Challenging Times for Insurance, Banking and Financial Supervision in Saudi Arabia (KSA)

Abstract

:1. Introduction

2. Overview of the Financial Systems

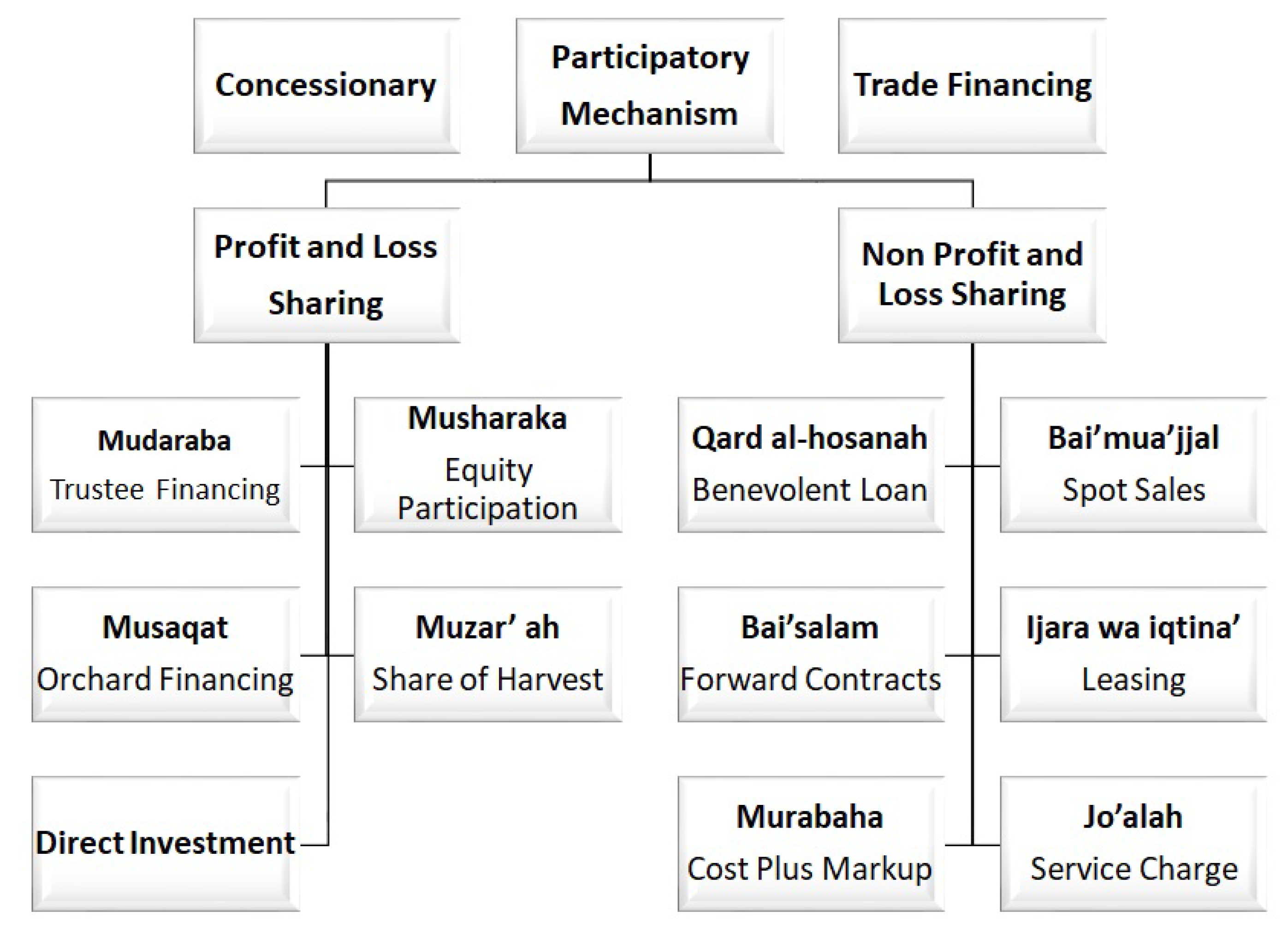

2.1. Background to Financial System: Sharia

2.2. Structure of the Financial System

2.3. Economic Transformation to Resulting in More Privatisations, Financial Reform?

2.4. Key Facts on the Insurance and Banking Sector

2.5. GDP and COVID-19 Pandemic

2.6. Corporate Governance in the Context of COVID-19

3. Insurance

3.1. Takaful

3.1.1. Mudharaba Model

3.1.2. Wakala–Waqf Model

3.1.3. Hybrid Model

3.1.4. Reinsurance

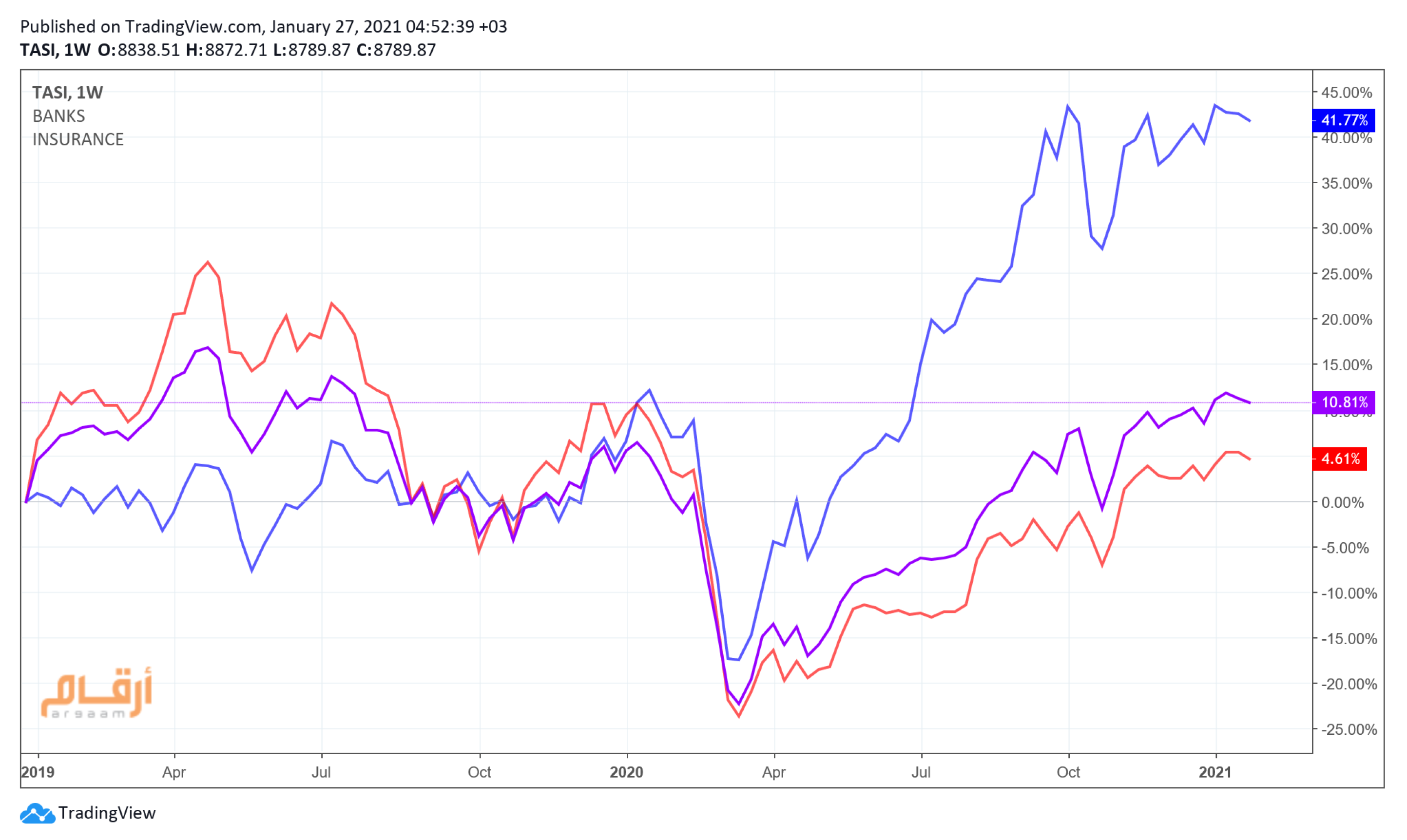

3.2. Insurance Market and Financials

3.3. Competition

3.4. Profitability and Capital

4. Banking

- Debt Service to Income (DTI) ratio (i.e., a monthly deduction cap) capped at a maximum of 33% of borrower’s monthly salary and 25% of borrower’s pension

