Factors Determining the Success of Decision Making and Performance of Portuguese Companies

Abstract

:1. Introduction

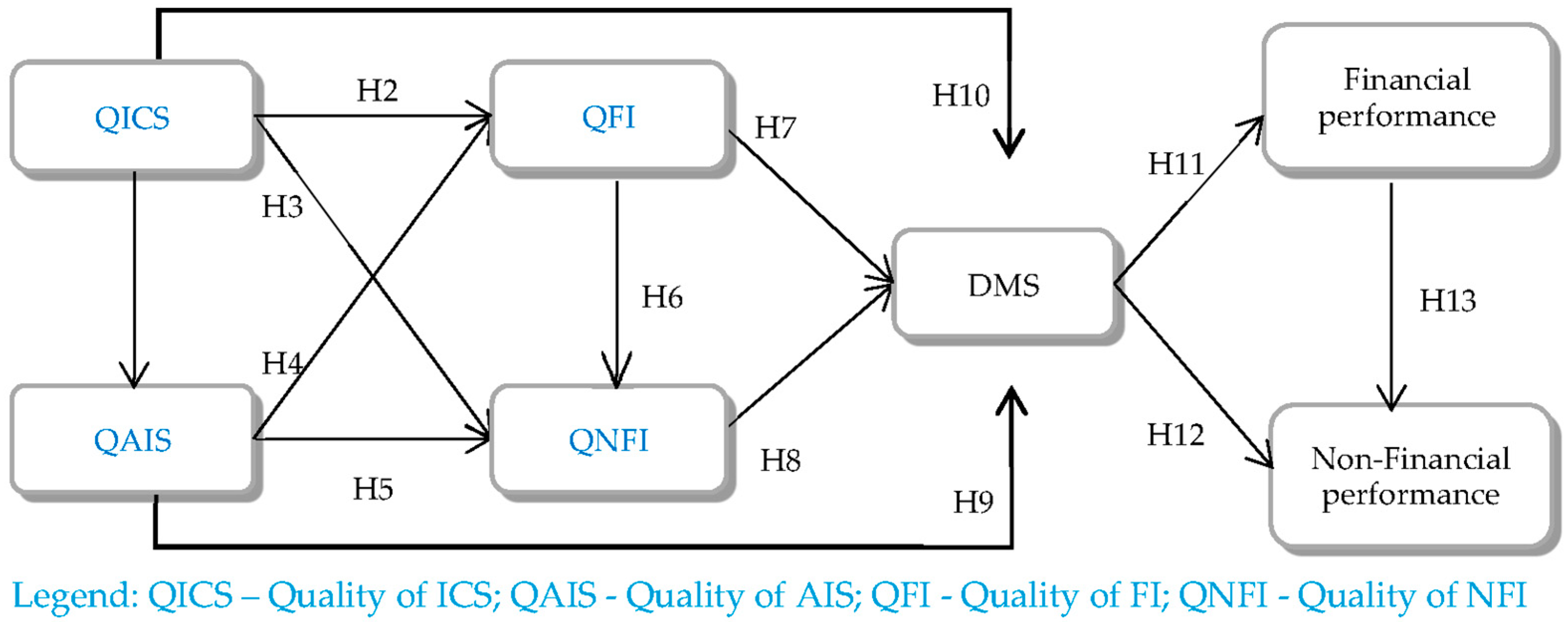

2. Theoretical Framework and Hypotheses

3. Methodology

4. Results

4.1. Assessment of the Measurement Model

4.2. Assessment of the Structural Model

4.2.1. Assessment of the Initial Structural Model

4.2.2. Assessment of the Revised Theoretical Model

4.2.3. Assessment of the Direct, Indirect, and Total Effects

4.2.4. Analysis of the Mediating Effect

5. Discussion of Results

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

| Latent Variables | Code | Measurement | Source |

|---|---|---|---|

| Quality of ICS | 1QICS | Internal control system has improved and promoted the company’s operational efficiency and effectiveness. | Phornlaphatrachakorn (2019) |

| 2QICS | Internal control system has allowed achieving firms’ business targets, goals, and objectives. | Phornlaphatrachakorn (2019) | |

| 3QICS | Internal control system has allowed building and creating effective operations, activity, and business practices. | Phornlaphatrachakorn (2019) | |

| 4QICS | Internal control system has allowed the company to prepare financial information with quality. | Adapted from Phornlaphatrachakorn (2019) | |

| 5QICS | Internal control system has allowed the company to prepare non-financial information with quality. | Adapted from Phornlaphatrachakorn (2019) | |

| 6QICS | The company complies with all required regulations, i.e., laws, rules, guidelines, standards, and other related issues within internal control quality. | Phornlaphatrachakorn (2019) | |

| 7QICS | The company’s internal control system has quality. | Pre-test | |

| Quality of AIS | 1QAIS | The automated data collection sped up the process to generate financial statements. | Adaptet from Soudani (2012) |

| 2QAIS | The current accounting information system has improved the quality of non-financial reporting. | Adaptadet from Soudani (2012) | |

| 3QAIS | Accounting information system has contributed to the integrity of the financial information reporting process. | Adaptet from Soudani (2012) | |

| 4QAIS | The accounting information system has contributed to the integrity of the non-financial information reporting process. | Adaptet from Soudani (2012) | |

| 5QAIS | The data processing caused the improvement of the quality of the financial reports. | Adaptet from Soudani (2012) | |

| 6QAIS | The automated data collection sped up the process of non-financil information preparation | Adaptadet from Soudani (2012) | |

| 7QAIS | The automated data collection sped up the process to generate financial statements and overcome human weaknesses in data processing. | Adaptet from Soudani (2012) | |

| 8QAIS | The automated data collection provides a platform with access to information, which facilitates the use of it. | Adaptet from Kpurugbara et al. (2016) | |

| 9QAIS | The company’s accounting information system works efficiently and effectively. | Pre-test | |

| Quality of FI | 1QFI | The company is distinguished by its accuracy in presenting users’ needs of financial data. | Dornier (2018) |

| 2QFI | The accuracy of financial information helps decision-making. | Dornier (2018) | |

| 3QFI | Financial information is carefully prepared to ensure its reliability | Adapted from Dornier (2018) | |

| 4QFI | The provided financial data are consistent with the users’ needs in different financial periods per year | Dornier (2018) | |

| 5QFI | Financial information is easily understood by its user. | Dornier (2018) | |

| 6QFI | Financial information is inclusive for all the financial aspects that users need in the decision-making process. | Dornier (2018) | |

