Exploring the Future Potential of Jute in Bangladesh

,

,  ,

,

Abstract

:1. Introduction

The Jute Sector in Bangladesh: History, Challenges, and Policy Developments

2. Methodology

2.1. Trend Analysis of the Jute Sector

2.2. Analysis of Competitiveness of Jute

| Prices: | Pid = domestic price of output i; |

| Pjd = domestic price of tradable input j; | |

| Pib = international price of output i; | |

| Pjb = international price of tradable input j; | |

| Pnd = market price of non-tradable input n; | |

| Pns = shadow price of non-tradable input n; | |

| Quantities: | Qi = quantity of output; |

| Qj = quantity of tradable input; | |

| Qn = quantity of non-tradable input; | |

| Revenue at private prices: | A = Pid × Qi; |

| Tradable inputs at private prices: | B = Pjd × Qj; |

| Domestic factors at private prices: | C = Pnd × Qn; |

| Revenue at social prices: | E = Pib × Qi; |

| Tradable inputs at social prices: | F = Pjb × Qj; |

| Domestic factors at social prices: | G = Pns × Qn; [14]. |

2.3. Ratio Indicators of Competitiveness

- (a)

- Nominal Protection Coefficient on Output (NPCO): This ratio shows the extent to which domestic prices for output differ from international reference prices. NPCO > 1 means that the domestic farm gate price is greater than the world price of output and is uncompetitive [22]. On the contrary, if NPCO < 1, the production system is competitive. NPCO is expressed as [14]:NPCO = (Pid × Qi)/(Pib × Qi)

- (b)

- Nominal Protection Coefficient on Input (NPCI): This ratio shows how much domestic prices for tradable inputs differ from their social prices. If NPCI > 1, the domestic input cost is greater than the comparable world prices and the system is unprotected by policy. If NPCI < 1, the system is protected by policy. NPCI is defined as follows [14]:NPCI = (Pjd × Qj)/(Pjb × Qj)

- (c)

- Effective Protection Coefficient (EPC): EPC is the ratio of value added in private prices (A–B) to value added in social prices (E–F). An EPC > 1 suggests that government policy protects the producers, while EPC < 1 indicates that producers are unprotected through policy interventions. EPC is expressed as [14]:EPC = {(Pid × Qi) − (Pjd × Qj)}/{(Pib × Qi) − (Pjb × Qj)}