- Loans limited to five years maximum tenor

- Loan to value limits on mortgage lending raised from 70% to 85%

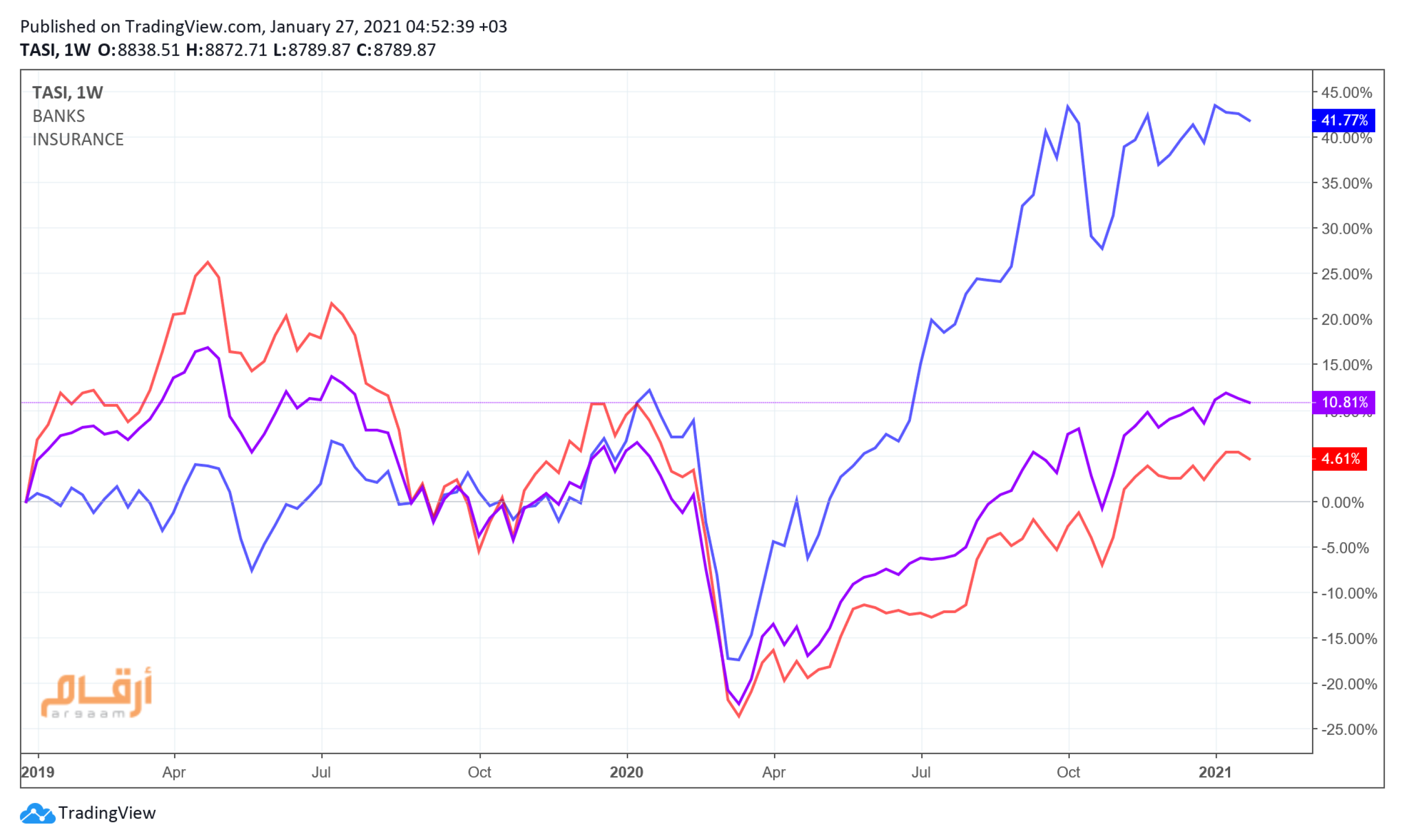

4.1. Profitability and Assets

4.2. Risk and Liquidity

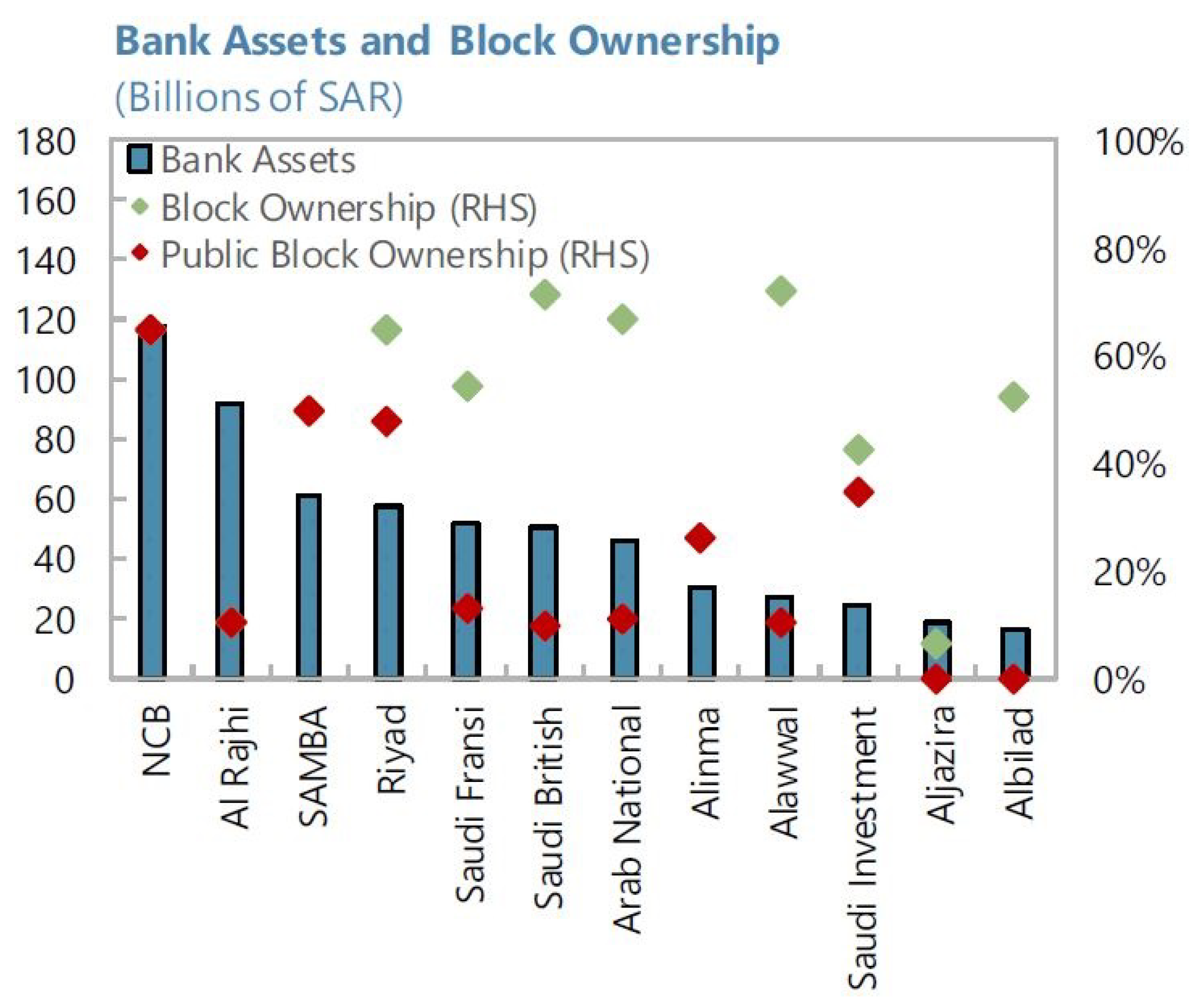

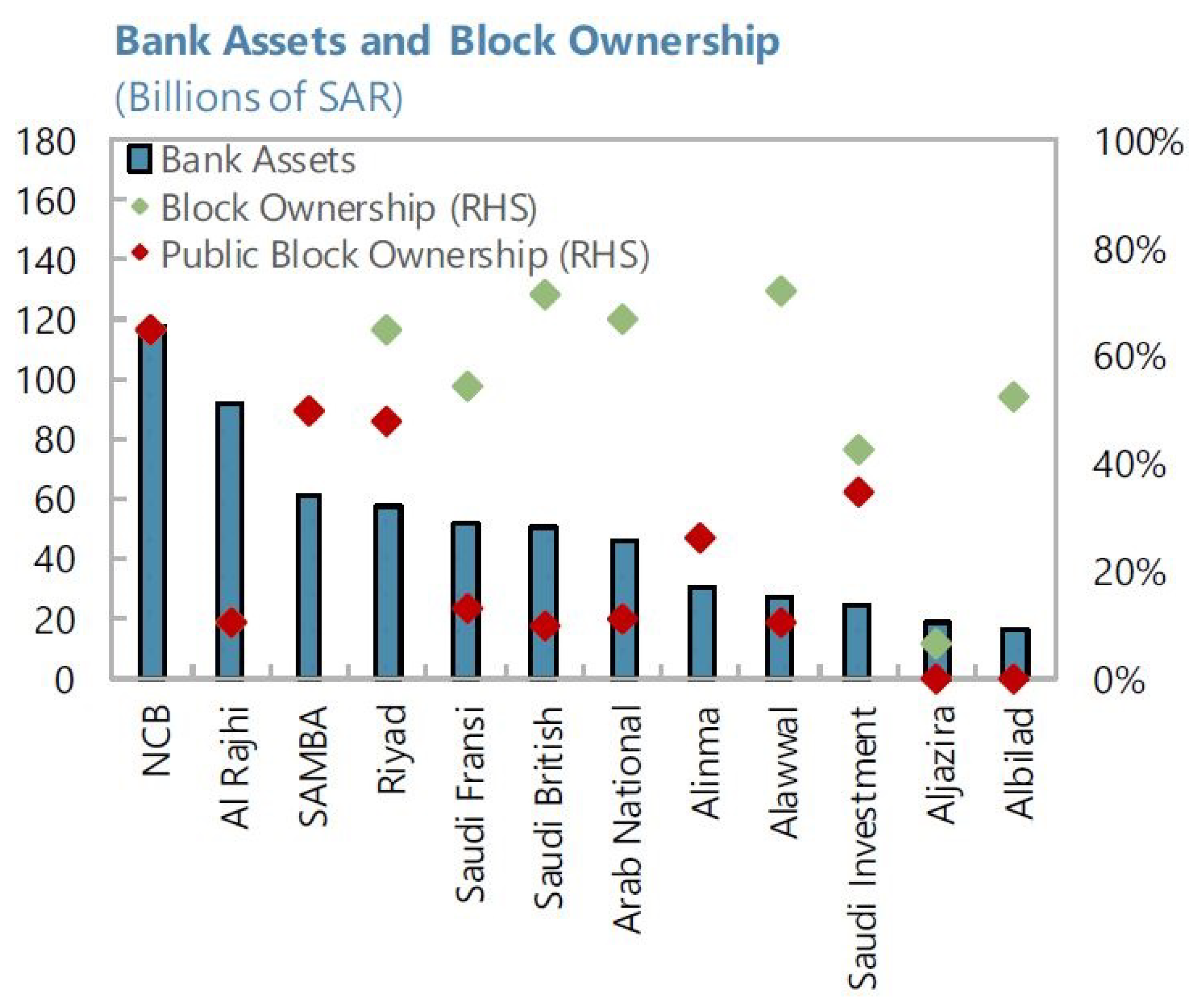

4.3. Banks’ Assets

4.4. Competition

5. Regulation

