1. Introduction

Micro, small, and medium enterprises (MSMEs) are not only the backbone of the Indonesian economy but also reflect the social dynamics and financial resilience of millions of small business owners [

1,

2]. An interesting phenomenon is how agro-industrial MSMEs in East Java experience a cycle of seasonal income in one period and financial droughts in another because of seasonal income fluctuations. For example, coffee farmers in Banyuwangi enjoy a surge in income during the harvest season but face difficulties in maintaining business continuity when production declines [

3]. Similarly, seafood processors in Lamongan often experience surpluses during the fishing season but face drastic drops in income during the off-season [

4]. These phenomena show how unstable income patterns can lead to suboptimal financial decisions, such as reliance on short-term debt or failure, to set aside reserve funds. According to a report by the authors of [

5], they faced challenges such as high interest rates, a lack of collateral, low financial literacy, and complex application processes, which often resulted in loan rejection. A survey reported in [

6] in collaboration with NielsenIQ Indonesia in 2024 revealed that only 46% of MSMEs in Indonesia will fully separate business and personal finances. This lack of separation can affect cash flow and business sustainability. In addition, a report in [

7] showed that two-thirds of small business owners in Indonesia had not accessed credit or loans in the past 12 months, with 62% stating that they did not need credit. This reflects the tendency to rely on self-funding, which can increase the risk of financial distress during periods of low revenue. This instability creates a major challenge for business sustainability, leaving many MSME players trapped in a cycle of seasonal incomes without effective financial awareness (FA) or financial capabilities (FCs).

MSME owners who lack financial literacy tend to neglect aspects such as product diversification and investment in technology to increase productivity, which contributes to the low sustainability of their businesses [

8,

9,

10]. In addition, ref. [

11] found that seasonal income instability increases the risk of financial behaviors, such as risky borrowing behavior (RBB) or risky paying behavior (RPB). In the context of the agro-industry in East Java, this creates additional pressure on business owners’ ability to achieve long-term financial goals (FGs). Research has extensively discussed the relationships between financial literacy, FC, and financial behavior. For example, ref. [

12] asserted that financial literacy is a key factor in helping individuals manage irregular incomes and reduce the risk of financial mistakes. According to [

13], good financial literacy can improve business owners’ ability to manage cash flows, although seasonal impacts remain a major challenge.

However, most of these studies are still general and do not highlight the complexity of financial behavior influenced by seasonal income in the agro-industrial sector. Empirical studies that specifically explore the relationship between financial literacy, risky financial behavior, and FG in the context of agro-industrial MSMEs are limited [

11,

14]. In addition, few studies have integrated concepts such as expected future financial security (EFFS) and current money management stress (CMMS) into financial behavior models. Research in [

15] shows that subjective financial literacy significantly affects financial self-efficacy, which has an impact on RPB, whereas objective financial literacy and the effect of financial self-efficacy on RBB tend to be insignificant. On the other hand, Ardini et al. [

16] revealed that digital financial literacy plays an important role in improving financial skills and FG, especially through the mediation of financial skills. Both studies highlight the importance of financial literacy in promoting sound financial behavior; however, a research gap remains in exploring the impact of seasonal income fluctuations on risky financial behavior, especially in the agro-industrial sector, which faces unique challenges in financial stability.

