Global Biofuels at the Crossroads: An Overview of Technical, Policy, and Investment Complexities in the Sustainability of Biofuel Development

Abstract

1. Introduction

2. Biofuel Production Pathways

2.1. Primary Fuel Types

2.1.1. Generation 1/Conventional Biofuels

2.1.2. Generation 2/Advanced Biofuels

3. Key Feedstocks for Biofuel Production

3.1. Lignocellulose

3.2. Algae

3.3. Corn

3.4. Jatropha

3.5. Palm

3.6. Soybeans

3.7. Sugarcane

3.8. Sweet Sorghum

3.9. Notable Comparisons

4. Key Issues and Performance Considerations with Biofuel Sustainability

4.1. The Food-Fuel Debate

4.2. Emissions

4.3. Land

4.4. Water

4.5. Biodiversity

4.6. Fuel Performance

4.7. Tradeoffs of Fuel Sustainability

5. Policy Considerations

5.1. Brazil

5.2. China

5.3. EU

5.4. India

5.5. United States

5.6. Unsustainable System Issues—Conflicts between Sustainability, Policy, and Trade

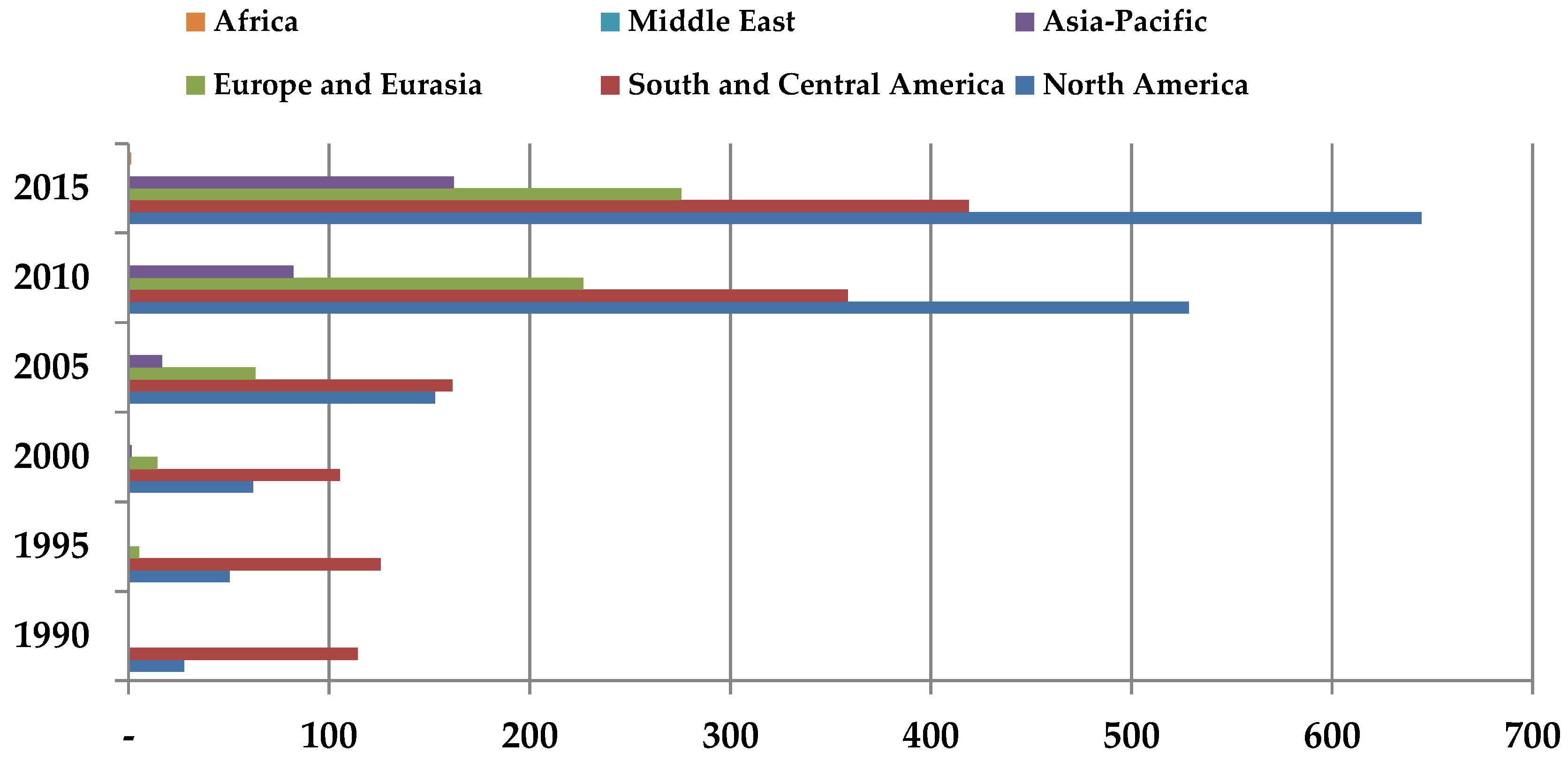

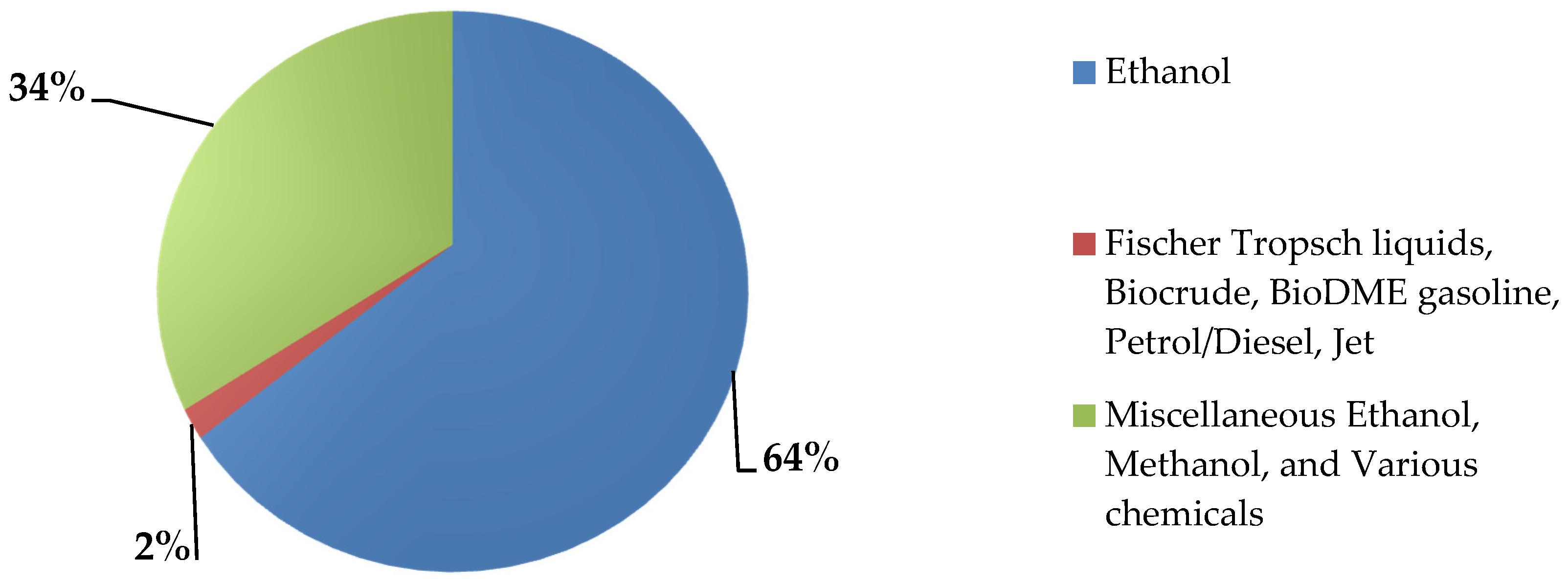

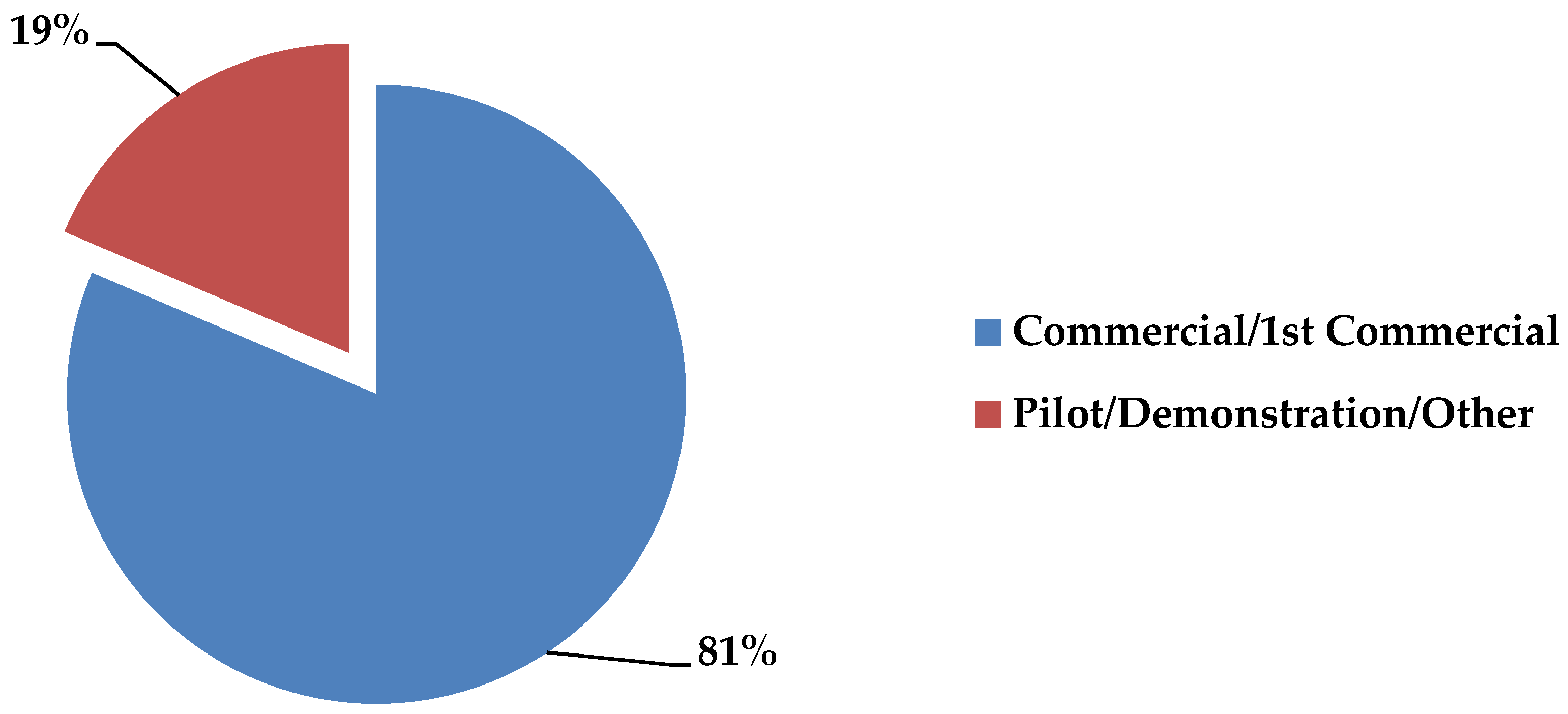

6. Investment in Biofuels

7. Conclusions

Acknowledgments

Conflicts of Interest

References

- Araújo, K. Low Carbon Energy Transitions: Turning Points in National Policy and Innovation; Oxford University Press: New York, NY, USA, 2017. [Google Scholar]

- Kovarik, B. History of Biofuels. In Biofuels Crops; Singh, B.P., Ed.; Center for Bioscience International (CABI): Wellington, UK, 2013. [Google Scholar]

- Renewable Energy Network 21 (REN21). Global Status Report; REN21: Paris, France, 2016. [Google Scholar]

- International Renewable Energy Agency (IRENA). Innovation Outlook: Advanced Liquid Biofuels; International Renewable Energy Agency: Abu Dhabi, UAE, 2016. [Google Scholar]

- International Renewable Energy Agency (IRENA). Boosting Biofuels; International Renewable Energy Agency: Abu Dhabi, UAE, 2016. [Google Scholar]

- International Energy Agency (IEA). CO2 Emissions from Combustion; IEA/OECD: Paris, France, 2016. [Google Scholar]

- IEA. Data Subscription, 2016. IEA/OECD: Paris, France. Available online: https://www.iea.org/statistics/onlinedataservice/ (accessed on 10 December 2016).

