ESG Scores as Indicators of Green Business Strategies and Their Impact on Financial Performance in Tourism Services: Evidence from Worldwide Listed Firms

Abstract

1. Introduction

- Estimation of the impact of the environmental dimension on financial performance.

- Evaluation of the effect of the social dimension on financial performance.

- Investigation of the relationship between the governance dimension and financial performance.

2. Literature Review

2.1. ESG Reporting and Sustainability Policy Frameworks

2.2. Environmental Pillar and Financial Performance in Tourism

2.3. Social Pillar and Financial Performance in Tourism

2.4. Governance Pillar and Financial Performance in Tourism

2.5. Effect of ESG Controversies on Financial Performance

2.6. Effect of Overall ESG Combined Score on Financial Performance

3. Methodology

3.1. Data and Sample

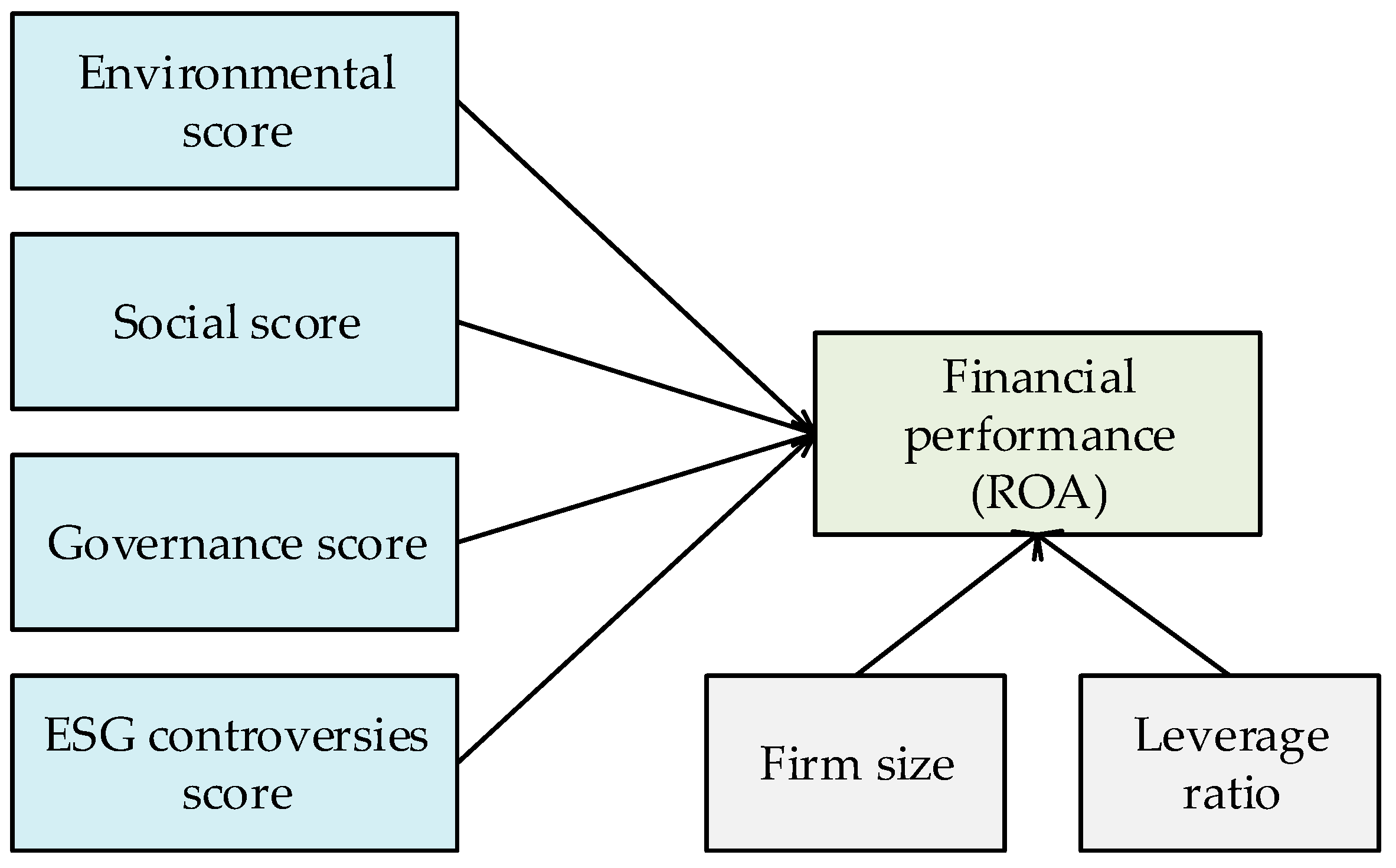

3.2. Variable Definitions and Model

3.2.1. Dependent Variable

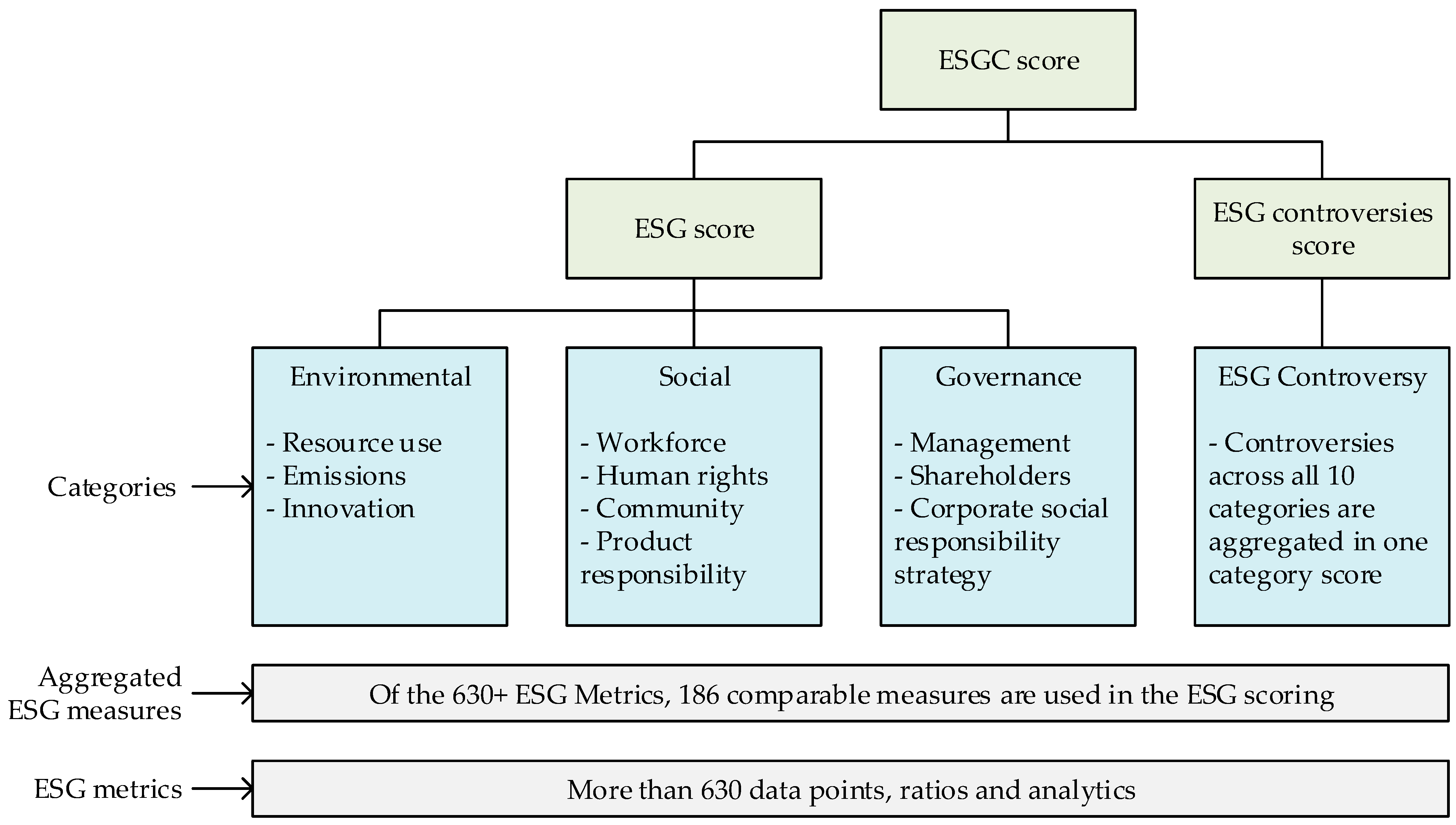

3.2.2. Explanatory Variable (ESG)

3.2.3. Control Variables

3.2.4. Model

4. Results and Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Ahmad, H., Yaqub, M., & Lee, S. H. (2023). Environmental-, social-, and governance-related factors for business investment and sustainability: A scientometric review of global trends. Environment, Development and Sustainability, 26(2), 2965–2987. [Google Scholar] [CrossRef] [PubMed]

- Ahmad, N., Mobarek, A., & Roni, N. N. (2021). Revisiting the impact of ESG on financial performance of FTSE350 UK firms: Static and dynamic panel data analysis. Cogent Business & Management, 8(1), 1900500. [Google Scholar]