| 7QFI | Financial information is provided in an appropriate time so they reach the decision maker before losing their ability to influence the taken decision. | Dornier (2018) | |

| 8QFI | Financial information represents in a reliable way what you want to portray. | Pre-test | |

| 9QFI | Financial information is free of value judgments. | Pre-test | |

| Quality of NFI | 1QNFI | The accuracy of non-financial information helps decision-making. | Adapted from Dornier (2018) |

| 2QNFI | Non-financial information is carefully prepared to ensure its quality | Adapted from Dornier (2018) | |

| 3QNFI | Non-financial information is easily understood by its user. | Adapted from Dornier (2018) | |

| 4QNFI | Non-financial information includes all the information necessary to make decisions. | Adapted from Dornier (2018) | |

| 5QNFI | Non-financial information is free of value judgements. | Pre-test | |

| Decision Making Success | 1DMS | The decisions made allowed the company to achieve advantages in terms of operations, management and performance | Phornlaphatrachakorn (2019) |

| 2DMS | Decisions made about investments took into account different alternatives or options, which allowed the company to choose the best solution. | Phornlaphatrachakorn (2019) | |

| 3DMS | Decisions made about future operations based on best practices/trends in doing business over the long term have contributed to better performance. | Adapted from Phornlaphatrachakorn (2019) | |

| 4DMS | The decisions taken have contributed to maximized operational efficiency and effectiveness. | Phornlaphatrachakorn (2019) | |

| 5DMS | The decisions made in the company determine its success. | Pre-test | |

| Performance | In the last 5 years | ||

| Financial Performance | 1FP | The company’s turnover has increased | Trailer et al. (1996) |

| 2FP | The size of the company has increased. | Trailer et al. (1996) | |

| 3FP | The number of the company’s employees increased | Trailer et al. (1996) | |

| 4FP | The company’s operating profit has improved/increased | Trailer et al. (1996); Soudani (2012) | |

| 5FP | The company’s return on asset has improved/increased (EBIT/Total Assets). | Trailer et al. (1996); adapted from Soudani (2012) | |

| 6FP | Return on equity improved/increased (EBIT/Equity). | Trailer et al. (1996); adapted from Soudani (2012) | |

| 7FP | Profitability on sales increased (EBIT/Sales). | Adapted from Soudani (2012) | |

| 8FP | The company’s financial performance has been successful. | Pre-test | |

| Non-Financial Performance | 9NFP | The company has improved its customer service | Adapted from Soudani (2012) |

| 10NFP | The company has improved working conditions, regardless of the employee’s position. | Adapted from Soudani (2012) | |

| 11NFP | The company has improved its performance in terms of social responsibility (voluntary effort on the part of the company in the creation of various measures to meet the expectations of the different interested parties—stakeholders). | Adapted from Soudani (2012) | |

| 12NFP | The company achieved improvements in customer satisfaction. | Adapted from Soudani (2012) | |

| 13NFP | The company has increased its employee retention rates. | Adapted from Soudani (2012) | |

| 14NFP | The company has increased its customer retention rates. | Adapted from Soudani (2012) | |

| 15NFP | The company’s (non-financial) performance has been successful. | Pre-test | |

References

- Al-Wattar, Yasir Mohammed Ali, Akeel Hamza Almagtome, and Karrar Mohammed Al-Shafeay. 2019. The Role of Integrating Hotel Sustainability Reporting Practices into an Accounting Information System to Enhance Hotel Financial Performance: Evidence from Iraq. African Journal of Hospitality, Tourism and Leisure 8: 1–6. [Google Scholar]

- Anggadini, Sri Dewi. 2015. The Effect of Top Management Support and Internal Control of the Accounting Information Systems Quality and Its Implications on the Accounting Information Quality. Information Management and Business Review 7: 93–102. [Google Scholar] [CrossRef] [Green Version]

- Anh, Tu Chuc, Lan Huong Tran Thi, Huy Pham Quang, and Thuy Truong Thi. 2020. Factors Influencing the Effectiveness of Internal Control in Cement Manufacturing Companies. Management Science Letters 10: 133–42. [Google Scholar] [CrossRef]

- Arroyo, Paulina, and HEC Montreal. 2008. The Three Dimensions of a Sustainable Management Accounting System. ASAC 29: 23–39. [Google Scholar]

- Asare, Stephen Kwaku, and Arnold Wright. 2012. The Effect of Type of Internal Control Report on Users’ Confidence in the Accompanying Financial Statement Audit Report. Contemporary Accounting Research 29: 152–75. [Google Scholar] [CrossRef]

- Ayu, Putu, Yohana Putri, Dan I. Dewa, and Made Endiana. 2020. Pengaruh Sistem Informasi Akuntansi Dan Sistem Pengendalian Internal Terhadap Kinerja Perusahaan (Studi Kasus Pada Koperasi Di Kecamatan Payangan). License Jurnal KRISNA: Kumpulan Riset Akuntansi 11: 179–89. [Google Scholar] [CrossRef]

- Azizi Ismail, Noor, and Malcolm King. 2007. Factors Influencing the Alignment of Accounting Information Systems in Small and Medium Sized Malaysian Manufacturing Firms. Journal of Information Systems and Small Business Ismail & King 1: 1–20. Available online: https://ojs.deakin.edu.au/index.php/jissb/article/view/1 (accessed on 1 June 2021).

- Barker, Richard, and Robert G. Eccles. 2018. Should FASB and IASB Be Responsible for Setting Standards for Nonfinancial Information? SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Bauer, Andrew M., Darren Henderson, and Daniel P. Lynch. 2018. Supplier Internal Control Quality and the Duration of Customer-Supplier Relationships. The Accounting Review 93: 59–82. [Google Scholar] [CrossRef]

- Baugh, Matthew, Matthew S. Ege, and Christopher G. Yust. 2021. Internal Control Quality and Bank Risk-Taking and Performance. AUDITING: A Journal of Practice & Theory 40: 49–84. [Google Scholar] [CrossRef]

- Baumgartner, Hand, and Christian Homburg. 1996. Applications of structural equation modeling in marketing and consumer research: A review. International Journal of Research in Marketing 13: 139–161. [Google Scholar] [CrossRef] [Green Version]

- Bennett, Martin, Peter James, and Leon Klinkers. 2017. Sustainable Measures—Evaluation and Reporting of Environmental and Social Performance. London and New York: Routledge; Taylor & Francis Group. [Google Scholar] [CrossRef]