- BP. Statistical Review of World Energy; BP: London, UK, 2016. [Google Scholar]

- Energy Information Administration (EIA). Available online: http://www.eia.gov/totalenergy/data/annual/index.php (accessed on 10 August 2016).

- International Civil Aviation Organization (ICAO). 2013 Environmental Report: Destination Green; International Civil Aviation Organization: Montreal, QC, Canada, 2013. [Google Scholar]

- International Air Transportation Association (IATA). 2015 Report on Alternative Fuels; International Air Transportation Association: Montreal, QC, Canada; Geneva, Switzerland, 2015. [Google Scholar]

- Milman, O. First Deal to Curb Aviation Emissions Agreed in Landmark UN Accord. The Guardian. Available online: https://www.theguardian.com/environment/2016/oct/06/aviation-emissions-agreement-united-nations (accessed on 6 October 2016).

- Huenteler, J.; Lee, H. The Future of Low Carbon Road Transport; Rapporteur’s Report; Belfer Center, Kennedy School of Government, Harvard University: Cambridge, MA, USA, 2015. [Google Scholar]

- Biofuels: The Fuel of the Future, Asia. Available online: http://www.biofuel.org.uk (accessed on 25 July 2016).

- German Agency for Technical Cooperation (GTZ); Worldwatch; German Federal Ministry of Food; Agriculture and Consumer Protection (BMELV). Biofuels for Transportation. 2006. Available online: http://www.worldwatch.org/system/files/EBF008_1.pdf (accessed on 10 October 2016).

- Organization for Economic Cooperation and Development (OECD)-UN Food and Agriculture Organization (FAO). Agricultural Outlook 2016–2025; OECD: Paris, France, 2016. [Google Scholar]

- International Energy Agency (IEA). Biofuels for Transport; IEA/OECD: Paris, France, 2011. [Google Scholar]

- Kojima, M.; Johnson, T. Potential for Biofuels in Transport in Developing Countries; ESMAP Paper, Knowledge Exchange Series No 4; World Bank: Washington, DC, USA, 2006. [Google Scholar]

- Seelke, C.; Yacobucci, B. Ethanol and Other Biofuels: Potential for U.S.-Brazil Cooperation; CRS Report RL34191, September 27, 2007, and Environmental Protection Agency (EPA), Renewable Fuel Standard Program. Available online: https://www.epa.gov/renewable-fuel-standard-program (accessed on 20 July 2016).

- Anderson, J.; DiCicco, D.; Ginder, J.; Kramer, U.; Raney-Pablo, H.; Wallington, T. High Octane Number Ethanol-Gasoline Blends. Fuel 2012, 97, 585–594. [Google Scholar] [CrossRef]

- U.S. Department of Agriculture (USDA). EU Biofuels Annual 2016; GAIN Report Number NL 6021; USDA: Washington, DC, USA, 2016.

- U.S. Department of Agriculture (USDA). EU’s General Court Rules Against Anti-Dumping Duty on US; GAIN Report GM E16025; USDA: Washington, DC, USA, 2016.

- U.S. Department of Agriculture (USDA). EU Biofuel Mandates by Member State; GAIN Report GM 16009; USDA: Washington, DC, USA, 2016.

- Theiss, T.; Alleman, T.; Brooker, A.; Elgowainy, A.; Fioroni, G.; Han, J.; Huff, S.; Johnson, C.; Kass, M.; Leiby, P.; et al. Summary of High-Octane, Mid-Level Ethanol Blends Study; ORNL/TM-2016/42; Oak Ridge National Laboratory: Oak Ridge, TN, USA, 2016.

- Consumer Reports. Diesel vs. Biodiesel vs. Vegetable Oil. Available online: http://www.consumerreports.org/cro/2012/05/diesel-vs-biodiesel-vs-vegetable-oil/index.htm (accessed on 20 August 2016).

- Solomon, B.; Bailis, R. (Eds.) Sustainable Development of Biofuels in Latin America and the Caribbean; Springer: New York, NY, USA, 2014. [Google Scholar]

- Department of Energy (DOE). Alternative Fuels Data Center. Available online: http://www.afdc.energy.gov/fuels/emerging.html (accessed on 28 August 2016).

- Aatola, H.; Larmi, M.; Sarjovaara, T.; Mikkonen, S. Hydrotreated Vegetable Oil (HVO) as a Renewable Diesel Fuel: Trade-off between NOx, Particulate Emission, and Fuel Consumption of a Heavy Duty Engine. SAE Int. J. Engines 2008, 1, 1251–1262. [Google Scholar] [CrossRef]

- Davis, R.; Tao, L.; Scarlata, C.; Tan, C.; Ross, J.; Lukas, J.; Sexton, D. Process Design and Economics for the Conversion of Lignocellulosic Biomass to Hydrocarbons; NREL/TP-5100-62498; National Renewable Energy Laboratory: Golden, CO, USA, 2015.