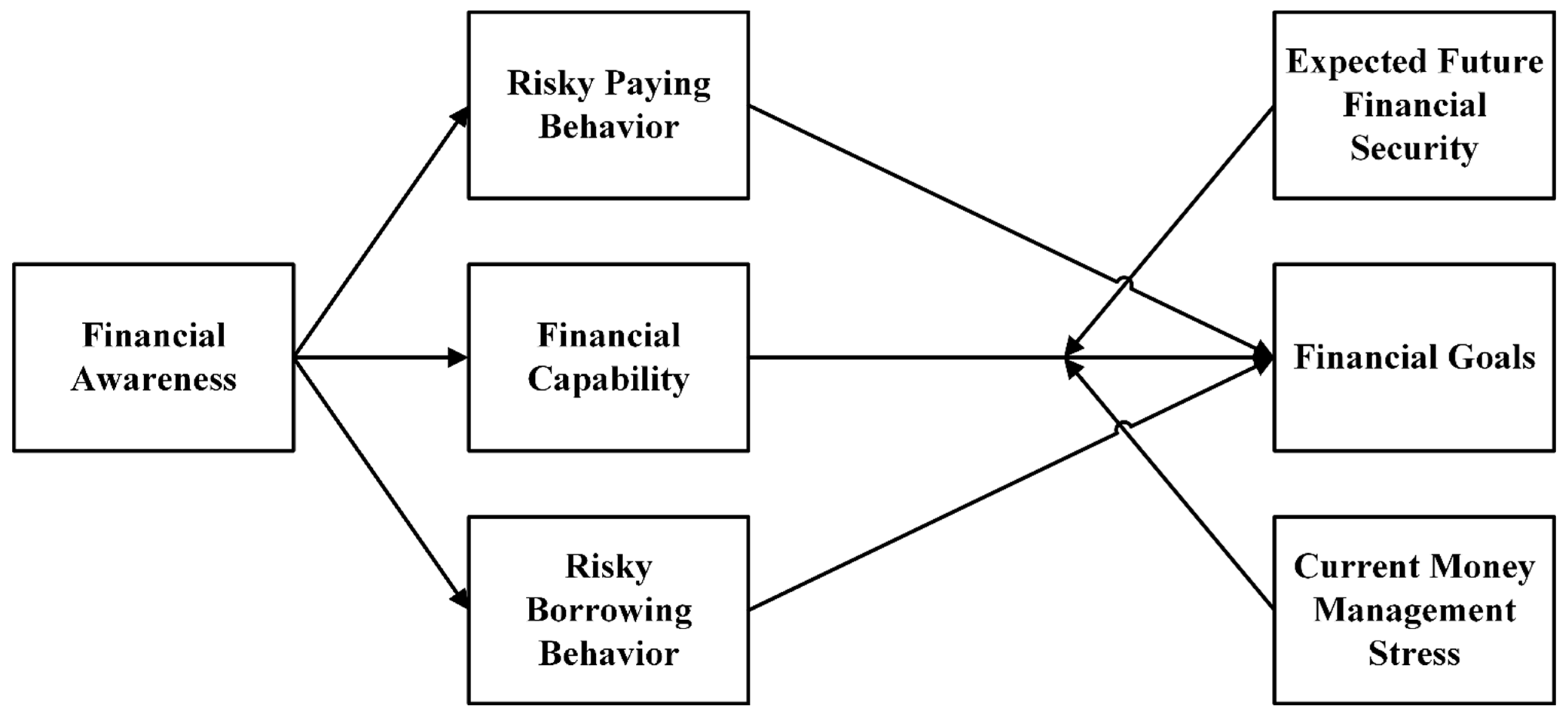

This study aims to bridge this gap by examining the interaction between FA, FC, risk, stress, and FG in the context of the seasonal income of agro-industrial MSMEs in East Java. Although financial literacy has been identified as an important factor in business management, there is a research gap in understanding how it interacts with variables, such as FC and risky financial behavior. Furthermore, most previous studies have not considered the psychological (financial) stress that business owners face due to cash flow instability. Recognizing and addressing the psychological aspects of financial stress are crucial for developing comprehensive support systems for business owners and ensuring the long-term resilience of MSMEs. This gap provides an opportunity for further exploring how FA can influence financial goals through the mediation of variables, such as FC, financial risk, and the moderation of future financial security. This approach is expected to provide a new and comprehensive model for the financial management of MSMEs, particularly in the agro-industrial context. The roles of EFFS and CMMS as moderating variables provide a new dimension in the relationship between FC and FG. EFFS reflects the extent to which business owners feel confident of their future financial stability, which may motivate them to set and achieve a more ambitious FG despite being faced with seasonal income. Meanwhile, the CMMS reflects the psychological pressure business owners experience in managing their daily cash flow and debt, which may hinder their focus on long-term FG. These two variables have the potential to strengthen or weaken the effect of FC on FG depending on how business owners manage future expectations and cope with current financial stress.

