Abstract

Although wealth inequality has many established negatives, this study investigates a potential positive, unprecedented wealth concentration makes it possible for solutions to large and seemingly intractable problems to be deployed by convincing a relatively small number of individuals to invest. In order to probe this potential outcome of inequality, this study quantifies the number of people necessary to radically reduce the greenhouse gas emissions responsible for global climate destabilization from the U.S. electric grid, which is one of the largest sources of emissions. Specifically, this study determined that 1544 GW of solar photovoltaic (PV) technology must be deployed to eliminate the use of fossil fuels on the U.S. electric grid, if PV is conservatively deployed as a function of population density. The results showed that only 79 American multi-billionaires would need to invest in PV. This investment would still leave each investor with a billion dollars of liquid assets as well as substantial long-term profits from PV. The analysis also concluded that 79 people is a conservative upper estimate of those that would need to be convinced of the usefulness of moving to a solar U.S. grid and that this estimate is likely to decrease further in the future.

1. Introduction

By the 1990s in most publicly held companies, the compensation of the highest-paid employees (e.g., top executives) was virtually independent of their job performance [1,2]. Simultaneously, income inequality has risen as the value provided to society by these top earners has become divorced from their earnings.1 Despite the relatively extreme income inequality observed in the U.S., the distribution of wealth is far more concentrated [5,6,7]. In 2017, the distribution of wealth has become clearly unequal, with the lower-income half of the American population owning about 1.1% of the total wealth, while the wealthiest 1% possessing about 35.5% of the wealth [8]. It is well known that much of this wealth is inherited and that the transmission of capital down the generations is an extremely important determinant of an individual’s or a household’s wealth [9,10,11,12,13]. For all of these extremely wealthy people, income is dominated not by their efforts (work), but by their investments (e.g., rental income, capital gains, dividends, interest, etc.). As, for example, the higher one’s income the greater the share of that income is dominated by capital gains [14]. In addition, U.S. tax law for capital gains has an effective tax rate of less than half of those whose income is based on labor [15] and decreases in taxes are evident as the rich become super rich [16]. This tax policy was one of the factors that has further concentrated wealth over time.

The majority of the literature negatively views wealth inequality as studies show that wealth inequality leads to high social costs [17]. Here, this literature will be summarized to put the potential benefit of inequality discussed in this paper into context. Inequality does not generate optimal outcomes for society if the incentives rest on rents [18]. Inequality can cause individuals to divert effort to securing favor from the wealthy because they possess the preponderance of capital, resulting in resource misallocation, corruption, nepotism, and the expected sub-optimal economic, social, and environmental consequences [17,18,19,20,21,22,23,24,25,26,27,28,29]. It has already been well-established that income inequality negatively affects economic growth in the future [19,20,21], in part because lower income households cannot stay healthy and accumulate physical and human capital [22,23] (e.g., poor, smart, young people cannot go on to college because of access to funding or perceived unacceptable debt burden, which reduces overall labor productivity [18]). This inequality also contributes to lower intergenerational mobility (e.g., less earnings mobility across the generations) [24] and increases the probability of political conflict [25]. Simultaneously, income inequality generally creates sub-optimal policy [26], which reduces the public good to help economic growth and creates an inequality of opportunities for the poor (e.g., access to education, credit, infrastructure, public decision making, etc.) [27]. In extreme situations, a preponderance of inequality can drive a global financial crisis [28] and policies that further inequality are formalized into law because of lobbying [29].

Although inequality has these established negatives, there is a positive to inequality that concentrates wealth for a few individuals, as follows: For solving large and capital-intensive problems, the number of individuals necessary to invest has grown smaller over time and may be approaching a point where the individuals could conceivably all know each other as they already preferentially associate with one another [30]. This association is important as it would make it possible for solutions to large and seemingly intractable problems to be deployed by convincing a relatively small number of individuals to invest within their social circle. In order to probe this potential benefit for inequality and wealth concentration, this study quantifies the number of billionaires necessary to reduce the greenhouse gas emissions responsible for climate destabilization in areas across the globe [31]. Specifically, it investigates elimination of carbon emissions from one of the largest sources—combustion of fossil fuels for the U.S. electric grid (e.g., the three grids made up of the Western interconnection, Eastern interconnection, and ERCOT (Electric Reliability Council of Texas), which are loosely connected, that service the continental U.S.) [32]. This study will determine the amount of solar photovoltaic (PV) technology that must be deployed to convert the U.S. electric grid, which is currently 1.2% solar [33], to eliminate all existing fossil fuels. Then, it will estimate the costs for that conversion and the number of billionaires that would be able to maintain billionaire status while still completing the conversion. The results will be presented and discussed in the context of leveraging wealth concentration by focusing excess capital from the wealthiest individuals to partially solve global climate destabilization from greenhouse gas (GHG) emissions that threaten everyone throughout all global societies.

2. Materials and Methods

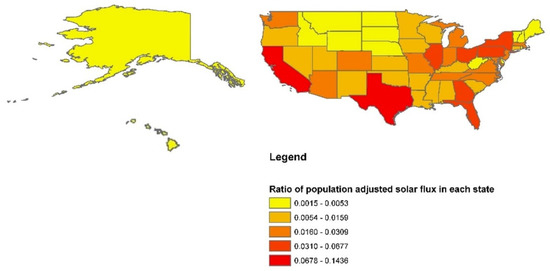

Data on U.S. population and solar flux was collected and geolocated. Three databases were obtained to analyze the ratio of population-adjusted solar flux for each state, as follows: (1) A shapefile of the United States was obtained from the ArcGIS database [34], (2) a shapefile of normal direct solar irradiance was obtained from the National Renewable Energy Laboratory database [35], and (3) the population density throughout the U.S. was obtained from the U.S. Census [36]. The ratio of population-adjusted solar flux in each state was transcribed to a map utilizing ArcMap version 10.6.1. Population-adjusted solar flux is needed to determine a practical PV deployment density over the U.S. and prevent unnecessarily costly adaptations of the electric grid for the placement of large PV systems in high solar flux areas. Thus, the calculations here are based on providing solar power where the people are located, which has the benefits of distributed generation.

In order to obtain the average population-adjusted solar flux for the U.S., FUSA in kWh/m2/day, the following equation was developed here and used the fraction of solar flux multiplied by the population of each state for the whole country:

where Fs is the average kWh/m2/day of solar irradiation in each state, s; and ps is the population of state, s. Thus, a ratio is determined of the population adjusted solar flux for each state in the large bracket. By summing this ratio, times the solar flux for the state, the average solar flux for the whole U.S. is determined.

The list of 2123 individuals that have more than a billion U.S. dollars in assets, maintained by Forbes [37], was first screened for Americans, which reduced the number to 568 individuals listed in Appendix A. In order to ensure that each individual maintained US$1 billion in wealth if they decided to invest in solarizing the U.S., the aggregate potential capital was calculated by:

where wn is the individual wealth for each person and Tc is the total number of individuals needed to meet a capital investment goal. So, for example, for all 568 Americans, C is equal to US$2511.7 billion.

U.S. Energy Information Administration data for 2017 [38] was used to calculate the energy needing to be resourced. The U.S. used 4.034 trillion kWh/year in 2017 in total, but fossil fuels, which all contribute to climate change, were only responsible for 2.536 trillion kWh/year [38]. So, this latter value was used. The National Renewable Energy Laboratory estimates [39] that the total installed system cost, which is one of the primary inputs used to compute the levelized cost of electricity (LCOE) [40], has declined to US$2.80 per direct current watts (Wdc) for residential systems, US$1.85 Wdc for commercial, US$1.03 Wdc for fixed-tilt utility-scale systems, and US$1.11 Wdc for one-axis tracking utility-scale systems. The value of US$1.03 Wdc for fixed-tilt utility-scale systems is used in the final analysis because previous learning rates [41,42,43,44,45] for the global PV industry has resulted in continuous and aggressive reduction in the costs of solar modules [46,47]. As of January 2019, the spot price of the lowest cost PV modules has dropped below US$0.20/W [48]. Technical improvements, like moving to black silicon, are expected to drop those costs further [49] and the International Renewable Energy Agency (IRENA) predicts that the prices will fall by 60% in the next decade [50]. Thus, it is within reason that the PV prices that have already been obtained in the U.S. on the large scale could be met on the small, distributed scale in the near future, with a massive scale up of the industry as analyzed here.

3. Results

The ratio of population-adjusted solar flux in each state is shown in Figure 1.

Figure 1.

Ratio of population-adjusted solar flux in each U.S. State.

Using Equation (2) and the data shown in Figure 1, the FUSA was found to be 4.499 kWh/m2/day. Using the conservative assumption that solar PV is deployed as a function of population and not optimal solar flux, this 4.499 kWh/m2/day demands that 1544 GW of installed PV. This amount of PV would produce the 2.536x1012 kWh needed to replace all fossil fuels for electricity production within the U.S. At $1.03/Wp (per peak Watt), this would entail an investment of US$1.59 trillion. Historically, US$1.59 trillion would be considered a substantial sum of capital, however, as discussed in the above, a relatively small number of people (568) in America now control more than this quantity of capital. After assuming that each multi-billionaire in the U.S. would dedicate their wealth in excess of $1 billion to solarization, the cumulative sum of Equation (2) was calculated and is shown in Table 1.

Table 1.

Cumulative American multi-billionaires necessary to reach investment goals of complete replacement of all of the fossil fuel-based electricity generation in the U.S. with solar.

As can be seen in Table 1, only 79 American multi-billionaires would need to invest to convert all of the U.S. to solar from fossil fuels. This investment would still leave each investor with a billion dollars to use in any way they please.

4. Discussion

The results of this study indicate that a relatively small number of America’s wealthiest individuals could completely convert the U.S. electric grid away from fossil fuels by replacing the remaining fossil fuel generation with solar. Seventy-nine Americans would need to give up some of their wealth to make this conversion possible and although they would each remain a billionaire, there are three areas that need to be discussed in the next three subsections, as follows:

- Why might multi-billionaires want to voluntarily give up their wealth to solarize the U.S.?

- What is the probability that multi-billionaires would be willing to make the required investment in solar even if they found the reasoning compelling?

- What are the primarily limitations of the methodology and assumptions made here that resulted in such a low number of individuals needing to give up their wealth to radically remake the U.S. electric grid?