- Murphy, C.; Kendall, A. Lifecycle Analysis of Biochemical Cellulosic Ethanol under Multiple Scenarios. GCB Bioenergy 2015, 7, 1019–1033. [Google Scholar]

- Hadar, Y. Sources for Lignocellulosic Raw Materials for the Production of Ethanol. In Lignocellulose Conversion; Springer: Heidelberg, Germany, 2013. [Google Scholar]

- Kahr, H.; Wimberger, J.; Schürz, D.; Jäger, A. Evaluation of the Biomass Potential for the Production of Lignocellulosic Bioethanol from Various Agricultural Residues in Austria and Worldwide. Energy Proc. 2013, 40, 146–155. [Google Scholar] [CrossRef][Green Version]

- Kumar, G.; Bakonyi, P.; Periyasamy, S.; Kim, S.H.; Nemestóthy, N.; Bélafi-Bakó, K. Lignocellulose biohydrogen: Practical challenges and recent progress. Renew. Sustain. Energy Rev. 2015, 44, 728–737. [Google Scholar] [CrossRef]

- U.S. Environmental Protection Agency (U.S. EPA). Biofuels and the Environment: The First Triennial Report to Congress (2011 Final Report); EPA/600/R-10/183F; U.S. Environmental Protection Agency: Washington, DC, USA, 2011.

- Dismukes, G.; Carrieri, D.; Bennette, N.; Ananyev, G.; Posewitz, M. Aquatic Phototrophs: Efficient Alternatives to Land-based Crops for Biofuels. Curr. Opin. Biotechnol. 2008, 19, 235–240. [Google Scholar] [CrossRef] [PubMed]

- Scott, S.; Davey, M.; Dennis, J.; Horst, I.; Howe, C.; Lea-Smith, D.; Smith, A. Biodiesel from Algae: Challenges and Prospects. Curr. Opin. Biotechnol. 2010, 21, 277–286. [Google Scholar] [PubMed]

- Elbehri, A.; Liu, A.; Segerstedt, A.; Liu, P.; Babilonia Estrada, R.; Hölldobler, B.W.; Davies, S.J.C.; Stephen Navarro, C.L.; Andrew, J.F.; Pérez, H. Biofuels and the Sustainability Challenge: A Global Assessment of Sustainability Issues, Trends and Policies for Biofuels and Related Feedstocks; FAO: Rome, Italy, 2013. [Google Scholar]

- European Environment Agency (EEA). How Much Bioenergy Can Europe Produce without Harming the Environment? EC: Copenhagen, Denmark, 2006. [Google Scholar]

- Aden, A. Water Usage for Current and Future Ethanol Production. Southwest Hydrol. 2007, 6, 22–23. [Google Scholar]

- National Research Council (NRC). Water Implications of Biofuels Production in the United States; NRC: Washington, DC, USA, 2008. [Google Scholar]

- Koundinya, V. Jatropha Profile; Agricultural Marketing Resource Center: Ames, IA, USA, 2008. [Google Scholar]

- Lane, J. Jatropha around the World. Biofuels Digest. Available online: http://www.biofuelsdigest.com/bdigest/2014/09/11/jatropha-around-the-world-as-sgb-raises-11m-heres-a-13-country-tour-development-activity/ (accessed on 11 September 2014).

- De Gorter, H.; Drabik, D.; Just, D. The Economics of Biofuel Policies; Palgrave: New York, NY, USA, 2015. [Google Scholar]

- Verheye, W.H. Growth and Production of Oil Palm; UNESCO-EOLSS Publishers: Belgium, Europe, 2010. [Google Scholar]

- Rosillo-Calle, F.; Pelkmans, L.; Walter, A. A Global Overview of Vegetable Oils, with Reference to Biodiesel, Task 40 IEA Bioenergy Report; IEA: Paris, France, 2009. [Google Scholar]

- Thoenes, P. Soybean International Commodity Profile, Background Paper for the Competitive Commercial Agriculture in Sub-Saharan Africa (CCAA) Study; FAO: Rome, Italy, 2006. [Google Scholar]

- FAO. Information. Available online: http://www.fao.org/ (accessed on 10 December 2016).

- FAOSTAT. Information. Available online: http://faostat3.fao.org/home/E.%2019%20Aug.%202016 (accessed on 10 December 2016).

- Brittaine, R.; Lutaladio, N. Jatropha: A Smallholder Bioenergy Crop. In Integrated Crop Management; FAO: Rome, Italy, 2010; Volume 8, pp. 1–95. [Google Scholar]

- Wahl, N.; Hildebrandt, T.; Moser, C.; Lüdeke-Freund, F.; Averdunk, K.; Bailis, R.; Barua, K.K.; Burritt, R.; Groeneveld, J.H.; Klein, A.-M.; et al. Insights into Jatropha Projects Worldwide: Key Facts & Figures from a Global Survey; Centre for Sustainability Management: Lüneburg, Germany, 2012. [Google Scholar]

- Sumathi, S.; Chai, S.P.; Mohamed, A.R. Utilization of Oil Palm as a Source of Renewable Energy in Malaysia. Renew. Sustain. Energy Rev. 2008, 12, 2404–2421. [Google Scholar] [CrossRef]

- Kandel, H.; Knodel, J.J. Canola Production Field Guide; NDSU Extension Service: Farg, ND, USA, 2011; pp. 1–122. [Google Scholar]

- North, S.; Eberbach, P.; Thompson, J. Wheat and Canola Water Requirements and the Effect of Spring Irrigation on Crop Yields in the Central Murray Valley. In Global Issues, Paddock Action; Verlag: Veterinärmedizin, Austria, 2008; pp. 1–5. [Google Scholar]

- Cereal Rye/The University of Vermont Extension Crops & Soils Team. Available online: http://northerngraingrowers.org/wp-content/uploads/RYE.pdf (accessed on 19 August 2016).

- USDA. Information. 2016. Available online: http://plants.usda.gov/core/profile?symbol=JACU2 (accessed on 30 June 2016).

