Is Corporate Political Activity an Investment or Agency? An Application of System GMM Approach

Abstract

1. Introduction

2. Literature Review

2.1. Corporate Political Activities

2.2. Relationship between CPA and FP

2.3. Concept of Corporate Reputation

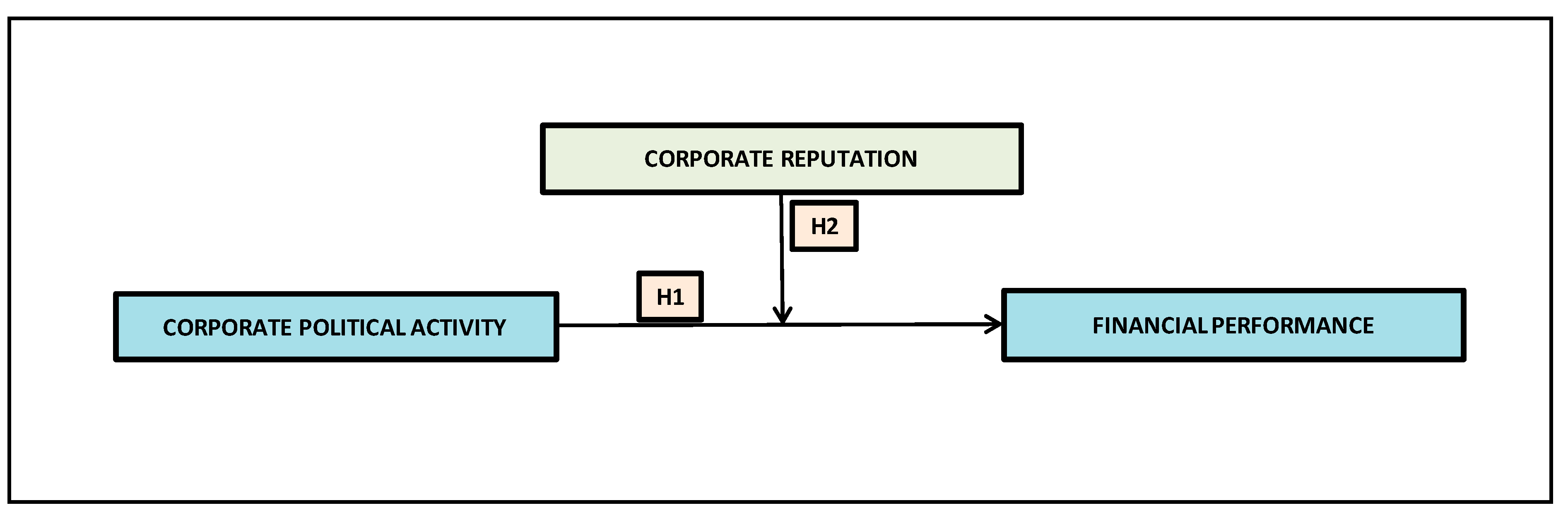

3. Research Hypotheses

3.1. Effect of the CPA on FP

3.2. Effect of the Interaction between CPA and CP on FP

4. Empirical Model, Methodology and Data

4.1. Measurement of Corporate Political Activity

4.2. Measurement of Corporate Reputation

4.3. Measurement of Financial Performance

4.4. Control Variables

4.5. Empirical Model