2.4. Profitability Analysis of Jute

2.5. The Stochastic Production Frontier Approach to Analyse the Productivity and Efficiency of Jute

2.6. Data and the Study Area

2.7. Empirical Specification of the Stochastic Production Frontier Model

3. Results and Discussion

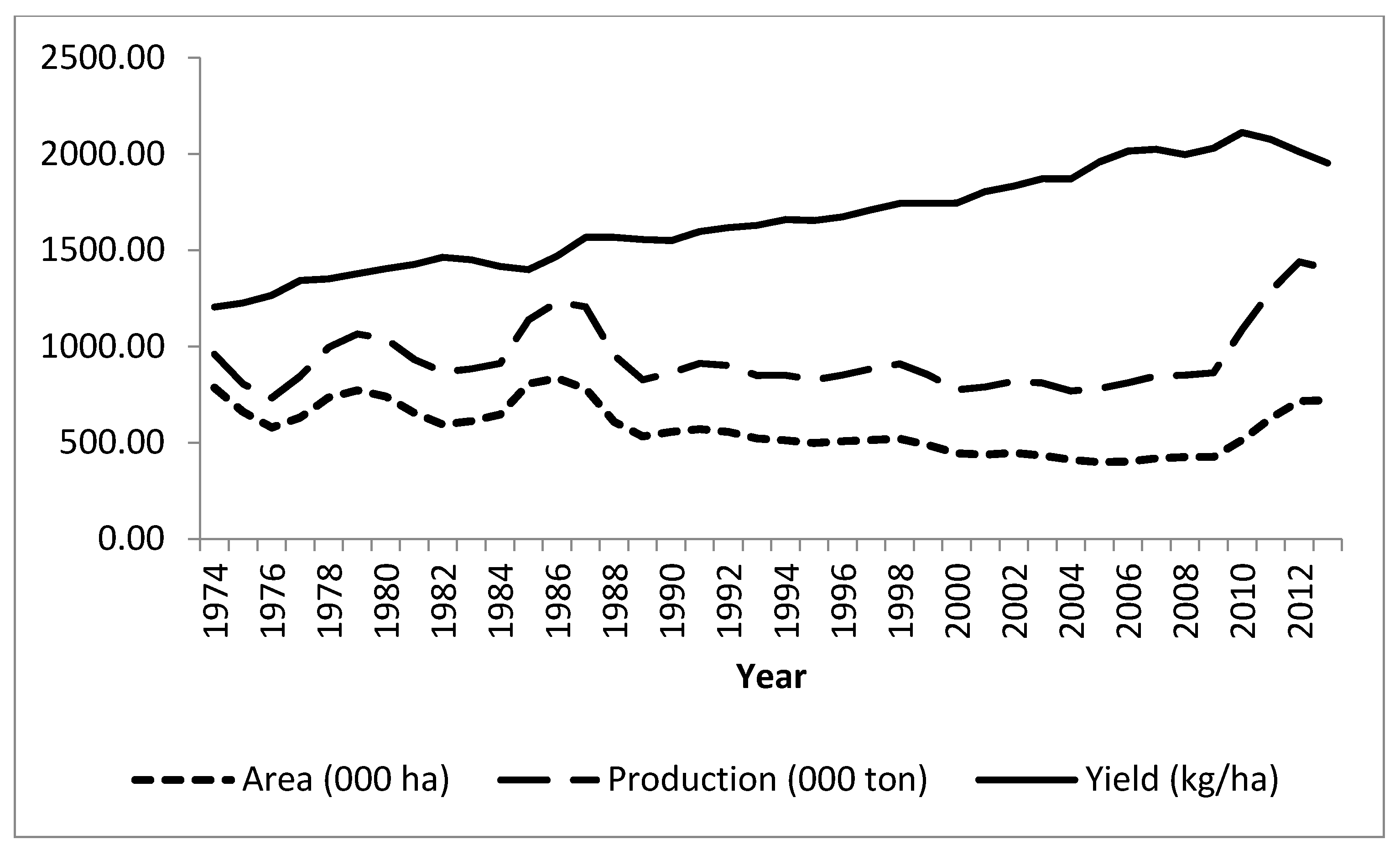