- Ahmadi, A. (2024). The effect of ESG controversies on the sustainable investment. Energy Research Letters, 6. [Google Scholar] [CrossRef]

- Al Amosh, H., & Khatib, S. F. A. (2023). ESG performance in the time of COVID-19 pandemic: Cross-country evidence. Environmental Science and Pollution Research, 30(14), 39978–39993. [Google Scholar] [CrossRef]

- Alareeni, B. A., & Hamdan, A. (2020). ESG impact on performance of US S&P 500-listed firms. Corporate Governance: The International Journal of Business in Society, 20(7), 1409–1428. [Google Scholar]

- Aouadi, A., & Marsat, S. (2018). Do ESG controversies matter for firm value? Evidence from international data. Journal of Business Ethics, 151, 1027–1047. [Google Scholar] [CrossRef]

- Arbelo, A., Arbelo-Pérez, M., De Vera, V., & Bilgihan, A. (2025). Green premiums: Assessing the revenue impact of eco-certification in the hospitality sector. International Journal of Contemporary Hospitality Management, 37(13), 64–83. [Google Scholar] [CrossRef]

- Aydoğmuş, M., Gülay, G., & Ergun, K. (2022). Impact of ESG performance on firm value and profitability. Borsa Istanbul Review, 22, S119–S127. [Google Scholar] [CrossRef]

- Bae, J.-H. (2022). Developing ESG evaluation guidelines for the tourism sector: With a focus on the hotel industry. Sustainability, 14(24), 16474. [Google Scholar] [CrossRef]

- Baum, T., Cheung, C., Kong, H., Kralj, A., Mooney, S., Nguyễn Thị Thanh, H., Ramachandran, S., Dropulić Ružić, M., & Siow, M. L. (2016). Sustainability and the tourism and hospitality workforce: A thematic analysis. Sustainability, 8(8), 809. [Google Scholar] [CrossRef]

- Baumüller, J., & Grbenic, S. (2021). Moving from non-financial to sustainability reporting: Analyzing the EU Commission’s proposal for a Corporate Sustainability Reporting Directive (CSRD). Facta Universitatis, Series: Economics and Organization, 18(4), 369–381. [Google Scholar] [CrossRef]

- Baumüller, J., & Sopp, K. (2022). Double materiality and the shift from non-financial to European sustainability reporting: Review, outlook and implications. Journal of Applied Accounting Research, 23(1), 8–28. [Google Scholar] [CrossRef]

- Becker-Olsen, K. L., Cudmore, B. A., & Hill, R. P. (2006). The impact of perceived corporate social responsibility on consumer behavior. Journal of Business Research, 59(1), 46–53. [Google Scholar] [CrossRef]

- Bodhanwala, S., & Bodhanwala, R. (2022). Exploring relationship between sustainability and firm performance in travel and tourism industry: A global evidence. Social Responsibility Journal, 18(7), 1251–1269. [Google Scholar] [CrossRef]

- Breijer, R., & Orij, R. P. (2022). The comparability of non-financial information: An exploration of the impact of the non-financial reporting directive (NFRD, 2014/95/EU). Accounting in Europe, 19(2), 332–361. [Google Scholar] [CrossRef]

- Buallay, A. (2019). Is sustainability reporting (ESG) associated with performance? Evidence from the European banking sector. Management of Environmental Quality: An International Journal, 30(1), 98–115. [Google Scholar] [CrossRef]

- Carnini Pulino, S., Ciaburri, M., Magnanelli, B. S., & Nasta, L. (2022). Does ESG disclosure influence firm performance? Sustainability, 14(13), 7595. [Google Scholar] [CrossRef]

- Cerciello, M., Busato, F., & Taddeo, S. (2023). The effect of sustainable business practices on profitability. Accounting for strategic disclosure. Corporate Social Responsibility and Environmental Management, 30(2), 802–819. [Google Scholar] [CrossRef]

- Chen, S., Song, Y., & Gao, P. (2023). Environmental, social, and governance (ESG) performance and financial outcomes: Analyzing the impact of ESG on financial performance. Journal of Environmental Management, 345, 118829. [Google Scholar] [CrossRef]

- Cheng, B., Ioannou, I., & Serafeim, G. (2014). Corporate social responsibility and access to finance. Strategic Management Journal, 35(1), 1–23. [Google Scholar] [CrossRef]

- Cicchiello, A. F., Marrazza, F., & Perdichizzi, S. (2023). Non-financial disclosure regulation and environmental, social, and governance (ESG) performance: The case of EU and US firms. Corporate Social Responsibility and Environmental Management, 30(3), 1121–1128. [Google Scholar] [CrossRef]

