1. Introduction

The reorganization of the welfare systems in OECD countries, particularly in Europe, is currently being redesigned in order to include the aging population. The most popular among the proposed solutions is “

live longer-work longer” [

1], also part of the new

Horizon 2020 framework, but the situation is not easy to deal with.

In Europe, the state has had a critical role in establishing rather generous state sponsored pensions, which were meant to provide retirement security to all older adults. These models were established after World War II, when the male-headed household was predominant and women were envisioned to be dependent upon men; even in Sweden a woman’s labor force participation was expected to be less than a man’s [

2]. This perspective has changed completely in the last 70 years, along with an emphasis on the goals of women’s economic independence and gender equality. What has been the impact of all of these changes in women’s labor market participation on gender equality in pensions? The picture was not positive before the Euro crisis in 2008 and current pension reforms may increase the gender gap in pensions [

3,

4].

Many European countries have begun (or have announced) programs intended to reduce the growth of entitlement programs, in particular of public pensions. Current costs are high, and the pressure will increase due to the aging of the population and to negative incentive effects.

The aging of populations and hampering economic growth increase pressure on public finances in many advanced capitalist societies. Consequently, governments have adopted pension reforms in order to relieve pressure on public finances. These reforms have contributed to a relative shift from public to private pension schemes. Since private social security plans are generally less redistributive than public social security, it can be hypothesized that the privatization of pension plans has led to higher levels of income inequality among the elderly [

5].

This paper focuses on the pension reform process in Europe and its links to the causes for current problems to the solutions required to make the pay-as-you-go entitlement programs in Europe sustainable above and beyond the financial crisis. It discusses current examples, which appear to be the most viable and effective options to bring entitlement systems closer to fiscal balance and still achieve their key aims. As Börsch-Supan [

6] suggests, there is no single policy prescription that can solve all problems at once. Reform elements include a freeze in the contribution and tax rates, an indexation of benefits to the dependency ratio, measures to stop the current trend towards early retirement, an adaptation of the normal retirement age to the increased life expectancy, and more reliance on private savings—elements of a sustainable but complex multi-pillar system of pensions and similar entitlement programs.

The several attempts to boost female employment, family-work reconciliation, and the representation of women in politics have targeted the younger, rather than the elderly population. Conversely, this has delayed serious consideration of the now urgent issue of the female condition during old age. Increased life expectation, demographic change, the instability of family relationships and the reform of pensions have made old women more liable to poverty [

7]. Besides, considering the elderly as a homogenous population, regardless of any differences in terms of fragility, this perspective is gender-neutral—as stressed by Elder and Giele [

8]—namely, it ignores the different work and family paths of men and women, with the risk of producing new gender inequalities between different generations.

The work-family balance policies aimed to increase women’s labor market participation by particularly facilitating part-time employment, as well as by providing pension entitlements for care periods outside the labor market. This second purpose is today questioned by several reversals of regulations, which are not always visible. At the same time, however, other seemingly gender-neutral reforms generally tend to have the opposite (ambiguous) effect. They do not guarantee a good level of individual income and pension to active women and their weak “derived” right. These measures include changes in pension calculation norms and pension composition, increasing the importance of non-public pensions [

9].

Older pension age and reduced social buffers, such as long-term unemployment benefits (currently supporting large numbers of men and women before they are due to reach pension age) could further weaken many old people, especially women, and make them more vulnerable than in the past [

10].

In the long term, the non-sustainability of universal benefits and social buffers has been exposed by the very structure of welfare systems. The most affected are the intermittently unemployed and people (such as single women, women who have never worked, or women who have divorced late in life) whose family situations cannot ensure well-being or financial security at difficult times. The loosening link between marriage and motherhood poses questions for pension systems still largely based on the male breadwinner model of pension provision for carers. So far, many women in Europe (especially in Southern Europe) including those who have been working for some years before motherhood, can rarely satisfy all the criteria necessary for the entitlement to a decent pension [

11].

Future female pensioners will not be in a significantly better position. In fact, they will be worse off because austerity measures under the guise of “pension reforms” are designed to reduce or eliminate the pension benefits, which are most critical for women. The numerous direct and indirect pension-determining factors related to life courses and welfare arrangements are interlinked on many sides and have been changing dramatically [

12,

13]. Welfare and social policy regimes are very unbalanced and do not recognize families’ and women’s needs with exception of widowhood in some countries. The wage gap is only a small part of the picture as there could be gender equality in wages, but still great inequality in lifetime earnings and thus a very large pension gap. For older women, this means facing a high risk of living alone, without economies of scale, with a reduced pension income and a high risk of mobility limitations. Therefore, a different concept of gender equality is necessary for older adults.

Moving from recent life-course theories and studies, this article looks at the effect of work-life policies options on the increasing gender pension gap in Italy within the context of Europe. It shows the main cultural and structural factors related to life courses and welfare arrangements. Their cumulative effects result in (continued) significant gender gaps across Europe with differences in single countries. In Italy in particular, family-work balance and the job market will probably increase this gap for older generations of women.

2. Gender Pension Gap for Old Women in Europe

Gender inequalities are relevant to life paths and welfare options (e.g., occupational rates, remuneration, and parental leaves), as well as their long-term effects (e.g., the gender pension gap).

Pensions are an important determinant for their beneficiaries’ economic independence. When examining independence for people in working age, we are naturally led to think about the gender pay gap. Focusing on gaps in pensions would be the natural follow-up to an interest in gender pay gaps. Those gaps would reflect the cumulated disadvantages of a career spent in a gender-biased labor market. This is even truer for older cohorts. Pension systems are not simply neutral reflections: they may amplify imbalances, by rewarding thrift; or they may dampen them, due to a social policy choice [

14]. According to many studies, the gender pension gap is the result of three main factors: (a) women participate less in the labor market; (b) when they do, they work fewer hours/years; and (c) on average, their salaries are lower. Sadly, these factors are intertwined and, even though the gap has decreased in the last few years, this process has been slowed down by the economic crisis [

14,

15,

16]. Women’s pension levels are affected by the individual, family, and social spheres: number of children, parental leaves, career, and type of welfare State. Some key aspects are work (dis)continuity, family responsibilities, and the different stages in the family cycle, the accessibility of social roles beyond that of the worker, financial instability during retirement, and a longer retirement period due to women’s longevity compared with men’s [

2,

17,

18,

19].