This study uncovers the complex mechanisms of these two moderators in guiding agro-industrial MSME owners’ financial decisions, particularly amid seasonal income uncertainty. This study uses the Behavioral Finance Theory (BFT) as a grand theory. This theory provides a relevant framework for understanding how psychological factors such as stress and expectations influence financial decision-making. The BFT enables an in-depth exploration of risky financial behaviors and FG, which are influenced by internal (FC) and external (seasonal income) factors. By adopting this theory, this study sheds light on the complex relationships between financial literacy, psychological factors, and financial outcomes relevant to the FG of agro-industrial MSME owners.

In

Section 2, this study explains the theoretical basis used in building the research model, accompanied by an explanation of each variable and the results of previous studies.

Section 3 presents the approach, measurement details, and data analysis techniques. In

Section 4, the research results are presented based on the results of statistical calculations, which are quite detailed and thorough, and in-depth discussion. In

Section 5, the conclusions and research implications are presented.

4. Result and Discussion

4.1. Characteristics Respondents

Table 2 presents the respondents’ demographic and business characteristics. The respondents, totaling 287 MSME owners from various regions, represented a diverse group with varying backgrounds in terms of gender, age, education, business tenure, and industry. The data provide insights into the key attributes that influence financial behavior and decision-making processes.

As shown in

Table 2, the majority of respondents were male, accounting for 58.54% of the total, whereas females represented 41.46%. Age distribution highlights that most respondents fall into the 30–40 year age range, constituting 31.71%, followed by those aged 41–50 years at 27.53%. The educational background showed a wide spectrum, with the highest proportion holding a bachelor’s degree (30.66%), indicating a relatively high level of formal education among the respondents. Business tenure reveals that 34.15% of respondents have been in business for 5–10 years, demonstrating a stable experience in managing enterprises. The types of business reflected the regional focus on agriculture, fisheries, and agro-industrial activities, with the highest representation from coffee and cocoa farming (20.21%). Technology adoption also played a crucial role, with 67.25% of the respondents utilizing financial technology, underscoring the growing reliance on digital tools for business operations. Access to credit varies, with 41.46% relying on bank loans and a smaller proportion relying on fintech lending or cooperatives. Financial literacy levels varied significantly, with 41.11% of the respondents categorized as having a moderate level of literacy.

4.2. Descriptive Statistics

Table 3 summarizes the descriptive statistics of the variables used in this study, including their mean and standard deviation ranges. The variables reflect the key aspects of financial behavior and outcomes among MSME owners.

FA demonstrated a mean range of 5.307 to 5.951, with a standard deviation between 1.077 and 1.450, indicating relatively high awareness levels, but some variation among respondents. FC has a mean range of 5.686–5.983 and a standard deviation of 1.064–1.382, showing the respondents’ ability to manage their financial obligations effectively, albeit with slight variability. The FG reflects a mean range of 5.700 to 5.937, with a standard deviation of 1.060 to 1.188, highlighting the importance of goal-oriented financial planning among the respondents. The RPB and RBB showed contrasting trends. While RPB has a high mean range of 5.878–5.885 with relatively low variability (0.975–1.276), RBB exhibits a lower mean range of 4.244–4.561 and a much higher standard deviation (2.108–2.189), indicating a significant inconsistency in borrowing behavior. The EFFS showed a mean range of 5.369–5.920 and a standard deviation of 1.031–1.263, reflecting a strong sense of financial stability and future planning among most respondents. In contrast, CMMS had a mean range of 4.686–5.157 and a standard deviation of 1.619–1.960, indicating moderate stress levels with some variation across the sample.

4.3. Common Method Bias (CMB)

Table 4 presents the inner VIF values for all structural paths in the model. The results show that all VIF values ranged between 1.000 and 1.760, which is well below the threshold of 3.3 recommended in [

52]. For example, the paths from CMMS to FG and from RPB to FG exhibited VIF values of 1.760 and 1.221, respectively, indicating low multicollinearity and a negligible common method bias. Similarly, the interaction terms, such as EFFS × FC to FG and CMMS × FC to FG, showed VIF values of 1.231 and 1.351, respectively, further confirming that the model does not suffer from CMB issues.

These results validate the robustness of the measurement model and ensure that the relationships between the constructs are not significantly influenced by the common method variance. Low VIF values strengthen the credibility of the findings and support the conclusion that observed relationships are likely to reflect the actual dynamics within the data.

