From Social to Financial: Understanding Trust in Extended Payment Services on Social Networking Platforms

Abstract

1. Introduction

2. Literature Review and Hypothesis Development

2.1. Theoretical Framework

2.1.1. KakaoPay: Transforming Mobile SNSs to Mobile Payment Services

2.1.2. Spillover Effect

2.1.3. Schema Congruity Theory

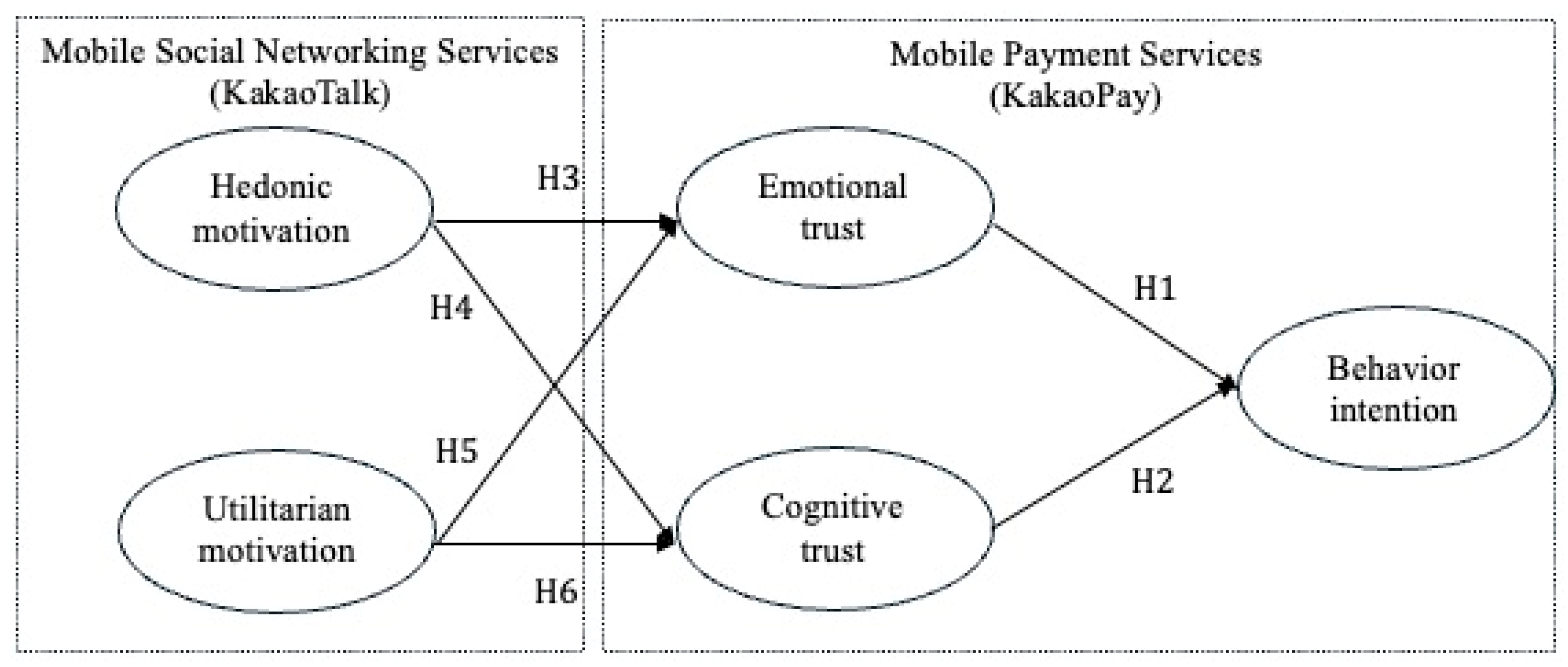

2.2. Hypothesis Development

2.2.1. User Trust and Behavioral Intention for KakaoPay

2.2.2. Motivation for the Use of Primary Services and Trust in Extended Services

2.2.3. The Strength of the Relationship Between Motivation and Trust

3. Research Methodology

3.1. Research Design

3.2. Measures

3.3. Data Collection Process

4. Data Analysis and Results

4.1. Reliability and Validity Analysis

4.2. Common Method Bias

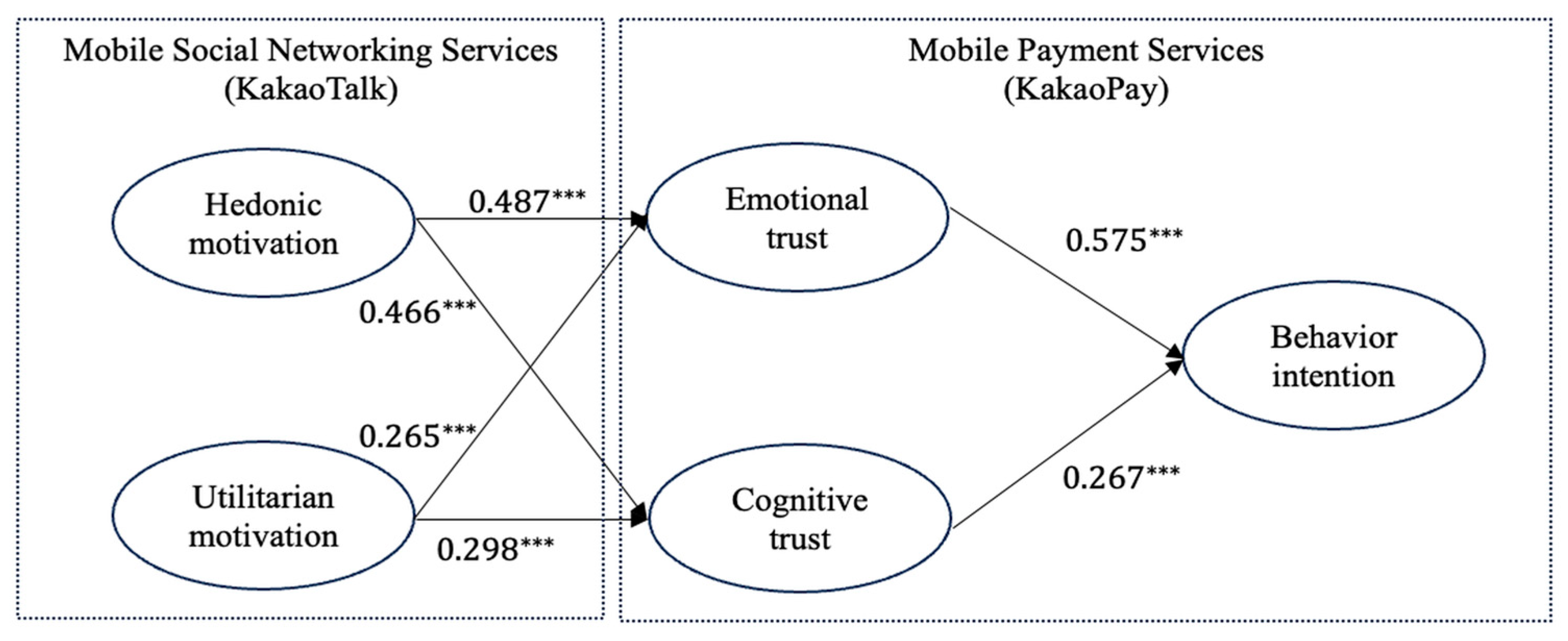

4.3. Path Analysis and Hypothesis Testing

5. Discussion

5.1. Theoretical Implications

5.2. Practical Implications

5.3. Limitations and Future Research

5.4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A. Constructs and Measurement Items

| Constructs | Code | Items | Reference |