In many countries, the increase of women’s participation in the labor market began in the late 1960s, while in the Mediterranean area data showed trends that are more discontinuous. In Italy and in Greece there was an alternation of growth and decline over time, while in Spain the increase in female activity rate was constant, although starting from a relatively low level, and it grew up slowly in the mid-1980s [

20,

21]. Concerning Italy, data highlight a decrease at the end of 1960s, followed by a subsequent growth. This period marks the beginning of the economic boom with the increased level of industrialization and the general improvement of living conditions, hitherto confined mainly to agriculture. The growing female participation in the labor market not only depends on the changing labor demand, but also on women’s active role in starting to seek out-of-home jobs. This trend increased also later in 1980s and 1990s.

The female activity rate largely depends on the number of children: especially passing the threshold of the first child, which lowers the rate by 10%–20%. These data confirm a close relationship between extra domestic work and family situations. Moreover, the subsequent reintegration, which should be realized in the age range 41–50, is not implemented at all.

In some G20 countries, the 25% target for a reduction in the gender gap of labor force participation by 2025 would only invoflve a modest further rise in participation rates for women (for example, in Canada and in France). In all, under the “25% by 25” scenario, there would be 126 million more women in G20 economies participating in the labor force—or a 5% increase in the total G20 labor force by 2025 compared with the baseline scenario. Some countries, including Germany, Japan, and Korea, would need to achieve close to gender parity in labor force participation to avoid the looming decline of their labor force. Reaching equality in working hours as well as in labor force participation can lead to additional increases, with significant rises projected in Australia, Germany, and the United Kingdom, where today more than 30% of employed women work part-time. A full convergence in the participation rate between men and women over 20 years could boost the GDP per capita growth rate, with increases of more than 0.5 percentage points expected in Japan and Korea, and about 1.0 percentage point in Italy [

22].

Pension levels in the EU are significantly gendered, although a gender pension gap is hardly ever simply a question of pension system design, since pension systems typically cumulate inequalities and filter them through to lead to pension outcomes. Women are in a disadvantageous position in the world of paid work (pay per hour, hours worked and years worked, number of interruptions). In Western countries, the greatest part of the pensions is financed through social insurance, and career inequalities generate inequalities in the total contributions paid. But pensions can do more than simply cumulate previous inequalities: the filter of the pension system is far from being neutral, considering that in many countries it depends on accumulated entitlements. Another crucial factor is whether the pension is calculated as a function of the final salary (retributive system) or on the basis of the accumulation of the contributions paid (contributive systems) [

23].

Despite efforts towards implementing equal opportunity measures, the factors determining pension levels are still subject to a gender discrimination that continues into old age [

16], particularly in the South of Europe (including Italy). Various pension reforms explicitly aim at improving women’s opportunities to build up pension entitlements. Some so-called “work-life balance policies” increase women’s labor market participation by particularly facilitating part-time employment, as well as pension entitlements for care periods outside the labor market. At the same time, other seemingly gender-neutral reforms tend to have the opposite effect. These measures include changes in pension calculation norms and pension composition, increasing the importance of non-public pensions, and this could have some negative effects on the situation of women [

24,

25].

Table 1 shows the substantial difference in pensions received by women and men and it reflects different life trajectories and pension systems. In all European countries, there is a difference between male and female retirement income, always in favor of men. Firstly, and most importantly, gender gaps in pensions in EU are very wide; secondly, these gaps are very different and one of the most important sources of differentiation between member states is the extent to which there remain gender gaps in coverage,

i.e., the extent to which women (more than men) do not have their own independent access to pension system benefits [

23].

Table 1.

Pension’s annual income mean values by gender in the EU (65–79 years old) (2012)

1.

Table 1.

Pension’s annual income mean values by gender in the EU (65–79 years old) (2012)1.

| | Mean Monthly Value of Pension Income (Euro) | Mean Annual Pension Income as (%) of 2011 GDP per Capita | Mean Annual Pension Income as (%) of 2011 National Poverty Line |

