1. Introduction

The rapid growth of intermittent renewable energy sources (RESs) for electricity generation requires flexible large-scale energy storage systems (ESSs). Electricity generated by some forms of RESs, such as wind or solar photovoltaic (PV), is difficult to forecast; therefore, ESSs are required for balancing electricity supply and demand [

1]. Pumped storage hydroelectricity (PSH) is the most mature and efficient storage technology and accounts for 98% of storage capacity worldwide [

2]. However, the development of new PSH projects is limited by topographic and environmental restrictions. Thus, disused underground space may be used as reservoir for large-scale storage systems such as underground pumped storage hydropower (UPSH) or adiabatic compressed air energy storage (A-CAES) [

3,

4] where the typical round trip energy efficiencies exceed 0.7–0.8 [

5,

6]. Unlike conventional PSH plants, which consist of two water reservoirs located at the surface, both upper and lower reservoirs may be underground in the case of UPSH plants. For that purpose, two different options may be considered: (1) to make use of existing infrastructure; or (2) to dig new tunnels. Winde et al. [

7,

8] explored the use of deep-level gold mines in South Africa for UPSH schemes. Pujades et al. [

9,

10] carried out a study considering the use of a closed slate mine located at Belgium with a capacity of 550,000 m

3 as a lower reservoir for UPSH. Bodeux et al. [

11] analyzed the interactions between groundwater and the slate chambers used as a subsurface water reservoir. Closed coal mines in Spain and Germany have also been proposed as underground reservoirs for UPSH [

12,

13,

14,

15]. Wong [

16] proposed digging new tunnels or shafts as a lower reservoir for UPSH in the Bukit Timah granite of Singapore. The economic feasibility of UPSH plants depends on the capital costs and the price spread between the electricity generated and consumed in turbine and pumping modes, respectively. In the Iberian electricity system, RES generation is granted priority during the dispatch and receives a fixed feed-in tariff. The day-ahead prices (spot prices), are set around noon on the day preceding the delivery. The day-ahead markets are complemented by intraday markets and ancillary services in the case of unforeseen events and changing weather conditions, which mainly could affect wind and solar PV generation. Finally, the balance of the electricity demand and supply is achieved through the ancillary services, which are managed by the system operator, taking the form of auctions in the Iberian electricity system.

Traditionally, a PSH plant has been operated by the price-arbitrage strategy. PSH plants have participated in the day-ahead market, selling the electricity generated at peak periods (peak price hours) and purchasing the electricity at off-peak periods [

17,

18]. However, the electricity price spread between the on-peak periods and off-peak periods has been reduced significantly, and the economic feasibility of a PSH might not be guaranteed participating just in the day-ahead electricity market. Lobato et al. [

19] carried out an overview of ancillary services in Spain, including a technical description and the management of the ancillary services markets. The study highlights the paramount importance of the ancillary services in a power system. Pérez-Díaz et al. [

20] reviewed the trends and challenges of PSH plants with the aim of optimizing their operation in the balancing markets. The study showed that ancillary services markets, particularly those related to balancing supply and demand, emerge as a valuable source of income for PSH plants.

Krishnan and Das [

21] studied the feasibility of CAES plants participating in the day-ahead and balancing markets of PJM and Midcontinent Independent System Operator (MISO), concluding that the profit may be increased 10-fold by providing ancillary services. Berrada et al. [

22] estimated the income of different ESSs (PSH, CAES and gravity energy storage) that participate in the day-ahead market, the real-time energy market and the regulation market of the New York Independent System Operator (NYISO). The results obtained showed that PSH and CAES may be economically feasible when operating in the regulation market. Chazarra et al. [

23] studied the economic viability of twelve PSH plants participating in the secondary regulation of the Iberian electricity system. The PSH plants were equipped with different fixed-speed and variable-speed units and with and without considering hydraulic short-circuit operation. They concluded that PSH plants equipped with variable speed technology, along with full converters with and without the possibility to operate in hydraulic short-circuit mode, and the PSH plants with ternary units obtain the lowest payback periods.

Recently, Maciejowska et al. [

24] developed a model that is able to predict the price spread between the day-ahead prices and the corresponding volume-weighted average intraday markets in the German electricity system. The research concluded that the sign of the price spread can be successfully predicted with econometric models, such as ARX and probit. Ekman and Jensen [

25] conducted a study of a generic ESS with a global energy efficiency of 0.7 participating in the day-ahead market and some balancing markets in Denmark. They concluded that only UPSH might be profitable as long as it participates both in the day-ahead and ancillary services markets. The contribution of a variable speed PSH to increasing the revenue has been assessed for participation in the day-ahead and secondary regulation reserve markets in the Iberian electricity system [

26]. Chazarra et al. [

27] developed a stochastic model for the weekly scheduling of a hydropower system to optimize the revenue in the Spanish electricity system. The obtained solution protects a multireservoir system against risk of water and storage unavailability. The effect of the complementarity between the variable renewable energy sources and the load on the flexibility of the power system was examined in the Korean electricity system [

28]. They examined an optimal mix ratio between the wind and solar PV and concluded that the ratios of the wind and solar PV to the total variable generation resource were 1.3% and 93.4%, respectively. Lago et al. [

29] proposed a deep neural network by using Bayesian optimization and functional analysis of variance to improve the predictive accuracy in a day-ahead energy market. Chazarra et al. [

30] estimated the maximum theoretical income of a PSH plant participating as a price-taker in the day-ahead and the secondary regulation reserve markets while considering different configurations of power plants in the Iberian electricity system. The results obtained demonstrate that the operation with the variable speed technology could be of considerable help in enlarging the income of the hydropower plant.