- Delegkos, A. E., Skordoulis, M., Kalantonis, P., & Xanthopoulou, A. (2022). Integrated reporting and value relevance in the energy sector: The case of European listed firms. Energies, 15(22), 8435. [Google Scholar] [CrossRef]

- Demiraj, R., Dsouza, S., & Demıraj, E. (2023). ESG scores relationship with firm performance: Panel data evidence from the European tourism industry. PressAcademia Procedia, 16(1), 116–120. [Google Scholar] [CrossRef]

- Dhaliwal, D. S., Li, O. Z., Tsang, A., & Yang, Y. G. (2011). Voluntary nonfinancial disclosure and the cost of equity capital: The initiation of corporate social responsibility reporting. The Accounting Review, 86(1), 59–100. [Google Scholar] [CrossRef]

- Dogru, T., Akyildirim, E., Cepni, O., Ozdemir, O., Sharma, A., & Yilmaz, M. H. (2022). The effect of environmental, social and governance risks. Annals of Tourism Research, 95, 103432. [Google Scholar] [CrossRef]

- Dolmans, M., Bourguignon, G., Cibrario Assereto, C., & Dictus, T. (2021). From ‘non-financial’ to ‘sustainability’ reporting. Cleary Gottlieb. Available online: https://www.clearygottlieb.com/-/media/files/alert-memos-2021/the-corporate-sustainability-reporting-directive.pdf (accessed on 10 April 2025).

- Dorfleitner, G., Kreuzer, C., & Sparrer, C. (2020). ESG controversies and controversial ESG: About silent saints and small sinners. Journal of Asset Management, 21(5), 393–412. [Google Scholar] [CrossRef]

- Drosos, D., & Skordoulis, M. (2018). The role of environmental responsibility in tourism. Journal for International Business and Entrepreneurship Development, 11(1), 30–39. [Google Scholar] [CrossRef]

- Epps, R. W., & Cereola, S. J. (2008). Do institutional shareholder services (ISS) corporate governance ratings reflect a company’s operating performance? Critical Perspectives on Accounting, 19(8), 1135–1148. [Google Scholar] [CrossRef]

- European Union. (2014). Directive 2014/95/EU as regards disclosure of non-financial and diversity information by certain large undertakings and groups. Official Journal of the European Union. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/HTML/?uri=CELEX:32014L0095&from=EN (accessed on 8 February 2025).

- European Union. (2022). Directive 2022/2464 as regards corporate sustainability reporting. Official Journal of the European Union. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/HTML/?uri=CELEX:32022L2464 (accessed on 8 February 2025).

- Filimonau, V., Matute, J., Mika, M., Kubal-Czerwińska, M., Krzesiwo, K., & Pawłowska-Legwand, A. (2022). Predictors of patronage intentions towards ‘green’ hotels in an emerging tourism market. International Journal of Hospitality Management, 103, 103221. [Google Scholar] [CrossRef]

- Font, X., Garay, L., & Jones, S. (2016). Sustainability motivations and practices in small tourism enterprises in European protected areas. Journal of Cleaner Production, 137, 1439–1448. [Google Scholar] [CrossRef]

- Freeman, R. E. (1984). Strategic management: A stakeholder approach. Pitman. [Google Scholar]

- Friede, G., Busch, T., & Bassen, A. (2015). ESG and financial performance: Aggregated evidence from more than 2000 empirical studies. Journal of Sustainable Finance & Investment, 5(4), 210–233. [Google Scholar]

- Friedman, M. (1970, September 13). The social responsibility of business is to increase its profits. New York Times Magazine. 122–126. [Google Scholar]

- Fu, T., & Li, J. (2023). An empirical analysis of the impact of ESG on financial performance: The moderating role of digital transformation. Frontiers in Environmental Science, 11, 1256052. [Google Scholar] [CrossRef]

- Ghosh, A. (2013). Corporate sustainability and corporate financial performance: The Indian context (Working paper no. 721). Indian Institute of Management Calcutta. [Google Scholar]

- Godfrey, P. C., Merrill, C. B., & Hansen, J. M. (2009). The relationship between corporate social responsibility and shareholder value: An empirical test of the risk management hypothesis. Strategic Management Journal, 30(4), 425–445. [Google Scholar] [CrossRef]

- Habib, A. M., & Mourad, N. (2024). The influence of environmental, social, and governance (ESG) practices on US firms’ performance: Evidence from the coronavirus crisis. Journal of the Knowledge Economy, 15(1), 2549–2570. [Google Scholar] [CrossRef]

- Hair, J. F., Black, W. C., Babin, B. J., & Anderson, R. E. (2010). Multivariate data analysis (7th ed.). Pearson. [Google Scholar]