| Hedonic motivation (HM) | HM1 | Using KakaoTalk piques my curiosity. | Salimon et al. (2017) |

| HM2 | Using KakaoTalk would provide a lot of pleasure. | ||

| HM3 | KakaoTalk has a lot of fun features. | ||

| HM4 | Using KakaoTalk would be always fun. | ||

| HM5 | I am always happy with KakaoTalk’s features. | ||

| HM6 | Using KakaoTalk would make me feel good. | ||

| HM7 | Overall, using KakaoTalk would be enjoyable. | ||

| Utilitarian motivation (UM) | UM1 | Using KakaoTalk could provide a lot of information quickly and easily. | Chen et al. (2013); H. Lee and Cho (2020) |

| UM2 | Using KakaoTalk could provide useful information. | ||

| UM3 | Using KakaoTalk could teach you things you did not know. | ||

| UM4 | Using KakaoTalk could provide helpful information. | ||

| UM5 | Using KakaoTalk is a cheap way to get information. | ||

| UM6 | Using KakaoTalk is helpful to me. | ||

| UM7 | Using KakaoTalk makes my job more productive. | ||

| UM8 | KakaoTalk is a great tool for getting things done quickly. | ||

| Cognitive trust (CT) | CT1 | I feel that payments and transfers using KakaoPay are accurate. | Dwyer et al. (2007); G. Kim et al. (2009) |

