estimating structural changes in the vertical price relationships in US beef and pork markets. J. Agric. Resour. Econ. 2010, 35, 228–244. [Google Scholar]

- Phillips, P.C.; Loretan, M. Estimating long-run economic equilibria. Rev. Econ. Stud. 1991, 58, 407–436. [Google Scholar] [CrossRef]

- Banerjee, A.; Dolado, J.J.; Galbraith, J.W.; Hendry, D. Co-integration, error correction, and the econometric analysis of non-stationary data. OUP Cat. 1993. [Google Scholar]

- Krugman, P. The finite world. The New York Times, 26 December 2010. [Google Scholar]

- Headey, D. Rethinking the global food crisis: The role of trade shocks. Food Policy 2011, 36, 136–146. [Google Scholar] [CrossRef]

- Tadasse, G.; Algieri, B.; Kalkuhl, M.; Von Braun, J. Drivers and Triggers of International Food Price Spikes and Volatility. In Food Price Volatility and Its Implications for Food Security and Policy; Kalkuhl, M., Von Braun, J., Torero, M., Eds.; Springer International Publishing: Cham, Switzerland, 2016; pp. 59–82. ISBN 978-3-319-28201-5. [Google Scholar]

- Ghosh, J. The Unnatural Coupling: Food and Global Finance. J. Agrar. Ch. 2010, 10, 72–86. [Google Scholar] [CrossRef]

- Yang, J.; Qiu, H.; Huang, J.; Rozelle, S. Fighting global food price rises in the developing world: The response of China and its effect on domestic and world markets. Agric. Econ. 2008, 39, 453–464. [Google Scholar] [CrossRef]

- Baldi, L.; Peri, M.; Vandone, D. Stock markets’ bubbles burst and volatility spillovers in agricultural commodity markets. Res. Int. Bus. Financ. 2016, 38, 277–285. [Google Scholar] [CrossRef]

- Chakravorty, U.; Hubert, M.-H.; Moreaux, M.; Nøstbakken, L. Will Biofuel Mandates Raise Food Prices? University of Alberta, Department of Economics: Edmonton, AB, Canada, 2011. [Google Scholar]

- Thompson, P.B. The Agricultural Ethics of Biofuels: The Food vs. Fuel Debate. Agriculture 2012, 2, 339–358. [Google Scholar] [CrossRef]

- Hochman, G.; Kaplan, S.; Rajagopal, D.; Zilberman, D. Biofuel and Food-Commodity Prices. Agriculture 2012, 2, 272–281. [Google Scholar] [CrossRef]

- Martin, W.; Anderson, K. Export Restrictions and Price Insulation During Commodity Price Booms. Am. J. Agric. Econ. 2012, 94, 422–427. [Google Scholar] [CrossRef]

- Wright, B.D. The Economics of Grain Price Volatility. Appl. Econ. Perspect. Policy 2011, 33, 32–58. [Google Scholar] [CrossRef]

- Kouyaté, C.; Von Cramon-Taubadel, S. Distance and border effects on price transmission: A meta-analysis. J. Agric. Econ. 2016, 67, 255–271. [Google Scholar] [CrossRef]

- Bakucs, L.Z.; Fertö, I.; Szabó, G.G. Price transmission in the Hungarian vegetable sector. Stud. Agric. Econ. 2007, 106, 23–40. [Google Scholar]

- Bakucs, L.Z.; Fertö, I. Marketing and pricing dynamics in the presence of structural breaks: The Hungarian pork market. J. Int. Food Agric. Bus. Mark. 2009, 21, 116–133. [Google Scholar] [CrossRef]

- Bakucs, L.Z.; Fertö, I. Marketing margins and price transmission on the Hungarian beef market. Acta Agric. Scand. Sect. C 2006, 3, 151–160. [Google Scholar]

- Bakucs, L.Z.; Fertö, I. Marketing margins and price transmission on the Hungarian pork meat market. Agribusiness 2005, 21, 273–286. [Google Scholar] [CrossRef]

- Guillen, J.; Franquesa, R. Testing for market power in the Spanish meat market: Price transmission elasticity and asymmetry using econometric models. Int. J. Comput. Econ. Econ. 2010, 1, 294–308. [Google Scholar] [CrossRef]

