1. Introduction

In response to the wave of global urbanization, increasing attention has recently been given to issues associated with urbanization development. As the most populous country in the world, China’s urbanization model has significant research value. On the one hand, China’s urbanization process has lagged behind other economies at the same level of development [

1]. In 2021, the China Development Planning and Reform Commission issued the National New Urbanization Plan 2021–2035, emphasizing that, “by 2025, the urbanization rate of the permanent resident population will increase steadily, the urbanization rate of the household registration population will be significantly increased, and the gap between the urbanization rate of the household registration population and the urbanization rate of the resident population will be significantly narrowed” [

2]. The urbanization lag has long been a critical challenge for the Chinese government. On the other hand, China’s urbanization rate has increased by 14.21% in the past decade, a relatively fast growth rate; the rapid increase in land use and land cover have led to more environmental pollution, ecosystem degradation, and biodiversity loss [

3,

4]. Rapid urbanization increases the likelihood of urban heat island formation, which endangers the physical and mental health of residents [

5]. In addition, due to the rapid urbanization development in China, some provinces have experienced “urbanization without growth,” which is similar to excessive urbanization in many developing countries [

6]. In addition, China’s urbanization has produced clear regional differences, with the urbanization level in the eastern region significantly higher than that in the central and western regions. China’s urbanization development is unstable, unbalanced, and incomplete. Promoting high−quality urbanization both scientifically and comprehensively, on the basis of the sustainable development theory, is an important issue faced by the Chinese government.

In terms of economic growth, as the world’s second−largest economy, the Chinese government also attaches significant importance to government venture capital. In 2005, the State Development and Reform Commission, the Ministry of Science and Technology, the Ministry of Finance, as well as other ministries and commissions, issued interim measures for the “Management of Venture Capital Enterprises,” which states that, “the state and local governments can set up government venture capital to support the establishment and development of venture capital enterprises through equity participation and financing guarantees.” In 2008, the General Office of the State Council issued the “Guidance on the Establishment and Operation of Government Venture Capital,” formulated by the Development and Reform Commission and other departments and made provisions on the establishment and operation of government venture capital.

Through an empirical study of Chinese provinces, Tao Hong and other scholars found that urbanization, as promoted by the Chinese local government, is not suitable for the local social, cultural, and economic environment and has produced a quasi−“urbanization without growth” [

6]. Government venture capital, as a measure of the economic development stage, plays a significant role in promoting regional economic development and enterprise innovation. Therefore, this study explores government venture capital to determine an effective government intervention policy in promoting high−quality urbanization development.

As a policy tool, government venture capital is an intervention on the supply side of capital to prevent market failure [

7]. The Chinese government venture capital may be used to invest in industries with strong externalities, such as public goods, and thus aid in urbanization development [

8]. Therefore, we propose the first hypothesis.

Hypothesis 1 (H1). The size of government venture capital can promote the level of urbanization development.

In addition, the impact of spatial factors on economic activity and urban development cannot be ignored. China’s urbanization has typical spatial group characteristics. Urban agglomeration construction in China can be traced back to one of the key regional proposals regarding comprehensive land development, as outlined in the National Land Planning submitted by the State Planning Commission to the State Council in 1990 [

9]. Since the turn of the 21st century, urban agglomeration has gradually become a new regional opportunity for China to participate in global competition and the international division of labor as well as a spatial subject to promote the new urbanization of the country [

10]. In the latest National New Urbanization Plan (2021–2035), the Chinese government further clarified the policy of a “coordinated and balanced development between mega polis and small cities.” Accordingly, the study of China’s urbanization development cannot be separated from the relationship between cities, and adjacent cities can promote regional development through this type of policy cooperation. Similarly, government venture capital initially aimed to pry and absorb the idle capital of society; however, with the establishment of surrounding city government venture capital, it will compete for the entire region‘s social capital, thus, creating a crowding−out effect on the local city’s government venture capital [

11]. On the basis of this, we propose the additional hypotheses:

Hypothesis 2a (H2a). The scale of government venture capital in surrounding cities positively affects a city’s urbanization development.