| CT2 | I feel that using KakaoPay for payments and transfers is safe. | ||

| CT3 | I feel that using KakaoPay for payments and transfers is reliable. | ||

| Emotional trust (ET) | ET1 | I feel secure using KakaoPay services. | Komiak and Benbasat (2006) |

| ET2 | I feel comfortable using KakaoPay services. | ||

| ET3 | I feel satisfied with KakaoPay services. | ||

| Behavior intention (BI) | BI1 | I intend to continue using KakaoPay in the future. | |

| BI2 | I plan to use KakaoPay more frequently in the future than now. |

References

- Aaker, D. A., & Keller, K. L. (1990). Consumer evaluations of brand extensions. Journal of Marketing, 54(1), 27–41. [Google Scholar] [CrossRef]

- Akdim, K., Casaló, L. V., & Flavián, C. (2022). The role of utilitarian and hedonic aspects in the continuance intention to use social mobile apps. Journal of Retailing and Consumer Services, 66, 102888. [Google Scholar] [CrossRef]

- Alalwan, A. A., Dwivedi, Y. K., Rana, N. P., Lal, B., & Williams, M. D. (2015). Consumer adoption of internet banking in Jordan: Examining the role of hedonic motivation, habit, self-efficacy and trust. Journal of Financial Services Marketing, 20(2), 145–157. [Google Scholar] [CrossRef]

- Anan, L., Chen, J., Mahajan, D., & Nadeau, M. C. (2022). Consumer trends in digital payments. McKinsey & Company. [Google Scholar]

- Anderson, K. C., Knight, D. K., Pookulangara, S., & Josiam, B. (2014). Influence of hedonic and utilitarian motivations on retailer loyalty and purchase intention: A facebook perspective. Journal of Retailing and Consumer Services, 21(5), 773–779. [Google Scholar] [CrossRef]

- Bhaduri, G. (2019). Expectations matter: Evaluation of brand’s pro-environmental initiatives based on consumers’ brand schemas and brand familiarity. Journal of Global Fashion Marketing, 11(1), 37–55. [Google Scholar] [CrossRef]

- Bhaduri, G., Ha-Brookshire, J. E., & Leshner, G. (2017). Too good to be true? Effect of consumers’ brand schemas on apparel brands’ fair labor marketing messages. Clothing and Textiles Research Journal, 35(3), 187–203. [Google Scholar] [CrossRef]

- Bitner, M. J. (1990). Evaluating service encounters: The effects of physical surroundings and employee responses. Journal of Marketing, 54(2), 69–82. [Google Scholar] [CrossRef]

- Briley, D. A., Morris, M. W., & Simonson, I. (2000). Reasons as carriers of culture: Dynamic versus dispositional models of cultural influence on decision making. Journal of Consumer Research, 27(2), 157–178. [Google Scholar] [CrossRef]

- Browne, M. W., & Cudeck, R. (1992). Alternative ways of assessing model fit. Sociological Methods & Research, 21(2), 230–258. [Google Scholar] [CrossRef]

- Calefato, F., Lanubile, F., & Novielli, N. (2015). The role of social media in affective trust building in customer–supplier relationships. Electronic Commerce Research, 15(4), 453–482. [Google Scholar] [CrossRef]

- Carter, R. E., & Curry, D. J. (2011). Perceptions versus performance when managing extensions: New evidence about the role of fit between a parent brand and an extension. Journal of the Academy of Marketing Science, 41(2), 253–269. [Google Scholar] [CrossRef]

- Chan, E. Y., & Saqib, N. U. (2015). Online social networking increases financial risk-taking. Computers in Human Behavior, 51, 224–231. [Google Scholar] [CrossRef]

- Chang, S. H., Chih, W. H., Liou, D. K., & Yang, Y. T. (2016). The mediation of cognitive attitude for online shopping. Information Technology & People, 29(3), 618–646. [Google Scholar] [CrossRef]

- Chauhan, V. (2024). Understanding users’ protective behavior and its suppressor effect on the perceived risk in M-wallet/banking use: An Indian urban-rural comparison. Technological Forecasting and Social Change, 201, 123255. [Google Scholar] [CrossRef]

- Chen, G. L., Yang, S. C., & Tang, S. M. (2013). Sense of virtual community and knowledge contribution in a P3 virtual community. Internet Research, 23(1), 4–26. [Google Scholar] [CrossRef]

