Land-Based Financing Elements in Infrastructure Policy Formulation: A Case of India

Abstract

1. Introduction

2. Method

3. Indian Project Experiences of Land-Based Financing

4. Elements of Land Monetization in Key Legislation and Policies in India

5. Comparison of Policies

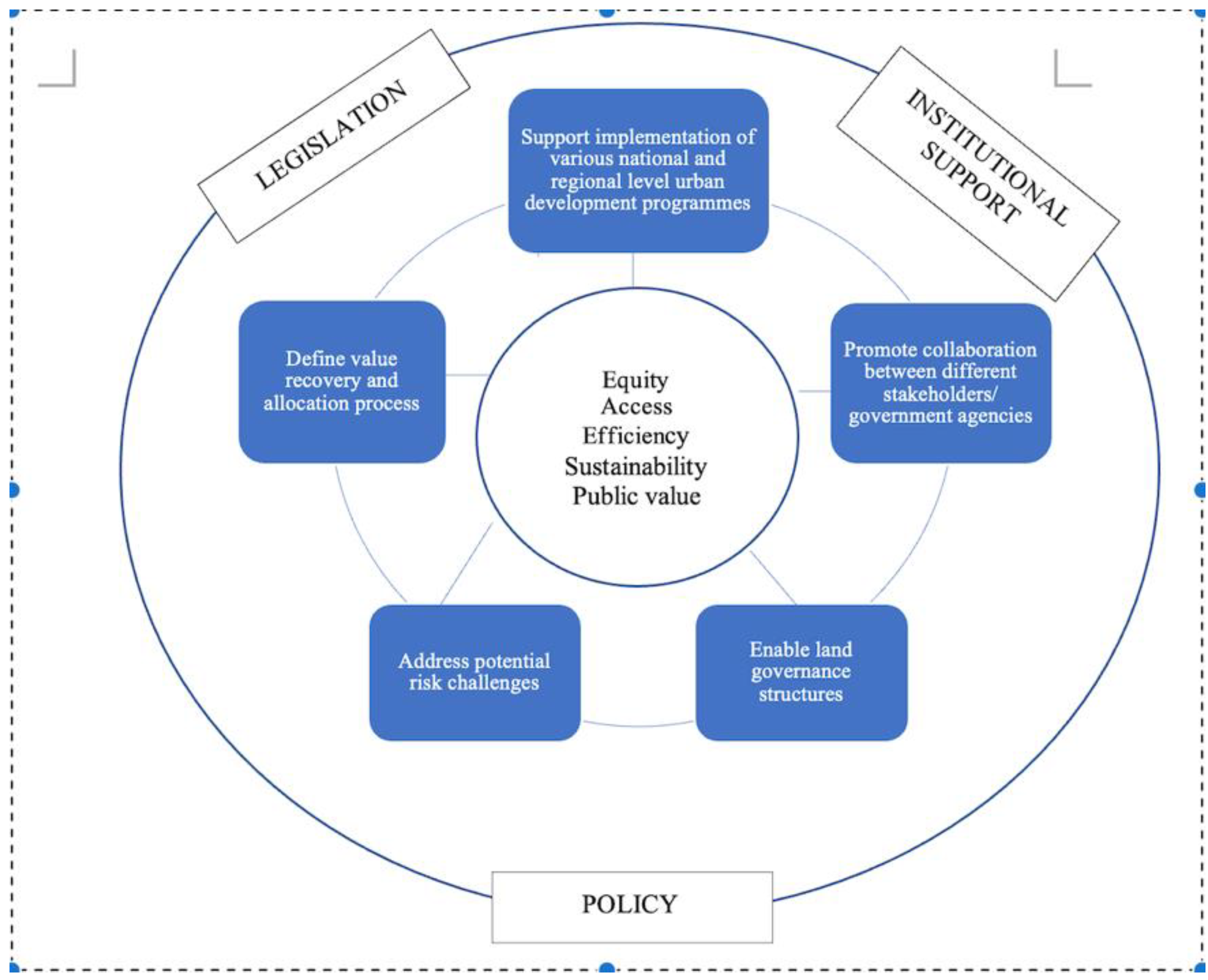

6. Policy Implications

7. Summary and Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Suzuki, H.; Cervero, R.; Iuchi, K. Transforming Cities with Transit. Transit and Land-Use Integration for Sustainable Urban Development, 1st ed.; World Bank: Washington, DC, USA, 2013. [Google Scholar]