- Serra, T.; Goodwin, B.K. Price transmission and asymmetric adjustment in the Spanish dairy sector. Appl. Econ. 2003, 35, 1889–1899. [Google Scholar] [CrossRef]

- Ben-Kaabia, M.; Gil, J.M. Asymmetric price transmission in the Spanish lamb sector. Eur. Rev. Agric. Econ. 2007, 34, 53–80. [Google Scholar] [CrossRef]

- Ben-Kaabia, M.; Gil, J.M.; Ameur, M. Vertical integration and non-linear price adjustments: The Spanish poultry sector. Agribusiness 2005, 21, 253–271. [Google Scholar] [CrossRef]

- Rezitis, A.N.; Reziti, I. Threshold cointegration in the Greek milk market. J. Int. Food Agribus. Mark. 2011, 23, 231–246. [Google Scholar] [CrossRef]

- Reziti, I.; Panagopoulos, Y. Asymmetric price transmission in the greek agri-food sector: Some tests. Agribus. Int. J. 2008, 24, 16–30. [Google Scholar] [CrossRef]

- Vavra, P.; Goodwin, B.K. Analysis of Price Transmission Along the Food Chain; OECD Publishing: Paris, Franace, 2005. [Google Scholar] [CrossRef]

- Bolotova, Y.V.; Novakovic, A.M. The impact of the New York state milk price gouging law on the price transmission process and supermarket pricing strategies in the fluid whole milk market. Agribusiness 2012, 28, 377–399. [Google Scholar] [CrossRef]

- Awokuse, T.O.; Wang, X. Threshold effects and asymmetric price adjustments in US dairy markets. Can. J. Agric. Econ. 2009, 57, 269–286. [Google Scholar] [CrossRef]

- Karantininis, K.; Katrakilidis, C.; Karfakis, C.; Persson, M. Price Transmission in the Swedish Pork Chain: New Evidence from Asymmetric ARDL modeling. In Proceedings of the EAAE 2011 Congress Change and Uncertainty Challenges for Agriculture, Food and Natural Resources, Zurich, Switzerland, 30 August–2 September 2011. [Google Scholar]

- Gervais, J.-P. Disentangling nonlinearities in the long-and short-run price relationships: An application to the US hog/pork supply chain. Appl. Econ. 2011, 43, 1497–1510. [Google Scholar] [CrossRef]

- Falkowski, J. Price transmission and market power in a transition context: Evidence from the Polish fluid milk sector. Post-Communist Econ. 2010, 22, 513–529. [Google Scholar] [CrossRef]

- London Economics Investigation of the Determinants of Farm-Retail Price Spreads 2004. Available online: https://londoneconomics.co.uk/wp-content/uploads/2011/09/92-Investigation-of-the-determinants-of-farm-retail-price-spreads.pdf (accessed on 30 November 2018).

- Santeramo, F.G.; Cramon-Taubadel, S. Von On perishability and Vertical Price Transmission: Empirical evidences from Italy. Bio-Based Appl. Econ. 2016, 5, 199–214. [Google Scholar]

- Madau, F.A.; Furesi, R.; Pulina, P. The existence of buyer power in the Italian fresh milk supply chain. Br. Food J. 2016, 118, 70–82. [Google Scholar] [CrossRef]

- Antonioli, F.; Ben Kaabia, M.; Arfini, F.; Gil, J.M. Price transmission dynamics for quality-certified food products: A comparison between conventional and organic fluid milk in Italy. Agribusiness 2018. [Google Scholar] [CrossRef]

- Carraro, A.; Stefani, G. Vertical price transmission in Italian agri–food chains: Does the transmission elasticity change always or sometimes. In Proceedings of the presentation at the XLVII Conference SIDEA, Campobasso, Italy, 22–25 September 2010; Volume 22, p. 25. [Google Scholar]

- Cacchiarelli, L.; Sorrentino, A. Antitrust intervention and price transmission in pasta supply chain. Agric. Food Econ. 2015, 4, 2. [Google Scholar] [CrossRef]