5.1. Saudi Arabian Monetary Agency (SAMA)

5.2. Depositors Protection Fund

5.3. Consumer Rights in KSA

5.4. Capital Market Authority of Saudi Arabia (CMA)

5.4.1. Strategic Priorities

5.4.2. Staff, Qualification, Training and Development

6. Quantitative Analysis and the Exposure to Oil

6.1. Data

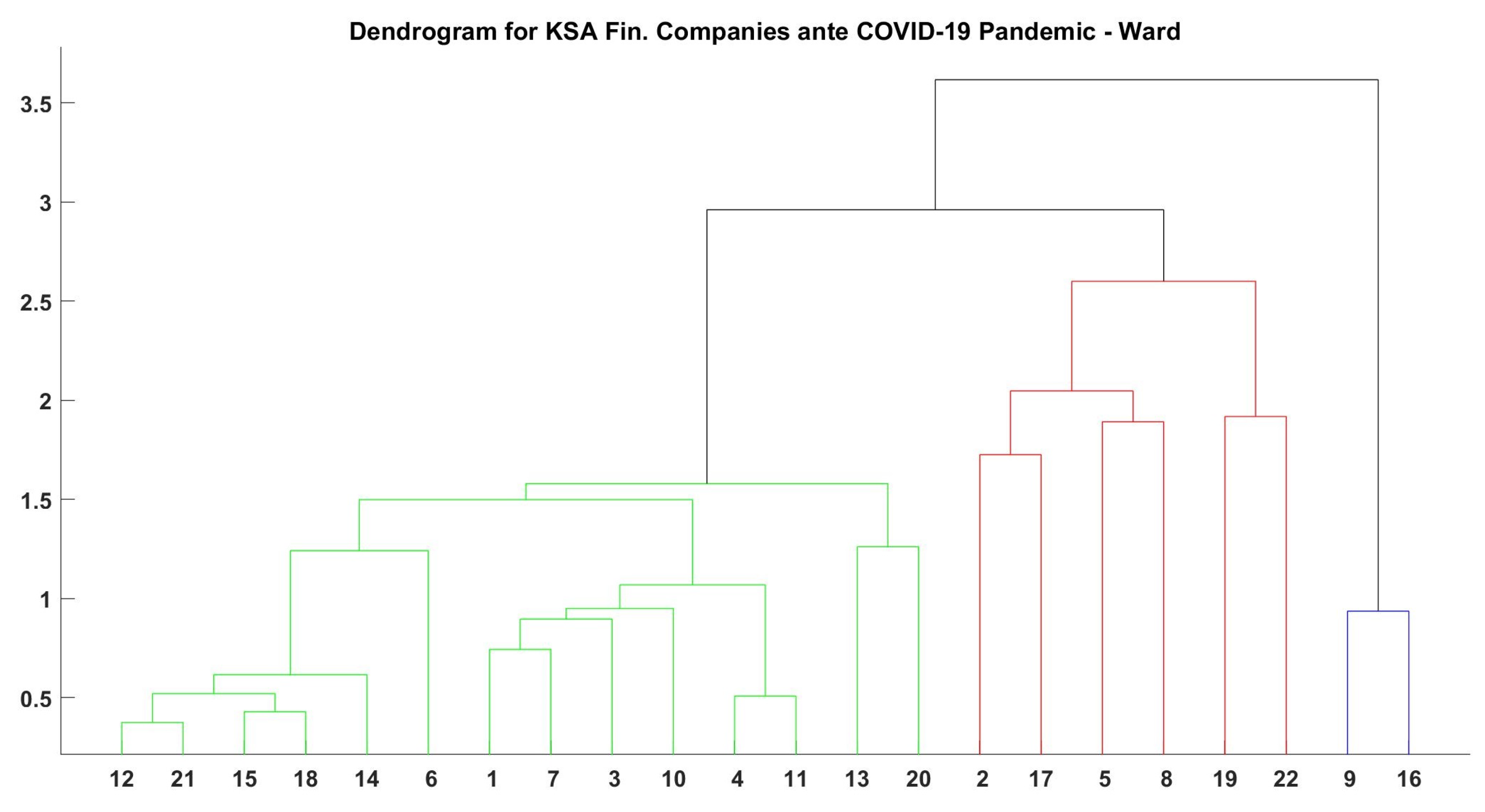

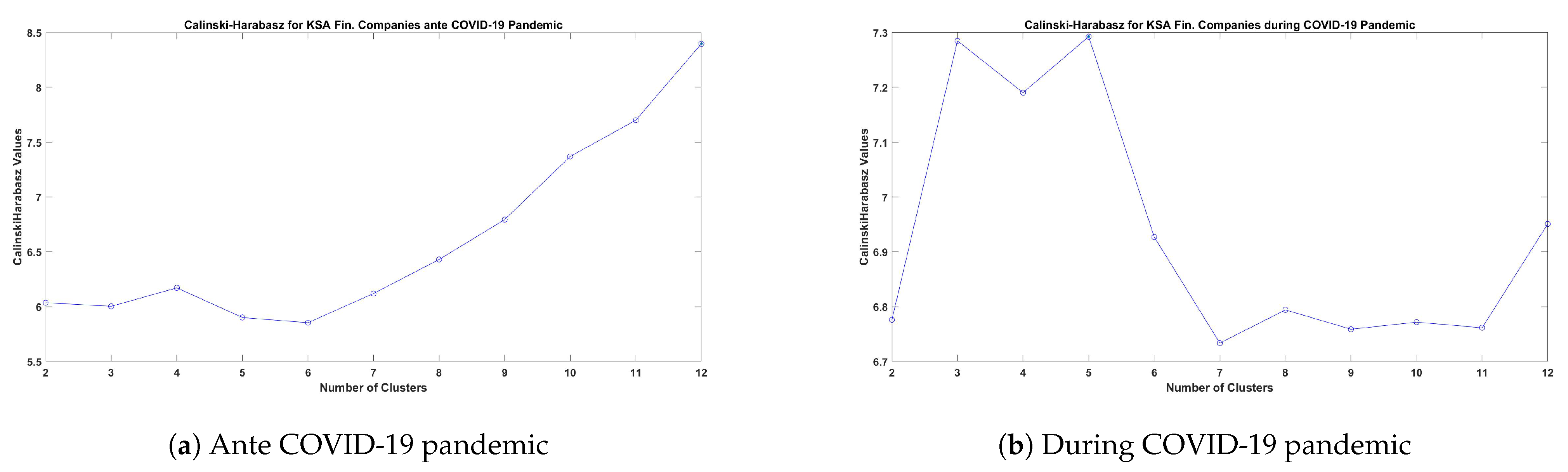

