Abstract

The effects of the world economic and financial crisis, which began in 2007 and is still in progress, has made increasingly sharp the line of demarcation between those able to access home ownership on the free market, and those unable to do so. For the European Union’s member states, Social Housing (SH) policies include all the initiatives aimed at providing housing support for all the weak segments of the population; these policies have declined differently by different Member States according to their specific needs. In Italy, the growing need for SH accommodation together with the shortage of public resources makes developing forms of Public–Private Partnership (PPP) necessary. Evaluation techniques like Break-Even Analysis and Contribution Margin Analysis are useful in planning interventions including SH initiatives in the context of real estate development or retraining initiatives in PPP (in negotiation processes or in project financing). These kinds of techniques especially allow evaluation of public and private convenience in PPP. In the present work, an assessment procedure has been structured: first the main parameters of a settlement of SH initiative in PPP are defined; subsequently, it is possible to assess the feasibility and the financial balance of the initiative itself. The procedure has been applied to a case study: the interrupted initiative of self-renovation in Via Grotta Perfetta 315 in Rome (Italy).

1. Introduction and Aims of the Work

In various member states of the European Union, over the past 20 years (1996–2016), access to home ownership has become a problem, involving ever greater segments of the population [1].

In several European settings, the effects of the world economic and financial crisis, which began in 2007 and is still in progress, has led to fewer jobs and lower income for the population, while making it harder to access credit and consequently increasing the cost of living—out of proportion with increases in wages and salaries—as well as home prices. These factors have made the line of demarcation between those able to access home ownership on the free market, and those unable to do so, increasingly sharp [1].

The social classes historically considered weakest (low income, unemployed, homeless, ex-convicts, immigrants) have been joined by other segments of the population consisting of family nuclei that, while not presenting the necessary prerequisites for accessing affordable and social housing, are unable to satisfy their housing needs on the free market (young couples, singles, separated/divorced spouses, students, the elderly). The composition of social housing demand is thus rather complex and varied [1].

For the European Union’s member states, Social Housing (SH) policies include all the initiatives aimed at providing housing support for all the weak segments of the population listed above. Cecodhas (European Liaison Committee for Social Housing) has defined SH as the set of “housing solutions for family nuclei whose needs cannot be met under market conditions, and for whom there are assignment rules” [1]. SH initiatives must therefore be aimed at [1]:

- meeting housing needs in terms of accessing and living in affordable, decent homes;

- increasing the supply of dwellings for affordable rent, through the construction, management, purchase, and rental of social housing;

- defining criteria for assignment and for the identification of target groups, on the basis of socioeconomic criteria as well as with reference to other types of vulnerability.

These initiatives are also considered an opportunity for: seeking to remedy housing inequality; fighting social exclusion and supporting social mixing; improving social integration and coexistence among various types of users; pursuing productive efficiency in buildings either to be constructed from the ground up or to be renovated, while seeking to pursue the highest possible quality in terms of function and energy savings; providing a flexible housing supply capable of better responding to fluctuations in demand [2,3,4,5,6].

In the European Union’s member states, the ‘housing problem’ presents different needs and responses. Consequently, although sharing the aims of SH actions, heterogeneous policies have been adopted, and the initiatives undertaken to cope with the housing issues of the weak segments of the population have differed accordingly.

Among Member States of the European Union, the amount of resources engaged in the implementation of SH programs can vary between 0% and 3% of Gross Domestic Product (see Section 2.1) [7].

Public–Private Partnerships (PPPs) are widely distributed in the settlement context as well as the use of public resources. Through PPPs, it is possible to allocate private financial resources for SH [8,9].

SH initiatives are the test bed for bringing social, economic, and energy sustainability together, and for developing forms of PPP (negotiated type or project financing), as they are considered a potential driver for the economy and for the real estate market during these years of profound global economic crisis. The implementation and programming of new SH initiatives in PPPs, structured in accordance with the current European settlement models—differentiation/integration both socially (residential SH also for temporary housing needs, such as student housing, jointly with/adjacent to the housing to be introduced onto the free market) and in function (mix of residential and non-residential functions, both public and private)—might help countries with the greatest SH needs (including Italy) to meet a portion of the large demand for housing expressed by the weakest segments of the population. In fact, in cases where—in the development of the urban settlement structure—‘prized’, central, or semi-central areas of the city are often taken out of circulation and need to be reconverted to new functions, it may be appropriate for municipal administrations to also avoid new land consumption, to take action by getting private investments involved in requalification solutions that integrate intended residential uses of SH, and not with others intended for services and productive functions [1].

To guarantee the implementability of SH initiatives also structured in this way, it is useful to rely on assessment models that allow technically, financially, and procedurally sustainable intervention possibilities to be planned right from the programming phase [10,11]. Especially in Italy, the purpose of this is to overcome the difficulties encountered in implementing the programs initiated in the past.

In an international setting, to assess real estate initiatives, a number of different techniques are used, making it possible to express judgments of benefit even among a number of alternative solutions. This is done by means of the following:

- “costing” (full costing, direct costing, advanced direct costing): breaking down costs by type (direct and indirect) and variability (fixed and variable) [12,13,14,15,16];

- Discount Cash Flow Analysis (DCFA) to examine results and financial risks [17,18,19,20,21];

- integration of economic and productive data; Cost Volume Profit Analysis (CVPA) [22,23,24,25,26,27] which includes: (i) Break-Even Analysis (BEA), allowing the break-even conditions in a productive process to be estimated [28,29,30,31,32,33,34,35,36]; (ii) Contribution Margin Analysis (CMA) [37,38,39,40], which, in a productive process, allows the financial sums remaining after the fixed costs for variable and extra-profit-related costs are dealt with to be estimated; (iii) Operating Leverage Analysis (OLA), which allows the riskiness of a productive process to be assessed [41,42,43].

However, at a European level, there are no specific assessment procedures suitable for supporting the competent public bodies (hereafter, SPU) and the private bodies/investors (hereafter, SPR) in promoting real estate initiatives aimed at building SH in PPP. Each Member State in the PPP assessment recognizes the European general guidelines in its own rules [44]; referring to the Italian case, the only national law reference that can be found is the article 16.4 (d)-ter of D.P.R. 380/2001 (and subsequent changes) related to the convenience allocation between SPU and SPR [45].

Some recent works have proposed applying CVPA (BEA, CMA, OLA) to assess an initiative’s key financial data with respect to its physical characteristics and size [27,28,46,47]; in particular, they have proposed using BEA to determine, in a real estate initiative aimed at building SH, the amount of area that can be built and sold at prices lower than market prices, in order for the initiative to reach ordinary market profitability given the market’s economic and size parameters. BEA thus makes an essential contribution for calibrating the real estate initiative with regard to the weight of the SH component in terms of settlement, and to the corresponding selling prices [27].

Even if CVPA does not take in account the time of the economic process (this is the only limits of this assessment technique), BEA, CMA, OLA, are however useful techniques for assessing the reciprocal conveniences of the Public and Private Entities in PPPs or in Project Financing, where SH is planned to be implemented in real estate development or retraining [27].

This work was inspired by the need expressed by Rome’s municipal administration to have an assessment tool able to find specific application for certain SH initiatives already begun and yet to be concluded (referring in particular to self-construction) due to supervening criticalities making it necessary to re-program the modes of intervention, while also verifying the possibility of relying on PPP interventions. The work consequently proposes an assessment model suitable for supporting a Public body (SPU) in carrying out, in PPP, “integrated” SH initiatives through the reconversion of abandoned sites/buildings, but is constructed in such a way as to be used in the case of initiatives involving green-field sites.

The proposed model, starting from the SH need that the SPU aims to meet (where applicable, a need ‘inherited’ from the uncompleted initiative) and from the identification of the specific size parameters admitted by the regulatory and legislative framework in force for the property (area/building) on which to develop the intervention:

- through the BEA, allows the financial feasibility to be assessed, for the SPR, of an intervention in PPP in which the building of SH is contemplated;

- through the CMA, allows the presence to be assessed, where applicable, of extra profits [48] of the initiative which, in this case, may be used to increase the supply of housing or of public services (balancing the initiative in terms of dividing the benefits between the SPU and the SPR).

Hereinafter, in Section 2 we present a brief overview of needs and implementation models adopted in Italy for the production of social housing with a specific focus on PPP; Section 3, shows the proposed model to evaluate initiatives including the SH in PPP; in Section 4, the model is applied to the intervention of self-renovation of Via di Grotta Perfetta 315 in Rome; Section 5, are drawn to the conclusions of this work.