- Bertolami, Mariana, Rinaldo Artes, Pedro João Gonçalves, Marcos Hashimoto, and Sergio Giovanetti Lazzarini. 2018. Sobrevivência de Empresas Nascentes: Influência Do Capital Humano, Social, Práticas Gerenciais e Gênero. Revista de Administração Contemporânea 22: 311–35. [Google Scholar] [CrossRef] [Green Version]

- Bosworth, Derek L. 2005. Determinants of Enterprise Performance. Available online: https://www.google.com/books?hl=en&lr=&id=x-91bjvD7QQC&oi=fnd&pg=PR9&dq=Bosworth,+D.+L.+(2005).+Determinants+of+enterprise+performance.+In+Marco+Andre+da+Silva+Costa,+Abdelhamid+Nedzhad,+Danijela+Lucic.+Economic+and+Social+Development.+Book+of+Proceedings+of+68+th+International+Scientific+Conference+on+Economic+and+Social+Deve&ots=pCkPE6BFnf&sig=ZVVzAFOj3bLZPbU2zK5hPAQcTmA (accessed on 1 June 2021).

- Boulianne, Emilio. 2007. Revisiting Fit between AIS Design and Performance with the Analyzer Strategic-Type. International Journal of Accounting Information Systems 8: 1–16. [Google Scholar] [CrossRef]

- Bozzolan, Saverio, and Antti Miihkinen. 2019. The Quality of Mandatory Non-Financial (Risk) Disclosures: The Moderating Role of Audit Firm and Partner Characteristics. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Cepêda, Catarina, and Albertina Monteiro. 2020. The ‘Accountant’s Perception of the Usefulness of Financial Information in Decision Making—A Study in Portugal. Review of Business Management 22: 363–80. [Google Scholar] [CrossRef]

- Chen, Yi Chun, Mingyi Hung, and Yongxiang Wang. 2018. The Effect of Mandatory CSR Disclosure on Firm Profitability and Social Externalities: Evidence from China. Journal of Accounting and Economics 65: 169–90. [Google Scholar] [CrossRef]

- COSO. 2013. Internal Control—Integrated Framework: Executive Summary. Available online: https://www.coso.org/documents/990025p-executive-summary-final-may20.pdf (accessed on 1 June 2021).

- Delazer, Margarete, Laura Zamarian, Elisabeth Bonatti, Nicola Walser, Giorgi Kuchukhidze, Thomas Bodner, Thomas Benke, Florian Koppelstaetter, and Eugen Trinka. 2011. Decision Making under Ambiguity in Temporal Lobe Epilepsy: Does the Location of the Underlying Structural Abnormality Matter? Epilepsy and Behavior 20: 34–37. [Google Scholar] [CrossRef]

- Dewi, Ratmi, and Jan Hoesada. 2020. The Effect of Government Accounting Standards, Internal Control Systems, Competence of Human Resources, and Use of Information Technology on Quality of Financial Statements. International Journal of Innovative Research and Advanced Studies (IJIRAS) 7: 4–10. Available online: http://www.ijiras.com/2020/Vol_7-Issue_1/paper_2.pdf (accessed on 1 June 2021).

- Dewi, Nur Fitri, S. M. Ferdous Azam, and Siti Khalidah Mohd Yusoff. 2019. Factors Influencing the Information Quality of Local Government Financial Statement and Financial Accountability. Management Science Letters 9: 1373–84. [Google Scholar] [CrossRef]

- Dimitrijevic, Dragomir, Vesna Milovanovic, and Vladimir Stancic. 2015. University of Information Technology and Management in Rzeszów Financial Internet. Cejsh.Icm.Edu.Pl 11: 34–44. [Google Scholar] [CrossRef]

- Do, Duc Tai, and Thi Thanh Long Dinh. 2020. Determinants Influencing the Quality of Accounting Service: The Case of Accounting Service Firms in Hanoi, Vietnam. Available online: http://m.growingscience.com/beta/3480-determinants-influencing-the-quality-of-accounting-service-the-case-of-accounting-service-firms-in-hanoi-vietnam.html (accessed on 1 June 2021).

- Dornier, Pavlos. 2018. Investigating the Impact of Comprehensive Information Systems on Accounting Information Quality. Electronic Business Journal 17: 1–15. Available online: http://electronic-businessjournal.com/images/2018/12/1-Investigating_the_Impact_of_Comprehensive_Information_Systems_on_Accounting_Information_Quality.pdf (accessed on 1 June 2021).

- Etikan, Ilker, Sulaiman Abubakar Musa, and Rukayya Sunusi Alkassim. 2016. Comparison of Convenience Sampling and Purposive Sampling. American Journal of Theoretical and Applied Statistics 5: 1–4. [Google Scholar] [CrossRef] [Green Version]

- Fachada, Francisco José Cunha. 2014. Sistema de Controlo Interno Na Administração Central Do Estado: O Caso Dos Organismos Do Ministério Das Finanças. Coimbra: Universidade de Coimbra, Available online: https://eg.uc.pt/handle/10316/27499 (accessed on 1 June 2021).

- Feng, Mei, Chan Li, and Sarah McVay. 2009. Internal Control and Management Guidance. Journal of Accounting and Economics 48: 190–209. [Google Scholar] [CrossRef]

- Fitriati, Azmi, and Azhar Susanto. 2017. The Accounting Information System Quality Improvement through Internal Control and Top Management Support Effectiveness. Journal of Theoretical and Applied Information Technology 95: 5003–11. [Google Scholar]

- Flöstrand, Per. 2006. The Valuation Relevance of Non-financial Information. Management Research News 29: 580–97. [Google Scholar] [CrossRef]

- Fornell, Claes, and David F. Larcker. 1981. Evaluating Structural Equation Models with Unobservable Variables and Measurement Error. Journal of Marketing Research 18: 39–50. [Google Scholar] [CrossRef]

- Frazer, Linval. 2020. Does Internal Control Improve the Attestation Function and by Extension Assurance Services? A Practical Approach. Journal of Accounting and Finance 20: 28–38. [Google Scholar] [CrossRef]

- Gal, Graham, and Orhan Akisik. 2020. The Impact of Internal Control, External Assurance, and Integrated Reports on Market Value. Corporate Social Responsibility and Environmental Management 27: 1227–40. [Google Scholar] [CrossRef]

- Gomes, Emilia. 2014. A Importância Do Controlo Interno No Planeamento de Auditoria. Revisores e Auditores 64: 8–31. [Google Scholar]

- Hair, Joseph F., Jr., Rolph E. Anderson, Ronald L. Tatham, and William C. Black. 1998. Multivariate Data Analysis, 5th ed. Upper Saddle River: Prentice Hall. [Google Scholar]

- Han, Xi. 2019. Internal Control and Non-Efficiency Investment of Listed Companies. Paper presented at 4th International Social Sciences and Education Conference (ISSEC 2019), Xiamen, China, June 27–28; vol. 4, pp. 343–48. [Google Scholar] [CrossRef]

- Harding, Ronnie. 1998. Environmental Decision-Making the Roles of Scientists, Engineers and the Public. Sydney: The Federation Press. [Google Scholar]

- Hendri, and Sarah Amelia. 2019. The Influence of Human Resources, and Internal Control on the Quality of Financial Statement: Accounting Information System as a Moderating Role. International Journal of Management, Accounting and Economics 6: 761–69. Available online: www.ijmae.com (accessed on 1 June 2021).