|---|

| | Men | Women | Men | Women | Men | Women |

| LU | 3970 | 2164 | 59 | 32 | 242 | 132 |

| DE | 1846 | 1022 | 69 | 38 | 188 | 104 |

| UK | 1696 | 979 | 72 | 42 | 178 | 103 |

| NL | 2383 | 1286 | 80 | 43 | 232 | 125 |

| FR | 1981 | 1236 | 77 | 48 | 192 | 120 |

| GR | 954 | 738 | 61 | 47 | 201 | 155 |

| IE | 1945 | 1147 | 67 | 40 | 197 | 116 |

| AT | 2540 | 1477 | 85 | 50 | 233 | 135 |

| ES | 1269 | 848 | 67 | 45 | 212 | 142 |

| PT | 908 | 595 | 68 | 44 | 218 | 143 |

| SE | 2283 | 1574 | 67 | 46 | 185 | 127 |

| IT | 1654 | 1064 | 78 | 49 | 202 | 133 |

| NO | 3224 | 2344 | 54 | 39 | 161 | 117 |

| BE | 1527 | 1116 | 56 | 41 | 153 | 112 |

| SI | 874 | 679 | 60 | 46 | 144 | 112 |

| FI | 1885 | 1392 | 65 | 48 | 166 | 123 |

| PL | 465 | 353 | 58 | 44 | 184 | 139 |

| DK | 2120 | 1982 | 59 | 55 | 160 | 149 |

| LT | 269 | 237 | 32 | 28 | 124 | 109 |

| HU | 368 | 312 | 45 | 38 | 155 | 131 |

| CZ | 500 | 429 | 41 | 35 | 128 | 110 |

| LV | 296 | 250 | 36 | 31 | 134 | 113 |

| SK | 422 | 384 | 40 | 36 | 122 | 111 |

| EE | 329 | 317 | 33 | 31 | 110 | 106 |

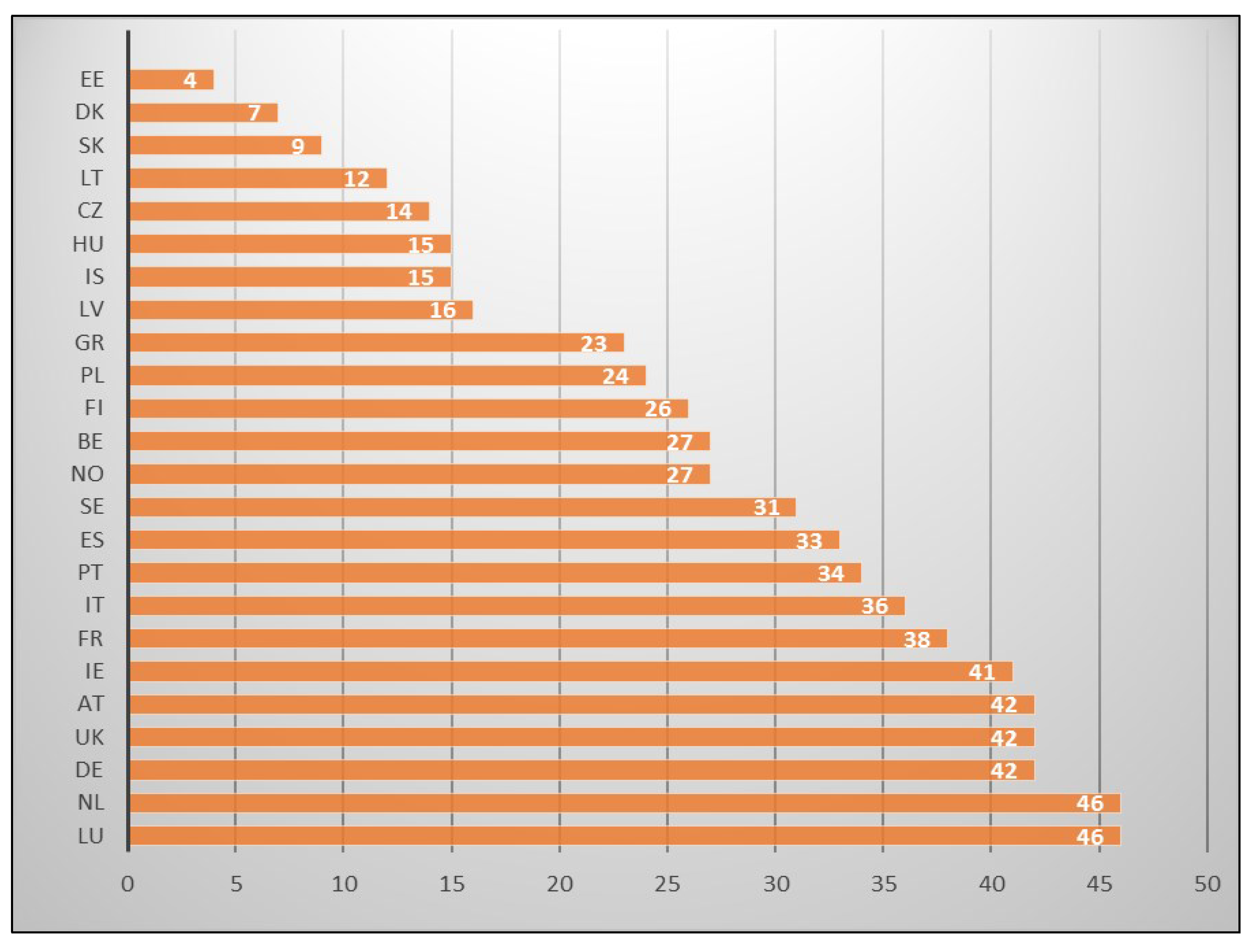

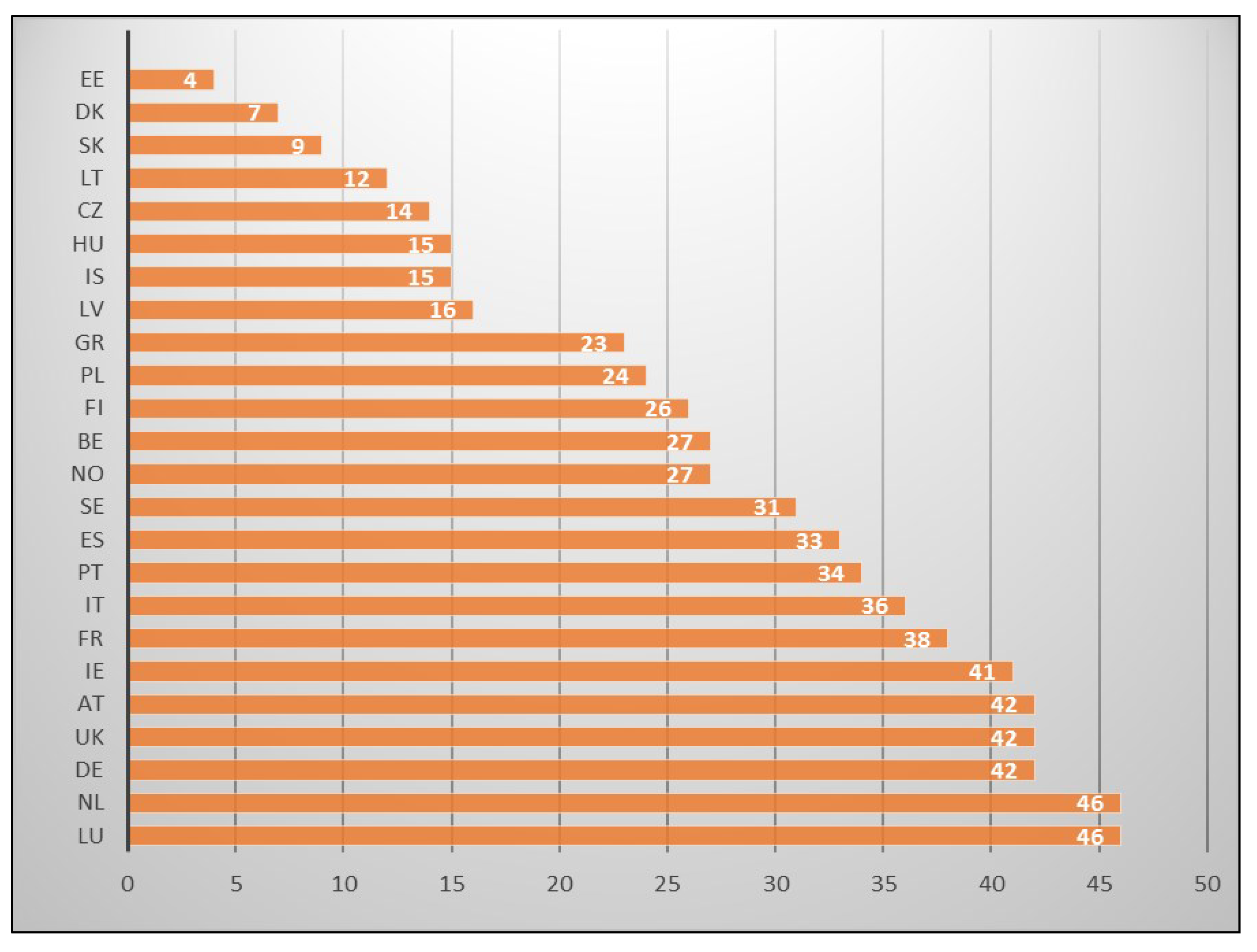

Studies on income from pension in Europe show the significant influence of gender differences [

26] (

Figure 1). The average gap among the EU-27 is 39%. On one extreme side Luxembourg and the Netherlands (46 percent) and Germany and UK (42 percent); on the other, Estonia (4 percent) and Denmark (7 percent). In Italy, the average is 36 percent, considering that many women have no income at all apart from widowhood, because they never worked. This difference in retirement income also results from the different employment rates between men and women, from a greater number of women working part-time and from getting lower wages than men. A large number of countries show a 30 percent gender pension gap, and as many as 17 out of 27 a > 30 percent gap. This evidence looks particularly interesting in relation to the 16 percent average salary gap,

i.e., half of the (30 percent) average pension gap [

14]. Moreover, in Italy, the most widespread pension scheme is based on income contribution, and that takes no account of periods of absence from work in order to manage house and family workloads, nor of the lower contribution of part-time jobs [

1,

8,

14].

Figure 1.

Pension’s gender gap by country. The percentages refer to the gap between men and women; Source: [

26].

Figure 1.

Pension’s gender gap by country. The percentages refer to the gap between men and women; Source: [

26].

3. Old Women’s Pension, Work-Family Issue, and Pensions Reforms

The reasons for analyzing the situation of women’s pensions separately from men’s depend on the different way women build up their transition to retirement and old age. A common assumption is that, beside the variety of European social and welfare policies, the pension gap is caused by a gender bias still considerably affecting women’s life paths [

27]. Much of the discussion surrounding women’s pensions has focused on their work histories. This focus reflects a male model of understanding pensions. The amount of the pension for men is largely determined by their work histories.

Many of the studies conducted so far have ascribed the above structural inequalities to the male breadwinner model (MBW), according to which women either do not work or work part-time, temporary employment [

12,

28]. Most EU countries, including Southern countries for sure, base their pension system on the MBW, whilst others, such as Sweden and the UK, have introduced individual pension schemes. Both systems negatively affect the women living outside the traditional family context (due to separation, divorce, or single status), and/or those not meeting all the eligibility criteria for individual pension schemes. Thus, women risk to end up with a much lower (or zero) income on reaching retirement age [