2. Social Housing: Needs and Implementation Overview

2.1. Social Housing Needs in Europe

The EU does not have any specific responsibilities with respect to housing; national governments develop their own housing policies facing similar challenges: for example, how to renew housing stocks, how to plan and combat urban sprawl, how to promote sustainable development, how to help young and disadvantaged groups to get into the housing market, or how to promote energy efficiency among homeowners. Questions of social housing, homelessness, or integration play an important role within the EU’s social policy agenda aimed to “combat social exclusion and poverty,” as “the Union recognises and respects the right to social and housing assistance so as to ensure a decent existence for all those who lack sufficient resources, in accordance with Community law and national laws and practices” [49]. The European platform against poverty and social exclusion (COM(2010) 758 final) sets out a series of actions to help reduce the number of people at risk of poverty or social exclusion by at least 20 million persons by 2020 (compared with 2008) and extended what was started in the European Council meeting in Nice in 2000, where an agreement was reached on a set of common objectives for the EU’s strategy against poverty and social exclusion, including two objectives related to housing, namely “to implement policies which aim to provide access for all to decent and sanitary housing, as well as basic services necessary to live normally having regard to local circumstances (electricity, water, heating, etc.),” and “to put in place policies which seek to prevent life crises, which can lead to situations of social exclusion, such as indebtedness, exclusion from school and becoming homeless” [50].

Indicators through which SH needs are identified relate to housing overcrowding, housing quality, and cost sustainability in relation to income [50].