4.1. Why Would a Multi-Billionaire Want to Invest in Solarizing the U.S.?

Both global GHG emissions [31] and global atmospheric carbon dioxide (CO2) concentrations are increasing rapidly [51], which creates an enormous urgency to cut emissions [52]. The resultant climate change is well-established with a high confidence as are the negative impacts on natural and socio-economic systems [53,54] including the following:

- (i)

- Higher temperatures and heat waves that result in thousands of deaths from hyperthermia and are expected to increase [55,56,57],

- (ii)

- other adverse effects on human society and health [58],

- (iii)

- crop failures [59,60] that aggravate global hunger and food insecurity [61,62,63],

- (iv)

- electric power outages [64,65],

- (v)

- rising sea levels that cause low-lying coastal areas throughout the world to submerge gradually, as well as erosion of shorelines [66,67],

- (vi)

- increased risk of flooding [68] and saltwater intrusion [69], as well as severe storms that cause more damage to coastal environments [70],

- (vii)

- risks to forests [71,72,73,74],

- (viii)

- droughts [75] and

- (ix)

- fire [71,76,77].

These negative externalities have been shown to be due to human activities, with a confidence level of 95% (primarily combustion of fossil fuels, which is the dominant cause of global warming from 1951 to 2010) [78,79]. Climate change is widely viewed as one of the greatest challenges of our age [80] and GHG emissions from electricity generation is one of the largest contributors to the problem in the U.S. (in 2016 transportation surpassed electric generation for the first time) [32]. Some of the billionaires shown in Table 1 have already discussed what a large problem climate change is and have begun to contribute to energy solutions by investing in Breakthrough Energy Ventures, which is a billion-dollar fund backed by some of the world’s top entrepreneurs and investors, including the following: Jeff Bezos, Bill Gates, Mark Zuckerberg, and Michael Bloomberg [81]. Bill Gates, for example, has thought hard about not only the solution to climate change, but others as well [82]. Other multi-billionaires on the list, like Elon Musk, the Tesla founder, said sustainable energy solutions are technologically viable and have been working aggressively for their success [83]. In addition, many of the companies that American multibillionaires control have made substantial investments in solar; so, they are familiar with the technical and economic potential of the technology. For example, Larry Page and Sergey Brin’s Google officially hit its 100% renewable energy target in 2018 [84] and the Walton’s Walmart has made a public commitment to solar [85], with the second most onsite PV of any company in the world [86]. Despite this promise, there are a minority on the list in Table 1 who are heavily invested in fossil fuels and would find the transition more challenging. For these individuals, as the potential liability for climate change becomes more serious [87], they might also be convinced to convert for the good of the companies they helped develop. As of this writing, no lawsuits have been won to make a corporation that is a GHG emitter liable for emissions. There are, however, multiple such lawsuits pending and, as the potential liability is so large that it could easily bankrupt most companies, converting to renewable energy could be used as a hedge against this risk [87].

Alternatively, these individuals may be interested in solarizing the electrical grid using a distributed generation model, proposed here, by following the largely successful securitization of PV assets [88,89,90,91] due to the purely economic advantages of PV. PV is made even more profitable by the plethora of tax incentives available, which result in large economic returns on investment. First, the renewable energy tax credit allows the system owner to effectively reduce system costs by 30% [92] and the systems are eligible for MACRS (Modified Accelerated Cost Recovery System) 5-year accelerated depreciation. It should be noted here that these tax credit and depreciation factors were conservatively not used in the financial estimates made in the results to eliminate any risk due to policy changes at the U.S. federal level, which would make the estimates inaccurate. Using these mechanisms could make the PV investments discussed in the results substantially profitable for the investors. It is noted that this profitability would need to be weighed against other potential sources of profits for the multi-billionaires, as well as their personal stake in the moving society towards sustainability.

As of this writing, the federal investment tax credit is available at 30% through 2019 and steps down to 26% in 2020, 22% in 2021, and 10% for commercial and industrial systems thereafter [93]. Business owned systems are also eligible for MACRS 5-year accelerated depreciation. The 2017 tax law allows for 5 years of 100% bonus depreciation for systems installed after September 27, 2017 [94]. The term 100% bonus depreciation means that the whole project’s applicable tax depreciation is accelerated to the first year of the system’s commissioning [95]. This is especially significant for investors in higher income tax brackets, as they see comparatively more value because electricity expenses are paid with after-tax dollars—they are not tax deductible. Different states offer solar energy property tax incentives, providing various amounts of tax exemptions on residential, commercial, and industrial solar PV systems [96]. A final tax incentive opportunity is the creation of Opportunity Zones [97]. This is an investment vehicle that attempts to match economic need with private investment. Qualified opportunity zone property includes any qualified opportunity zone stock, any qualified opportunity zone partnership interest, and any qualified opportunity zone business property [97]. Solar PV systems are well within the defined qualified business property. First, it allows for the temporary deferral of including gross income for gains that are reinvested in a qualified opportunity fund [97]. Second, it allows for exclusion of up to 15% of the gain on the original investment, that is deferred by the investment in the qualified opportunity fund if held for seven years [97]. Third, the taxpayer may elect to exclude the post-acquisition gains on investments from gross income in qualified opportunity funds that are held for at least ten years [97]. As an added bonus, opportunity zone tax benefits can be layered on top of the Renewable Energy Investment Tax Credit and accelerated depreciation to make an even better investment.

4.2. Probability of Solar Investment

Many of those on the list in Table 1 are already familiar with solar and are investing in it. With the potential to be in a group of the elite that would be potentially credited with “saving the world”, there is a non-zero probability that convincing all of these 79 individuals to make the investment is possible. This hypothesis is further supported by the number of multi-billionaires pledging to give away much of their fortunes before they die. This is formally being done in the Giving Pledge, which is a commitment by the world’s wealthiest individuals and families to dedicate the majority of their wealth to giving back to the rest of society through philanthropy [94]. At the end of 2018, the pledge had 187 pledgers including several on the list in Table 1, including Warren Buffett, Larry Ellison, James Simons, George Kaiser, and George Lucas [98]. None of these pledges were factored into the analysis here. In academia, there has been an enormous debate raging about inequality [19,99,100,101,102,103,104,105,106,107,108] but there appears to be a potential consensus forming among the world’s economic elite that their wealth should be used for the betterment of society. Future work is needed to quantify these consensuses and the probability that a relatively small group would collaborate on such a major project. It should also be noted that some of those on the list (e.g., Charles (5) and David (6) Koch) are heavily invested in fossil fuel industries, as well as climate denial activities [109]). However, as noted above, if even a single GHG emissions liability case is won, all investors in fossil fuel industries would financially benefit from immediate renewable energy investment to mitigate climate change-related liability. In addition, all of the analysis presented here assumed conventional economics (e.g., no value was assigned to environmental externalities). However, as the costs of climate change continue to mount [54,110,111], the discipline of green economics [112,113,114] may gain prominence over conventional economics, which would have the effect of making solar PV even more economically profitable.

4.3. Limitations

This study has several limitations. First, this study assumed that there was more than enough non-shaded optimal surface area to allow for distributed generation with PV, but it did not explicitly calculate siting for the 1544 GW of PV necessary to replace all of fossil fuel electricity production in the U.S. The nuances of territory and siting at both the large scale for PV output [115], as well as DG benefits [116,117] and roof top [118,119,120,121,122] as well as façade [123] locations have been covered extensively. Here, the conservative assumption about locating the PV systems was based on a distributed generation model where the PV would be located following population density in each state across the U.S. There are far more than enough optimal locations (surface area) to install PV in each region to cover more than 100% of the entire U.S. electricity use (let alone the 63% needed here) [124]. A more granular analysis is left for future work. Second, this study did not look at past investments nor to future investments that would reduce the need for the full 1544 GW of PV. The calculations for the PV necessary to completely eliminate fossil fuels from U.S. electric generation are only for the new solar investments necessary. All previous investments and investments in other renewable energy technologies, like wind power, are not considered. It also did not attempt to quantify profitable investments in energy efficiency and conserving technologies (e.g., lighting [125], moving from resistive electricity-based heating to heat pumps [126], buildings [127], and electric motors and drives [128]). It is highly likely that there will continue to be investments in energy efficiency and other renewable energy technologies. Thus, it is highly likely that the value of PV needed, calculated here, is an overestimate. Determining the degree of that overestimate is left for future work. Third, this study assumed modern PV technology. Again, the learning rate in PV production and the efficiency of the technologies can be expected to continue to climb, thus reducing PV costs further [48,49]. This again was taken as a conservative assumption, the correction of which is left for future work.

This study only looked at the generation component of electricity and did not take into account load balancing, efficiency, storage, power quality factor, or transmission. With the solar slated to be put in place, the investment in storage and transmission and other technologies to maintain operation of the grid would be expected to be provided using the conventional utility models. There is recent evidence that this assumption is valid in Germany, where renewables have been able to cover 100% of power for the first time as of January 2018 [129]. Critics may demand that the 79 billionaires must also pay for storage to regulate the grid. This study does not consider this additional investment for the following complexities related to the structure of the U.S. electric utilities, that would both increase as well as decrease costs that will be briefly summarized here. First, only roughly 63% of the power sources on the U.S. grid would need to be converted to solar to replace the existing fossil fuels. The solar specifically investigated here is for use in distributed generation (DG—the assumption based on population density-based deployment). It is well established that DG can postpone investments in generation, transmission, and distribution as electrical power demand grows and, at a large enough scale, eliminate them [130]. DG also reduces transmission losses [131]. Elimination of these losses would result in cost savings of about 10–15% [132]. Other DG benefits include decreased pollution and greenhouse gas emissions [133] and their concomitant potential reductions in mortality by converting to solar [134]. For coal replacement in particular, these premature deaths prevented can be substantial to the point that they number more per year than the current total coal mining employment [135]. In addition, DG provides transmission congestion relief, increased reliability, and ancillary services [131,136]. The economic impacts of these details are highly dependent on the potential for changes in laws revolving around electric utilities and green economics and are left for future work to ensure a smooth transition from fossil fuel generation to solar.

