1. Introduction

Sucrose (commonly known as sugar) is one of the most imported commodities worldwide for its volume of production (178.6 Mt in 2018). It is mainly extracted from sugarcane (

Saccharum officinarum L., a perennial tropical plant) and sugar beet (

Beta vulgaris var.

Saccariphera, a biennial plant), since they have a high concentration by weight: 7–18% and 8–22%, respectively (

Schiweck et al. 2002). Sugar is mainly transported in bulk (using auto silos and containers) or using bags of natural material (e.g., jute) or plastic (e.g., polyethylene or high-density polyethylene) of 25–50 kg in weight (

Brody 2006). The transport vector can be naval (ship), railway and road (

TIS (Transport Information Service) 2017).

In the last decade, world sugar production has gradually risen, due to higher food consumption and biofuel production. This stressed a market situation characterized by a greater complexity of trade between the producing and importing countries due to the high numbers of actors involved. This is also reflected in the European Union (EU) market where the system of production and sugar exportation quotas was definitively abolished by 1 October 2017, according to Regulation (EU) No. 1308/2013, to increase competitiveness and strengthen the European market in world trade (

European Commission 2013).

Consequently, the movement of sugar, especially in maritime trade (with containers), will significantly increase in the light of the EU market’s new structural and political–economic conditions. Generally, the containers are upholstered internally by a packaging system (which may be unique or a plurality of bags) to avoid food contamination with the metal of the box. To safeguard the quality of the sugar transported, it is necessary that the international technical specifications are respected (

ISO 22000:2005 2017;

BMT Survey 2017). Container packaging systems are, therefore, of great importance to ensure not only the food safety of the commodity, but also a reduction in economic and environmental costs (

Hansen et al. 2012;

Brody 2006). The role played by companies that offer bulk-packaging systems for the shipping sector has indeed become increasingly essential, since new and competitive scenarios are opening up.

The ability to offer an innovative packaging able to reduce environmental and economic costs for buyers (from sugar producers to logistic agencies), linked, for example, to easier commodity loading and unloading and packaging disposal, also becomes crucial for packaging producers’ market success.

In light of this, the present study aims at presenting the experience of a small, young Italian enterprise (i.e., Eceplast) that launched an innovative product (Barless Liner). It is certified for the quality management of production processes, environmental sustainability and food safety (ISO 22000), allowing the company to be recognized as a leader in bulk packaging systems (container liners) at the European level.

Hence, the paper, starting by describing the sugar market, provides useful information on a “virtuous” example of sustainable business strategy and on a specific “know-how” concerning the importance of using sustainable bulk commodity packaging to reduce economic and external costs in this sector. The methodology used to carry out this study is based on a qualitative analysis (systematic review) and face-to-face interview. The former has been necessary to gather data aimed at discussing the main topic, that is, the bulk-packaging system for the shipping sector, according to an innovative and sustainable approach. The latter has been used to collect in-depth information about the company, which is selected as a case study.

The paper was divided into the following sections: a literature review about maritime transport, with a specific focus on dry bulk shipping; description of the sugar market, highlighting the complex trade between the producing and importing countries, above all in the EU; the packaging systems used for international sugar shipping, focus on bulk-packaging systems; presentation of the case study and its sustainable business due to the adoption of innovation in bulk-packaging systems, underling its environmental and economic advantages; and conclusions.

2. Literature Review

Over the past century, international maritime transport has been the principal mode for allowing the exchange of commodities amongst countries, thus favoring globalization. Currently, it continues to play an essential role in international trade since it covers, in the world’s economy, over 90% of the world’s trade. In 2018, the total volumes of commodities carried by sea reached an all-time high of 11 billion tons (with a growth of around 3.9% per year in the last decade). This data is expected to grow by 3.8% per year in the next 5 years. Dry bulk commodities, followed by containerized cargo, other dry bulk, oil, gas and chemicals, contributed the most to this growth. Growing demand for goods and raw materials and more consolidation within the shipping industry are estimated to increase business operations for ship-owners even if, in 2019, uncertainty concerning trade tensions between China and the United States has had negative consequences on the world economy, leading to a decelerated demand for dry bulk and tankers (

UNCTAD 2019;

Clarksons 2019). Consequently, shipping is one of the most finance-intensive industries in the world and future financing needs are expected to increase (

Wohlstrand and Marek 2014).