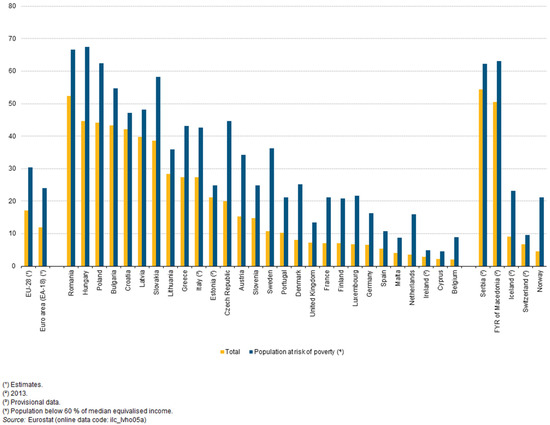

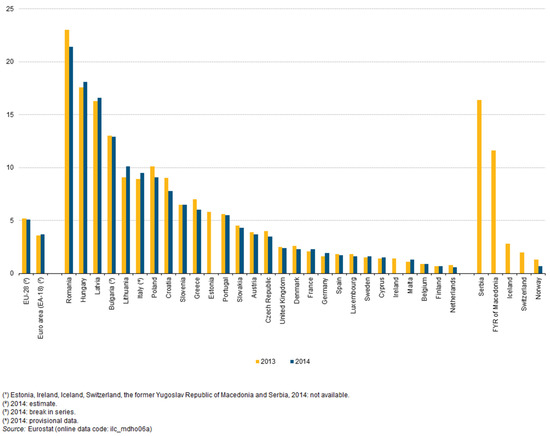

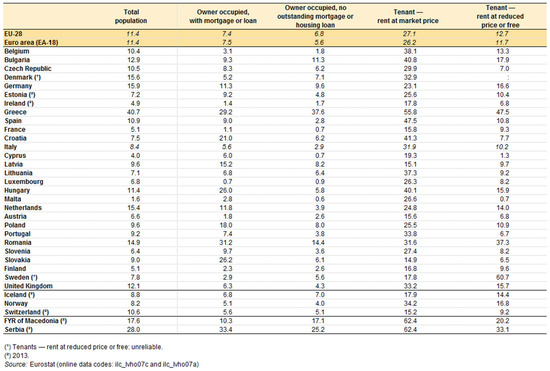

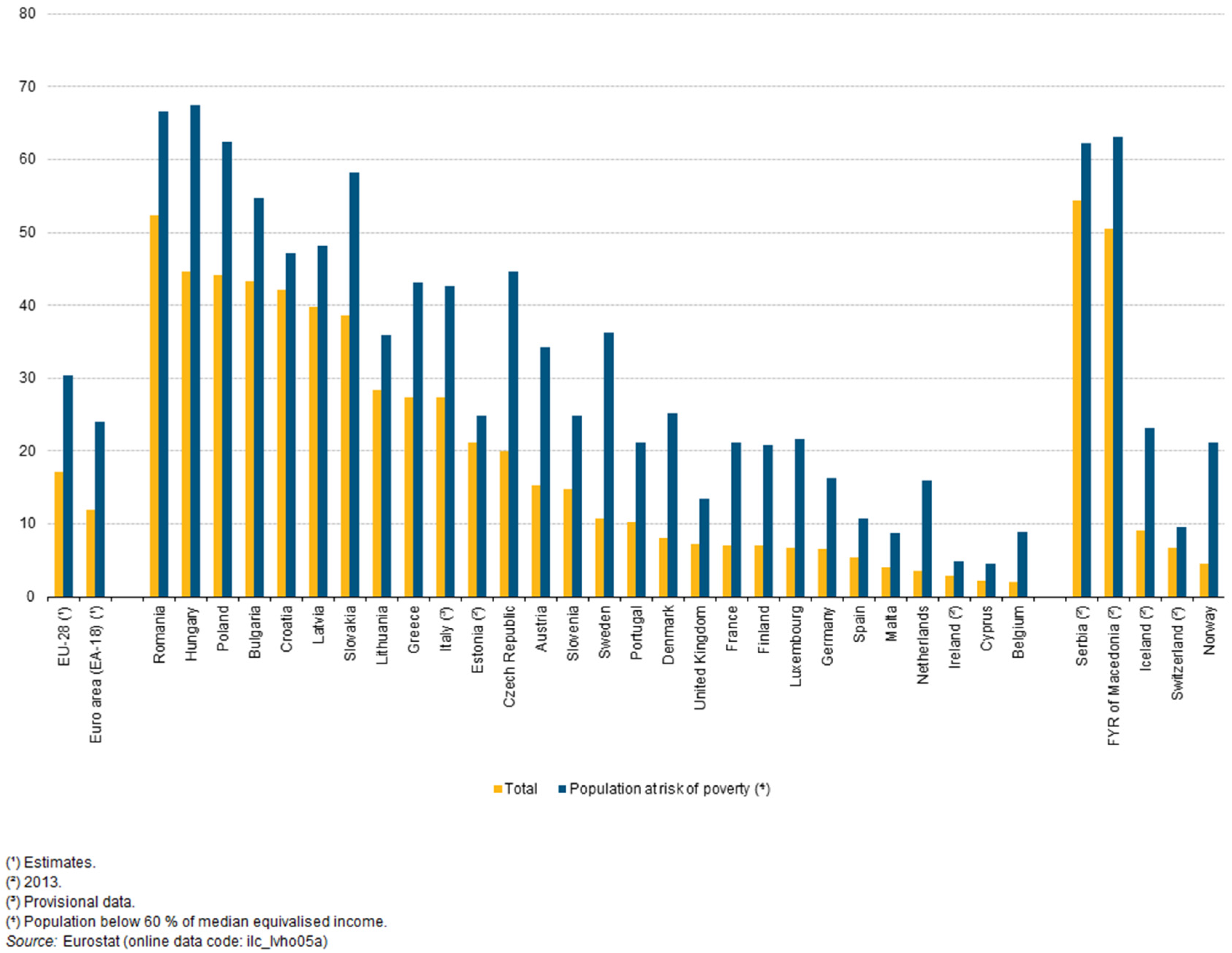

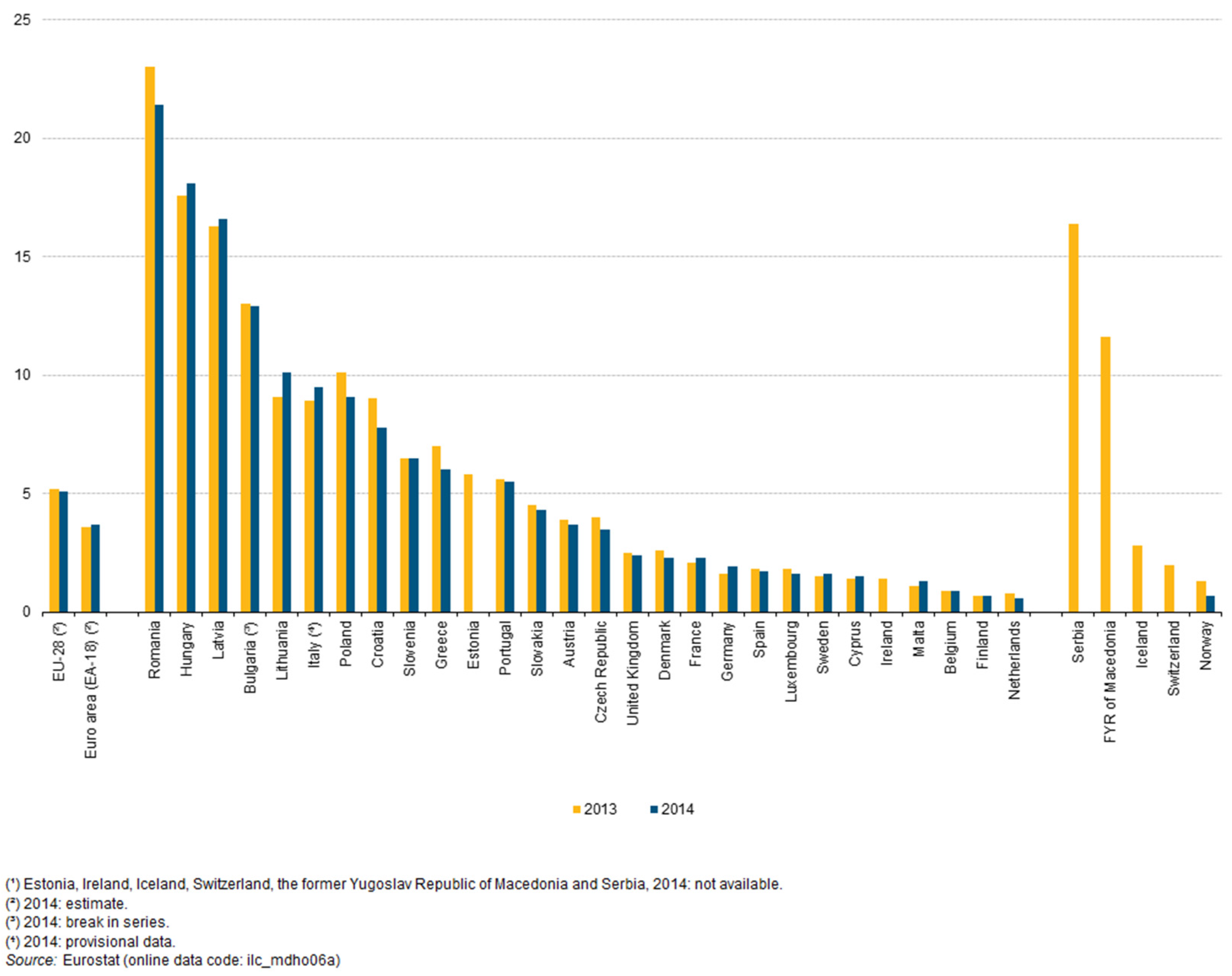

With reference to the 28 European Union Member States (EU 28), in 2014, 17.1% of the population lived in overcrowded conditions (Figure 1). About one-third (5.1%) of this population was living in severe housing discomfort (Figure 2) (at least one of the following conditions: lack of bath, presence of roof infiltration, overly dark accommodation) while the 11.4% of the population supported a housing cost over the 40% of their income (Figure 3), the latter considered as a limit threshold even for lower incomes [50].

Figure 1.

Overcrowding rate, 2014, % of specified population. Source: Eurostat [50] © European Union, 1995–2013.

Figure 2.

Severe housing deprivation, 2013 and 2014, % of population. Source: Eurostat [50] © European Union, 1995–2013.

Figure 3.

Housing cost overburden rate by tenure status, 2014, % of population. Source: Eurostat [50] © European Union, 1995–2013.

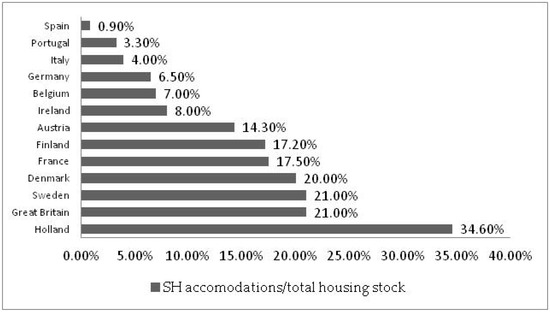

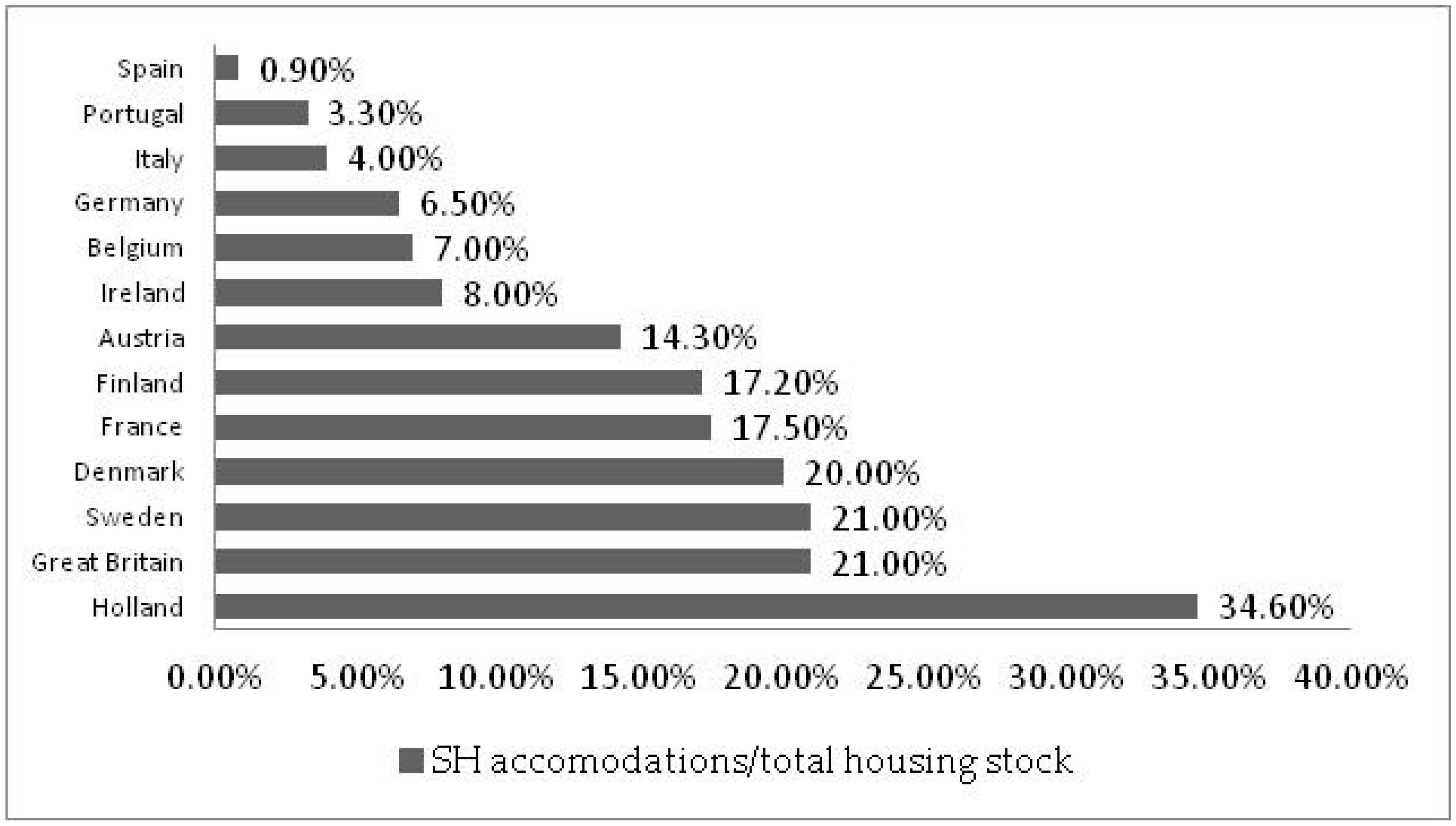

By comparing the public housing stock present in 13 main European countries with regard to their respective SH needs, a significant gap between the SH stock and the population who need social accommodation is present in some countries (Spain, Portugal, Italy, Germany, Belgium, Ireland); other countries (Austria, Finland, France, Denmark, Sweden, Great Britain, Holland) have sufficient SH stock in relation to their needs (Figure 4).

Figure 4.

Stock of public housing wealth in the biggest European countries. Source: author’s elaboration on Censis data [51].