- High Level Panel of Experts of Food Security and Nutrition (HLPE), UN Committee on World Food Security. Biofuels and Food Security, Report; HLPE: Rome, Italy, 2013. [Google Scholar]

- High Level Panel of Experts of Food Security and Nutrition (HLPE), UN Committee on World Food Security. Price Volatility and Food Security, Report; HLPE, UN Committee on World Food Security: Rome, Italy, 2011. [Google Scholar]

- Thompson, B.P. The Agricultural Ethics of Biofuels: The Food vs. Fuel Debate. Agriculture 2012, 2, 339–358. [Google Scholar]

- Oladosu, G.; Msangi, S. Biofuel-Food Market Interactions: A Review of Modeling Approaches and Findings. Agriculture 2013, 3, 53–71. [Google Scholar] [CrossRef]

- Tomei, J.; Helliwell, R. Food versus Fuel? Going Beyond Biofuels. Land Use Policy 2016, 56, 320–326. [Google Scholar] [CrossRef]

- UN Food and Agriculture Organization (FAO). Food Outlook, Biennial Report on Global Food Markets; FAO: Rome, Italy, 2016. [Google Scholar]

- Searchinger, T.; Heimlich, R.; Houghton, R.A.; Dong, F.; Elobeid, A.; Fabiosa, J.; Tokgoz, S.; Hayes, D.; Yu, T.-H. Use of U.S. Croplands for Biofuels Increases Greenhouse Gases through Emissions from Land-Use Change. Science 2008, 319, 1238–1240. [Google Scholar] [PubMed]

- Yang, Q.; Chen, G.Q. Greenhouse gas emissions of corn—Ethanol production in China. Ecol. Model. 2013, 252, 176–184. [Google Scholar] [CrossRef]

- Kahn Ribeiro, S.; Figueroa, M.; Creutzig, F.; Dubeux, C.; Hupe, J.; Kobayashi, S. 2012: Chapter 9—Energy End-Use: Transport. In Global Energy Assessment—Toward a Sustainable Future; Cambridge University Press: Cambridge, UK; New York, NY, USA; The International Institute for Applied Systems Analysis: Laxenburg, Austria, 2008; pp. 575–648. [Google Scholar]

- Holma, A.; Koponen, K.; Antikainen, R.; Lardon, L.; Leskinen, P.; Roux, P. Current Limits of Life Cycle Assessment Framework in Eevaluating Environmental Sustainability—Case of Two Evolving Biofuel Technologies. J. Clean. Prod. 2013, 54, 215–228. [Google Scholar] [CrossRef]

- Highina, B.; Bugaje, I.; Umar, B. A Review of Second Generation Biofuel: A Comparison of its Carbon Footprints. Eur. J. Eng. Technol. 2014, 2, 117–125. [Google Scholar]

- Ji, X.; Long, X. A Review of the Ecological and Socioeconomic Effects of Biofuel and Energy Policy Recommendations. Renew. Sustain. Energy Rev. 2016, 61, 41–52. [Google Scholar] [CrossRef]

- Xue, J.; Grift, T.; Hansen, A. Effect of Biodiesel on Engine Performance and Emissions. Renew. Sustain. Energy Rev. 2011, 15, 1098–1116. [Google Scholar] [CrossRef]

- UN Department of Economic and Social Affairs (UN DESA), Population Division. 2015 Revision, World Population Prospects, Report; ESA/P/WP.241; United Nations: New York, NY, USA, 2015. [Google Scholar]

- FAO; Earthscan/Routledge. The State of the World’s Land and Water Resources for Food and Agriculture; FAO and Earthscan/Routledge: Abingdon, UK, 2011. [Google Scholar]

- Fischer, G.; van Velthuizen, H.; Shah, M.; Nachtergaele, F. Global Agro-Ecological Assessment for Agriculture in the 21st Century; Report RR 02 02; IIASA; FAO: Laxenburg, Austria; Rome, Italy, 2002. [Google Scholar]

- Popp, J.; Lakner, Z.; Harangi-Rakos, M.; Fari, M. The Effect of Bioenergy Expansion: Food, Energy and Environment. Renew. Sustain. Energy Rev. 2014, 32, 559–578. [Google Scholar] [CrossRef]

- Borras, S.; Franco, J. Global Land Grabbing and Trajectories of Agrarian Change: A Preliminary Analysis. J. Agrar. Chang. 2012, 12, 34–59. [Google Scholar] [CrossRef]

- Edenhofer, O.; Pichs-Madruga, R.; Sokona, Y.; Seyboth, K.; Matschoss, P.; Kadner, S.; Zwickel, T.; Eickemeier, P.; Hansen, G.; Schlomer, S.; et al. Renewable Energy Sources and Climate Change Mitigation; Special Report of the IPCC; IPCC, 2011; Available online: http://www.ipcc.ch/report/srren/ (accessed on 10 August 2016).

- Doornbosch, R.; Steenblik, R. Biofuels: Is the Cure Worse the Curse? SG/SD/RT(2007)3/REV1; OECD, Round Table on Sustainable Development: Paris, France, 2007. [Google Scholar]

- Fischer, G.; van Velthuizen, H.; Nachtergaele, F. Global Agro-Ecological Zones Assessment; Report RP 06 003; IIASA: Vienna, Austria, 2006. [Google Scholar]

- Bransby, D.; McLaughlin, S.; Parrish, D. A Review of Carbon and Nitrogen Balances in Switchgrass Grown for Energy. Biomass Bioenergy 1998, 14, 379–384. [Google Scholar] [CrossRef]

- Scott, C.; Sugg, Z. Global Energy Development and Climate-Induced Water Scarcity-Physical Limits, Sectoral Constraints, and Policy Imperatives. Energies 2015, 8, 8211–8225. [Google Scholar] [CrossRef]

- Cowie, A.; Soimakallio, S.; Brandao, M. Environmental Risks and Opportunities of Biofuels. In The Law and Policy of Biofuels; Bouthillier, Y.L., Cowie, A., Martin, P., McLeod-Kilmurray, H., Eds.; Edward Elgar: Cheltenham, UK, 2016. [Google Scholar]

- De Baan, L.D.; Alkemade, R.; Koellner, T. Land Use Impacts on Biodiversity in LCA: A Global Approach. Int. J. Life Cycle Assess. 2013, 18, 1216–1230. [Google Scholar]

- De Baan, L.; Mutel, C.; Curran, M.; Hellweg, S.; Koellner, T. Land Use in Lifecycle Assessment. Environ. Sci. Technol. 2013, 47, 9281–9290. [Google Scholar] [CrossRef] [PubMed]