- Hassan, A. S., & Meyer, D. F. (2022). Does countries’ environmental, social and governance (ESG) risk rating influence international tourism demand? A case of the Visegrád Four. Journal of Tourism Futures, 11(1), 62–81. [Google Scholar] [CrossRef]

- Hassel, L., Nilsson, H., & Nyquist, S. (2005). The value relevance of environmental performance. European Accounting Review, 14(1), 41–61. [Google Scholar] [CrossRef]

- Igbinovia, I. M., & Agbadua, B. O. (2023). Environmental, social, and governance (ESG) reporting and firm value in Nigeria manufacturing firms: The moderating role of firm advantage. Jurnal Dinamika Akuntansi Dan Bisnis, 10(2), 149–162. [Google Scholar] [CrossRef]

- Ionescu, G. H., Firoiu, D., Pirvu, R., & Vilag, R. D. (2019). The impact of ESG factors on market value of companies from travel and tourism industry. Technological and Economic Development of Economy, 25(5), 820–849. [Google Scholar] [CrossRef]

- Isnurhadi, I., Oktarini, K. W., Meutia, I., & Mukhtaruddin, M. (2020). Effects of stakeholder engagement and corporate governance on integrated reporting disclosure. Indonesian Journal of Sustainability Accounting and Management, 4(2), 164–173. [Google Scholar] [CrossRef]

- Junius, D., Adisurjo, A., Rijanto, Y. A., & Adelina, Y. E. (2020). The impact of ESG performance to firm performance and market value. Jurnal Aplikasi Akuntansi, 5(1), 21–41. [Google Scholar] [CrossRef]

- Khan, A., Bibi, S., Li, H., Fubing, X., Jiang, S., & Hussain, S. (2023). Does the tourism and travel industry really matter to economic growth and environmental degradation in the US: A sustainable policy development approach. Frontiers in Environmental Science, 11, 1147504. [Google Scholar] [CrossRef]

- Kocherlakota, S., Aruna, C., & Sirisha Reddy, R. D. (2023). Do ESG had influence on return on investments of BRICS listed stock exchanges: An empirical study. European Journal of Military Studies, 13(2), 6000–6011. [Google Scholar]

- Leopizzi, R., Pizzi, S., & D’Addario, F. (2021). The relationship among family business, corporate governance, and firm performance: An empirical assessment in the tourism sector. Administrative Sciences, 11(1), 8. [Google Scholar] [CrossRef]

- Lewellen, J. (2004). Predicting returns with financial ratios. Journal of Financial Economics, 74(2), 209–235. [Google Scholar] [CrossRef]

- Li, J., Haider, Z. A., Jin, X., & Yuan, W. (2019). Corporate controversy, social responsibility and market performance: International evidence. Journal of International Financial Markets, Institutions and Money, 60, 1–18. [Google Scholar] [CrossRef]

- Luu, E., & Rubio, S. (2024). Millennial managers. Corporate Governance: An International Review, 32(4), 732–755. [Google Scholar] [CrossRef]

- Ma, Y., Feng, G. F., Yin, Z. J., & Chang, C. P. (2024). ESG disclosures, green innovation, and greenwashing: All for sustainable development? Sustainable Development, 33(2), 1797–1815. [Google Scholar] [CrossRef]

- Makhdalena, M., Zulvina, D., Zulvina, Y., Amelia, R. W., & Wicaksono, A. P. (2023). ESG and firm performance in developing countries: Evidence from ASEAN. Etikonomi, 22(1), 65–78. [Google Scholar] [CrossRef]

- Moneva, J. M., Bonilla-Priego, M. J., & Ortas, E. (2020). Corporate social responsibility and organisational performance in the tourism sector. Journal of Sustainable Tourism, 28(6), 853–872. [Google Scholar] [CrossRef]

- Naeem, N., Cankaya, S., & Bildik, R. (2022). Does ESG performance affect the financial performance of environmentally sensitive industries? A comparison between emerging and developed markets. Borsa Istanbul Review, 22, S128–S140. [Google Scholar] [CrossRef]

- Nirino, N., Santoro, G., Miglietta, N., & Quaglia, R. (2021). Corporate controversies and company’s financial performance: Exploring the moderating role of ESG practices. Technological Forecasting and Social Change, 162, 120341. [Google Scholar] [CrossRef]

- Ohlson, J. A. (1995). Earnings, book values, and dividends in equity valuation. Contemporary Accounting Research, 11(2), 661–687. [Google Scholar] [CrossRef]

- Oikonomou, I., Brooks, C., & Pavelin, S. (2012). The impact of corporate social performance on financial risk and utility: A longitudinal analysis. Financial Management, 41(2), 483–515. [Google Scholar] [CrossRef]