- Cheong, Y., & Kim, K. (2011). The interplay between advertising claims and product categories in food advertising: A schema congruity perspective. Journal of Applied Communication Research, 39(1), 55–74. [Google Scholar] [CrossRef]

- Chin, A. G., Harris, M. A., & Brookshire, R. (2022). An empirical investigation of intent to adopt mobile payment systems using a trust-based extended valence framework. Information Systems Frontiers, 24(1), 329–347. [Google Scholar] [CrossRef]

- Choi, B., & Lee, I. (2017). Trust in open versus closed social media: The relative influence of user- and marketer-generated content in social network services on customer trust. Telematics and Informatics, 34(5), 550–559. [Google Scholar] [CrossRef]

- Chopdar, P. K., Korfiatis, N., Sivakumar, V. J., & Lytras, M. D. (2018). Mobile shopping apps adoption and perceived risks: A cross-country perspective utilizing the unified theory of acceptance and use of technology. Computers in Human Behavior, 86, 109–128. [Google Scholar] [CrossRef]

- Cook, K. S., & Emerson, R. M. (1987). Social exchange theory. Newbury Park. [Google Scholar]

- Dash, G., & Paul, J. (2021). CB-SEM vs. PLS-SEM methods for research in social sciences and technology forecasting. Technological Forecasting and Social Change, 173, 121092. [Google Scholar] [CrossRef]

- de Blanes Sebastián, M. G., Antonovica, A., & Sarmiento Guede, J. R. (2023). What are the leading factors for using Spanish peer-to-peer mobile payment platform Bizum? The applied analysis of the UTAUT2 model. Technological Forecasting and Social Change, 187, 122235. [Google Scholar] [CrossRef]

- de Sena Abrahão, R., Moriguchi, S. N., & Andrade, D. F. (2016). Intention of adoption of mobile payment: An analysis in the light of the unified theory of acceptance and use of technology (UTAUT). RAI Revista de Administracao e Inovacao, 13(3), 221–230. [Google Scholar] [CrossRef]

- Deci, E. L., & Ryan, R. M. (1985). The general causality orientations scale: Self-determination in personality. Journal of Research in Personality, 19(2), 109–134. [Google Scholar] [CrossRef]

- Dimitriadis, S., & Kyrezis, N. (2010). Linking trust to use intention for technology-enabled bank channels: The role of trusting intentions. Psychology & Marketing, 27(8), 799–820. [Google Scholar] [CrossRef]

- Dwyer, C., Hiltz, S., & Passerini, K. (2007, August 9). Trust and privacy concern within social networking sites—A comparison of Facebook and MySpace [Conference paper]. Americas Conference on Information Systems (AMCIS 2007), Keystone, CO, USA. [Google Scholar]

- Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39–50. [Google Scholar] [CrossRef]

- Gefen, D. (2000). E-commerce: The role of familiarity and trust. Omega, 28(6), 725–737. [Google Scholar] [CrossRef]

- Gefen, D., & Straub, D. W. (2004). Consumer trust in B2C e-Commerce and the importance of social presence: Experiments in e-Products and e-Services. Omega, 32(6), 407–424. [Google Scholar] [CrossRef]

- Gerrath, M. H. E. E., & Biraglia, A. (2021). How less congruent new products drive brand engagement: The role of curiosity. Journal of Business Research, 127, 13–24. [Google Scholar] [CrossRef]

- Gollwitzer, P. M. (1999). Implementation intentions: Strong effects of simple plans. American Psychologist, 54(7), 493–503. [Google Scholar] [CrossRef]

- Gong, X., Zhang, K. Z. K., Chen, C., Cheung, C. M. K., & Lee, M. K. O. (2020). What drives trust transfer from web to mobile payment services? The dual effects of perceived entitativity. Information & Management, 57(7), 103250. [Google Scholar] [CrossRef]

- Ha, H. Y., John, J., John, J. D., & Chung, Y. K. (2016). Temporal effects of information from social networks on online behavior: The role of cognitive and affective trust. Internet Research, 26(1), 213–235. [Google Scholar] [CrossRef]

- Ha, Y. W., Kim, J., Libaque-Saenz, C. F., Chang, Y., & Park, M. C. (2015). Use and gratifications of mobile SNSs: Facebook and KakaoTalk in Korea. Telematics and Informatics, 32(3), 425–438. [Google Scholar] [CrossRef]

- Huang, C. C., Chang, Y. W., Hsu, P. Y., & Prassida, G. F. (2020). A cross-country investigation of customer transactions from online to offline channels. Industrial Management & Data Systems, 120(12), 2397–2422. [Google Scholar] [CrossRef]