This mode has also changed greatly in recent years because more attention has been paid to reducing its environmental impact and to improving its efficiency by introducing containerization and ultra-large container vessels, that allow relevant economies of scale (

Halim et al. 2018); designing for ports’ effective voluntary programs and appropriately motivating participation from global shipping companies that visit these ports (

Linder 2018); increasing energy efficiency in shipping, through reduced speed at sea, enabled by a shorter time in port, whilst maintaining the same transport service (

Johnson and Styhre 2015).

To support this statement, the authors conducted a systematic review to verify how many academic papers have been published on this topic and to describe the scientific evolution of these studies. For this reason, data were collected through a combination of (a) database searches (cross-discipline platforms of Elsevier) as of 7 November 2019, and (b) screening references of studies retrieved under (a). The aim was to select highly referenced studies, to identify, highlight and assess all data related to the above-mentioned subject. For an initial selection, the key words were: (i) sugar market; (ii) sugar shipping and/or transport; (iii) maritime transport, (iv) bulk packaging system and, (v) dry bulk shipping. The search was not limited to a specific period.

The qualitative analysis revealed a few articles on the specific topic (sugar along with bulk packaging system). Indeed, the majority of in-depth studies were expressly focused on: (a) the environmental impact of international trade by shipping and aspects of the dry bulk shipping industry; and, (b) the sugar industry, where some details were provided for overall sugarcane agribusiness diversification.

Concerning the importance of environmental concerns, (

Gritsenko 2017) stressed that: “maritime transport is a significant contributor to the global Greenhouse Gas (GHG) with emissions set to grow”. According to the Third International Maritime Organization (IMO) GHG Study, the annual CO

2 estimate in international shipping decreased from 2.8% in 2007 to 2.2% in 2012. Nevertheless, this value will considerably increase by 2050, reaching 17% of global GHG, in the case of maintaining the current regulatory measures (Energy Efficiency Design Index—EEDI, and the Ship Energy Efficiency Management Plan—SEEMP), while the European Commission, in 2011, set a goal to reduce emissions from shipping by at least 40% by 2050 (

European Commission 2011).

For this reason, it is useful to complement technical standardization in the areas of ship design and operations, with policies targeting shipping sectors.

To this end, a previous study, written by (

Wang et al. 2015), declared that: “various market-based measures have been proposed to reduce CO

2 emissions from international shipping. One promising mechanism under consideration is the Emission Trading Scheme (ETS)”. They demonstrated, by elaborating an economic model, that currently the ETS application is not effective, due to the particular characteristics of the sector: inhomogeneous carriers, and different market structures and companies across different shipping sectors. Therefore, it was important to continue to study and evaluate certain key issues regarding the ETS itself, although numerous political and institutional factors might be responsible for such slow progress.

Some years later, (

van der Loeff et al. 2018) confirmed that: “although maritime transport offers by far the most energy efficient mode of long-distance mass cargo transportation, it has a significant responsibility for anthropogenic climate change … Despite its importance, the maritime shipping sector has been traditionally overlooked in climate mitigation discussions, since this sector was largely neglected in the 1997 Kyoto Protocol”. The main problems for effective application of CO

2 abatement measures, in this sector, involve the absence of reliable emissions data and the inherent difficulty of exactly accounting for the quota of emissions attributable to the involved countries, companies and commodities, as well as the threat to global trade interests.

Specific research on seaborne containers, by (

Yang et al. 2018), highlighted that: “uncertainties as a result of climate change, epidemics, and increasing economic upheaval create risks for the proper functioning of container supply chains (CSC) and stimulate the research and development of resilient and sustainable container transportation”. Consequently, it is necessary to include green perspectives into the management of intermodal container transportation for improving the environmental performance of international trade flows, mainly considering the different methods and practices currently used in various transport segments (e.g., port, shipping and road) and geographical regions.

This aspect was also stressed by (

Shin et al. 2018), stating that: “research on sustainability of maritime logistics is on the rise, yet fragmented in terms of conceptual development, empirical testing and validation, and theory building. These issues are related to green ports/shipping, carbon emission/climate change and region-specific environmental regulation/management”. Specifically, they stressed that, in the case of maritime logistics, it is necessary to implement optimal logistics systems, sustainable supply chain design, and service quality management in order to deal with the sustainability issues.

As regarding the aspects of dry bulk shipping industry, a first study in the literature of maritime economics, examining the impact of subsidies on the fleet renewal schemes of shipping companies, has been presented by (

Yang et al. 2019). They proposed a “model of general applicability and use to shipping companies wishing to design efficient ship renewal schemes under various market and regulatory circumstances”. In the framework of environmental sustainability, this research could represent a starting point to provide useful evidences to governments and supranational regulatory organizations, such as IMO and the European Commission, for implementing or evaluating scrapping subsidies for environmental or other purposes.