- Herz, Robert H., Brad J. Monterio, and Jeffrey C. Thomson. 2017. Leveraging the COSO Internal Control—Integrated Framework to Improve Confidence in Sustainability Performance Data. pp. 1–55. Available online: www.linkedin.com/in/bradmonterio (accessed on 1 June 2021).

- Hla, Daw, and Susan Peter Teru. 2015. Efficiency of Accounting Information System and Performance Measures-Literature ‘Review’. International Journal of Multidisciplinary and Current Research 3. Available online: http://ijmcr.com (accessed on 1 June 2021).

- Hussin, Husnayati, Malcolm King, and Paul Cragg. 2002. IT Alignment in Small ‘Firms’. European Journal of Information Systems 11: 108–27. [Google Scholar] [CrossRef]

- Ibrahim, Fahmi, Diyana Najwa Haji Ali, and Nur Suaidah Awang Besar. 2020. Accounting Information Systems (AIS) in SMEs: Towards an Integrated Framework. International Journal of Asian Business and Information Management 11: 51–67. [Google Scholar] [CrossRef]

- Indrani, M. W., Moonsamy Naidoo, and Guneratne Wickremasinghe. 2020. Exploring Adoption and Implementation of Strategic Management Tools and Techniques by Listed Companies in the Sri Lankan Context 1 2 2. International Journal of Accounting & Business Finance 6: 106–23. [Google Scholar] [CrossRef]

- INE, Instituto Nacional de Estatística. 2020. Portal Do INE Portal. População Média Anual Residente (N.o) Por Local de Residência (NUTS), Sexo e Grupo Etário (Por Ciclos de Vida). Available online: https://www.ine.pt/xportal/xmain?xpid=INE&xpgid=ine_indicadores&contecto=pi&indOcorrCod=0008067&selTab=tab0 (accessed on 1 June 2021).

- Ježovita, Ana. 2015. Accounting Information in a Business Decision-Making Process-Evidence from Croatia. Zagreb International Review of Economics & Business 18: 61–79. [Google Scholar] [CrossRef] [Green Version]

- Ji, Xu-Dong, Wei Lu, and Wen Qu. 2017. Voluntary Disclosure of Internal Control Weakness and Earnings Quality: Evidence from China. The International Journal of Accounting 52: 27–44. [Google Scholar] [CrossRef]

- Jokipii, Annukka. 2010. Determinants and Consequences of Internal Control in Firms: A Contingency Theory Based Analysis. Journal of Management and Governance 14: 115–44. [Google Scholar] [CrossRef]

- Kaplan, David, Ramayya Krishnan, Rema Padman, and James Peters. 1998. Assessing Data Quality in Accounting Information Systems. Communications of the ACM 41: 72–78. [Google Scholar] [CrossRef]

- Kpurugbara, Nwinee, Yikarebogha Erorogha Akpos, Vincent G. Nwiduuduu, and Ibinabo Tams-Wariboko. 2016. Impact of Accounting Information System on Organizational Effectiveness-A Study of Selected Small and Medium Scale Enterprises in Woji, Portharcourt. Internaltional Journal of Research 3: 974–82. [Google Scholar]

- Le, Thi Tam, Thi Mai Anh Nguyen, and Thi Thu Hien Phan. 2019. Environmental Management Accounting and Performance Efficiency in the Vietnamese Construction Material Industry-a Managerial Implication for Sustainable Development. Sustainability 11: 5152. [Google Scholar] [CrossRef] [Green Version]

- Leiwakabessy, Theophilia Fina Febrione. 2020. The Effect of Government Internalal Control System, Human Resource Competency, and Accounting Information Systems to the Quality of the Local Government. Jurnal Sosial Humaniora 11. Available online: http://ojs.unida.ac.id/JSH/article/view/3066 (accessed on 1 June 2021).

- Li, Chan, Gary F. Peters, Vernon J. Richardson, and Marcia Weidenmier Watson. 2012. The Consequences of Information Technology Control Weaknesses on Management Information Systems: The Case of Sarbanes-Oxley Internal Control Reports. MIS Quarterly: Management Information Systems 36: 179–204. [Google Scholar] [CrossRef] [Green Version]

- Majid, Jamaluddin, Memen Suwandi, Lince Bulutoding, and Andi Wawo Sumarlin. 2020. The Influence of Accounting Information Systems and Internal Control on the Quality of Financial Statement with Intellectual Intelligence as a Moderating Variable (a Study on Coffee Shops in Makassar City). International Journal of Research Science & Management 7. Available online: http://repositori.uin-alauddin.ac.id/18228/ (accessed on 1 June 2021).

- Malo-Alain, Alaa Mohamad, Magdy Melegy Abdul Hakim Melegy, and Mahmoud Ragab Yassein Ghoneim. 2019. The Effects of Sustainability Disclosure on the Quality of Financial Reports in Saudi Business Environment. Academy of Accounting and Financial Studies Journal 23: 1–12. [Google Scholar]

- Marôco, João. 2010. Análise de Equações Estruturais: Fundamentos Teóricos, Software & Aplicações. Available online: https://www.google.com/books?hl=en&lr=&id=oYK1MG8tc3UC&oi=fnd&pg=PR9&dq=Marôco,+J.+(2010).+Análise+de+Equações+Estruturais+-+Fundamentos+teóricos,+Software+e+Aplicações.+ReportNumber.&ots=0m-_I86j9D&sig=BXFFKxOaH8pOt7_XKkUlRMHhR-4 (accessed on 1 June 2021).