- Bahl, R.W.; Linn, J.F.; Wetzel, D.L. Financing Metropolitan Governments in Developing Countries, 1st ed.; Lincoln Institute of Land Policy: Washington, DC, USA, 2013. [Google Scholar]

- Chakravorty, S. A new price regime: Land markets in Urban and Rural India. Econ. Polit. Wkly. 2013, 48, 45–54. [Google Scholar]

- Singh, S. Land Acquisition in India: An Examination of the 2013 Act and Options. J. L. Rural Stud. 2016, 4, 1. [Google Scholar] [CrossRef]

- United Nations. SDG Indicators—SDG Indicators. 2017. Available online: https://unstats.un.org/sdgs/indicators/indicators-list/ (accessed on 24 July 2020).

- Besley, T.; Burgess, R. Land reform, poverty reduction, and growth: Evidence from India. Q. J. Econ. 2000, 2, 389–430. [Google Scholar] [CrossRef]

- UN-Habitat. Affordable Land and Housing in Latin America and the Caribbean, 1st ed.; UN-Habitat: Nairobi, Kenya, 2011; Available online: https://unhabitat.org/affordable-land-and-housing-in-latin-america-and-the-caribbean-2 (accessed on 20 January 2021).

- Munoz-Gielen, D. Improving Public-Value Capturing in Urban Development. Innov. L. Prop. Tax. 2011, 150–170. Available online: https://www.researchgate.net/publication/285574748_Improving_public-value_capture_in_urban_development (accessed on 15 December 2020).

- Gandhi, S.; Phatak, V.K. Land-based Financing in Metropolitan Cities in India: The Case of Hyderabad and Mumbai. Urbanisation 2016, 1, 31–52. [Google Scholar] [CrossRef]

- Rics. RICS Valuation—Professional Standards (Red Book). Basis of Value; Royal Institution of Chartered Surveyors: London, UK, 2012; Available online: https://www.rics.org/globalassets/rics-website/media/upholding-professional-standards/sector-standards/valuation/rics-valuation--global-standards-jan.pdf (accessed on 15 December 2020).

- George, H. Progress and Poverty (Edited and Abridged for Modern Readers by Bob Drake, 2006); Aziloth Books: London, UK, 1879. [Google Scholar]

- Smolka, M.O. Implementing Value Capture in Latin America: Policies and Tools for Urban Development Policy Focus Report Series; Lincoln Institute of Land Policy: Cambridge, MA, USA, 2013. [Google Scholar]

- Berrisford, S.; Cirolia, L.R.; Palmer, I. Land-based financing in sub-Saharan African cities. Environ. Urban 2018, 1, 35–52. [Google Scholar] [CrossRef]

- Shatkin, G. The real estate turn in policy and planning: Land monetization and the political economy of peri-urbanization in Asia. Cities 2016, 53, 141–149. [Google Scholar] [CrossRef]

- Ramachandraiah, C. Making of Amaravati. Econ. Polit. Wkly. 2016, 51, 68–75. [Google Scholar]

- Wolf-Powers, L. Reclaim Value Capture for Equitable Urban Development. Metropolitics 2019. Available online: https://metropolitics.org/Reclaim-Value-Capture-for-Equitable-Urban-Development.html (accessed on 20 January 2021).

- Immergluck, D. Large redevelopment initiatives, housing values, and gentrification: The case of the Atlanta beltline. Urban Stud. 2009, 46, 1723–1745. [Google Scholar] [CrossRef]

- Van der Veen, M.; Altes, W.K.K. Urban development agreements: Do they meet guiding principles for a better deal? Cities 2011, 28, 310–319. [Google Scholar] [CrossRef]

- Peterson, G.E. Unlocking Land Values to Finance Urban Infrastructure; The World Bank: Washington, DC, USA, 2008. [Google Scholar]

- Nallathiga, R. Urban infrastructure development in India: Resource requirements and mobilization methods. IUP J. Infrastruct. 2010, 8, 26–37. [Google Scholar]

- RICS Research. Real Estate and Construction Professionals in India by 2020; RICS Research: London, UK, 2011. [Google Scholar]

- RICS Research. Bridging the Gap; RICS Research: London, UK, 2020. [Google Scholar]

- Kelkar, D.V. Report of the Committee on Revisiting and Revitalising Public Private Partnership model of Infrastructure; Government of India: New Delhi, India, 2015.