More specifically, (

Moutzouris and Nomikos 2019) analyzed the relationship between second-hand vessel prices, net earnings, and holding period returns in sectors of the dry bulk shipping industry. They showed that “high shipping earnings yields strongly and negatively predict future net earnings growth. Furthermore, there is no consistent evidence of time-varying expected returns in the second hand dry bulk shipping industry”. These evidences had never been reported before in the shipping literature, thus representing a valuable study for providing a framework to determine prices in shipping assets, with finite economic lives and also subject to wear and tear. Certainly, this data might also affect the application of environmental subsidies and actions for reducing the GHG emissions released by the dry bulk shipping industry.

In this framework, it is also interesting to examine which innovations in packaging systems for dry bulk shipping industry are able to ensure not only the food safety of the dry commodity, but also the reduction of economic and environmental costs for logistic operators. This is mostly true for the sugar shipping that will increase due to the new EU structural and political–economic conditions, as previously described.

In addition, (

Bezuidenhout and Baier 2009) highlighted that: “almost none of the research conducted to date brings long-term sustainability, environmental issues, value adding, the sugar markets and marketing beyond the mill into a overall supply chain context. This is considered a significant shortcoming in the sugar industries of the world, since many modern supply chains do consider these issues holistically”. This means that researchers have mainly investigated the integration of sugarcane supply systems, especially in a harvesting context, assessing long-term strategic issues, while omitting the importance of shipping logistics.

Moreover, (

Higgins et al. 2007) underlined that: “sugar industries around the world are primarily ‘‘push chains’’, where sugarcane is pushed through the chain to produce raw sugar with minimal product differentiation and sold at market value as a bulk commodity. A general sugar value chain consists of growing, harvesting, cane transport, mill processing, sugar transport and storage/shipping/marketing sectors”. Consequently, in order to increase the sugar value chain opportunities, a technical solution along with the participation of actors from across the chain, are needed, considering also the last phase of the sugar value chain, which is the shipping sector.

Therefore, the present study may represent a starting point to deal with one aspect of the sugar supply chain and to develop further empirical researches.

5. A New Sustainable Bulk-Packaging System: Eceplast’s Barless Liner

In order to collect information about the case study, i.e., Eceplast S.r.l., the European leader enterprise in the bulk container liners, the method of in-depth face-to-face interviewing has been used. Specifically, the authors asked specific questions about the company and the technological innovation introduced as a sustainable business strategy to pursue a higher competitiveness in the market. The interviewees were N. Altobelli (Commercial director) and S. Di Cori (Investment and regulations).

In Italy, the company Eceplast S.r.l. is certainly an interesting case because, starting from a patent for a packaging system for the transport of dry bulk in containers, it has increased its competitive advantages in this sector.

The company, founded in 1995, is located in the industrial zone of Troia (a small town in the Apulia region of Southern Italy) and has 90 employees. From its founding year until 2008, production was marked by the implementation of a first patent to facilitate the loading and unloading of bulk commodities. This patent has allowed the company to become a leader in the European Union (

Altobelli 2019).

From 2008 to today, the company has been in a phase called Industrial 4.0, characterized by technological automation of its processes. In addition to the production plant, the site hosts administrative and commercial offices, a research and development sector and quality control.

Eceplast’s activities are mainly the production of packaging for dry and liquid bulk transport and for spare parts and components for the automotive sector. Over the years, it has been able to market about 380 packaging models in 90 countries. Almost all production lines are highly automated, with on-board computers, sensors and integrated intelligence.

The various transport packaging typologies can be grouped as follows: liner bags for dry bulk products, and thermos-protectors to protect and ship temperature-sensitive cargo. These were designed to lower costs and minimize carbon footprint with reuse and recycling programs. Eceplast is introducing a new, more scientific approach to thermal issues on the European intermodal transport market: paper sacks, spare parts and components for the automotive sector (

Eceplast 2019).

The present study focuses on packaging systems concerning dry bulk product transport (in this case sugar) with container. The company is the major producer of “liner bags” for containers, as previously mentioned. Generally, the liner bags use a container’s open side for loading and unloading of bulk products. They are systems made of linear polyethylene and polyethylene, both of low density, reinforced with raffia fabric and with the possibility of using steel bars, anchored to a stiffening wall with special holes.