- Martínez-Ferrero, Jennifer, Isabel M. Garcia-Sanchez, and Beatriz Cuadrado-Ballesteros. 2013. Effect of Financial Reporting Quality on Sustainability Information Disclosure. Wiley Online Library 22: 45–64. [Google Scholar] [CrossRef]

- Martos, A., R. Pacheco-Torres, J. Ordóñez, and E. Jadraque-Gago. 2016. Towards Successful Environmental Performance of Sustainable Cities: Intervening Sectors. A Review. Renewable and Sustainable Energy Reviews 57: 479–95. [Google Scholar] [CrossRef]

- Mbabazise, Mbabazi, Twesige Daniel, Mazimpaka Claude, and Jaya Shukla. 2015. Reporting of Non-Financial Information and Its Impact on the Decisions Taken in Private Institutions in Rwanda: Case Study Norhern Province. International Journal of Small Business and Entrepreneurship Research 2: 57–71. Available online: www.eajournals.org (accessed on 1 June 2021).

- Menicucci, Elisa. 2020. Earnings Quality. Earnings Quality: Definitions, Measures, and Financial Reporting. Cham: Springer International Publishing. [Google Scholar] [CrossRef]

- Mirnenko, Volodymyr I., Ivan M. Tkach, Maryna V. Potetiuieva, Mykhaylo Yu. Mechetenko, Mykola Ya Tkach, and Olena Holota. 2020. Analysis of Approaches to Assessing Effectiveness of the System of Internal Control of the Military Organization as the Element of Public Internal Financial. Espacios 41: 14–20. Available online: http://www.revistaespacios.com/a20v41n08/20410814.html (accessed on 1 June 2021).

- Mndzebele, Nomsa. 2012. The Usage of Accounting Information Systems for Effective Internal Controls in the Hotels. International Journal of Advanced Computer Technology 2. Available online: https://www.ijact.org/ijactold/volume2issue5/IJ0250003.pdf (accessed on 1 June 2021).

- Mohammed Al-Shafeay, Karrar, and Akeel Almagtome. 2019. The Role of Integrating Hotel Sustainability Reporting Practices into an Accounting Information System to Enhance Hotel Financial Performance: Evidence from Iraq. Researchgate.Net. Available online: https://www.researchgate.net/publication/336778683 (accessed on 1 June 2021).

- Montenegro, Tânia Menezes, and Lúcia Lima Rodrigues. 2020. Determinants of the Attitudes of Portuguese Accounting Students and Professionals towards Earnings Management. Journal of Academic Ethics 18: 301–32. [Google Scholar] [CrossRef]

- Moreno-Enguix, María del Rocío, Ester Gras-Gil, and Joaquín Henández-Fernández. 2019. Relation between Internet Financial Information Disclosure and Internal Control in Spanish Local Governments. Aslib Journal of Information Management 71: 176–94. [Google Scholar] [CrossRef]

- Muda, Iskandar, Abdul Haris Harahap, Syafruddin Ginting, Azhar Maksum, and Erwin Abubakar. 2018. Factors of Quality of Financial Report of Local Government in Indonesia. IOP Conference Series: Earth and Environmental Science 126: 1–6. [Google Scholar] [CrossRef]

- Napitupulu, Ilham Hidayah. 2018. Organizational Culture in Management Accounting Information System: Survey on State-Owned Enterprises (SOEs) Indonesia. Article Global Business Review 19: 1–16. [Google Scholar] [CrossRef]

- Nguyen, Hieu Thanh, and Anh Huu Nguyen. 2020. Determinants of Accounting Information Systems Quality: Empirical Evidence from Vietnam. Accounting 6: 185–98. [Google Scholar] [CrossRef]

- Patel, B. 2015. Effects of Accounting Information System on Organizational Profitability. International Journal of Research and Analytical Reviews 2: 72–76. [Google Scholar]

- Petcharat, Nickie, and Joseph M. Mula. 2009. Identifying System Characteristics for Development of a Sustainability Management Accounting Information System: Towards a Conceptual Design for the Manufacturing Industry. Paper presented at 2009 Fourth International Conference on Cooperation and Promotion of Information Resources in Science and Technology, Beijing, China, November 21–23; pp. 56–64. [Google Scholar] [CrossRef] [Green Version]

- Phornlaphatrachakorn, Kornchai. 2019. Internal Control Quality, Accounting Information Usefulness, Regulation Compliance, and Decision-Making Success: Evidence from Canned and Processed Foods Businesses in Thailand. International Journal of Business 24: 198–215. Available online: https://www.craig.csufresno.edu/ijb/Volumes/Volume24/V24N2-5.pdf (accessed on 1 June 2021).

- Ping, Robert A. 2004. On assuring valid measures for theoretical models using survey data. Journal of Business Research 57: 125–41. [Google Scholar] [CrossRef]

- Pizzi, Simone. 2018. The Relationship between non-financial reporting, environmental strategies and financial performance. empirical evidence from Milano stock exchange. Administrative Sciences 8: 76. [Google Scholar] [CrossRef] [Green Version]

- Pordata. 2019. Retrato de Portugal PORDATA, Edição 2019. Available online: https://www.pordata.pt/ebooks/PT2019v20190711/mobile/index.html (accessed on 1 June 2021).

- Pordata. 2020. Nascimentos, Mortes e Sobrevivência a 1 Ano de Empresas Não Financeiras. Available online: https://www.pordata.pt/ (accessed on 1 June 2021).

- Pravitasari, Nirwana Putri. 2018. Effect of Accounting Information System For Internal Control «Sippuh Online» in Pt. Dwimajaya Utama. Russian Journal of Agricultural and Socio-Economic Sciences 80: 167–71. [Google Scholar] [CrossRef]

- Rashedi, Hadi, and Toraj Dargahi. 2019. How Influence the Accounting Information Systems Quality of Internal Control on Financial Reporting Quality. Journal of Modern Developments in Management and Accounting 2: 33–45. Available online: http://jmdma.ir/index.php/JMDMA/article/view/40 (accessed on 1 June 2021).