4.4. Measurement Model

Table 5 presents the factor loadings, composite reliability (CR), and average variance extracted (AVE) for the constructs measured. These metrics are crucial for assessing the reliability and validity of a measurement model. Factor loadings represent the correlation between each indicator and its underlying constructs. CR evaluates the internal consistency of the construct, and AVE indicates the proportion of variance captured by the construct relative to the variance due to measurement error.

Most items in the table exhibit factor loadings above the commonly accepted threshold of 0.6 [

53], indicating that the indicators adequately represent their respective constructs. Constructs such as CMMS and RBB showed particularly strong factor loadings, with values ranging from 0.829 to 0.942. These high loadings reflect strong relationships between the items and their constructs, thus enhancing the overall reliability of the model. The CR values for these constructs were also above the threshold of 0.7 [

50], thus ensuring internal consistency. However, some items showed factor loadings below 0.6, such as FC1 (0.532) and FC2 (0.595) under the financial capability (FC) construct. Items with factor loadings below 0.6 contribute less to the construct and may reduce the overall model fit. According to the measurement theory, removing such items can improve the construct’s reliability and validity, particularly if their exclusion raises the CR and AVE above the recommended thresholds. For example, eliminating FC1 and FC2 could potentially strengthen the representation of financial capability in the model by focusing on stronger indicators, such as FC3 and FC4. Similarly, for the FA construct, FA3 showed a factor loading of 0.593, which is slightly below the threshold. Although this value is close to acceptable, its inclusion may slightly weaken the construct’s overall validity. Removing this item could enhance AVE and ensure that the construct better captures the essence of financial awareness. The EFFS4 was also deleted to enhance the AVE of the EFFS constructs.

Table 6 presents the Fornell–Larcker criterion results used to assess discriminant validity in the measurement model [

40]. Discriminant validity ensures that each construct in the model is distinct from others. This criterion is satisfied if the square root of the AVE for each construct (diagonal values) is greater than the correlation between that construct and all other constructs (off-diagonal values) [

45].

All constructs in the model satisfy the Fornell–Larcker criterion. For instance, the square root of the AVE for RBB (0.926) was significantly higher than its correlation with other constructs, such as FG (0.062) and EFFS (0.183). Similarly, RPB has a square root of AVE of 0.806, which is higher than its correlation with constructs such as FA (0.282) and FC (0.287).

