Drivers of Sustainability Credentialling in the Red Meat Value Chain—A Mixed Methods Study

Abstract

1. Introduction

2. Materials and Methods

2.1. Consultation with Australian Red Meat Processors

- What sustainability credentials are currently being provided, and to whom?

- What demands for sustainability credentials are likely to emerge in future?

- Perceived opportunities and risks associated with sustainability credentialling.

2.2. Desk-Based Research

3. Results

3.1. Consumer Value Drivers of Sustainability Credentialling

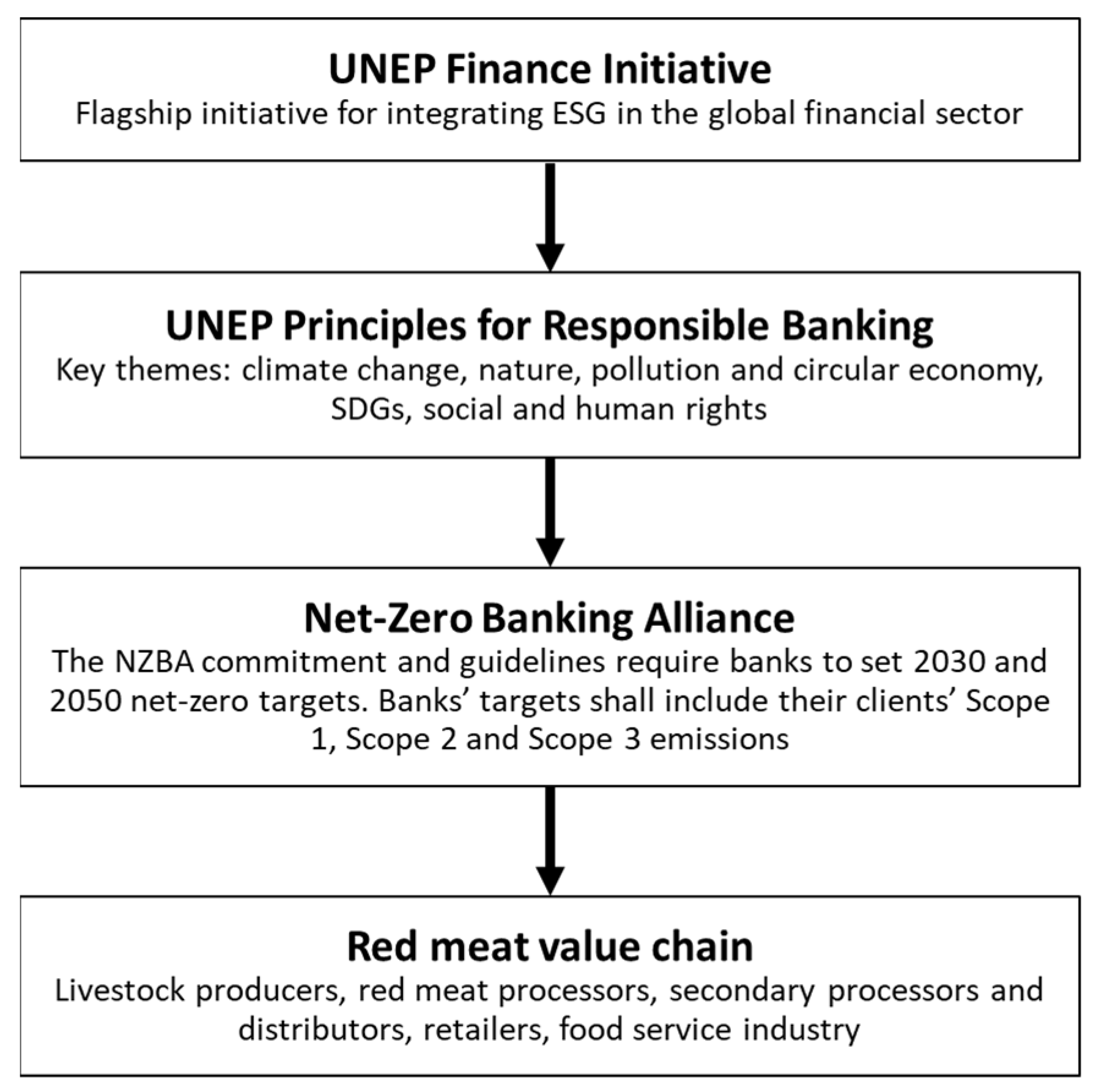

3.2. Drivers of Sustainability Credentialling beyond the Value Chain

{kind=link}

{kind=link}

| Bank | Signed NZBA | Scope |

|---|---|---|

| ANZ Group | October 2021 | NZBA and Principles for Responsible Banking |

| Commonwealth Bank of Australia | January 2022 | NZBA and Principles for Responsible Banking |