- Balakrishnan, S. Highway urbanization and land conflicts: The challenges to decentralization in India. Pac. Aff. 2013, 86, 785–811. [Google Scholar] [CrossRef]

- Kulshreshtha, R.; Kumar, A.; Tripathi, A.; Likhi, D.K. Critical Success Factors in Implementation of Urban Metro System on PPP: A Case Study of Hyderabad Metro. Glob. J. Flex. Syst. Manag. 2017, 18, 303–320. [Google Scholar] [CrossRef]

- Chaudhuri, S. Impact of privatisation on performance of airport infrastructure projects in India: A preliminary study. Int. J. Aviat. Manag. 2011, 1, 40. [Google Scholar] [CrossRef]

- Sahoo, K. Deregulation in development project: A case of Dhamra port project in Odisha. Ocean Coast. Manag. 2014, 100, 151–158. [Google Scholar] [CrossRef]

- Sharma, K.K.; Misra, S.K.; Singla, A.K. Role of Public Private Partnership in Bus Terminals: A Case Study of Punjab. Think India 2019, 22, 116–128. [Google Scholar] [CrossRef]

- Germán, L.; Bernstein, A.E. Land value capture. Policy Br. 2018, 2016–2019. Available online: https://www.lincolninst.edu/sites/default/files/pubfiles/land-value-capture-policy-brief.pdf (accessed on 15 December 2020).

- Kelkar, V.L.; Rajaraman, I.; Misra, S. Report of the Committee on Roadmap for Fiscal Consolidation; Government of India: New Delhi, India, 2012.

- Kanuri, C.; Revi, A.; Espey, J.; Kuhle, H. Getting Started With the SDGs in Cities; Sustainable Development Solutions Network: New York, NY, USA, 2016. [Google Scholar]

- Tiwari, P. India Habitat III, National Report, 2016. Minist. Hous. Urban Poverty Alleviation 2016, 32, 978–998. [Google Scholar]

- Kundu, D. Urban Development Programmes in India: A Critique of JnNURM. Soc. Chang. 2014, 44, 615–632. [Google Scholar] [CrossRef]

- Government of India MHUA. Smart Cities Mission, Government of India. Resource Website. 2015. Available online: http://smartcities.gov.in/content/ (accessed on 15 December 2020).

- Roy, S. The Smart City Paradigm in India: Issues and Challenges of Sustainability and Inclusiveness. Soc. Sci. 2016, 44, 29. [Google Scholar]

- Kundu, D.; Sietchiping, R.; Kinyanjui, M. Developing National Urban Policies; Springer: Singapore, 2020. [Google Scholar]

{kind=link}

{kind=link}

| Parameters | Description |

|---|---|

| Contributors | Who are the stakeholders from whom the increased value created by public sector interventions/public infrastructure is recovered? |

| Beneficiaries | Who are the stakeholders to whom the benefits of the value created will accrue? |

| Process | How is the value–recovery mechanism linked to budgets of the policy proponents and land monetization benefits related to taxation? |

| Financial Risks | Who are the stakeholders likely to bear the financial risks associated with future cash flows with current investments? |

| Governance Actors | Who are the stakeholders (actors) involved in the governance of value recovery, distribution, and allocation? |