- Oklevik, O., Gössling, S., Hall, C. M., Jacobsen, J. K. S., Grøtte, I. P., & McCabe, S. (2020). Overtourism, optimisation, and destination performance indicators: A case study of activities in Fjord Norway. In Tourism and degrowth (pp. 60–80). Routledge. [Google Scholar]

- Ortiz-Martínez, E., & Marín-Hernández, S. (2024). Sustainability information in European small-and medium-sized enterprises. Journal of the Knowledge Economy, 15(2), 7497–7522. [Google Scholar] [CrossRef]

- Porter, M. E., & van der Linde, C. (1995). Toward a new conception of the environment-competitiveness relationship. Journal of Economic Perspectives, 9(4), 97–118. [Google Scholar] [CrossRef]

- Rahman, H. U., Zahid, M., & Al-Faryan, M. A. S. (2023). ESG and firm performance: The rarely explored moderation of sustainability strategy and top management commitment. Journal of Cleaner Production, 404, 136859. [Google Scholar] [CrossRef]

- Rodríguez-Fernández, M., Sánchez-Teba, E. M., López-Toro, A. A., & Borrego-Domínguez, S. (2019). Influence of ESGC indicators on financial performance of listed travel and leisure companies. Sustainability, 11(19), 5529. [Google Scholar] [CrossRef]

- Skordoulis, M., Kavoura, A., Stavropoulos, A. S., Zikas, A., & Kalantonis, P. (2025). Financial stability and environmental sentiment among millennials: A cross-cultural analysis of Greece and the Netherlands. International Journal of Financial Studies, 13(2), 64. [Google Scholar] [CrossRef]

- Skordoulis, M., Kyriakopoulos, G., Ntanos, S., Galatsidas, S., Arabatzis, G., Chalikias, M., & Kalantonis, P. (2022). The mediating role of firm strategy in the relationship between green entrepreneurship, green innovation, and competitive advantage: The case of medium and large-sized firms in Greece. Sustainability, 14(6), 3286. [Google Scholar] [CrossRef]

- Skordoulis, M., Ntanos, S., Kyriakopoulos, G. L., Arabatzis, G., Galatsidas, S., & Chalikias, M. (2020). Environmental innovation, open innovation dynamics and competitive advantage of medium and large-sized firms. Journal of Open Innovation: Technology, Market, and Complexity, 6(4), 195. [Google Scholar] [CrossRef]

- Skordoulis, M., Patsatzi, O., Kalogiannidis, S., Patitsa, C., & Papagrigoriou, A. (2024a). Strategic management of multiculturalism for social sustainability in hospitality services: The case of hotels in Athens. Tourism and Hospitality, 5(4), 977–995. [Google Scholar] [CrossRef]

- Skordoulis, M., Stavropoulos, A. S., Papagrigoriou, A., & Kalantonis, P. (2024b). The strategic impact of service quality and environmental sustainability on financial performance: A case study of 5-star hotels in Athens. Journal of Risk and Financial Management, 17(10), 473. [Google Scholar] [CrossRef]

- Sotiropoulos, M., Skordoulis, M., Kalantonis, P., & Papagrigoriou, A. (2023). The impact of board diversity on firms’ performance: The case of retail industry in Europe. In The international conference on strategic innovative marketing and tourism (pp. 787–795). Springer Nature. [Google Scholar]

- Spence, M. (1973). Job Market Signaling. The Quarterly Journal Of Economics, 87(3), 355–374. [Google Scholar] [CrossRef]

- Stavropoulos, A. S., & Zounta, S. (2025). Cash conversion cycle and profitability: Evidence from Greek service firms. Journal of Risk and Financial Management, 18(4), 208. [Google Scholar] [CrossRef]

- Sunlu, U. (2003). Environmental impacts of tourism. In D. Camarda, & L. Grassini (Eds.), Local resources and global trades: Environments and agriculture in the Mediterranean region (pp. 263–270). CIHEAM. [Google Scholar]

- Taliento, M., Favino, C., & Netti, A. (2019). Impact of environmental, social, and governance information on economic performance: Evidence of a corporate ‘sustainability advantage’ from Europe. Sustainability, 11(6), 1738. [Google Scholar] [CrossRef]

- United Nations. (2015). Transforming our world: The 2030 agenda for sustainable development. Department of Economic and Social Affairs. Available online: https://sdgs.un.org/2030agenda (accessed on 14 April 2024).

