1. Introduction

In most sub-Saharan countries, people with political and economic power do not want to pay taxes, and tax compliance is low for other people [

1,

2,

3]. On average, property tax contributed to less than 0.5% of the gross domestic product (GDP) in African countries [

4]. Tanzania—specifically, Zanzibar—is in a similar situation. Property taxes are not a significant source of revenue for public goods because of broad exemptions, lack of accuracy and equity in valuation, low tax compliance rates, and weak administration and enforcement systems [

5,

6,

7,

8,

9,

10,

11,

12].

Therefore, valuation systems and administrative capacity are crucial in determining the importance of property tax as a revenue generator in African countries. First, the government should assess buildings and improvements to reflect market values. To do so, the market price data collection and valuation system should be well established. This increases the values on the valuation rolls divided by the real market values of properties (called “valuation ratio” by Kelly and Musunu [

5]). Second, to increase the tax revenue collected over the total tax liability (called “collection ratio” by Kelly and Musunu [

5]), the government should improve property tax administrative capacity to collect property taxes in a cost-effective manner. These solutions are also commonly suggested for developing countries [

13,

14,

15]. In this study, we focus on valuation-related issues because property taxes based on the estimated taxable value cannot be efficiently and equitably imposed in the absence of a well-established valuation system.

Tanzania has prioritized the improvement of its valuation system since 1993 [

5]. In 1993, the Tanzanian government implemented property tax reform to enhance property tax revenue. This tax reform adopted the valuation-based strategy that improved the capacity to estimate the values of buildings and land improvements for tax purposes. This reform aimed to increase the valuation ratio by improving the valuation system. In general, Tanzania has relied on the flat rating system, in which the flat tax amount per building, adjusted according to location, size, and building use, is applied to taxable buildings and improvements. The 1993 Tax Reform introduced the ad valorem tax system, wherein tax amounts for each taxable building are determined based on the valuation. However, three problems arise. First, according to Kelly and Musunu [

5], despite this policy effort, taxes are currently levied under this system on only a third of the country’s properties in Dar Es Salaam, Tanzania. Moreover, the tax amount in the area-based (flat rating) tax system may be approximately 50% lower than that in the ad valorem tax system for a given property. Second, Tanzania struggles to build market value data, and buildings are valued for property tax assessment through a cost replacement approach. Third, the Tanzanian government relies heavily on the private sector for valuation because of its own lack of valuation capacity. In this system, valuers in the private sector estimate each building’s taxable value.

Compared to Tanzania, the Zanzibar government faces a more severe problem. In Zanzibar, there is no formal property valuation system. Taxes are levied using self-declared information regarding building values. Owing to the lack of capacity, the Zanzibar government cannot verify whether the values declared by building owners reflect the properties’ actual values. Therefore, taxpayers have a strong incentive to avoid their tax burden by reporting lower self-declared property values. The Zanzibar government should thus establish a formal valuation system for property taxes.

A well-established and functioning property valuation system is essential for creating sustainable revenue sources and requires the following:

Proximity to market prices (transaction prices should be used);

Objective consistency (subjectivity in valuation should be minimized);

Fairness (a government body must be in charge);

Cost efficiency (time and costs must be minimized through objective assessment standards and computerization); and

Convenience of operation (must be easy to operate by public officers at all levels).

It is crucial to reflect market value in the taxable value to facilitate revenue enhancement. According to the 2008 Property Tax Act (PTA), the Zanzibar government has recognized that a property’s taxable value should reflect the market value of property taxes. In 2008, the central government in Zanzibar established a legal foundation in terms of the PTA. Section 8 of this act states, “The taxable value of a property shall be the property’s market value, or where the market value cannot be ascertained, the rateable value shall be the replacement cost”. However, the 2008 PTA cannot be implemented without a well-functioning valuation system. In this situation, property taxes levied based on an outdated law cannot be considered a sustainable revenue source for providing local public services.

Problems related to valuation systems are common across African countries. About 75 percent of African 51 countries with property taxes have adopted the discrete individual value-based property tax system. However, it is inefficient in the following aspects: number of valuers, valuation capacity and moral capability of valuers, and revaluations or unacceptably long intervals between revaluations [

16,

17,

18,

19,

20]. Cheloti and Mooya argued that the valuation system in African countries is flawed because it lacks quality property market data [

16].