29]. Public policies provide pensions for married women and widows; likewise, work pension schemes also include widows’ pensions. Therefore, a kind of compensation has been set for unpaid domestic roles, particularly maternity, through marriage [

13]

2. If the family remains united, according to the MBW, there will be no problems until widowhood, a condition that is, however protected in most countries

3 [

31,

32,

33]. Otherwise, women will experience the collapse of their financial independence and risk poverty—often being able to count only on informal family networks.

The study of pension reforms in the different welfare regimes is useful in understanding the diversity of experiences between countries. In the majority of EU countries, the traditional system includes a survivor’s pension as part of the basic social insurance package. If the surviving spouse has no pension of her own, she would inherit her husband’s pension, usually reduced. In the case where the woman is independently entitled to her own social insurance pension, there is a variety of practices implying differences in gender gap emergence (being able to draw both pensions, having to choose one or being able to draw part of the survivor’s pension if there is another entitlement) [

23].

It helps to determine whether certain welfare states are really being dismantled and whether the Liberal group’s approach has become dominant in recent decades. In studying the characteristics of pension policies and their changes, we discuss both the management of social risks in aging societies and the policy profile of pension reforms. Different welfare regime types represent different responsibilities assumed by the market, the state, and the family in the management of social risks and social security. The Liberal welfare regime is distinguished by the dominant role of the market in the management of social risks with lower responsibility on the part of the state and the family. In the welfare states of the Social Democratic regime, the state plays a larger role than the market and the family in meeting the social needs of citizens. While all of the these actors play a moderate role in the management of social risks in the Continental European group, the family remains the key actor in the Southern European group [

34].

The significant impact of the maternity experience on the women’s situation at pensionable age varies in the different European countries [

35], affecting women’s careers as well as their general life course. The experience of maternity can significantly influence the financial security of women during their retirement age, the latter varying according to different contexts and welfare systems. The literature contains many studies on the so-called “orderly careers” [

36,

37,

38] but these models fit men’s roles better than women’s, especially where older generations are concerned. Many studies show that, for married men, parenthood typically has a positive impact on their careers or delays retirement [

12,

39]. The interpretation is that, when faced with greater financial responsibilities due to the presence of under-age children, a man will increase his work efforts. The situation of women who become mothers, especially in Southern Europe, is much more complex but it helps to understand the long-term risk of vulnerability.

Data on these trends show that, when welfare systems generously provide benefits for working mothers during maternity by offering parental leaves and/or

ad hoc care (as happens in Scandinavian countries), their pension treatment and life quality in their late years are more similar to men’s—and not just in financial terms [

40]. Conversely, limited access to maternity and parental leaves in Southern Europe force working mothers to either prematurely re-integrate into the labor market or leave it for good [

41,

42].