| Project | Key Features |

|---|---|

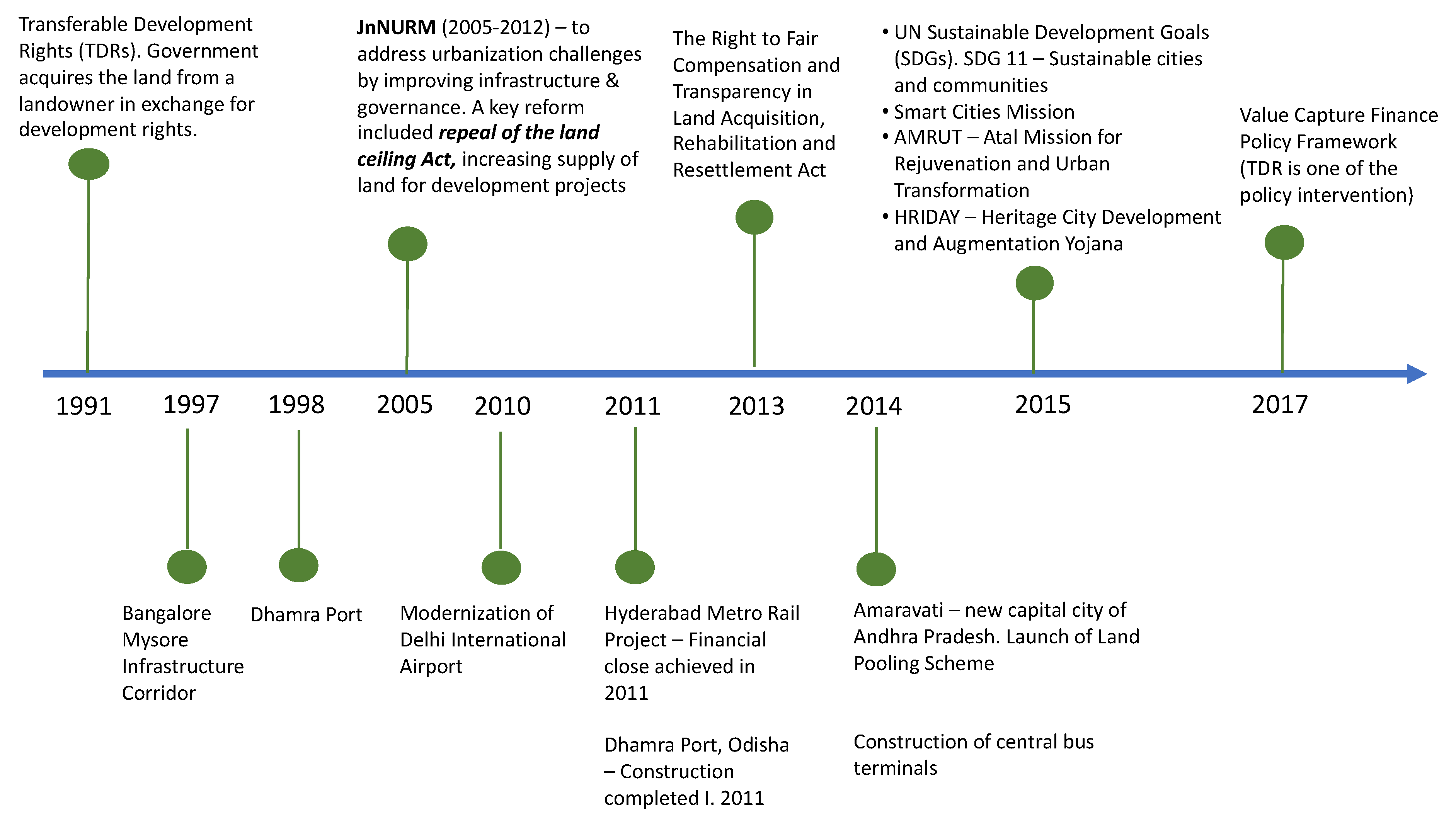

| Amaravati City | Amaravati, city assumed importance in 2014 when it was designated as the administrative capital of the newly carved state of Andhra Pradesh. Anticipating the challenges that would come from rapid urbanization, population increase, and the associated increase in the value of land in the urban area, the Government of Andhra Pradesh introduced the “Land Pooling Scheme (LPS)” as an innovative land-use planning instrument to capture the land value increases in a manner that is equitable and balances development with urbanization. The unique feature of the LPS was to ensure that landowners benefit directly from the increase in land value when the capital city would be developed, by making them stakeholders in the development process. The scheme encouraged landowners to contribute their plot of land in return for a smaller plot of urban serviced land (returnable plot), expected to be higher in value and was also promised annuity payments (to support livelihoods) and skill upgrading programs for setting up self-owned enterprises [15]. |