- Cacchiarelli, L.; Sorrentino, A. Market power in food supply chain: Evidence from Italian pasta chain. Br. Food J. 2018, 120, 2129–2141. [Google Scholar] [CrossRef]

- Monasterolo, I.; Pasqualino, R.; Janetos, A.C.; Jones, A. Sustainable and Inclusive Food Systems through the Lenses of a Complex System Thinking Approach—A Bibliometric Review. Agriculture 2016, 6, 44. [Google Scholar] [CrossRef]

- Ravallion, M. Testing market integration. Am. J. Agric. Econ. 1986, 68, 102–109. [Google Scholar] [CrossRef]

- Sexton, R.J.; Kling, C.L.; Carman, H.F. Market integration, efficiency of arbitrage, and imperfect competition: Methodology and application to US celery. Am. J. Agric. Econ. 1991, 73, 568–580. [Google Scholar] [CrossRef]

- Zanias, G.P. Testing for integration in European Community agricultural product markets. J. Agric. Econ. 1993, 44, 418–427. [Google Scholar] [CrossRef]

- Baulch, B. Testing for food market integration revisited. J. Dev. Stud. 1997, 33, 512–534. [Google Scholar] [CrossRef]

- Ardeni, P.G. Does the law of one price really hold for commodity prices? Am. J. Agric. Econ. 1989, 71, 661–669. [Google Scholar] [CrossRef]

- Baffes, J. Some further evidence on the law of one price: The law of one price still holds. Am. J. Agric. Econ. 1991, 73, 1264–1273. [Google Scholar] [CrossRef]

- ISMEA Scheda di Settore Cereali 2017. Available online: http://www.ismeamercati.it/flex/cm/pages/ServeBLOB.php/L/IT/IDPagina/3524. (accessed on 18 January 2019).

- Dickey, D.A.; Fuller, W.A. Distribution of the Estimators for Autoregressive Time Series with a Unit Root. J. Am. Stat. Assoc. 1979, 74, 427–431. [Google Scholar]

- Perron, P. The great crash, the oil price shock, and the unit root hypothesis. Econom. J. Econ. Soc. 1989, 1361–1401. [Google Scholar] [CrossRef]

- Zivot, E.; Andrews, D.W.K. Further evidence on the great crash, the oil-price shock, and the unit-root hypothesis. J. Bus. Econ. Stat. 2002, 20, 25–44. [Google Scholar] [CrossRef]

- Lee, J.; Strazicich, M.C. Minimum Lagrange multiplier unit root test with two structural breaks. Rev. Econ. Stat. 2003, 85, 1082–1089. [Google Scholar] [CrossRef]

- Perron, P. Dealing with structural breaks. Palgrave Handb. Econ. 2006, 1, 278–352. [Google Scholar]

- Bai, J.; Perron, P. Estimating and testing linear models with multiple structural changes. Econometrica 1998, 47–78. [Google Scholar] [CrossRef]

- Bai, J.; Perron, P. Computation and analysis of multiple structural change models. J. Appl. Econ. 2003, 18, 1–22. [Google Scholar] [CrossRef]

- Engle, R.F.; Granger, C.W. Co-integration and error correction: Representation, estimation, and testing. Econom. J. Econ. Soc. 1987, 251–276. [Google Scholar] [CrossRef]

- Arai, Y.; Kurozumi, E. Testing for the null hypothesis of cointegration with a structural break. Econ. Rev. 2007, 26, 705–739. [Google Scholar] [CrossRef]

- Phillips, P.C. Time series regression with a unit root. Econom. J. Econ. Soc. 1987, 277–301. [Google Scholar] [CrossRef]