Another limitation is addressing the variations in the PV power that exist in a high PV penetration scenario, like the one discussed in this study is due to (i) the night/day cycle, (ii) the yearly cycle, and (iii) fluctuating cloud conditions. Variations (i) and (ii) will be addressed by changes in the grid and investments by conventional utilities as more PV is deployed and storage becomes necessary. However, reason (iii) (of fluctuating cloud conditions and thus rapidly changing PV power) is the largest problem that needs to be addressed at high penetration rates immediately. However, cloud variations can be largely mitigated using the deployment recommended in this study (e.g., DG). Specifically, by deploying solar PV systems over a larger geographic area, any specific clouds have only a small effect on the overall grid. For example, if a network of PV installations is dispersed throughout a 100 km2 area, the tolerable acute penetration for PV will increase to 18.1% and if the area expands to 1000 km2, the limit for PV penetration is 35.8% [137]. It should be noted that, in the solar PV, penetration level is the real time percentage (not the overall percentage of PV electricity generation), which would of course be considerably less as peak sun hours are only available for a few hours each day. Effectively, this means that a PV penetration many times the current value could be tolerated from the grid before any changes are necessary. As an increasing penetration of PV is made, if it is deployed with DG strategies, the penetration level can get to about a third before significant changes have to be made. Some existing policies and pricing methods will help make these changes less challenging. In many cases, this will mean using existing techniques for load shedding, load temporal displacement, and the usage of more storage. For example, time of use metering (TOU), which currently favors using electricity at night, will be reversed so that using electricity in the middle of the day will be the least costly when PV is at full output. As the goal of elimination of fossil fuel production for the grid is approached, utilities would need to invest in storage and other technologies to ensure normal operation and they would do it following the same basis that they currently do to make capital investments for generation that would no longer be necessary. The details of this arrangement and the timeline are left for future work.

Overall, this study is overly conservative in the number of billionaires needed to solarize the U.S. because it made the assumption that solar would be distributed based on population density and that current PV prices would be used. There is an expectation of cost decreases based on deployment of known technologies, as well as the scale, as society approaches a sustainable future [138]. The following effects would be expected after 79 of the wealthiest Americans began to invest all but US$1 billion in conversion of the U.S. electric grid away from fossil fuels. First, the price of solar, after the first shock to supply by the rapidly increased demand, would be decreased. Similar drops would be expected in the balance of systems components (i.e., racking, electronics) as well as, eventually, storage. In addition, less PV would be necessary if it were strategically located in high solar flux areas in certain utility regions. Similarly, the growth of other renewable energy sources, like wind, which currently costs less than fossil fuel generation, is expected to continue and would also reduce the demand for solar. Likewise, with the surge in demand from the proposed solar replacement of all fossil-fuel generation in the U.S., the price per unit solar would be expected to drop considerably. At the same time, the concentration of wealth continues to increase in the U.S. [139,140,141], and globally (the richest 26 globally own more wealth than the bottom 50% of humanity [142]). All of these factors combine to mean less and less individuals will need to be convinced as time goes forward. For these reasons, it can be comfortably concluded that 79 is a conservative estimate on the number of American multi-billionaires that would need to be convinced of the usefulness of moving to a solar U.S. grid in order to make it a reality. Finally, this analysis can be expanded beyond the U.S. to globally reduce greenhouse gas emissions, while accounting for the life cycle of greenhouse gas emissions of various types [143], as well as the impact on emissions as a function of growth of PV [144].

5. Conclusions

Although wealth inequality has many established negatives, this study has shown the potential positive that, when solving large capital-intensive problems, the number of individuals that need to be convinced to act has become small and manageable. Here, we have investigated the potential to reduce greenhouse gas emissions, responsible for climate destabilization in areas across the globe, in the U.S. electric grid by first determining the amount of solar PV technology that must be deployed to eliminate all fossil fuels from the U.S. electric grid, the costs for that conversion, and the number of multi-billionaires that would be able to maintain billionaire status while still completing the conversion. The results show that only 79 American multi-billionaires are needed. The analysis also concludes that this is a conservative estimate on the number that would need to be convinced of the usefulness of moving to a solar U.S. grid and that upper estimate is likely to decrease even further in the future.

Author Contributions

Conceptualization, J.M.P.; Methodology, J.M.P.; Validation, E.P.; Formal Analysis, J.M.P. and E.P.; Investigation, J.M.P. and E.P.; Resources, J.M.P.; Data Curation, E.P.; Writing-Original Draft Preparation, J.M.P.; Writing-Review & Editing, J.M.P. and E.P.; Visualization, E.P.; Funding Acquisition, J.M.P.

Funding

This research was funded by the Witte Endowment.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

| 2018 RANKING REAL TIME RANKING | |||

| 2018 World Rank | American Multi-Billionaires | Wealth (B US$) | Source of Wealth |