Thanks to the first Italian patent, released in 1998, No. IT1290065, Eceplast launched on the international market an innovative transport system that is effective, hygienic and 100% waterproof. This system provides the welding of the cylindrical plastic pieces flexible on perpendicular plastic surfaces to facilitate loading and unloading and enhance security and structural integrity

The liner bag price for a buyer is equal to 80 euros, without considering reduction (up to 65%) of container management costs due to the following: elimination of cleaning costs; optimization of transport streams (containers after discharge are ready to be loaded); decrease of cargo bed wear (every loading without a liner damages floor planes, which deteriorate due to the necessary subsequent washings); and, obviously, cleaner containers have a greater benefit (

Altobelli 2019). Finally, the liner bags are waterproof, as they avoid percolation losses during transportation and prevent expensive penalties. For hazardous materials, they represent the ideal solution to reduce the risk of contamination and pollution.

Eceplast’s liner bags have been certificated by ISO 9001:2008 and ISO 14000:2004 rules, for quality and environmental management, respectively, and by ISO 22000:2005 for food safety management. This latter certification, obtained in 2010, is designed to harmonize existing national and international standards about food safety and Hazard Analysis and Critical Control Points (HACCP) (

Eceplast 2019). The ISO 22000 standard was published by the TC34 Committee in September 2005, under the name “Food Safety Management Systems—Requirements for any Organization in the Food Sector”, and adopted by the UNI (National Board of Unification) in April 2006. The set of technical standards concern food safety “from field to table”, based on the fundamental elements recognized internationally by all operators in the sector (ISO/TS 22002-1:2009; 22004:2005; 22003:2007; ISO 22005:2007; ISO 22006:2009) (ISO 22000:2005).

The Patent of New the Barless Liner: Sustainable Business Strategy

In the “liner bags” category, special attention is paid to a new product called a Barless Liner. Its patent application was submitted in April 2014 with the aim of introducing a technological innovation in the “standard liners”, mainly to eliminate the high disposal cost for final buyers (commodity producers and/or logistics companies) due to the presence of steel bars.

Eceplast, starting from what has already been done by Illinois Machine Works (Texas) with patent No. USA US2007267410, has deposited a patent application, No. PCT/IT2014/000099, entitled “Supporting structure for a container cargo”. Indeed, the proposed innovation is to remove steel bars and reduce general costs, thanks to the maximization of bulk loading times, the higher installation speed, and the higher level of safety compared to standard products. In other words, its purpose is to provide a supporting structure that is simpler to be realized and more efficient from a structural point of view (

Altobelli 2015). Additionally, the Barless Liner has a positive impact on the environment, because its use reduces the amount of waste in the short and medium term. In fact, it can be 100% recycled (

Eceplast 2019). The Barless Liner’s price is 100 euros; even if more expensive than standard liner bags (+20 euros), this product is the best solution, since the buyer does not support other costs (e.g., security, disposal, loading and unloading, and taxes linked to weight).

Specifically, the new support structure is located on the open side of a container, and it is characterized by a series of pre-tensioned belts, which are connected to an elastically deformable composite element in the center of the ring. This new system allows optimization of the assembly phases of the supporting structure. The tension of the entire structure is, in fact, adjustable, acting on any belt.

Furthermore, the benefits and technology of Eceplast’s barless innovation are shared with the container shipment world to create a “barless safety system (BSS) network” involving customers, distributors, suppliers, and end-users in this crowdsourcing innovation. The network improves customer value and drives advancements across the shipping industry. Eceplast grants access to BSS developments, good practices for the sales team, a better price, tutorial video, and return and refund policy (

Eceplast 2019).