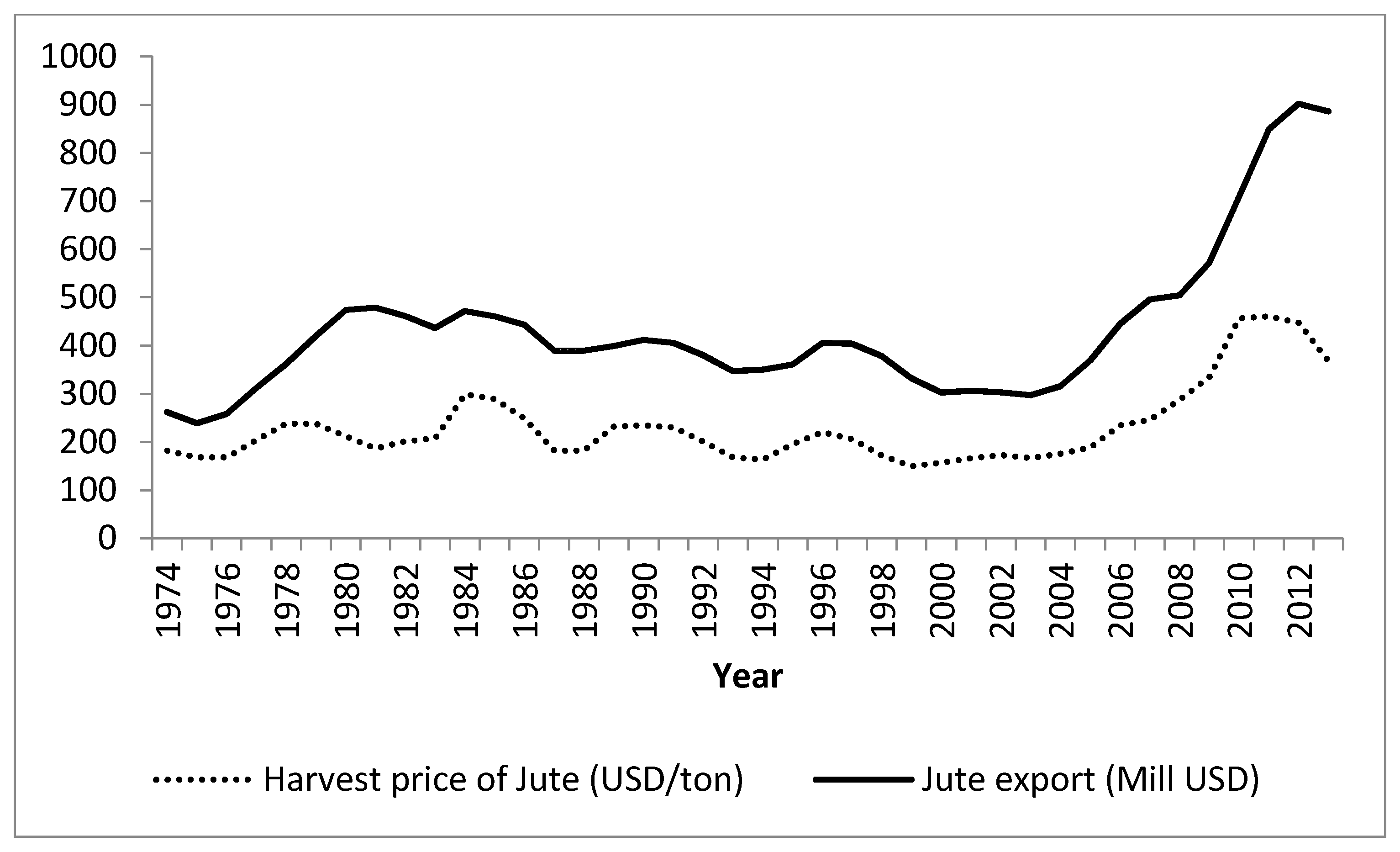

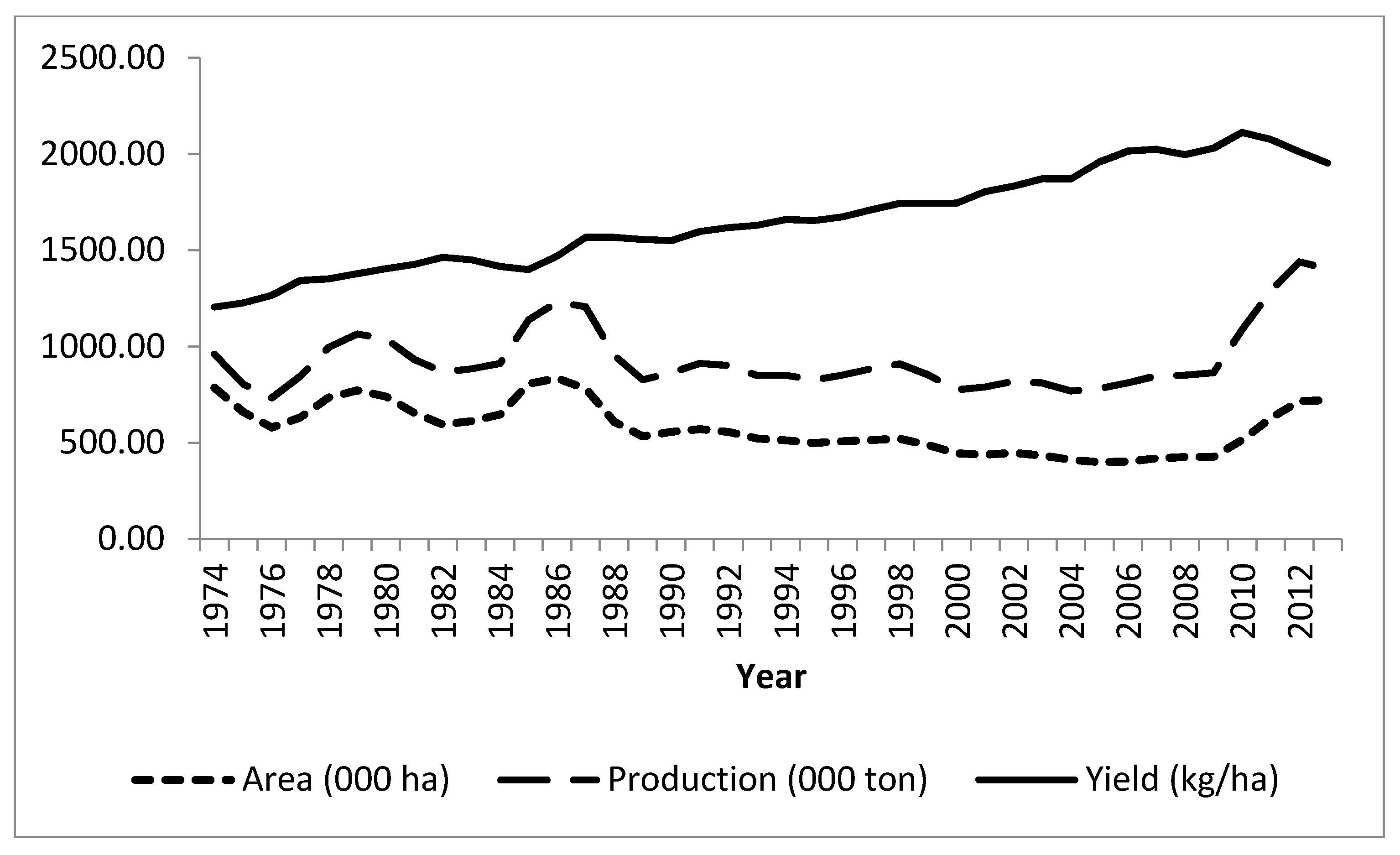

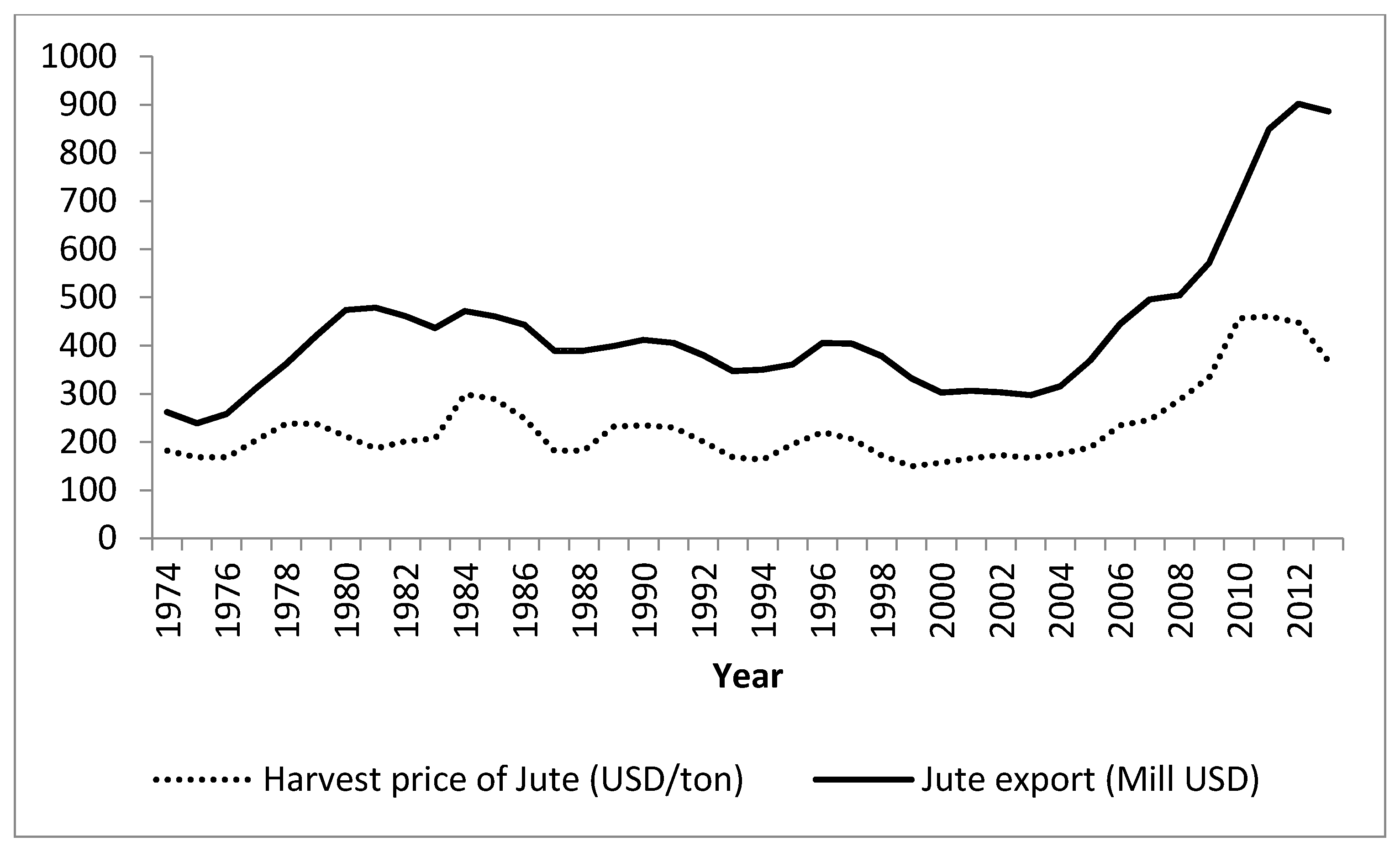

3.1. Trends in the Jute Sector over the Past Four Decades (1973–2013)

3.2. Competitiveness of Jute

3.3. Financial Profitability of Jute

3.4. Production Structure and Drivers of Jute Productivity

3.5. Drivers of Technical Inefficiency in Jute Production

4. Discussion and Policy Implications

Acknowledgments

Author Contributions

Conflicts of Interest

References

- Basu, G.; Roy, A.N. Blending of Jute with Different Natural Fibres. J. Nat. Fibers 2008, 4, 13–29. [Google Scholar] [CrossRef]