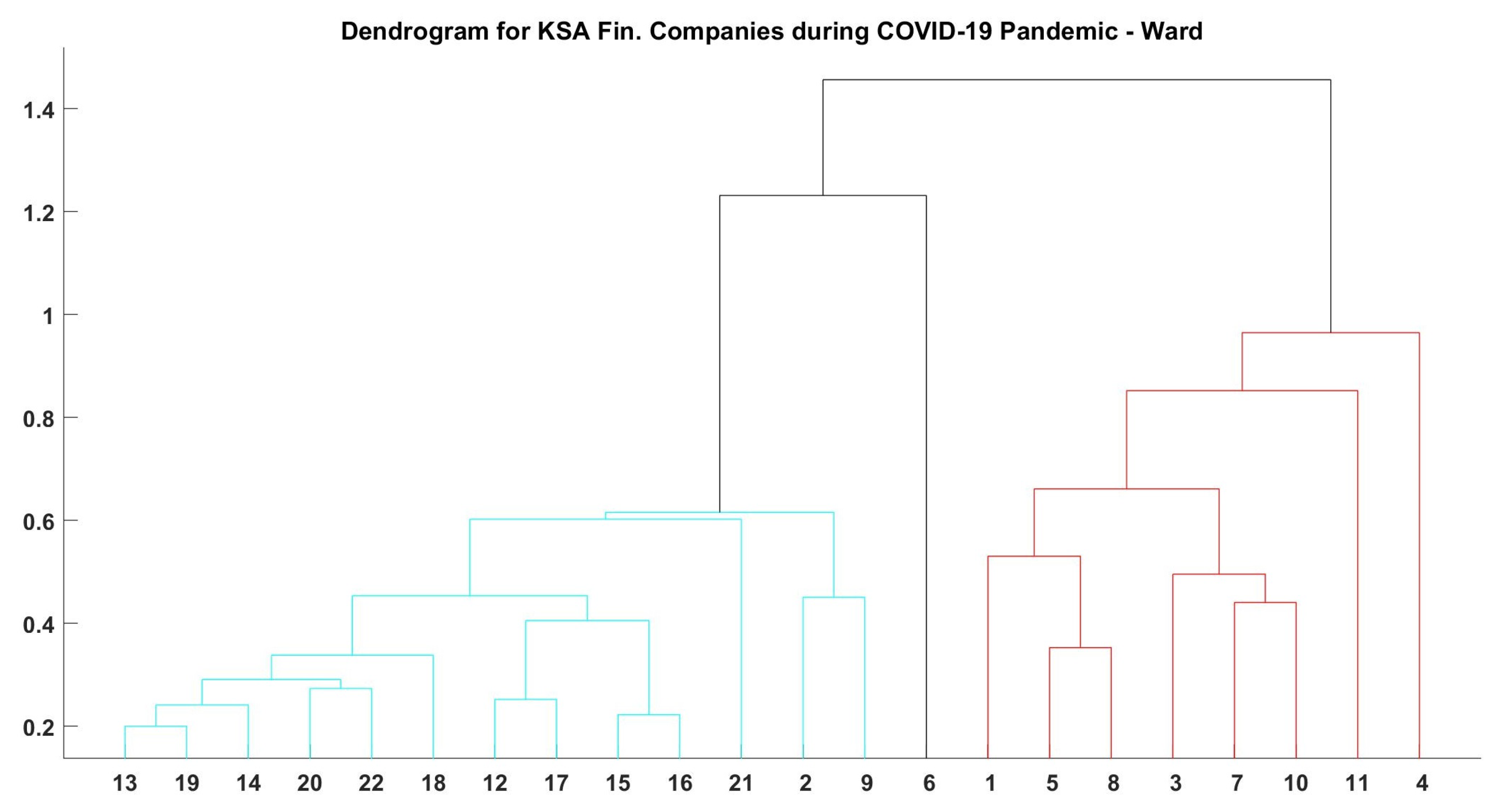

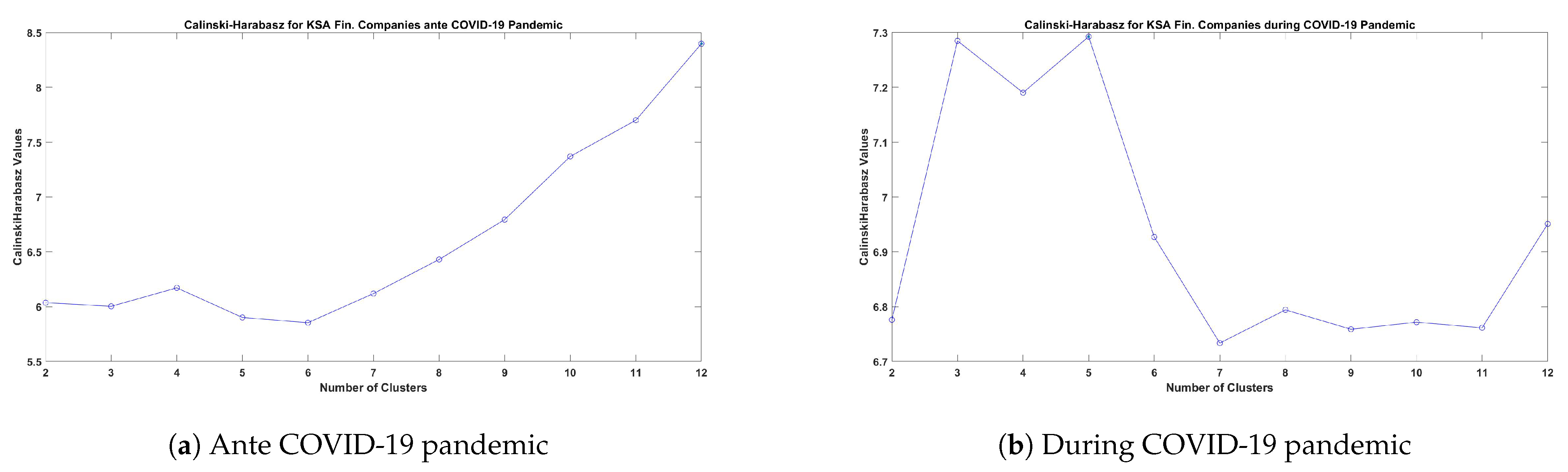

6.2. Cluster Analysis

6.3. Correlation

6.4. Econometric Analysis

Results of the Analysis

7. Discussion

8. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A. Panel Analysis

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Panel: Individual Effects by Company | ||||