- Huang, S., Hai, X., Adam, N. A., Fu, Q., Ahmad, A., Zapodeanu, D., & Badulescu, D. (2022). The relationship between corporate social responsibility on social media and brand advocacy behavior of customers in the banking context. Behavioral Sciences, 13(1), 32. [Google Scholar] [CrossRef] [PubMed]

- Hwang, Y., & Kim, D. J. (2007). Customer self-service systems: The effects of perceived Web quality with service contents on enjoyment, anxiety, and e-trust. Decision Support Systems, 43(3), 746–760. [Google Scholar] [CrossRef]

- Jang, J. M., & Kim, H. (2022). Diverging influences of usability in online authentication system: The role of culture (US vs. Korea). International Journal of Bank Marketing, 40(2), 384–400. [Google Scholar] [CrossRef]

- Jebarajakirthy, C., & Shankar, A. (2021). Impact of online convenience on mobile banking adoption intention: A moderated mediation approach. Journal of Retailing and Consumer Services, 58, 102323. [Google Scholar] [CrossRef]

- Johnson, D., & Grayson, K. (2005). Cognitive and affective trust in service relationships. Journal of Business Research, 58(4), 500–507. [Google Scholar] [CrossRef]

- Kilani, A. A. H. Z., Kakeesh, D. F., Al-Weshah, G. A., & Al-Debei, M. M. (2023). Consumer post-adoption of e-wallet: An extended UTAUT2 perspective with trust. Journal of Open Innovation: Technology, Market, and Complexity, 9(3), 100113. [Google Scholar] [CrossRef]

- Kim, B. (2024). South Korea’s megacorp and super app: Kakao’s paths to market dominance. Media, Culture & Society, Advance online publication. 01634437241294207. [Google Scholar] [CrossRef]

- Kim, C., Jeon, H. G., & Lee, K. C. (2020). Discovering the role of emotional and rational appeals and hidden heterogeneity of consumers in advertising copies for sustainable marketing. Sustainability, 12(12), 5189. [Google Scholar] [CrossRef]

- Kim, G., Shin, B., & Lee, H. G. (2009). Understanding dynamics between initial trust and usage intentions of mobile banking. Information Systems Journal, 19(3), 283–311. [Google Scholar] [CrossRef]

- Kim, S. S. (2009). The integrative framework of technology use: An extension and test. MIS Quarterly, 33(3), 513–537. [Google Scholar] [CrossRef]

- Komiak, S. Y., & Benbasat, I. (2006). The effects of personalization and familiarity on trust and adoption of recommendation agents. MIS Quarterly, 30(4), 941–960. [Google Scholar] [CrossRef]

- Kruglanski, A. W., Shah, J. Y., Pierro, A., & Mannetti, L. (2002). When similarity breeds content: Need for closure and the allure of homogeneous and self-resembling groups. Journal of Personality and Social Psychology, 83(3), 648–662. [Google Scholar] [CrossRef]

- Kwak, K. T., Choi, S. K., & Lee, B. G. (2014). SNS flow, SNS self-disclosure and post hoc interpersonal relations change: Focused on Korean Facebook user. Computers in Human Behavior, 31, 294–304. [Google Scholar] [CrossRef]

- Lee, A. Y., & Labroo, A. A. (2004). The effect of conceptual and perceptual fluency on brand evaluation. Journal of Marketing Research, 41(2), 151–165. [Google Scholar] [CrossRef]

- Lee, H., & Cho, C. H. (2020). Uses and gratifications of smart speakers: Modelling the effectiveness of smart speaker advertising. International Journal of Advertising, 39(7), 1150–1171. [Google Scholar] [CrossRef]

- Lee, J., Ryu, M. H., & Lee, D. (2019). A study on the reciprocal relationship between user perception and retailer perception on platform-based mobile payment service. Journal of Retailing and Consumer Services, 48, 7–15. [Google Scholar] [CrossRef]

- Leong, L. Y., Hew, T. S., Ooi, K. B., Chong, A. Y. L., & Lee, V. H. (2021). Understanding trust in ms-commerce: The roles of reported experience, linguistic style, profile photo, emotional, and cognitive trust. Information & Management, 58(2), 103416. [Google Scholar] [CrossRef]

- Li, C., & Huang, F. (2024). The impact of virtual streamer anthropomorphism on consumer purchase intention: Cognitive trust as a mediator. Behavioral Sciences, 14(12), 1228. [Google Scholar] [CrossRef]

