1. Introduction

It is well known that a set of orthogonal polynomials can be associated to a density function with existing moments of all order. This clears the way for the tailoring of the shape of a given distribution from “inside” through a polynomial shape-adapter, built on the orthogonal polynomials engendered by the same distribution (e.g., [

1,

2,

3,

4]).

So far, this method—which can be viewed as an inheritance of the Gram–Charlier expansion—has proved effective when applied to distributions to account for possibly severe kurtosis and skewness (e.g., [

5,

6]). In this paper, we gain further insight into the matter and work out a similar orthogonal-polynomial-based approach to increasing the values of the moments—in particular, the fourth—within a multivariate spherical framework. Spherical distributions—a particular class of elliptical distributions [

7,

8] whose contours of equal density have spherical shapes—prove effective in several applications, such as portfolio theory and the capital asset market (e.g., [

9,

10]). However, it sometimes happens that the kurtosis of such a distribution is lower than required, thus imposing the need for a reshaping to duly fit in with empirical evidence.

After running through the procedure to derive a spherical distribution via a density generator, the Gram–Charlier-like expansion is duly specified, and the involved orthogonal polynomial derived in terms of the moments of the so-called modular variable (see

Appendix A).

The paper proceeds as follows.

Section 2 sets the groundwork by providing a determinantal representation of orthogonal polynomials in terms of closed-form expressions of the moments of the weight function, paving the way for the notion of Gram–Charlier-like expansion.

Section 3 addresses the issue of the density reshaping problem via orthogonal polynomials in a multidimensional framework on a spherical distribution argument.

Section 4, focusing on kurtosis behavior, deals with the orthogonal-polynomial approach to density reshaping by investigating a few selected spherical laws—namely, the Gaussian, the logistic, and the hyperbolic secant ones, their Gram–Charlier-like expansions, and the related moments.

Section 5 presents some concluding remarks. Finally an appendix, devoted to spherical laws, completes the paper.

2. Orthogonal Polynomials and Related Gram–Charlier-Like Expansions

Recently, Zoia et al. have shown how to modify the moments of a univariate distribution f(.) by making use of Gram–Charlier-like expansions based on orthogonal polynomials associated to f(.) [

3,

6]. In this regard, the monic orthogonal polynomial of degree

h, with density f(x) as weight function, is defined in terms of the moments of f(x) as follows [

11]:

where

and

denotes the (

i,

j) entry of the adjoint of the Hankel moment matrix

, noting that

. In the following, we will assume to operate with even density functions of standardized variables. Odd moments vanish accordingly, and orthogonal polynomials

are even functions if h is even, and odd otherwise.

As already remarked, the moments of a density function

f(.) can be modified to some extent by moving to a properly chosen Gram–Charlier-like expansion

built on its own orthogonal polynomials. In particular, consider an expansion specified as follows

where

Here

j is even,

> 0 subject to

being positive, and

and

are given by

respectively. From the properties of the orthogonal polynomials, it follows that the moments

up to the

j-th order of

are the same as the moments

of the parent density

f(.). That is,

More generally, we prove the following

Theorem 1. The moment of order 2h of is an algebraic function of the even moments of f(x) of order up to 2h + j, which varies linearly with β, that is Proof. The proof follows in a straightforward manner from the representation (8) of ; bearing in mind (9).

In light of Theorem 1, factor (7) reshapes the density f(x) by modifying its j-th moment to the extent of β, and in so doing, it operates as a polynomial shape adapter.

If we were interested in modifying more than one moment of the parent density f(x), a similar argument could be advanced by making use of a properly designed polynomial shape adapter depending upon the orthogonal polynomials corresponding to the moments to be adjusted. Further, this polynomial approach to density reshaping can be given a multivariate formulation from a spherical distribution standpoint, as we will show here below.

3. Multivariate Extensions via Spherical Distributions

In what follows, the issue of density reshaping based on orthogonal polynomials will be extended to n-dimensional spherical distributions (see

Appendix A). As a premise, in order to single out the polynomial shape adapter for reshaping a spherical density, let us recall that the density function

of a spherical variable can be conveniently expressed in terms of the density

of its modular variable

R (see

Appendix A) as follows

where

with

denoting the Euler Gamma function.

As a by-product, the moments of

R determine the moments of the spherical variable (see [

8,

12]). It follows that a change in an even moment of the modular variable will affect the even moments of the parent spherical one.

Now, let us reshape

by means of a

j-th degree polynomial

where

is defined as in (8), and let

be the resulting density. According to (12), the density of the reshaped spherical vector is given by

The above formula provides the Gram–Charlier-like expansion of the spherical density obtained via the polynomial adapter (14) in the argument , where .

