Agritourism and Farms Diversification in Italy: What Have We Learnt from COVID-19?

Abstract

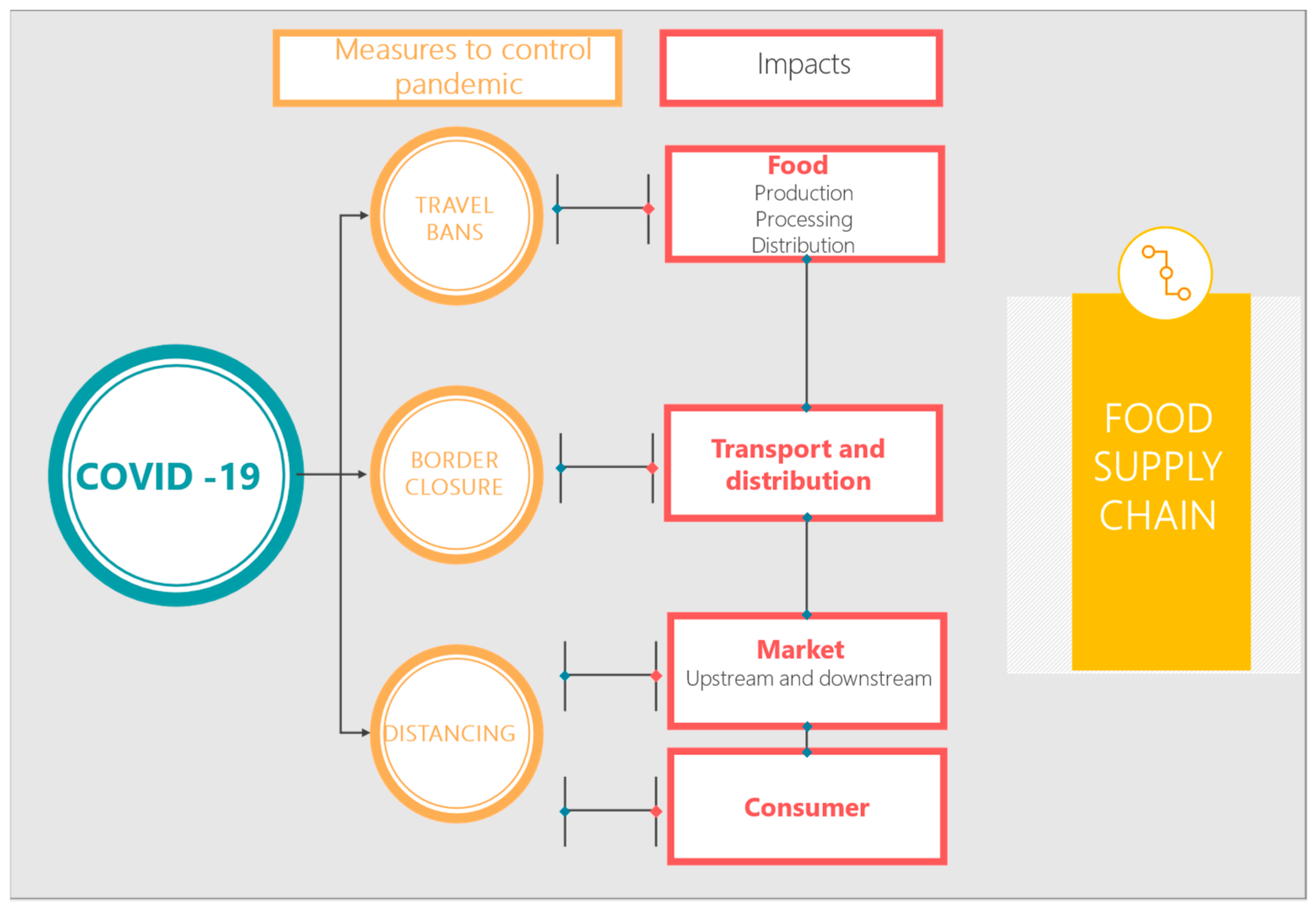

:1. Introduction

2. The Theoretical Approach: Farm Diversification as a form of Resilience Strategy

3. Materials and Methods

Data Collection

- changes in consumer demand for food and farm response;

- acquisition of new customers;

- changes in customer purchasing and consumption behaviors;

- revenue forecasts;

- changes to the organizational structure;

- expansion of the services offered.