The example of parental leaves is a good illustration of the female condition in comparative terms. Parental leaves are a “family right” to be shared between partners in Austria, Denmark, Finland, and Luxembourg, whilst they are individual rights in Belgium, France, Germany, Greece, Italy, Ireland, Portugal, Spain, Netherlands, and the UK. In Iceland, Norway, and Sweden they are a “mixed” (part family, part individual) right. These countries have a specific form of leave for fathers: if unused, the leave cannot be made available to the mother. On the other hand, parental leaves tend to be taken by mothers in most countries, whilst fathers only use them if they are well remunerated, as families have more financial problems when fathers are off work. Prolonged leaves, as applied for after the maternity period or a parental leave, can last two or three more years but their retribution is lower. They are a prerogative for women and constitute a sort of “reconciliation for women”; however, they could also re-enforce gender differences between paid and unpaid work and become a trap for mothers, as they make it harder for women to resume work to its former level. In order to counter these negative effects, in some countries, such as Sweden, the women who use prolonged leaves are regarded as no different from other female employees.

Caring for old relatives is a responsibility typically undertaken by women who, as they approach the end of their careers, are forced to interrupt work again—

i.e., after having done so in order to raise their children. This is often a point of no return. The number of the vulnerable elderly is increasing and, unlike in Northern Europe, in Italy families are the main suppliers of assistance. Despite a relative increase in the forms of institutional care, their delivery is fragmented and allocated to a number of public and private actors. Not always are these able to adequately replace informal welfare [

43].

Here too, empirical evidence shows various trends according to the context, with less favourable situations for Southern European women [

44,

45]. In Spain and Italy, where many over-50s have never worked outside their homes, or have done so irregularly, middle-aged women who have lost their partners suffer greater exposure to financial risk, if compared to their counterparts elsewhere in Europe, even though many can benefit from co-residence with their adult children, thus finding protection, however limited, from poverty [

46]. The proportion of old people living with their children is about 30 percent in Spain and in Italy, and about 18 percent in France, while in Denmark it is negligible. Financial support, however, is often from the parents towards their children [

47]. Besides, as mentioned, in Southern-European welfare systems the family (namely, the daughters) take on the responsibility of looking after the elderly [

48].

As shown in

Table 2, in different countries, pension contributions vary according to career and salary.

Table 2.

Structure of entitlement programs, 2011. Percentage of total entitlement programs in Europe.

Table 2.

Structure of entitlement programs, 2011. Percentage of total entitlement programs in Europe.

| 2011 | Pensions | Health | Working Age | Children/Other |

|---|

| Austria | 43.0 | 24.5 | 20.5 | 12.1 |

| Belgium | 31.8 | 25.7 | 27.5 | 15.1 |

| Czech Republic | 32.7 | 29.2 | 23.1 | 15.1 |

| Denmark | 19.6 | 22.3 | 26.8 | 31.3 |

| Estonia | 31.7 | 22.1 | 30.4 | 15.8 |

| Finland | 31.6 | 22.0 | 25.1 | 21.3 |

| France | 42.5 | 25.0 | 16.6 | 15.9 |

| Germany | 39.4 | 30.6 | 15.6 | 14.4 |

| Greece | 51.1 | 25.8 | 10.0 | 13.1 |

| Hungary | 40.8 | 22.8 | 23.6 | 12.8 |

| Ireland | 16.8 | 27.0 | 36.8 | 19.3 |

| Italy | 51.9 | 24.7 | 11.5 | 11.8 |

| Luxembourg | 27.8 | 27.7 | 28.1 | 16.4 |

| Netherlands | 21.3 | 27.5 | 27.3 | 23.9 |

| Norway | 22.6 | 25.4 | 26.4 | 25.6 |

| Poland | 45.2 | 22.0 | 17.2 | 15.5 |

| Portugal | 44.8 | 26.9 | 18.7 | 9.7 |

| Slovak Republic | 31.9 | 30.7 | 23.7 | 13.7 |

| Slovenia | 41.5 | 24.3 | 19.2 | 15.0 |

| Spain | 33,0 | 23.8 | 25.5 | 17.8 |

| Sweden | 26.4 | 24.4 | 20.8 | 28.5 |

| Switzerland | 33.2 | 28.2 | 24.7 | 13.9 |

| United Kingdom | 23.0 | 29.3 | 23.2 | 24.6 |

In response to the demographic challenges and fiscal constraints, many European welfare states have moved toward the privatization and marketization of pensions in order to improve their financial sustainability. The privatization of retirement income responsibility has led to a shift from dominantly public pensions to a multi-pillar architecture with growing private pillars composed of personal, firm-based, or collectively negotiated pension arrangements. At the same time, marketization has led to the introduction and expansion of prefunded pension savings based on financial investments, as well as stronger reliance of market-logic principles in the remaining public pay-as-you-go (PAYG) pensions. However, there are also important cross-national variations in the speed, scope, and structural outcome of the privatization and marketization of European pension systems. Liberal market economies, but also some coordinated market economies (the Netherlands, Switzerland, and the Nordic countries) have embraced multi-pillar strategies earlier and more widely, while the Bismarckian pension systems and the post-socialist transition countries of Eastern Europe have been belated converts. The recent financial market and economic crisis, however, indicates that the double transformation may entail short-term problems and long-term uncertainties about the social and political sustainability of these privatized and marketed multi-pillar strategies [

50].

These different vantage points according to generation are triggering debates between workers, who are contributing to the pension system, and retirees, who are benefiting from past contributions to the system. It is argued by Aysan and Beaujot [

34] that this conflict can lead to a change in the perception of aging from being a public/life-course issue to being a private/life-stage problem. Even though aging becomes a private problem for an individual with a private pension plan, it also becomes a social and political problem when dealing, for example, with the need for pension reform. That is, the approaches to pensions and social security are linked with the demographic dynamics of particular countries. All countries face aging populations, but countries in the Social Democratic regime cluster have shown greater ability to influence the level of childbearing, along with an interest in maximizing labor force participation of men and women to pay for generous social benefits. The Liberal regime is based on greater privatization. With their differential treatment of different groups in society, the Continental and the Southern European regimes have the most difficulty in achieving reforms, and they face the highest rates of population aging, too. While the market plays a significant role in the retirement and pension systems in the Liberal group, the state remains the key actor in the Social Democratic group. In other European countries, however, the family (especially in Southern Europe) still plays decisive roles in caring for the elderly. In spite of these differences, there are important uniformities across regimes, which include attempts to delay retirement, to convert pensions to defined-contribution plans, and to have a higher dependence on private plans, all in the interest of seeking to achieve sustainability. In conclusion, different welfare regimes have developed their own approaches to public pension reform.