| The Bangalore-Mysore Infrastructure Corridor | The project was conceived in the 1980s as an expressway of about 111 km connecting the heritage city of Mysore to the capital city Bangalore. The project proposed by Nandi Infrastructure Corridor Enterprises Ltd. was also to include residential, industrial, and commercial facilities. The objective was to de-congest Bangalore city and attract people to shift to the upcoming townships along the corridor. The government of Karnataka entered into a Framework Agreement with the developer in the year 1997 agreeing to provide land for the project. However, several rounds of litigation ensued, challenging the land acquisition process for the project and refusal to grant permission by the Planning Authority for the construction of group housing [24]. |

| Hyderabad Metro Rail Project | The rail project comprising 66 stations in 72 km estimated at Rs. 14,132 crores are being developed by L&T Hyderabad Metro Rail Private Limited, Hyderabad. Nearly, 40% of the revenues are estimated to come from real estate development and lease revenues therefrom [25]. |

| Modernization of Delhi International Airport | Rajiv Gandhi International Airport was a greenfield airport built on approximately 5000 acres of land. Nearly 45 acres were identified as phase 1 development for commercial and hospitality facilities comprising about 14 assets. Out of 5000 rooms, 3000 rooms were budget rooms and the remaining were categorized as luxurious rooms. The cost of construction was estimated to be Rs. 75 lakhs to Rs. 1 crore per room. The concession agreement was signed on 4.4.2006 and construction completed on 31.3.2010. The other major components of the project included the renovation of Terminals 1A, 1B, 1C, and Terminal 2 of the existing airport [26]. |

| Dhamra Port, Odisha | Dhamra is a port close to the mineral-rich industrial states of Odisha, Jharkhand and Chattisgarh developed on a Build Own Operate Share Transfer framework. The 25.0 MTPA project with a concession period of 408 months was bid out on a revenue share basis. The concession agreement was signed on 2.4.1998. Excess land allotted to the project was met with challenges [27]. |

| Modern Central Bus Terminus cum Commercial Complex, Haldia, West Bengal | Eleven acres of land near HPL Township was identified for the project, out of which the private partner was to develop a modern Central Bus Terminus on 7 acres of land and operate it for 20 years. The remaining 4 acres of land was to be developed commercially by the PPP partner who was also expected to operate and maintain the facilities for 50 years [28]. |

| Construction of central bus terminal, Makarpura, Vadodara | Constructed on 6.3 acres as a BOT project for a concession period of 378 months. The concession agreement was signed in 2010 with Hubtown (Vadodara) Bus Terminal Ltd. at a project cost of Rs. 60.28 crores [28]. |

| Title | Salient Features Related to Land Monetization |

|---|---|

| JNNURM guidelines(Mission period starts—2005-06) | Amongst others, the guidelines propose that ULBs will develop and manage municipal assets to ensure sustainable public service delivery to the citizens especially the urban poor and people living in peri-urban areas. It is expected that the State Level Nodal Agency/ULBs would leverage financial resources in addition to financial assistance from the Central and State Governments. To ensure bankability, it is envisaged that liquidity support mechanism, up-front debt service reserve facility, deep discount bonds, contingent liability support, and equity support are to be established. The other reform proposed is to earmark 20–25% of developed land for EWS and LIG housing projects. This was suggested to enhance the supply of land for affordable houses for the urban poor and to provide them access to basic services. It was envisaged that with the increased housing supply, the ULBs would be able to garner higher amounts towards property tax. The other reform envisaged in the guidelines is the repealing of the Urban Land Ceiling Act, 1976. Its objective was to facilitate the availability of urban land at affordable prices by increasing its supply in the market. The objective of the reform in the rent control act is to bring out amendments in existing provisions for balancing the interests of landlords and tenants. Additionally, the increased investment in housing would lead to increased housing stock and increased revenue from property tax. So far twelve states have yet to make desired amendments in the rent control act [33] |