4. Results: Consequences of COVID-19

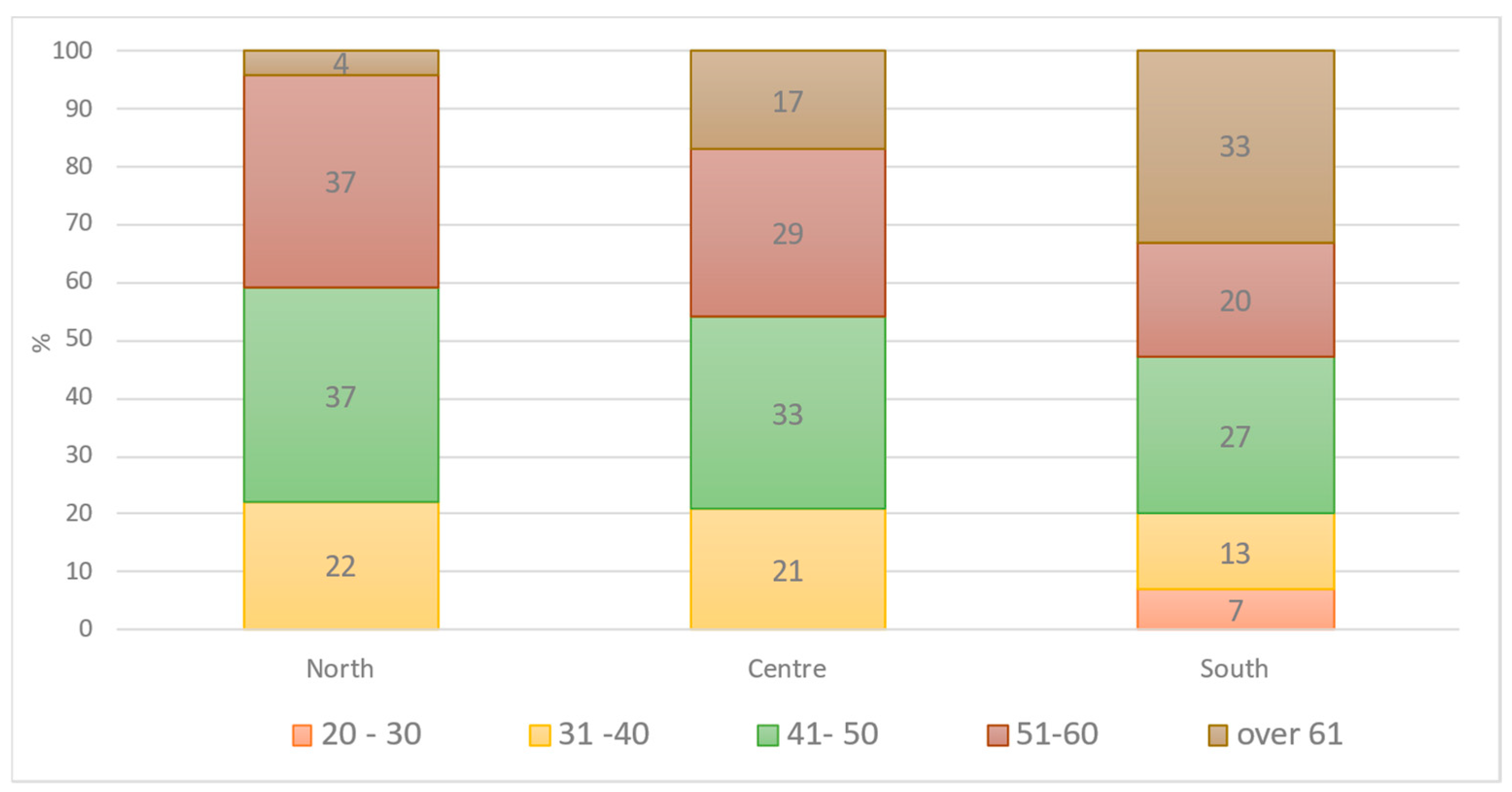

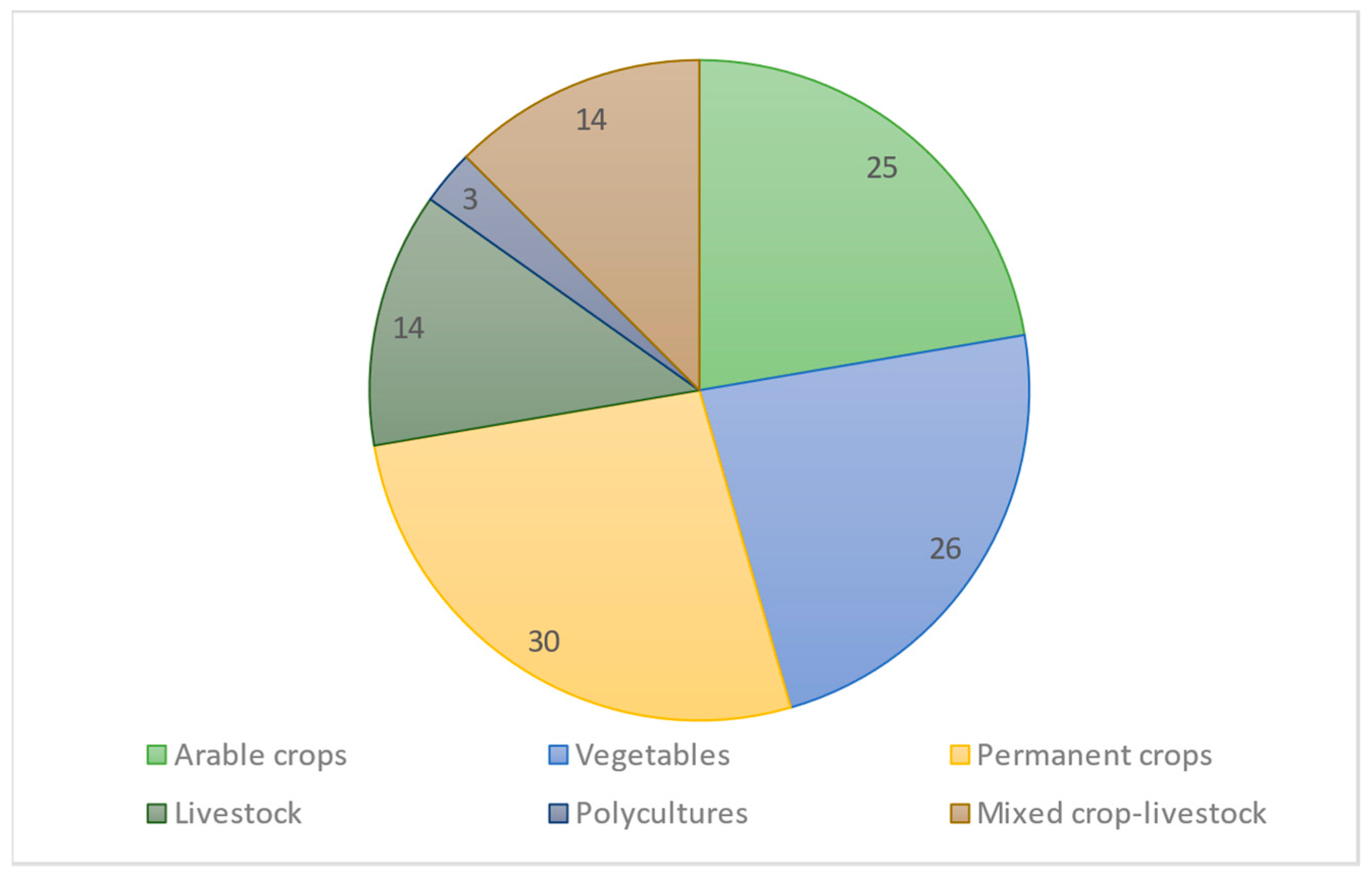

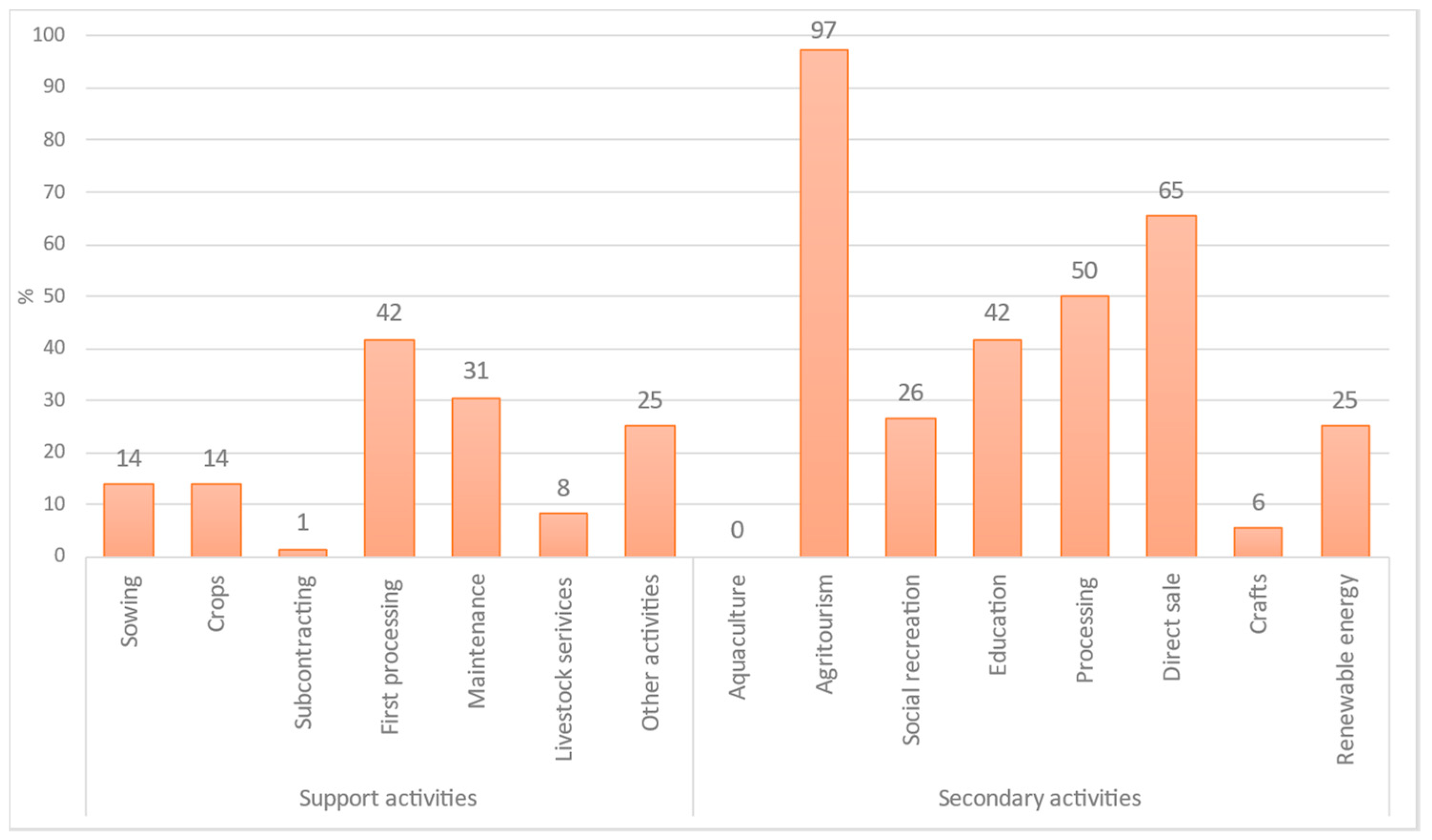

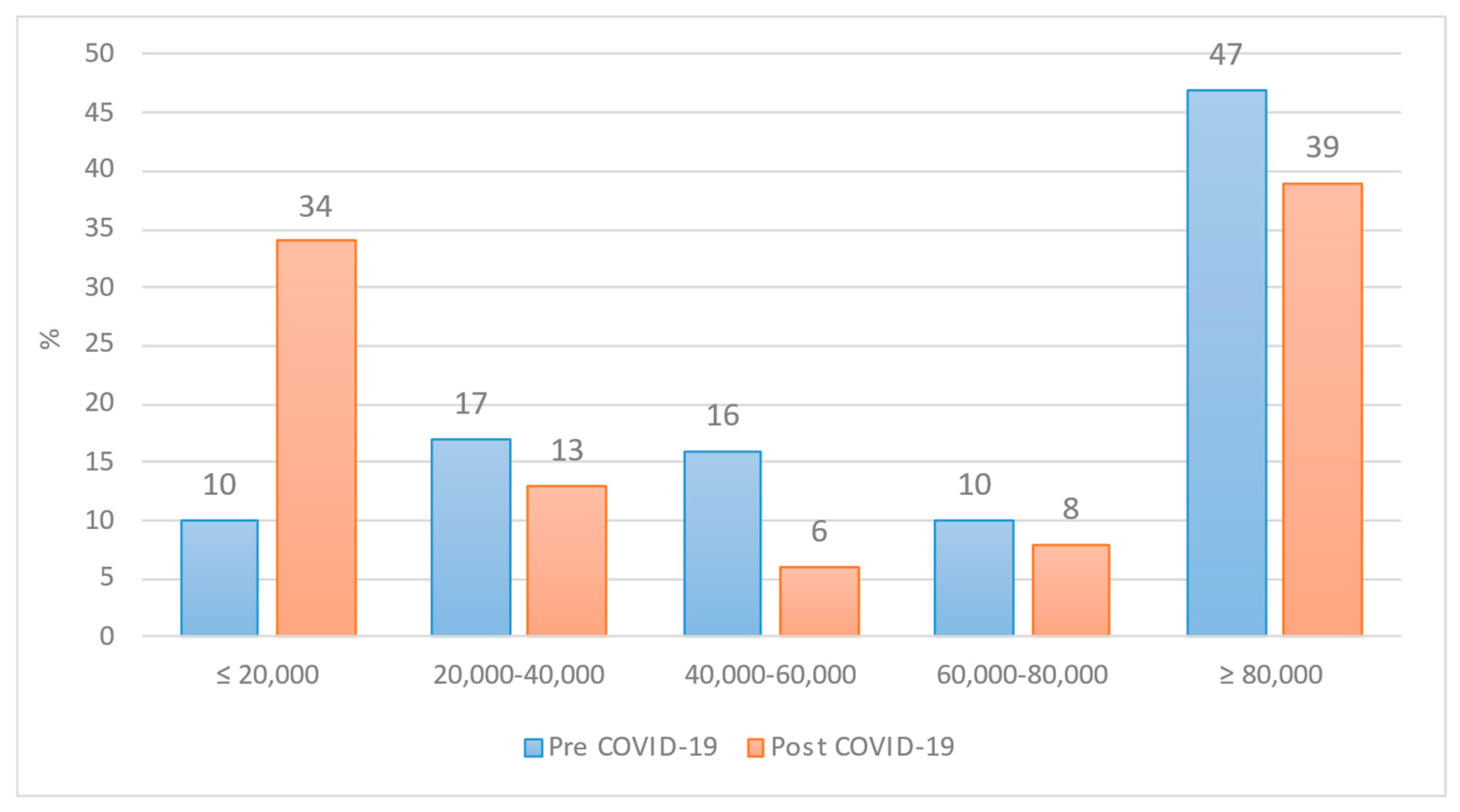

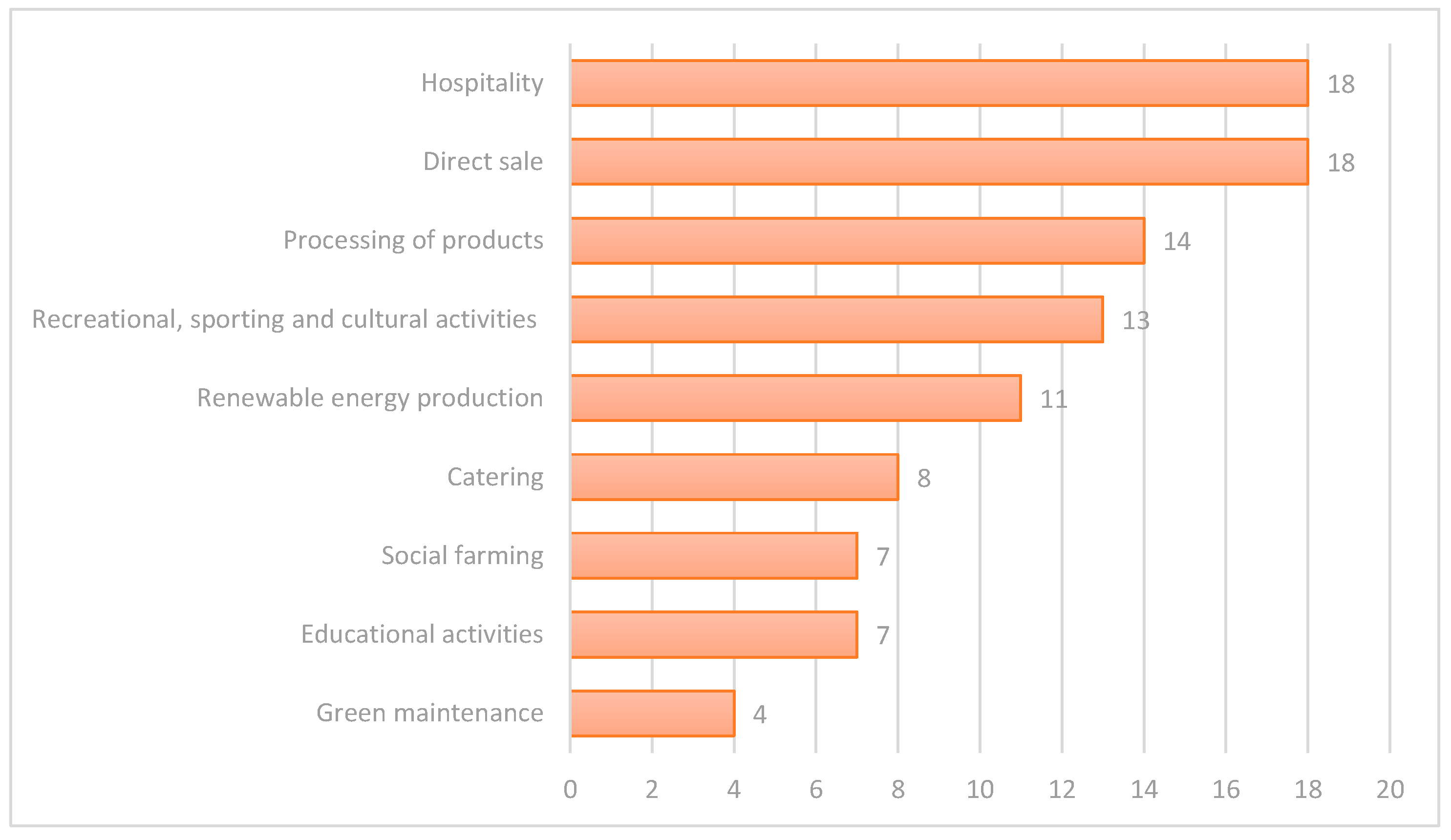

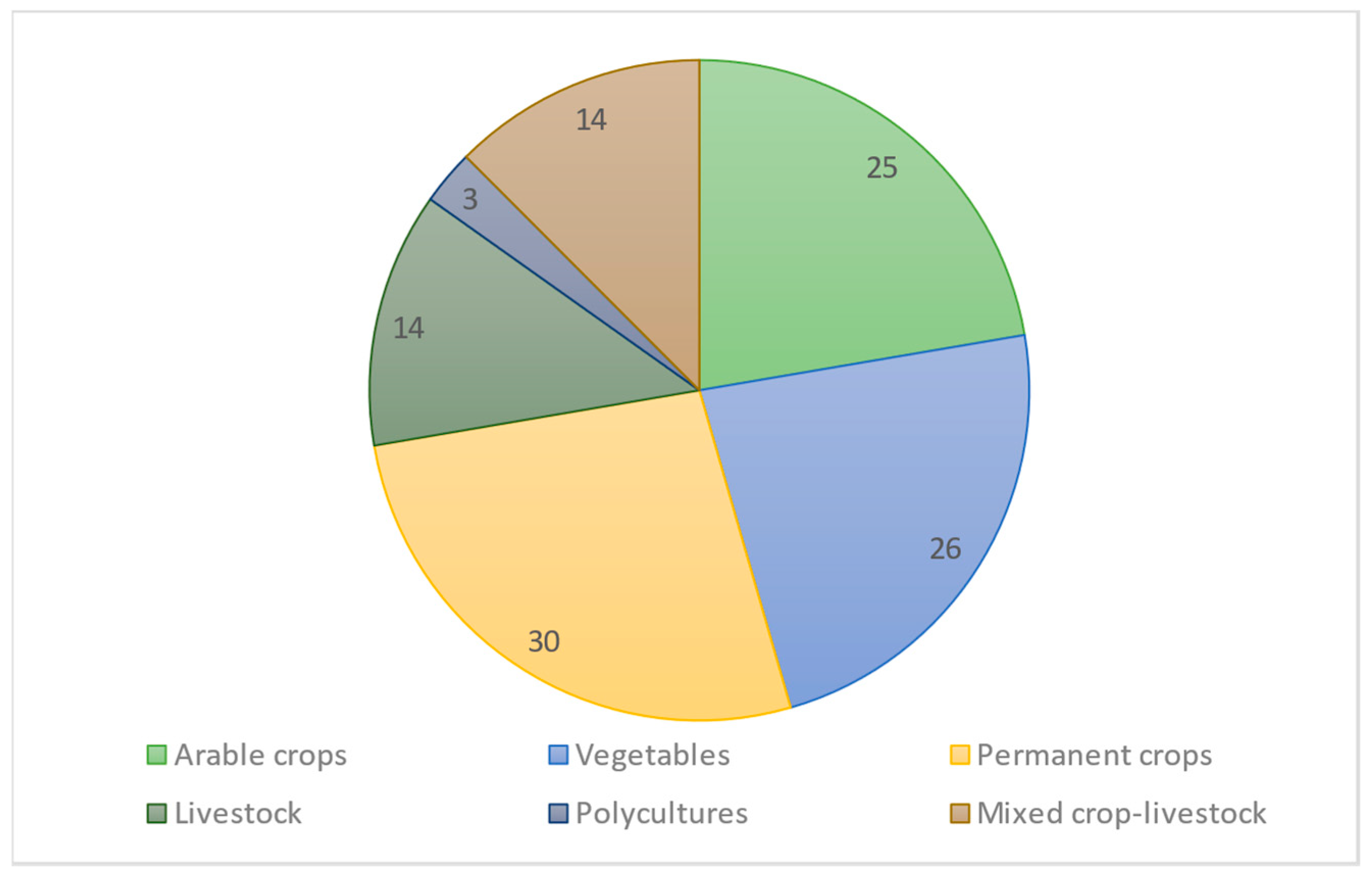

4.1. Main Characteristics of Agricultural Farms

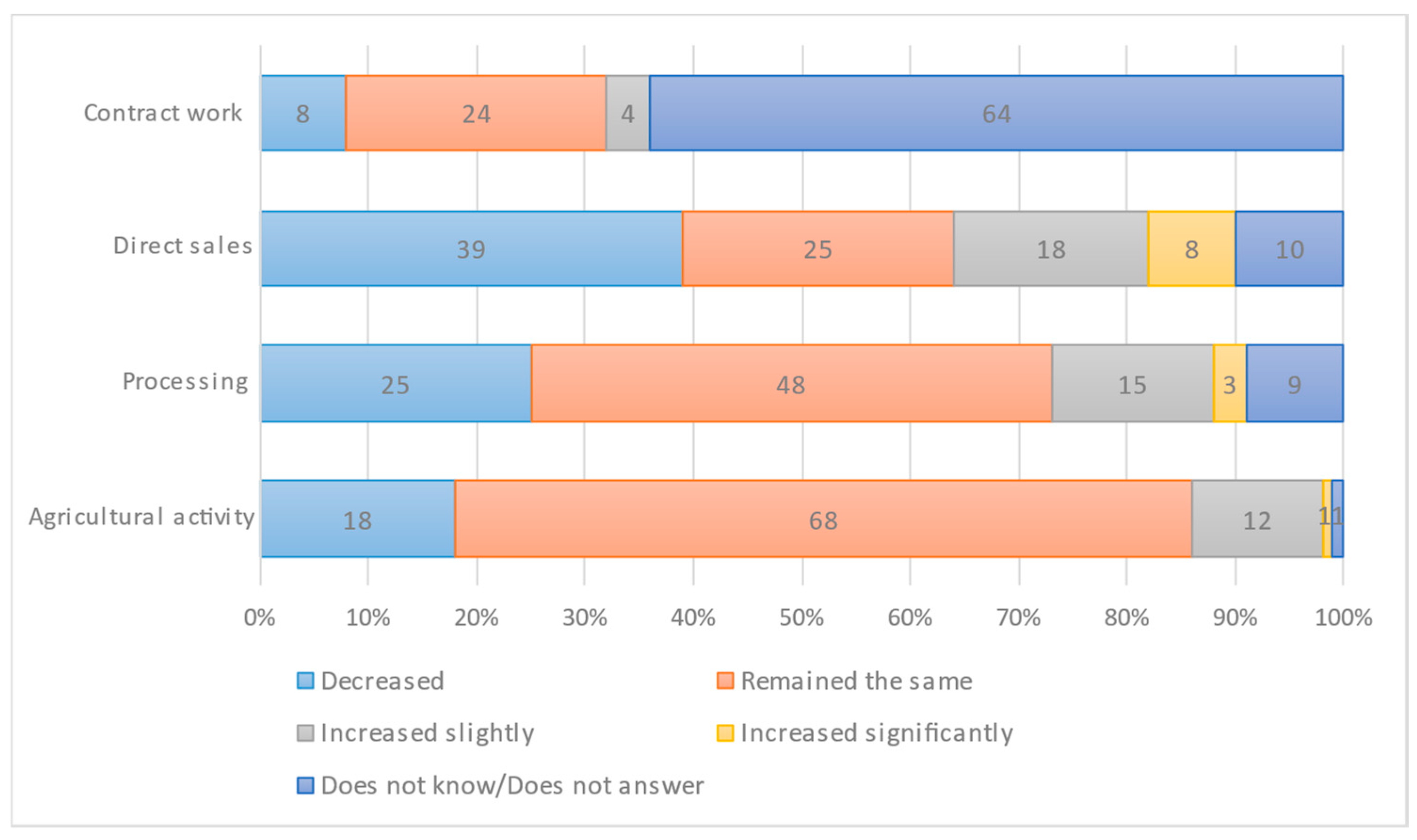

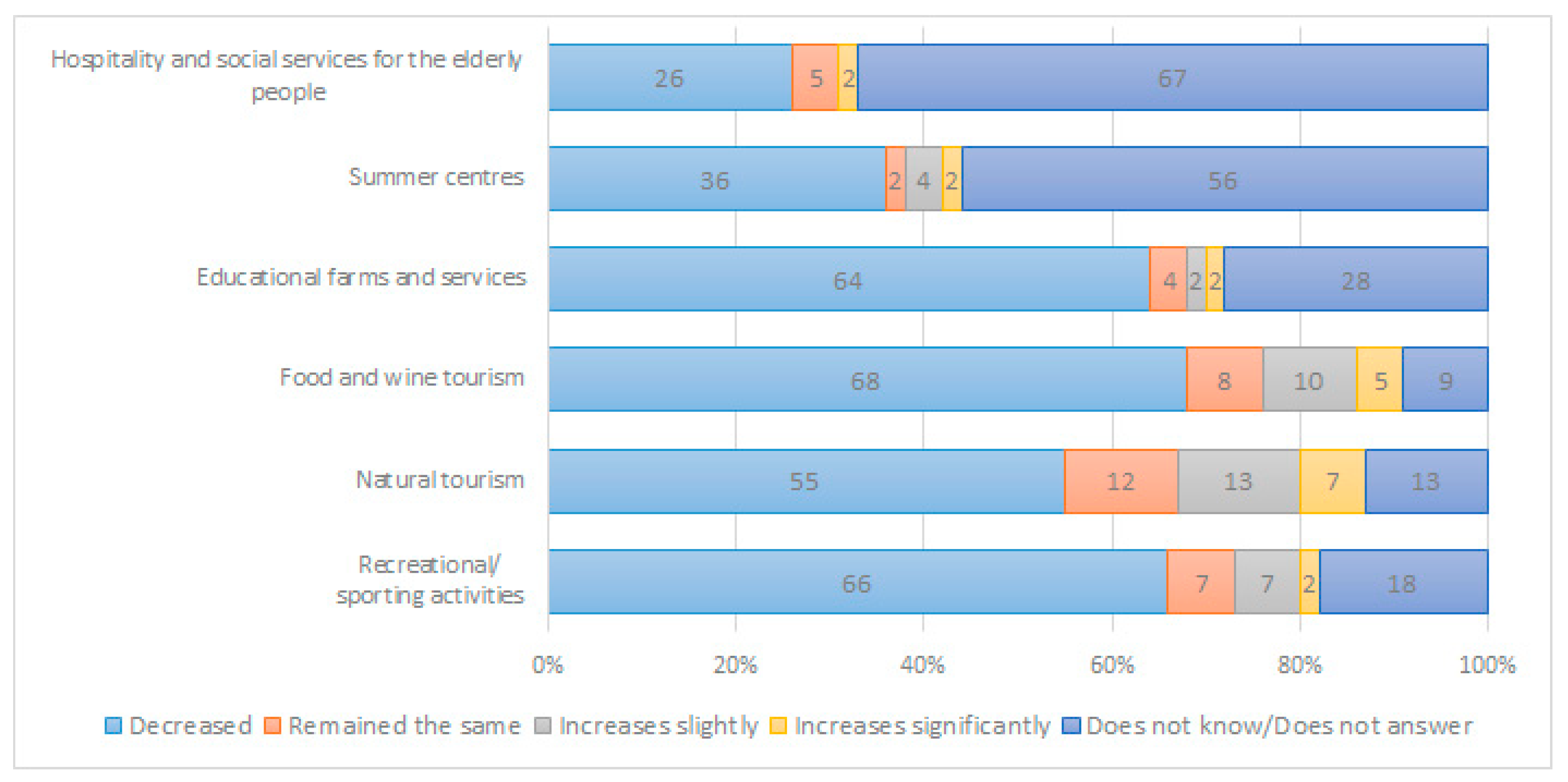

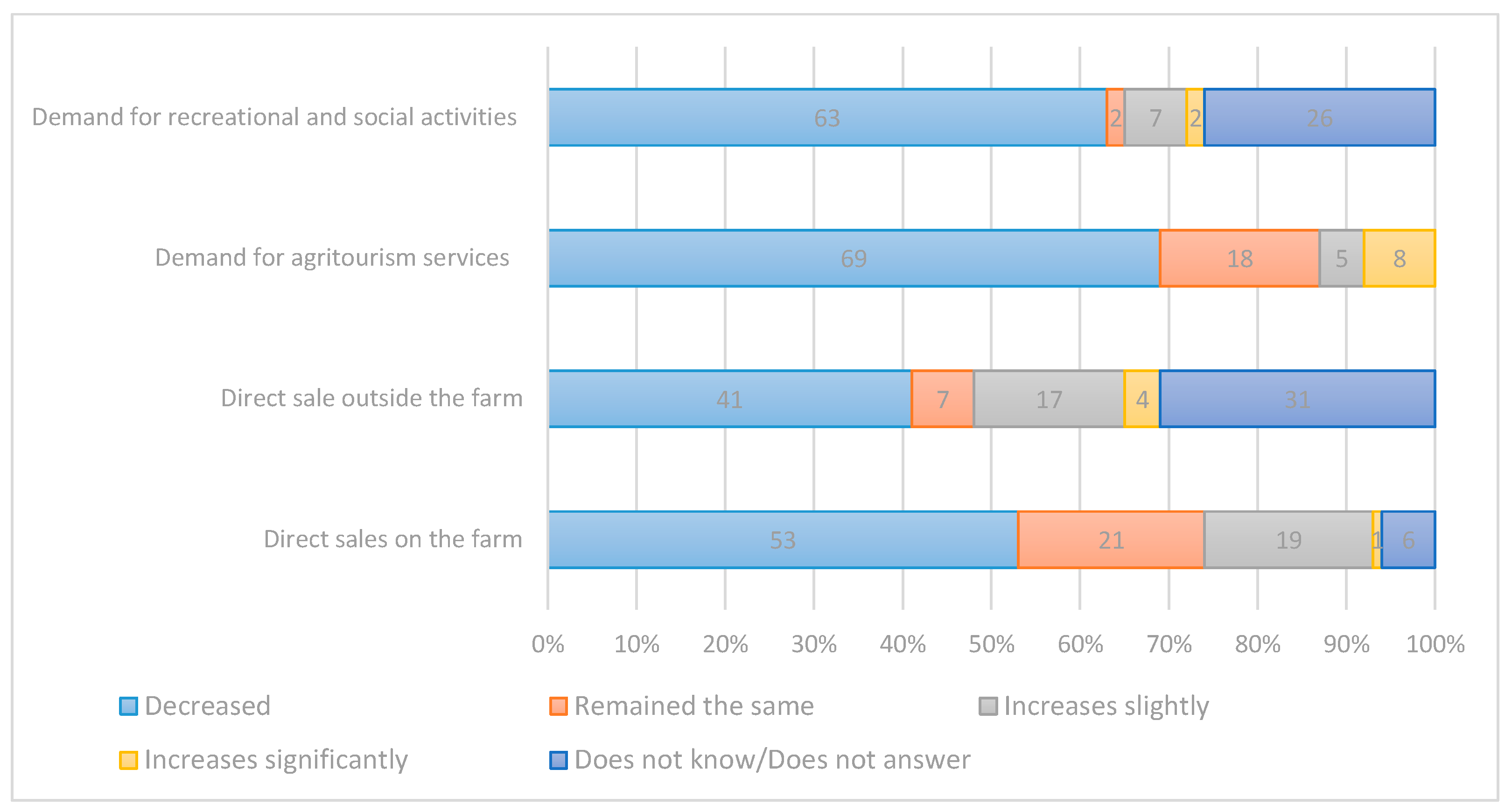

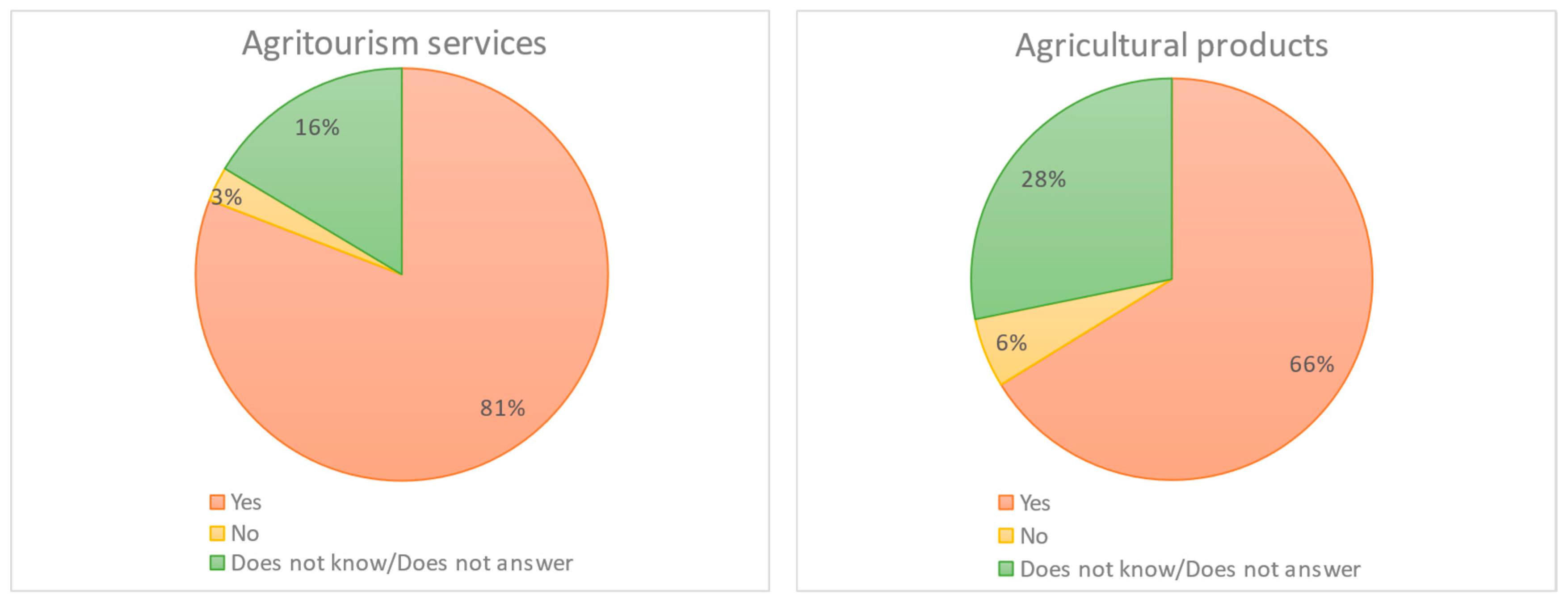

4.2. Perceived Impacts on Sales Channels and the Tourism Offer

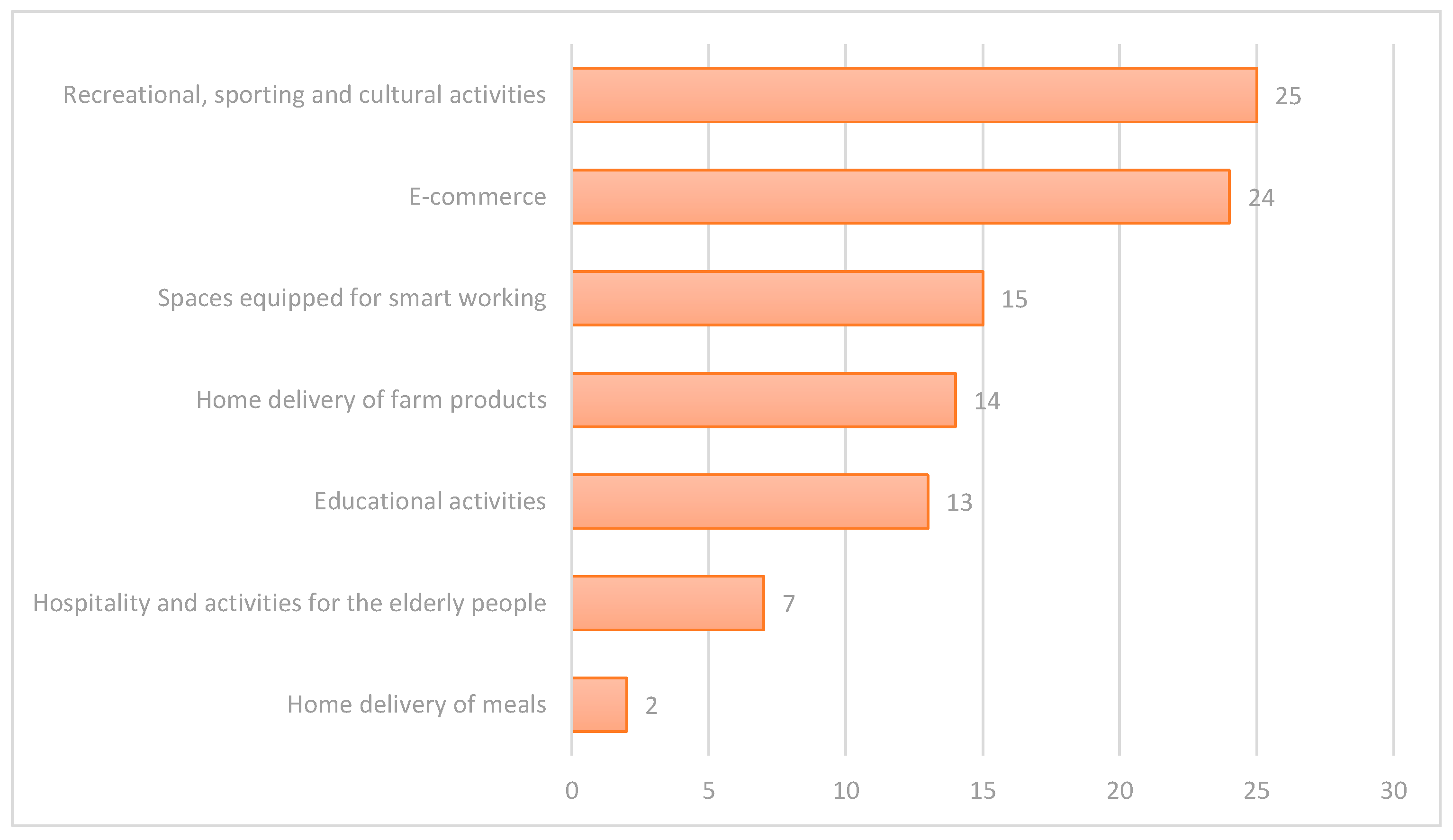

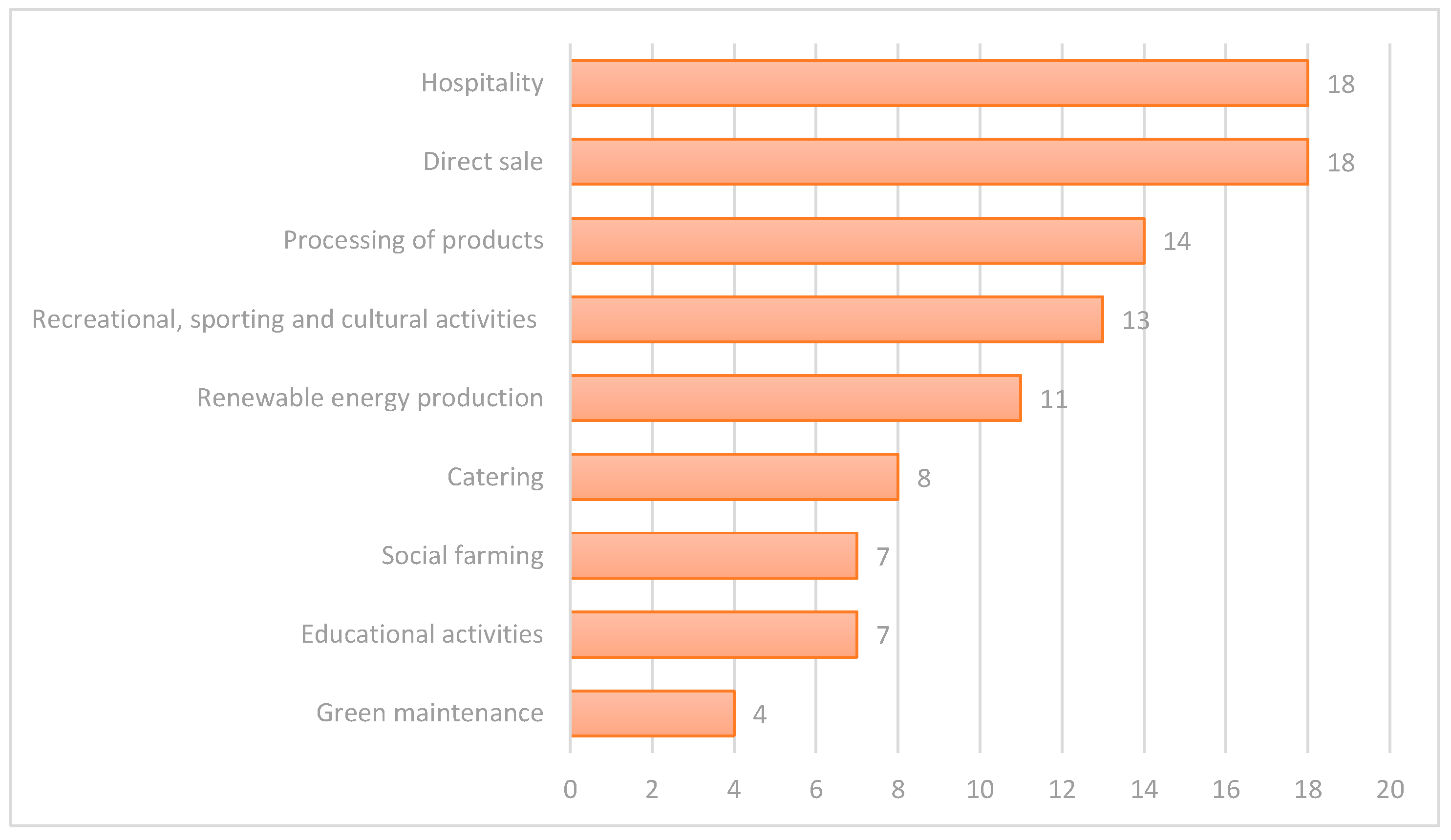

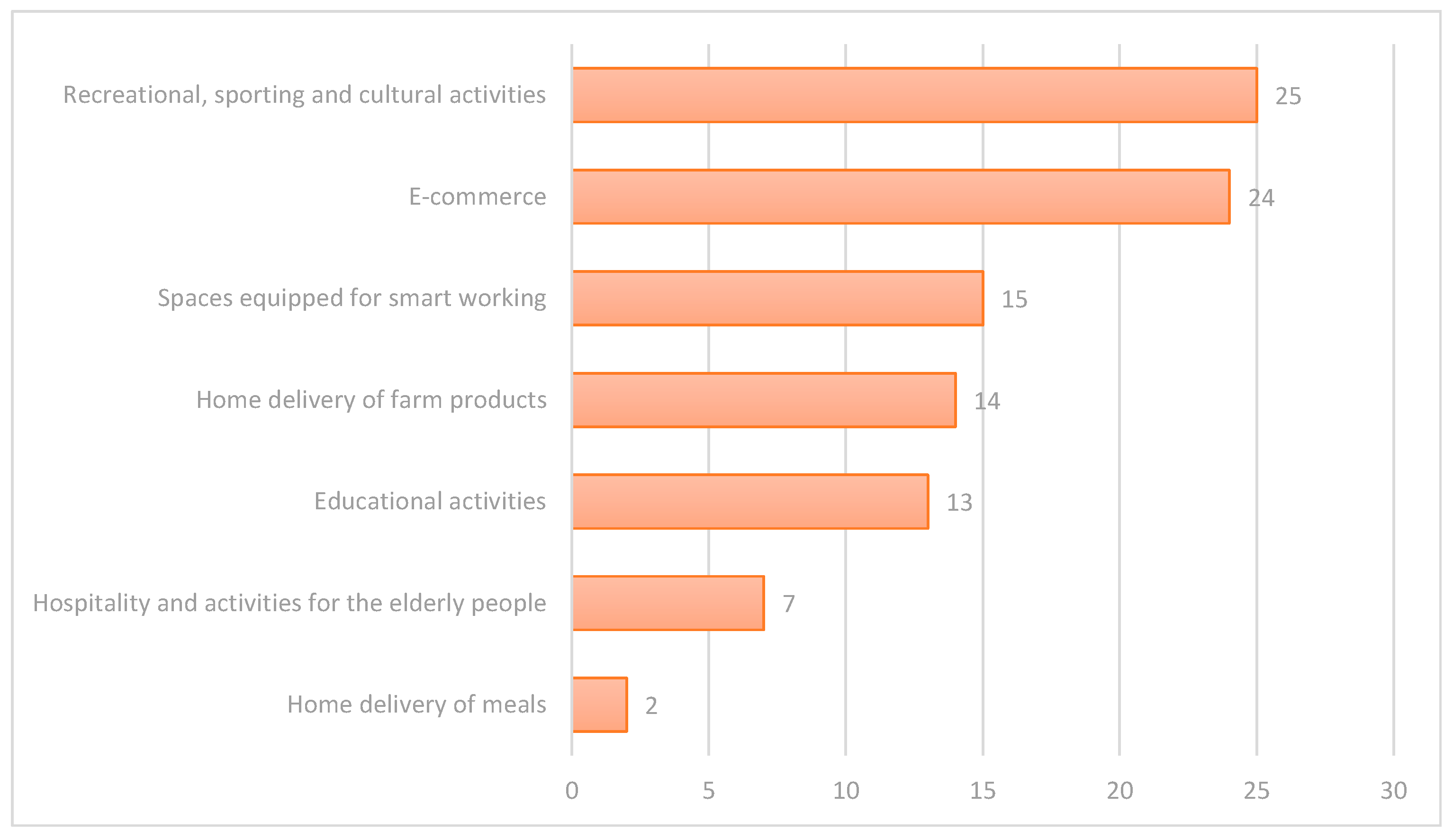

4.3. Repositioning Strategies

5. Findings and Discussions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Borsellino, V.; Kaliji, A.A.; Schimmenti, E. COVID-19 Drives Consumer Behaviour and Agro-Food Markets towards Healthier and More Sustainable Patterns. Sustainability 2020, 12, 8366. [Google Scholar] [CrossRef]