- Li, X., Zhu, X., Lu, Y., Shi, D., & Deng, W. (2023). Understanding the continuous usage of mobile payment integrated into social media platform: The case of WeChat Pay. Electronic Commerce Research and Applications, 60, 101275. [Google Scholar] [CrossRef]

- Lian, J. W., & Li, J. (2021). The dimensions of trust: An investigation of mobile payment services in Taiwan. Technology in Society, 67, 101753. [Google Scholar] [CrossRef]

- Lin, J., Wang, B., Wang, N., & Lu, Y. (2014). Understanding the evolution of consumer trust in mobile commerce: A longitudinal study. Information Technology and Management, 15(1), 37–49. [Google Scholar] [CrossRef]

- Lin, X., Suanpong, K., Ruangkanjanases, A., Lim, Y. T., & Chen, S. C. (2021). Improving the sustainable usage intention of mobile payments: Extended unified theory of acceptance and use of technology model combined with the information system success model and initial trust model. Frontiers in Psychology, 12, 634911. [Google Scholar] [CrossRef] [PubMed]

- Mensah, A., Ofori, K. S., Ampong, G. O. A., Addae, J. A., Kouakou, A. N., & Tumaku, J. (2018, May 29). Exploring users’ continuance intention towards mobile SNS: A mobile value perspective [Conference paper]. Emerging Technologies for Developing Countries, Cotonou, Benin. [Google Scholar] [CrossRef]

- Meyers-Levy, J., & Tybout, A. M. (1989). Schema congruity as a basis for product evaluation. Journal of Consumer Research, 16(1), 39–54. [Google Scholar] [CrossRef]

- Nan, D., Kim, Y., Park, M. H., & Kim, J. H. (2020). What motivates users to keep using social mobile payments? Sustainability, 12(17), 6878. [Google Scholar] [CrossRef]

- Newaz, M. T., Chandna, V., Dass, M., & Arnett, D. (2023). Using R-A theory and the optimal distinctiveness perspective to understand the strategic marketing approaches used by platform-based organizations: The cases of Facebook and Twitter in digital ecosystems. Journal of Business Research, 167, 114192. [Google Scholar] [CrossRef]

- Ng, E., Tan, B., Sun, Y., & Meng, T. (2022). The strategic options of fintech platforms: An overview and research agenda. Information Systems Journal, 33(2), 192–231. [Google Scholar] [CrossRef]

- Oliveira, T., Thomas, M., Baptista, G., & Campos, F. (2016). Mobile payment: Understanding the determinants of customer adoption and intention to recommend the technology. Computers in Human Behavior, 61, 404–414. [Google Scholar] [CrossRef]

- Pal, A., Herath, T., De’, R., & Rao, H. R. (2021). Is the convenience worth the risk? An investigation of mobile payment usage. Information Systems Frontiers, 23(4), 941–961. [Google Scholar] [CrossRef]

- Park, J., Amendah, E., Lee, Y., & Hyun, H. (2019). M-payment service: Interplay of perceived risk, benefit, and trust in service adoption. Human Factors and Ergonomics in Manufacturing & Service Industries, 29(1), 31–43. [Google Scholar] [CrossRef]

- Park, Y. W., & Lee, A. R. (2019). The moderating role of communication contexts: How do media synchronicity and behavioral characteristics of mobile messenger applications affect social intimacy and fatigue? Computers in Human Behavior, 97, 179–192. [Google Scholar] [CrossRef]

- Peng, X., Xing, Y., Tian, Y., Fei, M., & Wang, Q. (2023). Nonmonetary rewards of referral reward programs and recommendation intention: The role of reward–product congruity. Decision Support Systems, 173, 113999. [Google Scholar] [CrossRef]

- Podsakoff, P. M., MacKenzie, S. B., Lee, J. Y., & Podsakoff, N. P. (2003). Common method biases in behavioral research: A critical review of the literature and recommended remedies. Journal of Applied Psychology, 88(5), 879–903. [Google Scholar] [CrossRef] [PubMed]

- Salimon, M. G., Yusoff, R. Z. B., & Mohd Mokhtar, S. S. (2017). The mediating role of hedonic motivation on the relationship between adoption of e-banking and its determinants. International Journal of Bank Marketing, 35(4), 558–582. [Google Scholar] [CrossRef]

- Shan, S., Yang, Y., & Li, C. (2024). Which receives more attention, online review sentiment or online review rating? Spillover effect analysis from JD.com. Behavioral Sciences, 14(9), 823. [Google Scholar] [CrossRef]