|---|---|---|---|---|

| ID | Ieffect | Std. Error | t-Stat | p-Value |

| 1010 | −0.249415 | 0.02593 | −9.6186 | 0 *** |

| 1020 | −0.016858 | 0.02593 | −0.6501 | 0.516 |

| 1030 | −0.073187 | 0.025947 | −2.8206 | 0.005 *** |

| 1050 | −0.044353 | 0.025936 | −1.7101 | 0.088 * |

| 1060 | 0.004819 | 0.025928 | 0.1859 | 0.853 |

| 1080 | −0.02256 | 0.025929 | −0.8701 | 0.384 |

| 1090 | 0.03074 | 0.025937 | 1.1852 | 0.236 |

| 1120 | 0.022084 | 0.02593 | 0.8517 | 0.395 |

| 1140 | −0.027879 | 0.025972 | −1.0734 | 0.283 |

| 1150 | −0.125308 | 0.025941 | −4.8305 | 0 *** |

| 1180 | 0.005621 | 0.025941 | 0.2167 | 0.828 |

| 8020 | −0.153727 | 0.02593 | −5.9285 | 0 *** |

| 8040 | −0.087692 | 0.025931 | −3.3818 | 0.001 *** |

| 8050 | 0.014213 | 0.025929 | 0.5482 | 0.584 |

| 8060 | −0.053373 | 0.025934 | −2.058 | 0.04 ** |

| 8070 | −0.021558 | 0.025934 | −0.8313 | 0.406 |

| 8120 | −0.120458 | 0.025928 | −4.6458 | 0 *** |

| 8170 | 0.005591 | 0.025928 | 0.2156 | 0.829 |

| 8210 | 0.051687 | 0.025943 | 1.9923 | 0.047 ** |

| 8230 | 0.013024 | 0.025955 | 0.5018 | 0.616 |

| 8250 | −0.070516 | 0.025932 | −2.7193 | 0.007 *** |

| 8300 | −0.177277 | 0.02593 | −6.8367 | 0 *** |

| OVERALL | −0.049835 | 0.000261 | −190.8164 | 0 *** |

| Panel: Individual Effects by Company | ||||

|---|---|---|---|---|

| ID | Ieffect | Std. Error | t-Stat | p-Value |

| 1010 | 0.00244 | 0.022101 | 0.1104 | 0.912 |

| 1020 | 0.031266 | 0.022116 | 1.4137 | 0.158 |

| 1030 | 0.042878 | 0.022146 | 1.9362 | 0.053 * |

| 1050 | 0.068113 | 0.022088 | 3.0837 | 0.002 *** |

| 1060 | 0.078135 | 0.02209 | 3.5372 | 0 *** |

| 1080 | 0.092734 | 0.022132 | 4.19 | 0 *** |

| 1090 | 0.068514 | 0.022098 | 3.1005 | 0.002 *** |

| 1120 | 0.094865 | 0.022113 | 4.29 | 0 *** |

| 1140 | 0.113965 | 0.022106 | 5.1554 | 0 *** |

| 1150 | −0.256709 | 0.022104 | −11.6137 | 0 *** |

| 1180 | −0.081388 | 0.022108 | −3.6813 | 0 *** |

| 8020 | −0.047632 | 0.022128 | −2.1526 | 0.032 ** |

| 8040 | 0.034045 | 0.022112 | 1.5397 | 0.124 |

| 8050 | 0.058896 | 0.022088 | 2.6665 | 0.008 *** |

| 8060 | 0.019769 | 0.022142 | 0.8928 | 0.372 |

| 8070 | 0.05896 | 0.022111 | 2.6666 | 0.008 *** |

| 8120 | 0.034966 | 0.02214 | 1.5793 | 0.115 |

| 8170 | 0.068463 | 0.022097 | 3.0983 | 0.002 *** |

| 8210 | 0.292915 | 0.022133 | 13.2344 | 0 *** |

| 8230 | 0.069564 | 0.022147 | 3.141 | 0.002 *** |

| 8250 | 0.048067 | 0.022118 | 2.1732 | 0.03 ** |

| 8300 | 0.019322 | 0.022221 | 0.8695 | 0.385 |

| OVERALL | −0.049835 | 0.000261 | −190.8164 | 0 *** |

| 1 | For that indicator, The World Bank provides data for Saudi Arabia from 2009 to 2015. The average value for Saudi Arabia during that period was 393.7 billion U.S. dollars with a minimum of 318.73 billion U.S. dollars in 2009 and a maximum of 421.06 billion U.S. dollars in 2015 The Global Economy (2016). |

References

- Ahmad, Mohd, Tariq Masood, and Mohd Saeed Khan. 2010. Problems and Prospects of Islamic Banking: A Case Study of Takaful. Available online: https://mpra.ub.uni-muenchen.de/22232/ (accessed on 10 May 2021).

- Alkhaldi, Bader Abdulaziz. 2015. The Saudi capital market: The crash of 2006 and lessons to be learned. International Journal of Business, Economics and Law 8: 135–46. [Google Scholar]

- Álvarez, Inmaculada C., Javier Barbero, and José L. Zofío. 2017. A panel data toolbox for Matlab. Journal of Statistical Software 76: 1–27. [Google Scholar] [CrossRef] [Green Version]

- Ambrose, Jillian. 2016. Can Saudi Aramco Really Be Worth $2.5 Trillion? The Telegraph. Available online: http://www.telegraph.co.uk/business/2016/05/01/saudi-aramco-how-do-you-put-a-price-tag-on-the-worlds-most-impor/ (accessed on 27 October 2020).

- Argaam. 2020. Available online: tradingview.com (accessed on 27 December 2020).

- Argaam. 2021. Available online: tradingview.com (accessed on 15 May 2021).

- Baltagi, Badi. 2008. Econometric Analysis of Panel Data. Hoboken: John Wiley & Sons. [Google Scholar]

- Bank for International Settlements. 2018. Regulatory Consistency Assessment Programme (RCAP) Assessment of Basel Large Exposures Framework—Kingdom of Saudi Arabia. Basel: Basel Committee on Banking Supervision. [Google Scholar]

- Belsley, David A., Edwin Kuh, and Roy E. Welsch. 2005. Regression Diagnostics: Identifying Influential Data and Sources of Collinearity. Hoboken: John Wiley & Sons, vol. 571. [Google Scholar]

- Bikker, Jacob A., and Katharina Haaf. 2002. Measures of competition and concentration in the banking industry: A review of the literature. Economic & Financial Modelling 9: 53–98. [Google Scholar]

- Blas, Javier. 2016. Too Big to Value: Why Saudi Aramco Is in a League of Its Own. Bloomberg. Available online: http://www.bloomberg.com/news/articles/2016-01-07/too-big-to-value-why-saudi-aramco-is-in-a-league-of-its-own/ (accessed on 27 October 2016).

- Caliński, Tadeusz, and Jerzy Harabasz. 1974. A dendrite method for cluster analysis. Communications in Statistics-theory and Methods 3: 1–27. [Google Scholar] [CrossRef]

- Capital Market Authority. 2015. Annual Report 2015. Riyadh: Capital Market Authority. [Google Scholar]

- Capital Market Authority. 2018. Annual Report 2018. Riyadh: Capital Market Authority. [Google Scholar]

- Capital Market Authority. 2020. About the Capital Market Authority. Riyadh: Capital Market Authority. [Google Scholar]

- Carpinelli, Luisa, and Matteo Crosignani. 2015. The Effect of Central Bank Liquidity on Bank Credit Supply. New York: New York University & Mimeo. [Google Scholar]

- Damak, Mohamed. 2021. Banks in Emerging Markets: 15 Countries, Three Main Risks (January 2021 Update). New York: S&P Global. [Google Scholar]

- Deliu, Delia. 2020. The Intertwining between Corporate Governance and Knowledge Management in the Time of COVID-19: A Framework. Journal of Emerging Trends in Marketing and Management 1: 93–110. [Google Scholar]

- Demirguc-Kunt, Asli, Alvaro Pedraza, and Claudia Ruiz-Ortega. 2020. Banking Sector Performance during the COVID-19 Crisis. Washington, DC: World Bank. [Google Scholar]

- Di Lorenzo, Emilia, and Marilena Sibillo. 2020. Economic Paradigms and Corporate Culture after the Great COVID-19 Pandemic: Towards a New Role of Welfare Organisations and Insurers. Sustainability 12: 8163. [Google Scholar] [CrossRef]

- Diron, Marie, and Alexander Perjessey. 2019. Saudi Arabia’s Credit Profile Supported by Very High Fiscal and Economic Strength and External Liquidity Buffers. New York: Moody’s. [Google Scholar]

- Dyck, Steffen. 2016. Saudi Arabia’s Fiscal Position. New York: Moody’s. [Google Scholar]

- Fadaak, Turki, and Saeed I. Alghamdi. 2016. Saudi Insurance Sector 2015. Riyadh: Albilad Capital, March. [Google Scholar]

- Fadaak, Turki, and Saeed I. Alghamdi. 2017. Saudi Insurance Sector 2017. Riyadh: Albilad Capital. [Google Scholar]

- Financial Stability Board (FSB). 2012. Progress in the Implementation of G20/FSB Recommendations—June 2012—Jurisdiction: Saudi Arabia. Basel: FSB. [Google Scholar]

- Financial Stability Board (FSB). 2012. Thematic Review on Deposit Insurance Systems—8 February 2012. Basel: FSB. [Google Scholar]

- Financial Stability Board (FSB). 2015. Peer Review of Saudi Arabia—5 November 2015. Basel: FSB. [Google Scholar]

- Fitch Solutions. 2020. Saudi Arabia Banking and Financial Services Report. Available online: https://store.fitchsolutions.com/all-products/saudi-arabia-banking-financial-services-report (accessed on 10 May 2021).

- Friederich, Jan. 2017. Fitch Downgrades Saudi Arabia to A+; Fitch Ratings. Available online: https://www.fitchratings.com/research/sovereigns/fitch-downgrades-saudi-arabia-to-a-outlook-stable-30-09-2019 (accessed on 10 May 2021).