- Cutts, M.; Kirsten, J. Asymmetric Price Transmission and Market Concentration: An Investigation into Four South African Agro-Food Industries. S. Afr. J. Econ. 2006, 74, 323–333. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Test | ADF | ZA | LS | |||||

|---|---|---|---|---|---|---|---|---|

| Level | Level+Trend | Level | Level+Trend | Trend | Level | Level+Trend | ||

| Durum wheat | −2.49 | −2.84 | −3.85 | −4.93 | −3.06 | −3.18 | −4.54 | |

| Semolina | −2.80 | −3.21 | −4.49 | −6.01 | −3.29 | −2.88 | −4.33 | |

| Pasta | −1.04 | −2.84 | −7.59 | −7.16 | −3.76 | −3.27 | −4.67 | |

| Soft wheat | −1.83 | −2.33 | −3.42 | −3.43 | −2.87 | −2.78 | −4.19 | |

| Flour | −1.74 | −2.88 | −3.63 | −3.71 | −3.00 | −2.90 | −4.17 | |

| Bread | −0.57 | −2.25 | −5.57 | −8.96 | −2.35 | −2.45 | −4.18 | |

| Critical Value | ||||||||

| 1% | −3.48 | −4.02 | −5.43 | −5.57 | −4.93 | −4.55 | −6.32 | −6.45 |

| 5% | −2.88 | −3.44 | −4.80 | −5.08 | −4.42 | −3.84 | −5.73 | −5.67 |

| 10% | −2.58 | −3.14 | −3.50 | −5.32 | −5.31 | |||

| Specifications: zt = {1, variable}, q = 2, M = 3, ε = 0.20, xt = {0} p = 0 | ||||

| y | Semolina | Pasta | Wheat flour | Bread |

| z | Durum wheat | Semolina | Soft wheat | Wheat flour |

| sup FT(1) | 12.33 *** | 214.90 *** | 70.25 *** | 1,177.43 *** |

| sup FT(2) | 73.05 *** | 336.69 *** | 40.20 *** | 2,085.04 *** |

| sup FT(3) | 329.99 *** | 1,357.70 *** | 58.89 *** | 27,553.76 *** |

| UD max | 329.99 *** | 1,357.70 *** | 70.25 *** | 27,553.76 *** |

| sup FT(2|1) | 96.08 *** | 80.70 *** | 18.68 ** | 72.97 *** |

| sup FT(3|2) | 16.78 * | 205.14 *** | 48.87 *** | |

| Break dates | ||||

| Feb. 03 | Apr. 03 | Aug. 02 | Dec. 01 | |

| C.I. 95% | Aug. 00—Feb. 03 | Mar. 03—Jun. 03 | May 02—Mar. 03 | Oct. 01—Feb. 02 |

| Oct. 05 | Jul. 05 | May 07 | Sep. 04 | |

| C.I. 95% | Aug. 05—Feb. 06 | Jan. 05—Aug. 05 | Oct. 05—Dec. 08 | May 04—Oct. 04 |