| #1 | Jeff Bezos | 112 | Amazon |

| #2 | Bill Gates | 90 | Microsoft |

| #3 | Warren Buffett | 84 | Berkshire Hathaway |

| #5 | Mark Zuckerberg | 71 | |

| #8 | Charles Koch | 60 | Koch Industries |

| #8 | David Koch | 60 | Koch Industries |

| #10 | Larry Ellison | 58.5 | software |

| #11 | Michael Bloomberg | 50 | Bloomberg LP |

| #12 | Larry Page | 48.8 | |

| #13 | Sergey Brin | 47.5 | |

| #14 | Jim Walton | 46.4 | Walmart |

| #15 | S. Robson Walton | 46.2 | Walmart |

| #16 | Alice Walton | 46 | Walmart |

| #21 | Sheldon Adelson | 38.5 | casinos |

| #22 | Steve Ballmer | 38.4 | Microsoft |

| #28 | Phil Knight | 29.6 | Nike |

| #34 | Jacqueline Mars | 23.6 | candy, pet food |

| #34 | John Mars | 23.6 | candy, pet food |

| #39 | Michael Dell | 22.7 | Dell computers |

| #44 | Paul Allen | 21.7 | Microsoft, investments |

| #47 | Thomas Peterffy | 20.3 | discount brokerage |

| #48 | Len Blavatnik | 20.2 | diversified |

| #52 | James Simons | 20 | hedge funds |

| #54 | Elon Musk | 19.9 | Tesla Motors |

| #58 | Laurene Powell Jobs | 18.8 | Apple, Disney |

| #67 | Ray Dalio | 17.7 | hedge funds |

| #73 | Carl Icahn | 16.8 | investments |

| #80 | Donald Bren | 16.3 | real estate |

| #83 | Abigail Johnson | 15.9 | money management |

| #83 | Lukas Walton | 15.9 | Walmart |

| #94 | Rupert Murdoch | 15 | newspapers, TV network |

| #100 | Harold Hamm | 14.1 | oil & gas |

| #102 | Steve Cohen | 14 | hedge funds |

| #102 | Dustin Moskovitz | 14 | |

| #106 | Charles Ergen | 13.4 | satellite TV |

| #106 | Eric Schmidt | 13.4 | |

| #108 | Philip Anschutz | 13 | investments |

| #108 | Jim Kennedy | 13 | media |

| #108 | Blair Parry-Okeden | 13 | media, automotive |

| #113 | Leonard Lauder | 12.9 | Estee Lauder |

| #117 | Stephen Schwarzman | 12.6 | investments |

| #121 | Donald Newhouse | 12.3 | media |

| #132 | Andrew Beal | 11.6 | banks, real estate |

| #134 | John Menard, Jr. | 11.5 | home improvement stores |

| #138 | David Tepper | 11 | hedge funds |

| #145 | Pierre Omidyar | 10.5 | eBay |

| #152 | Ronald Perelman | 9.8 | leveraged buyouts |

| #154 | Micky Arison | 9.7 | Carnival Cruises |

| #158 | Thomas Frist, Jr. | 9.6 | health care |

| #162 | Charles Schwab | 9.4 | discount brokerage |

| #164 | Herbert Kohler, Jr. | 9.3 | plumbing fixtures |

| #170 | Jan Koum | 9.1 | |

| #172 | James Goodnight | 9 | software |

| #172 | Ken Griffin | 9 | hedge funds |

| #178 | James Chambers | 8.7 | media, automotive |

| #178 | Katharine Rayner | 8.7 | media, automotive |

| #178 | Margaretta Taylor | 8.7 | media, automotive |

| #181 | Gordon Moore | 8.5 | Intel |

| #183 | Stanley Kroenke | 8.3 | sports, real estate |

| #186 | John Malone | 8.1 | cable television |

| #190 | Carl Cook | 8 | medical devices |

| #190 | David Geffen | 8 | movies, record labels |

| #190 | George Soros | 8 | hedge funds |

| #196 | Edward Johnson, III. | 7.9 | money management |

| #198 | David Duffield | 7.8 | business software |

| #198 | George Kaiser | 7.8 | oil & gas, banking |

| #198 | Patrick Soon-Shiong | 7.8 | pharmaceuticals |

| #205 | Stephen Ross | 7.6 | real estate |

| #207 | Pauline MacMillan Keinath | 7.4 | Cargill |

| #211 | Eli Broad | 7.3 | investments |

| #211 | Sun Hongbin | 7.3 | real estate |

| #211 | Christy Walton | 7.3 | Walmart |

| #217 | Shahid Khan | 7.2 | auto parts |

| #222 | John Doerr | 7.1 | venture capital |

| #242 | David Green | 6.8 | retail |

| #242 | Hank & Doug Meijer | 6.8 | supermarkets |

| #251 | Brian Acton | 6.6 | |

| #251 | Ann Walton Kroenke | 6.6 | Walmart |

| #261 | Leon Black | 6.5 | private equity |

| #261 | John Paulson | 6.5 | hedge funds |

| #265 | David Shaw | 6.4 | hedge funds |

| #265 | John A. Sobrato | 6.4 | real estate |

| #274 | Daniel Gilbert | 6.3 | Quicken Loans |

| #281 | Richard Kinder | 6.2 | pipelines |

| #281 | Robert Kraft | 6.2 | New England Patriots |

| #281 | Ralph Lauren | 6.2 | Ralph Lauren |

| #287 | Les Wexner | 6.1 | retail |

| #289 | Whitney MacMillan | 6 | Cargill |

| #296 | Marijke Mars | 5.9 | candy, pet food |

| #296 | Pamela Mars | 5.9 | candy, pet food |

| #296 | Valerie Mars | 5.9 | candy, pet food |

| #296 | Victoria Mars | 5.9 | candy, pet food |

| #305 | Nancy Walton Laurie | 5.8 | Walmart |

| #305 | Tom & Judy Love | 5.8 | retail & gas stations |

| #305 | Robert Rowling | 5.8 | hotels, investments |

| #305 | Dennis Washington | 5.8 | construction, mining |

| #315 | David Sun | 5.7 | computer hardware |

| #315 | John Tu | 5.7 | computer hardware |

| #321 | Jensen Huang | 5.6 | semiconductors |

| #321 | Charles Johnson | 5.6 | money management |

| #321 | Jerry Jones | 5.6 | Dallas Cowboys |

| #321 | Richard LeFrak | 5.6 | real estate |

| #321 | Steven Rales | 5.6 | manufacturing |

| #334 | Dannine Avara | 5.5 | pipelines |

| #334 | Scott Duncan | 5.5 | pipelines |

| #334 | Milane Frantz | 5.5 | pipelines |

| #334 | Diane Hendricks | 5.5 | roofing |

| #334 | Gabe Newell | 5.5 | videogames |

| #334 | Randa Williams | 5.5 | pipelines |

| #351 | Richard DeVos | 5.4 | Amway |

| #351 | George Roberts | 5.4 | private equity |

| #351 | Edward Roski, Jr. | 5.4 | real estate |

| #365 | Jim Davis | 5.3 | New Balance |

| #365 | David Filo | 5.3 | Yahoo |

| #365 | Henry Kravis | 5.3 | private equity |

| #372 | Israel Englander | 5.2 | hedge funds |

| #372 | Marian Ilitch | 5.2 | pizza, sports team |

| #372 | Bruce Kovner | 5.2 | hedge funds |

| #372 | George Lucas | 5.2 | Star Wars |

| #372 | Robert Rich, Jr. | 5.2 | frozen foods |

| #382 | Bernard Marcus | 5.1 | Home Depot |

| #382 | Fred Smith | 5.1 | FedEx |

| #382 | Ronda Stryker | 5.1 | medical equipment |

| #388 | Martha Ingram | 5 | book distribution, transportation |

| #388 | Karen Pritzker | 5 | hotels, investments |

| #404 | Robert Bass | 4.9 | oil, investments |

| #404 | Marc Benioff | 4.9 | business software |

| #404 | Charles Dolan | 4.9 | cable television |

| #404 | Ray Lee Hunt | 4.9 | oil, real estate |

| #404 | John Overdeck | 4.9 | hedge funds |

| #404 | Sumner Redstone | 4.9 | media |

| #404 | Reinhold Schmieding | 4.9 | medical devices |

| #404 | David Siegel | 4.9 | hedge funds |

| #404 | Sam Zell | 4.9 | real estate, private equity |

| #422 | Bubba Cathy | 4.8 | Chick-fil-A |

| #422 | Dan Cathy | 4.8 | Chick-fil-A |

| #422 | Rupert Johnson, Jr. | 4.8 | money management |

| #422 | Travis Kalanick | 4.8 | Uber |

| #422 | Trevor Rees-Jones | 4.8 | oil & gas |

| #422 | Jeff Skoll | 4.8 | eBay |

| #422 | Daniel Ziff | 4.8 | investments |

| #422 | Dirk Ziff | 4.8 | investments |

| #422 | Robert Ziff | 4.8 | investments |

| #441 | Stanley Druckenmiller | 4.7 | hedge funds |

| #441 | Ted Lerner | 4.7 | real estate |

| #441 | Gwendolyn Sontheim Meyer | 4.7 | Cargill |

| #441 | J. Christopher Reyes | 4.7 | food distribution |

| #441 | Jude Reyes | 4.7 | food distribution |

| #441 | Sheldon Solow | 4.7 | real estate |

| #456 | Jeremy Jacobs, Sr. | 4.6 | food service |

| #456 | Chris Larsen | 4.6 | cryptocurrency |

| #466 | Paul Tudor Jones, II. | 4.5 | hedge funds |

| #466 | John Sall | 4.5 | software |

| #466 | Leonard Stern | 4.5 | real estate |

| #480 | Tamara Gustavson | 4.4 | self-storage |

| #480 | John Morris | 4.4 | sporting goods retail |

| #480 | Robert Smith | 4.4 | private equity |

| #480 | Russ Weiner | 4.4 | energy drinks |

| #499 | Rocco Commisso | 4.3 | telecom |

| #499 | Tilman Fertitta | 4.3 | Houston Rockets, entertainment |

| #499 | Terrence Pegula | 4.3 | natural gas |

| #499 | Robert Pera | 4.3 | wireless networking gear |

| #499 | Gary Rollins | 4.3 | pest control |

| #499 | Randall Rollins | 4.3 | pest control |

| #499 | Alejandro Santo Domingo | 4.3 | beer |

| #499 | Andres Santo Domingo | 4.3 | beer |

| #499 | Roger Wang | 4.3 | retail |

| #514 | Stephen Bisciotti | 4.2 | staffing, Baltimore Ravens |

| #514 | Austen Cargill, II. | 4.2 | Cargill |

| #514 | James Cargill, II. | 4.2 | Cargill |

| #514 | Archie Aldis Emmerson | 4.2 | timberland, lumber mills |

| #514 | Marianne Liebmann | 4.2 | Cargill |

| #514 | Bobby Murphy | 4.2 | Snapchat |

| #514 | Igor Olenicoff | 4.2 | real estate |

| #514 | Walter Scott, Jr. | 4.2 | utilities, telecom |

| #514 | Clemmie Spangler, Jr. | 4.2 | investments |

| #527 | Arthur Blank | 4.1 | Home Depot |

| #527 | Jack Dangermond | 4.1 | mapping software |

| #527 | James Jannard | 4.1 | sunglasses |

| #527 | Isaac Perlmutter | 4.1 | Marvel comics |

| #527 | H. Ross Perot, Sr. | 4.1 | computer services, real estate |

| #527 | Thomas Pritzker | 4.1 | hotels, investments |

| #527 | Julian Robertson, Jr. | 4.1 | hedge funds |

| #527 | Evan Spiegel | 4.1 | Snapchat |

| #527 | Kelcy Warren | 4.1 | pipelines |

| #550 | Ben Ashkenazy | 4 | real estate |

| #550 | Dagmar Dolby | 4 | Dolby Laboratories |

| #550 | Dan Friedkin | 4 | Toyota dealerships |

| #550 | Ronald Lauder | 4 | Estee Lauder |

| #550 | Michael Moritz | 4 | venture capital |

| #550 | Richard Schulze | 4 | Best Buy |

| #550 | Jeff Sutton | 4 | real estate |

| #572 | Rick Caruso | 3.9 | real estate |

| #572 | Tom Gores | 3.9 | private equity |

| #572 | Stewart and Lynda Resnick | 3.9 | agriculture, water |