In the following, we will focus on a polynomial correction hinging on the

4-th degree orthogonal polynomial, which is intended to reshape the parent distribution

so as to meet kurtosis requirements to the required extent. By setting

j = 4, the polynomial adapter (14) becomes

and gives rise to a Gram–Charlier-like expansion tailored to embody certain facts, such as fat tails and accentuated peakedness peculiar to financial data, whose manifestation is a possibly severe kurtosis.

Following [

8], the kurtosis

K of an

n-dimensional spherical variable is defined as follows

and can be read as

times the kurtosis of a symmetric zero mean univariate variable

Z such that Z=

with

as density.

According to (18), an increase in kurtosis of a spherical variable can be obtained by pushing up the fourth moment of its modular variable. This can be done by reshaping

R via the fourth degree polynomial (17). The parameters

,

j = 0,1,2, defined in accordance with (9), can be computed as follows:

in terms of the moments

of the modular variable

R.

In this regard, we have the following:

Theorem 2. The moments of order j, denoted with , of the modular variable R are given bywhere is the Pochhammer symbol, is defined as follows And denotes the density generator of the parent spherical variable (see Appendix A). Proof. According to [

8], the

j-th moment of the modular variable

R is given by

which, taking into account (21), can be written as in (20).

Assuming this, the Gram–Charlier-like expansion of a spherical distribution

designed to fit in with the empirical evidence of possibly severe kurtosis is thus given by

where

is as in (17) with coefficients given by (19), and

> 0 subject to

being positive. In this connection, we have the following

Theorem 3. The Gram–Charlier-like expansion (23) is positive if satisfies the following inequalities Proof. The function

is positive provided the polynomial

is also. Now, some computation proves that

where the right-hand side of the above formula is a negative quantity. It follows that

as long as

satisfies (24).

4. Polynomial Expansions of Some Spherical Distributions

In this section, the fourth order polynomial shape adapters for selected n-dimensional spherical variables are devised. The distributions considered are the Gaussian, the logistic, and the hyperbolic secant. These distributions, once polynomially adjusted, prove to be effective in handling series with different degrees of excess kurtosis. Before stating the theorems we are primarily interested in, we need the following

Lemma 1. The moments of the modular variable R, needed to determine the parameters , j = 0,1,2, of the shape adapter , take the closed forms here below, for the spherical Gaussian, logistic, and hyperbolic secant laws, respectively.- (i)

- (ii)

- (iii)

Spherical hyperbolic secant (HS),

Hereandwith and denoting Riemann and the Hurwitz zeta functions, respectively. Proof. Formulas (27)–(29) ensue from (20) upon noting that

, defined as in (21), becomes

for the spherical Gaussian in light of (A8).

This same parameter

becomes

for the spherical logistic in light of (A9).

Finally,

becomes

for the hyperbolic secant in light of (A10).

Theorem 4. The Gram–Charlier-like expansions of the spherical Gaussian, logistic, and hyperbolic secant densities are, respectively, given bywhere for each distribution, the coefficients of the polynomial are evaluated according to (19) from the moments of the corresponding modular variable as per (27)–(29). The expansions (35)–(37) are positive subject to (24). Proof. The proofs of (35)–(37) follow from (23) by making use of Lemma 1 for the evaluation of the coefficients of the polynomial

and Theorem A2 in

Appendix A for the spherical representation of the distributions in hand.

The analysis of the kurtosis level attainable by a spherical Gram–Charlier-like expansion as compared with that of the parent spherical law is of major interest, not only from an analytical standpoint but also for operational purposes. Based on this, we can state the following

Theorem 5. The increase in kurtosis , achievable when moving from a spherical density to its Gram–Charlier-like expansion, iswhere β is a parameter subject to (24). Proof. Formula (38) can be easily established by noting that (bearing in mind Theorem 1) the effect of the polynomial shape adapter is to increase the fourth moment of

R by a quantity equal to

β. Hence, it follows from (18) that the increase in kurtosis of the Gram–Charlier-like expansion is equal to

which, by making use of (20), is the same as (38).

Looking at (38), we can see that the increase in kurtosis depends on both β and n via the coefficient . The following charts shed some light on the behavior of kurtosis on either β and n, or both, as they vary.

Figure 1 shows

as a function of β for the three aforementioned Gram–Charlier-like expansions for different values of the dimension

n. For each expansion,

attains its maximum value in correspondence with the upper bound

of

as per formula (24). Looking at the graphs in

Figure 1, we see that, as for the univariate case, the higher the fourth moment of the modular variable

R, the higher the upper bound of β and of

in turn.