| Mar. 08 | Jan. 08 | Sep. 07 | ||

| C.I. 95% | Dec. 07—May 08 | Nov. 07—Feb. 08 | Aug. 07—Oct. 07 | |

| Gregory Hansen (ADF*, Zt*) | Arai-Kurozumi-Kejrival | |||||||

|---|---|---|---|---|---|---|---|---|

| Test | C | C/T | C/S | V3(λ) | V2(λ) | λ1 | λ2 | λ3 |

| Semolina/Durum wheat | −4.73 | −4.84 | −5.21 | 0.04 | 0.24 | 0.54 | 0.74 | |

| Pasta/Semolina | −4.06 | −5.86 | −4.04 | 0.05 | 0.28 | 0.48 | 0.70 | |

| Wheat flour/Soft wheat | −5.50 | −6.89 | −5.58 | 0.15 | 0.29 | 0.67 | ||

| Bread/Wheat flour | −2.72 | −2.95 | −3.71 | 0.12 | 0.23 | 0.46 | 0.70 | |

| Critical Value | ||||||||

| 1% | 0.15 | 0.16 | ||||||

| 5% | 0.09 | 0.09 | ||||||

| 10% | −4.34 | −4.72 | −4.68 | 0.07 | 0.08 | |||

| Pasta Chain | |||||

|---|---|---|---|---|---|

| upstream (farm-wholesale) | downstream (wholesale-retail) | ||||

| Semolina | Pasta | ||||

| Est. Param. | t-stat. | Est. Param. | t-stat. | ||

| Intercept: | |||||

| Constant (D1) | 1.24 | 2.12 | Constant (D1) | 3.91 | 39.27 |

| D2 | 1.50 | 2.19 | D2 | 0.60 | 2.03 |

| D3 | −1.18 | −1.92 | D3 | −0.82 | −4.07 |

| D4 | 1.07 | 1.76 | D4 | 0.72 | 6.95 |

| Farm Price: | |||||

| Durum wheat | 0.74 | 5.96 | Semolina | 0.16 | 7.35 |

| Durum wheat*D2 | −0.33 | −2.24 | Semolina*D2 | −0.12 | −1.92 |

| Durum wheat*D3 | 0.27 | 2.07 | Semolina*D3 | 0.19 | 4.44 |

| Durum wheat*D4 | −0.21 | −1.63 | Semolina*D4 | −0.10 | −4.45 |

| Phillips & Loretan (1,1,1,) Terms: | |||||

| Contempor. coeff. | −0.67 | −4.62 | Contempor. coeff. | −0.03 | −1.17 |

| Lead coeff. | 0.37 | 2.69 | Lead coeff. | 0.04 | 1.72 |

| Lag coeff. | 0.13 | 0.97 | Lag coeff. | −0.01 | −0.61 |

| Lagged residuals | 0.82 | 11.28 | Lagged residuals | 0.66 | 9.21 |

| Adjusted R2 | 0.93 | Adjusted R2 | 0.99 | ||

| Durbin-Watson | 1.49 | Durbin-Watson | 1.91 | ||

| Bread Chain | |||||

|---|---|---|---|---|---|

| upstream (farm-wholesale) | downstream (wholesale-retail) | ||||

| Wheat flour | Bread | ||||

| Intercept: | Est. Param. | t-stat. | Est. Param. | t-stat. | |

| Constant (D1) | 2.16 | 5.23 | Constant (D1) | 1.22 | 14.95 |

| D2 | 1.53 | 3.58 | D2 | 1.78 | 14.27 |

| D3 | 0.35 | 0.83 | D3 | 2.99 | 21.48 |

| D4 | 3.85 | 43.78 | |||

| Farm Price: | |||||

| Soft wheat | 0.54 | 6.15 | Wheat flour | 0.73 | 42.12 |

| Soft wheat*D2 | −0.30 | −3.21 | Wheat flour*D2 | −0.37 | −14.13 |

| Soft wheat*D3 | −0.04 | −0.40 | Wheat flour*D3 | −0.61 | −21.22 |

| Wheat flour*D4 | −0.76 | −40.65 | |||

| Phillips & Loretan (1.1,1,) Terms: | |||||

| Contempor. coeff. | −0.23 | −3.88 | Contempor. coeff. | −0.06 | −2.27 |

| Lead coeff. | 0.19 | 3.37 | Lead coeff. | 0.03 | 1.01 |

| Lag coeff. | 0.04 | 0.67 | Lag coeff. | 0.05 | 2.09 |

| Lagged residuals | 0.80 | 12.83 | Lagged residuals | 0.97 | 19.07 |

| Adjusted R2 | 0.96 | Adjusted R2 | 0.997 | ||

| Durbin-Watson | 1.66 | Durbin-Watson | 1.87 | ||

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ricci, E.C.; Peri, M.; Baldi, L. The Effects of Agricultural Price Instability on Vertical Price Transmission: A Study of the Wheat Chain in Italy. Agriculture 2019, 9, 36. https://doi.org/10.3390/agriculture9020036

Ricci EC, Peri M, Baldi L. The Effects of Agricultural Price Instability on Vertical Price Transmission: A Study of the Wheat Chain in Italy. Agriculture. 2019; 9(2):36. https://doi.org/10.3390/agriculture9020036

Chicago/Turabian StyleRicci, Elena Claire, Massimo Peri, and Lucia Baldi. 2019. "The Effects of Agricultural Price Instability on Vertical Price Transmission: A Study of the Wheat Chain in Italy" Agriculture 9, no. 2: 36. https://doi.org/10.3390/agriculture9020036

APA StyleRicci, E. C., Peri, M., & Baldi, L. (2019). The Effects of Agricultural Price Instability on Vertical Price Transmission: A Study of the Wheat Chain in Italy. Agriculture, 9(2), 36. https://doi.org/10.3390/agriculture9020036