| #572 | Jerry Speyer | 3.9 | real estate |

| #572 | Harry Stine | 3.9 | agriculture |

| #572 | Steven Udvar-Hazy | 3.9 | aircraft leasing |

| #588 | Nathan Blecharczyk | 3.8 | Airbnb |

| #588 | Brian Chesky | 3.8 | Airbnb |

| #588 | Joe Gebbia | 3.8 | Airbnb |

| #588 | Jeff Greene | 3.8 | real estate, investments |

| #588 | Robert McNair | 3.8 | energy, sports |

| #588 | Ira Rennert | 3.8 | investments |

| #588 | Henry Samueli | 3.8 | semiconductors |

| #606 | Nick Caporella | 3.7 | beverages |

| #606 | Mark Cuban | 3.7 | online media |

| #606 | Ken Fisher | 3.7 | money management |

| #606 | H. Fisk Johnson | 3.7 | cleaning products |

| #606 | Imogene Powers Johnson | 3.7 | cleaning products |

| #606 | S. Curtis Johnson | 3.7 | cleaning products |

| #606 | Helen Johnson-Leipold | 3.7 | cleaning products |

| #606 | Winifred Johnson-Marquart | 3.7 | cleaning products |

| #606 | Michael Milken | 3.7 | investments |

| #629 | Jeffery Hildebrand | 3.6 | oil |

| #629 | Edward Johnson, IV. | 3.6 | money management |

| #629 | Elizabeth Johnson | 3.6 | money management |

| #629 | Peter Kellogg | 3.6 | investments |

| #629 | Rodger Riney | 3.6 | discount brokerage |

| #629 | Steven Spielberg | 3.6 | Movies |

| #629 | Anita Zucker | 3.6 | chemicals |

| #652 | Judy Faulkner | 3.5 | health IT |

| #652 | Joshua Harris | 3.5 | private equity |

| #652 | Douglas Leone | 3.5 | venture capital |

| #652 | Anthony Pritzker | 3.5 | hotels, investments |

| #652 | J.B. Pritzker | 3.5 | hotels, investments |

| #652 | Mitchell Rales | 3.5 | manufacturing, investments |

| #652 | Bernard Saul, II. | 3.5 | banking, real estate |

| #652 | Donald Sterling | 3.5 | real estate |

| #679 | Riley Bechtel | 3.4 | engineering, construction |

| #679 | Stephen Bechtel, Jr. | 3.4 | engineering, construction |

| #679 | Jimmy Haslam | 3.4 | gas stations, retail |

| #679 | Min Kao | 3.4 | navigation equipment |

| #679 | Steve Wynn | 3.4 | casinos, hotels |

| #703 | John Arnold | 3.3 | hedge funds |

| #703 | Sid Bass | 3.3 | oil, investments |

| #703 | John Brown | 3.3 | medical equipment |

| #703 | Charles Cohen | 3.3 | real estate |

| #703 | Rakesh Gangwal | 3.3 | airline |

| #703 | Reid Hoffman | 3.3 | |

| #703 | Amos Hostetter, Jr. | 3.3 | cable television |

| #703 | Ken Langone | 3.3 | investments |

| #703 | George Lindemann | 3.3 | investments |

| #703 | Mary Alice Dorrance Malone | 3.3 | Campbell Soup |

| #703 | Henry Nicholas, III. | 3.3 | semiconductors |

| #703 | Pat Stryker | 3.3 | medical equipment |

| #729 | Neil Bluhm | 3.2 | real estate |

| #729 | Andrew & Peggy Cherng | 3.2 | restaurants |

| #729 | Scott Cook | 3.2 | software |

| #729 | Leon G. Cooperman | 3.2 | hedge funds |

| #729 | John Paul DeJoria | 3.2 | hair products, tequila |

| #729 | Tom Golisano | 3.2 | payroll services |

| #729 | Daniel Loeb | 3.2 | hedge funds |

| #729 | Daniel Och | 3.2 | hedge funds |

| #729 | Marc Rowan | 3.2 | private equity |

| #729 | Haim Saban | 3.2 | TV network, investments |

| #729 | Lynn Schusterman | 3.2 | oil & gas, investments |

| #729 | Mark Shoen | 3.2 | U-Haul |

| #729 | Meg Whitman | 3.2 | eBay |

| #766 | John Catsimatidis | 3.1 | oil, real estate |

| #766 | Do Won & Jin Sook Chang | 3.1 | fashion retail |

| #766 | Barry Diller | 3.1 | online media |

| #766 | Jack Dorsey | 3.1 | Twitter, Square |

| #766 | Allan Goldman | 3.1 | real estate |

| #766 | Jane Goldman | 3.1 | real estate |

| #766 | Amy Goldman Fowler | 3.1 | real estate |

| #766 | Diane Kemper | 3.1 | real estate |

| #766 | James Leprino | 3.1 | cheese |

| #766 | Richard Sands | 3.1 | Food & Beverage |

| #766 | Donald Trump | 3.1 | television, real estate |

| #766 | Romesh T. Wadhwani | 3.1 | software |

| #791 | Clifford Asness | 3 | Investment Management |

| #791 | Tom Benson | 3 | New Orleans Saints |

| #791 | Jim Breyer | 3 | venture capital |

| #791 | Valentin Gapontsev | 3 | lasers |

| #791 | Johnelle Hunt | 3 | trucking |

| #791 | John Middleton | 3 | tobacco |

| #791 | Jorge Perez | 3 | real estate |

| #791 | Jean (Gigi) Pritzker | 3 | hotels, investments |

| #791 | Michael Rubin | 3 | online retail |

| #791 | Robert Sands | 3 | Food & Beverage |

| #791 | Herb Simon | 3 | real estate |

| #791 | Don Vultaggio | 3 | AriZona Beverages |

| #822 | Chuck Bundrant | 2.9 | fishing |

| #822 | Gerald Ford | 2.9 | banking |

| #822 | Joseph Grendys | 2.9 | poultry processing |

| #822 | Randal Kirk | 2.9 | pharmaceuticals |

| #822 | Jeff Rothschild | 2.9 | |

| #822 | Thomas Siebel | 2.9 | business software |

| #822 | Paul Singer | 2.9 | hedge funds |

| #822 | Jon Stryker | 2.9 | medical equipment |

| #822 | Vincent Viola | 2.9 | electronic trading |

| #859 | William Conway, Jr. | 2.8 | private equity |

| #859 | Daniel D’Aniello | 2.8 | private equity |

| #859 | Jim Davis | 2.8 | staffing & recruiting |

| #859 | Doris Fisher | 2.8 | Gap |

| #859 | John Fisher | 2.8 | Gap |

| #859 | Kieu Hoang | 2.8 | medical products |

| #859 | H. Wayne Huizenga | 2.8 | investments |

| #859 | Osman Kibar | 2.8 | biotech |

| #859 | Penny Pritzker | 2.8 | hotels, investments |

| #859 | David Rubenstein | 2.8 | private equity |

| #859 | Mark Walter | 2.8 | finance |

| #859 | William Wrigley, Jr. | 2.8 | chewing gum |

| #859 | Mortimer Zuckerman | 2.8 | real estate, media |

| #887 | Ray Davis | 2.7 | pipelines |

| #887 | Edward DeBartolo, Jr. | 2.7 | shopping centers |

| #887 | Bennett Dorrance | 2.7 | Campbell Soup |

| #887 | Don Hankey | 2.7 | auto loans |

| #887 | Reed Hastings | 2.7 | Netflix |

| #887 | James Irsay | 2.7 | Indianapolis Colts |

| #887 | Bob Parsons | 2.7 | web hosting |

| #887 | Phil Ruffin | 2.7 | casinos, real estate |

| #887 | Howard Schultz | 2.7 | Starbucks |

| #887 | E. Joe Shoen | 2.7 | U-Haul |

| #887 | Frank VanderSloot | 2.7 | nutrition and wellness products |

| #887 | Ty Warner | 2.7 | real estate, plush toys |

| #887 | Oprah Winfrey | 2.7 | TV shows |

| #924 | David Bonderman | 2.6 | private equity |

| #924 | Phillip Frost | 2.6 | pharmaceuticals |

| #924 | B. Wayne Hughes | 2.6 | self-storage |

| #924 | Stephen Mandel, Jr. | 2.6 | hedge funds |

| #924 | Sean Parker | 2.6 | |

| #924 | Jay Paul | 2.6 | real estate |

| #924 | Patrick Ryan | 2.6 | insurance |

| #924 | Thomas Secunda | 2.6 | Bloomberg LP |

| #924 | Warren Stephens | 2.6 | investment banking |

| #924 | Glen Taylor | 2.6 | printing |

| #924 | Jerry Yang | 2.6 | Yahoo |

| #965 | Edward Bass | 2.5 | oil, investments |

| #965 | Lee Bass | 2.5 | oil, investments |

| #965 | Bert Beveridge | 2.5 | vodka |

| #965 | George Bishop | 2.5 | oil & gas |

| #965 | Norman Braman | 2.5 | art, car dealerships |

| #965 | Kenneth Feld | 2.5 | circus, live entertainment |

| #965 | Noam Gottesman | 2.5 | hedge funds |

| #965 | Jonathan Gray | 2.5 | investments |

| #965 | John Henry | 2.5 | sports |

| #965 | Aerin Lauder | 2.5 | cosmetics |

| #965 | Jane Lauder | 2.5 | cosmetics |

| #965 | Jeffrey Lorberbaum | 2.5 | flooring |

| #965 | Joe Mansueto | 2.5 | investment research |

| #965 | C. Dean Metropoulos | 2.5 | investments |

| #965 | Arturo Moreno | 2.5 | billboards, Anaheim Angels |

| #965 | Richard Peery | 2.5 | real estate |

| #965 | Larry Robbins | 2.5 | hedge funds |

| #965 | Charles Simonyi | 2.5 | Microsoft |

| #965 | Mark Stevens | 2.5 | venture capital |

| #965 | Peter Thiel | 2.5 | Facebook, Palantir |

| #965 | Elaine Wynn | 2.5 | casinos, hotels |

| #965 | Denise York | 2.5 | San Francisco 49ers |

| #965 | David Zalik | 2.5 | financial technology |

| #1020 | George Argyros | 2.4 | real estate, investments |

| #1020 | John Arrillaga | 2.4 | real estate |

| #1020 | Peter Buck | 2.4 | Subway sandwich shops |

| #1020 | Drayton McLane, Jr. | 2.4 | Walmart, logistics |

| #1020 | Daniel Pritzker | 2.4 | hotels, investments |

| #1020 | John Pritzker | 2.4 | hotels, investments |

| #1020 | Eric Smidt | 2.4 | hardware stores |

| #1020 | Alexander Spanos | 2.4 | real estate, Los Angeles Chargers |

| #1070 | David Gottesman | 2.3 | investments |

| #1070 | Bill Haslam | 2.3 | truck stops |

| #1070 | W. Herbert Hunt | 2.3 | oil |

| #1070 | Bradley Jacobs | 2.3 | logistics |

| #1070 | Brad Kelley | 2.3 | tobacco |

| #1070 | Vinod Khosla | 2.3 | venture capital |

| #1070 | Clayton Mathile | 2.3 | pet food |

| #1070 | J. Joe Ricketts | 2.3 | TD Ameritrade |

| #1070 | Dan Snyder | 2.3 | Washington Redskins |

| #1070 | John Tyson | 2.3 | food processing |

| #1103 | Ron Baron | 2.2 | money management |

| #1103 | Timothy Boyle | 2.2 | Columbia Sportswear |

| #1103 | Chase Coleman, III. | 2.2 | hedge fund |

| #1103 | Jim Coulter | 2.2 | private equity |

| #1103 | Frank Fertitta, III. | 2.2 | casinos, mixed martial arts |

| #1103 | Lorenzo Fertitta | 2.2 | casinos, mixed martial arts |

| #1103 | Ernest Garcia, II. | 2.2 | used cars |

| #1103 | Stanley Hubbard | 2.2 | DirecTV |

| #1103 | Thomas Lee | 2.2 | private equity |

| #1103 | Eric Lefkofsky | 2.2 | Groupon |

| #1103 | Phillip T. (Terry) Ragon | 2.2 | health IT |

| #1103 | Stewart Rahr | 2.2 | drug distribution |

| #1103 | T. Denny Sanford | 2.2 | banking, credit cards |

| #1103 | Julio Mario Santo Domingo, III. | 2.2 | beer |