- Kazal, M.M.H.; Rahman, S.; Alam, M.J.; Hossain, S.T. Financial and Economic Profitability of Selected Agricultural Crops in Bangladesh; NFPCSP-FAO Research Grant Report #05/11; Food Planning and Monitoring Unit, Ministry of Food, Government of Bangladesh: Dhaka, Bangladesh, 2013.

- Bangladesh Bureau of Statistics. Statistical Yearbook of Bangladesh, 2009; Bangladesh Bureau of Statistics: Dhaka, Bangladesh, 2010.

- Mackie, G. Prospects for Traditional Jute Products. J. Nat. Fibers 2005, 2, 105–110. [Google Scholar] [CrossRef]

- Gupta, D.; Sahu, P.K.; Banerjee, R. Forecasting jute production in major contributing countries in the world. J. Nat. Fibers 2009, 6, 127–137. [Google Scholar] [CrossRef]

- Muhammad, A. Closure of Adamjee Jute Mills: Ominous Sign. Econom. Political Wkly. 2002, 37, 3895–3897. [Google Scholar]

- Ministry of Textiles and Jute. Draft National Jute Policy 2014 (in Bangla); Ministry of Textiles and Jute, Government of Bangladesh: Dhaka, Bangladesh, 2015. Available online: https://www.bangladeshtradeportal.gov.bd/index.php?r=site/display&id=211 (accessed on 29 March 2017).

- Rahman, S. Whether crop diversification is a desired strategy for agricultural growth in Bangladesh? Food Policy 2009, 34, 340–349. [Google Scholar] [CrossRef]

- Planning Commission. The Fifth Five-Year Plan (1997–2002); Ministry of Planning, Government of Bangladesh: Dhaka, Bangladesh, 1998.

- Planning Commission. The Sixth Five-Year Plan (2011–2015); Ministry of Planning, Government of Bangladesh: Dhaka, Bangladesh, 2011.

- International Monitory Fund. Bangladesh Poverty Reduction Strategy Paper; IMF Country Report No. 04/410; International Monitory Fund: Washington, DC, USA, 2005. [Google Scholar]

- Rahman, S. Six decades of agricultural land use change in Bangladesh: Effects on crop diversity, productivity, food availability and the environment, 1948–2006. Singap. J. Trop. Geogr. 2010, 31, 254–269. [Google Scholar] [CrossRef]

- Gonzales, L.A.; Kasryno, F.; Perez, N.D.; Rosegrant, M.W. Economic Incentives and Comparative Advantage in Indonesian Food Crop Production; Research Report 93; International Food Policy Research Institute: Washington, DC, USA, 1993. [Google Scholar]

- Rahman, S.; Kazal, M.M.H.; Begum, I.A.; Alam, M.J. Competitiveness, Profitability, Input Demand and Output Supply of Maize Production in Bangladesh. Agriculture 2016, 6, 21. [Google Scholar] [CrossRef]

- Rashid, M.A.; Hassan, M.K.; Harun-ur-Rashid, A.K.M. Domestic and International Competitiveness of Production of Selected Crops in Bangladesh; NFPCSP-FAO Research Grant Report CF #01/08; Food Planning and Monitoring Unit, Ministry of Food, Govt. of Bangladesh: Dhaka, Bangladesh, 2009.

- Khan, N.P. Comparative advantage of wheat production in Pakistan and its policy implications. Pak. J. Agric. Econom. 2001, 4, 17–29. [Google Scholar]

- Chaudhry, M.G.; Kayani, N.N. Implicit Taxation of Pakistan’s Agriculture: An Analysis of the Commodity and Input Prices. Pak. Dev. Rev. 1991, 30, 225–242. [Google Scholar]

- Appleyard, D.R. Report on Comparative Advantage; Agricultural Price Commission Series # 61; Agricultural Price Commission: Islamabad, Pakistan, 1987.