- Bakalis, S.; Valdramidis, V.; Argyropoulos, D.; Ahrne, L.; Chen, J.; Cullen, P.; Cummins, E.; Datta, A.K.; Emmanouilidis, C.; Foster, T.; et al. How COVID-19 changed our food systems and food security paradigms. Curr. Res. Food Sci. 2020, 3, 166–172. [Google Scholar] [CrossRef] [PubMed]

- Mastronardi, L.; Cavallo, A.; Romagnoli, L. How did Italian diversified farms tackle COVID-19 pandemic first wave challenges? Socio-Econ. Plan. Sci. 2021, 82, 101096. [Google Scholar] [CrossRef] [PubMed]

- Amato, M.; Verneau, F.; Coppola, A.; La Barbera, F. Domestic Food Waste and COVID-19 Concern: An Application of the Theory of Planned Behaviour. Sustainability 2021, 13, 8366. [Google Scholar] [CrossRef]

- Apostolopoulos, N.; Ratten, V.; Petropoulos, D.; Liargovas, P.; Anastasopoulou, E. Agri-food sector and entrepreneurship during the COVID-19 crisis: A systematic literature review and research agenda. Strateg. Chang. 2021, 30, 159–167. [Google Scholar] [CrossRef]

- Naja, F.; Hamadeh, R. Nutrition amid the COVID-19 pandemic: A multi-level framework for action. Eur. J. Clin. Nutr. 2020, 74, 1117–1121. [Google Scholar] [CrossRef]

- Benedek, Z.; Fertő, I.; Marreiros, C.G.; de Aguiar, P.M.; Pocol, C.B.; Čechura, L.; Põder, A.; Pääso, P.; Bakucs, Z. Farm diversification as a potential success factor for small-scale farmers constrained by COVID-related lockdown. Contributions from a survey conducted in four European countries during the first wave of COVID-19. PLoS ONE 2021, 16, e0251715. [Google Scholar] [CrossRef]

- Vittuari, M.; Bazzocchi, G.; Blasioli, S.; Cirone, F.; Maggio, A.; Orsini, F.; Penca, J.; Petruzzelli, M.; Specht, K.; Amghar, S.; et al. Envisioning the Future of European Food Systems: Approaches and Research Priorities after COVID-19. Front. Sustain. Food Syst. 2021, 5, 642787. [Google Scholar] [CrossRef]

- Grant, F.; Scalvedi, M.L.; Scognamiglio, U.; Turrini, U.; Rossi, L. L’impatto dell’emergenza COVID-19 Sulle Abitudini Alimentari Degli Italiani nel Periodo Della Quarantena di Marzo-Aprile 2020; Special Issue O-ERSA 2020; Centro di Ricerca Alimenti e Nutrizione: Roma, Italy, 2021; ISBN 9788833850962. [Google Scholar]