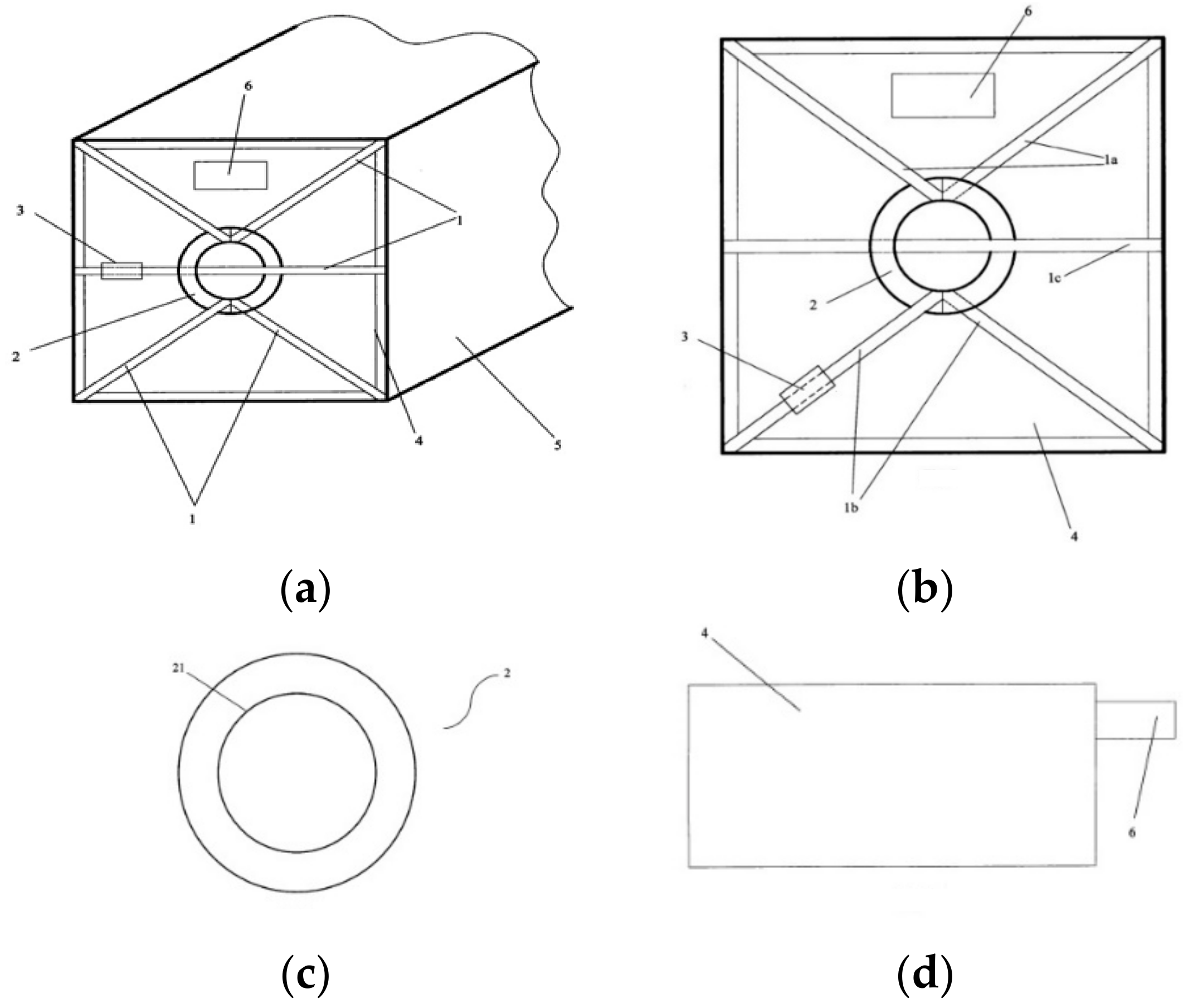

Figure 5 represents the set of images, attached to the patent, for a detailed description of the technological innovation:

- ✓

Figure 5a shows the cargo-supporting structure applied to the rear open side of a generic container;

- ✓

Figure 5b is a front view of the open side, with the cargo-supporting structure;

- ✓

Figure 5c indicates a detail of the deformable and non-extensible element;

- ✓

Figure 5d illustrates a side view of the inner liner of the container.

Figure 5a describes the open side of an ISO

4 (5) 20-foot or ISO 40-foot (6 or 12 m) container with the cargo-supporting structure, which is the object of the invention. In detail, it is made up of a liner for the transport of bulk (4). Furthermore, the structure consists of pre-tensioned belts (1), deformable and non-extensible element (2) and tensioner (3) means. There is also an opening for the introduction or extraction of bulk (6). The innovation is the deformable element conforming to a circular ring, in which the belts pass. This can be deformed but not spread wide because, inside, it has wire that gives greater rigidity to the ring itself.

In the front view (

Figure 5b), it is possible to notice the system of belts anchored on the inner wall of the container. Each of them must also be fixed to the center ring, to act as support of the same; in addition, they are arranged horizontally and diagonally, with anchorages in the opposite position. There is a possibility that each belt can move around the ring several times, mostly for assuring the anchorage. The whole structure is tensioned by means of special ratchet levers (3), which can act on each belt. It is preferable to act on the belt located at the bottom of the liner (4). Unlike known systems, this type of structure can be tensioned by a single cargo point to balance the entire structure uniformly, thanks to the inner structure of the ring.