4.6. Econometric Methodology

4.7. Data and Sample Period

5. Empirical Results and Discussion

5.1. CPA-FP Relationship

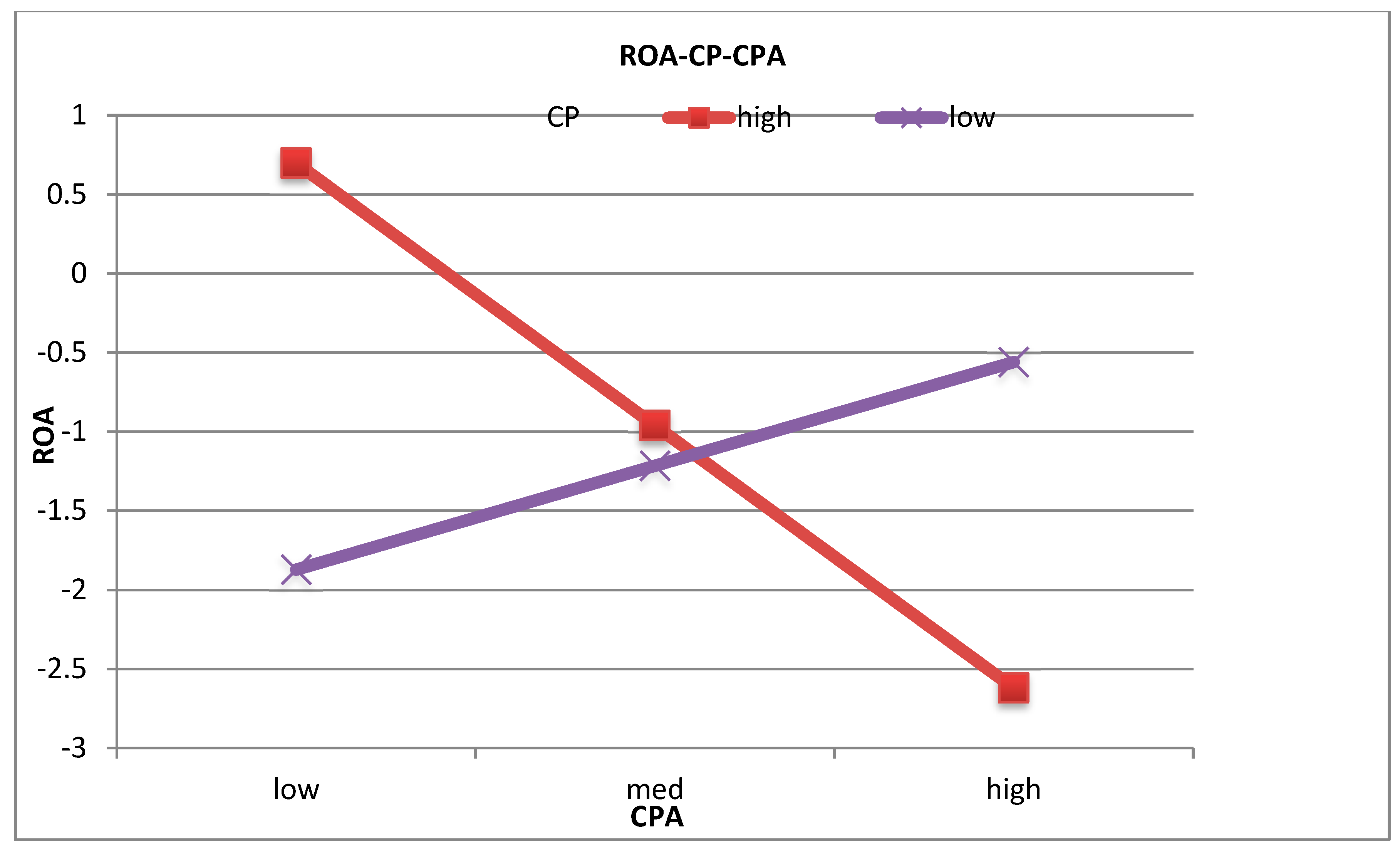

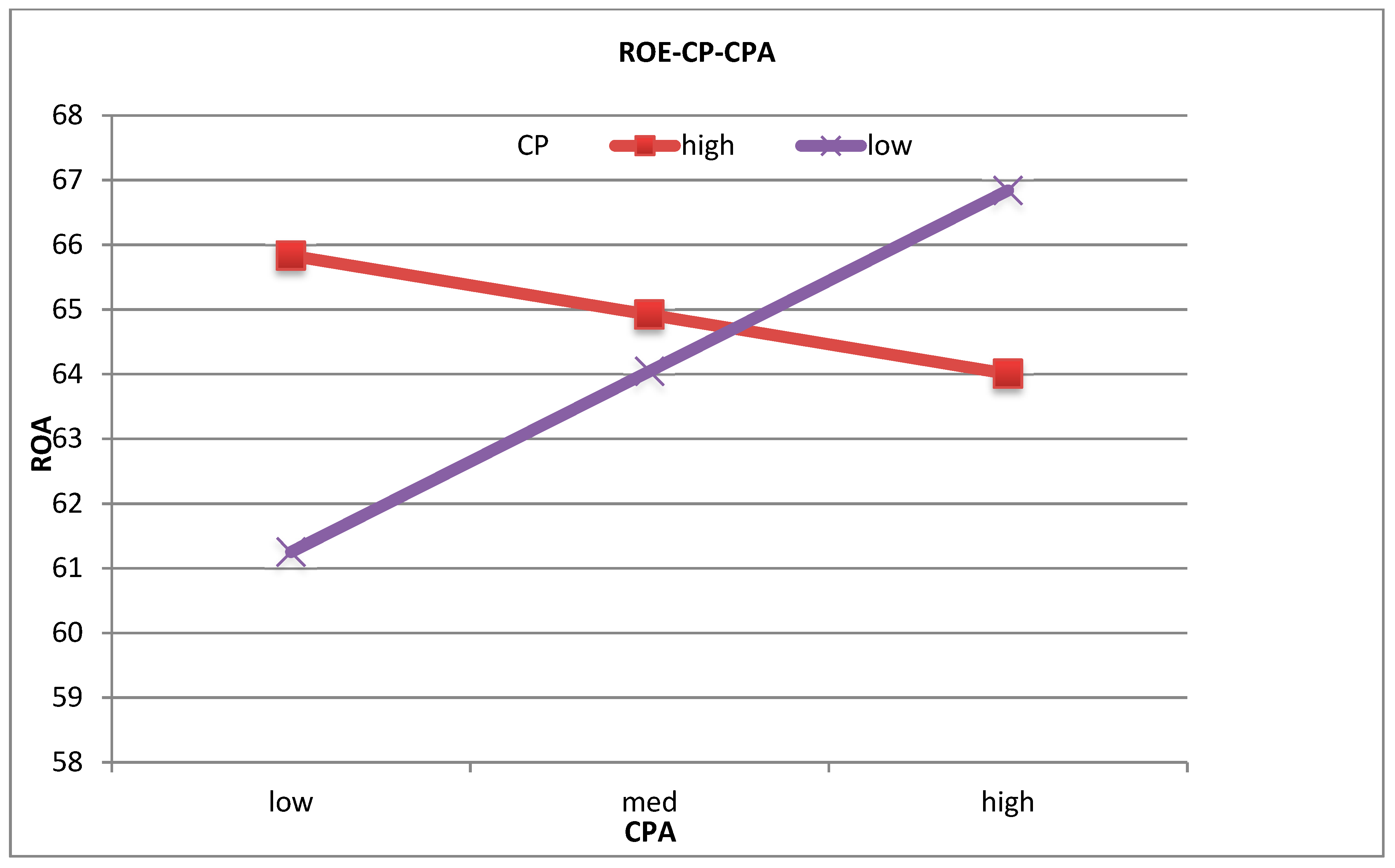

5.2. Determining the Interactive Effect of the CP and CPA on the FP

6. Robustness Test

7. Conclusions

7.1. Implications for Theory and Literature

7.2. Managerial and Policy Implications

7.3. Future Research

Funding

Conflicts of Interest

References

- Aggarwal, Rajesh K., Felix Meschke, and Tracy Yue Wang. 2012. Corporate political donations: Investment or agency? Business and Politics 14: 1–38. [Google Scholar] [CrossRef]