| Macquarie Group | October 2021 | Net Zero Banking Alliance |

| National Australia Bank | December 2021 | NZBA and Principles for Responsible Banking |

| Westpac Banking Corporation | July 2022 | NZBA and Principles for Responsible Banking |

| Coöperatieve Rabobank | November 2021 | Blue Finance, NZBA, and Principles for Responsible Banking |

4. Discussion

4.1. Opportunities and Risks

4.2. Implications for the Red Meat Industry

5. Conclusions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Fearne, A.; Martinez, M.G.; Dent, B. Dimensions of sustainable value chains: Implications for value chain analysis. Supply Chain Manag. Int. J. 2012, 17, 575–581. [Google Scholar] [CrossRef]

- Akyüz, Y.; Salali, H.E.; Atakan, P.; Günden, C.; Yercan, M.; Lamprinakis, L.; Kårstad, S.; Solovieva, I.; Kasperczyk, N.; Mattas, K.; et al. Case study analysis on agri-food value chain: A guideline-based approach. Sustainability 2023, 15, 6209. [Google Scholar] [CrossRef]

- Ridoutt, B.; Sanguansri, P.; Bonney, L.; Crimp, S.; Lewis, G.; Lim-Camacho, L. Climate change adaptation strategy in the food industry—Insights from product carbon and water footprints. Climate 2016, 4, 26. [Google Scholar] [CrossRef]

- Porter, M.E. Competitive Advantage: Creating and Sustaining Superior Performance; Free Press: New York, NY, USA, 1985. [Google Scholar]

- ISO 14020:2020; International Organization for Standardization. Environmental Statements and Programmes for Products—Principles and General Requirements. ISO: Geneva, Switzerland, 2020.

- ISO 17033:2019; International Organization for Standardization. Ethical Claims and Supporting Information—Principles and Requirements. ISO: Geneva, Switzerland, 2019.

- McRobert, K.; Gregg, D.; Fox, T.; Heath, R. Development of the Australian Agricultural Sustainability Framework 2021–22; Australian Farm Institute: Eveleigh, NSW, Australia, 2022. [Google Scholar]

- Tait, P.; Saunders, C.; Guenther, M.; Rutherford, P. Emerging versus developed economy consumer willingness to pay for environmentally sustainable food production: A choice experiment approach comparing Indian, Chinese and United Kingdom lamb consumers. J. Clean. Prod. 2016, 124, 65–72. [Google Scholar] [CrossRef]

- Bastounis, A.; Buckell, J.; Hartmann-Boyce, J.; Cook, B.; King, S.; Potter, C.; Bianchi, F.; Rayner, M.; Jebb, S.A. The impact of environmental sustainability labels on willingness-to-pay for foods: A systematic review and meta-analysis of discrete choice experiments. Nutrients 2021, 13, 2677. [Google Scholar] [CrossRef] [PubMed]

- Li, S.; Kallas, Z. Meta-analysis of consumers’ willingness to pay for sustainable food products. Appetite 2021, 163, 105239. [Google Scholar] [CrossRef] [PubMed]

- Katare, B.; Yim, H.; Byrne, A.; Wang, H.H.; Wetzstein, M. Consumer willingness to pay for environmentally sustainable meat and a plant-based meat substitute. App. Econ. Perspect. Policy 2023, 45, 145–163. [Google Scholar] [CrossRef]

- Schrobback, P.; Zhang, A.; Ha, T.M. Demand for Agri-Food Attributes and Attribute Claim Assurance in China and Vietnam from Importers’ Perspective; CSIRO: Canberra, Australia, 2022.

- Cook, B.; Costa Leite, J.; Rayner, M.; Stoffel, S.; van Rijn, E.; Wollgast, J. Consumer interaction with sustainability labelling on food products: A narrative literature review. Nutrients 2023, 15, 3837. [Google Scholar] [CrossRef] [PubMed]

- Regulation on Deforestation-Free Products. Available online: https://environment.ec.europa.eu/topics/forests/deforestation/regulation-deforestation-free-products_en (accessed on 1 February 2024).