- Velte, P. (2017). Does ESG performance have an impact on financial performance? Evidence from Germany. Journal of Global Responsibility, 8(2), 169–178. [Google Scholar] [CrossRef]

- Voumik, L. C., Islam, M. A., & Nafi, S. M. (2024). Does tourism have an impact on carbon emissions in Asia? An application of fresh panel methodology. Environment, Development and Sustainability, 26(4), 9481–9499. [Google Scholar] [CrossRef]

- Wang, S., & Wang, D. (2022). Exploring the relationship between ESG performance and green bond issuance. Frontiers in Public Health, 10, 897577. [Google Scholar] [CrossRef]

- World Travel & Tourism Council (WTTC). (2022). Travel & tourism economic impact. Available online: https://wttc.org/research/economic-impact (accessed on 21 April 2024).

- Yoon, B., & Chung, Y. (2018). The effects of corporate social responsibility on firm performance: A stakeholder approach. Journal of Hospitality and Tourism Management, 37, 89–96. [Google Scholar] [CrossRef]

- Zabri, S. M., Ahmad, K., & Wah, K. K. (2016). Corporate governance practices and firm performance: Evidence from top 100 public listed companies in Malaysia. Procedia Economics and Finance, 35, 287–296. [Google Scholar] [CrossRef]

- Zahid, R. A., Saleem, A., & Maqsood, U. S. (2023). ESG performance, capital financing decisions, and audit quality: Empirical evidence from Chinese state-owned enterprises. Environmental Science and Pollution Research, 30(15), 44086–44099. [Google Scholar] [CrossRef] [PubMed]

- Zhao, J., Yang, D., Zhao, X., & Lei, M. (2023). Tourism industry and employment generation in emerging seven economies: Evidence from novel panel methods. Economic Research, 36(3), 2206471. [Google Scholar] [CrossRef]

- Zhou, Y., Li, X., & Yuen, K. F. (2023). Sustainable shipping: A critical review for a unified framework and future research agenda. Marine Policy, 148, 105478. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Country | Observations | Percentage % |

|---|---|---|

| Australia | 12 | 8% |

| Bahrain | 1 | 1% |

| Canada | 3 | 2% |

| Hong Kong | 8 | 5% |

| China | 4 | 3% |

| France | 3 | 2% |

| Germany | 1 | 1% |

| Greece | 1 | 1% |

| Ireland | 1 | 1% |

| Italy | 1 | 1% |

| Japan | 4 | 3% |

| Korea | 2 | 1% |

| Malaysia | 3 | 2% |

| Mexico | 1 | 1% |

| New Zealand | 2 | 1% |

| Philippines | 1 | 1% |

| South Africa | 5 | 3% |

| Spain | 1 | 1% |

| Sri Lanka | 1 | 1% |

| Taiwan | 1 | 1% |

| Thailand | 1 | 1% |

| United Kingdom | 15 | 10% |

| Gibraltar | 1 | 1% |

| Malta | 1 | 1% |

| United States of America | 72 | 47% |

| Macau | 3 | 2% |

| Brazil | 1 | 1% |

| Isle of Man | 2 | 1% |

| Uruguay | 1 | 1% |

| Singapore | 1 | 1% |

| Variable | Mean | Median | Std. Dev. | Minimum | Maximum |

|---|---|---|---|---|---|

| ROA | 0.021412 | 0.032191 | 0.12050 | −1.8843 | 0.38682 |

| ESG Combinde Score | 47.048 | 47.145 | 21.220 | 2.5000 | 91.130 |

| Environmental Score | 39.681 | 38.000 | 29.974 | 0.00000 | 96.000 |

| Social Score | 49.503 | 49.000 | 23.496 | 1.0000 | 97.000 |

| Governance Score | 50.646 | 50.000 | 21.590 | 5.0000 | 98.000 |

| ESG Controvercies Score | 90.623 | 100.00 | 22.399 | 1.0000 | 100.00 |

| ESG Combined Score | Environmental Score | Social Score | Governance Score | ESG Controversies Score | ROA | Leverage | Size | |

|---|---|---|---|---|---|---|---|---|

| ESG Combined Score | 1.0000 | 0.9056 | 0.9228 | 0.6822 | −0.2110 | 0.0763 | 0.0935 | 0.3993 |

| Environmental Score | 1.0000 | 0.8172 | 0.4606 | −0.2376 | 0.0439 | 0.1196 | 0.5330 | |

| Social Score | 1.0000 | 0.4619 | −0.2004 | 0.0928 | 0.0735 | 0.3601 | ||

| Governance Score | 1.0000 | −0.1396 | 0.0735 | 0.0085 | 0.0867 | |||

| ESG Controversies Score | 1.0000 | −0.0118 | −0.1480 | −0.2157 | ||||

| ROA | 1.0000 | −0.3405 | 0.0700 | |||||

| Leverage | 1.0000 | 0.1989 | ||||||

| Size | 1.0000 |

| Independent Variables and Control Variables | Coefficient | Std. Error | t-Ratio | p-Value |