- Simonin, B. L., & Ruth, J. A. (1998). Is a company known by the company it keeps? Assessing the spillover effects of brand alliances on consumer brand attitudes. Journal of Marketing Research, 35(1), 30–42. [Google Scholar] [CrossRef]

- Suh, B., & Han, I. (2002). Effect of trust on customer acceptance of Internet banking. Electronic Commerce Research and Applications, 1(3–4), 247–263. [Google Scholar] [CrossRef]

- Syn, S. Y., & Oh, S. (2015). Why do social network site users share information on Facebook and Twitter? Journal of Information Science, 41(5), 553–569. [Google Scholar] [CrossRef]

- Tang, Y. M., Chau, K. Y., Hong, L., Ip, Y. K., & Yan, W. (2021). Financial innovation in digital payment with WeChat towards electronic business success. Journal of Theoretical and Applied Electronic Commerce Research, 16(5), 1844–1861. [Google Scholar] [CrossRef]

- Teng, H., Xia, Q., Shou, J., & Zhao, J. (2023). Positive or negative spillover? The influence of online channel satisfaction on offline channel adoption. Journal of Business Research, 154, 113332. [Google Scholar] [CrossRef]

- Thomas, S., & Jadeja, A. (2021). Psychological antecedents of consumer trust in CRM campaigns and donation intentions: The moderating role of creativity. Journal of Retailing and Consumer Services, 61, 102589. [Google Scholar] [CrossRef]

- Wang, J., Shahzad, F., & Ashraf, S. F. (2023). Elements of information ecosystems stimulating the online consumer behavior: A mediating role of cognitive and affective trust. Telematics and Informatics, 80, 101970. [Google Scholar] [CrossRef]

- Wongkitrungrueng, A., & Assarut, N. (2020). The role of live streaming in building consumer trust and engagement with social commerce sellers. Journal of Business Research, 117, 543–556. [Google Scholar] [CrossRef]

- Wu, W., Wang, S., Ding, G., & Mo, J. (2023). Elucidating trust-building sources in social shopping: A consumer cognitive and emotional trust perspective. Journal of Retailing and Consumer Services, 71, 103217. [Google Scholar] [CrossRef]

- Xu, C., Ryan, S., Prybutok, V., & Wen, C. (2012). It is not for fun: An examination of social network site usage. Information & Management, 49(5), 210–217. [Google Scholar] [CrossRef]

- Yadav, P., Kumar, A., Mishra, S. K., & Kochhar, K. (2024). Financial equality through technology: Do perceived risks deter Indian women from sustained use of mobile payment services? International Journal of Information Management Data Insights, 4(2), 100266. [Google Scholar] [CrossRef]

- Zenker, S., Braun, E., & Gyimothy, S. (2021). Too afraid to travel? Development of a PANDEMIC (COVID-19) Anxiety Travel Scale (PATS). Tourism Management, 84, 104286. [Google Scholar] [CrossRef]

- Zhang, K. Z. K., Gong, X., Chen, C., Zhao, S. J., & Lee, M. K. O. (2019). Spillover effects from web to mobile payment services. Internet Research, 29(6), 1213–1232. [Google Scholar] [CrossRef]

- Zhao, Y., & Pan, Y. H. (2023). A study of the impact of cultural characteristics on consumers’ behavioral intention for mobile payments: A comparison between China and Korea. Sustainability, 15(8), 6956. [Google Scholar] [CrossRef]

- Zhou, T. (2011a). The effect of initial trust on user adoption of mobile payment. Information Development, 27(4), 290–300. [Google Scholar] [CrossRef]

- Zhou, T. (2011b). The impact of privacy concern on user adoption of location-based services. Industrial Management & Data Systems, 111(2), 212–226. [Google Scholar] [CrossRef]

- Zhou, T. (2013). An empirical examination of continuance intention of mobile payment services. Decision Support Systems, 54(2), 1085–1091. [Google Scholar] [CrossRef]

- Zhou, T. (2014a). An empirical examination of initial trust in mobile payment. Wireless Personal Communications, 77(2), 1519–1531. [Google Scholar] [CrossRef]

- Zhou, T. (2014b). Understanding the determinants of mobile payment continuance usage. Industrial Management & Data Systems, 114(6), 936–948. [Google Scholar] [CrossRef]