| #1103 | Ted Turner | 2.2 | cable television |

| #1103 | William Young | 2.2 | plastics |

| #1157 | Leslie Alexander | 2.1 | sports team |

| #1157 | Todd Christopher | 2.1 | hair care products |

| #1157 | Gordon Getty | 2.1 | Getty Oil |

| #1157 | Alec Gores | 2.1 | private equity |

| #1157 | Catherine Lozick | 2.1 | valve manufacturing |

| #1157 | David Murdock | 2.1 | Dole, real estate |

| #1157 | H. Ross Perot, Jr. | 2.1 | real estate |

| #1157 | Tor Peterson | 2.1 | commodities |

| #1157 | Kavitark Ram Shriram | 2.1 | venture capital, Google |

| #1157 | David Walentas | 2.1 | real estate |

| #1157 | Ronald Wanek | 2.1 | furniture |

| #1215 | S. Daniel Abraham | 2 | Slim-Fast |

| #1215 | Ron Burkle | 2 | supermarkets, investments |

| #1215 | James Clark | 2 | Netscape, investments |

| #1215 | Christopher Cline | 2 | coal |

| #1215 | Alexandra Daitch | 2 | Cargill |

| #1215 | Glenn Dubin | 2 | hedge funds |

| #1215 | Robert Duggan | 2 | pharmaceuticals |

| #1215 | Thomas Hagen | 2 | insurance |

| #1215 | Bruce Karsh | 2 | private equity |

| #1215 | Henry Laufer | 2 | hedge funds |

| #1215 | Jeffrey Lurie | 2 | Philadelphia Eagles |

| #1215 | Sarah MacMillan | 2 | Cargill |

| #1215 | Howard Marks | 2 | private equity |

| #1215 | Jonathan Nelson | 2 | private equity |

| #1215 | Peter Peterson | 2 | investments |

| #1215 | Antony Ressler | 2 | finance |

| #1215 | Rodney Sacks | 2 | energy drinks |

| #1215 | Brian Sheth | 2 | investments |

| #1215 | Lucy Stitzer | 2 | Cargill |

| #1215 | Katherine Tanner | 2 | Cargill |

| #1215 | Amy Wyss | 2 | medical equipment |

| #1215 | Jon Yarbrough | 2 | video games |

| #1215 | Charles Zegar | 2 | Bloomberg LP |

| #1284 | James Dinan | 1.9 | hedge funds |

| #1284 | Bill Gross | 1.9 | investments |

| #1284 | Jeffrey Gundlach | 1.9 | investments |

| #1284 | Jennifer Pritzker | 1.9 | hotels, investments |

| #1284 | Alan Trefler | 1.9 | software |

| #1284 | Evan Williams | 1.9 | |

| #1339 | Nicolas Berggruen | 1.8 | investments |

| #1339 | James France | 1.8 | Nascar, racing |

| #1339 | Stewart Horejsi | 1.8 | Berkshire Hathaway |

| #1339 | Hamilton James | 1.8 | investments |

| #1339 | John Kapoor | 1.8 | healthcare |

| #1339 | William Lauder | 1.8 | Estee Lauder |

| #1339 | Linda Pritzker | 1.8 | hotels, investments |

| #1339 | Brian Roberts | 1.8 | Comcast |

| #1339 | William Stone | 1.8 | software |

| #1394 | Herbert Allen, Jr. | 1.7 | investment banking |

| #1394 | John Farber | 1.7 | chemicals |

| #1394 | Robert Fisher | 1.7 | Gap |

| #1394 | William Fisher | 1.7 | Gap |

| #1394 | Timothy Headington | 1.7 | oil & gas, investments |

| #1394 | Jim Justice, II. | 1.7 | coal |

| #1394 | William Koch | 1.7 | oil, investments |

| #1394 | Marc Lasry | 1.7 | hedge funds |

| #1394 | David Lichtenstein | 1.7 | real estate |

| #1394 | Craig McCaw | 1.7 | telecom |

| #1394 | Miguel McKelvey | 1.7 | WeWork |

| #1394 | Vincent McMahon | 1.7 | Entertainment |

| #1394 | Gary Michelson | 1.7 | medical patents |

| #1394 | Jerry Moyes | 1.7 | transportation |

| #1394 | Charles Munger | 1.7 | Berkshire Hathaway |

| #1394 | Nelson Peltz | 1.7 | investments |

| #1394 | Roger Penske | 1.7 | cars |

| #1394 | Henry Swieca | 1.7 | hedge funds |

| #1394 | Todd Wagner | 1.7 | online media |

| #1477 | Bill Austin | 1.6 | hearing aids |

| #1477 | Louis Bacon | 1.6 | hedge funds |

| #1477 | William Berkley | 1.6 | insurance |

| #1477 | Aneel Bhusri | 1.6 | business software |

| #1477 | O. Francis Biondi | 1.6 | hedge funds |

| #1477 | David Booth | 1.6 | mutual funds |

| #1477 | Steve Conine | 1.6 | online retail |

| #1477 | Stephen Feinberg | 1.6 | private equity |

| #1477 | Paul Foster | 1.6 | oil refining |

| #1477 | Mario Gabelli | 1.6 | money management |

| #1477 | Christopher Goldsbury | 1.6 | salsa |

| #1477 | Brian Higgins | 1.6 | hedge funds |

| #1477 | Michael Jordan | 1.6 | Charlotte Hornets, endorsements |

| #1477 | Edward Lampert | 1.6 | Sears |

| #1477 | Thai Lee | 1.6 | IT provider |

| #1477 | Billy Joe (Red) McCombs | 1.6 | real estate, oil, cars, sports |

| #1477 | Manuel Moroun | 1.6 | transportation |

| #1477 | Sheryl Sandberg | 1.6 | |

| #1477 | Niraj Shah | 1.6 | online retail |

| #1477 | Ben Silbermann | 1.6 | |

| #1477 | Thomas Steyer | 1.6 | hedge funds |

| #1477 | Charlotte Colket Weber | 1.6 | Campbell Soup |

| #1561 | Bill Alfond | 1.5 | shoes |

| #1561 | Susan Alfond | 1.5 | shoes |

| #1561 | Ted Alfond | 1.5 | shoes |

| #1561 | Carol Jenkins Barnett | 1.5 | Publix supermarkets |

| #1561 | Martha Ford | 1.5 | Ford Motor |

| #1561 | Richard Hayne | 1.5 | Urban Outfitters |

| #1561 | Seth Klarman | 1.5 | investments |

| #1561 | Eren Ozmen | 1.5 | aerospace |

| #1561 | Fatih Ozmen | 1.5 | aerospace |

| #1561 | Mark Pincus | 1.5 | online games |

| #1561 | Kevin Plank | 1.5 | Under Armour |

| #1561 | Nicholas Pritzker, II. | 1.5 | hotels, investments |

| #1561 | Fayez Sarofim | 1.5 | money management |

| #1561 | Kevin Systrom | 1.5 | |

| #1561 | Jim Thompson | 1.5 | logistics |

| #1561 | Jonathan Tisch | 1.5 | insurance, NFL team |

| #1561 | Kenneth Tuchman | 1.5 | outsourcing |

| #1650 | Herb Chambers | 1.4 | car dealerships |

| #1650 | John Edson | 1.4 | leisure craft |

| #1650 | David Einhorn | 1.4 | hedge funds |

| #1650 | Victor Fung | 1.4 | trading company |

| #1650 | Alan Gerry | 1.4 | cable television |

| #1650 | J. Tomilson Hill | 1.4 | investments |

| #1650 | George Joseph | 1.4 | insurance |

| #1650 | Michael Krasny | 1.4 | retail |

| #1650 | James Leininger | 1.4 | medical products |

| #1650 | Gary Magness | 1.4 | cable TV, investments |

| #1650 | Forrest Preston | 1.4 | health care |

| #1650 | Jerry Reinsdorf | 1.4 | sports teams |

| #1650 | Evgeny (Eugene) Shvidler | 1.4 | oil & gas, investments |

| #1650 | Peter Sperling | 1.4 | education |

| #1650 | Kenny Troutt | 1.4 | telecom |

| #1650 | Dan Wilks | 1.4 | natural gas |

| #1650 | Farris Wilks | 1.4 | natural gas |

| #1650 | Richard Yuengling, Jr. | 1.4 | beer |

| #1756 | Edmund Ansin | 1.3 | television |

| #1756 | Steve Case | 1.3 | AOL |

| #1756 | Darwin Deason | 1.3 | Xerox |

| #1756 | Jamie Dimon | 1.3 | banking |

| #1756 | Anne Gittinger | 1.3 | Nordstrom department stores |

| #1756 | Irwin Jacobs | 1.3 | semiconductors |

| #1756 | Mitchell Jacobson | 1.3 | industrial equipment |

| #1756 | Alexander Karp | 1.3 | software firm |

| #1756 | Sidney Kimmel | 1.3 | retail |

| #1756 | Rodney Lewis | 1.3 | natural gas |

| #1756 | Cargill MacMillan, III. | 1.3 | Cargill |

| #1756 | John MacMillan | 1.3 | Cargill |

| #1756 | Martha MacMillan | 1.3 | Cargill |

| #1756 | William MacMillan | 1.3 | Cargill |

| #1756 | Craig Newmark | 1.3 | Craigslist |

| #1756 | Bruce Nordstrom | 1.3 | Nordstrom department stores |

| #1756 | Alexander Rovt | 1.3 | fertilizer, real estate |

| #1756 | Leonard Schleifer | 1.3 | pharmaceuticals |

| #1756 | Wilma Tisch | 1.3 | diversified |

| #1756 | Jayshree Ullal | 1.3 | computer networking |

| #1756 | Stephen Winn | 1.3 | real estate services |

| #1867 | Marc Andreessen | 1.2 | venture capital investing |

| #1867 | Thomas Bailey | 1.2 | money management |

| #1867 | Charles Brandes | 1.2 | money management |

| #1867 | Henry Engelhardt | 1.2 | insurance |

| #1867 | Donald Foss | 1.2 | auto loans |

| #1867 | Robert Friedland | 1.2 | mining |

| #1867 | Donald Friese | 1.2 | manufacturing |

| #1867 | Ryan Graves | 1.2 | uber |

| #1867 | B. Wayne Hughes, Jr. | 1.2 | storage facilities |

| #1867 | Thomas James | 1.2 | finance |

| #1867 | Gail Miller | 1.2 | basketball, car dealers |

| #1867 | Michael Price | 1.2 | investments |

| #1867 | Lynsi Snyder | 1.2 | In-N-Out Burger |

| #1867 | Thomas Tull | 1.2 | movies |

| #1867 | Alfred West, Jr. | 1.2 | money management |

| #1999 | William Ackman | 1.1 | hedge funds |

| #1999 | J. Hyatt Brown | 1.1 | insurance |

| #1999 | Bharat Desai | 1.1 | IT consulting |

| #1999 | Joseph Edelman | 1.1 | hedge funds |

| #1999 | Paul Fireman | 1.1 | Reebok |

| #1999 | J. Christopher Flowers | 1.1 | investments |

| #1999 | Drew Houston | 1.1 | cloud storage service |

| #1999 | Richard Kayne | 1.1 | investments |

| #1999 | Isaac Larian | 1.1 | toys |

| #1999 | Frank Laukien | 1.1 | scientific equipment |

| #1999 | Nancy Lerner | 1.1 | banking, credit cards |

| #1999 | Norma Lerner | 1.1 | banking |

| #1999 | Randolph Lerner | 1.1 | banking, credit cards |

| #1999 | William Macaulay | 1.1 | energy investments |

| #1999 | John Martin | 1.1 | pharmaceuticals |

| #1999 | Andrea Reimann-Ciardelli | 1.1 | consumer goods |

| #1999 | Chris Sacca | 1.1 | venture capital investing |

| #1999 | Michael Steinhardt | 1.1 | hedge funds |

| #1999 | Laurie Tisch | 1.1 | insurance, NFL team |

| #1999 | Steven Tisch | 1.1 | insurance |

| #1999 | James Truchard | 1.1 | software |

| 568 people | Billions total in wealth | 3079.7 | |

References

- Jensen, M.C.; Murphy, K.J. CEO Incentives—It’s Not How Much You Pay, But How. Harvard Business Review. 1 May 1990. Available online: https://hbr.org/1990/05/ceo-incentives-its-not-how-much-you-pay-but-how (accessed on 8 November 2018).