Hypothesis 2b (H2b). The promotion of the government venture capital scale of surrounding cities has a negative crowding−out effect on a city’s urbanization development.

Among the major urban agglomerations in China, the Yangtze River Delta urban agglomeration plays a strategic role in the overall situation and opening pattern of China‘s national modernization drive. The Yangtze River Delta is an important engine of China‘s economic and social development and has been one of the most urbanized areas in China in recent years. In order to intensely study the role of government venture capital as an important part of China‘s economic system in the process of urbanization, this study introduces the relevant data of the Yangtze River Delta region government venture capital and cities. Shanghai, as a highly developed city, has little demand for the “guidance” function of government venture capital [

12]. Therefore, to avoid the endogenous impact, this study intentionally removed Shanghai data when examining prefecture−level cities in the Yangtze River Delta and used the data of 40 prefecture−level cities in Jiangsu, Zhejiang, and Anhui provinces from 2015 to 2020 as the sample. Next, using the spatial measurement method, this study empirically analyzed the impact of government venture capital on the level of urbanization development and the impact of surrounding cities using the government venture capital model in this city.

The remainder of this paper is organized as follows.

Section 2 introduces the related literature.

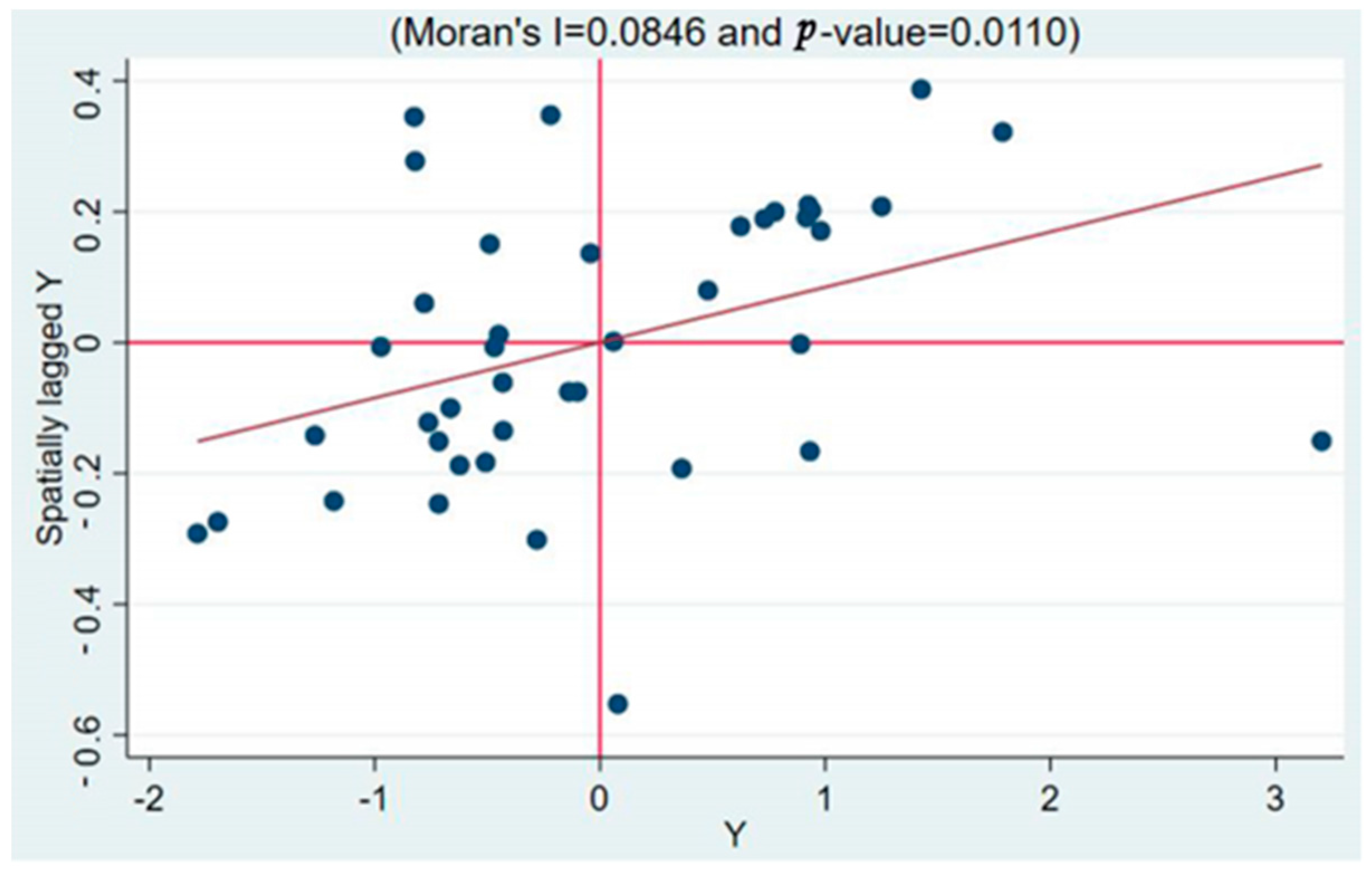

Section 3 introduces the data sources, variable definitions, and various research methods used, including factor analysis, spatial econometric model, and Moran’s test.

Section 4 reveals that the specific load of each factor is obtained through factor analysis, and the spatial−temporal evolution law of the urbanization level of cities in the Yangtze River Delta is presented through images.

Section 5 designs an empirical model for empirical testing.

Section 6 presents a series of robustness tests. Finally,

Section 7 and

Section 8 concludes the paper and provides policy recommendations, such as expanding the scale of government venture capital for underdeveloped cities.

2. Literature Review

Urbanization has been extensively studied in academic circles. Schwirian and Prehn stated that urbanization can be regarded in three ways: (1) as the process of radiation from the concept and practice of urban centers to the surrounding areas of the city; (2) changes in behavior and survival mode; and (3) the process of increasing the proportion of the urban population [