Their solutions are straightforward. Governments should improve their property valuation (buildings and improvements, in our case) capacity to reflect the market value. Therefore, it is crucial for governments to increase the number of valuers and improve their valuation and moral capacities. Moreover, as suggested by Cheloti and Mooya [

16], governments should build a database for property market transactions to overcome problems of incomplete and unreliable property market information. However, the challenge is that it takes time for developing countries to collect market transaction data and build a better valuation system. Thus, most African countries have adopted the discrete individual valuation system, which relies on each valuer’s capacity. According to McCluskey and Franzsen [

18], this system is ineffective when a few qualified valuers value many taxable properties in a limited period, a problem observed in most African countries, including Uganda, Tanzania, and Zambia. Therefore, they recommended the following three alternatives: (1) an area-based valuation method, (2) a flat rating method, and (3) a value banding method. Under the area-based valuation method, properties are valued by multiplying the area of land and buildings by the value per unit area. The flat rating method applies a flat rate tax amount per property, according to its use, size, and location. For example, residential properties in a specific area have the same tax amount per unit area. Thus, this method is similar to the area-based valuation method. The value banding method has been implemented in Great Britain since 1993 and in Ireland since 2013 [

18,

21]. In this system, there are several valuation bands (or groups), with each band having a range of values. All properties are classified in the valuation band according to an estimate of their capital or rental value [

18,

20,

22]. Bahl [

23] and Brzeski [

24] argued that the area-based method impedes equity because it does not account for locational values. Therefore, adjusting the flat property value or tax amount for each building is crucial for reflecting locational values such as area, road accessibility, and distance to desirable or undesirable facilities. In this context, the value banding method is the most viable option. However, in this method, the capital (market) or rental values for each property should first be estimated using market sales data, annual rental payment data, or value-related data. Thus, this method may be inappropriate if the property market is flawed, and property sales data are unavailable.

In this study, we propose a new valuation method derived from the area-based method by considering the case of Zanzibar. However, there are three main differences between the two methods. First, the new valuation method further subdivides the defined region according to valuers’ knowledge and experience. Unlike the individual discrete value-based method, this method does not require many qualified valuers. The more subdivided the region, the easier it is to evaluate properties that reflect market prices. Second, property values are determined based on a range of values in the given sub-region. If market data are unavailable, the property values in the sub-region are estimated using the median values of the range. The estimated property values reflect the accurate market price when this range is updated annually. Third, to overcome the problems related to locational values, we introduce the price ratio table. This table can be generated using an annual survey of property values. If a yearly survey cannot be conducted, this table can be created using expert valuers’ knowledge and experience. It does not require a large number of valuers. The price ratios in the table are determined using the property characteristics associated with locational values. Therefore, the final property value is calculated by multiplying the property value (=property value per unit area × total area) by the price ratio. This method could be considered a hybrid valuation method combining the traditional area-based and value-based methods. Another benefit of this hybrid method is the application of the simple mass valuation system to an area-based system. This is necessary because in Tanzania, individual property valuations are conducted by private sector valuers under the ad valorem method. However, too many properties are valued under time and resource restrictions. Kelly and Musunu [

5] stated that the mass valuation system could address problems such as the backlog of out-of-date and incomplete valuations owing to individual valuations. The proposed hybrid valuation method is useful in the following scenarios: when (1) the property market does not function well; (2) quality property sales data are not available; (3) there are few qualified valuers; and (4) the capacity and resources for valuation are limited.

In this study, we focus on Zanzibar for two reasons. First, Zanzibar faces all of the abovementioned circumstances. Second, the government only estimates the values of buildings for property taxes. Therefore, locational values are not considered because of nationalized land. For property taxes to be a revenue generator, we should include locational values in the taxable values. The implementation of the traditional area-based valuation method is limited in Zanzibar, as it does not properly reflect the locational values. Therefore, we examine the case of Zanzibar to determine a better valuation system. In the short term, we propose a detailed cost-effective area-based method with a mass valuation system. This method can also be applied to Tanzania or other African countries with similar policy environments.

2. The 2008 Property Tax Act (PTA) and Its Policy Issues

In Zanzibar, property taxes are levied based on an outdated law, the 1934 Ordinance, which is currently not legally enforceable. Therefore, local governments cannot force taxpayers to pay these taxes, making tax compliance less likely. Furthermore, people have the incentive to pay less taxes by lowering the tax base. It is difficult for residents of developing countries to avoid the property tax burden, as they cannot hide their properties and the corresponding market values. Owing to such visibility, property taxes are critical for funding local services. However, in Zanzibar, property taxes are levied on self-declared information regarding building values. Thus, the tax base is likely to be underdetermined.