Today, women tend to work more than in the past (often in part-time jobs) even though they are over-represented in less well-paid jobs compared with men [

15]. The older generations of women tend to have spent less time in paid employment and to have earned less than their younger counterparts. They formed a family when they were younger, tending to have more children and to interrupt work for long periods, or tending to leave work altogether on the arrival of their first-born. The frequent interruptions and very low pensionable age have contributed to further shortening women’s careers, thus jeopardizing their income, as wives would depend on their husbands’ pensions alone. In the future, women will have to build their pension income through substantial contributions whilst still in the labor market; or, given the growing number of divorces

4, they will have to rely on (family) protection networks [

51]. The current differences in career profile between men and women are likely to produce future gender disparities in retirement income as well as in intentions and possibilities [

52]. Many recent pension reforms try to correct gender pension inequality. If earning imbalance will also be limited, the pension gender gap will gradually decrease on its own. Here, the crucial factor is reciprocity,

i.e., a closer link to entitlement and contributions. The problem is that reciprocity could take inequalities existing in employment and reproduce them in pensions (maybe amplifying them). Citizens’ pensions, given as a right to individuals of both genders who reach a certain age, can foster a significant gender gap reduction in older ages, considering that older women may have few years of contributions, and therefore a very small pension, or they might not reach the minimum [

23].

Consequently, in order to understand the men-women income disparity in old age, it is necessary to consider both welfare and family-policy factors in the different countries. If gender-specific policies on equal pay and non-discrimination are important, to consider the impact of other policies on families’ income and poverty levels as just as crucial in terms of their consequences for the elderly

5. Reconciliation policies and their needs should reach further, since, for example, economic policies on work conditions and employment do affect retirement expectations. Women’s disadvantage comes, on the one hand, from lower pay, work leaves, and part-time employment; on the other, from their longer life expectation compared to men’s. As stressed by Frericks and Maier [

11], future female pensioners will thus be further disadvantaged by the persistence of gender disparities in salary levels, as this affects their options to invest in supplementary pension schemes.

It is therefore crucial to understand how pension reforms account for the changed conditions affecting different generations of women, particularly in order to reduce the poverty risk and ensure women’s financial independence in their old age, as well as to increase pension-related benefits.

Pension reforms have also attempted to boost women’s opportunities to increase their pension contributions independently. These measures generally include changes in the ways contributions and combined pension schemes are calculated, thus stressing the importance of (or the need for) private pensions. EU member States are gradually adapting their pension systems to the evolution of men’s and women’s economic roles by eliminating discriminatory policies and by increasing family-work reconciliation ones. These reforms, different from country to country, have often supported family-work reconciliation policies in order to foster women’s employment by promoting part-time work and additional pension contributions for care periods spent outside the labor market. At the same time, the effects of some gender-neutral reforms tend to run contrary to the desired ones. However, the effects of gender discrimination will still be felt by the older generations, whilst the new ones lack the appropriate instruments to assess the reforms and their future impact [

53,

54].

A growing risk of these circumstances is the financial and subsistence levels of elderly women. Many international studies have highlighted that the risk of poverty for the elderly is higher among women than among men, independently of the indicators or data used in the different countries [

55]. Among pensioners, most of the destitute are women: in OECD countries the poverty rate for men aged 65+ was 11 percent and 15 percent for women in the mid-2000s, a trend confirmed by the most recent data [

15,

56]. Elderly people living alone are much more at risk of becoming poor than those who live within a family [

57]; old women living alone are poorer than men; finally, the poverty hazard further increases after age 75 [

31,

58,

59]. Unlike men, many female pensioners see their income drastically reduced, whilst their financial cover is often inadequate. A single-person household presents a higher risk of poverty than a two-person household, because there is no possibility for the economies ofscale [

60]. Whilst single mothers generally used to be widows, today they tend to be divorcees. Among these, the 50+ risk becoming one-person families, unable to benefit from the economies of scale enjoyed by couples. Unfortunately, retirement systems have often been based on the assumption of a two-person household.

Besides, the length of the retirement period affects gender differences in relation to the poverty risk. Women live longer than men and, by the time they reach 65, they have a life-expectancy that is four times higher, which means they will receive pension payments for a longer period. However, they are also more likely to be widowed and live alone, receiving a small survivor’s pension; in later years, they will have to face an increasing number of problems and financial needs. In documenting this difference, research shows a positive correlation between the strongly interconnected factors of poverty risk and marital status, life conditions, and number of children. As for marital status, the risk of poverty is definitely lower among married women, according to most studies, and higher among the divorced, the separated and the women who have never married, while it is slightly lower among the widows [

32,

61]. As for financial independence, it derives, for the elderly, from the income received after leaving work at a pensionable age or, for those who have never worked, from other subsidies. Retirement income protection is the cumulative result of different life paths. For men, the main one is career, although there are also factors such as a second marriage in their 50s, ensuring family stability and support. For women, instead, the route towards financial (in)security during retirement depends on the intertwined paths of maternity, work, and care [

62,

63].

Studies on financial independence for the working-age population [

56,

59] take into account the gender pay gap likewise, the pension gap between men and women being an indicator of how this inequality is reflected (and sometimes increases) in old age. This difference shows the cumulative disadvantages of a career path within a gender-biased labor market, and especially applies to the older generations. Pension and welfare schemes can thus widen or reduce inequality because of social policies.