13]. As the urbanization level continues to rise, so too do theories surrounding urbanization, including Albert Otto Hirschman’s “unbalanced growth theory” [

14], Walt Whitman Rostow’s “theory of economic growth stage” [

15], Milton Friedman’s “Core−Edge Model” [

16], and Ray M. Northam‘s “S−shaped Curve of urbanization process,” all of which have great influence [

17].

With the deepening of research, the impact of economic activities on urbanization development has gradually entered the field of scholars’ vision. Chenery first discovered a link between the urbanization process and the level of economic development using empirical research [

18]. Lin et al. used the Granger causality test to determine that venture capital can stimulate economic growth [

19]. Government intervention research on venture capital is an indispensable component of the entrepreneurship and regional innovation systems fields [

20]. Early on, academic research on government intervention was conducted. Consequently, from the 1950s to the present, the research paradigm has matured, and the research framework has gradually taken shape. With the improvement of government intervention policy tools, particularly the establishment of government venture capital, which has become the predominant method of practical intervention, the focus of academic research has shifted from the early theoretical analysis of how venture capital is addressing market failure, to the quantitative demonstration of the impact of government venture capital operations.

After gradually clarifying the concept and motivation of government venture capital, current research efforts on government venture capital focus primarily on its operating mechanism and impact effects. In terms of operational mechanism, Cumming and MacIntosh believe that government venture capital with pure official background is contracted by policymakers, and the “slap the head” decisions without professional skills will lead to inefficient operation of the fund [

21,

22]. Wilson and Silva found that the Istanbul Venture Capital Initiative, the United Kingdom Future Technologies Fund, and the Belgian ARKimedes Fund all support the venture capital market [

23]. In addition, Fang Su and other Chinese scholars have studied and analyzed the operation mode of government venture capital in the United States, Israel, Italy, Australia, and other countries, and have explored the theoretical assistance of their experience in promoting government venture capital in China [

24,

25,

26,

27,

28,

29,

30,

31,

32].