Figure 5c shows the central ring, constituted of an elastomer matrix and a reinforcing element. The first one is a cured rubbery material; the latter is a steel ring, placed on the inner circumference (21) or on a series of steel wires placed in the rubber matrix.

Finally,

Figure 5d shows schematically the Barless Liner inside the container. The same is constituted of low-density polyethylene with a thickness of about 0.14 mm. It is also possible to insert a raffia cloth, to be interposed between the liner and the structure so far described, to ensure a clear separation between the bulk material and the cargo-supporting structure (

Altobelli 2015).

To have a preliminary idea of the main differences between Eceplast’s patent proposal and a standard liner system,

Table 1 and

Table 2 have been elaborated.

Table 1 indicates the reduction in the materials used, whereas

Table 2 shows the optimization of the loads using a plurality of bags (pieces).

From a preliminary assessment, the significant reduction in the use of steel, replaced by the introduction of a small amount of polyester, is evident. This innovation increases the container capacity and reduces its weight and, thus, it can contribute to the reduction in environmental impact in terms of fossil fuel use and resulting greenhouse gas emissions. This is due to the saving of energy required for transport (with lighter vehicles the energy consumption will be less) and the reduced steel production. In addition, the possibility of using a Barless Liner several times helps to reduce waste production, according to the “circular economy” concept (

Foschi and Bonoli 2019), and could be considered a tool to mitigate climate change in seaport container activities (

Mamatok et al. 2019). Therefore, this packaging system combines sustainable technology and product innovation to improve maritime trade from and to the EU, in addition to ensuring cost reductions and meeting food safety standards certified by ISO 22000.

6. Conclusions

In recent years, there has been a growing demand for bulk-packaging systems for container shipping, above all in Europe. This is critical especially for the international movement of sugar that, after the abolition of EU sugar quotas on 1 October 2017, introduced in 2006 by the PAC to restructure and defend the industry, will certainly increase. Consequently, it is important to offer efficient services and products to companies operating in this sector to reduce the economic and environmental impacts linked to this activity.

In this field, some innovations have been adopted during the last decades. One of the most interesting is the 20 ft Barless Liner, developed by Eceplast S.r.l., an Italian company that could certainly represent a virtuous example, both for its specific technological innovation and for its sustainable business strategy.

Indeed, innovative products certified for the quality management of production processes, environmental sustainability and food safety allow the company to be recognized as a leader in container liners at the European level. The new patent application “Supporting structure for a container cargo”, registered in the United States in 2016 and still pending in the European Union, will surely strengthen its position in the market. The core innovation is the optimization of the assembly phase of the supporting structure. The tension of the entire structure is, in fact, adjustable, acting on any belt. This means that the structure can be tensioned by a single cargo point, which can balance the entire structure uniformly, thanks to the inner structure of the ring. The 20 ft Barless Liner presents certainly economic benefit: for Eceplast, because its production cost is 5% lower than standard liners, because of the abolition of steel bars (

Altobelli 2019) and, for buyers (both commodity producers and logistic companies), because the management costs could be reduced by 65%, because of the disposal cost of steel bars, the increment of space for loading a higher number of bags, and the improvement of the transport efficiency. Certainly, all these elements contribute to more general environmental benefits too: a minor amount of material used; reduction of waste disposal; and fossil fuel saving in international shipping. In this sense, this paper is limited to a preliminary study, while the authors aim at developing a Life Cycle Assessment (LCA) study, comparing the environmental impacts of production and use of Liner 20 ft Barless, with those of a standard liner. This allows analysis of all the real benefits deriving from this new technological innovation, stressing the opportunities for the whole market, and the actors involved in the supply chain.

Finally, the research findings of the current study should be useful for managerial implications for other practitioners. Firstly, it is important to take into account the environmental sustainability approach in the own business strategy, above all in this period of time, where concerns about climate change are at the core of world economic development policy. This approach could reinforce their position on the market, raising their competitiveness. Secondly, it should be profitable to focus on business, concerning the implementation in the maritime transport of optimal logistic systems, in order to deal with sustainability issues. As widely discussed, this will be one of the sectors of the growing GHG emissions, considering the increase in world population and, consequently, of international trade by shipping. Therefore, the need to reduce its environmental impact could be one of the main topics of the further international agreements of worldwide governments.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}