In general, SH-related expenditures account for about the 1% of the European Union’s Gross Domestic Product, although differences are noteworthy from country to country (Scenari Immobiliari, 2010): around 3% in the Netherlands, Sweden, UK; Ranging from 1% to 2% in Austria, Denmark, France, Germany; 1% in Ireland, Italy, Belgium, Finland, and Luxembourg; Less than 1% in Portugal and Spain [7]. There is a direct correspondence with data in Figure 4: states with more social housing than their own stock are the ones with the highest SH-related expenditure relative to Gross Domestic Products.

Italy is one of countries where the ‘housing problem’ has mushroomed since the mid-1990s. Overcrowding affects 27% of the population while severe housing discomfort affects 10% of the population. Furthermore in particular, the Italian real estate market has seen the gap between housing costs (incidence per month) and household income grow wider; in this setting, Italy has also seen a significant increase in families in a state of housing emergency, resulting particularly from court-ordered evictions due to rent arrears. In fact in Italy, between 2010 and 2016, housing selling prices fell considerably from the previous decade (2000–2009) when they recorded continuous gains; the number of transactions dropped considerably (averaging about 50% nationally); the average selling price diminished by 40%, and rent by 30%. Despite this, the incidence (in large cities) of the housing cost (about €8000–9000/year) on the income of households belonging to the weak segments of the population (about €22,000/year gross income) continues to be unsustainable, also given the higher unemployment and lower job security. In brief, there is a persisting need for housing—both for sale and for rent—that is ‘lower-cost’ than the prices demanded on the market, even though these have fallen considerably in recent years.

According to Eurostat (2017), in Italy, 8.4% of population—about 2,000,000 families—spends more than 40% of their disposable income on housing. Among the about 2,000,000 families, the actual (2017) unmet housing need is difficult to calculate because municipalities do not update the lists for public housing assignments annually. The only datum of reference (2013) shows approximately 650,000 applications sent in by family nuclei (2017) listed on the municipal rankings for public housing assignments [52]. The 650,000 applications were submitted by those who are in overcrowded condition, in serious housing discomfort, or by those who support unsustainable housing costs in relation to their income; in general, family nuclei/parties may be assigned public housing when they meet particular requirements: no owned real estate, total household income under approximately €22,000/year (gross), dependent children and/or elderly [53].

The need of the family nuclei awaiting public housing assignments comes on top of the unquantifiable need expressed by those parties that, although needing rent- or price-controlled housing, have yet to file an application [54,55].

Considering that there are 28,800,000 lodgings in Italy, it is estimated that there are 1,150,000 SH lodgings, at 4% of the total stock (Figure 4).

Social housing is therefore required in Italy to reach a total of 1,800,000 units (+60% compared to the existing one). More than two decades of scant public resources devoted to SH policies have made it impossible (2017) to initiate processes to build homes in a number sufficient to meet a continually increasing, stratified need [52]. Nowadays (2017) in Italy, the financial resources for new buildings are in the form of grants for both subsidised housing (‘edilizia convenzionata’) and supported housing (‘edilizia sovvenzionata’) but also for the maintenance of the already obsolete and inadequate existing assets of current housing standards. The latter are lower than the European average of about 1.5% of GDP [7]. Considering the entity of the financial resources for the subsidised and supported housing, on an average of about 500 million a year, it is possible to project a rather long time (about 30–40 years) to meet the current housing demand of the weakest sections of the population (see Section 2).

This situation is even more critical when considered in the persistence of the worldwide and national economic crisis (2017) that has significantly impacted the Italian residential real estate market and the economic conditions of families.

The public authorities (municipal administrations; residential construction firms) are attempting to provide an operative response towards increasing the demand for social housing, in both quality and quantity, with the scant financial resources available to them.

2.2. Social Housing Implementation Programs and Public–Private Partnership in Italy

In Italy, given this housing need, from 2009 to date (2017), SH programs have been initiated to build approximately 14,000 homes—meeting only 3% of the ‘low-cost’ housing demand—planned generally on green-field sites [52].

Therefore, Italy has a persisting significant prior need. Shedding about 4% of its sales revenue every year since 2004 [56], Italy’s housing industry is in crisis. Considering this, the start of multifunctional urban transformation initiatives, in PPP, that contemplate building SH, might be an opportunity both to satisfy prior need and to revitalize the construction industry. The following elements are significant in this context: planning initiatives that are effective in containing public finances and, at the same time, the contribution that assessment may provide for this purpose.

For the most part, the initiatives promoted on Italian territory are aimed at building new housing (subsidized construction, whether publicly subsidized or under an agreement with the municipality) in urban environments, generally in the periphery due to the lower land value of the areas specifically designated for this settlement function; there are also cases of recovery of existing housing stock, as well as sporadic initiatives of self-construction and self-renovation. For a number of decades (from the 1960s to the 1990s), a considerable portion of the housing need was met with significant and constant allocations of public resources earmarked for new residential construction, publicly subsidized or under an agreement with the municipality.

Starting in 1998, any new financing assigned for subsidized construction interventions was virtually halted; the scant remaining funds were transferred to the Regions (and consequently to the residential construction firms) and employed to build new housing only in sporadic cases of limited scope; more often, they were folded into budget items earmarked for the maintenance of a real estate stock now for the most part obsolete, which requires considerable and ongoing ordinary and extraordinary maintenance efforts.

Allocations continued in support of initiatives subsidized under an agreement with the municipality—still today (2017) the most widespread mode of social housing production. For the beneficiaries of these interventions promoted by municipalities, cooperatives, and even residential construction firms, the home is to be purchased at agreed-upon prices or, as in the “20,000 alloggi in affitto” (“20,000 homes for rent”) program, the home is leased at an agreed-upon rent which, after a certain number of years, may allow the residential unit to be redeemed under a rent-to-buy arrangement.

In the late 1990s, self-construction and self-renovation began to be considered, in public SH programs and policies, as one of the tools available to public administration to combat housing distress and to foster social integration, with settlement production costs deemed lower (although there is a long-held conviction that with self-construction/self-recovery, it may be possible to achieve a 40–60% reduction in the production cost, it has been shown [57] that this statement may be considered only partially true) than those that may ordinarily be estimated for a building with characteristics included in the sphere of public residential building—whether facilitated, under an agreement with the municipality, or otherwise. In fact, given that housing distress is becoming considerable, in Italy self-construction and self-renovation still represents an opportunity (in many cases, not one that has concluded positively) limited to ‘weak’ family nuclei with low income capacity, but in a condition and with the desire to associate (in a cooperative) and, in general, to work in their free time with other family nuclei to construct a residential building, commensurately with the needs and number of associated families; they take on and share, voluntarily and through association, the risks connected with this productive operation, in which they are assisted and coordinated by coordination/mediation bodies and by public administration [55].

Although the programs initiated/carried out, both nationally and locally, are heterogeneous in nature, they share common problems in implementing these actions. Connected with procedural and operational difficulties, these problems, in a significant number of initiatives, have led to [52]:

- non-completion/interruption of work;

- excessively long construction processes (often exceeding 10 years)—well beyond the scheduled deadlines even for many of the works that have been finished,

- significant difference between estimated and actual costs (cost overruns);

- interruptions in work progress due to problems derived from designs not developed in suitable detail.

Some municipal administrations, to cope with the SH need and the housing emergencies resulting from evictions, occupations, or unforeseeable natural phenomena, have resorted to renting private housing stock on the open market. However, these solutions, although intended as short-term stopgaps for the housing emergency, became protracted over time, seriously straining budgets and already-scant public resources allocated to resolving the social housing shortage in a more structural fashion.

These problems have in fact resulted in a failure to satisfy the very housing need for which these initiatives had been undertaken, thereby producing serious social and economic effects connected with the non-use of areas and buildings intended for SH despite the costs incurred.

In order to try to reduce the gap between the supply and demand of social buildings to be made available under more accessible conditions than the markets, also with reference to national-level programs (and financing), various initiatives—financed directly with public funding or at times through forms of direct or indirect PPP—could be undertaken to build housing (owned or rented) for ‘weak segments’ of the population.

In order to compensate the dearth of resources of the bodies tasked with initiating SH initiatives, recourse to PPP has been trialled in recent years, also by conferring publicly owned properties—non-earning and/or to be capitalized on, and often sited in central or semi-central urban areas—to (socially responsible) real estate funds constituted ad hoc.

In PPP, operative models may be identified for building SH without relying on new public financing while at the same time creating opportunities for economic development and social integration [58]. This is done by implementing interventions that are multifunctional (mix of public and private services, SH units, and the free market) and that have a contained environmental and energy impact.