Research on the impact of government venture capital primarily focuses on the impact on the investment market. Gompers et al. believe that government venture capital can promote private capital to enter the venture capital market, especially in seed enterprises with less private capital investment, which partially compensates for market failure [

33]. Seunghwan Oh confirmed the significance of the monitoring effect in enhancing various performance variables, such as corporate growth, job creation, and innovation capacity. In particular, the size of this effect was maximized in mid−stage companies and high−tech industries [

34]. Leleux and Brander found that government venture capital can promote the joint force of public and private capital to maintain long−term economic growth [

35,

36]. Yan Alperovych found that the choices of location, colocation, syndication, and industry focus of a GVC program substantially influenced the extent to which it is able to achieve such goals. Important policy implications were discussed [

37]. Yang Minli et al. explored whether government venture capital can introduce social funds into the venture capital market [

38]. Shi Guoping et al. used the difference−in−difference model to determine whether government venture capital can act on early and high−tech enterprises [

39]. Additionally, some scholars have studied the impact of government venture capital at the micro level. Yan and Bertoni empirically explored the impact of government venture capital on innovation output [

40,

41]. Meanwhile, Dong Jianwei et al. used the negative binomial distribution model to test the influence of government venture capital on enterprise innovation [

42].

The aforementioned literature and policies have examined government venture capital from multiple perspectives and dimensions. However, most of these studies are based on macro−level policy theory analysis or demonstrate the effectiveness of a specific industry and city government venture capital on entrepreneurial innovation. Few scholars are currently investigating the impact of government venture capital on the critical issue of urbanization development. Therefore, the research of this paper can fill up this academic gap to some extent.

4. Construction of Urbanization Index System

In this study, 13 variables of urbanization were analyzed using factor analysis. First, to test whether the variables could be analyzed by factor analysis, Stata was used to test the urbanization panel data of 41 cities in the Yangtze River Delta from 2016 to 2020. The results are presented in

Table 3.

Table 3 shows that the

p-value of Bartlett’s spherical hypothesis test result was 0.000, which is significant at the level of 1%. Therefore, the original spherical hypothesis is rejected, indicating that the 13 urbanization−related indicators are not independent. Concurrently, the KMO value was 0.816, greater than 0.6, indicating that the selected samples can be factor analyzed.

Next, a factor analysis was conducted on the 13 variables. The results are presented in

Table 4. The factor analysis method typically extracts explanatory factors with eigenvalues greater than 1. The eigenvalues of Factor1, Factor2, and Factor3 are all greater than 1. Simultaneously, the cumulative contribution rate of these three factors reached 71.58%, which was greater than 70%. Therefore, this study believes that these three factors can appropriately represent the 13 urbanization variables.

A scree plot was generated to test the rationality of the factor selection. Evidently, the characteristic root map of the first three factors is steep; however, after the fourth factor, it becomes more gradual. Therefore, the first three factors were selected (

Figure 2).

To understand the specific load of each factor, the factor analysis results were rotated, with the factor load matrix obtained, as shown in

Table 5. The main loads of F1 are population, electricity, goods, income, and expenditure, which are referred to as the living standard factors in this study. The main loads of F2 are education, tertiary, water, and libraries, which are referred to as urban construction−level factors in this study. The main load of F3 is sewage, green, health, and greening, which are referred to as ecological health factors in this study.

In this paper, the scores of each factor are calculated by STATA17.0, and the weights of each factor are calculated by rotation results. Finally, the comprehensive score of urbanization level of each observation value is obtained by weighted calculation (

Table 6).

Figure 3 shows the spatial distribution map of the comprehensive score of urbanization level in the Yangtze River Delta region from 2016 to 2020.