- Monke, E.A.; Pearson, S.R. The Policy Analysis Matrix for Agricultural Development; Cornell University Press: Ithaca, NY, USA, 1989. [Google Scholar]

- Molla, M.M.U.; Sabur, S.A.; Begum, I.A. Financial and economic profitability of jute in Bangladesh: A comparative assessment. J. Agric. Nat. Resour. Sci. 2015, 2, 295–303. [Google Scholar]

- Shahabuddin, Q.; Dorosh, P. Comparative Advantage in Bangladesh Crop Production, MSSD Discussion Paper No. 47; International Food Policy Research Institute: Washington, DC, USA, 2002. [Google Scholar]

- Reddy, A.A.; Bantilan, M.C.S. Competitiveness and technical efficiency: Determinants in the groundnut oil sector in India. Food Policy 2012, 37, 255–263. [Google Scholar] [CrossRef]

- Rahman, S.; Rahman, M.S. Exploring the potential and performance of maize production in Bangladesh. Int. J. Agric. Manag. 2014, 3, 99–106. [Google Scholar]

- Aigner, D.J.; Lovell, C.A.K.; Schmidt, P. Formulation and estimation of stochastic frontier production function models. J. Econom. 1977, 6, 21–37. [Google Scholar] [CrossRef]

- Battese, G.; Coelli, T. A model for technical inefficiency effects in a stochastic frontier production function for panel data. Empir. Econom. 1995, 20, 325–332. [Google Scholar] [CrossRef]

- Bangladesh Bureau of Statistics. Statistical Yearbook of Bangladesh, 1975 through 2013; Various Issues (1975–2013); Bangladesh Bureau of Statistics: Dhaka, Bangladesh, 2014.

- Bangladesh Bank. Economic Trends, Monthly, December 2013; Bangladesh Bank: Dhaka, Bangladesh, 2013. [Google Scholar]

- StataCorp. STATA Version 8; Stata Press Publications: College Station, TX, USA, 2003. [Google Scholar]

- Rahman, S.; Hasan, M.K. Impact of environmental production conditions on productivity and efficiency: A case study of wheat farmers in Bangladesh. J. Environ. Manag. 2008, 88, 1495–1504. [Google Scholar] [CrossRef] [PubMed]

- Coelli, T.J. Estimators and hypothesis tests for a stochastic frontier function: A Monte-Carlo analysis. J. Prod. Anal. 1995, 6, 247–268. [Google Scholar] [CrossRef]

- Coelli, T.; Rahman, S.; Thirtle, C. Technical, allocative, cost and scale efficiencies in Bangladesh rice cultivation: A non-parametric approach. J. Agric. Econom. 2002, 53, 607–626. [Google Scholar] [CrossRef]

- Bravo-Ureta, B.E.; Solis, D.; Lopez, V.H.M.; Maripani, J.F.; Thiam, A.; Rivas, T. Technical efficiency in farming: A meta regression analysis. J. Prod. Anal. 2007, 27, 57–72. [Google Scholar] [CrossRef]

- Rahman, S.; Rahman, M.M. Impact of land fragmentation and resource ownership on productivity and efficiency: The case of rice producers in Bangladesh. Land Use Policy 2008, 26, 95–103. [Google Scholar] [CrossRef]

- Food and Agricultural Organisation (FAO). FAOSTAT Database; Food and Agricultural Organisation of the United Nations: Rome, Italy, 2017; Available online: http://www.fao.org/faostat/en/#data/TP (accessed on 28 March 2017).

- Bangladesh Jute Research Institute (BJRI). Bangladesh Jute Research Institute Official Website. Undated. Available online: http://www.bjri.gov.bd/bjri_english/ (accessed on 22 October 2017).

- Bangladesh Bureau of Statistics. Statistical Yearbook of Bangladesh, 2014; Bangladesh Bureau of Statistics: Dhaka, Bangladesh, 2016.