Table 1 shows that property tax revenues account for only 2.7% of the total local revenues. Moreover, the block grant from the central government contributes to 49.2% of the total revenues of the urban municipal council (UMC) in Stone Town in Zanzibar. Revenues from local sources are primarily received in terms of parking fees, trading licenses, sewerage, sanitation charges, and other sources. Therefore, property taxes play a limited role in funding local services because of low compliance rates and inaccurate valuations.

In 2008, Zanzibar’s central government prepared the 2008 PTA to secure sustainable property tax revenues that facilitate the effective provision of local public goods. The main features of the 2008 PTA are as follows:

The central government sets the property tax rate and collects tax revenue because local governments lack the capacity to do so;

Property tax rates differ depending on the type of property—0.1% for residential and 0.2% for commercial properties; and

Property tax exemptions are wide-ranging, with problematic exemptions for owner-occupied residential properties and properties with market values exceeding 50 million TZS.

The 2008 PTA is subject to some problems based on the coverage ratio of the property tax. Owner-occupied residential properties comprise a large proportion of properties. High-valued properties have market values exceeding 50 million TZS (about 21,710 U.S. dollars as of January 2022). This threshold seems high when considering the GDP per capita in Tanzania (1,552,000 TZS, approximately 674 U.S. dollars as of January 2022). Accordingly, these exemptions narrow the tax base significantly. Moreover, regions with few high-value properties may not generate enough revenue to fund local public services. In such cases, the revenue gap between wealthy and poor regions widens. In addition, under the 2008 PTA, the market value represents the values of buildings and improvements because the government owns the land, and locational values are not considered in their valuation. Therefore, the tax base only reflects the values for a property’s physical characteristics. Additionally, the tax base shrinks because of depreciation. Thus, eliminating tax exemptions is essential in broadening the tax base and solving these problems. Furthermore, the locational values should be considered when valuing buildings and improvements.

Although policy efforts are required to eliminate the tax exemptions, the 2008 PTA is an improvement over the outdated law in terms of effective property tax. However, this law remains unimplemented because of the absence of a formal property assessment system. As property taxes are levied based on the estimated tax that reflects market values (unlike other taxes, such as income taxes), the establishment of a property assessment system is the most urgent requirement for the imposition of property taxes in Zanzibar. However, the central government owns the land; according to Section 3 of the 2008 PTA, taxable properties are defined as “any building, structure, or erection of an immovable nature”. This presents challenges in the realization of fair taxation. Owing to nationalized land, neither the land transaction market nor land market prices exist. As the building value estimated by the replacement cost method—such as in Tanzania—does not innately capture the locational value (land value), levying property taxes on building values could impede vertical equity. For example, the tax burden could be similar for properties with different locational or usage values. Thus, to improve equity, it is crucial to include locational values in the calculation of taxable values.

3. Materials and Methods

In Zanzibar, there is no formal valuation system for property tax; however, valuation methods are used for other taxes, such as the inheritance tax. The current valuation practices in Zanzibar recognize and include the value of the underlying land in property valuation. For example, government inheritance valuation reports state that “Land is legally considered to have got value not only to the government but also to individual members of the society”. This implies that land value is already considered in the valuations of inherited properties. In addition, Section 18 of the Land Tenure Act of 1992 stipulates that there should be no restriction on selling a right of occupancy. It implies that the locational or usage values (or right of occupancy value) of the land can be included in the building value, resulting in fairer and more balanced property taxation.

The simplest property value assessment method is its comparison with the market prices of similar properties that have been recently traded in the surrounding area, or the addition of land value to the building value as estimated by the replacement cost method. However, it is limited by the access to market price data. In this case, the only possible valuation method is the area-based method. However, the traditional area-based method may not account for factors such as the quality of buildings and improvements or access to amenities. This method results in inequality because, in a given region, the same flat tax amount is assigned regardless of the actual market value [

15]. This issue can be resolved by adjusting the flat tax amount for the given region, based on the locational values. Through this standard adjustment process, the taxable values approach the market values, improving equity. Similar examples of a hybrid valuation system can be found in other countries such as Chile, Indonesia, and Romania [

15,

25]. However, the hybrid valuation method proposed in this study may be better, as the flat tax amount is adjusted based on several characteristics that affect locational values. In this adjustment process, we suggest using the valuers’ knowledge and experience because the estimated taxable values are much closer to the property values, which include locational values. The assessment of buildings and improvements considering locational values is presented below.