- Aguilera-Caracuel, Javier, and Jaime Guerrero-Villegas. 2018. How corporate social responsibility helps MNEs to improve their reputation. The moderating effects of geographical diversification and operating in developing regions. Corporate Social Responsibility and Environmental Management 25: 355–72. [Google Scholar] [CrossRef]

- Aiken, Leona S., Stephen G. West, and Raymond R. Reno. 1991. Multiple Regression: Testing and Interpreting Interactions. Thousand Oaks: Sage. [Google Scholar]

- Anastasiadis, Stephanos. 2014. Toward a view of citizenship and lobbying: Corporate engagement in the political process. Business & Society 53: 260–99. [Google Scholar]

- Ansolabehere, Stephen, John M. De Figueiredo, and James M. Snyder, Jr. 2003. Why is there so little money in US politics? Journal of Economic Perspectives 17: 105–30. [Google Scholar] [CrossRef]

- Ansolabehere, Stephen, James M. Snyder, Jr., and Michiko Ueda. 2004. Did firms profit from soft money? Election Law Journal 3: 193–98. [Google Scholar] [CrossRef]

- Antia, Murad, Incheol Kim, and Christos Pantzalis. 2013. Political geography and corporate political strategy. Journal of Corporate Finance 22: 361–74. [Google Scholar] [CrossRef]

- Arellano, Manuel, and Stephen Bond. 1991. Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. The Review of Economic Studies 58: 277–97. [Google Scholar] [CrossRef]

- Baron, David P. 2001. Private politics, corporate social responsibility and integrated strategy. Journal of Economics & Management Strategy 10: 7–45. [Google Scholar]

- Bénabou, Roland, and Jean Tirole. 2010. Individual and corporate social responsibility. Economica 77: 1–19. [Google Scholar] [CrossRef]

- Bernstein, Leopold A., and John J. Wild. 1989. Financial Statement Analysis: Theory, Application and Interpretation. Homewood: Irwin, vol. 212, pp. 213–573. [Google Scholar]

- Bliss, Mark A., and Ferdinand A. Gul. 2012. Political connection and cost of debt: Some Malaysian evidence. Journal of Banking & Finance 36: 1520–27. [Google Scholar]

- Blundell, Richard, and Stephen Bond. 1998. Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics 87: 115–43. [Google Scholar] [CrossRef]

- Blundell, Richard, Stephen Bond, and Frank Windmeijer. 2001. Estimation in dynamic panel data models: Improving on the performance of the standard GMM estimator. In Nonstationary Panels, Panel Cointegration and Dynamic Panels. London: Emerald Group Publishing Limited, pp. 53–91. [Google Scholar]

- Bonardi, Jean-Philippe. 2011. Corporate political resources and the resource-based view of the firm. Strategic Organization 9: 247–55. [Google Scholar] [CrossRef]

- Bonardi, J. P., G. L. Holburn, and R. G. Vanden Bergh. 2006. Nonmarket strategy performance: Evidence from US electric utilities. Academy of Management Journal 49: 1209–28. [Google Scholar] [CrossRef]

- Bond, Stephen, Anke Hoeffler, and Jonathan Temple. 2001. GMM Estimation of Empirical Growth Models. Oxford: Economics Group, Nuffield College, University of Oxford. [Google Scholar]

- Boubakri, Narjess, Jean-Claude Cosset, and Walid Saffar. 2012. The impact of political connections on firms’ operating performance and financing decisions. Journal of Financial Research 35: 397–423. [Google Scholar] [CrossRef]

- Bouwen, Pieter. 2002. Corporate lobbying in the European Union: The logic of access. Journal of European public policy 9: 365–90. [Google Scholar] [CrossRef]

- Brambor, Thomas, William Roberts Clark, and Matt Golder. 2006. Understanding interaction models: Improving empirical analyses. Political Analysis 14: 63–82. [Google Scholar] [CrossRef]

- Brammer, Stephen, and Andrew Millington. 2008. Does it pay to be different? An analysis of the relationship between corporate social and financial performance. Strategic Management Journal 29: 1325–43. [Google Scholar] [CrossRef]

- Brown, Richard S. 2016. Lobbying, political connectedness and financial performance in the air transportation industry. Journal of Air Transport Management 54: 61–69. [Google Scholar] [CrossRef]

- Burt, R. S. 2009. Structural Holes: The Social Structure of Competition. Cambridge: Harvard University Press. [Google Scholar]

- Carretta, Alessandro, Vincenzo Farina, Abhishek Gon, and Antonio Parisi. 2012. Politicians ‘on board’: Do political connections affect banking activities in Italy? European Management Review 9: 75–83. [Google Scholar] [CrossRef]

- Chaney, Paul K., Mara Faccio, and David Parsley. 2011. The quality of accounting information in politically connected firms. Journal of Accounting and Economics 51: 58–76. [Google Scholar] [CrossRef]

- Chen, Hui, David Parsley, and Ya-Wen Yang. 2015. Corporate lobbying and firm performance. Journal of Business Finance & Accounting 42: 444–81. [Google Scholar]

- Cooper, Michael J., Huseyin Gulen, and Alexei V. Ovtchinnikov. 2010. Corporate political contributions and stock returns. The Journal of Finance 65: 687–724. [Google Scholar] [CrossRef]

- Cyert, Richard M., and James G. March. 1963. A behavioral theory of the firm. Englewood Cliffs 2: 169–87. [Google Scholar]

- Dang, Chongyu, Zhichuan Frank Li, and Chen Yang. 2018. Measuring firm size in empirical corporate finance. Journal of Banking & Finance 86: 159–76. [Google Scholar]

- De Figueiredo, John M., and Rui J. P. de Figueiredo, Jr. 2002. The allocation of resources by interest groups: Lobbying, litigation and administrative regulation. Business and Politics 4: 161–81. [Google Scholar] [CrossRef]