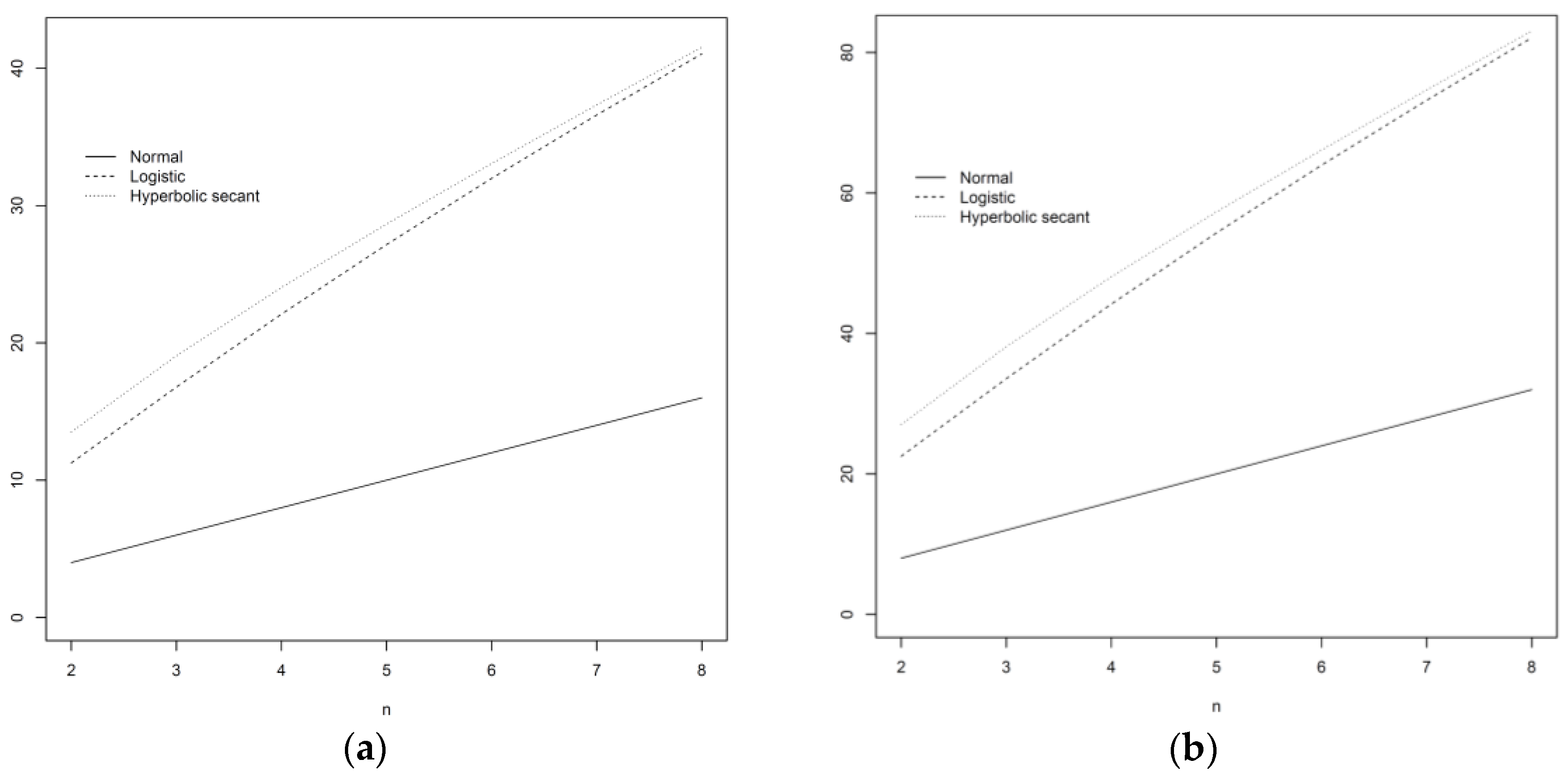

Figure 2 shows

for the three Gram–Charlier-like expansions, as a function of

n in correspondence to the two values of

, the upper bound

and half of the same (

Figure 2a,b).

Figure 3 shows the kurtosis ranges of the Gram–Charlier expansions for increasing values of the dimension

n.

5. Concluding Remarks

In this paper, the orthogonal-polynomial approach to density reshaping is developed in a multivariate framework on a spherical distribution argument. This paper extends recent insights (see [

3,

5,

6]) on the issue of tailoring distributions in order to account for over-kurtosis. Starting from a given spherical distribution, the orthogonal polynomials of its related modular variable are provided and used to design the intended distribution shape adapter. This allows us to specify a Gram–Charlier-like expansion whose moments can be tailored to match empirical evidence requirements. The paper basically focuses on the fourth moment, and the approach provides expansions of the spherical Gaussian, logistic, and hyperbolic secant laws, which are well-equipped to handle possible severe kurtosis occurring at a multivariate level.

{kind=link}

{kind=link}

{kind=link}