To set up a PPP aimed at making public housing, services, and infrastructure integrated with private housing, services, and infrastructure, in which a Public Body (SPU) is guarantor and a Private Body (SPR) makes the initiative a reality with its own capital, it is necessary to:

- identify an asset (area/building), publicly or privately owned, on which to carry out the intervention, and the SH need to be met;

- determine, with regard to the regulatory/legislative framework in force, the content of the initiative (construction potential, intended uses, urbanization);

- have the asset in the initiative at full disposal; the identified property must be or become able to be used by the SPU and then be conferred to the SPR in accordance with the modes provided for by law (transfer in ownership, concession for a determined period of years) through forms of public procedure;

- carry out the settlement transformation intervention; through the contribution of own capital, the SPR builds both public real estate complexes (SH and any buildings for public services) and private ones (private residences and services), in addition to carrying out the urbanization works needed to guarantee the intervention’s full efficiency;

- deliver, at the end of the intervention, the real estate complexes for public/social use to the SPU; the SPU will assign (lease, rent to buy) the SH units, and start operating these and any other non-residential real estate units built by the SPR;

- introduce, in the free market, real estate complexes to private functions; these properties are sold (or rented) by the SPR to recoup the invested capital.

For the PPP to work, the following conditions must be met: (i) a market capable of absorbing what is built and freely sellable; (ii) financially sustainable management of real estate complexes with respect to the income of SH recipients.

The initiative is assessed for a balanced division between the SPU and the SPR of (financial) commitments and benefits: the financial commitment that the SPR takes on to build public complexes, guaranteeing sustainable expenses during the phase of operating SH buildings, is offset by assigning the potential to construct private residential/non-residential buildings (to be sold on the free market) in line with the regulatory and legislative framework in force. Profitability, then, must be adequate for the risks and particular features of the initiative undertaken [59,60].

3. A Model to Assess Interventions in Social Housing Public–Private Partnership

3.1. Articulation

The proposed assessment model is structured so it can be applied to verify the conditions of a balanced division of benefits between the SPU and the SPR in an integrated initiative of urban transformation in PPP aimed at building SH. It may be applied (in advance) both to promote a new initiative and to assess the possibility of achieving the set objectives in an intervention already begun with other modes of operation but ‘interrupted’. In the second case, it will also allow the envisioned results of the initiative already undertaken to be compared with those foreseen in the PPP scenario.

It is organized in the following phases:

- Acquisition of the objectives that the municipal administration intends to pursue with the initiative; quantification of the need for SH and for services; location of the initiative: these elements are the input data for the assessment;

- Definition of the initiative’s settlement parameters; calculation, through logical/mathematical functions, of: construction potential (phase 2.a); urban planning standards (phase 2.b); appurtenant car parks (phase 2.c); type of settlement with regard to maximum height and coverage ratio (phase 2.d): these parameters translate regulatory references into settlement quantities. They make it possible to define the scope of the initiative (in both quality and quantity) and are also indispensable for implementing—while reducing the riskiness and margins of approximation—the financial feasibility assessment phase, as it is interconnected with and dependent upon the dimensions of these same settlement parameters [61];

- Verification of the financial feasibility; calculation of the breakeven construction potential BEA (phase 3.a), and its comparison with the initiative’s construction potential (phase 3.b). To assess the financial feasibility, the choice was made to use BEA, by virtue of the possibility of considering productive/settlement and financial parameters at the same time; having estimated the fixed and variable costs of a settlement transformation intervention, as well as the assets’ unit sale values achievable with that intervention, BEA makes it possible to determine the breakeven construction potential necessary for the intervention to be financially sustainable, which is to say for it to be able to compensate the SPR with ordinary market profitability [27]; the initiative’s financial feasibility will derive from comparison between the intervention’s construction potential and the breakeven construction potential;

- Verification of the initiative’s balance; estimate of any extra profits through CMA (phase 4.a), and, where needed, proposal for balancing the initiative (phase 4.b). The choice was made to use CMA to verify the initiative’s balance conditions. In particular, CMA, from which the possibility of estimating the extra profits generated with the initiative—if financially feasible—derives, allows the financial quantity generated to repay the fixed costs to be estimated; then, by subtracting the fixed costs from this amount, the extra profit that the operation generates can be estimated. With respect to the results of BEA and CMA, scenarios may be constructed to be submitted to the municipal administration, which is tasked with the decisions on the intervention. These may provide for a balanced division of any extra profits between the SPU and the SPR.

3.2. Development of the Assessment Procedure

3.2.1. Acquisition of the Objectives the Municipality Intends to Pursue with the Initiative (Phase 1)

As already discussed, the assessment procedure was structured, first of all, with respect to the need to be applied in order to assess certain SH initiatives already begun and left uncompleted due to supervening criticalities, for which the modes of intervention must be reprogramed (assessing reliance on PPP), but also in the case of starting new initiatives. The intervention to be assessed is generally started by a municipal administration in order to achieve objectives connected with: (i) meeting part of the SH need, expressed and quantifiable as the number and size of housing units to be built; (ii) any provision of public infrastructure and services needed in the urban setting that is the object of intervention. The municipal administration identifies the asset (area and/or building) on which the intervention is performed (regarding the initiative that is incomplete or yet to be started), and quantifies the SH requirement to be met with the intervention, as well as any shortage of buildings/infrastructure that the initiative intends to remedy. In assessing a reprogramming of a ‘critical’ intervention, if needed, additional assets on which to carry out the initiative may be identified, thereby extending the perimeter of the new intervention in PPP or modifying its location with respect to the original configuration of the uncompleted initiative.

3.2.2. Definition of the Initiative Settlement Parameters (Phase 2)

The admissible construction potential q, expressed in cubic meters/square meters (m3/m2) or square meters/square meters (m2/m2), is identified by examining the planning instruments in force on the area/building that is the object of the initiative.

It is necessary to take into consideration any limitations derived from instruments/norms to protect the landscape, and environmental limitations, as well as the regulations having effect on the intervention asset (regulations that provide incentives, such as “Piano Casa” for example; or that create exceptions, such as urban planning variances and/or program agreements). The admissible construction potential is provided by the sum of the partial construction potentials referring to the admissible intended uses/functions (residential, tertiary, commercial, tourism/hospitality, etc.), qf, on the intervention asset

where

- qf1 = construction potential intended use 1;

- qf2 = construction potential intended use 2;

- qfn = construction potential intended use n.

Considering that, generally, residential and non-residential intended uses/functions may be discerned, it is deduced that

where

- qr = residential construction potential;

- qnr = non-residential construction potential.

Having defined qr, it is possible to estimate the construction potential that can be sold on the free market, qa, by subtracting from the construction potential q the construction potential qSH to be allocated to SH, which the SPR must transfer to the SPU, as well as the spaces (areas/volumes), SD, that cannot be sold because they are intended for the distribution of the building/common spaces.

The sellable construction potential qa may have an intended use that is residential, qar, or non-residential, qan, also as a function of the regulatory prescriptions considered on the intervention area.

The (admissible) construction potential q constitutes the settlement parameter from which all the other settlement parameters considered below may be calculated.

The urban planning standards, SU, expressed in m2, qualify the initiative (phase 2.b), endowing it with the minimum public spaces needed for the secondary urban functions (greenery, car parks, services). The calculation of the Sus (usable areas) is needed to comprehend their actual availability within intervention area Ai.

The Sus cannot be settled if ; if the standards cannot be settled in the intervention area; the monetization potential should be assessed, in this case by inserting this amount among the intervention’s fixed costs in the BEA. Should it be impossible to establish or monetize the standards, or to deviate from this regulatory constraint, the intervention does not possess the prerequisites for being implemented.

where

- qur = unit residential construction potential per settled inhabitant (inhab) pursuant to the regulations in force;

- Spc = per capita urban planning standard per settled inhabitant pursuant to the regulations in force;

- cnr = coefficient of reference for urban planning standards referring to non-residential construction potentials as per the regulations in force;

- Sus = suppressed urban planning standards to be recovered (where applicable).

In the Italian case, to define these parameters, consideration is again made of the indications in Ministerial Decree no. 1444/68

- qur = 25 m2 or 80 m3 per inhabitant (m2/inhab or m3/inhab)

- Spc = 18 m2 per inhabitant (m2/inhab)

- cnr = 80% of gross usable area

The areas, at ground level or roofed, to be used for private appurtenant car parks PP (phase 2.c), expressed in m2, are to be calculated based on the ratio between the admissible construction potential q, and the construction potential of reference as per the regulations in force qpp.