- Delmas, Magali A., and Maria J. Montes-Sancho. 2010. Voluntary agreements to improve environmental quality: Symbolic and substantive cooperation. Strategic Management Journal 31: 575–601. [Google Scholar] [CrossRef]

- Den Hond, Frank, Kathleen A. Rehbein, Frank GA de Bakker, and Hilde Kooijmans-van Lankveld. 2014. Playing on two chessboards: Reputation effects between corporate social responsibility (CSR) and corporate political activity (CPA). Journal of Management Studies 51: 790–813. [Google Scholar]

- Dozier, David M. 1993. Image, reputation and mass communication effects. In Image und PR. Belfast: VS Verlag für Sozialwissenschaften, pp. 227–50. [Google Scholar]

- Drutman, Lee. 2015. The Business of America is Lobbying: How Corporations Became Politicized and Politics Became More Corporate. Oxford: Oxford University Press. [Google Scholar]

- Faccio, Mara, Ronald W. Masulis, and John J. McConnell. 2006. Political connections and corporate bailouts. The Journal of Finance 61: 2597–635. [Google Scholar] [CrossRef]

- Fan, Joseph P. H., Tak Jun Wong, and Tianyu Zhang. 2007. Politically connected CEOs, corporate governance and Post-IPO performance of China’s newly partially privatized firms. Journal of Financial Economics 84: 330–57. [Google Scholar] [CrossRef]

- Fombrun, Charles, and Mark Shanley. 1990. What’s in a name? Reputation building and corporate strategy. Academy of Management Journal 33: 233–58. [Google Scholar]

- Fraser, Donald R., Hao Zhang, and Chek Derashid. 2006. Capital structure and political patronage: The case of Malaysia. Journal of Banking & Finance 30: 1291–308. [Google Scholar]

- Frynas, Jedrzej George, and Kamel Mellahi. 2003. Political risks as firm-specific (dis) advantages: Evidence on transnational oil firms in Nigeria. Thunderbird International Business Review 45: 541–65. [Google Scholar] [CrossRef]

- Fryxell, Gerald E., and Jia Wang. 1994. The fortune corporate reputation index: Reputation for what? Journal of management 20: 1–14. [Google Scholar] [CrossRef]

- Gatewood, Robert D., Mary A. Gowan, and Gary J. Lautenschlager. 1993. Corporate image, recruitment image and initial job choice decisions. Academy of Management Journal 36: 414–27. [Google Scholar]

- Gensch, Dennis H. 1978. Image-measurement segmentation. Journal of Marketing Research, 384–94. [Google Scholar] [CrossRef]

- Getz, Kathleen A. 1997. Research in corporate political action: Integration and assessment. Business & Society 36: 32–72. [Google Scholar]

- Gotsi, Manto, and Alan M. Wilson. 2001. Corporate reputation: Seeking a definition. Corporate Communications: An International Journal 6: 24–30. [Google Scholar] [CrossRef]

- Griffin, Jennifer J., and John F. Mahon. 1997. The corporate social performance and corporate financial performance debate: Twenty-five years of incomparable research. Business & Society 36: 5–31. [Google Scholar]

- Hadani, Michael, and Douglas A. Schuler. 2013. In search of El Dorado: The elusive financial returns on corporate political investments. Strategic Management Journal 34: 165–81. [Google Scholar] [CrossRef]

- Hadani, Michael, Jean-Philippe Bonardi, and Nicolas M. Dahan. 2017. Corporate political activity, public policy uncertainty and firm outcomes: A meta-analysis. Strategic Organization 15: 338–66. [Google Scholar] [CrossRef]

- Hall, Marshall, and Leonard Weiss. 1967. Firm size and profitability. The Review of Economics and Statistics 49: 319–31. [Google Scholar] [CrossRef]

- Hansen, Randall, and Jobst Koehler. 2005. Issue definition, political discourse and the politics of nationality reform in France and Germany. European Journal of Political Research 44: 623–44. [Google Scholar] [CrossRef]

- Hansen, Wendy L., and Neil J. Mitchell. 2000. Disaggregating and explaining corporate political activity: Domestic and foreign corporations in national politics. American Political Science Review 94: 891–903. [Google Scholar] [CrossRef]

- Hart, David M. 2004. “Business” Is Not an Interest Group: On the Study of Companies in American National Politics. Annual Review of Political Science 7: 47–69. [Google Scholar] [CrossRef]

- Harvey, Campbell R., Karl V. Lins, and Andrew H. Roper. 2004. The effect of capital structure when expected agency costs are extreme. Journal of Financial Economics 74: 3–30. [Google Scholar] [CrossRef]

- Hawkins, Angus. 1998. British Party Politics, 1852–1886. London: Macmillan International Higher Education. [Google Scholar]

- Henisz, Witold J., and Bennet A. Zelner. 2003. The strategic organization of political risks and opportunities. Strategic Organization 1: 451–60. [Google Scholar] [CrossRef]

- Hermalin, Benjamin E., and Michael S. Weisbach. 1998. Endogenously chosen boards of directors and their monitoring of the CEO. The American Economic Review 88: 96–118. [Google Scholar]

- Hersch, Philip, Jeffry M. Netter, and Christopher Pope. 2008. Do campaign contributions and lobbying expenditures by firms create “political” capital? Atlantic Economic Journal 36: 395–405. [Google Scholar] [CrossRef]

- Hillman, Amy J. 2005. Politicians on the board of directors: Do connections affect the bottom line? Journal of Management 31: 464–81. [Google Scholar] [CrossRef]

- Hillman, Amy J., and Michael A. Hitt. 1999. Corporate political strategy formulation: A model of approach, participation and strategy decisions. Academy of Management Review 24: 825–42. [Google Scholar] [CrossRef]