- Başev, S.E. Effect of economic crisis on food consumption behaviour of British Consumers. Int. J. Educ. Res. 2014, 2, 289–316. [Google Scholar]

- Lowenberg-DeBoer, J.; Behrendt, K.; Boot, A.; Byrne, R.; de Silva, C.; Eastham, J. Longer Term Impacts of the COVID-19 Pandemic on European Agriculture. In Proceedings of the 3rd INFER Symposium on Agri-Tech Economics for Sustainable Futures, Harper Adams University, Newport, UK, 21–22 September 2020. [Google Scholar]

- Montanari, F.; Ferreira, I.; Lofstrom, F.; Varallo, C.; Volpe, S.; Smith, E.; Kirova, M.; Wion, A.; Kubota, U.; Albuquerque, J.D. Research for AGRI Committee—Preliminary Impacts of the COVID-19 Pandemic on European Agriculture: A Sector-Based Analysis of Food Systems and Market Resilience; European Parliament—Policy Department for Structural and Cohesion Policies: Brussels, Belgium, 2021. [Google Scholar]

- Fratto, F.; Galasso, G.; Hausmann, C.; Selmi, U. Agriturismo e Multifunzionalità Scenario e Prospettive. Documento Realizzato Nell’ambito del Programma Rete Rurale Nazionale 2014-20; Rapporto; ISMEA: Rome, Italy, 2020; ISBN 9788896095300. [Google Scholar]

- Gruère, G.; Brooks, J. Viewpoint: Characterising early agricultural and food policy responses to the outbreak of COVID-19. Food Policy 2021, 100, 102017. [Google Scholar] [CrossRef]

- Schuh, B.; Münch, A.; Badouix, M.; Hat, K.; Brkanovic, S. Research for AGRI Committee—The Future of the European Farming Model: Socio-Economic and Territorial Implications of the Decline in the Number of Farms and Farmers in the EU; European Parliament, Policy Department for Structural and Cohesion Policies: Brussels, Belgium, 2022. [Google Scholar] [CrossRef]

- Nguyen, K. 2020 State of Food Security and Nutrition in the World Report. Rising Hunger and COVID-19 Present Formidable Challenges. 2020. Available online: https://www.ifpri.org/blog/2020-state-food-security-and-nutrition-world-report-risinghunger-and-covid-19-present (accessed on 2 May 2022).