In Italy, as of 2017, the regulation of reference for estimating the areas to be allocated to PP, is Law no. 122/1989, article 2, paragraph 2 (some regions have legislated by updating, for certain types of intervention, the reference parameter defined by Law no. 122/1989.), which indicates a parameter of no less than one square foot for every 10 cubic metres of construction.

For the PPs, the possibility of settlement in the remaining area of intervention Ar must be verified, by calculating what remains of the intervention area (Ai) after having settled the usable areas

Should it occur that , it is possible to settle the PPs in the external intervention areas. If , the PPs may be planned in underground levels intended for car parking. In this case, the BEA must list the cost for building the PPs among the intervention’s fixed costs.

The building types that can be settled in the intervention derive from the minimum height of the building(s) that may be settled (Hmin) (phase 2.d), identified with respect to the maximum covered area (indicated in the technical regulations and in the municipal construction regulations). Hmin must also be verified with respect to the maximum height parameters Hmax admitted by the general/implementative instrument in force.

In Italy, buildings may be settled with the following typologies

- cottages and/or duplexes and/or row houses, if ;

- apartment blocks if .

With regard to the building type that may be settled, the variable costs and the unit prices of the initiative, as necessary for implementing the BEA, must be appropriately estimated.

3.2.3. Verification of the Financial Feasibility of the Initiative (Phase 3)

BEA (phase 3.a) makes it possible to estimate the construction potential (expressed in m2/m3 or m2/m3 (depending on whether Cf, Cv, Pu are parametrized for square or cubic metre)), called ‘break-even’, q*, which is to say the minimum needed to repay the fixed and variable costs, thereby guaranteeing an ordinary profitability in market terms for the SPR (function of risks and of specific features of the initiative), in accordance with the formula

The fixed costs Cf, to be estimated in relation to the settlement parameters defined in phase 2, regard: any market value of the building/area of intervention, if owned by the SPR including notary and registration expenses (Cf1); demolition of pre-existing buildings (Cf2); performance of works for the area’s urbanization and for rendering it suitable (Cf3); monetization of the unavailable SUs (Cf3); building of non-sellable underground appurtenant car parks (Cf4); construction (technical cost) of public buildings (SH and other uses where applicable) to be transferred to the SPu (Cf5); financial charges related to the fixed costs (Cf6); technical expenses related to the fixed costs (Cf7). The fixed costs include, but as a deduction, the amounts paid by the SPu to the SPR that need not be repaid, such as non-repayable public funding (Cf8) and/or grants by the housing’s assignees (Cf9). The fixed costs may be estimated in a summary-direct fashion by obtaining comparables (direct sources), or through the aid of typological price listings (indirect sources).

The unit selling prices (Pu) regard the proceeds derived from the sale of ‘private’ buildings that may be earned with the intervention. For a quick and—at any rate—effective implementation of the model, they are estimated in summary-direct fashion taking account of the data provided by data banks that reveal selling prices.

The variable unit costs correspond to the production cost of the ‘private’ buildings that can be constructed with the intervention: construction (technical cost) of sellable buildings (Cv1), technical expenses related to variable costs (Cv2), concession charges (Cv3), financial charges related to variable costs (Cv4), ordinary promoter’s profit (Cv5), unforeseen costs (Cv6). The variable costs are also estimated in summary-direct fashion by obtaining comparables (direct sources) or through the aid of typological price listings (indirect sources).

The intervention’s financial feasibility is verified by comparing q with q* (phase 3.b).

The SH intervention in PPP will be financially as follows

feasible if qa ≥ q*

If the SH intervention in PPP is feasible, the conditions exist for an SPR to be able to implement the intervention by transferring to the SPU the stock of SH units, and selling the private stock on the market.

not feasible if qa < q*

The feasibility condition, q > q*, yields the presence of a differential construction potential (q − q*) which corresponds to an extra profit (Ep) (in addition to the ordinary market profit) that must be estimated.

3.2.4. Checking the Balance of the Initiative (Phase 4)

To estimate the extra profit, using CMA, it is first necessary to calculate the total contribution margin (Mct)

where

- Pu = unit prices of the initiative’s sellable buildings;

- Cvu = variable unit costs of constructing the initiative’s buildings;

- q = construction potential of the initiative.

In this way, by subtracting from the Mct the initiative’s Cf, the extra profit may be quantified (phase 4.b).

The extra profits may be broken down, depending on their size, between the SPU and the SPR. In Italy, the scenario that anticipates this breakdown must be formulated with respect to the minimum prerequisite attesting to the condition of the intervention’s public interest through the division of the extra profit, in the amount of no less than 50%, between the SPU and the SPR. The portion destined for the SPU may be used to build additional SH units or for public works.

4. Application of the Model

4.1. Intervention Case: SH in PPP as an Alternative to a Self-Renovation Initiative

The proposed model was applied to a SH case study regarding one of the self-renovation initiatives brought forward in the Municipality of Rome through the residential reconversion of abandoned public school buildings: Via Grotta Perfetta 315 (Municipio XI).

This initiative has yet to be completed (as of 2017), approximately 20 years after the start (1997) of these interventions, and 14 years after the work site was opened (2003). The examination of the causes leading to suspending the works at an initial state of progress [55], and to the impossibility of completing them despite the considerable sums spent by the public administration in an attempt to complete them, demonstrates the grave inefficiency of the planned process and the economic and social damage produced for the housing assignees and for society at large.

Trialling on this case study was initiated to assess whether it was possible to achieve the objectives initially set, without employing additional public resources and in quick and certain amounts of time, by a PPP to be implemented on the same intervention asset through the demolition of a school building and the construction of a new residential building with units intended for SH and for the free market.

4.2. Acquisition of the Objectives the AC Intends to Pursue with the Initiative

The intervention involves a lot of approximately 7,500 m2 which has: a school building with three storeys above the ground, 9.60 m in height on the eave line, covering approximately 1,600 m2 of Gross Useful Area corresponding to approximately 5,100 cm; open-air sports facilities; and a yard with a number of tall trees.

The self-renovation intervention provides for:

- the municipal administration to adjust the original school building structure, with the construction of 18 three-room units plus a social space, charged against municipal and regional allocations;

- the assignee cooperative, consisting of the future beneficiaries, to carry out all the finishing construction works both of the common parts and outside the building, by means of a loan guaranteed by the municipal administration.

Given the clear impossibility of proceeding with the school structure adjustment intervention, the municipality’s Single Programming Document of the three-year period 2016–2018 provided €500,000 for the building’s demolition. No possible alternative intervention for transforming the asset has been taken into consideration to date (2017).

The trial therefore aims to outline the possible intervention case for the complex’s transformation, calling for meeting the SH need, equal to 18 three-room units, through a PPP intervention in line with the current regulatory framework in force (phase 1).

According to the General Urban Plan, the area is classified as “Public greenery and public services at the local level”; this classification would permit no other intended use than that referring to public equipment and services; however, upon the approval of the transformation intervention by a Municipal Council Decision, a variation in the intended use of the building and of the appurtenant area may be hypothesized, also by assigning a bonus for additional construction potential.

This possibility is also contemplated by the new proposed Lazio Regional Law approved by the Regional Council in January 2017, and in the approval phase with the Regional Council, in “Regulations for urban regeneration and for building rehabilitation”.

The law states that, in order to regenerate abandoned buildings, construction potential increases of up to 40%, and changes in intended use to entirely residential uses, may be provided for, also as an exception to the provisions of the urban planning instruments in force.

4.3. Definition of the Initiative Settlement Parameters

The construction potential, q, and its breakdown into residential, qr, and non-residential, qnr (phase 2.a), are equal to (application of the Formulas (1) and (2)):

To estimate the sellable gross usable area qa (Formula (3)), it is supposed that: (i) qSH has been calculated taking into consideration each of the 18 SH units is 60 m2 of gross usable area; (ii) the distributive spaces qD account for 10% of the total designed gross usable area:

The gross usable area equal to 936 m2 makes it possible to settle 15 units (of approximately 60 m2) to be sold on the free market.

For the calculation of the areas for the legal urban planning standards (phase 2.b) in accordance with the model’s provisions (Formula (4)), the total construction potential q was considered, broken down into qr (100%) and qnr (0%):

Considering that, according to the Municipal Construction Regulation (hereinafter REC), the lot’s maximum covered area must be no greater than 20% of the lot’s land area, an open area of intervention Ai equal to 80% of the land lot, and therefore 6,000 m2, results.

Since the areas to be destined for SU are less than Ai (1,613 m2 < 6,000 m2), these may be settled in the free areas of the intervention lot, and therefore no (fixed) cost for the monetization of the standards must be considered.