- Hillman, Amy J., Gerald D. Keim, and Douglas Schuler. 2004. Corporate political activity: A review and research agenda. Journal of Management 30: 837–57. [Google Scholar] [CrossRef]

- Holtz-Eakin, Douglas, Whitney Newey, and Harvey S. Rosen. 1988. Estimating vector autoregressions with panel data. Econometrica: Journal of the Econometric Society 56: 1371–95. [Google Scholar] [CrossRef]

- Hull, Clyde Eiríkur, and Sandra Rothenberg. 2008. Firm performance: The interactions of corporate social performance with innovation and industry differentiation. Strategic Management Journal 29: 781–89. [Google Scholar] [CrossRef]

- Imai, Masami. 2006. Mixing family business with politics in Thailand. Asian Economic Journal 20: 241–56. [Google Scholar] [CrossRef]

- Insead, Laurence Capron, and Olivier Chatain. 2008. Competitors’ resource-oriented strategies: Acting on competitors’ resources through interventions in factor markets and political markets. Academy of Management Review 33: 97–121. [Google Scholar] [CrossRef]

- Johnson, Simon, and Todd Mitton. 2003. Cronyism and capital controls: Evidence from Malaysia. Journal of Financial Economics 67: 351–82. [Google Scholar] [CrossRef]

- Keillor, Bruce D., Timothy J. Wilkinson, and Deborah Owens. 2005. Threats to international operations: Dealing with political risk at the firm level. Journal of Business Research 58: 629–35. [Google Scholar] [CrossRef]

- Keim, Gerald. 2001. Managing business political activities in the USA: Bridging between theory and practice. Journal of Public Affairs: An International Journal 1: 362–75. [Google Scholar] [CrossRef]

- Keim, Gerald D., and Carl P. Zeithaml. 1986. Corporate political strategy and legislative decision making: A review and contingency approach. Academy of Management Review 11: 828–43. [Google Scholar] [CrossRef]

- Kerr, William R., William F. Lincoln, and Prachi Mishra. 2014. The dynamics of firm lobbying. American Economic Journal: Economic Policy 6: 343–79. [Google Scholar]

- Khwaja, Asim Ijaz, and Atif Mian. 2005. Do lenders favor politically connected firms? Rent provision in an emerging financial market. The Quarterly Journal of Economics 120: 1371–411. [Google Scholar] [CrossRef]

- Kim, Yonghwan, Hsuan-Ting Chen, and Homero Gil De Zúñiga. 2013. Stumbling upon news on the Internet: Effects of incidental news exposure and relative entertainment use on political engagement. Computers in Human Behavior 29: 2607–14. [Google Scholar] [CrossRef]

- Kolk, Ans, and David Levy. 2001. Winds of Change: Corporate Strategy, Climate change and Oil Multinationals. European Management Journal 19: 501–9. [Google Scholar] [CrossRef]

- Kroszner, Randall S., and Thomas Stratmann. 2005. Corporate campaign contributions, repeat giving and the rewards to legislator reputation. The Journal of law and Economics 48: 41–71. [Google Scholar] [CrossRef]

- Lee, Seung-Hyun, and David H. Weng. 2013. Does bribery in the home country promote or dampen firm exports? Strategic Management Journal 34: 1472–87. [Google Scholar] [CrossRef]

- Lev, Baruch, Christine Petrovits, and Suresh Radhakrishnan. 2010. Is doing good good for you? How corporate charitable contributions enhance revenue growth. Strategic Management Journal 31: 182–200. [Google Scholar] [CrossRef]

- Levy, David L., and Daniel Egan. 2003. A neo-Gramscian approach to corporate political strategy: Conflict and accommodation in the climate change negotiations. Journal of Management Studies 40: 803–29. [Google Scholar] [CrossRef]

- Lin, Woon Leong. 2019. Do Firm’s Organisational Slacks Influence the Relationship between Corporate Lobbying and Corporate Financial Performance? More Is Not Always Better. International Journal of Financial Studies 7: 1–23. [Google Scholar] [CrossRef]

- Lin, Woon, Jo Ho, and Murali Sambasivan. 2019. Impact of Corporate Political Activity on the Relationship between Corporate Social Responsibility and Financial Performance: A Dynamic Panel Data Approach. Sustainability 11: 60. [Google Scholar] [CrossRef]

- Loudon, David, and Albert Della-Bitta. 1993. Consumer Behavior, 4th ed. New York: McGraw-Hil Inc. [Google Scholar]

- Love, E. Geoffrey, and Matthew Kraatz. 2009. Character, conformity, or the bottom line? How and why downsizing affected corporate reputation. Academy of Management Journal 52: 314–35. [Google Scholar] [CrossRef]

- Lux, Sean, T. Russell Crook, and David J. Woehr. 2011. Mixing business with politics: A meta-analysis of the antecedents and outcomes of corporate political activity. Journal of Management 37: 223–47. [Google Scholar] [CrossRef]

- Lyon, Thomas P., and John W. Maxwell. 2008. Corporate social responsibility and the environment: A theoretical perspective. Review of Environmental Economics and Policy 2: 240–60. [Google Scholar] [CrossRef]

- Mahon, John F. 2002. Corporate reputation: Research agenda using strategy and stakeholder literature. Business & Society 41: 415–45. [Google Scholar]

- Margolis, Joshua D., Hillary Anger Elfenbein, and James P. Walsh. 2009. Does It Pay to Be Good ... and Does It Matter? A Meta-Analysis of the Relationship between Corporate Social and Financial Performance. Available online: https://ssrn.com/abstract=1866371 or http://dx.doi.org/10.2139/ssrn.1866371. (accessed on 10 June 2018).