- Constanza, R.; d’Arge, R.; de Groot, R.; Farber, S.; Grasso, M.; Hannon, B.; Limburg, K.; Naeem, S.; O’Neill, R.V.; Paruelo, J.; et al. The Value of the World’s Ecosystem Services and Natural Capital. Nature 1997, 387, 253–260. [Google Scholar] [CrossRef]

- Constanza, R.; de Groot, R.; Sutton, P.; van der Ploeg, S.; Anderson, S.; Kubizewski, I.; Farber, S.; Turner, R. Changes in the Value of Global Ecosystems Services. Glob. Environ. Chang. 2014, 26, 152–158. [Google Scholar] [CrossRef]

- Morgera, E.; Kulovesi, K.; Gobena, A. Case Studies on Bioenergy Policy and Law: Options for Sustainability; FAO Legal Office: Rome, Italy, 2009. [Google Scholar]

- USEPA. A Comprehensive Analysis of Biodiesel Impacts on Exhaust Emissions; US Environmental Protection Agency (EPA): Washington, DC, USA, 2002.

- Grosjean, D.; Miguel, A.H.; Tavares, T.M. Urban Air Pollution in Brazil: Acetaldehyde and other Carbonyls. Atmos. Environ. Part B Urban Atmos. 1990, 24, 101–106. [Google Scholar]

- Liska, A.J.; Yang, H.; Milner, M.; Goddard, S.; Blanco-Canqui, H.; Pelton, M.P.; Fang, X.X.; Zhu, H.; Suyker, A.E. Biofuels from Crop Residue can Reduce Soil Carbon and Increase CO2 emissions. Nat. Clim. Chang. 2014, 4, 398–401. [Google Scholar] [CrossRef]

- Groom, M.; Gray, E.; Townsend, E. Biofuels and Biodiversity. Conserv. Biol. 2008, 22, 602–609. [Google Scholar] [CrossRef] [PubMed]

- Carriquiry, M.; Du, X.; Tomilsina, G. Second-Generation Biofuels: Economics and Policies, Policy Research Working Papers; The World Bank Development Research Group, Environment and Energy Team: Washington, DC, USA, 2010; Volume 5406, p. 57. [Google Scholar]

- Wang, M.; Jan, J.; Dunn, J.; Cai, H.; Elgowainy, A. Well-to-wheels Energy Use and Greenhouse Gas Emissions of Ethanol from Corn, Sugarcane, and Cellulosic Biomass for U.S. Use. Environ. Res. Lett. 2012, 7, 4. [Google Scholar]

- Spang, E.S.; Moomaw, W.R.; Gallagher, K.S.; Kirshen, P.H.; Marks, D.H. The Water Consumption of Energy Production: An International Comparison. Environ. Res. Lett. 2014, 9, 10. [Google Scholar] [CrossRef]

- Pradhan, A.; Shrestha, D.; Van Gerpen, J.; McAloon, A.; Yee, W.; Haas, M.; Duffield, J. Reassessment of Life Cycle Greenhouse Gas Emissions for Soybean Biodiesel. Trans. ASABE 2012, 55, 2257–2264. [Google Scholar] [CrossRef]

- Fore, S.; Porter, P.; Lazerus, W. Net Energy Balance of Small-Scale On-Farm Biodiesel Production from Canola and Soybean. Biomass Bioenergy 2011, 35, 2234–2244. [Google Scholar] [CrossRef]

- Buratti, C.; Moretti, E.; Fantozzi, F. Assessing the GHG Emissions of Rapeseed and Soybean Biodiesel in Compliance to the EU Renewable Energy Directive Methodology for Biofuels. In Proceedings of the 18th European Biomass Conference and Exhibition, Lyon, France, 3–7 May 2010. [Google Scholar]

- Harto, C.; Meyers, R.; Williams, E. Life Cycle Water Use of Low Carbon Transport Fuels. Energy Policy 2010, 38, 4933–4944. [Google Scholar] [CrossRef]

- U.S. Department of Agriculture (USDA). Brazil Biofuels Annual 2016; GAIN Report Number BR 16009; Brazilian Law 13.263/2016; USDA: Washington, DC, USA, 2016.

- Langevin, M.S. The Brazilian Biodiesel Program. Available online: http://www.ensec.org/index.php?option=com_content&view=article&id=273:brazilian-biodiesel-program&catid=112:energysecuritycontent&Itemid=367 (accessed on 14 December 2010).

- U.S. Department of Agriculture (USDA). China Biofuels Annual Report; GAIN Report CH 15030; USDA: Washington, DC, USA, 2015.

- Lane, J. Biofuels Mandates around the World: 2016. Biofuels Digest. Available online: http://www.biofuelsdigest.com/bdigest/2016/01/03/biofuels-mandates-around-the-world-2016/ (accessed on 3 January 2016).

- European Union, Climate and Energy Package. Available online: http://ec.europa.eu/clima/policies/strategies/2020/index_en.htm (accessed on 15 October 2016).

- U.S. Department of Agriculture (USDA). India Biofuels Annual 2016; GAIN Report Number IN 6088; USDA: Washington, DC, USA, 2016.

- PTI, India Will Soon be Zero Petroleum Import Country. India Times. 6 September 2016. Available online: http://economictimes.indiatimes.com/industry/energy/oil-gas/india-will-soon-be-zero-petroleum-import-country-nitin-gadkari/articleshow/54031397.cms (accessed on 6 September 2016).

- Bramcourt, K. The Renewable Fuel Standard (RFS): Waiver Authority and Modification of Volumes; Congressional Research Service: Washington, DC, USA, 2016. [Google Scholar]

- Bramcourt, K. The Renewable Fuel Standard (RFS). In Brief; Congressional Research Service: Washington, DC, USA, 2016; pp. 7–5700. [Google Scholar]

- 42 USC 7547 (o)(5). Available online: https://casetext.com/statute/42-usc-7547-nonroad-engines-and-vehicles (accessed on 10 December 2016).