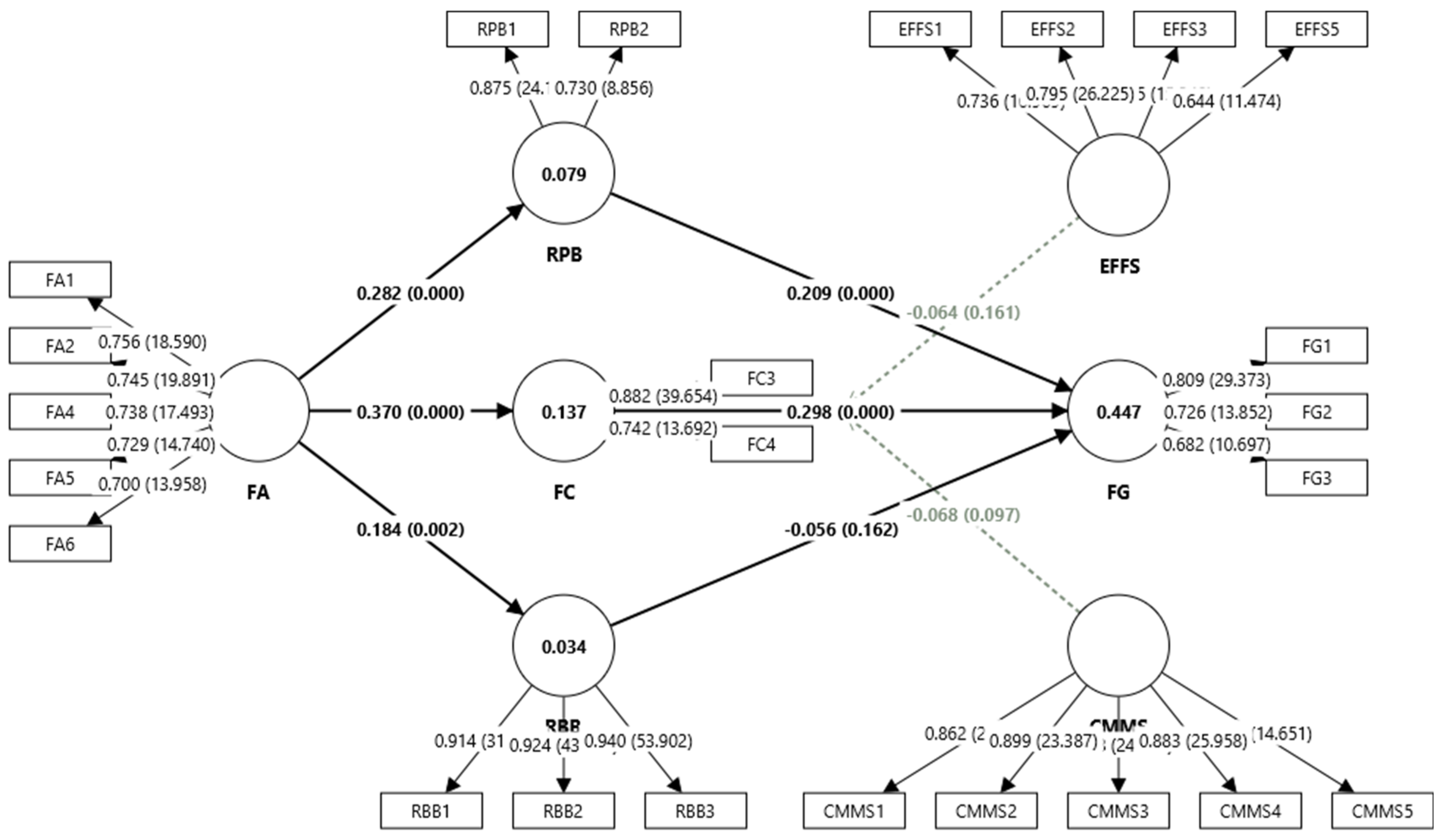

The final model was refined by removing low-loading items (e.g., FA3, FC1, and FC2) to improve construct validity and overall model fit (see

Figure 2). The retained items provided stronger and more reliable measurements of their respective constructs, enhancing the clarity and precision of the relationships.

4.5. Structural Model

Table 7 presents the model fit indicators and R-squared values for the structural model, providing an understanding of its overall quality and explanatory power. Model fit indicators, such as SRMR, d_ULS, d_G, chi-square, and NFI, assess the extent to which the estimated model aligns with the observed data, whereas R-square and Q

2 evaluate the variance explained by the constructs.

The Standardized Root Mean Square Residual (SRMR) measures the average discrepancy between the observed and predicted correlations. An SRMR value below 0.08 indicates a good model fit, and the saturated model achieves a value of 0.082, which is close to the threshold, whereas the estimated model shows a slightly higher value of 0.138, suggesting room for improvement. The d_ULS and d_G indicators assess the discrepancy between implied and observed covariance matrices. The saturated model has lower values (2.020 and 0.501, respectively) than the estimated model (5.677 and 0.647, respectively), indicating that the saturated model fits better with the observed data. The chi-square value for the saturated model was 882.478, which increased to 1040.399 in the estimated model. While higher chi-square values typically indicate poorer fit, they should be interpreted cautiously in larger sample sizes, as chi-square is sensitive to the sample size. The normed fit index (NFI), which compares the fit of the proposed model to a null model, was 0.730 for the saturated model and 0.681 for the estimated model. Both values were below the conventional threshold of 0.9, indicating a moderate fit. The R-squared values indicate the proportion of the variance explained by the independent variables for each construct. FC has an R-square of 0.137 (adjusted 0.134), suggesting that the predictors explain 13.7% of the variance in FC. FG exhibited a higher R-squared of 0.447 (adjusted 0.433), indicating that 44.7% of its variance was explained by the predictors, demonstrating the strongest explanatory power in the model. The RBB had a low R-squared value of 0.034 (adjusted 0.030), indicating minimal explanatory power. Similarly, the RPB showed an R-square of 0.079 (adjusted 0.076), reflecting the limited variance explained. A Q2 value of 0.575 indicated the model’s predictive relevance for endogenous constructs. A Q2 value above 0 confirms the model’s ability to predict and implies its robustness in explaining financial behaviors and goals within the context of the study.