4. Aging and Retirement in Italy: Family-Work Trade-Off and Women’s Pension

A relevant aspect of gender inequality, but a relatively unexplored one in Italian scientific literature, is related to old age and retirement. In fact, women are particularly affected because of their greater average age compared with men’s [

16,

64]; for the same reason, they are more exposed to the risk of widowhood, in itself a widespread financial problem, since reversible pensions cannot always guarantee financial security. Besides, women’s careers are usually made unstable by flexible work. Whether chosen or inevitable, this flexibility makes the access to retirement more difficult. Costs for maternity breaks are more likely to influence women’s future and present situation, especially in male breadwinner model countries. In addition, in all countries, pension reforms tend to turn from the retributive into the contributive system [

65].

Going deeper into the Italian case, the severity of the demographic crisis has deeply affected the welfare system in general, because of the perverse combination of lower birth rates and high life expectancy at retirement time.

The economic and occupational globalization has further stiffened the existing separation between standard (full time, permanent) and non-standard (temporary, part time, intermittent, contract-based) work relationships. Hence, the competition between

insiders (stable and guaranteed workers)and

outsiders (unemployed, or informal/ irregular workers). In Italy, less than 5 women out of 10 do paid work (outside their homes) in a labor market based on the

insider-outsider model. Such a situation marginalizes the younger generations, especially women. Two-thirds of the welfare budget are appointed to work and old age pension. Besides, 36 percent of the 55–64 population are still working and 19 percent of the young people between 15 and 24 years old are unemployed/ NEET [

66]

6. In this context, women’s careers tend to be less stable than men’s because of their(not always chosen) occupational flexibility. This flexibility, in fact, can be a bumpy road to the retirement phase. As anticipated, one crucial factor for this is maternity, as it can influence not only women’s careers but their overall life path.

The changes introduced in the pension system in Europe in the 1990s and 2000s have left the condition of workers approaching retirement practically unaltered. Most significantly affected are the cohorts of the so-called baby-boomers (born after 1960). The bleakest scenarios feature, again, women, the self-employed and, generally, atypical workers. Women and men alike increasingly risk unemployment once they have turned 50; their pensions face a rocky future, with amounts likely to drop well below those granted to their older counterparts.

The socio-economic history of Italy reveals similarities and differences in the last decades as regards welfare state, the gender gap, women’s employment, and retirement. The last few decades have seen Italy undergo a transformation from a mainly agricultural to a post-industrial model [

66]. The labor force, however, remains rather low-profile compared with other developed countries, and if women’s participation in the labor market has increased, it is still quite limited. Both countries missed the Lisbon Agenda objectives, such as women’s employment at 60% and even those for 2020 EU strategy (75 percent men and women employed). The actual unemployment rate is around 50 percent for women and 53 percent for men after the 2008 crisis. The reforms made by Amato in 1992 (law decree no. 503) and Dini in 1995 (law no. 335) aimed to set the relationship between social security spending and GDP and raise the default retirement age. Nevertheless, social security expenses in 2000, in Italy (25 percent of GDP), were lower than the EU average (27.1 percent). The last pension reform, launched in the worst years of economic crisis (2009), was the outcome of long-running debates but focused on the issue of increasing longevity rather than on gender equality, with the aim of substantially extending the retirement age for men and women. The saved funds (about 4 billion euro), instead of being used to promote female employment (as initially planned), have been redistributed. One of the side effects of the reform was to reduce availability of grandmothers for child care (especially in the South), rendering it even more difficult for young women to get back to work after maternity [

67].

In the autumn of 2011, the financial crisis, which in Europe had turned into a “sovereign debt” crisis for those countries with high public debt, reached a peak. At that time in Italy, in order to quickly recover financial stability, a major reform of the public pension system was introduced (law 214/2011). The key elements of the reform are: (i) the immediate abolition of the early retirement option, which allowed retirement up to five years before reaching the old age requirement; (ii) the application of the Notional Defined Contribution (NDC) benefit computation mechanism to all workers for seniority accrued since 2012; (iii) the strict link between the increase in life expectancy and age and seniority requirements; and (iv) the (further) homogenization of requisites between genders—the old-retirement age requirement for women will be harmonized to that for men by 2018—and between working schemes [

68].

Analyzing the effects of the pension reform of 2011 on individuals’ retirement age, adequacy and distribution of the benefits for various categories of Italian workers, the main findings are an increase in the average retirement age, generally raising over time, coupled with a sizeable increase in average replacement rates. However, the most affected group is represented by women employees born in 1955 and retiring in the period 2012–2021, who face an average increase in retirement age of four years, while benefiting from an increase in the average replacement rate of 13 percentage points [

69].

A gender-based analysis of the labor market for elderly workers reveals a comparatively discontinuous situation that significantly affects the pension gender gap in Italy. In the 1980s and 1990s public work-demand reduction policies, together with further aggravating factors affecting labor costs, favoured the early retirement option, mostly for women, reaching to age 50 (or even earlier). This was a benefit for employers too, as they could save on the costs of permanent workers and hire more “flexible”, lower-paid, staff [

70]. In addition, Italian women in their 50s (as well as their counterparts in the rest of Southern Europe) tend to lose their jobs and cannot always be eligible for a work pension [

71]. According to data from the Eurostat

Labor Force Survey [

72], 26 percent of Italian women declared themselves to be outside the labor market because of being pensioners (

vs. the 36 percent of the total European women). In Italy, only one “non-working” woman out of four says she is retired (

vs. the European men about 59 percent; Italian men the 68 who are pensioners). Latest data illustrate a wide gap between Italian men’s and women’s’ employment rates (40 percent of 50–64 years old women are employed vs 65 percent of men at the same age; among the 50+ women only 19 percent

vs. 36 percent of men) [

73]. For both the women and the men there is an increasing danger of losing their jobs on reaching 50 years of age, as a consequence of the fragmentation of job types. These workers risk not being entitled to a pension and, if and when they are, this will amount to considerably less than the older generation’s.