- Hesket, J. Is There an “Efficient Market” in CEO Compensation? 2005. Available online: http://hbswk.hbs.edu/item/is-there-an-efficient-market-in-ceo-compensation (accessed on 8 November 2018).

- Hembree, D. CEO Pay Skyrockets to 361 Times That of the Average Worker. Forbes. 2018. Available online: https://www.forbes.com/sites/dianahembree/2018/05/22/ceo-pay-skyrockets-to-361-times-that-of-the-average-worker/#16dcf48d776d (accessed on 8 November 2018).

- Lewis, A. Fraud, Failure and Bankruptcy Pay Well for CEOs. Markewatch, 2013. Available online: https://www.marketwatch.com/story/fraud-failure-and-bankruptcy-pay-well-for-ceos-2013-08-28 (accessed on 8 November 2018).

- Quadrini, V.; Rıos-Rull, J.V. Dimensions of inequality: Facts on the US distribution of earnings, income and wealth. Fed. Reserv. Bank Minneap. Q. Rev. 1997, 21, 3–21. [Google Scholar]

- Rodriguez, S.B.; Rios-Rull, J.V.; Diaz-Gimenez, J.; Quadrini, V. Updated facts on the US distributions of earnings, income, and wealth. Fed. Reserv. Bank Minneap. Q. Rev. 2002, 26, 2–36. [Google Scholar]

- Atkinson, A.B.; Bourguignon, F. (Eds.) Handbook of Income Distribution; Elsevier: Amsterdam, The Netherlands, 2014; Volume 2. [Google Scholar]

- Credit Suisse. U.S. Wealth Distribution in 2017 | Statistic. 2018. Available online: https://www.statista.com/statistics/203961/wealth-distribution-for-the-us/ (accessed on 8 November 2018).

- Becker, G.S.; Tomes, N. An equilibrium theory of the distribution of income and intergenerational mobility. J. Political Econ. 1979, 87, 1153–1189. [Google Scholar] [CrossRef]

- Becker, G.S.; Tomes, N. Human capital and the rise and fall of families. J. Labor Econ. 1986, 4 Pt 2, S1–S39. [Google Scholar] [CrossRef]

- Kotlikoff, L.J.; Summers, L.H. The role of intergenerational transfers in aggregate capital accumulation. J. Political Econ. 1981, 89, 706–732. [Google Scholar] [CrossRef]

- Mulligan, C.B. Parental Priorities and Economic Inequality; University of Chicago Press: Chicago, IL, USA, 1997. [Google Scholar]

- Hurd, M.D.; Smith, J.P. Anticipated and actual bequests. In Themes in the Economics of Aging; University of Chicago Press: Chicago, IL, USA, 2001; pp. 357–392. [Google Scholar]

- Frank, R. Where the Rich Make Their Income. CNBC. Available online: https://www.cnbc.com/2015/04/09/where-the-rich-make-their-income.html (accessed on 16 November 2018).

- Steverman, B. Why American Workers Pay Twice as Much in Taxes as Wealthy Investors. Bloomberg. 12 September 2017. Available online: https://www.bloomberg.com/news/features/2017-09-12/why-american-workers-pay-twice-as-much-in-taxes-as-wealthy-investors (accessed on 16 November 2018).

- Ingraham, C. As the Rich Become Super-Rich, they pay lower taxes. For real. The Washington Post. 4 June 2015. Available online: https://www.washingtonpost.com/news/wonk/wp/2015/06/04/as-the-rich-become-super-rich-they-pay-lower-taxes-for-real/ (accessed on 16 November 2018).

- Dabla-Norris, M.E.; Kochhar, M.K.; Suphaphiphat, M.N.; Ricka, M.F.; Tsounta, E. Causes and Consequences of Income Inequality: A Global Perspective; International Monetary Fund: Washington, DC, USA, 2015; ISBN 978-1-5135-4437-3. [Google Scholar]

- Stiglitz, J.E. The Price of Inequality: How Today’s Divided Society Endangers Our Future; W. W. Norton & Company: New York, NY, USA, 2012; ISBN 978-0-393-08869-4. [Google Scholar]

- Ostry, M.J.D.; Berg, M.A.; Tsangarides, M.C.G. Redistribution, Inequality, and Growth; International Monetary Fund: Washington, DC, USA, 2014; ISBN 978-1-4843-9704-6. [Google Scholar]

- Berg, A.; Ostry, J.D.; Zettelmeyer, J. What makes growth sustained? J. Dev. Econ. 2012, 98, 149–166. [Google Scholar] [CrossRef]

- Cingano, F. Trends in Income Inequality and its Impact on Economic Growth. OECD iLibrary 2014. [Google Scholar] [CrossRef]

- Aghion, P.; Caroli, E.; Garcia-Penalosa, C. Inequality and Economic Growth: The Perspective of the New Growth Theories. J. Econ. Lit. 1999, 37, 1615–1660. [Google Scholar] [CrossRef]

- Galor, O.; Moav, O. From Physical to Human Capital Accumulation: Inequality and the Process of Development. Rev. Econ. Stud. 2004, 71, 1001–1026. [Google Scholar] [CrossRef]

- Corak, M. Income Inequality, Equality of Opportunity, and Intergenerational Mobility. J. Econ. Perspect. 2013, 27, 79–102. [Google Scholar] [CrossRef]

- Lichbach, M.I. An Evaluation of “Does Economic Inequality Breed Political Conflict?” Studies. World Politics 1989, 41, 431–470. [Google Scholar] [CrossRef]

- Claessens, S.; Perotti, E. Finance and inequality: Channels and evidence. J. Comp. Econ. 2007, 35, 748–773. [Google Scholar] [CrossRef]

- Bourguignon, F.; Dessus, S. Equity and development: Political economy considerations. In No Growth without Equity? Walton, M.L., Ed.; Equity and Development; The World Bank: Santiago, Chile, 2009; ISBN 978-0-8213-7767-3. [Google Scholar]

- Rajan, R.G. Fault Lines: How Hidden Fractures Still Threaten the World Economy; Princeton University Press: Princeton, NJ, USA, 2011; ISBN 978-1-4008-3980-3. [Google Scholar]

- Acemoglu, D.; Naidu, S.; Restrepo, P.; Robinson, J.A. Democracy, public policy and inequality. Am. Political Sci. Rev. 2012, 106, 495–516. [Google Scholar]

- Corley, T.C. Rich Habits—The Daily Success Habits of Wealthy Individuals; Langdon Street Press: Minneapolis, MN, USA, 2010; ISBN 978-1-934938-93-5. [Google Scholar]

- Pachauri, R.K.; Allen, M.R.; Barros, V.R.; Broome, J.; Cramer, W.; Christ, R.; Church, J.A.; Clarke, L.; Dahe, Q.; Dasgupta, P.; et al. Climate Change 2014: Synthesis Report. Contribution of Working Groups I, II and III to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change; Pachauri, R.K., Meyer, L., Eds.; IPCC: Geneva, Switzerland, 2014; ISBN 978-92-9169-143-2. [Google Scholar]

- U.S. EPA. Greenhouse Gas Inventory Data Explorer. Available online: https://www3.epa.gov/climatechange/ghgemissions/inventoryexplorer/#electricitygeneration/allgas/source/all (accessed on 13 March 2019).

- U.S. Energy Information Administration. What Is U.S. Electricity Generation by Energy Source?—FAQ—U.S. Energy Information Administration (EIA). Available online: https://www.eia.gov/tools/faqs/faq.php?id=427&t=3 (accessed on 18 December 2018).

- ArcGIS. States_Basic. 2012. Available online: https://www.arcgis.com/home/item.html?id=f7f805eb65eb4ab787a0a3e1116ca7e5 (accessed on 11 January 2019).

- NREL. Geospatial Data Science. 2012. Available online: https://www.nrel.gov/gis/data-solar.html (accessed on 11 January 2019).

- U.S. Census Bureau. National Population totals and Components of Change: 2010–2018. 2018. Available online: https://www.census.gov/data/tables/time-series/demo/popest/2010s-national-total.html#par_textimage (accessed on 22 January 2019).

- The World’s Billionaires. Forbes. Available online: https://www.forbes.com/billionaires/list/ (accessed on 12 October 2018).

- U.S. Energy Information Administration (EIA)—Total Energy Monthly Data. Available online: https://www.eia.gov/totalenergy/data/monthly/ (accessed on 18 December 2018).

- NREL Report Shows Utility-Scale Solar PV System Cost Fell Nearly 30% Last Year | NREL | News | NREL. Available online: https://www.nrel.gov/news/press/2017/nrel-report-utility-scale-solar-pv-system-cost-fell-last-year.html (accessed on 18 December 2018).