- Friederich, Jan, and Krisjanis Krustins. 2020. Fitch Rating of Saudi Arabia; Fitch Ratings. Available online: https://www.fitchratings.com/research/sovereigns/fitch-affirms-saudi-arabia-at-a-outlook-stable-09-04-2020/dodd-frank-disclosure (accessed on 10 May 2021).

- GASTAT. 2021. The General Authority for Statistics (GASTAT), Gross Domestic Product. Riyadh: GASTAT. [Google Scholar]

- House, Karen Elliott. 2013. On Saudi Arabia: Its People, Past, Religion, Fault Lines–and Future. New York: Vintage. [Google Scholar]

- Hussain, Monsur, James Watson, and Emil Dupont. 2020. Coronavirus Rating Impact: EMEA Emerging Market Banks. New York: Fitch Ratings. [Google Scholar]

- International Monetary Fund (IMF). 2019. Financial Inclusion of Small and Medium-Sized Enterprises in the Middle East and Central Asia. IMF Department Paper 19/02. Washington, DC: IMF. [Google Scholar]

- International Monetary Fund (IMF). 2019. Saudi Arabia, IMF Country Report No. 19/290. Washington, DC: IMF. [Google Scholar]

- Jaffer, Sohail. 2007. Islamic Insurance: Trends, Opportunities and the Future of Takaful. Bend: Linnius. [Google Scholar]

- Jain, K. Anil, and Richard C. Dubes. 1988. Algorithms for Clustering Data. Prentice-Hall Advanced Reference Series; Saddle River: Prentice-Hall. [Google Scholar]

- Jan, Amin, Maran Marimuthu, Muhammad Pisol, Mat Isa, and Pia A. Albinsson. 2018. Sustainability practices and banks financial performance: A conceptual review from the Islamic banking industry in Malaysia. International Journal Business Management 13. [Google Scholar] [CrossRef] [Green Version]

- Jan, Amin, Maran Marimuthu, Muhammad Pisol bin Mohd, and Mat Isa. 2019. The nexus of sustainability practices and financial performance: From the perspective of Islamic banking. Journal of Cleaner Production 228: 703–17. [Google Scholar] [CrossRef]

- Jan, Amin, Mário Nuno Mata, Pia A. Albinsson, José Moleiro Martins, Rusni Bt Hassan, and Pedro Neves Mata. 2021. Alignment of Islamic banking sustainability indicators with sustainable development goals: Policy recommendations for addressing the COVID-19 pandemic. Sustainability 13: 2607. [Google Scholar] [CrossRef]

- Kendall, Maurice George. 1948. Rank Correlation Methods. Santa Barbara: Griffin. [Google Scholar]

- Khan, M. Mansoor, and M. Ishaq Bhatti. 2008. Islamic banking and finance: On its way to globalization. Managerial Finance 34: 708–25. [Google Scholar] [CrossRef] [Green Version]

- KSA. 2017. Kingdom of Saudi Arabia: Vision 2030. Available online: https://www.vision2030.gov.sa/ (accessed on 10 May 2021).

- Lester, Rodney. 2011. The Insurance Sector in the Middle East and North Africa: Challenges and Development Agenda. Washington, DC: The World Bank. [Google Scholar]

- Lone, Fayaz Ahmad, and Salim Alshehri. 2015. Growth and potential of Islamic banking in GCC: The Saudi Arabia experience. Journal of Islamic Banking 3: 35–43. [Google Scholar] [CrossRef]

- Long, David E. 2005. Culture and customs of Saudi Arabia. University Park: Penn State Press. [Google Scholar]

- McKinsey. 2015. Saudi Arabia beyond Oil: The Investment and Productivity Transformation. McKinsey Global Institute. Available online: https://www.mckinsey.com/~/media/McKinsey/Featured%20Insights/Employment%20and%20Growth/Moving%20Saudi%20Arabias%20economy%20beyond%20oil/MGI%20Saudi%20Arabia_Executive%20summary_December%202015.pdf (accessed on 10 May 2021).

- Murphy, Caryle. 2012. A Kingdom’s Future: Saudi Arabia through the Eyes of Its Twentysomethings. Washington, DC: Woodrow Wilson International Center for Scholars, Middle East Program. [Google Scholar]

- Nereim, Vivian, and Reema Al Othman. 2020. Saudi Arabia Less Pessimistic than IMF as Economy Shrinks Again. New York: Bloomberg. [Google Scholar]

- Nicola, Maria, Zaid Alsafi, Catrin Sohrabi, Ahmed Kerwan, Ahmed Al-Jabir, Christos Iosifidis, Maliha Agha, and Riaz Agha. 2020. The socio-economic implications of the coronavirus and COVID-19 pandemic: A review. International Journal of Surgery 78: 185–93. [Google Scholar] [CrossRef] [PubMed]

- Noor, Osama. 2020. Saudi Arabia: Insurance Sector Returns to Growth in 2019. Middle East Insurance Review. Available online: https://www.meinsurancereview.com/News/View-NewsLetter-Article?id=61174&Type=MiddleEast (accessed on 10 May 2021).

- Nurunnabi, Mohammad. 2020. Recovery planning and resilience of SMEs during the COVID-19: Experience from Saudi Arabia. Journal of Accounting & Organizational Change 16: 643–53. [Google Scholar]

- OECD. 2020. COVID-19 Crisis Response in MENA Countries. Paris: OECD. [Google Scholar]

- Oilprice.com. 2021. Available online: Oilprice.com (accessed on 10 May 2021).

- Orlando, Giuseppe, and Maximilian Haertel. 2014. A parametric approach to counterparty and credit risk. Journal of Credit Risk 10. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2789610 (accessed on 20 May 2021).

- Orlando, Giuseppe, and Roberta Pelosi. 2020. Non-performing loans for Italian companies: When time matters. an empirical research on estimating probability to default and loss given default. International Journal of Financial Studies 8: 68. [Google Scholar] [CrossRef]

- Oxford Business Group. 2013. Saudi Arabia’s Insurance Sector Set for Consolidation. Dubai: Oxford Business Group. [Google Scholar]

- Parkinson, Andrew. 2016. Saudi Banks: Peer Review. New York: Fitch Ratings. [Google Scholar]

- Platonova, Elena, Mehmet Asutay, Rob Dixon, and Sabri Mohammad. 2018. The impact of corporate social responsibility disclosure on financial performance: Evidence from the GCC Islamic banking sector. Journal of Business Ethics 151: 451–71. [Google Scholar] [CrossRef] [Green Version]

- Raghu, Mandagolathu. 2016. Saudi Arabia and Its US Dollar Peg Dilemma. The National. Available online: https://www.thenationalnews.com/business/saudi-arabia-and-its-us-dollar-peg-dilemma-1.146367 (accessed on 10 May 2021).

- Ramsdale, Redmond, and Amin Sakhri. 2020. Saudi Banks: 2019 Results Dashboard. New York: Fitch Ratings. [Google Scholar]

- Ramsdale, Redmond, Amin Sakhri, Marc Ellsmore, and Nicolas Charreyron. 2020. Saudi Arabian Banks: Peer Review. New York: Fitch Ratings. [Google Scholar]

- SAMA. 2020. SAMA—Annual Statistics 2019. Riyadh: SAMA. [Google Scholar]

- SAMA. 2020. Saudi Arabia Monetary Authority. Riyadh: SAMA. [Google Scholar]

- Saudi Arabian Monetary Agency. 2009. Annual Report 2009. Riyadh: SAMA. [Google Scholar]

- Schmalz, Martin C. 2018. Common-ownership concentration and corporate conduct. Annual Review of Financial Economics 10: 413–48. [Google Scholar] [CrossRef] [Green Version]

- Shahina, Alaa, Stefania Bianchi, and Zainab Fattah. 2016. Saudi Arabia Injects $5.3 Billion into Banks to Ease Crunch. New York: Bloomberg. [Google Scholar]

- Sharif, Arif. 2016. Reality Check for Saudi Banks. New York: Bloomberg. [Google Scholar]

- Sillah, Bukhari MS, and Nizar Harrathi. 2015. Bank efficiency analysis: Islamic banks versus conventional banks in the Gulf Cooperation Council Countries 2006–2012. International Journal of Financial Research 6: 143–50. [Google Scholar] [CrossRef] [Green Version]

- Tadawul. 2017. Nomu—The Saudi Parallel Market. Riyadh: Tadawul. [Google Scholar]

- Tadawul. 2019. Tadawul—Saudi Stock Exchange. Riyadh: Tadawul. [Google Scholar]

- Tadawul. 2020. Tadawul—Saudi Stock Exchange. Riyadh: Tadawul. [Google Scholar]

- Teresiene, Deimante, Greta Keliuotyte-Staniuleniene, and Rasa Kanapickiene. 2021. Sustainable Economic Growth Support through Credit Transmission Channel and Financial Stability: In the Context of the COVID-19 Pandemic. Sustainability 13: 2692. [Google Scholar] [CrossRef]

- The Global Economy. 2016. Saudi Arabia: Stock Market Capitalization, in Dollars. Atlanta: The Global Economy, Available online: http://www.theglobaleconomy.com/Saudi-Arabia/stock_market_capitalization_dollars/ (accessed on 27 October 2016).