- Mathis, Sarah M. 2007. The Politics of Land Reform: Tenure and Political Authority in Rural Kwazulu-Natal. Journal of Agrarian Change 7: 99–120. [Google Scholar] [CrossRef]

- McGuire, Jean B., Alison Sundgren, and Thomas Schneeweis. 1988. Corporate social responsibility and firm financial performance. Academy of Management Journal 31: 854–72. [Google Scholar]

- McWilliams, Abagail, and Donald Siegel. 2001. Corporate social responsibility: A theory of the firm perspective. Academy of Management Review 26: 117–27. [Google Scholar] [CrossRef]

- Nye, Joseph S., Jr. 2004. Soft Power: The Means to Success in World Politics. New York: Public Affairs. [Google Scholar]

- Okhmatovskiy, Ilya. 2010. Performance implications of ties to the government and SOEs: A political embeddedness perspective. Journal of Management Studies 47: 1020–47. [Google Scholar] [CrossRef]

- Oliver, Christine, and Ingo Holzinger. 2008. The effectiveness of strategic political management: A dynamic capabilities framework. Academy of Management Review 33: 496–520. [Google Scholar] [CrossRef]

- Orlitzky, Marc, Frank L. Schmidt, and Sara L. Rynes. 2003. Corporate social and financial performance: A meta-analysis. Organization Studies 24: 403–41. [Google Scholar] [CrossRef]

- Peloza, John. 2009. The challenge of measuring financial impacts from investments in corporate social performance. Journal of Management 35: 1518–41. [Google Scholar] [CrossRef]

- Rajwani, Tazeeb, and Tahiru Azaaviele Liedong. 2015. Political activity and firm performance within nonmarket research: A review and international comparative assessment. Journal of World Business 50: 273–83. [Google Scholar] [CrossRef]

- Rehbein, Kathleen, and Douglas A. Schuler. 2015. Linking corporate community programs and political strategies: A resource-based view. Business & Society 54: 794–821. [Google Scholar]

- Rehbein, K. A., D. A. Schuler, and J. P. Doh. 2005. Firm political capital: A social network perspective. In Academy of Management Annual Meeting, Honolulu, Hawaii, August. Honolulu: Based on Manuscript, vol. 12, p. 2005. [Google Scholar]

- Richter, Brian Kelleher, Krislert Samphantharak, and Jeffrey F. Timmons. 2009. Lobbying and taxes. American Journal of Political Science 53: 893–909. [Google Scholar] [CrossRef]

- Roberts, John. 1990. Postmodernism, Politics and Art. Manchester: Manchester University Press. [Google Scholar]

- Roodman, David. 2009. How to do xtabond2: An introduction to difference and system GMM in Stata. The Stata Journal 9: 86–136. [Google Scholar] [CrossRef]

- Rudy, Bruce C., and Jason Cavich. 2017. Nonmarket Signals: Investment in Corporate Political Activity and the Performance of Initial Public Offerings. Business & Society. [Google Scholar] [CrossRef]

- Schuler, Douglas A., Kathleen Rehbein, and Roxy D. Cramer. 2002. Pursuing strategic advantage through political means: A multivariate approach. Academy of Management Journal 45: 659–72. [Google Scholar]

- Schwaiger, Manfred. 2004. Components and parameters of corporate reputation. Schmalenbach Business Review 56: 46–71. [Google Scholar] [CrossRef]

- Simpson, W. Gary, and Theodor Kohers. 2002. The link between corporate social and financial performance: Evidence from the banking industry. Journal of Business Ethics 35: 97–109. [Google Scholar] [CrossRef]

- Snyder, Richard. 1992. Explaining transitions from neopatrimonial dictatorships. Comparative Politics 24: 379–99. [Google Scholar] [CrossRef]

- Stigler, George J. 1971. The theory of economic regulation. The Bell Journal of Economics and Management Science 2: 3–21. [Google Scholar] [CrossRef]

- Stulz, René M. 1990. Managerial discretion and optimal financing policies. Journal of Financial Economics 26: 3–27. [Google Scholar] [CrossRef]

- Sun, Pei, Kamel Mellahi, and Mike Wright. 2012. The contingent value of corporate political ties. Academy of Management Perspectives 26: 68–82. [Google Scholar] [CrossRef]

- Tu, G., B. Lin, and F. Liu. 2013. Political connections and privatization: Evidence from China. Journal of Accounting and Public Policy 32: 114–35. [Google Scholar] [CrossRef]

- Unsal, Omer, M. Kabir Hassan, and Duygu Zirek. 2016. Corporate lobbying, CEO political ideology and firm performance. Journal of Corporate Finance 38: 126–49. [Google Scholar] [CrossRef]

- Waisman, Maya, Pengfei Ye, and Yun Zhu. 2015. The effect of political uncertainty on the cost of corporate debt. Journal of Financial Stability 16: 106–17. [Google Scholar] [CrossRef]

- Wang, Chia-Jane. 2015. Instrumental variables approach to correct for endogeneity in finance. In Handbook of Financial Econometrics and Statistics. New York: Springer, pp. 2577–600. [Google Scholar]

- Wesseling, J. H., J. C. M. Farla, and M. P. Hekkert. 2015. Exploring car manufacturers’ responses to technology-forcing regulation: The case of California’s ZEV mandate. Environmental Innovation and Societal Transitions 16: 87–105. [Google Scholar]

- Windmeijer, Frank. 2005. A finite sample correction for the variance of linear efficient two-step GMM estimators. Journal of Econometrics 126: 25–51. [Google Scholar] [CrossRef]