- About the National Greenhouse and Energy Reporting Scheme. Available online: https://www.cleanenergyregulator.gov.au/NGER/About-the-National-Greenhouse-and-Energy-Reporting-scheme (accessed on 1 February 2024).

- Thomas, D.T.; Mata, G.; Toovey, A.F.; Hunt, P.W.; Wijffels, G.; Pirzl, R.; Strachan, M.; Ridoutt, B.G. Climate and biodiversity credentials for Australian grass-fed beef: A review of standards, certification and assurance schemes. Sustainability 2023, 15, 13935. [Google Scholar] [CrossRef]

- The 17 Goals. Available online: https://sdgs.un.org/goals (accessed on 1 February 2024).

- MLA. The Australian Red Meat and Livestock Industry—State of the Industry Report 2023; Meat & Livestock Australia: North Sydney, NSW, Australia, 2023. [Google Scholar]

- Coles Finest Certified Carbon Neutral Range. Available online: https://www.coles.com.au/about/our-partners/farming/carbon-neutral (accessed on 7 February 2024).

- Climate Active Certification. Available online: https://www.climateactive.org.au/be-climate-active/certification (accessed on 7 February 2024).

- Great Southern Farms 100% Grass Fed Australian Beef and Lamb. Available online: https://greatsouthernfarms.com.au/ (accessed on 7 February 2024).

- Greenham Natural Beef. Available online: https://www.greenham.com.au/greenham-natural-beef/ (accessed on 7 February 2024).

- Commonwealth Bank of Australia. 2023 Climate Report; CBA: Sydney, NSW, Australia, 2023. [Google Scholar]

- National Australia Bank. Climate Report 2023. Available online: https://www.nab.com.au/content/dam/nab/documents/reports/corporate/2023-climate-report.pdf (accessed on 2 January 2024).

- Westpac Group. Westpac 2023 Climate Report. Available online: https://www.westpac.com.au/content/dam/public/wbc/documents/pdf/aw/ic/Westpac-2023-Climate-Report.pdf (accessed on 2 January 2024).

- Australia and New Zealand Banking Group. 2023 Climate-Related Financial Disclosures. Available online: https://www.anz.com.au/content/dam/anzcomau/about-us/anz-2023-climate-related-financial-disclosures.pdf (accessed on 2 January 2024).

- The Cooperative Rabobank. Global Standard on Sustainable Development. Available online: https://media.rabobank.com/m/3197e93d12fa9d9/original/Sustainability-Policy-Framework.pdf (accessed on 12 February 2024).

- Net-Zero Banking Alliance. Available online: https://www.unepfi.org/net-zero-banking/ (accessed on 12 February 2024).

- Australia’s First Sustainability-Linked Loan for Agriculture. Available online: https://www.commbank.com.au/articles/newsroom/2021/07/sustainability-linked-loan-for-agriculture.html (accessed on 2 January 2024).

- Partnership for Carbon Accounting Financials (PCAF). The Global GHG Accounting and Reporting Standard Part A: Financed Emissions, 2nd ed.; Partnership for Carbon Accounting Financials: Parkes, ACT, Australia; Available online: https://carbonaccountingfinancials.com/en/ (accessed on 12 February 2024).

- Net-Zero Banking Alliance—Our Members. Our Members—United Nations Environment—Finance Initiative. Available online: http://unepfi.org (accessed on 12 February 2024).

- Australian Government, Treasury. Climate-Related Financial Disclosures; Consultation Paper, June 2023; Commonwealth of Australia: Parkes, ACT, Australia, 2023.

- Climate-Related Financial Disclosure: Exposure Draft Legislation. Available online: https://treasury.gov.au/consultation/c2024-466491#:~:text=The%20Exposure%20Draft%20legislation%20seeks,climate%2Drelated%20risks%20and%20opportunities (accessed on 13 February 2024).

- Exposure Draft ED SR1 Australian Sustainability Reporting Standards—Disclosure of Climate-related Financial Information. Available online: https://aasb.gov.au/news/exposure-draft-ed-sr1-australian-sustainability-reporting-standards-disclosure-of-climate-related-financial-information/ (accessed on 13 February 2024).

- Council of Financial Regulators—Climate Change. Available online: https://www.cfr.gov.au/financial-stability/climate-change.html (accessed on 13 February 2024).