- Ratcliff, Roger, Marios G. Philiastides, and Paul Sajda. 2009. Quality of Evidence for Perceptual Decision Making Is Indexed by Trial-to-Trial Variability of the EEG. Proceedings of the National Academy of Sciences of the United States of America 106: 6539–44. [Google Scholar] [CrossRef] [Green Version]

- Raucci, Domenico, Lara Tarquinio, Daniela Rupo, and Salvatore Loprevite. 2020. Non-Financial Performance Indicators: The Power of Measures to Operationalize the Law. In Sustainability and Law. Cham: Springer International Publishing, pp. 275–91. [Google Scholar] [CrossRef]

- Rouissi, Chiraz. 2020. User Satisfaction and Information System: Case for an Emerging Country. Marketing and Management of Innovations, 87–105. [Google Scholar] [CrossRef]

- Sajady, Hussein, Mohsen Dastgir, and H. Hashem Nejad. 2008. Evaluation of the Effectiveness of Accounting Information Systems. International Journal of Information Science and Management 6: 49–59. [Google Scholar]

- Salehi, Mahdi, Vahab Rostami, and Abdolkarim Mogadam. 2010. Usefulness of Accounting Information System in Emerging Economy: Empirical Evidence of Iran. International Journal of Economics and Finance 2. [Google Scholar] [CrossRef]

- Sari, Maya. 2018. The Effect of the Government of Internal Control System on the Quality of Financial Statements in the Coal Regency Village Of-Fice. Accounting, 134–44. Available online: http://proceedings.conference.unpas.ac.id/index.php/icis/article/view/520 (accessed on 1 June 2021).

- Schroeder, Joseph H., and Marcy L. Shepardson. 2016. Do SOX 404 Control Audits and Management Assessments Improve Overall Internal Control System Quality? Accounting Review 91: 1513–41. [Google Scholar] [CrossRef]

- Schwartz, Mark S. 2016. Ethical Decision-Making Theory: An Integrated Approach. Journal of Business Ethics 139: 755–76. [Google Scholar] [CrossRef]

- Shahsavarani, Amir Mohammad, Esfandiar Azad, and Marz Abadi. 2015. The Bases, Principles, and Methods of Decision-Making: A Review of Literature. International Journal of Medical Reviews Review Article International Journal of Medical Reviews 2. Available online: www.amazon.com (accessed on 1 June 2021).

- Soudani, Siamak Nejadhosseini. 2012. The Usefulness of an Accounting Information System for Effective Organizational Performance. International Journal of Economics and Finance 4: 136–145. Available online: https://www.academia.edu/download/39214984/16517-52549-1-SM.pdf (accessed on 1 June 2021). [CrossRef]

- Steenkamp, Jan Benedict E. M., and Hans C. M. van Trijp. 1991. The Use of Lisrel in Validating Marketing Constructs. International Journal of Research in Marketing 8: 283–99. [Google Scholar] [CrossRef]

- Susanto, Azhar. 2016. The Effect of Internal Control on Accounting Information System. International Business Management 10: 5523–29. [Google Scholar] [CrossRef]

- Trailer, Jeff W., Robert C. Hill, and Gregory B. Murphy. 1996. Measuring Performance in Entrepreneurship Research. Journal of Business Research 36: 15–23. [Google Scholar] [CrossRef]

- Triono, BRM Suryo, and Septiana Novita Dewi. 2020. Pengaruh Sistem Pengendalian Intern Terhadap Kualitas Laporan Keuangan Pemerintah Daerah. Jurnal Akuntansi Dan Pajak 21. [Google Scholar] [CrossRef]

- Verrecchia, Robert E. 1990. Information Quality and Discretionary Disclosure. Journal of Accounting and Economics 12: 365–80. [Google Scholar] [CrossRef]

- Wali, Sonda, and Sana Mardessi Masmoudi. 2020. Internal Control and Real Earnings Management in the French Context. Journal of Financial Reporting and Accounting 18: 363–87. [Google Scholar] [CrossRef]

- Wauchope, R. D., T. M. Buttler, A. G. Hornsby, P. W. M. Augustijn-Beckers, and J. P. Burt. 1992. The SCS/ARS/CES Pesticide Properties Database for Environmental Decision-Making. Reviews of Environmental Contamination and Toxicology. [Google Scholar] [CrossRef]

- Zebua, Justika, Muhammad Rasuli, and Vera Oktari. 2020. Determinan Kualitas Laporan Keuangan Pemerintah Daerah: Studi Pada Opd Pemerintah Kota Pekanbaru. Jurnal Kajian Akuntansi Dan Bisnis Terkini 1: 170–83. Available online: www.cakaplah.com (accessed on 1 June 2021). [CrossRef]

- Zeina, Nur, Maya Sari, and Djumhana Purwanegara. 2016. The Effect of Quality Accounting Information System in Indonesian Government (BUMD at Bandung Area) View Project Website View Project The Effect of Quality Accounting Information System in Indonesian Government (BUMD at Bandung Area). Research Journal of Finance and Accounting www.Iiste.Org ISSN 7. Available online: www.iiste.org (accessed on 1 June 2021).

- Zeina, Nur, Maya Sari, Nunuy Nur Afifah, Azhar Susanto, and Memed Sueb. 2019. Quality Accounting Information Systems with 3 Important Factors in BUMN Bandung Indonesia. Atlantis-Press.Com. Available online: https://www.atlantis-press.com/article/125916454.pdf (accessed on 1 June 2021).

- Zhang, Hao. 2014. A Framework for Integrating Systems Thinking into Sustainable Manufacturing. Available online: https://ir.library.oregonstate.edu/concern/graduate_thesis_or_dissertations/qz20sx98s (accessed on 1 June 2021).

- Zyznarska-Dworczak, Beata. 2018. Legitimacy Theory in Management Accounting Research. Problemy Zarzadzania 16: 195–203. [Google Scholar] [CrossRef]