The urbanization level in the study area of the Yangtze River Delta region generally shows the characteristics of high levels in the east, low in the southwest, and continually increasing from 2016 to 2020. The urbanization score of Nanjing in 2016 is significantly higher than that in other cities, which is at the highest grade. However, the urbanization score is mainly at the lowest grade in the northern region of the study area. As time goes by, the urbanization level of cities around Nanjing and Suzhou increased conspicuously. Compared with 2016, the urbanization level of the study area in 2020 is generally higher, and cities in the east−central part are mostly highly urbanized. The urbanization level of cities in the northern part are relatively low, which are always below average. A plausible reason for this kind of distribution is that the core cities such as Nanjing, Suzhou, and Hangzhou have more developed scientific and economic conditions, and convenient transportation, which can radiate to the surrounding area to promote urbanization, while the northern cities are lacking these conditions.

7. Discussion and Analysis

The results presented in

Table 8 demonstrate the validity of H1 and H2a, indicating that:

- (1)

The promotion of the scale of government venture capital by the government of surrounding cities contributes to promoting the urbanization development of the city.

- (2)

The size of government venture capital positively affects the improvement in local urbanization levels.

So that they would better correspond with the actual hypotheses.

Table 9,

Table 10 and

Table 11 exhibit that the direct effects of government venture capital are primarily achieved by promoting the living standards of residents and the level of urban construction, whereas the indirect effects are reflected through the living standards of residents and the levels of ecological health. Specifically, the establishment of H1 is consistent with the conclusion of this study: the government directs funds to compensate for market failure by supporting public goods with strong positive externalities, such as infrastructure, which directly promote the development and construction of the city and contribute to promoting the urbanization process.

The establishment of H2a demonstrates that the indirect effect emphasized in this study is also significantly positive, likely because government venture capital in urban agglomerations cooperates more than it competes. Alternatively, this may also be due to the fact that, as a developed region of China, the Yangtze River Delta urban agglomeration has sufficient idle social capital, and it is therefore difficult to produce a crowding−out effect or reduce the crowding−out effect. Infrastructure government venture capital promotes the construction of the city, while providing employment and a higher standard of living for city residents. Simultaneously, the industrial government venture capital and the innovation government venture capital may compensate for the key nodes of the industrial chain through cooperation between cities and strengthen the industrial cluster to boost the economic level of the entire region and raise the standard of living for its residents. Moreover, the indirect effects of ecological health were notably positive. In recent years, the Chinese government has focused more on environmental issues. Some cities have established green industry government venture capital on the basis of the experience of developed countries. Through coordination and cooperation among local governments, the entire green ecological health system can be improved, thus, promoting the development of ecological health levels in the entire region.

8. Conclusions and Implications

8.1. Conclusions

The improvement of the urbanization level is the inevitable outcome of a country’s or region’s social and economic development, and a mark of social progress. As a special form of venture capital, government venture capital plays a significant role in promoting regional development and enterprise innovation. This study analyzed the relationship between the regional urbanization level and the scale of government venture capital. On the basis of the panel data of each prefecture−level city in the Yangtze River Delta from 2015 to 2020, this study visually presents the urbanization score of each prefecture−level city through the comprehensive evaluation index of the urbanization level constructed by factor analysis, and draws additional conclusions using a spatial econometric model. The conclusions are as follows:

First, the urbanization development in the Yangtze River Delta has a clear spatial and temporal distribution. The urbanization level of the prefecture−level cities distributed in the eastern and middle regions of the Yangtze River Delta was higher, whereas that of the northwestern regions of the Yangtze River Delta was generally lower. From a provincial perspective, the urbanization level of cities in Jiangsu and Zhejiang Provinces surrounding their respective capitals, Nanjing and Hangzhou, is relatively high, whereas the urbanization level of prefecture−level cities in Anhui is generally low. Additionally, as time passed, the characteristics of this distribution became more apparent. The spatial agglomeration effect primarily presented the characteristics of high−high and low−low agglomerations.