- Wu, Wenfeng, Chongfeng Wu, Chunyang Zhou, and Jun Wu. 2012. Political connections, tax benefits and firm performance: Evidence from China. Journal of Accounting and Public Policy 31: 277–300. [Google Scholar] [CrossRef]

| 1 | See detail of methodology, please visit: http://fortune.com/worlds-most-admired-companies/list/. |

| 2 | See (Arellano and Bond 1991; Blundell and Bond 1998) for more details about the estimation procedure used in the initial System GMM estimation. |

| 3 |

{kind=link}

{kind=link}

{kind=link}

| Variable | Unit of Measurement | Obs | Mean | Std. Dev | Min | Max |

|---|---|---|---|---|---|---|

| ROA | Net income before extraordinary items to a total asset of the firm | 1000 | 6.001 | 5.841 | −30.491 | 40.270 |

| ROE | Net income before extraordinary items to total equity of firm | 1000 | 12.357 | 33.223 | −201.090 | 227.880 |

| ln CPA | Log of the total amount of lobbying to total net sales of the firm | 1000 | 8.429 | 1.834 | −2.323 | 11.635 |

| CP | Reputation scores from 0 to 10 | 1000 | 7.789 | 0.702 | 5.210 | 9.800 |

| Leverage | Long-term debt of firms to their total equity | 1000 | 5.267 | 28.596 | 2.120 | 91.210 |

| Free Cash | Free cash flow to the total of sales | 1000 | 8.510 | 16.558 | −218.360 | 241.110 |

| Advertising | Advertising expenses to total net sales of firm | 1000 | 11.284 | 14.107 | 0.268 | 108.480 |

| ln Total Assets | Log of total asset of the firm | 1000 | 11.470 | 1.267 | 7.382 | 12.632 |

| ln Revenue | Log of total net sales of firm | 1000 | 11.157 | 1.206 | 4.121 | 13.095 |

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | |

|---|---|---|---|---|---|---|---|---|---|

| ROA | 1 | ||||||||

| ROE | 0.5158 | 1 | |||||||

| ln CPA | 0.1429 | 0.1391 | 1 | ||||||

| CP | 0.2546 | 0.0469 | 0.1841 | 1 | |||||

| Leverage | −0.0414 | 0.5407 | 0.0643 | −0.0287 | 1 | ||||

| Free cash | 0.2115 | 0.0540 | 0.0208 | 0.1137 | −0.0301 | 1 | |||

| Advertising | 0.0487 | 0.0182 | −0.0384 | −0.0246 | 0.0503 | 0.0128 | 1 | ||

| ln Total Assets | −0.1435 | −0.0378 | 0.3271 | 0.0753 | 0.0413 | 0.1248 | 0.0225 | 1 | |

| ln Revenue | 0.0290 | 0.0648 | 0.3257 | 0.1687 | 0.0808 | −0.0509 | −0.2130 | 0.6866 | 1 |

| Static | Dynamic | ||||

|---|---|---|---|---|---|

| Variables | Pooled OLS | Fixed Effect | Pooled OLS | Fixed Effect | System GMM |

| ROAt−1 | 0.563 *** | 0.245 *** | 0.278 *** | ||

| (0.0355) | (0.0369) | (0.1680) | |||

| ln CPA | 0.458 *** | 0.178 | 0.234 | −0.298 | −0.209 |

| (0.0829) | (0.287) | (0.0478) | (0.287) | (0.186) | |

| Leverage | −0.00879 * | −0.00471 | −0.00247 | −0.00413 | −0.000831 |

| (0.00387) | (0.00530) | (0.00506) | (0.00289) | (0.0000889) | |

| Free Cash | 0.00846 *** | 0.0184 ** | 0.0234 *** | 0.0212 | 0.0132 |

| (0.00869) | (0.00787) | (0.00817) | (0.00872) | (0.0221) | |

| Advertising | 0.0276 | −0.178 *** | 0.00753 | −0.231 *** | −0.167 |

| (0.0171) | (0.0265) | (0.00897) | (0.0534) | (0.0966) | |

| ln Total Assets | −1.752 *** | −3.124 *** | −0.763 *** | −5.264 *** | −3.245 *** |