{kind=link}

{kind=link}

| Items | Revenue | Costs | Profit | |

|---|---|---|---|---|

| Tradable Inputs | Domestic Factors | |||

| Private prices | A | B | C | D |

| Social prices | E | F | G | H |

| Variables | Units | First 31 Years | Latter 10 Years | Total Period |

|---|---|---|---|---|

| 1973–2003 | 2004–2013 | 1973–2013 | ||

| Average Values | ||||

| Area cultivated | ‘000 ha | 599.76 | 506.55 | 576.46 |

| Total production | ‘000 mt | 910.21 | 1015.0 | 936.41 |

| Productivity | t ha−1 | 1.54 | 2.01 | 1.66 |

| Harvest price | USD | 201.59 | 320.12 | 231.23 |

| Value of export | million USD | 374.67 | 604.81 | 432.21 |

| Average Annual Compound Growth Rates | ||||

| Area cultivated | % | −1.8 *** | 7.3 *** | −1.1 *** |

| Total production | % | −0.5 * | 7.7 *** | 0.2 |

| Productivity | % | 1.3 *** | 0.5 | 1.3 *** |

| Harvest price | % | −0.7 * | 11.0 *** | 1.1 *** |

| Value of export | % | −0.1 | 12.1 *** | 1.4 *** |

| Items | Kishoreganj | Faridpur |

|---|---|---|

| Revenue at social prices (BDT) | 35,457.31 | 35,457.31 |

| Tradable inputs at social prices (BDT) | 3223.99 | 3683.33 |

| Domestic factors at social prices (BDT) | 24,583.73 | 32,389.88 |

| Profits at social prices (BDT) | 7649.60 | −615.90 |

| Nominal Protection Coefficient on Output (NPCO) | 0.80 | 1.26 |

| Nominal Protection Coefficient on Input (NPCI) | 0.45 | 0.43 |

| Effective Protection Coefficient (EPC) | 0.84 | 1.35 |

| Region | Unit | Kishoreganj (Traditional Jute) | Faridpur (White Jute) |

|---|---|---|---|

| Average yield/productivity | kg ha−1 | 2340.00 | 2500.00 |

| Sale price | BDT mt−1 | 28,433.33 | 44,666.67 |

| Human labor | BDT ha−1 | 30,583.90 | 50,899.50 |

| Machinery Inputs | BDT ha−1 | 1763.40 | 4864.70 |

| Material Inputs | BDT ha−1 | 14,602.90 | 7047.90 |

| Total variable cost (TVC) | BDT ha−1 | 46,950.22 | 62,812.10 |

| Interest on operating capital | BDT ha−1 | 1173.80 | 1570.30 |

| Land use cost | BDT ha−1 | 19,899.00 | 32,307.00 |

| Total fixed cost (TFC) | BDT ha−1 | 21,072.70 | 33,877.30 |

| Total cost (TC) | BDT ha−1 | 68,022.97 | 96,689.40 |

| Gross return (GR) | BDT ha−1 | 79,811.37 | 119,491.00 |

| Gross margin (GM = GR − TVC) | BDT ha−1 | 32,861.18 | 56,678.90 |

| Net return (NR = GR − TC) | BDT ha−1 | 11,788.47 | 22,801.60 |

| Undiscounted BCR | 1.17 | 1.24 |

| Hypothesis | Critical Value of χ2 (v, 0.95) | LR Statistic/z Statistic | Decision |

|---|---|---|---|

| Choice of the functional form (H0: β11 = β22 = … = β67 = 0) | 41.37 | 280.98 *** | Translog function is appropriate |

| Frontier test H0: M3T = 0 (i.e., no inefficiency component) | - | 25.26 *** | Frontier not OLS |

| Presence of inefficiency (H0: γ = 0) | 3.84 | 93.22 *** | Inefficiencies are present |

| No effect of socio-economic variables on inefficiency (H0: δ1 = δ2 = … = δ6 = 0) | 12.59 | 29.74 *** | Have effects of socio-economic on inefficiency |

| Constant returns to scale in production (H0: α1 + α2 + … + α5 = 1) | 3.84 | 42.34 *** | Decreasing returns to scale in production |