Through longitudinal data, Barbieri and Scherer [

66] represented Italian families (ILFI—

Indagine sulle Famiglie Italiane,

i.e., a survey on Italian families) from 1997 to 2005, by analyzing the working histories of individuals aged 50–70 (birth cohorts: 1930–1934; 1935–1939; 1940–1944; 1945–1949; 1950–1954). As for the female sample, their participation in the labor market is relatively limited, and they leave it rather early. The incidence of part-time work at 50 is gradually increasing from the older cohorts to the younger ones, especially among women. This type of career path has a definite gender connotation, with women being the majority. As for individual careers, the data show that women approaching the end of their employment tend to move towards domestic work. Again, the hazard of being unemployed at 50+ increases throughout the cohorts, with the youngest being most at risk, because of government cuts in social protection measures. Interestingly, couples are less exposed to losing their jobs in their mature years, which confirms the protective effect of the marital/cohabiting status. Women’s careers are more frequently interrupted, with spells of informal or atypical work, confirming a basic weakness due to the widespread occupational gender segregation in work environments less subject to social protection. The risks of inequality and social exclusion will be dramatically higher for the forthcoming older generations. For the elderly generation of women, however, the gender pension gap is already a sad reality. All this considered, for Italian women over 50 the “familist” or “Mediterranean” welfare model has actually boomeranged. These women are forced to take on responsibility for the care of the elderly in the family, which causes them to leave work prematurely and exposes them, to a higher degree than men, to the risks of poverty and exclusion. This prospect will probably worsen in the future, given the steady decrease in fertility rates, the lower availability of care-givers within the family, and the increasing numbers of elderly and very old people. Furthermore, the economic crisis and the flexibilization of the labor market are getting worse and worse for women in particular [

74].

Many of them, who had once left work in order to look after their young children, will face again the dilemma of working outside their homes or caring for old relatives. It is understood that, in most cases, they will have to opt for the latter

7. In the Italian case, over three-quarters of the vulnerable elderly remain the responsibility of their families as far as care is concerned, whilst children tend to leave their family of origin only in their late 20s [

75]. Besides, the load of domestic tasks and assistance, which lowers the demand for women’s work and slows down the offer of formal care services, makes the prospect of a large family look quite unattractive

8.

The changes introduced in the pension system in the 1990s and 2000s have left Italian workers approaching retirement virtually unaffected. Conversely, they would have a significant impact on the so-called “baby-boomers” (

i.e., those born after 1960). Even though the data available so far suggest no definite conclusions, some trends have emerged about the consequences of future pension provisions. The least favourable scenarios concern, again, women, the self-employed, and those whose career patterns have been irregular, thus involving lower contributions. Unfortunately, this circumstance in the early old age is able to affect not only men’s and women’s economic and health situation, but even their whole QoL (quality of life) in later life [

77]. Italian women have disadvantages even when they get a pension. Men generally obtain higher pensions benefits using 56 percent of the whole amount destined for the pension system. The widest gender gap is in the 60–64 years old group, in which the mean amount for women is 60 percent of that of men [

78].

The above arguments point to the presence of a vicious circle and its possible causes. There are, of course, structural factors causing low fertility, limited female participation in the labor market, and social and financial risks potentially affecting elderly women. These trends, however, largely depend on the role of the State, even though trying to break the bonds of gender-sensitive cultural and normative expectations appears to be a problem too. In fact, The Italian system has been criticized for considering any changes in the family as a problem and for addressing such problem only by strengthening family values to which care and work reconciliation policies are considered instrumental [

79,

80]. Social policies, in turn, depend on more complex choices than the dualism between family benefits and the delivery of services, which introduces the issue of the complex relationship between formal and informal care provisions [

43].

These forewarning signs highlight the symbolic and financial price women will have to pay, especially on reaching retirement age, for having been mothers too.

5. Conclusions

The pension gender gap is a crucial issue concerning welfare systems, the financial independence and the increasing risk of poverty for elderly women in Europe and in the Mediterranean countries. Women’s condition in Italy is burdened by prospective pension reforms that are already in the European agenda. These reforms consider adult life as an individual situation and not as a process in which job career is linked with family life and care tasks. Maternity, together with the other above described family and job factors, makes women’s working lives less stable and necessarily more flexible if compared with men’s. In the absence of specific social and pension policies, this (not always chosen) flexibility makes women’s access to retirement less straightforward.

In Italy, the impact of maternity on pension rights is much stronger for women who have reached retirement age, and this is aggravated by the effect of the time spent on child and family care, and of women’s more discontinuous presence in the labor market. Even the new generations of working women, with autonomous pension rights, often need a reversible pension in the case of widowhood, because of their lower pay and shorter working life, as well as higher protection against a possible separation/divorce, with the consequent hazard of slipping beyond the poverty threshold in their late years.

Currently, the male breadwinner model protects older widows better than a more mainstream emphasis on an individual approach. This is because the lifetime earnings of women are significantly less than the lifetime earnings of men, and these earnings are not expected to converge anytime soon. Inequality in this situation can be the result of treating women as individuals without consideration of their unpaid family work. For pensions, treating women as individuals and ignoring their work life choice will have the same result: greater gender gaps in pension income outcomes. Similar inequalities will remain as long as there is no recognition of the high risk of older women living alone. Living alone requires higher expenses per person, especially for housing and utilities. Furthermore, older women living alone risk secondary poverty due to the fact that they are less able to manage their affairs on their own due to a higher risk of disability than men of the same age.

In conclusion, the situation described so far points to the possible causes of a vicious circle. The increase in female participation in the labor market has taken place within a traditional family model. The double-income family is a recent trend, with women with flexible work and lower pay levels than men. Unstable jobs, the responsibility of care tasks and medium-low education levels are predictors of a financially and socially vulnerable old age for women. In the recent years of the economic crisis, women in Italy and in Mediterranean Europe have short careers, delayed access to the labor market, and discontinuous pension contribution payments. The combination of gender with the male breadwinner model has thus created a disadvantage for women.

Any prospective solution to this problem should consider the possible interactions between family choices and obligations to prevent unwanted effects on old- and new-generation women who have struggled to reconcile family with work. Any equality strategies should encompass both gender and age factors, as well as the subjects’ different experience stages, considering gender policies in the different countries, and evaluating if and how diverse power structures can combine to produce positive (or negative) effects in each national context. Even though, of course, pension gender inequality is linked to work experience type and average life expectancy, the pension system could be redesigned in such a way as to avoid, or at least reduce, inequality.

{kind=link}