For the estimate of the area to be destined for PP (phase 2.c) the ratio between the intervention volume and admissible construction potential q was considered (Formula (5))

The remaining free areas, Ar, still available for settling the PPs after having identified the urban planning standard areas, equal (Formula (6))

The area to be destined for PP is thus less than Ar (717 m2 < 4,387 m2). Consequently, the PPs may be built at ground level.

The height of the building(s) that may be settled (H) was calculated (phase 2.c) considering that in the REC, the lot’s maximum covered area must be less than 20%. This height, H, was also verified with respect to the maximum zone height, which may be obtained from the technical regulations of the General Urban Plan and the REC, equalling 16 m.

In the case under study, even though extensive building types could be provided for, the hypothesis is to repurpose a building with characteristics similar to those of the prior pre-existing building (three storeys above the ground with height equal to 9.60 m at the eave line, in addition to a storey, where needed, for technical installations).

4.4. Verification of the Financial Feasibility of the Initiative

To implement the BEA, the fixed costs, the variable costs, and the unit selling prices (proceeds) of the intervention case in PPP (Table 1) were estimated, with regard to the settlement parameters calculated in phase 2.

Table 1.

BEA for intervention in Via Grotta Perfetta 315

The parametric costs needed to estimate the fixed costs and the variable costs were obtained from the appropriately updated Price Lists for Construction Types [62]. In the fixed costs, no consideration was made of the sums originally established to be borne by the assignee cooperative and by the municipal administration (net of those already spent); consideration, however, was made, in the financial items of the initiative hypothesized in PPP, of the €500,000 provided for in the 2016–2018 single planning document (DUP).

The unit selling prices (proceeds) were estimated taking into account the quotations surveyed by Real Estate Market Observatory (Osservatorio del Mercato Immobiliare) at the Revenue Agency (Agenzia delle Entrate) for the intervention area (first half 2016, the latest available).

The breakeven construction potential q* (phase 3.a), for the intervention to be financially sustainable, equals (Formula (8)):

The sellable construction potential qa, estimated earlier, equal to 936 m2, is therefore greater than the breakeven construction potential q*.

Since qa > q* (Formula (9)), the possibility was therefore verified as undertaking, on the considered asset, an intervention of SH in PPP (phase 3.b).

4.5. Verification of the Balance of the Initiative

Since the breakeven construction potential q* is less (albeit not by much) than the construction potential qa, the extra profit (Ep) beyond ordinary market profit was calculated by proceeding to determine (phase 4.a):

- first, the total margin of contribution (Formulas (11) and (12))

- then, the extra profit

The extra profit equal to €165,803 is slight; since, in accordance with the provisions of the regulations in force, it should be destined for the SPU in an amount of no less than 50%, it may be reasonably supposed that it may be fully allocated for unforeseen costs or for miscellaneous improvements during the work site completion phase.

In brief, the intervention case in PPP on the asset at Via di Grotta Perfetta, is financially feasible, and might permit, in 18–24 months, the construction of the 18 SH units with 15 of the housing units to be sold on the free market, with no additional costs for the assignees or the municipal administration.

The SPR might undertake a productive activity with a sales revenue that may be supposed as equalling about €3,200,000 (fixed costs + variable costs), which may be connected with benefits in terms of employment (temporary work site jobs) and during the operating phase (meeting the housing need).

5. Conclusions

The proposed model allows the financial feasibility of a SH initiative in PPP to be assessed, considering the intervention possibilities that arise from the regulations in force and from the requirements in force in the intervention area. Its trial on the asset at Via Grotta Perfetta 315 allowed a scenario for the construction of SH in a PPP to be defined, as an alternative to the original self-renovation intervention that could not be carried out.

It has been shown that, through the use of the proposed procedure, starting from a structured manner of establishing the settlement parameters that physically define the intervention itself by outlining a meta-design hypothetical case, the feasibility and financial margins may be assessed through established financial analysis techniques like BEA and CMA.

The assessments done and the presence of a SPR lowers the risk that the initiative will not be done by the deadlines and in the manner as provided for.

From this perspective, the model may be considered in support of the activity of the SPU and the SPR which, though they have different roles, intend to operate on the territory by initiating balanced, sustainable interventions for the weakest segments of the population with specific reference to accessing and managing home ownership.

Author Contributions

The paper must be attributed in equal parts to the authors.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Cecodhas. Housing Europe Review 2012: The Nuts and the Bolts of European Housing System. 2011. Available online: http://www.housingeurope.eu/resource-105/the-housing-europe-review-2012 (accessed on 9 May 2017).

- Benon, K.; Mbabazize, M.; Shukla, J. Effect of private sector involvement in public private partnership performance in housing construction projects in city of Kigali. Eur. J. Bus. Soc. Sci. 2016, 5, 237–250. [Google Scholar]

- Davidson, N.M. Affordable Housing and Public-Private Partnerships; Routledge: London, UK, 2016. [Google Scholar]

- Mital, K.M.; Mital, V. Public Private Partnership and Social Infrastructure; Computer Society of India: Mumbai, India, 2016; Available online: http://www.csi-sigegov.org/1/13_353.pdf (accessed on 9 May 2017).

- Roberts, P.; Sykes, H.; Granger, R. Urban Regeneration; Sage: New York, NY, USA, 2016. [Google Scholar]

- Löhr, D. Sustainable housing: A ground lease partnership model. Land Use Policy 2017, 60, 281–286. [Google Scholar] [CrossRef]

- Scenari Immobiliari. Social Housing in Europa e Focus Sull’Italia. 2010. Available online: http://www.scenari-immobiliari.it/ITPublic/download_free_list.aspx?IdArt=563 (accessed on 9 May 2017).

- Clifton, C.; Duffield, C. Improved PFI/PPP service outcomes through the integration of alliance principles. Int. J. Proj. Manag. 2006, 24, 573–586. [Google Scholar] [CrossRef]

- Sagalyn, L.B. Public/private development: Lessons from history, research, and practice. J. Am. Plan. Assoc. 2007, 73, 7–22. [Google Scholar] [CrossRef]

- Napoli, G.; Giuffrida, S.; Trovato, M.R. Fair planning and affordability housing in urban policy. The case of syracuse (Italy). In Proceedings of the International Conference on Computational Science and Its Applications, Beijing, China, 4–7 July 2016. [Google Scholar]

- Guarini, M.R.; Battisti, F. Benchmarking multi-criteria evaluation methodology’s application for the definition of benchmarks in a negotiation-type public-private partnership. A case of study: The integrated action programmes of the Lazio Region. Int. J. Bus. Intell. Data Min. 2014, 9, 271–317. [Google Scholar] [CrossRef]

- Bubbio, A. L’activity Based Costing per la Gestione dei Costi di Struttura e Delle Spese Generali; Libero Istituto Universitario Carlo Cattaneo: Castellanza, Italy, 1993. [Google Scholar]

- Bartoli, F. Tecniche e Strumenti per L’analisi Economico-Finanziaria. Piani, Programmi, Modelli e Indicatori Economico-Finanziari alla Luce di Basilea 2; Franco Angeli: Milan, Italy, 2006. [Google Scholar]

- Drury, C.M. Management and Cost Accounting; Springer: Berlin, Germany, 2013. [Google Scholar]

- Kaplan, R.S.; Shank, J.K.; Horngren, C.T.; Boer, G.; Ferrara, W.L.; Robinson, M.A. Contribution margin analysis: No longer relevant/strategic cost management: The new paradigm. J. Manag. Account. Res. 1990, 2, 1–32. [Google Scholar]

- Garvey, P.R.; Book, S.A.; Covert, R.P. Probability Methods for Cost Uncertainty Analysis: A Systems Engineering Perspective; CRC Press: Boca Raton, FL, USA, 2016. [Google Scholar]

- Shrieves, R.E.; Wachowicz, J.M., Jr. Free cash flow (FCF), economic value added (EVA™), and net present value (NPV): A reconciliation of variations of discounted-cash-flow (DCF) valuation. Eng. Econ. 2001, 46, 33–52. [Google Scholar] [CrossRef]

- Ozdemir, U.; Ozbay, I.; Ozbay, B.; Veli, S. Application of economical models for dye removal from aqueous solutions: Cash flow, cost-benefit, and alternative selection methods. Clean Technol. Environ. Policy 2014, 16, 423–429. [Google Scholar] [CrossRef]

- McNeil, A.J.; Frey, R.; Embrechts, P. Quantitative Risk Management: Concepts, Techniques and Tools; Princeton University Press: Princeton, NJ, USA, 2015. [Google Scholar]