- Toskas, Panagiotis, and Graham Coutts. 2020. Industry Profile and Operating Environment: Saudi Arabian Insurance. New York: Fitch Ratings. [Google Scholar]

- Tradingeconomics. 2020. Saudi-Arabia Stock Market. Tradingeconomics: Available online: https://www.saudiexchange.sa/wps/portal/tadawul/home/ (accessed on 10 May 2021).

- Visser, Hans. 2019. Islamic Finance: Principles and Practice. Jotham: Edward Elgar Publishing. [Google Scholar]

- Vogel, Frank E. 2000. Islamic Law and the Legal System of Saudí: Studies of Saudi Arabia. Leiden: Bril, vol. 8. [Google Scholar]

- World Bank. 2020. Market Capitalization of Listed Domestic Companies (% of GDP)—Saudi Arabia. Washington, DC: World Bank. [Google Scholar]

| 2017 | 2018 | 2019 | 2020 | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Q1 | Q2 | Q3 | Q4 | Q1 | Q2 | Q3 | Q4 | Q1 | Q2 | Q3 | Q4 | Q1 | Q2 | Q3 | ||

| 1 | Agriculture, Forestry & Fishing | 1 | 0 | 0 | 1 | 0 | 1 | 0 | 0 | 1 | 1 | 2 | 2 | 0 | −10 | 1 |

| 2 | Mining & Quarrying | −1.7 | −2.2 | −4.7 | −5.2 | 0.6 | 1.6 | 4.2 | 8.1 | 1.0 | −2.9 | −6.4 | −5.9 | −2.8 | −4.5 | −7.2 |

| (a) Crude Petroleum & Natural Gas | −1.8 | −2.3 | −4.8 | −5.3 | 0.6 | 1.6 | 4.2 | 8.1 | 1.0 | −3.0 | −6.5 | −6.0 | −2.9 | −4.5 | −7.3 | |

| (b) Other | 5.3 | 3.1 | 4.3 | 4.7 | 5.5 | 2.3 | 0.5 | 0.8 | 4.5 | 2.5 | 6.9 | 5.3 | 4.6 | −3.3 | 1.0 | |

| 3 | Manufacturing | −0.2 | 2.0 | 2.7 | 0.8 | 2.5 | 2.0 | 1.7 | 2.2 | 0.0 | −2.3 | −2.4 | −1.6 | −8.8 | −11.6 | −10.1 |

| (a) Petroleum Refining | −3.0 | 6.9 | 3.9 | 0.5 | −0.1 | −3.1 | −2.1 | −3.4 | 1.5 | −3.8 | −6.1 | −4.0 | −24.2 | −14.0 | −18.4 | |

| (b) Other | 1.0 | −0.2 | 2.1 | 0.9 | 3.6 | 4.4 | 3.4 | 4.8 | −0.6 | −1.6 | −0.8 | −0.5 | −2.6 | −10.5 | −6.6 | |

| 4 | Electricity, Gas and Water | −1.5 | 0.8 | 2.6 | 0.8 | 2.9 | −0.1 | 3.6 | 0.4 | 1.1 | −6.3 | −4.8 | −1.2 | 0.2 | −7.8 | 0.1 |

| 5 | Construction | −3.3 | −5.2 | −1.6 | −2.9 | −2.4 | −2.8 | −3.6 | −5.0 | 1.3 | 4.9 | 4.6 | 7.7 | 2.2 | −4.7 | 0.2 |

| 6 | Wholesale & Retail Trade, Restaurants & Hotels | −2.0 | 0.3 | 2.4 | 1.6 | 0.7 | 0.6 | 0.9 | 1.5 | 1.9 | 5.8 | 8.0 | 9.2 | 4.8 | −18.3 | −5.2 |

| 7 | Transport, Storage & Communication | 1.8 | 0.9 | 3.5 | 2.9 | −0.1 | 0.4 | 5.4 | 2.8 | 4.9 | 6.4 | 5.6 | 5.5 | 4.1 | −16.3 | −6.3 |

| 8 | Finance, Insurance, Real Estate | 4.1 | 4.7 | 5.4 | 7.1 | 2.6 | 3.4 | 2.6 | 4.0 | 4.8 | 5.4 | 6.3 | 5.6 | 1.0 | −0.7 | 1.1 |

| (a) Crude Petroleum & Natural Gas | 5.9 | 6.3 | 5.4 | 5.2 | 3.0 | 2.2 | 2.1 | 2.9 | 4.8 | 2.4 | 3.1 | 3.2 | −1.4 | −1.1 | 1.6 | |

| (b) Others | 1.9 | 2.8 | 5.5 | 9.2 | 2.1 | 4.8 | 3.1 | 5.2 | 4.9 | 9.0 | 10.0 | 8.1 | 3.9 | −0.3 | 0.6 | |

| 9 | Community, Social & Personal Services | 1.3 | 1.5 | 0.6 | 2.0 | 5.0 | 6.6 | 4.4 | 4.6 | 4.4 | 7.4 | 7.8 | 8.4 | 3.7 | −12.6 | −5.5 |

| 10 | Imputed Bank Services Charge | 0.8 | 1.0 | 1.1 | 2.0 | −4.2 | 1.1 | 2.1 | 6.0 | 1.2 | 4.3 | 5.2 | 3.2 | 7.8 | 9.3 | 5.3 |

| Sub—Total | −0.6 | −0.4 | −0.9 | −1.3 | 1.1 | 1.5 | 2.9 | 4.6 | 1.8 | 0.2 | −1.2 | −0.5 | −1.5 | −7.8 | −5.6 | |

| B. Producers of Government Services | −2.2 | 0.3 | 2.4 | 1.1 | 3.4 | 4.4 | 1.6 | 2.4 | 1.1 | 0.8 | 4.4 | 0.2 | 1.5 | −1.3 | 1.8 | |

| Total Except Import Duties | −0.9 | −0.3 | −0.5 | −0.9 | 1.4 | 1.9 | 2.7 | 4.3 | 1.7 | 0.3 | −0.5 | −0.4 | −1.0 | −7.0 | −4.7 | |

| Import Duties | 26.6 | −29.1 | 49.8 | −37.6 | −6.2 | −38.4 | −28.0 | 2.4 | 0.4 | 26.0 | 1.9 | 8.8 | 4.7 | −11.9 | 4.0 | |

| Gross Domestic Product | −0.7 | −0.7 | −0.2 | −1.3 | 1.4 | 1.6 | 2.4 | 4.3 | 1.7 | 0.5 | −0.5 | −0.3 | −1.0 | −7.0 | −4.6 | |

| Total General Insurance | Total Health Insurance | Protection and Saving Insurance | Total | |

|---|---|---|---|---|

| 2019 | ||||

| Gross Written Premiums | 14,280.70 | 22,474.91 | 1,134.88 | 37,890.49 |

| change y/y | 1.80% | 13.03% | 2.92% | 8.21% |

| Net Written Premiums | 9260.57 | 21,621.95 | 797.20 | 31,679.73 |

| change y/y | −6.73% | 11.92% | 0.30% | 5.45% |

| Retention Ratio | 64.85 | 96.20 | 70.25 | 231.30 |

| change y/y | −8.38% | −0.99% | −0.26% | −2.97% |

| GWP SAR’000 | Pre-Zakat Profit/Loss SAR’000 | ||||||

|---|---|---|---|---|---|---|---|

| # | Company | 2019 | 2018 | Change % | Market Share % (2019) | 2019 | 2018 |

| 1 | Bupa | 10,410,868 | 8,566,648 | 21.53% | 28.19% | 712,654 | 525,431 |

| 2 | Tawuniya | 8,375,860 | 7,641,245 | 9.61% | 22.68% | 402,165 | −213,339 |

| 3 | Al-Rajhi | 2,569,804 | 2,973,594 | −13.58% | 6.96% | 108,885 | 185,027 |

| 4 | Medgulf | 2,421,277 | 2,069,473 | 17.00% | 6.56% | 19,176 | −204,527 |

| 5 | AXA Arabia | 1,409,777 | 1,445,860 | −2.50% | 3.82% | 108,474 | 76,426 |

| 6 | Walaa (Saudi United) | 1,215,394 | 1,104,957 | 9.99% | 3.29% | 23,159 | 100,365 |