- U.S. Public Law 109-58. Available online: https://www.gpo.gov/fdsys/pkg/PLAW-109publ58/content-detail.html (accessed on 10 December 2016).

- U.S. Public Law 110-140. Available online: https://www.gpo.gov/fdsys/pkg/PLAW-110publ140/content-detail.html (accessed on 10 December 2016).

- U.S. Public Law 114-113. Available online: https://www.gpo.gov/fdsys/pkg/PLAW-114publ113/html/PLAW-114publ113.htm (accessed on 10 December 2016).

- 26 U.S. Code 6426. Available online: https://www.gpo.gov/fdsys/granule/USCODE-2010-title26/USCODE-2010-title26-subtitleF-chap65-subchapB-sec6426 (accessed on 10 December 2016).

- U.S. Public Law 114-113 and 26 U.S. Code 40A. Available online: https://www.law.cornell.edu/uscode/text/26/40A (accessed on 10 December 2016).

- U.S. Public Law. 113–79. Available online: https://www.gpo.gov/fdsys/pkg/PLAW-113publ79/html/PLAW-113publ79.htm (accessed on 10 December 2016).

- U.S. Public Law 112–240. Available online: https://www.gpo.gov/fdsys/pkg/PLAW-112publ240/html/PLAW-112publ240.htm (accessed on 10 December 2016).

- 7 U.S. Code 8105. Available online: https://www.law.cornell.edu/uscode/text/7/8105 (accessed on 10 December 2016).

- International Institute for Sustainable Development (IISD). The U.S. Close to the Controversial Splash and Dash Biofuels Subsidy Loophole. 2016. Available online: https://www.iisd.org/gsi/news/united-states-closes-controversial-splash-and-dash-biofuels-subsidy-loophole (accessed on 10 November 2008).

- EU. Anti-Dumping Biodiesel. 2016. Available online: http://trade.ec.europa.eu/tdi/case_history.cfm?id=1893&init=1893 (accessed on 31 December 2016).

- EU. DS473: European Union—Anti-Dumping Measures on Biodiesel from Argentina. 2016. Available online: https://www.wto.org/english/tratop_e/dispu_e/cases_e/ds473_e.htm (accessed on 31 December 2016).

- EU. European Union—Anti-Dumping Measures on Biodiesel from Indonesia. 2015. Available online: https://www.wto.org/english/tratop_e/dispu_e/cases_e/ds480_e.htm (accessed on 31 December 2016).

- EU. EU No 1194/2013 of 19 November 2013; EU Court Annuls Anti-Dumping Duties Slapped on Biodiesel Exports. Buenos Aires Herald. Available online: http://www.buenosairesherald.com/article/221645/eu-court-annuls-antidumping-duties-slapped-on-biodiesel-exports (accessed on 16 September 2016).

- California Environmental Protection Agency. Low Carbon Fuel Standard; 2016. Available online: https://www.arb.ca.gov/fuels/lcfs/lcfs.htm (accessed on 26 November 2016).

- Energy Information Administration (EIA). Biofuels Issues and Trends; EIA: Washington, DC, USA, 2012. [Google Scholar]

- UN Environment Programme and Bloomberg New Energy Finance (UNEP-BNEF). Global Trends in Sustainable Energy Investments 2016; Frankfurt School-UNEP Centre/BNEF: Frankfurt, Germany, 2016. [Google Scholar]

- UN Environment Programme and Bloomberg New Energy Finance (UNEP-BNEF). Global Trends in Sustainable Energy Investments 2009; Frankfurt School-UNEP Centre/BNEF: Frankfurt, Germany, 2009. [Google Scholar]

- Hochman, G. Biofuels at a Crossroads. Choices 2014, 29, 1–5. [Google Scholar]

- Reuters, United Airlines buy $30 Million Stake Fulcrum Bioenergy. 30 June 2016. Available online: http://www.reuters.com/article/us-fulcrum-ual-idUSKCN0PA1IW20150630 (accessed on 30 June 2016).

- Business Wire, JetBlue Announces One of the Largest Renewable Jet Fuel Purchase Agreements in Aviation History, Business Wire. Available online: http://www.businesswire.com/news/home/20160919006273/en/JetBlue-Announces-Largest-Renewable-Jet-Fuel-Purchase (accessed on 19 September 2016).

- Dupont. Available online: http://www.dupont.com/ (accessed on 15 October 2016).

- International Renewable Energy Agency (IRENA). Project Inventory, Advanced Liquid Biofuels; IRENA: Abu Dhabi, UAE, 2016. [Google Scholar]

- International Energy Agency (IEA). Medium Term Renewable Energy Market Report 2016; IEA/OECD: Paris, France, 2016. [Google Scholar]

- International Energy Agency (IEA). World Energy Outlook 2015; IEA/OECD: Paris, France, 2015. [Google Scholar]

- Uduman, N.; Qi, Y.; Danquah, M.; Forde, G.; Hoadley, A. Dewatering of Microalgal cultures: A Major Bottleneck to Algae-based Fuels. J. Renew. Sustain. Energy 2010, 2, 012701. [Google Scholar] [CrossRef]

- International Energy Agency (IEA). World Energy Outlook 2016; IEA/OECD: Paris, France, 2013. [Google Scholar]

- Financier Worldwide, Abengoa Fails to Renew and Files for Bankruptcy. Financier Worldwide Magazine. February 2016. Available online: https://www.financierworldwide.com/abengoa-fails-to-renew-and-files-for-bankruptcy/#.WIO8gPkrLIU (accessed on 1 February 2016).