In this work, the economic feasibility of three UPSH plants is analyzed considering DTCs between 4 and 10 h. The generation and consumption of electricity and the number of annual generation cycles have been estimated assuming a round trip energy efficiency of 0.77. The day-ahead and ancillary services markets in the Iberian electricity system are analyzed for optimizing the profitability of investment. Secondary regulation, deviation management and tertiary regulation services have been considered to maximize the income from selling energy and minimize the cost for purchasing energy. The capital costs of UPSH plants have also been calculated for the first time, considering the case of using the existing infrastructure and the case of excavating new tunnels or caverns as a lower water reservoir. Finally, a profitability analysis has been carried out using the net present value (NPV), internal rate of return (IRR) and payback period (PB).

2. Methodology

A three-step scheme of the methodology proposed to study the economic feasibility and profitability of UPSH plants is shown in

Figure 1.

The model considers the electricity prices in the day-ahead and ancillary services markets hour by hour for a time period of three years (2016–2018). In step 1, the maximum and minimum prices are analyzed for the energy generated and consumed in the Iberian electricity system, considering DTCs between 4 and 10 h. The number of annual generation cycles and the amount of energy generated are obtained for all scenarios. In step 2, the investment costs of a UPSH plant are estimated for the case of using the existing infrastructure and the case of excavating new tunnels or caverns as a lower reservoir. Amortization costs are calculated considering a typical operation period of 35 years. Finally, in step 3, the operating margin, which is defined as the income from selling energy minus the costs for purchasing energy and the operation costs (O&M, start-up costs, hydraulic cannon and grid access tariffs), is estimated for the three hydropower stations (HPSs) considered in this study.

The earnings before interest and taxes (EBIT) and the cash flows have been calculated to analyze the economic feasibility and the profitability. The NPV, i.e., the difference between the present value of cash inflows and the present value of cash outflows over a period of time; IRR, i.e., a discount rate that makes the NPV of all cash flows from a project equal to zero; and PB, i.e., the time in which the initial outlay of an investment is expected to be recovered, have been calculated in all scenarios.

2.1. Technical Data of UPSH Plants

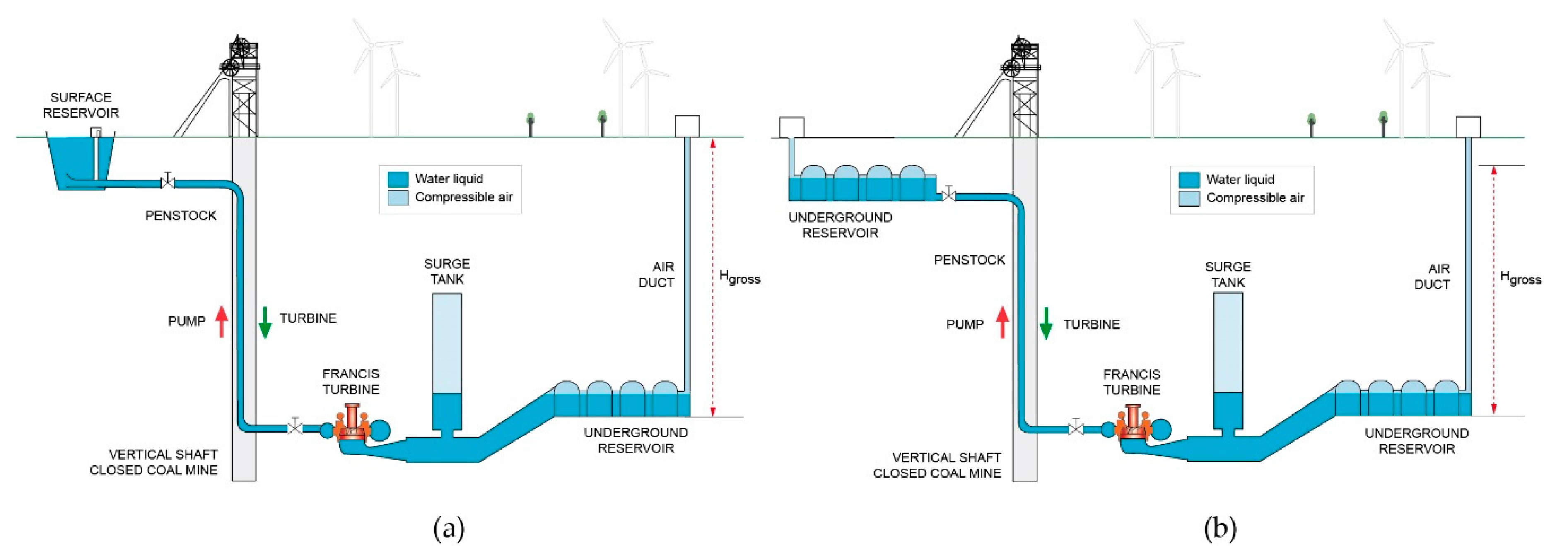

Figure 2 shows two different schemes of UPSH plants in a closed mine.