| 7 | Allianz SF | 1,011,666 | 870,716 | 16.19% | 2.74% | 41,614 | 37,050 |

| 8 | Al Etihad | 861,936 | 929,776 | −7.30% | 2.33% | 64,308 | 88,136 |

| 9 | Malath | 835,236 | 729,076 | 14.56% | 2.26% | 18,365 | 15,630 |

| 10 | SAICO | 834,341 | 949,993 | −12.17% | 2.26% | −2382 | −13,013 |

| 11 | Wataniya | 735,044 | 712,324 | 3.19% | 1.99% | 23,783 | 20,433 |

| 12 | Gulf Union | 558,796 | 328,002 | 70.36% | 1.51% | −30,739 | 5,750 |

| 13 | Arabian Shield | 543,717 | 625,101 | −13.02% | 1.47% | 16,941 | 34,292 |

| 14 | ACIG | 529,352 | 500,013 | 5.87% | 1.43% | 7155 | 2,358 |

| 15 | SALAMA | 503,504 | 734,982 | −31.49% | 1.36% | −54,115 | 16,343 |

| 16 | Saqr | 455,703 | 350,379 | 30.06% | 1.23% | −39,861 | 818 |

| 17 | United Cooperative | 420,292 | 391,968 | 7.23% | 1.14% | 15,539 | −60,172 |

| 18 | Solidarity | 391,021 | 245,857 | 59.04% | 1.06% | −43,920 | −59,695 |

| 19 | Arabia Cooperative | 332,418 | 350,787 | −5.24% | 0.90% | −37,762 | 3419 |

| 20 | Alinma Tokio Marine | 331,141 | 353,591 | −6.35% | 0.90% | −34,031 | −31,746 |

| 21 | Buruj | 305,541 | 319,997 | −4.52% | 0.83% | 15,186 | 72,417 |

| 22 | Gulf General | 279,690 | 264,675 | 5.67% | 0.76% | −3,789 | −28,927 |

| 23 | Chubb Arabia | 258,223 | 233,973 | 10.36% | 0.70% | 35,398 | 49,497 |

| 24 | Amana | 248,054 | 137,446 | 80.47% | 0.67% | −27,706 | −20,217 |

| 25 | Ahli Takaful | 238,841 | 338,346 | −29.41% | 0.65% | 13,746 | 10,421 |

| 26 | Al Alamiya | 219,941 | 293,533 | −25.07% | 0.60% | 23,659 | 31,263 |

| 27 | Al Ahlia | 192,248 | 172,981 | 11.14% | 0.52% | −44,210 | 15,815 |

| 28 | SABB takaful | 155,153 | 139,966 | 10.85% | 0.42% | −19,098 | 1056 |

| 29 | Enaya | 154,028 | 138,244 | 11.42% | 0.42% | −101,352 | −91,835 |

| 30 | Aljazira Takaful | 130,283 | 101,145 | 28.81% | 0.35% | 37,755 | 31,840 |

| Total | 36,929,149 | 34,014,648 | 8.57% | 100.00% | 1,248,997 | 600,316 | |

| Ante COVID-19 | With COVID-19 | ||||||

|---|---|---|---|---|---|---|---|

| # | Company | Code | Corr. with TASI | Corr. with Oil | Corr. with TASI | Corr. with Oil | Perf. |

| 1 | Gulf Union Alahlia | 8120 | 0.58 | 0.39 | 0.00 | −0.19 | 41.65% |

| 2 | Bupa | 8210 | −0.07 | −0.26 | −0.18 | −0.45 | 39.02% |

| 3 | Malath Coop. Ins. | 8020 | 0.22 | −0.06 | 0.17 | −0.08 | 85.01% |

| 4 | Allianz Saudi Fransi | 8040 | 0.16 | −0.11 | 0.16 | 0.35 | −19.09% |

| 5 | Arabian Shield | 8070 | 0.37 | 0.34 | 0.28 | 0.10 | 48.89% |

| 6 | Salama | 8050 | 0.51 | 0.36 | −0.05 | −0.19 | 56.68% |

| 7 | Walaa Coop. Ins. | 8060 | 0.18 | 0.52 | 0.34 | 0.16 | 12.38% |

| 8 | Al-Etihad | 8170 | 0.58 | 0.31 | 0.27 | 0.08 | 37.09% |

| 9 | Al Rajhi Ins. | 8230 | 0.27 | 0.50 | 0.12 | −0.07 | 23.21% |

| 10 | AXA Coop. Ins. | 8250 | 0.57 | 0.48 | −0.16 | −0.43 | 68.71% |

| 11 | Wataniya Ins. | 8300 | 0.27 | −0.06 | −0.00 | −0.24 | 88.98% |

| 12 | Riyad Bank | 1010 | 0.65 | 0.56 | 0.50 | 0.69 | 1.13% |

| 13 | Bank AlJazira | 1020 | 0.70 | 0.57 | 0.35 | 0.54 | −13.23% |

| 14 | Saudi Inv. Bank | 1030 | 0.77 | 0.55 | 0.40 | 0.59 | −22.05% |

| 15 | Banque Saudi Fransi | 1050 | 0.65 | 0.53 | 0.50 | 0.65 | −0.38% |

| 16 | Saudi British Bank | 1060 | 0.65 | 0.52 | 0.38 | 0.78 | −22.06% |

| 17 | Arab National Bank | 1080 | 0.51 | 0.46 | 0.27 | 0.64 | −11.32% |

| 18 | Samba Financial Group | 1090 | 0.60 | 0.59 | 0.47 | 0.65 | −8.09% |

| 19 | Al Rajhi Banking | 1120 | 0.19 | 0.36 | 0.43 | 0.20 | 20.32% |

| 20 | Bank Albilad | 1140 | 0.60 | 0.28 | 0.39 | 0.24 | 22.97% |

| 21 | Alinma Bank | 1150 | 0.77 | 0.57 | 0.39 | 0.67 | −30.13% |

| 22 | National Comm. Bank | 1180 | 0.48 | 0.49 | 0.48 | 0.78 | −6.52% |

| Panel: Fixed Effects (within) (FE) | ||||

|---|---|---|---|---|

| N = 1078 | n = 22 | T = 49 (Balanced panel) | ||

| R-squared = 0.095 | ||||

| Wald F(3, 1053) = 36.755 | p-value < 0.001 | |||

| RSS = 34.686 | ESS = 12.274 | TSS = 12.274 | ||

| Stock Extra Perf. | Coefficient | Std. Error | t-stat | p-value |

| Stock Trad. Volumes | 0.066 | 0.008 | 7.952 | 0.000 *** |

| Brent Trad. Volumes | −0.021 | 0.003 | −6.699 | 0.000 *** |

| Interaction | −0.013 | 0.006 | −2.345 | 0.019 ** |

| Panel: Fixed effects (within) (FE) | ||||

|---|---|---|---|---|

| N = 550 | n = 22 | T = 25 (Balanced panel) | ||

| R-squared = 0.088 | ||||

| Wald F(3, 525) = 16.949 | p-value = 0.000 | |||

| RSS = 6.402 | ESS = 6.264 | TSS = 6.264 | ||

| Stock Extra Perf. | Coefficient | Std. Error | t-stat | p-value |

| Stock Trad. Volumes | 0.010465 | 0.006042 | 1.7319 | 0.084 * |

| Brent Trad. Volumes | −0.01471 | 0.002449 | −6.0084 | 0 *** |

| Interaction | −0.00558 | 0.002057 | −2.711 | 0.007 *** |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Orlando, G.; Bace, E. Challenging Times for Insurance, Banking and Financial Supervision in Saudi Arabia (KSA). Adm. Sci. 2021, 11, 62. https://doi.org/10.3390/admsci11030062

Orlando G, Bace E. Challenging Times for Insurance, Banking and Financial Supervision in Saudi Arabia (KSA). Administrative Sciences. 2021; 11(3):62. https://doi.org/10.3390/admsci11030062

Chicago/Turabian StyleOrlando, Giuseppe, and Edward Bace. 2021. "Challenging Times for Insurance, Banking and Financial Supervision in Saudi Arabia (KSA)" Administrative Sciences 11, no. 3: 62. https://doi.org/10.3390/admsci11030062

APA StyleOrlando, G., & Bace, E. (2021). Challenging Times for Insurance, Banking and Financial Supervision in Saudi Arabia (KSA). Administrative Sciences, 11(3), 62. https://doi.org/10.3390/admsci11030062