- Corrigan, T. U.S. Objects to Abengoa Bankruptcy-Exit Plan. Available online: http://www.wsj.com/articles/u-s-objects-to-abengoa-bankruptcy-exit-plan-1480630625 (accessed on 1 December 2016).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Generation 1 Ethanol | Generation 2/Cellulosic Ethanol | Biodiesel (FAME/RME) | Drop-in Replacement Fuel: Renewable Diesel | Drop-in Replacement Fuel | BioButanol | Biogas | |

|---|---|---|---|---|---|---|---|

| Feedstock | Sugar or starch-based biomass (Corn, sugarcane, sugar beets, etc.) | Cellulosic material (non-edible corn and sugarcane, etc.) | Vegetable oils, animal fat (soybean, Jatropha, palm) | Flexible mix of raw materials (veg, oils, waste fats) | Cellulosic materials (non-edible corn and sugarcane, etc.) | Cellulosic materials (straw, leaves, grass, etc.) | Waste in landfills, Wastewater, Animal waste, etc. |

| Technology Process | Fermentation, distillation; for starch-based feedstock (corn or cassava) hydrolysis of starch | Hydrolysis then Fermentation | Esterification/Trans-Esterification | Hydrotreating , gasification, pyrolysis, and other thermochemical and biochemical pathways | Fermentation/catalytic conversion, etc. | Fermentation | Natural Action of microorganism |

| End product | Anhydrous ethanol blended as an additive to gasoline; Hydrous ethanol (stand-alone fuel) | Anhydrous ethanol blended as an additive to gasoline; Hydrous ethanol (stand-alone fuel) | Ester-based conventional biodiesel | Bio-based hydro-carbon (renewable diesel, jet fuel, bionaptha, biopropane) | Bio-based hydrocarbon | BioButanol additive to gasoline (mostly low mixtures such as 10%–15% butanol) | Methane, up to 40% CO2, other impurities: H2S, NH3, siloxanes |

| Chemical composition | C2H5OH | C2H5OH | O‖R’-C-O-R (R, R’ = alkyl groups) | CnH2n+2 | C6H14-C12H26 | C4H9OH | CH4 |

| Feedstock (Generation Type) | * Growth Time [47] | * Growth Temperature [47] | * Water Requirements [47] | * Major Growers [48] |

|---|---|---|---|---|

| Algae (Second) | Dependent on type of algae, temperature and light conditions (authors’ assessments) | 16–27 °C | Varies with land and sea-based production; Water intensity is generally high; temperature and pH dependent; Light intensity 1000–10,000 | Emergent |

| Corn (First) | 110–140 days | 18–20 °C | 500–800 mm | Brazil, USA, and China |

| Jatropha (Second) | 90 days [49] | 16–21 °C [41] | 254–1016 mm [41] | Myanmar, India, China, and Indonesia [50] |

| Lignocellulose (Second) | Varies based on source. Grasses: 3–4 months, waste residue such as corn stover takes as long as the crop from which it is derived [31]. | Varies based on source. | Usually need very little water [31] | Emergent |

| Palm (First) | 5–6 months [51] | 27–28 °C [44] | Minimum of 1800 mm [44] | Nigeria, Malaysia, and Indonesia |

| Rapeseed or Canola (First) | 85–110 days [52] | Soil temperatures of 3–12 °C [52] | 300–600 mm [53] | China, India, and Canada |

| Rye (Second) | Not available | 1–4 °C but below 29 °C for germination [54] | Not available | Germany, Poland, and Russia |

| Sorghum (Second) | 110–140 days | 25–35 °C | 450–650 mm | Nigeria, India, and Sudan |

| Soybeans (First) | 100–130 days | 18–35 °C | 450–700 mm | Argentina, Brazil, and USA |

| Sugar beets (First) | 140–200 days | 20–25 °C | 550–750 mm | France, USA, and Russia |

| Sugarcane (First) | 15–16 months | 32–38 °C | 1500–2500 mm | Brazil, China, and India |

| Wheat (First) | 100–130 days | 15–20 °C | 450–650 mm | Russia, China, and India |

| Biofuel | GHG Emissions CO2 e/MJ | Water Intensity L/L Product | Energy Intensity MJ/L | Net Energy Balance MJ/L Product |

|---|---|---|---|---|

| Gasoline (Baseline) | 94 g * | 2.8–4.6 * | 35.4 [90] | 28.3 * |

| Corn Ethanol | 76 g: major contributors 31 g (ethanol production) and 17 g (fertilizer) [90] | 175.4 [91] | 21.3 [90] | 10.1 [90] |

| Sugarcane ethanol | 45 g (includes 16 g from land use change) [90] | 526 [91] | 21.3 [90] | 16.4 [90] |

| Soybean biodiesel | 59.19 g [92] | 369.2 [91] | 32.7 [92] | |

| Rapeseed/canola-based biofuel (Biodiesel) | 59.19 g [92] | 645.5 [91] | 32.7 [92] | 21.6 [93] |

| Cellulosic ethanol | 43 g [94] | 6.5 (Switchgrass) 387 (drought conditions) [95] | 21.3 [90] | 21 (Switchgrass) 20.4 (corn stover) 21.4 (miscanthus) [90] |

| Algae biodiesel | 44 (enclosed production) 216 (open production) [95] | 32.7 [92] |

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Araújo, K.; Mahajan, D.; Kerr, R.; Silva, M.d. Global Biofuels at the Crossroads: An Overview of Technical, Policy, and Investment Complexities in the Sustainability of Biofuel Development. Agriculture 2017, 7, 32. https://doi.org/10.3390/agriculture7040032

Araújo K, Mahajan D, Kerr R, Silva Md. Global Biofuels at the Crossroads: An Overview of Technical, Policy, and Investment Complexities in the Sustainability of Biofuel Development. Agriculture. 2017; 7(4):32. https://doi.org/10.3390/agriculture7040032

Chicago/Turabian StyleAraújo, Kathleen, Devinder Mahajan, Ryan Kerr, and Marcelo da Silva. 2017. "Global Biofuels at the Crossroads: An Overview of Technical, Policy, and Investment Complexities in the Sustainability of Biofuel Development" Agriculture 7, no. 4: 32. https://doi.org/10.3390/agriculture7040032

APA StyleAraújo, K., Mahajan, D., Kerr, R., & Silva, M. d. (2017). Global Biofuels at the Crossroads: An Overview of Technical, Policy, and Investment Complexities in the Sustainability of Biofuel Development. Agriculture, 7(4), 32. https://doi.org/10.3390/agriculture7040032