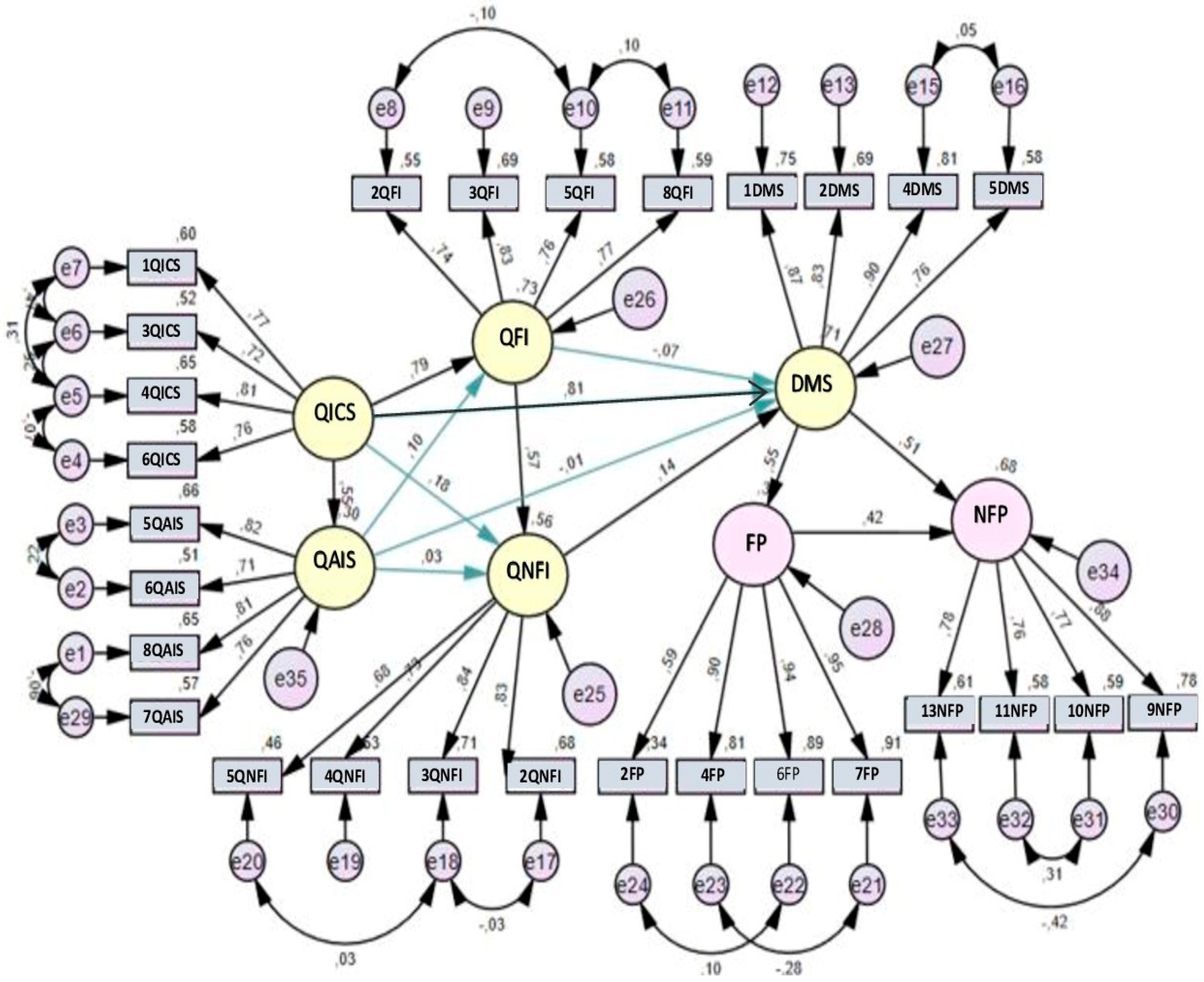

| Construct | c.s. |

|---|---|

| Quality of ICS (CR = 0.93, AVE = 0.66) | |

| 1QICS—Internal control system has improved and promoted the company’s operational efficiency and effectiveness. | 0.904 * |

| 3QICS—Internal control system has allowed building and creating effective operations, activity, and business practices. | 0.834 * |

| 4QICS—Internal control system has allowed the company to prepare financial information with quality. | 0.824 * |

| 6QICS—The company complies with all required regulations, i.e., laws, rules, guidelines, standards, and other related issues within internal control quality. | 0.667 * |

| Quality of AIS (CR = 0.92, AVE = 0.61) | |

| 5QAIS—The data processing caused the improvement of the quality of the financial reports. | 0.864 * |

| 6QAIS—The automated data collection speed up the process of non-financial information preparation | 0.758 * |

| 7QAIS—The automated data collection speed up the process to generate financial statements and overcome human weaknesses in data processing. | 0.744 * |

| 8QAIS—The automated data collection provides a platform with access to information, which facilitates the use of it. | 0.752 * |

| Quality of FI (CR = 0.90, AVE = 0.56) | |

| 2QFI—The accuracy of financial information helps decision-making. | 0.724 * |

| 3QFI—Financial information is carefully prepared to ensure its reliability. | 0.831 * |

| 5QFI—Financial information is easily understood by its user. | 0.719 * |

| 8QFI—Financial information represents in a reliable way what you want to portray. | 0.723 * |

| Quality of Non-Financial Information (CR = 0.91, AVE = 0.60) | |

| 2QNFI—Non-financial information is carefully prepared to ensure its quality. | 0.804 * |

| 3QNFI—Non-financial information is easily understood by its user. | 0.846 * |

| 4QNFI—Non-financial information includes all the information necessary to make decisions. | 0.735 * |

| 5QNFI—Non-financial information is free of value judgements. | 0.701 * |

| DMS (CR = 0.95, AVE = 0.73) | |

| 1DMS—The decisions made allowed the company to achieve advantages in terms of operations, management, and performance. | 0.857 * |

| 2DMS—Decisions made about investments took into account different alternatives or options, which allowed the company to choose the best solution. | 0.837 * |

| 4DMS The decisions taken have contributed to maximized operational efficiency and effectiveness. | 0.910 * |

| 5DMS The decisions made in the company determine its success. | 0.764 * |

| Performance | |

| Financial Performance (CR = 0.948, AVE = 0.733) | |

| 2FP—The size of the company has increased. | 0.597 * |

| 4FP—The company’s operating profit has improved/increased. | 0.881 * |

| 6FP—Return on equity improved/increased (EBIT/Equity). | 0.967 * |

| 7FP—Profitability on sales increased (EBIT/Sales). | 0.930 * |

| Non-Financial Performance (CR = 0.928, AVE = 0.645) | |

| 9NFP—The company has improved its customer service. | 0.792 * |

| 10NFP—The company has improved working conditions, regardless of the employee’s position. | 0.850 * |

| 11NFP—The company has improved its performance in terms of social responsibility (voluntary effort on the part of the company in the creation of various measures to meet the expectations of the different interested parties—stakeholders). | 0.842 * |

| 13NFP—The company has increased its employee retention rates. | 0.721 * |

| Fit Measure | ||||

|---|---|---|---|---|

| X2/gl | RMSEA | GFI | NFI | CFI |

| 1.813 | 0.046 | 0.902 | 0.926 | 0.965 |

| <3 | <0.05 | >0.90 | >0.90 | >0.90 |

| Parameters | Non-Standardised Coefficient | Standardised Coefficient | p-Value | R2 | ||