- Branker, K.; Pathak, M.J.M.; Pearce, J.M. A review of solar photovoltaic levelized cost of electricity. Renew. Sustain. Energy Rev. 2011, 15, 4470–4482. [Google Scholar] [CrossRef]

- Albrecht, J. The future role of photovoltaics: A learning curve versus portfolio perspective. Energy Policy 2007, 35, 2296–2304. [Google Scholar] [CrossRef]

- Yu, C.F.; van Sark, W.G.J.H.M.; Alsema, E.A. Unraveling the photovoltaic technology learning curve by incorporation of input price changes and scale effects. Renew. Sustain. Energy Rev. 2011, 15, 324–337. [Google Scholar] [CrossRef]

- Hong, S.; Chung, Y.; Woo, C. Scenario analysis for estimating the learning rate of photovoltaic power generation based on learning curve theory in South Korea. Energy 2015, 79, 80–89. [Google Scholar] [CrossRef]

- Trappey, A.J.C.; Trappey, C.V.; Tan, H.; Liu, P.H.Y.; Li, S.-J.; Lin, L.-C. The determinants of photovoltaic system costs: An evaluation using a hierarchical learning curve model. J. Clean. Prod. 2016, 112, 1709–1716. [Google Scholar] [CrossRef]

- Mauleón, I. Photovoltaic learning rate estimation: Issues and implications. Renew. Sustain. Energy Rev. 2016, 65, 507–524. [Google Scholar] [CrossRef]

- Feldman, D.; Barbose, G.; Margolis, R.; Wiser, R.; Darghout, N.; Goodrich, A. Photovoltaic (PV) Pricing Trends: Historical, Recent, and Near-Term Projections; Technical Report No. DOE/GO-102012-3839; Lawrence Berkeley National Lab.: Berkeley, CA, USA, 2012.

- Barbose, G.L.; Darghouth, N.R.; Millstein, D.; LaCommare, K.; DiSanti, N.; Widiss, R. Tracking the Sun 10: The Installed Price of Residential and Non-Residential Photovoltaic Systems in the United States. Available online: https://emp.lbl.gov/publications/tracking-sun-10-installed-price (accessed on 25 July 2018).

- PVinsights. Available online: http://pvinsights.com/ (accessed on 18 January 2019).

- Modanese, C.; Laine, H.S.; Pasanen, T.P.; Savin, H.; Pearce, J.M. Economic Advantages of Dry-Etched Black Silicon in Passivated Emitter Rear Cell (PERC) Photovoltaic Manufacturing. Energies 2018, 11, 2337. [Google Scholar] [CrossRef]

- Reuters. Solar Costs to Fall Further, Powering Global Demand-Irena. Available online: https://www.reuters.com/article/singapore-energy-solar/solar-costs-to-fall-further-powering-global-demand-irena-idUSL4N1MY2F8 (accessed on 5 March 2018).

- Earth’s CO2 Home Page. Available online: https://www.co2.earth/ (accessed on 21 January 2019).

- IPCC. Special Report:Global Warming of 1.5 °C. Available online: https://www.ipcc.ch/sr15/ (accessed on 21 January 2019).

- Moss, R.H.; Edmonds, J.A.; Hibbard, K.A.; Manning, M.R.; Rose, S.K.; van Vuuren, D.P.; Carter, T.R.; Emori, S.; Kainuma, M.; Kram, T.; et al. The next generation of scenarios for climate change research and assessment. Nature 2010, 463, 747–756. [Google Scholar] [CrossRef] [PubMed]

- Stern Review: The Economics of Climate Change (Miscellaneous) | ETDEWEB. Available online: https://www.osti.gov/etdeweb/biblio/20838308 (accessed on 18 January 2019).

- Dhainaut, J.-F.; Claessens, Y.-E.; Ginsburg, C.; Riou, B. Unprecedented heat-related deaths during the 2003 heat wave in Paris: Consequences on emergency departments. Crit. Care 2003, 8, 1. [Google Scholar] [CrossRef] [PubMed]

- Poumadère, M.; Mays, C.; Mer, S.L.; Blong, R. The 2003 Heat Wave in France: Dangerous Climate Change Here and Now. Risk Anal. 2005, 25, 1483–1494. [Google Scholar] [CrossRef] [PubMed]

- Fouillet, A.; Rey, G.; Laurent, F.; Pavillon, G.; Bellec, S.; Guihenneuc-Jouyaux, C.; Clavel, J.; Jougla, E.; Hémon, D. Excess mortality related to the August 2003 heat wave in France. Int. Arch. Occup. Environ. Health 2006, 80, 16–24. [Google Scholar] [CrossRef]

- D’Amato, G.; Cecchi, L. Effects of climate change on environmental factors in respiratory allergic diseases. Clin. Exp. Allergy 2008, 38, 1264–1274. [Google Scholar] [CrossRef]

- Challinor, A.J.; Simelton, E.S.; Fraser, E.D.G.; Hemming, D.; Collins, M. Increased crop failure due to climate change: Assessing adaptation options using models and socio-economic data for wheat in China. Environ. Res. Lett. 2010, 5, 034012. [Google Scholar] [CrossRef]

- Jones, P.G.; Thornton, P.K. The potential impacts of climate change on maize production in Africa and Latin America in 2055. Glob. Environ. Chang. 2003, 13, 51–59. [Google Scholar] [CrossRef]

- Parry, M.L.; Rosenzweig, C.; Iglesias, A.; Livermore, M.; Fischer, G. Effects of climate change on global food production under SRES emissions and socio-economic scenarios. Glob. Environ. Chang. 2004, 14, 53–67. [Google Scholar] [CrossRef]

- Parry, M.; Rosenzweig, C.; Livermore, M. Climate change, global food supply and risk of hunger. Philos. Trans. R. Soc. B Biol. Sci. 2005, 360, 2125–2138. [Google Scholar] [CrossRef] [PubMed]

- Schmidhuber, J.; Tubiello, F.N. Global food security under climate change. Proc. Natl. Acad. Sci. USA 2007, 104, 19703–19708. [Google Scholar] [CrossRef] [PubMed]

- Klinenberg, E. Are you ready for the next disaster? New York Times Magazine, 6 June 2008. [Google Scholar]

- Vine, E. Adaptation of California’s electricity sector to climate change. Clim. Chang. 2012, 111, 75–99. [Google Scholar] [CrossRef]

- Moorhead, K.K.; Brinson, M.M. Response of Wetlands to Rising Sea Level in the Lower Caostal Plain of North Carolina. Ecol. Appl. 1995, 5, 261–271. [Google Scholar] [CrossRef]

- Frihy, O.E. The Nile delta-Alexandria coast: Vulnerability to sea-level rise, consequences and adaptation. Mitig. Adapt. Strateg. Glob. Chang. 2003, 8, 115–138. [Google Scholar] [CrossRef]

- Nicholls, R.J.; Hoozemans, F.M.J.; Marchand, M. Increasing flood risk and wetland losses due to global sea-level rise: Regional and global analyses. Glob. Environ. Chang. 1999, 9, S69–S87. [Google Scholar] [CrossRef]

- Bobba, A.G. Numerical modelling of salt-water intrusion due to human activities and sea-level change in the Godavari Delta, India. Hydrol. Sci. J. 2002, 47, S67–S80. [Google Scholar] [CrossRef]

- Desantis, L.R.G.; Bhotika, S.; Williams, K.; Putz, F.E. Sea-level rise and drought interactions accelerate forest decline on the Gulf Coast of Florida, USA. Glob. Chang. Biol. 2007, 13, 2349–2360. [Google Scholar] [CrossRef]

- Dale, V.H.; Joyce, L.A.; McNulty, S.; Neilson, R.P.; Ayres, M.P.; Flannigan, M.D.; Hanson, P.J.; Irland, L.C.; Lugo, A.E.; Peterson, C.J.; et al. Climate Change and Forest DisturbancesClimate change can affect forests by altering the frequency, intensity, duration, and timing of fire, drought, introduced species, insect and pathogen outbreaks, hurricanes, windstorms, ice storms, or landslides. BioScience 2001, 51, 723–734. [Google Scholar] [CrossRef]

- Flannigan, M.D.; Stocks, B.J.; Wotton, B.M. Climate change and forest fires. Sci. Total Environ. 2000, 262, 221–229. [Google Scholar] [CrossRef]

- Allen, C.D.; Macalady, A.K.; Chenchouni, H.; Bachelet, D.; McDowell, N.; Vennetier, M.; Kitzberger, T.; Rigling, A.; Breshears, D.D.; Hogg, E.H. (Ted); et al. A global overview of drought and heat-induced tree mortality reveals emerging climate change risks for forests. For. Ecol. Manag. 2010, 259, 660–684. [Google Scholar] [CrossRef]

- Carnicer, J.; Coll, M.; Ninyerola, M.; Pons, X.; Sánchez, G.; Peñuelas, J. Widespread crown condition decline, food web disruption, and amplified tree mortality with increased climate change-type drought. Proc. Natl. Acad. Sci. USA 2011, 108, 1474–1478. [Google Scholar] [CrossRef] [PubMed]

- Dai, A. Increasing drought under global warming in observations and models. Nat. Clim. Chang. 2013, 3, 52–58. [Google Scholar] [CrossRef]

- Amiro, B.D.; Stocks, B.J.; Alexander, M.E.; Flannigan, M.D.; Wotton, B.M. Fire, climate change, carbon and fuel management in the Canadian boreal forest. Int. J. Wildland Fire 2001, 10, 405–413. [Google Scholar] [CrossRef]

- Flannigan, M.; Stocks, B.; Turetsky, M.; Wotton, M. Impacts of climate change on fire activity and fire management in the circumboreal forest. Glob. Chang. Biol. 2009, 15, 549–560. [Google Scholar] [CrossRef]

- UN News Centre. 2014. Available online: http://www.un.org/apps/news/story.asp?NewsID=47047#.VDLw1BaaXGU (accessed on 6 October 2014).

- IPCC Fifth Assessment Report. 2013. Available online: http://www.ipcc.ch/publications_and_data/publications_and_data_reports.shtml (accessed on 29 September 2014).

- What Are the 10 Biggest Global Challenges? WE Forum. Available online: https://www.weforum.org/agenda/2016/01/what-are-the-10-biggest-global-challenges/ (accessed on 21 January 2019).

- Friedman, Z. Why Bill Gates, Jeff Bezos, Mark Zuckerberg & Richard Branson Are Investing In These 2 Startups. Available online: https://www.forbes.com/sites/zackfriedman/2018/06/14/bill-gates-jeff-bezos-mark-zuckerberg-branson-startups/ (accessed on 21 January 2019).

- Climate Change and the 75% Problem | Bill Gates. Available online: https://www.gatesnotes.com/Energy/My-plan-for-fighting-climate-change (accessed on 21 January 2019).