Figure 3 illustrates the bootstrapping results of the final structural model, which provides statistical significance and reliability for the hypothesized relationships and factor loadings. Bootstrapping is a resampling technique that generates robust standard errors and t-values to test the significance of the path coefficients and indicator loadings.

The path analysis results in

Table 8 provide a detailed understanding of the relationships between the variables in the structural model and examine their significance and impact.

FA demonstrated a strong and significant direct relationship with FC, as indicated by a path coefficient (O) of 0.370 and a t-statistic of 5.845 (p < 0.000). This highlights the critical role of the FA in shaping individuals’ ability to effectively manage their financial obligations, reflecting a clear connection between awareness and capability. FA also significantly influenced RBB and RPB, with path coefficients of 0.184 (t = 2.904, p = 0.002) and 0.282 (t = 4.011, p < 0.000), respectively. These results suggest that individuals with higher financial awareness are more likely to proactively manage their borrowing and payment behaviors, although RBB’s influence of RBB on FG is not statistically significant (O = −0.056, p = 0.162). This lack of significance indicates that borrowing behavior, while being affected by awareness, does not directly impact FG achievement.

As an intermediary construct, FC had a substantial and significant positive effect on FG (O = 0.298, t = 4.116, p < 0.000). This underscores the importance of financial capability in facilitating long-term goal-setting and achievement, aligning with the model’s focus on the practical application of financial skills. Moreover, the indirect path from FA to FG through FC was also significant (O = 0.110, t = 3.155, p = 0.001), reinforcing the cascading effect of awareness through capability on goal attainment. The influence of RPB on FG is significant and positive (O = 0.209, t = 3.432, p < 0.000), demonstrating that effective payment behavior contributes to the realization of financial goals. Conversely, the moderating effects of EFFS and CMMS on the FC-to-FG relationship were not significant, with path coefficients of −0.064 (p = 0.161) and −0.068 (p = 0.097), respectively. These results suggest that while psychological factors such as future security and financial stress are important, their interactions with capability may not strongly influence the direct pathway to goal attainment in this study. Interestingly, the indirect paths involving FA, RBB, and FG (O = −0.010, p = 0.187) are not significant, indicating that risky borrowing behavior does not mediate the relationship between financial awareness and goal attainment. By contrast, the indirect path through RPB (O = 0.059, t = 2.208, p = 0.014) is significant, highlighting that effective payment behavior serves as a critical mediator for FA to positively impact FG.

4.6. Discussion

The findings of this study underscore the significant role of FA and FC in shaping the financial behaviors and goals of agro-industrial MSME owners in East Java, a group highly vulnerable to seasonal income fluctuations. As observed in previous studies [

1,

2,

54], MSMEs constitute the foundation of the Indonesian economy. However, many of these enterprises are ensnared in a cyclical pattern of financial instability due to irregular income streams. This study adds to the body of knowledge by illustrating how FA influences FC and risky financial behaviors such as RBB and RPB and ultimately affects FG attainment. The path analysis results revealed that FA directly affected FC with a path coefficient of 0.370 (

p < 0.000). This finding aligns with previous research in [

25], which emphasizes the critical role of FA in equipping business owners with the knowledge and skills needed to manage finances effectively. Agro-industrial MSMEs benefit from high FA because it enables them to allocate resources efficiently during periods of peak income while preparing for challenges during the off-season. Similarly, ref. [

26] notes that FA is a fundamental component of financial literacy, empowering MSMEs to make better decisions about budgeting, debt management, and investment.