3.1. Land Valuation Method

For land valuation, a mass assessment method with emphasis on both horizontal and vertical equity as well as cost efficiency would encompass two main components:

The first component, a reference price for properties, comprises one of two forms: either reasonable prices of selected reference (sample) lots that are representative of the stratification of prices in a certain region, or a range of values for each sub-region in the taxable area. The second option already exists in the form of a land value table in Zanzibar (shown in

Table 2 below) and is applied in valuation for other purposes, such as inheritance, price determination, and transfer fees.

Table 2 shows the upper and lower ranges of land prices of properties that are categorized primarily by location and some other factors, including road accessibility and level of planning.

Dividing the whole region into various subsections with different price levels provides a good starting point for individual valuers and serves as the basis for systematic mass valuation. However, the table needs to be further developed because of the following reasons:

The price ranges for each location are too large.

The exact boundaries for each location are ambiguous, enabling inaccurate and inefficient use.

As the taxable areas are categorized without a set of constant criteria, there is confusion regarding allocation of taxable properties.

For mass assessment, as shown in

Table 3, each sub-region should be specifically determined using each area’s boundaries. Additionally, the areas must be categorized narrowly so that properties in the same area share a common price level and are similarly affected by the same price determinant factors. The subdivision of the areas should be determined by expert valuers who are familiar with the price ranges and determinants for the entire Zanzibar region.

Once the areas are categorized and the price ranges are set for a given area, a simple land price ratio table can be used to calculate the price of each individual land in each location. In the next step, the land value is assessed by considering the street type, level of planning, and other important price determinants. The land price ratio table is a simplified land price assessment table that allows the user to easily derive individual land prices. It is a matrix of scales with land characteristics extracted from multiple regression analyses in their original form. The prices of sample lands are analyzed for each area with similar land characteristics, after which the price determinants are extracted and correlation analysis is performed to create a land assessment model using the model’s parameter values.

In the short run, a complex land price ratio table is unnecessary for Zanzibar. One or two land price ratio tables including the most important price determinants (for example, road access or level of planning), as judged by the Valuation Division or a relevant government body, would suffice. The values (multipliers) within the land price ratio table would ideally be derived through regression analysis of existing price data such as transaction data, valuation precedents, or valuations of sample properties. However, if there are insufficient accurate price data for the above analysis, a price ratio table can be created through discussions among existing expert valuers.

Table 4 and

Table 5 present examples of such land price ratio tables.

The land price ratio table allows for a systematic valuation of all properties based on their area and one or two of the most important property characteristics (or more, if deemed necessary).