Second, the increasing scale of government venture capital can help improve the urbanization level in a region, and the expansion of the government venture capital’s scale by the surrounding cities is also conducive to the improvement of the local urbanization level. With the characteristics of the combination of marketization and policy, government venture capital guides social capital into the field of venture capital by supporting the development of venture capital enterprises to promote regional industrial transformation and upgrading, as well as the development of regional economies and indirectly promotes the improvement of regional urbanization levels. The expanding scale of government venture capital in neighboring cities creates favorable conditions for the coordinated development of industries across regions, which can also contribute to the improvement of local urbanization levels.

Finally, government venture capital primarily promotes the development of local urbanization by promoting the standards of urban construction and the living standards of residents and fosters the development of regional urbanization by enhancing the level of ecological sanitation. In addition, the development of the tertiary sector will contribute significantly to the local urbanization process.

8.2. Implications

On the basis of the above conclusions, this study provides theoretical support for the development and improvement of China’s government venture capital system and urbanization construction through the following targeted policy recommendations:

First, due to the characteristics of high−high and low−low agglomeration in the spatial distribution of urbanization levels, cities with low urbanization levels will struggle to drive the development of urbanization in surrounding cities and towns. Therefore, for cities with low urbanization levels, the government should appropriately expand the scale of the local government venture capital to better leverage social capital. They should also strengthen complementarity and cooperation with the more developed surrounding cities to realize the full inflow of resources from high to low through cross−border government venture capital, which promotes the urbanization process of less developed cities.

Second, optimize the fund management system and promote the clustered development of capital industry. Establishing a scientific operational process is the key to ensuring the positive development of capital. The government venture capital established by government investment should clarify the project selection principle and bring in a senior talent management team, in order for the capital to have positive development prospects, drive regional economic development, alleviate employment pressure, and actively explore industrial transformation and upgrading to better promote the level of regional urbanization. Since this study found there’s a space spillover effect for government venture capital to facilitate the process of urbanization, the government can build high−level government guidance funds in cities like Hefei and Xuzhou. With the government guidance funds and national laboratories or new collaborative innovation platforms, these cities can attract excellent investment management institutions with rich industry experience to cooperate in setting up funds, and promote the high−quality gathering and development of regional venture capital industry, so as to further improve the urbanization level of this whole region.

Finally, governments should utilize venture capital to continuously deepen the reform of the service industry, promote high−quality development of the tertiary sector, and contribute key forces to the development of regional urbanization. In recent years, the emerging strategic service industry has become a new driver of economic growth. Social forces actively participating in the construction of public services, tourism, culture, sports, health, pension, and other industries enjoy a strong developmental momentum. Ultimately, vigorously developing the modern emerging service industry can not only bring considerable economic benefits, but also provide residents with more abundant material living conditions, which can contribute to the improvement of the local urbanization level in many aspects.

8.3. Reflections

Through static and dynamic analyses, this research revealed the positive impact of government venture capital on urbanization from a geospatial point of view. In addition, a multidimensional evaluation system was constructed to calculate the urbanization level of 40 cities in the YZD region. However, there may be some limitations to this study. Since it is relatively difficult to acquire the data on government venture capital, especially in economically underdeveloped areas where the guidance fund system is still in the early stages, this research only conducted an empirical study based on the YZD region and does not have a comparative analysis to explore the differences and experiences of different regions for reference. Furthermore, there may be some omitted factors that affected the urbanizing process when constructing the urbanization level evaluation system. In addition, this study only revealed the correlation between urbanization and government venture capital from a macro perspective, and more methods should be utilized to explain the theoretical mechanisms. Therefore, the next step for us will be to collect data from various geological regions and conduct further research in a national perspective, along with the refinement of the urbanization level calculation system. Meanwhile, based on this research framework, more empirical methods will be used to uncover the deeper theoretical connections and influence path between urbanization and government venture capital.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}