- Chin, W.L.; Musa, S.F.P.D. Agritourism resilience against COVID-19: Impacts and management strategies. Cogent Soc. Sci. 2021, 7, 1950290. [Google Scholar] [CrossRef]

- Morris, C.; Winter, M. Integrated farming systems: The third way for European agriculture? Land Use Policy 1999, 16, 193–205. [Google Scholar] [CrossRef]

- Ammirato, S.; Felicetti, A.M.; Raso, C.; Pansera, B.A.; Violi, A. Agritourism and Sustainability: What We Can Learn from a Systematic Literature Review. Sustainability 2020, 12, 9575. [Google Scholar] [CrossRef]

- Barbieri, C.; Mshenga, P.M. The Role of the Firm and Owner Characteristics on the Performance of Agritourism Farms. Sociol. Rural. 2008, 48, 166–183. [Google Scholar] [CrossRef]

- Ammirato, S.; Felicetti, A.M. The Agritourism as a Means of Sustainable Development for Rural Communities: A Research from the Field. Int. J. Interdiscip. Environ. Stud. 2014, 8, 17–29. [Google Scholar] [CrossRef]

- Fortune Business Insights. Agritourism Market Size, Share & COVID-19 Impact Analysis, by Type (Direct-market, Education & Experience, and Event & Recreation), and Regional Forecast, 2020–2027. Report ID: FBI103297. 2020. Available online: https://www.fortunebusinessinsights.com/agritourism-market-103297 (accessed on 15 March 2022).

- Van der Ploeg, J.D.; Roep, D. Multifunctionality and Rural Development: The Actual Situation in Europe. Multifunctional Agriculture: A New Paradigm for European Agriculture and Rural Development; Ashgate Publishing Company: Aldershot, UK, 2003; pp. 37–54. [Google Scholar]

- Salvioni, C.; Ascione, E.; Henke, R. Structural and economic dynamics in diversified Italian farms. Bio-Based Appl. Econ. 2013, 2, 257–275. [Google Scholar] [CrossRef]

- Carlsen, J.; Getz, D.; Ali-Knight, J. The Environmental Attitudes and Practices of Family Businesses in the Rural Tourism and Hospitality Sectors. J. Sustain. Tour. 2001, 9, 281–297. [Google Scholar] [CrossRef]

- Giurea, R.; Precazzini, I.; Ragazzi, M.; Achim, M.I.; Cioca, L.I.; Conti, F.; Torretta, V.; Rada, E.C. Good Practices and Actions for Sustainable Municipal Solid Waste Management in the Tourist Sector. Resources 2018, 7, 51. [Google Scholar] [CrossRef]

- Giaccio, V.; Mastronardi, L.; Marino, D.; Giannelli, A.; Scardera, A. Do Rural Policies Impact on Tourism Development in Italy? A Case Study of Agritourism. Sustainability 2018, 10, 2938. [Google Scholar] [CrossRef]

- European Commission. Agenda 2000. For a Stronger and Wider Union; European Commission: Brussels, Belgium, 1997. [Google Scholar]

- Garrod, B.; Wornell, R.; Youell, R. Re-Conceptualising Rural Resources as Countryside Capital: The Case of Rural Tourism. J. Rural. Stud. 2006, 22, 117–128. [Google Scholar] [CrossRef]

- Nickerson, N.P.; Black, R.J.; McCool, S.F. Agritourism: Motivations behind Farm/Ranch Business Diversification. J. Travel Res. 2001, 40, 19–26. [Google Scholar] [CrossRef]

- Tew, C.; Barbieri, C. The Perceived Benefits of Agritourism: The Provider’s Perspective. Tour. Manag. 2012, 33, 215–224. [Google Scholar] [CrossRef]

- Sgroi, F.; Di Trapani, A.M.; Testa, R.; Tudisca, S. The rural tourism as development opportunity or farms. The case of direct sales in sicily. Am. J. Agric. Biol. Sci. 2014, 9, 407–419. [Google Scholar] [CrossRef]

- Lupi, C.; Giaccio, V.; Mastronardi, L.; Giannelli, A.; Scardera, A. Exploring the features of agritourism and its contribution to rural development in Italy. Land Use Policy 2017, 64, 383–390. [Google Scholar] [CrossRef]

- Roman, M.; Niedziółka, A.; Krasnodebski, A. Respondents’ Involvement in Tourist Activities at the Time of the COVID-19 Pandemic. Sustainability 2020, 12, 9610. [Google Scholar] [CrossRef]

- Khan, M.R.; Khan, H.U.R.; Lim, C.K.; Tan, K.L.; Ahmed, M.F. Sustainable Tourism Policy, Destination Management and Sustainable Tourism Development: A Moderated-Mediation Model. Sustainability 2021, 13, 12156. [Google Scholar] [CrossRef]

- Cretu, C.-M.; Turtureanu, A.-G.; Sirbu, C.-G.; Chitu, F.; Marinescu, E.Ş.; Talaghir, L.-G.; Robu, D.M. Tourists’ Perceptions Regarding Traveling for Recreational or Leisure Purposes in Times of Health Crisis. Sustainability 2021, 13, 8405. [Google Scholar] [CrossRef]

- Roman, M.; Prus, P. Innovations in Agritourism: Evidence from a Region in Poland. Sustainability 2020, 12, 4858. [Google Scholar] [CrossRef]

- Palmi, P.; Lezzi, G.E. How Authenticity and Tradition Shift into Sustainability and Innovation: Evidence from Italian Agritourism. Int. J. Environ. Res. Public Health 2020, 17, 5389. [Google Scholar] [CrossRef]

- Phillip, S.; Hunter, C.; Blackstock, K. A Typology for Defining Agritourism. Tour. Manag. 2010, 31, 754–758. [Google Scholar] [CrossRef]

- Frochot, I. A Benefit Segmentation of Tourists in Rural Areas: A Scottish Perspective. Tour. Manag. 2005, 26, 335–346. [Google Scholar] [CrossRef]

- Lamie, R.D.; Chase, L.; Chiodo, E.; Dickes, L.; Flanigan, S.; Schmidt, C.; Streifeneder, T. Agritourism around the globe: Definitions, authenticity, and potential controversy. J. Agric. Food Syst. Community Dev. 2020, 10, 1–5. [Google Scholar] [CrossRef]

- Chase, L.C.; Stewart, M.; Schilling, B.; Smith, B.; Walk, M. Agritourism: Toward a conceptual framework for industry analysis. J. Agric. Food Syst. Community Dev. 2018, 8, 13–19. [Google Scholar] [CrossRef]

- Finizia, A.; Fratto, F.; Galasso, A.; Hausmann, C.; Nucera, M.; Selmi, U. Agriturismo e Multifunzionalità Scenario e Prospettive. Documento Realizzato Nell’ambito del Programma Rete Rurale Nazionale 2014-20; Rapporto 2021; ISMEA: Rome, Italy, 2021. [Google Scholar]

- Fioriti, L.; Montanaro, C.; Nucera, M.; Parmigiani, P.; Ronga, M.; Sarnari, T.; Selmi, U.; Schiano lo Moriello, M. Emergenza COVID–19. IV Rapporto Sulla Domanda e L’offerta dei Prodotti Alimentari Nell’emergenza COVID-19. Documento realizzato nell’ambito del Programma Rete Rurale Nazionale 2014-20; ISMEA: Rome, Italy, 2021. [Google Scholar]

- ISTAT-Istituto Nazionale di Statistica. Struttura e Produzioni Delle Aziende Agricole; ISTAT: Rome, Italy, 2016. [Google Scholar]

- Gargano, G.; Licciardo, F.; Verrascina, M.; Zanetti, B. The Agroecological Approach as a Model for Multifunctional Agriculture and Farming towards the European Green Deal 2030—Some Evidence from the Italian Experience. Sustainability 2021, 13, 2215. [Google Scholar] [CrossRef]

- ISTAT-Istituto Nazionale di Statistica. 6 Censimento Generale Dell’Agricoltura; ISTAT: Rome, Italy, 2010. [Google Scholar]

- Poudel, P.B.; Poudel, M.R.; Gautam, A.; Phuyal, S.; Tiwari, C.K.; Bashyal, N.; Bashyal, S. COVID-19 and its global impact on food and agriculture. J. Biol. Today’s World 2020, 9, 221–225. [Google Scholar] [CrossRef]

- Mastronardi, L.; Cavallo, A.; Romagnoli, L. Diversified Farms Facing the COVID-19 Pandemic: First Signals from Italian Case Studies. Sustainability 2020, 12, 5709. [Google Scholar] [CrossRef]

- Montanari, F.; Arayess, S.; Barbarasa, T.; Clavarino, A.; Ferreira, I.; Mahy, A.; Alicja, A.M.; Christina, S.; Agnieszka-Szymecka, S.A.; Varallo, W.; et al. The response of the eu agri-food chain to the COVID-19 pandemic: Chronicles from the eu and selected member states. Eur. Food Feed. Law Rev. 2020, 15, 336–356. [Google Scholar]

- Di Marcantonio, F.; Solano Hermosilla, G.; Ciaian, P. The COVID-19 Pandemic in the Agri-Food Supply Chain: Impacts and Responses: Evidence from an EU Survey; EUR 31009 EN; Publications Office of the European Union: Luxembourg, 2022; ISBN 978-92-76-49128-6. [Google Scholar] [CrossRef]