- International Financial Reporting Standards Foundation—General Sustainability-related Disclosures. Available online: https://www.ifrs.org/projects/completed-projects/2023/general-sustainability-related-disclosures/ (accessed on 13 February 2024).

- Task Force on Climate-Related Financial Disclosures. Available online: https://www.fsb-tcfd.org/ (accessed on 13 February 2024).

- Financial Stability Board. Available online: https://www.fsb.org/ (accessed on 13 February 2024).

- Taskforce on Nature-Related Financial Disclosures. Available online: https://tnfd.global/ (accessed on 13 February 2024).

- Edmans, A. The end of ESG. Financ. Manag. 2023, 52, 3–17. [Google Scholar] [CrossRef]

- Elsner, C.; Neumann, M. Caught between path-dependence and green opportunities—Assessing the impetus for green banking in South Africa. Earth Syst. Gov. 2023, 18, 100194. [Google Scholar] [CrossRef]

- Etty, T.; van Zeben, J.; Carlarne, C.; Duvic-Paoli, L.-A.; Huber, B.; Huggins, A. The possibility of radical change in transnational environmental law. Transnat. Environ. Law 2022, 11, 447–461. [Google Scholar] [CrossRef]

- Parker, C.; Sheedy-Reinhard, L. Are banks responsible for animal welfare and climate disruption? A critical review of Australian banks’ due diligence policies for agribusiness lending. Transnat. Environ. Law 2022, 11, 603–628. [Google Scholar] [CrossRef]

- Ridoutt, B.; Lehnert, S.A.; Denman, S.; Charmley, E.; Kinley, R.; Dominik, S. Potential GHG emission benefits of Asparagopsis taxiformis feed supplement in Australian beef cattle feedlots. J. Clean. Prod. 2022, 337, 130499. [Google Scholar] [CrossRef]

- Black, J.L.; Davison, T.M.; Box, I. Methane emissions from ruminants in Australia: Mitigation potential and applicability of mitigation strategies. Animals 2021, 11, 951. [Google Scholar] [CrossRef] [PubMed]

- Almeida, A.K.; Hegarty, R.S.; Cowie, A. Meta-analysis quantifying the potential of dietary additives and rumen modifiers for methane mitigation in ruminant production systems. Anim. Nutr. 2021, 7, 1219–1230. [Google Scholar] [CrossRef]

- Hegarty, R.S.; Passetti, R.A.C.; Dittmer, K.M.; Wang, Y.; Shelton, S.; Emmet-Booth, J.; Wollenberg, E.; McAllister, T.; Beauchemin, K.; Gurwick, N.; et al. An Evaluation of Evidence for Efficacy and Applicability of Methane Inhibiting Feed Additives for Livestock. An Evaluation of Emerging Feed Additives to Reduce Methane Emissions from Livestock. Available online: https://globalresearchalliance.org/wp-content/uploads/2021/12/An-evaluation-of-evidence-for-efficacy-and-applicability-of-methane-inhibiting-feed-additives-for-livestock-FINAL.pdf (accessed on 22 August 2022).

- Fouts, J.Q.; Honan, M.C.; Roque, B.M.; Tricarico, J.M.; Kebreab, E. Enteric methane mitigation interventions. Transl. Anim. Sci. 2022, 6, txac041. [Google Scholar] [CrossRef]

- Mayberry, D.; Bartlett, H.; Moss, J.; Davison, T.; Herrero, M. Pathways to carbon-neutrality for the Australian red meat sector. Agric. Syst. 2019, 175, 13–21. [Google Scholar] [CrossRef]

- Allen, M.R.; Shine, K.P.; Fuglestvedt, J.S.; Millar, R.J.; Cain, M.; Frame, D.J.; Macey, A.H. A solution to the misrepresentations of CO2-equivalent emissions of short-lived climate pollutants under ambitious mitigation. NPJ Clim. Atmos. Sci. 2018, 1, 16. [Google Scholar] [CrossRef]

- Cain, M.; Lynch, J.; Allen, M.R.; Fuglestvedt, J.S.; Frame, D.J.; Macey, A.H. Improved calculation of warming equivalent emissions for short-lived climate pollutants. NPJ Clim. Atmos. Sci. 2019, 2, 29. [Google Scholar] [CrossRef]

- Collins, W.J.; Frame, D.J.; Fuglestvedt, J.S.; Shine, K.P. Stable climate metrics for emissions of short and long-lived species—Combining steps and pulses. Environ. Res. Lett. 2020, 15, 024018. [Google Scholar] [CrossRef]