The significant relationship between FA and RPB (path coefficient = 0.282,

p < 0.000) and RBB (path coefficient = 0.184,

p = 0.002) further validates the critical influence of financial awareness on reducing risky financial behaviors. This finding is consistent with [

9], which showed that seasonal income instability exacerbates the likelihood of risky financial behavior among MSMEs. For instance, the implementation of the final tax for MSMEs at 0.5% turnover (PP 23/2018) did not consider seasonal income fluctuations. MSMEs with unstable incomes still have to pay taxes based on turnover, even though they experience periods of low income. Moreover, FC emerged as a pivotal mediator between FA and FG with a significant indirect effect (path coefficient = 0.110,

p = 0.001). This result corroborates the findings of [

16], which noted that FC significantly enhances the ability to achieve financial goals by fostering disciplined financial management. Conversely, low FC often results in suboptimal financial decisions such as failing to separate personal and business finances, as noted in the [

6] survey. RPB also significantly influences FG (path coefficient = 0.209,

p < 0.000), indicating that timely and disciplined payment practices contribute positively to achieving long-term FG. This finding aligns with that of [

10], which emphasized that reducing risky financial behaviors is essential for sustainable business management. However, the impact of RBB on FG was found to be insignificant (

p = 0.162), suggesting that borrowing behaviors, although influenced by FA, may not directly translate into FG achievement.

This finding is similar to the conclusions of [

15], who noted that subjective financial literacy plays a more critical role in addressing RPB than RBB does. The moderating effects of EFFS and CMMS on the FC–FG relationship were not significant, with

p-values of 0.161 and 0.097, respectively. This psychological factor is due to the government’s policy weaknesses, and the absence of insurance schemes or adequate financial protection for agro-industrial MSMEs makes them vulnerable to weather risks, natural disasters, and market price fluctuations. Without such protection, businesses are more likely to rely on informal loans with high interest rates or risky financial practices. However, previous research in [

35,

36] suggests that these variables can still shape financial behaviors indirectly, as individuals with high EFFS are more optimistic and forward-looking, whereas those with high CMMS may struggle to focus on long-term planning.

Any uncertainty in import policies that is unfavorable to agro-industrial MSMEs, such as the import of large quantities of food commodities during the local harvest season, can cause local product prices to fall. Conversely, complicated export regulations can hinder businesses from selling their products to foreign markets. This research helps develop a mitigation strategy by involving several important factors, such as FA and FC, and psychological factors, such as EFFS and CMMS, in a cohesive model to address the unique challenges faced by agro-industrial MSMEs. The application of the BFT offers a robust framework for understanding the interplay between cognitive, emotional, and external factors that influence financial behaviors and outcomes. As the focus of [

21,

22], MSME owners are subject to the cognitive biases and emotional pressures that shape their financial decisions.

5. Conclusions

This study shows that FA significantly affects FC, RBB, and RPB, highlighting its foundational role in fostering disciplined financial practices. FC emerges as a key mediator in the relationship between FA and FG, emphasizing the importance of financial literacy and capability in achieving long-term business sustainability. While RPB significantly contributes to FG, the effect of RBB on FG is insignificant, suggesting that borrowing behavior may not directly translate into financial goal achievement. Additionally, psychological factors, such as EFFS and CMMS, did not significantly moderate the relationship between FC and FG, indicating their limited direct influence.

This study has significant theoretical and practical implications for improving the financial behavior and sustainability of agro-industrial MSMEs. The findings contribute to the BFT by emphasizing the critical role of FA as a key driver of FC and its influence on risky financial behaviors and FG achievement. The inclusion of psychological variables, such as EFFS and CMMS, provides a deeper understanding of how emotional and cognitive factors shape financial decision-making. This study validates the mediating role of FC in linking FA to FG, offering a theoretical model for exploring financial resilience in businesses that face seasonal income challenges.

This study reveals the urgent need for tailored financial literacy programs that address specific issues faced by MSME owners, such as managing irregular cash flows and minimizing risky financial behavior. Moreover, stress management resources should be made available to help MSME owners cope with financial pressures, which can impair decision-making and long-term planning. Policymakers can promote sector-specific interventions, including subsidies during the off-season and incentives for technological investment to ensure income stability and business continuity. Enhancing inclusive financing mechanisms is anticipated to augment the productivity and competitiveness of MSMEs, thereby facilitating the creation of improved employment opportunities and fostering economic growth in alignment with Sustainable Development Goal (SDG) 8, particularly within the agro-industrial sector. This research has limitations in only using a quantitative approach, and it was only carried out in several cities in East Java. Further research can explore this problem using other approaches more thoroughly in every city in East Java.

,

,

{kind=link}

{kind=link}

{kind=link}