|---|---|---|---|---|---|---|

| QICS | - | QAIS | 0.642 | 0.552 | *** | 0.30 |

| QICS | - | QFI | 0.818 | 0.794 | *** | 0.73 |

| QAIS | - | QFI | 0.093 | 0.105 | 0.082 | |

| QICS | - | QNFI | 0.208 | 0.178 | 0.157 | 0.56 |

| QAIS | - | QNFI | 0.033 | 0.033 | 0.574 | |

| QFI | - | QNFI | 0.651 | 0.575 | *** | |

| QFI | - | DMS | −0.063 | −0.068 | 0.636 | 0.71 |

| QNFI | - | DMS | 0.111 | 0.136 | 0.057 | |

| QAIS | - | DMS | −0.008 | −0.01 | 0.858 | |

| QICS | - | DMS | 0.767 | 0.807 | *** | |

| DMS | - | FP | 0.663 | 0.55 | *** | 0.30 |

| DMS | - | NFP | 0.737 | 0.509 | *** | 0.68 |

| FP | - | NFP | 0.509 | 0.424 | *** | |

| Hypothesis | Parameters | Non-Standardised Coefficient | Standardised Coefficient | p-Value | R2 | ||

|---|---|---|---|---|---|---|---|

| H1 | QICS | - | QAIS | 0.611 | 0.533 | *** | 0.284 |

| H2 | QICS | - | QFI | 0.711 | 0.74 | *** | 0.697 |

| H4 | QAIS | - | QFI | 0.133 | 0.158 | 0.002 * | |

| H6 | QFI | - | QNFI | 0.92 | 0.759 | *** | 0.576 |

| H8 | QNFI | - | DMS | 0.175 | 0.216 | *** | 0.650 |

| H10 | QICS | - | DMS | 0.618 | 0.654 | *** | |

| H11 | DMS | - | FP | 1.019 | 0.541 | *** | 0.293 |

| H12 | DMS | - | NFP | 0.728 | 0.498 | *** | 0.697 |

| H13 | FP | - | NFP | 0.348 | 0.449 | *** | |

| Direct | Indirect | Total | |

|---|---|---|---|

| Effects on QAIS | |||

| QICS-QAIS | 0.53 | 0.533 | |

| Effects on QFI | |||

| QICS-QAIS-QFI | 0.084 | 0.824 | |

| QICS-QFI | 0.74 | ||

| Effects on QNFI | |||

| QICS-QAIS-QFI-QNFI | 0.064 | 0.626 | |

| QICS-QFI-QNFI | 0.562 | ||

| Effects on DMS | |||

| QICS-QAIS-QFI-QNFI-DMS | 0.014 | 0.789 | |

| QICS-QFI-QNFI-DMS | 0.121 | ||

| QICS-DMS | 0.654 | ||

| Effects on FP | |||

| QICS-QAIS-QFI-QNFI-DMS-FP | 0.007 | 0.427 | |

| QICS-QFI-QNFI-DMS-FP | 0.066 | ||

| QICS-DMS-FP | 0.354 | ||

| Effects on NFP | |||

| QICS-QAIS-QFI-QNFI-DMS-FP-NFP | 0.003 | 0.584 | |

| QICS-QAIS-QFI-QNFI-DMS- NFP | 0.007 | ||

| QICS-QFI-QNFI-DMS- FP-NFP | 0.060 | ||

| QICS-QFI-QNFI-DMS-NFP | 0.029 | ||

| QICS-DMS-FP-NFP | 0.159 | ||

| QICS-DMS-NFP | 0.326 | ||

| Hypotheses | Results | Literature |

|---|---|---|

| H1: The quality of ICS has a positive impact on the quality of AIS. | Accepted | Supported by Susanto (2016) and Anggadini (2015) |

| H2: The quality of AIS has a positive impact on the quality of FI. | Accepted | Supported by Dewi and Hoesada (2020), Dewi et al. (2019), Satuan Kerja Perangkat Daerah (SKPD) and Majid et al. (2020) Phornlaphatrachakorn (2019) |

| H3: The quality of ICS has a positive impact on the quality of NFI. | Rejected | Contradiction with Bauer et al. (2018) and Frazer (2020) |

| H4: The quality of AIS has a positive impact on the quality of FI. | Accepted | Supported by Majid et al. (2020); Muda et al. (2018); and Salehi et al. (2010). |

| H5: The quality of AIS has a positive impact on the quality of NFI. | Rejected | Contradiction with Petcharat and Mula (2009) and Zyznarska-Dworczak (2018). Suported by Al-Wattar et al. (2019) |

| H6: The quality of FI has a positive impact on the quality of NFI. | Accepted | Supported by Martínez-Ferrero et al. (2013) |

| H7: The quality of FI has a positive impact on DMS. | Rejected | Contradiction with Menicucci (2020) |

| H8: The quality of NFI has a positive impact on DMS. | Accepted | Supported by Boulianne (2007); Barker and Eccles (2018); Mbabazise et al. (2015); and Pizzi (2018). |

| H9: The quality of AIS contributes positively to DMS. | Rejected | Contradiction with Sajady et al. (2008); Ibrahim et al. (2020) and Nguyen and Nguyen (2020) |

| H10: the quality of ICS contributes positively to DMS. | Accepted | Supported by Phornlaphatrachakorn (2019) |

| H11: DMS contributes positively to Financial Performance. | Accepted | Supported by Bosworth (2005); Patel (2015); Pravitasari (2018); Phornlaphatrachakorn (2019); Wauchope et al. (1992); and Zhang (2014). |

| H12: DMS contributes positively to Non-Financial Information. | Accepted | Supported by Bosworth (2005); Patel (2015); Pravitasari (2018); Phornlaphatrachakorn (2019); Wauchope et al. (1992); and Zhang (2014). |

| H13: Financial Performance contributes positively to Non-Financial Information. | Accepted | Supported by (Ayu et al. 2020 ) |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Monteiro, A.P.; Vale, J.; Silva, A. Factors Determining the Success of Decision Making and Performance of Portuguese Companies. Adm. Sci. 2021, 11, 108. https://doi.org/10.3390/admsci11040108

Monteiro AP, Vale J, Silva A. Factors Determining the Success of Decision Making and Performance of Portuguese Companies. Administrative Sciences. 2021; 11(4):108. https://doi.org/10.3390/admsci11040108

Chicago/Turabian StyleMonteiro, Albertina Paula, Joana Vale, and Amélia Silva. 2021. "Factors Determining the Success of Decision Making and Performance of Portuguese Companies" Administrative Sciences 11, no. 4: 108. https://doi.org/10.3390/admsci11040108

APA StyleMonteiro, A. P., Vale, J., & Silva, A. (2021). Factors Determining the Success of Decision Making and Performance of Portuguese Companies. Administrative Sciences, 11(4), 108. https://doi.org/10.3390/admsci11040108