| (0.213) | (0.548) | (0.243) | (0.789) | (1.458) | |

| ln Revenue | 1.205 *** | 2.899 *** | 0.356 ** | 6.709 *** | 4.153 ** |

| (0.291) | (0.641) | (0.245) | (0.763) | (1.745) | |

| Year Dummy | Yes | Yes | Yes | Yes | Yes |

| Constant | 4.891 ** | 12.879 ** | 1.874 | −11.453 * | 58.642 |

| (1.924) | (5.789) | (1.991) | (6.324) | (10.841) | |

| Observation | 1000 | 1000 | 1000 | 1000 | 1000 |

| Number of Firms | 100 | 100 | 100 | ||

| Number of Instruments | 22 | ||||

| AR(1) | −3.17 (0.001) | ||||

| AR(2) | −0.14 (0.756) | ||||

| Hansen Test | 48.37 (0.178) | ||||

| Different-in-Hansen Test | 6.45 (0.265) | ||||

| Dynamic | |||

|---|---|---|---|

| Variables | Model 1 | Model 2 | Model 3 |

| ROAt−1 | 0.247 *** | 0.187 *** | 0.212 *** |

| (0.0415) | (0.0229) | (0.0624) | |

| ln CPA | −0.245 | −5.591 ** | |

| (0.577) | (2.415) | ||

| CP*CPA | −0.899 ** | ||

| (0.579) | |||

| CP | 0.235 | 0.475 * | 7.598 ** |

| (0.263) | (0.345) | (3.863) | |

| Leverage | −0.00247 | −0.00413 | −0.000831 |

| (0.00506) | (0.00289) | (0.0000889) | |

| Free Cash | −0.000897 | −0.000458 | −0.000558 |

| (0.00144) | (0.00143) | (0.000331) | |

| Advertising | −0.223 *** | −0.241 *** | −0.351 *** |

| (0.0504) | (0.0507) | (0.0578) | |

| ln Total Assets | −2.863 *** | −2.254 *** | −5.265 *** |

| (0.443) | (0.669) | (1.878) | |

| ln Revenue | 4.356 *** | 5.709 *** | 4.153 ** |

| (0.875) | (0.633) | (1.885) | |

| Year Dummy | Yes | Yes | Yes |

| Constant | 34.878 | 28.455 | −48.645 |

| (5.981) | (4.366) | (11.551) | |

| Observation | 1000 | 1000 | 1000 |

| Number of Firms | 100 | 100 | 100 |

| Number of Instruments | 26 | 26 | 26 |

| AR(1) | −3.45 (0.001) | −3.15 (0.003) | −3.18 (0.001) |

| AR(2) | 0.23 (0.879) | 0.55 (0.468) | −0.534 (0.856) |

| Hansen Test | 23.08 (0.325) | 40.33 (0.423) | 34.37 (0.658) |

| Different-in-Hansen Test | 7.37 (0.266) | 2.74 (0.696) | 5.45 (0.345) |

| Static | Dynamic | ||||

|---|---|---|---|---|---|

| Variables | Pooled OLS | Fixed Effect | Pooled OLS | Fixed Effect | System GMM |

| ROEt−1 | 0.574 *** | 0.267 *** | 0.348 *** | ||

| (0.0245) | (0.0289) | (0.0880) | |||

| ln CPA | 2.448 *** | 0.413 | 0.785 ** | −1.265 | 0.0578 |

| (0.599) | (1.267) | (0. 478) | (1.402) | (0.186) | |

| Leverage | 0.608 *** | 0.306 *** | −0.347 *** | −0.413 *** | −0.351 *** |

| (0.0287) | (0.0530) | (0.0406) | (0.0209) | (0.0789) | |

| Free Cash | 0.786 *** | 0.0564 | 0.0434 *** | 0.0241 | −0.0132 |

| (0.0569) | (0.0530) | (0.0417) | (0.0572) | (0.321) | |

| Advertising | 0.0287 | −0.778 *** | −0.00402 | −0.731 *** | −0.167 * |

| (0.0371) | (0.215) | (0.00567) | (0.245) | (0.156) | |

| ln Total Assets | −5.652 *** | −13.324 *** | −3.763 *** | −5.286 *** | −10.245 |

| (0.913) | (0.848) | (0.663) | (0.889) | (4.458) | |

| ln Revenue | 2.305 *** | 2.339 *** | 0.456 ** | 6.719 *** | 4.153 |

| (0.411) | (0.751) | (0.345) | (0.233) | (1.545) | |

| Year Dummy | Yes | Yes | Yes | Yes | Yes |

| Constant | −5.661 ** | 4.879 ** | 3.874 | −9.453 * | 5.642 |

| (1.874) | (6.749) | (1.131) | (6.424) | (1.821) | |

| Observation | 1000 | 1000 | 1000 | 1000 | 1000 |

| Number of Firms | 100 | 100 | 100 | ||

| Number of Instruments | 22 | ||||

| AR(1) | −3.26 (0.021) | ||||

| AR(2) | 1.84 (0.356) | ||||

| Hansen Test | 53.37 (0.138) | ||||

| Different-in-Hansen Test | 4.45 (0.165) | ||||

| Dynamic | |||

|---|---|---|---|

| Variables | Model 1 | Model 2 | Model 3 |

| ROEt−1 | 0.327 *** | 0.387 *** | 0.289 *** |

| (0.00455) | (0.00429) | (0.0124) | |

| ln CPA | −0.233 | −6.531 *** | |

| (0.427) | (0.615) | ||

| CP*CPA | −0.877 *** | ||

| (0.899) | |||

| CP | 0.455 | 1.475 * | 5.598 ** |

| (0.243) | (0.445) | (0.893) | |

| Leverage | 0.237 *** | 0.423 *** | 0.731 *** |

| (0.00406) | (0.00349) | (0.00759) | |

| Free Cash | −0.0297 | −0.0558 | −0.0358 |

| (0.0644) | (0.0343) | (0.0431) | |

| Advertising | −0.403 *** | −0.751 *** | −0.341 *** |

| (0.1104) | (0.3507) | (0.0478) | |

| ln Total Assets | −4.763 *** | −2.789 *** | −5.532 *** |

| (0.533) | (0.579) | (1.228) | |

| ln Revenue | 5.356 | 5.219 | 3.153 * |

| (0.445) | (0.433) | (1.855) | |

| Year Dummy | Yes | Yes | Yes |

| Constant | 29.898 | 18.456 | -28.345 |

| (3.981) | (3.366) | (1.451) | |

| Observation | 1000 | 1000 | 1000 |

| Number of Firms | 100 | 100 | |

| Number of Instruments | 26 | 26 | 26 |

| AR(1) | −2.45 (0.011) | −3.25 (0.002) | −3.38 (0.000) |

| AR(2) | 0.33 (0.869) | 0.55 (0.488) | −0.434 (0.846) |

| Hansen Test | 13.08 (0.625) | 10.13 (0.523) | 14.37 (0.768) |

| Different-in-Hansen Test | 2.37 (0.366) | 2.44 (0.696) | 3.45 (0.345) |

© 2019 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lin, W.L. Is Corporate Political Activity an Investment or Agency? An Application of System GMM Approach. Adm. Sci. 2019, 9, 5. https://doi.org/10.3390/admsci9010005

Lin WL. Is Corporate Political Activity an Investment or Agency? An Application of System GMM Approach. Administrative Sciences. 2019; 9(1):5. https://doi.org/10.3390/admsci9010005

Chicago/Turabian StyleLin, Woon Leong. 2019. "Is Corporate Political Activity an Investment or Agency? An Application of System GMM Approach" Administrative Sciences 9, no. 1: 5. https://doi.org/10.3390/admsci9010005

APA StyleLin, W. L. (2019). Is Corporate Political Activity an Investment or Agency? An Application of System GMM Approach. Administrative Sciences, 9(1), 5. https://doi.org/10.3390/admsci9010005