| Variables | Parameters | Coefficient | t-Ratio |

|---|---|---|---|

| Production Function | |||

| Constant | α0 | 6.5036 *** | 108.39 |

| ln Labour | α1 | 0.1116 ** | 2.06 |

| ln Fertiliser | α2 | 0.0053 | 0.16 |

| ln Organic manure | α3 | −0.0019 | −0.23 |

| ln Mechanical power | α4 | 0.0467 | 1.11 |

| ln Irrigation | α5 | 0.0679 *** | 11.21 |

| ln Seed | α6 | −0.0476 | −1.17 |

| ln Land | α7 | 0.6901 *** | 11.13 |

| 0.5 × (ln Labour)2 | β11 | 0.3490 *** | 4.75 |

| 0.5 × (ln Fertiliser)2 | β22 | 0.0678 | 1.25 |

| 0.5 × (ln Organic manure)2 | β33 | 0.0050 | 1.26 |

| 0.5 × (ln Mechanical power)2 | β44 | 0.0601 | 1.42 |

| 0.5 × (ln Irrigation)2 | β55 | 0.0358 *** | 5.25 |

| 0.5 × (ln Seed)2 | β66 | −0.0448 *** | −3.64 |

| 0.5 × (ln Land)2 | β77 | 0.6214 *** | 5.75 |

| ln Labour × ln Fertiliser | β12 | −0.2249 *** | −3.34 |

| ln Labour × ln Organic manure | β13 | −0.1036 *** | −2.90 |

| ln Labour × ln Mechanical power | β14 | −0.0326 *** | −3.95 |

| ln Labour × ln Irrigation | β15 | 0.1051 | 1.02 |

| ln Labour × ln Seed | β16 | −0.0399 ** | −2.02 |

| ln Labour × ln Land | β17 | −0.1796 | −1.51 |

| ln Fertiliser × ln Organic manure | β23 | 0.1216 ** | 1.96 |

| ln Fertiliser × ln Mechanical power | β24 | −0.0042 | −0.34 |

| ln Fertiliser × ln Irrigation | β25 | −0.0338 | −0.64 |

| ln Fertiliser × ln Seed | β26 | −0.0360 *** | −2.69 |

| ln Fertiliser × ln Land | β27 | 0.1222 | 1.02 |

| ln Organic manure × ln Mechanical power | β34 | 0.0103 | 1.01 |

| ln Organic manure × ln Irrigation | β35 | 0.2429 *** | 3.59 |

| ln Organic manure × ln Seed | β36 | 0.0214 ** | 2.36 |

| ln Organic manure × ln Land | β37 | −0.2871 *** | −3.40 |

| ln Mechanical power × ln Irrigation | β45 | 0.0075 | 0.33 |

| ln Mechanical power × ln Seed | β46 | −0.0267 | −1.20 |

| ln Mechanical power × ln Land | β47 | −0.2800 *** | −2.69 |

| ln Irrigation × ln Seed | β56 | −0.0017 | −0.77 |

| ln Irrigation × ln Land | β57 | 0.0413 | 1.32 |

| ln Seed × ln Land | β67 | −0.0063 | −0.38 |

| Model Diagnostics | |||

| σ2 = σu2 + σv2 | σ2 | 0.23 | 72.86 *** |

| γ = σu2/(σu2 + σv2) | γ | 0.99 | 93.22 *** |

| Log likelihood | 56.81 | ||

| Inefficiency Effects Function | |||

| Constant | δ0 | −0.6524 ** | −2.02 |

| Marginal farmer | δ1 | 0.2152 * | 1.73 |

| Subsistence pressure | δ2 | −0.0073 | −0.21 |

| Experience of the farmer | δ3 | 0.0006 | 0.13 |

| Land fragmentation | δ4 | −0.0111 | −0.42 |

| Involvement in NGOs | δ5 | 0.5771 *** | 4.63 |

| Education of the farmers | δ6 | 0.0123 | 0.91 |

| Total number of observations | 289 | ||

| Items | Proportion of Farmers |

|---|---|

| Efficiency Levels | |

| Up to 60% | 20.07 |

| 61–70% | 19.03 |

| 71–80% | 21.11 |

| 81–90% | 15.57 |

| 91% and above | 24.22 |

| Efficiency Measures | |

| Mean efficiency score | 0.75 |

| Standard deviation | 0.17 |

| Minimum | 0.09 |

| Maximum | 0.99 |

| Mean Efficiency by Farm Size Categories | |

| Marginal | 0.71 |

| Small | 0.77 |

| Medium/large | 0.76 |

| F-test for difference by farm size categories | 2.80 * |

| Mean Efficiency by NGO Membership | |

| Not involved in NGO | 0.82 |

| Members of NGO | 0.70 |

| t-test for mean difference by NGO involvement | 6.10 *** |

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Rahman, S.; Kazal, M.M.H.; Begum, I.A.; Alam, M.J. Exploring the Future Potential of Jute in Bangladesh. Agriculture 2017, 7, 96. https://doi.org/10.3390/agriculture7120096

Rahman S, Kazal MMH, Begum IA, Alam MJ. Exploring the Future Potential of Jute in Bangladesh. Agriculture. 2017; 7(12):96. https://doi.org/10.3390/agriculture7120096

Chicago/Turabian StyleRahman, Sanzidur, Mohammad Mizanul Haque Kazal, Ismat Ara Begum, and Mohammad Jahangir Alam. 2017. "Exploring the Future Potential of Jute in Bangladesh" Agriculture 7, no. 12: 96. https://doi.org/10.3390/agriculture7120096

APA StyleRahman, S., Kazal, M. M. H., Begum, I. A., & Alam, M. J. (2017). Exploring the Future Potential of Jute in Bangladesh. Agriculture, 7(12), 96. https://doi.org/10.3390/agriculture7120096