- Ascione, E. La diffusione dell’autoconsumo nelle imprese agricole. Riv. Econ. Agrar. 2015, 2, 163–184. [Google Scholar] [CrossRef]

- Phillipson, J.; Gorton, M.; Turner, R.; Shucksmith, M.; Aitken-McDermott, K.; Areal, F.; Cowie, P.; Hubbard, C.; Maioli, S.; McAreavey, R.; et al. The COVID-19 Pandemic and Its Implications for Rural Economies. Sustainability 2020, 12, 3973. [Google Scholar] [CrossRef]

- Cavallo, C.; Sacchi, S.; Carfora, F. Resilience effects in food consumption behaviour at the time of COVID-19: Perspectives from Italy. Heliyon 2020, 12, e05676. [Google Scholar] [CrossRef]

- Grunert, K.G.; De Bauw, M.; Dean, M.; Lähteenmäki, L.; Maison, D.; Pennanen, K.; Sandell, M.A.; Stasiuk, K.; Stickel, L.; Tarrega, A.; et al. No lockdown in the kitchen: How the COVID-19 pandemic has affected food-related behaviours. Food Res. Int. 2021, 150, 110752. [Google Scholar] [CrossRef] [PubMed]

- Tendall, D.; Joerin, J.; Kopainsky, B.; Edwards, P.; Shreck, A.; Le, Q.; Kruetli, P.; Grant, M.; Six, J. Food system resilience: Defining the concept. Glob. Food Secur. 2015, 6, 17–23. [Google Scholar] [CrossRef]

- Brzustewicz, P.; Singh, A. Sustainable Consumption in Consumer Behavior in the Time of COVID-19: Topic Modeling on Twitter Data Using LDA. Energies 2021, 14, 5787. [Google Scholar] [CrossRef]

- Li, S.; Kallas, Z.; Rahmani, D.; Gil, J.M. Trends in Food Preferences and Sustainable Behavior during the COVID-19 Lockdown: Evidence from Spanish Consumers. Foods 2021, 10, 1898. [Google Scholar] [CrossRef] [PubMed]

- Béné, C. Resilience of local food systems and links to food security—A review of some important concepts in the context of COVID-19 and other shocks. Food Secur. 2020, 12, 805–822. [Google Scholar] [CrossRef] [PubMed]

- Filippini, R.; Marraccini, E.; Lardon, S. Contribution of periurban farming systems to local food systems: A systemic innovation perspective. Bio-Based Appl. Econ. 2021, 10, 19–34. [Google Scholar] [CrossRef]

- Gössling, S.; Scott, D.; Hall, M. Pandemics, tourism and global change: A rapid assessment of COVID-19. J. Sustain. Tour. 2021, 29, 1758708. [Google Scholar] [CrossRef]

- A Farm to Fork Strategy for a Fair, Healthy and Environmentally-Friendly Food System; Communication from the Commission 381 Final; EU Publications Office: Luxembourg, 2020.

- Bock, A.; Bontoux, L.; Rudkin, J. Concepts for a Sustainable EU Food System; RC126575; EU Publications Office: Luxembourg, 2022; ISBN 978-92-76-43727-7. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

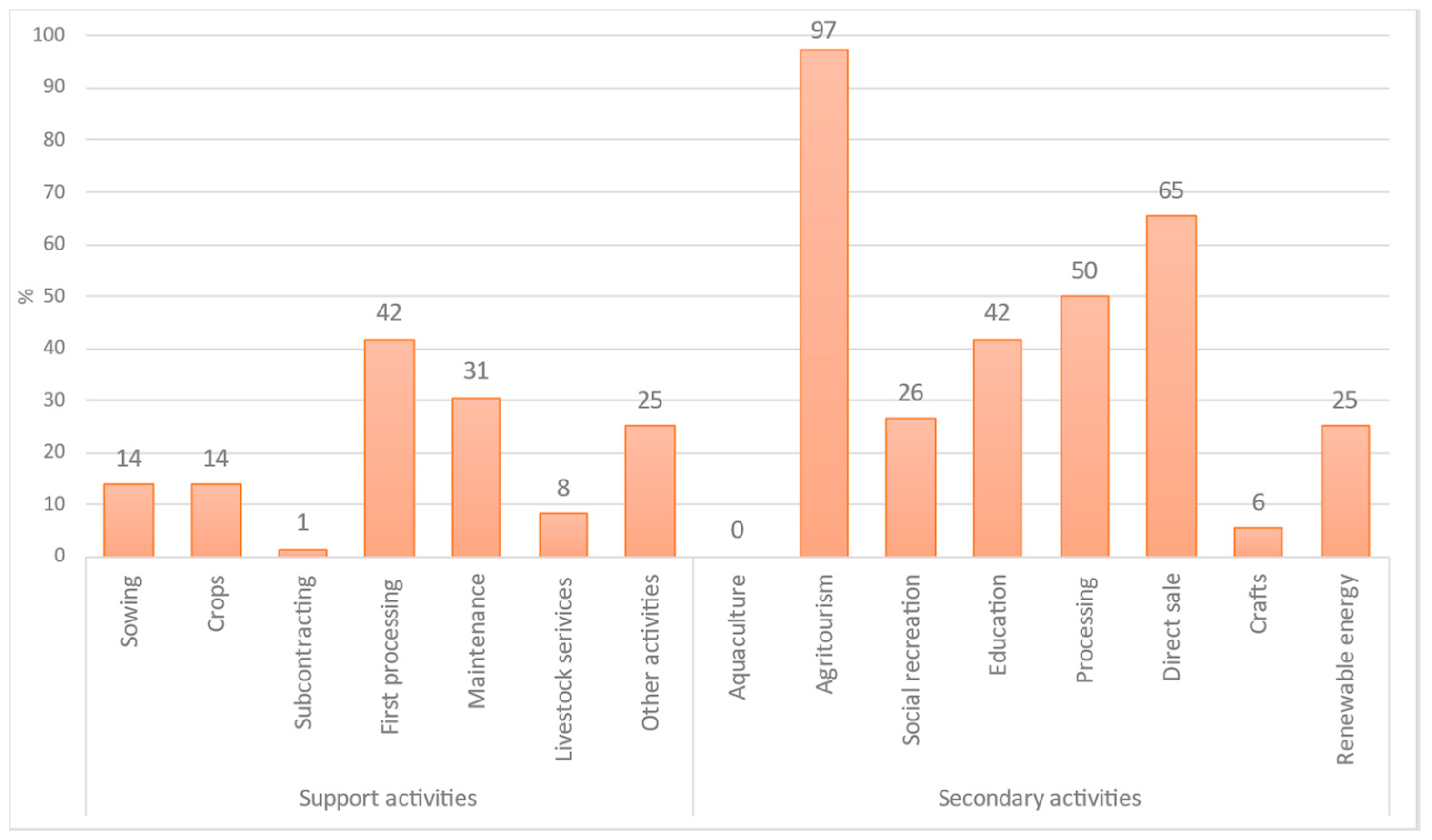

| Support Activities | Secondary Activities |

|---|---|

|

|

| 1–1.99 | 2–4.99 | 5–9.99 | 10–19.99 | 20–29.99 | 30–49.99 | 50–99.99 | 100 and More | DK/NO | |

|---|---|---|---|---|---|---|---|---|---|

| North | 4 | 8 | 11 | 5 | 1 | 3 | 3 | 3 | 1 |

| Centre | 4 | 6 | 7 | 3 | 4 | 0 | 6 | 4 | 1 |

| South | 0 | 0 | 6 | 8 | 1 | 1 | 3 | 6 | 0 |

| Total | 8 | 14 | 24 | 17 | 7 | 4 | 11 | 10 | 3 |

| Sales Channels | Pre COVID | Post COVID |

|---|---|---|

| On-farm consumption * | 47 | 48 |

| Direct sales on the farm | 42 | 31 |

| Direct sale outside the farm | 25 | 19 |

| Sales to wholesalers/brokers | 48 | 40 |

| Large-scale retail sales | 5 | 6 |

| E-commerce-online sales | 19 | 25 |

| Sale to cooperatives/consortia/producer organizations | 45 | 48 |

| Specialized retailers/restaurants | 24 | 18 |

| Other | 38 | 57 |

| Agritourism Services | Values in % | Agricultural Products | Values in % |

|---|---|---|---|

| New customers were acquired | 44 | New customers were acquired | 37 |

| Established customers increased demand | 20 | Established customers increased demand | 8 |

| Established customers decreased demand | 18 | Established customers decreased demand | 20 |

| Established customers left demand unchanged | 18 | Established customers left demand unchanged | 35 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zanetti, B.; Verrascina, M.; Licciardo, F.; Gargano, G. Agritourism and Farms Diversification in Italy: What Have We Learnt from COVID-19? Land 2022, 11, 1215. https://doi.org/10.3390/land11081215

Zanetti B, Verrascina M, Licciardo F, Gargano G. Agritourism and Farms Diversification in Italy: What Have We Learnt from COVID-19? Land. 2022; 11(8):1215. https://doi.org/10.3390/land11081215

Chicago/Turabian StyleZanetti, Barbara, Milena Verrascina, Francesco Licciardo, and Giuseppe Gargano. 2022. "Agritourism and Farms Diversification in Italy: What Have We Learnt from COVID-19?" Land 11, no. 8: 1215. https://doi.org/10.3390/land11081215

APA StyleZanetti, B., Verrascina, M., Licciardo, F., & Gargano, G. (2022). Agritourism and Farms Diversification in Italy: What Have We Learnt from COVID-19? Land, 11(8), 1215. https://doi.org/10.3390/land11081215