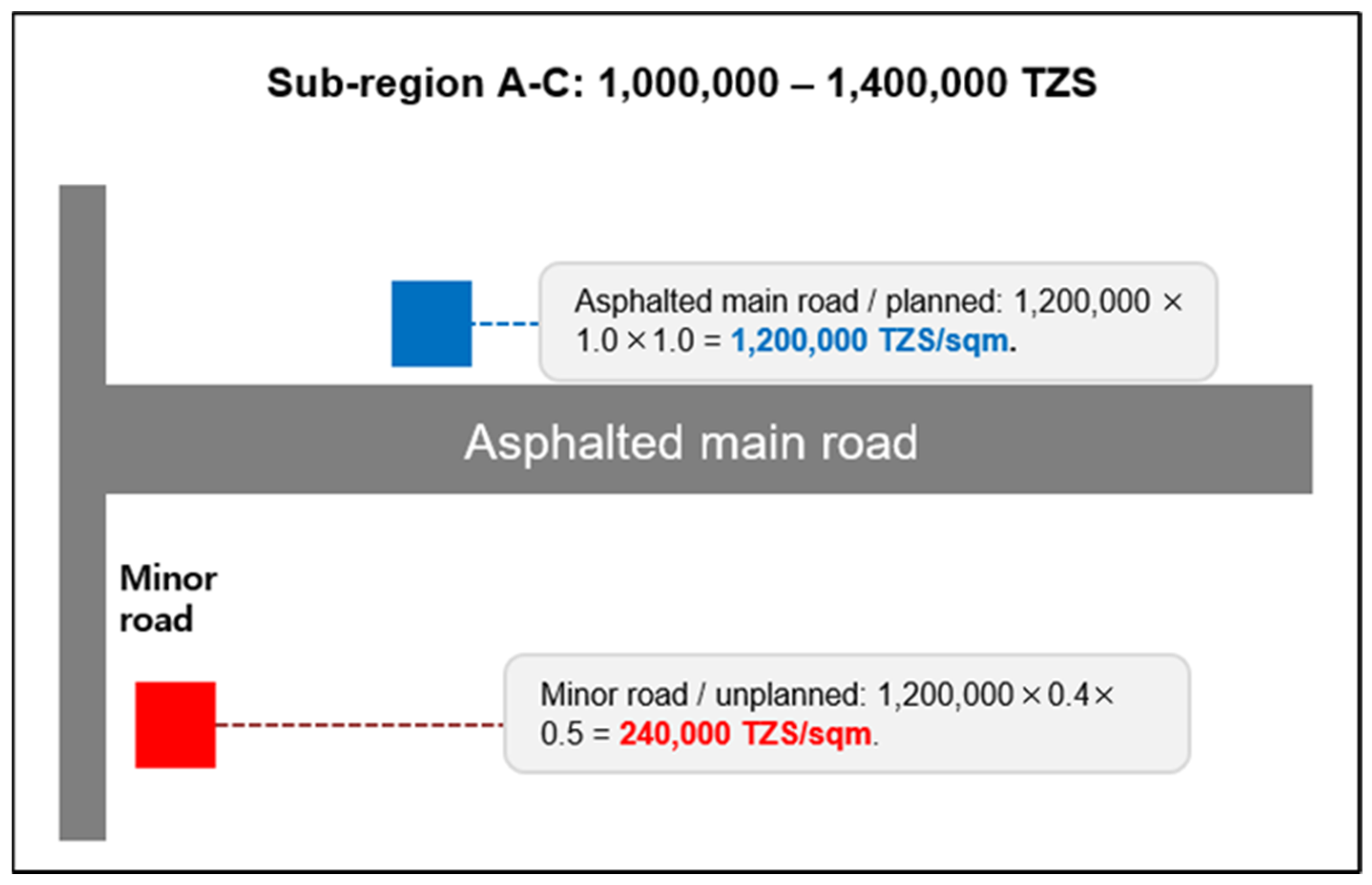

The final value of the individual property is derived as follows. Let us assume that, as shown in

Figure 1, the taxable value of Property A (located within sub-region A-C, has access to a minor road, is unplanned) must be derived through the mass assessment model. According to the land value in

Table 3, the value range for sub-region A-C for this year is surveyed as between 1,000,000 and 1,400,000 TZS, with the median value being 1,200,000 TZS. According to the land price ratio tables, the multiplier for access to a minor road is 0.4, whereas that for an unplanned lot is 0.5. Thus, if the only two price determinants for the region are road accessibility and level of planning, the final taxable value would be 1,200,000 × 0.5 × 0.4 = 240,000 TZS. With the inclusion of more price determinants and further classification of sub-regions, the model becomes more precise and objective. Although not as accurate as specific valuations, it effectively derives fair values en masse, emphasizing vertical and horizontal assessment equality.

3.2. Building Valuation Method

A cost approach based on objective reproduction costs can be applied for building valuation. This would include a more detailed building unit price index and depreciation tables based on the years that have elapsed and building conditions. The assessment of building value involves two steps. First, objective building price determinants must be established, followed by the creation of a more detailed building unit price index. The building unit price index is created by examining blueprints and construction statements of actual construction cases. The index would contain the unit (reproduction) costs for standard buildings that are representative of each building type and material. The information shown in

Figure 2 must be contained in the building unit price index.

Table 6 and

Figure 3 show an example of such an index. Standard unit costs would be required for each classification number, comprising the most important determinants of building price, such as usage, main structure, or building grade.

For example, as shown in

Figure 3, the standard unit cost for an average-grade, single-residential, cement block residential building (classification no. 1-1-2) would be 6.92 USD/m

2, with a durable life of 20 years.

4. Results and Discussion

Zanzibar is currently experiencing rapid urbanization. Local governments need stable and reliable revenue sources to meet the needs of residents and firms for local public services, and property taxation is one of the best options available for Tanzania and other African countries. However, property taxes currently fail to generate sufficient revenues to provide adequate local public services. Therefore, the poor quality of local public goods could negatively affect tax compliance [

26].