|---|---|---|---|---|

| Constant | −0.0521 | 0.0265 | −1.962 | 0.0502 |

| ESG Combined Score | −0.0028 | 0.0019 | −1.432 | 0.1525 |

| Environmental Score | 0.0006 | 0.0005 | 1.068 | 0.2861 |

| Social Score | 0.0015 | 0.0009 | 1.740 | 0.0424 |

| Governance Score | 0.0009 | 0.0006 | 1.560 | 0.1192 |

| ESG Controversies Score | 0.0004 | 0.0001 | 2.584 | 0.0100 |

| Leverage | −0.0011 | 0.0003 | −3.682 | 0.0003 |

| Size | 0.0019 | 0.0019 | 0.9919 | 0.3216 |

| Independent Variables | Coefficient | Std. Error | t-Ratio | p-Value | |

|---|---|---|---|---|---|

| Model 1a | |||||

| Constant | 0.2571 | 0.0954 | 2.695 | 0.073 | *** |

| Environmental Score | −0.0014 | 0.0003 | −4.339 | <0.0001 | *** |

| Leverage | −0.0013 | 0.0003 | −4.337 | <0.0001 | *** |

| Size | −0.0210 | 0.0120 | −1.746 | 0.0814 | * |

| Within R2: 0.1003 | |||||

| Model 1b | |||||

| Constant | 0.3298 | 0.0937 | 3.519 | 0.0005 | *** |

| Social Score | −0.0013 | 0.0004 | −3.014 | 0.0027 | *** |

| Leverage | −0.0014 | 0.0003 | −4.484 | <0.0001 | *** |

| Size | −0.0291 | 0.0119 | −2.449 | 0.0147 | ** |

| Within R2: 0.082 | |||||

| Model 1c | |||||

| Constant | 0.3798 | 0.0893 | 4.250 | <0.0001 | *** |

| Governance Score | −0.0009 | 0.0004 | −2.210 | 0.0288 | ** |

| Leverage | −0.0014 | 0.0008 | −1.827 | 0.0698 | * |

| Size | −0.0374 | 0.0118 | −3.171 | 0.0019 | *** |

| Within R2: 0.079 | |||||

| Model 2 | |||||

| Constant | 0.2828 | 0.0960 | 2.945 | 0.0038 | *** |

| ESG Controversies Score | 0.0006 | 0.0001 | 4.019 | <0.0001 | *** |

| Leverage | −0.0014 | 0.0008 | −1.717 | 0.0882 | * |

| Size | −0.0386 | 0.0115 | −3.356 | 0.0010 | *** |

| Within R2: 0.089 | |||||

| Model 3 | |||||

| Constant | 0.2961 | 0.1011 | 2.927 | 0.0040 | *** |

| ESG Combined Score | −0.0021 | 0.0005 | −3.741 | 0.0003 | *** |

| Leverage | −0.0014 | 0.0007 | −1.807 | 0.0729 | * |

| Size | −0.0208 | 0.0014 | −1.466 | 0.1449 | |

| Within R2: 0.1004 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Matsali, C.; Skordoulis, M.; Papagrigoriou, A.; Kalantonis, P. ESG Scores as Indicators of Green Business Strategies and Their Impact on Financial Performance in Tourism Services: Evidence from Worldwide Listed Firms. Adm. Sci. 2025, 15, 208. https://doi.org/10.3390/admsci15060208

Matsali C, Skordoulis M, Papagrigoriou A, Kalantonis P. ESG Scores as Indicators of Green Business Strategies and Their Impact on Financial Performance in Tourism Services: Evidence from Worldwide Listed Firms. Administrative Sciences. 2025; 15(6):208. https://doi.org/10.3390/admsci15060208

Chicago/Turabian StyleMatsali, Chrysoula, Michalis Skordoulis, Aristidis Papagrigoriou, and Petros Kalantonis. 2025. "ESG Scores as Indicators of Green Business Strategies and Their Impact on Financial Performance in Tourism Services: Evidence from Worldwide Listed Firms" Administrative Sciences 15, no. 6: 208. https://doi.org/10.3390/admsci15060208

APA StyleMatsali, C., Skordoulis, M., Papagrigoriou, A., & Kalantonis, P. (2025). ESG Scores as Indicators of Green Business Strategies and Their Impact on Financial Performance in Tourism Services: Evidence from Worldwide Listed Firms. Administrative Sciences, 15(6), 208. https://doi.org/10.3390/admsci15060208