- De Fusco, R.A.; McLeavey, D.W.; Pinto, J.E.; Runkle, D.E.; Anson, M.J. Quantitative Investment Analysis; John Wiley & Sons: Hoboken, NJ, USA, 2015. [Google Scholar]

- Copiello, S. A discounted cash flow variant to detect the optimal amount of additional burdens in public-private partnership transactions. MethodsX 2016, 3, 195–204. [Google Scholar] [CrossRef] [PubMed]

- Liao, M. Model sampling: A stochastic cost-volume-profit analysis. Account. Rev. 1975, 50, 780–790. [Google Scholar]

- Adar, Z.; Barnea, A.; Lev, B. A comprehensive cost-volume-profit analysis under uncertainty. Account. Rev. 1977, 52, 137–149. [Google Scholar]

- Ismail, B.E.; Louderback, J.G. Optimizing and satisficing in stochastic cost-volume-profit analysis. Decis. Sci. 1979, 10, 205–217. [Google Scholar] [CrossRef]

- Constantinides, G.M.; Ijiri, Y.; Leitch, R.A. Stochastic cost-volume-profit analysis with a linear demand function. Decis. Sci. 1981, 12, 417–427. [Google Scholar] [CrossRef]

- Chung, K.H. Cost-volume-profit analysis under uncertainty when the firm has production flexibility. J. Bus. Financ. Account. 1993, 20, 583–592. [Google Scholar] [CrossRef]

- Morano, P.; Tajani, F. The break-even analysis applied to urban renewal investments: A model to evaluate the share of social housing financially sustainable for private investors. Habitat Int. 2017, 59, 10–20. [Google Scholar] [CrossRef]

- Cafferky, M. Breakeven Analysis: The Definitive Guide to Cost-Volume-Profit Analysis; Business Expert Press: New York, NY, USA, 2010. [Google Scholar]

- Dean, J. Cooperative research in cost-price relationships. Account. Rev. 1969, 14, 181–184. [Google Scholar]

- Colantoni, C.S.; Manes, R.P.; Whinston, A. Programming profit rates and pricing decisions. Account. Rev. 1969, 44, 467–481. [Google Scholar]

- Alhabeeb, M.J. Mathematical Finance; John Wiley & Sons: Hoboken, NJ, USA, 2012. [Google Scholar] [CrossRef]

- Hassan, N.; Marquette, R.P.; McKeon, J.M., Jr. Sensitivity analysis: An accounting tool for decision making. Manag. Account. 1978, 59, 43–50. [Google Scholar]

- Klipper, H. Break-even analysis with variable product mix. Manag. Account. 1978, 59, 51–54. [Google Scholar]

- Chan, K. Break-even analysis: A unit cost model. CGA Mag. 1985, 31, 19–20. [Google Scholar]

- Schweitzer, M.; Trossmann, E.; Lawson, G.H. Break-Even Analyses: Basic Model, Variants, Extensions; John Wiley & Sons: Hoboken, NJ, USA, 1992. [Google Scholar]

- Welsch, G.A. I Budget: Come Prepararli e Impiegarli per Programmare e Controllare L’attività Aziendale; Franco Angeli: Milan, Italy, 1994. [Google Scholar]

- Kee, R.C. Implementing cost-volume profit analysis using an activity based costing system. Adv. Manag. Account. 2001, 10, 77–94. [Google Scholar]

- Horngren, C.T. A contribution margin approach to the analysis of capacity utilization. Account. Rev. 1967, 42, 254–264. [Google Scholar]

- Kaplan, R.S.; Atkinson, A.A. Advanced Management Accounting; PHI Learning: New Delhi, India, 2015. [Google Scholar]

- Stenis, J. Environmental optimisation in fractionating industrial wastes using contribution margin analysis as a sustainable development tool. Environ. Dev. Sustain. 2005, 7, 363–376. [Google Scholar] [CrossRef]

- Lev, B. On the association between operating leverage and risk. J. Finance. Quant. Anal. 1974, 9, 627–641. [Google Scholar] [CrossRef]

- Peterson, M.A. Cash flow variability and firm’s pension choice: A role for operating leverage. J. Financ. Econ. 1994, 36, 361–383. [Google Scholar] [CrossRef]

- Novy-Marx, R. Operating leverage. Rev. Financ. 2011, 15, 103–134. [Google Scholar] [CrossRef]

- European Commission. Green Paper on Public Private Partnerships. 2004. Available online: http://eur-lex.europa.eu/legal-content/EN/TXT/HTML/?uri=LEGISSUM:l22012&from=IT (accessed on 9 May 2017).

- Battisti, F.; Guarini, M.R. Public interest evaluation in negotiated public-private partnership. Int. J. Multi-Criteria Decis. Mak. 2017, 7. in press. [Google Scholar]

- Li, D.; Chen, H.; Hui, E.C.M.; Xiao, C.; Cui, Q.; Li, Q. A real option-based valuation model for privately-owned public rental housing projects in China. Habitat Int. 2014, 43, 125–132. [Google Scholar] [CrossRef]

- Tajani, F.; Morano, P. Evaluation of vacant and redundant public properties and risk control: A model for the definition of the optimal mix of eligible functions. J. Prop. Invest. Financ. 2017, 35, 75–100. [Google Scholar] [CrossRef]

- Giuffrida, S.; Napoli, G.; Trovato, M.R. Industrial areas and the city. Equalization and compensation in a value-oriented allocation pattern. In Proceedings of the International Conference on Computational Science and Its Applications, Beijing, China, 4–7 July 2016. [Google Scholar]

- European Commission. Charter of Fundamental Rights. 2000. Available online: http://www.europarl.europa.eu/charter/pdf/text_en.pdf (accessed on 9 May 2017).

- Eurostat. Housing Statistics. 2017. Available online: http://ec.europa.eu/eurostat/statistics-explained/index.php/Housing_statistics (accessed on 9 May 2017).

- Censis. 48° Rapporto Sulla Situazione Sociale Del Paese; Franco Angeli: Rome, Italy, 2014. [Google Scholar]

- Federcasa. Abitazioni Sociali. Motore di Sviluppo—Fattore di coesione. 2014. Available online: http://www.federcasa.it/documenti/archivio/Federcasa_DOSSIER_alloggio_sociale_agg_04_2014.pdf (accessed on 9 May 2017).

- Cassa Depositi e Prestiti. Social Housing. Il Mercato Immobiliare in Italia: Focus Sull’edilizia Sociale; Cassa Depositi e Prestiti: Rome, Italy, 2014. [Google Scholar]

- Guarini, M.R.; Battisti, F. Social housing and redevelopment of building complexes on brownfield sites: The financial sustainability of residential projects for vulnerable social groups. Adv. Mater. Res. 2014, 869–870, 3–13. [Google Scholar] [CrossRef]

- Guarini, M.R. Self-renovation in Rome: Ex Ante, in Itinere and Ex post evaluation. In Proceedings of the International Conference on Computational Science and Its Applications, Beijing, China, 4–7 July 2016. [Google Scholar]

- ANCE. Rapporto 2016 Sulla Presenza Delle Imprese di Costruzione Italiane Nel Mondo. 2016. Available online: https://www.ilcorrieredelgiorno.it/wp-content/uploads/2017/04/RAPPORTO-ANCE-2016.pdf (accessed on 9 May 2017).

- Guarini, M.R. Costi finanziari ed economici nell’autocostruzione. In La città Dimenticata una Proposta per L’emergenza Abitativa; Ferretti, L.V., Mariano, C., Eds.; Prospettive Edizioni: Rome, Italy, 2014. [Google Scholar]

- Guarini, M.R.; Battisti, F. Evaluation and management of land-development processes based on the public-private. Adv. Mater. Res. 2014, 869–870, 154–161. [Google Scholar] [CrossRef]

- Manganelli, B.; Del Giudice, V.; De Paola, P. Linear programming in a multi-criteria model for real estate appraisal. In Proceedings of the International Conference on Computational Science and Its Applications, Beijing, China, 4–7 July 2016. [Google Scholar]

- De Mare, G.; Granata, M.F.; Nesticò, A. Weak and strong compensation for the prioritization of public investments: Multidimensional analysis for pools. Sustainability 2015, 7, 16022–16038. [Google Scholar] [CrossRef]

- Bencardino, M.; Nesticò, A. Demographic changes and real estate values. A quantitative model for analyzing the urban-rural linkages. Sustainability 2017, 9, 536. [Google Scholar] [CrossRef]

- Collegio Ingegneri e Architetti Milano. Prezzi Tipologie Edilizie; DEI: Rome, Italy, 2014. [Google Scholar]

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).