To provide a desirable level of local public goods, the Tanzanian government introduced the ad valorem valuation system. However, this method is not widely used because of the lack of market transaction data. Additionally, when using the ad valorem valuation method, individual property valuations are heavily based on a parcel-by-parcel valuation used by private sector valuers. Thus, although the replacement cost method is relatively widely used, it does not account for locational values when valuing buildings and improvements. In Zanzibar, an important agenda for effective property taxation would be the establishment of a formal valuation system. Notwithstanding the relevance of the area-based method in this context, it may not be desirable because the same tax amount is imposed throughout the same region (or zone), thereby impeding equity. To avoid this problem, it is critical to adjust each property’s tax amount based on locational values. The simple and systematic mass assessment model proposed in this study can be used to derive the locational values of all taxable properties if the following hold: (1) the taxable areas are divided into sub-regions based on land value stratification; (2) land value ranges are set for each sub-region; (3) land value determinants are identified; and (4) land price ratio tables for the identified land value determinants are created. The accuracy of assessments depends on how the locational values are assessed. In this context, individual valuers play an essential role in capturing locational values because their knowledge and experience are helpful in dividing the area targeted for property tax assessment into several regions, thereby reducing the intraregional variance in land values. This hybrid area-based method can be beneficial for Tanzania and Zanzibar.

Eventually, in the long run, a systematic mass assessment of all property prices should be conducted by ensuring the following attributes: (1) thorough characteristics surveys for all properties; (2) accurate valuation of reference lots based on the market transaction data; and (3) a well-maintained standard comparison table. This valuation method is commonly used in developed countries and its implementation requires a mature property market and well-prepared system for transaction data collection.

A question arises as to why the land value should be reflected in the values of buildings and improvements. Historically, the land value tax has been considered as a benefit tax [

27]. George [

28] first argued that a land tax promotes fairness because the land value is affected by the community’s economic activities and not by individual efforts. The study argues that a land tax is efficient because it does not distort economic decisions. Thus, in traditional theory, taxing only land is more desirable because taxes on buildings discourage investment in properties, whereas taxes on land provide an incentive for efficient land use. Furthermore, the tax on buildings can be viewed as a capital tax. As capital is mobile, unlike land, taxes on capital distort its allocation. Oates and Schwab [

29] supported the argument proposed by George [

28]. They showed that land taxes do not influence economic decisions, the tax burden falls entirely on landowners, and a land tax does not affect the form or timing of development of unused land parcels. In addition, Oates and Schwab [

30] and Plassmann and Tideman [

31] empirically showed that a land tax does not affect economic development. In this context, Dye and England [

32] argued that land value taxation should be considered based on theoretical discussion and empirical evidence, even though there exist constitutional, statutory, or administrative problems.

Although a land tax can be viewed as a benefit tax, most countries levy taxes on both land and buildings. If so, it must be evaluated whether it is desirable to levy taxes on buildings. Hoyt [

33] and Krelove [

34] showed that taxing buildings is important to provide an optimal level of local public services because it covers the increased cost of providing local public services to a new household that joins a community. However, Wilson [

35] argued that taxing buildings alone only partially accounts for the increased costs. Therefore, taxing both land and buildings is necessary; however, considering an efficient property tax, the tax rate for land can be larger than that for buildings. In Zanzibar, this argument can be perceived as reflecting the land values in the values of buildings and improvements.

Finally, as Kelly and Musunu [

5] argued, property tax reforms should be comprehensive. This implies that the government should continue to make efforts to increase the coverage and collection ratios. First, the exemption of property tax should be limited. Governments should design a property tax system with a lower tax rate and broader tax base. As all property owners benefit from increases in public investment, it is reasonable to levy a property tax on all properties, with few exceptions. Eliminating tax exemptions will reduce efficiency loss and improve equity. If the tax base is expanded, the property tax rate can be lowered to collect the target level of tax revenue under the 2008 PTA. Hence, lowering property tax rates may reduce tax resistance. Second, the government should improve the capacity to bill and collect tax revenue. Administrative capacity improvements can contribute to property tax revenues that are adequate for providing local public services in Zanzibar. This result is more likely when the valuation system simultaneously improves and reflects locational values.

While our proposed valuation method reduces the gap in the literature, the scope of our study is limited because of the lack of data. In the future, it is important to test whether the new hybrid valuation method is a feasible policy option using property market data. To overcome the data limitations, researchers can conduct surveys to examine how the new hybrid valuation method affects the taxable values. Providing empirical evidence about how locational values are captured in reality will be valuable for successful implementation [

36]. Another limitation of this study is that the new hybrid valuation method may not be generalizable because of the heterogeneity of policy environments across African countries, which presents a scope for further research.

{kind=link}

{kind=link}

{kind=link}