- Ridoutt, B. Climate neutral livestock production—A radiative forcing-based climate footprint approach. J. Clean Prod. 2021, 291, 125260. [Google Scholar] [CrossRef]

- Ridoutt, B. Climate impact of Australian livestock production assessed using the GWP* climate metric. Liv. Sci. 2021, 246, 104459. [Google Scholar] [CrossRef]

- Myhre, G.; Shindell, D.; Bréon, F.-M.; Collins, W.; Fuglestvedt, J.; Huang, J.; Koch, D.; Lamarque, J.-F.; Lee, D.; Mendoza, B.; et al. Chapter 8 Anthropogenic and natural radiative forcing. In Climate Change 2013: The Physical Science Basis. Contribution of Working Group I to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change; Stocker, T.F., Qin, D., Plattner, G.-K., Tignor, M., Allen, S.K., Boschung, J., Nauels, A., Xia, Y., Bex, V., Midgley, P.M., Eds.; Cambridge University Press: Cambridge, UK, 2013; pp. 659–740. [Google Scholar]

- Ridoutt, B.; Huang, J. When climate metrics and climate stabilization goals do not align. Environ. Sci. Technol. 2019, 53, 14093–14094. [Google Scholar] [CrossRef]

- Paris Agreement. Available online: https://unfccc.int/sites/default/files/english_paris_agreement.pdf (accessed on 4 July 2023).

- The Commitment. Available online: https://www.unepfi.org/net-zero-banking/commitment/ (accessed on 8 December 2023).

- Climate Change Widespread, Rapid, and Intensifying—IPCC. Available online: https://www.ipcc.ch/2021/08/09/ar6-wg1-20210809-pr/ (accessed on 4 July 2023).

- Smith, C.; Nicholls, Z.R.J.; Armour, K.; Collins, W.; Forster, P.; Meinshausen, M.; Palmer, M.D.; Watanabe, M. The earth’s energy budget, climate feedbacks, and climate sensitivity supplementary material. In Climate Change 2021: The Physical Science Basis. Contribution of Working Group I to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change; Masson-Delmotte, V., Zhai, P., Pirani, A., Connors, S.L., Péan, C., Berger, S., Caud, N., Chen, Y., Goldfarb, L., Gomis, M.I., et al., Eds.; Cambridge University Press: Cambridge, UK, 2023; Available online: https://www.ipcc.ch/ (accessed on 22 May 2023).

- FAO. Methane Emissions in Livestock and Rice Systems—Sources, Quantification, Mitigation and Metrics; Livestock Environmental Assessment and Performance (LEAP) Partnership: Rome, Italy, 2023. [Google Scholar]

- del Prado, A.; Lynch, J.; Liu, S.; Ridoutt, B.; Pardo, G.; Mitloehner, F. Opportunities and challenges in using GWP* to report the impact of ruminant livestock on global temperature change. Animal 2023, 17, 100790. [Google Scholar] [CrossRef]

| First Reporting Period 1 | Thresholds for Large Entities and Their Controlling Entities Meeting at Least Two of Three Criteria | ||

|---|---|---|---|

| Consolidated Annual Revenue | Consolidated Gross Assets | Number of Employees | |

| FY 2024/25 | AUD 500 M | AUD 1 B | 500 |

| FY 2026/27 | AUD 200 M | AUD 500 M | 250 |

| FY 2027/28 | AUD 50 M | AUD 25 M | 100 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ridoutt, B. Drivers of Sustainability Credentialling in the Red Meat Value Chain—A Mixed Methods Study. Agriculture 2024, 14, 697. https://doi.org/10.3390/agriculture14050697

Ridoutt B. Drivers of Sustainability Credentialling in the Red Meat Value Chain—A Mixed Methods Study. Agriculture. 2024; 14(5):697. https://doi.org/10.3390/agriculture14050697

Chicago/Turabian StyleRidoutt, Bradley. 2024. "Drivers of Sustainability Credentialling in the Red Meat Value Chain—A Mixed Methods Study" Agriculture 14, no. 5: 697. https://doi.org/10.3390/agriculture14050697

APA StyleRidoutt, B. (2024). Drivers of Sustainability Credentialling in the Red Meat Value Chain—A Mixed Methods Study. Agriculture, 14(5), 697. https://doi.org/10.3390/agriculture14050697