Figure 2a shows a UPSH scheme with an upper surface reservoir and an underground lower reservoir. Conversely,

Figure 2b depicts a shallow upper reservoir and an underground lower reservoir. Note that the gross head is reduced when a shallow upper reservoir is considered. This reduction in gross head implies a decrease in storable amount of energy.

The technical data of the three hydropower stations (HPSs) are shown in

Figure 3, considering DTCs between 4–10 h day

−1. The water flow rate is lower in pumping mode and therefore the pumping cycle time at full load increases to 5.40 and 13.30 h day

−1. The storage capacities are 0.46, 0.8 and 1.6 Mm

3 for HPS 1, HPS 2 and HPS 3, respectively, and remain constant in each DTC (4–10 h). Although the amount of storable energy does not vary, the output powers decrease from 125, 219 and 440 MW to 50, 87 and 176 MW for HPS 1, HPS 2 and HPS 3, respectively, when the turbine cycle time increases from 4 to 10 h day

−1. A maximum gross pressure of 4.41 MPa has been considered. The water flow rates in turbine mode are 12.78, 22.23 and 44.45 m

3 s

−1 for HPS 1, HPS 2 and HPS 3, respectively, considering a DTC of 10 h, while the efficiency values are 0.91 and 0.90 in turbine and pump mode, respectively. The water flow rates in pumping mode are 9.61, 16.71 and 33.42 m

3 s

−1 for HPS 1, HPS 2 and HPS 3, respectively, when the pumping cycle time at full load is 13.30 h day

−1. In addition, the round trip energy efficiency is assumed to be 0.77 [

6].

2.2. Electric Power System Data

The economic feasibility of UPSH plants is obtained considering the historical hourly values of the prices in the day-ahead and ancillary services markets in the Iberian electricity system during a period of three years (2016–2018). The main objective of this work is to estimate the maximum income from selling energy (turbine mode) and the minimum cost for purchasing energy (pumping mode) while participating in the day-ahead and balancing markets. The following markets and services for the mentioned years have been studied: (i) the day-ahead market; (ii) the upward secondary regulation; (iii) the upward deviation management; and (iv) the tertiary regulation (upward and downward).

The overall amounts of energy managed in secondary regulation, deviation management and tertiary regulation in 2018 were 2592, 2358 and 3301 GWh, respectively. The purpose of the secondary regulation service is to maintain the generation-demand balance, automatically correcting deviations with respect to the anticipated power exchange schedule and the system frequency deviations. The objective of the deviation management service is to resolve the deviations between generation and demand which could appear in the period between the end of one intraday market and the beginning of the next intraday market horizon. Finally, the purpose of the tertiary regulation service is to resolve the deviations between generation and consumption and the restoration of the secondary control band reserve used. These ancillary services are managed and remunerated by market mechanisms in the Iberian electricity system.

4. Conclusions

The economic feasibility of UPSH plants participating in the day-ahead and ancillary services markets in the Iberian electricity system is presented for three HPSs. A deterministic model has been applied in order to maximize the income and minimize the costs for purchasing electricity. Different DTCs between 4 and 10 h have been considered in order to evaluate the economic feasibility of UPSH plants. In addition, the investment costs when making use of existing underground infrastructure and when excavating new tunnels or caverns as a lower reservoir have been estimated in order to evaluate the profitability of the investment.

The results obtained show that the number of annual production cycles and the amount of electricity generated decrease when the DTC increases. The maximum number of annual production cycles is 360 when the DTC is 4 h and decreases to 323 when the DTC increases to 10 h. Although the spread between the income from selling electricity and the costs for purchasing energy decreases when the DTC increases, the operating margin increases due to investment costs. In the profitability model, IRRs greater than or equal to 6% are reached when the investment costs are lower than 2000 € kW−1 and the DTC is greater than 5 h. In general, it can be concluded that the IRR increases when the investment costs decrease and the DTC increases.

A UPSH plant is not economically feasible when new infrastructure has to be built. Maximum IRRs of 2.43%, 2.61% and 2.75% have been obtained for HPS 1, HPS 2 and HPS 3, respectively, with a minimum PB of around 24 years. On the contrary, the investment cost of a UPSH plant is reduced by 46.6% (1675 € kW−1) when the existing underground infrastructure is used as a lower reservoir. Under these conditions, a UPSH plant could be economically feasible (IRRs greater than 6% and PBs lower than 15 years) when participating in the ancillary services markets, dimensioning DTCs greater than 6 h and using the existing underground infrastructure as a lower reservoir.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}