- Zhou, T., & Li, H. (2014). Understanding mobile SNS continuance usage in China from the perspectives of social influence and privacy concern. Computers in Human Behavior, 37, 283–289. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Characteristic | Category | Frequency | Percentage (%) |

|---|---|---|---|

| Gender | Male | 243 | 50.8 |

| Female | 235 | 49.2 | |

| Age (years) | 20–29 | 98 | 20.5 |

| 30–39 | 96 | 20.1 | |

| 40–49 | 84 | 17.6 | |

| 50–59 | 82 | 17.2 | |

| 60–69 | 95 | 19.9 | |

| 70–79 | 23 | 4.8 | |

| Educational level | Below high school | 113 | 23.6 |

| College/university degree | 302 | 63.2 | |

| Master’s degree | 48 | 10 | |

| Doctorate/Ph.D. | 15 | 3.1 | |

| Occupation | Student | 43 | 9 |

| Housewife | 89 | 18.6 | |

| Company worker | 254 | 53.1 | |

| Self-employed | 43 | 9 | |

| Other occupation | 49 | 10.3 |

| Construct Items | Factor Loading | AVE | C R | Cronbach’s α | ||

|---|---|---|---|---|---|---|

| KakaoTalk | Hedonic motivation (HM) | HM1 | 0.809 | 0.706 | 0.944 | 0.943 |

| HM2 | 0.846 | |||||

| HM3 | 0.853 | |||||

| HM4 | 0.873 | |||||

| HM5 | 0.796 | |||||

| HM6 | 0.830 | |||||

| HM7 | 0.872 | |||||

| Utilitarian motivation (UM) | UM1 | 0.745 | 0.638 | 0.933 | 0.933 | |

| UM2 | 0.716 | |||||

| UM3 | 0.715 | |||||

| UM4 | 0.849 | |||||

| UM5 | 0.873 | |||||

| UM6 | 0.825 | |||||

| UM7 | 0.834 | |||||

| UM8 | 0.814 | |||||

| KakaoPay | Emotional trust (ET) | ET1 | 0.840 | 0.723 | 0.887 | 0.886 |

| ET2 | 0.841 | |||||

| ET3 | 0.870 | |||||

| Cognitive trust (CT) | CT1 | 0.800 | 0.720 | 0.885 | 0.883 | |

| CT2 | 0.860 | |||||

| CT3 | 0.883 | |||||

| Behavioral intention (BI) | BI1 | 0.906 | 0.730 | 0.843 | 0.890 | |

| BI2 | 0.800 | |||||

| Mean | SD | HM | UM | ET | CT | BI | |

|---|---|---|---|---|---|---|---|

| HM | 4.910 | 1.197 | 0.840 | ||||

| UM | 5.768 | 1.298 | 0.801 ** | 0.799 | |||

| ET | 4.979 | 1.170 | 0.647 ** | 0.622 ** | 0.856 | ||

| CT | 5.107 | 1.182 | 0.643 ** | 0.633 ** | 0.783 ** | 0.849 | |

| BI | 4.779 | 1.422 | 0.481 ** | 0.511 ** | 0.682 ** | 0.642 ** | 0.854 |

| Hypothesis | B | S.E. | t-Value | Result | |

|---|---|---|---|---|---|

| H1 | ET--> BI | 0.691 *** | 0.085 | 8.108 | Supported |

| H2 | CT--> BI | 0.299 *** | 0.076 | 3.954 | Supported |

| H3 | HM --> ET | 0.451 *** | 0.077 | 5.821 | Supported |

| H4 | HM --> CT | 0.462 *** | 0.098 | 5.667 | Supported |

| H5 | UM --> ET | 0.297 *** | 0.081 | 3.193 | Supported |

| H6 | UM --> CT | 0.357 *** | 0.093 | 3.635 | Supported |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhang, Q.; Kim, H. From Social to Financial: Understanding Trust in Extended Payment Services on Social Networking Platforms. Behav. Sci. 2025, 15, 659. https://doi.org/10.3390/bs15050659

Zhang Q, Kim H. From Social to Financial: Understanding Trust in Extended Payment Services on Social Networking Platforms. Behavioral Sciences. 2025; 15(5):659. https://doi.org/10.3390/bs15050659

Chicago/Turabian StyleZhang, Qian, and Heejin Kim. 2025. "From Social to Financial: Understanding Trust in Extended Payment Services on Social Networking Platforms" Behavioral Sciences 15, no. 5: 659. https://doi.org/10.3390/bs15050659

APA StyleZhang, Q., & Kim, H. (2025). From Social to Financial: Understanding Trust in Extended Payment Services on Social Networking Platforms. Behavioral Sciences, 15(5), 659. https://doi.org/10.3390/bs15050659