| Smart City guidelines | “Para 3.1 (i) Promoting mixed land use in area-based developments—planning for ‘unplanned areas’ containing a range of compatible activities and land uses close to one another to make land use more efficient. The States will enable some flexibility in land use and building bye-laws to adapt to change.” “Para 5.1.2 Redevelopment will effect a replacement of the existing built-up environment and enable co-creation of a new layout with enhanced infrastructure using mixed land use and increased density. Redevelopment envisages an area of more than 50 acres, identified by Urban Local Bodies (ULBs) in consultation with citizens.” “Para 5.1.3 Greenfield development will introduce most of the Smart Solutions in a previously vacant area (more than 250 acres) using innovative planning, plan financing and plan implementation tools (e.g., land pooling/land reconstitution) with provision for affordable housing, especially for the poor. Unlike retrofitting and redevelopment, greenfield developments could be located either within the limits of the ULB or within the limits of the local Urban Development Authority (UDA).” “Para 11.3 (i) The GOI funds and the matching contribution by the States/ULB will meet only a part of the project cost. Balance funds are expected to be mobilized from i. States/ULBs own resources from a collection of user fees, beneficiary charges and impact fees, land monetization, debt, loans, etc.” “Para 13.1.3 The National Mission Director will have the responsibility to…… (iii) Oversee capacity building and assisting in handholding of SPVs, State, and ULBs. This includes developing and retaining a best practice repository (Model RFP documents, Draft DPRs, Financial models, land monetization ideas, best practices in SPV formation, use of financial instruments and risk mitigation techniques) and mechanism for knowledge sharing across States and ULBs (through publications, workshops, seminars)” [34,35] |

| AMRUT guidelines | “Para 6.10 Conditionalities: ……, in the AMRUT no projects should be included which do not have land available and no project work order should be issued if all clearances from all the departments have not been received by that time. Moreover, the cost of land purchase will be borne by the States/ULBs.” “..Explore innovative ways for resource mobilization, private financing, and land leveraging for funding of projects.” It also provides that in the appraisal of the DPR, the National Mission Director may decide to “Mobilize external resources and improve internal resource generation of the ULBs. For instance, facilitate access to municipal bonds by credit rating ULBs, providing assistance to ULBs to monetize land and prepare Tax Increment Financing Proposals (TIF), obtain private funding, etc.” [36] |

| Land Acquisition Act, 2013 | The objective of the Act (amongst other things) is to ensure the development of infrastructural facilities and urbanization. The Act envisages that the affected persons become partners in development leading to an improvement in their social and economic status. Land can be acquired for a public purpose and it includes agro-processing, industrial corridors, water harvesting, education, sports, etc. (Section 2(1)). The law further provides on the method to be followed in the process of land acquisition for the determination of the social impact and public purpose (Chapter II—Sections 4 to 9) Section 26 (3) (c)—”Provided that in a case where the Requiring Body offers its shares to the owners of the lands (whose lands have been acquired) as a part compensation, for the acquisition of land, such shares in no case shall exceed twenty-five percent. of the value so calculated under sub-section (I) or sub-section (2) or sub-section (3) as the case may be”: [4] |

| The Andhra Pradesh Infrastructure Development Enabling Act, 2001 | To provide for the rapid development of physical and social infrastructure in the State and attract private sector participation An ‘Infrastructure Authority’ is established to conceptualize and identify projects and ensuring their conformance to the objectives of the State. The Authority also has the responsibility to categorize projects, prepare a project shelf, road map for project development, decide financial support, etc. It also has the responsibility to receive and consider projects from Government agencies and also advise them in the development of infrastructure. The prioritization of projects is to be carried out based on ‘demand and supply gap, inter-linkages and any other relevant parameters’. |

| GIDB Act | The objective of the Act is to allow persons from the non-Government sector to ‘participate in financing, construction, maintenance, and operation of projects. GIDB is the nodal agency for PPP projects in the State. The Board also acts as a policy advisor to the State Government and is vested with appropriate functions to prioritize various projects of the Government, to consider proposals received from private parties, to undertake technical and financial studies, to coordinate with concerned agencies. |

| Infrastructure Policy, Government of Karnataka | “Facilitating private participation in developing infrastructure facilities in the state by providing opportunities to private parties for participating in new infrastructure facilities development as well maintaining the existing infrastructure facilities. Infrastructure Development Department of the GoK is the nodal agency for appraisal and approval of infrastructure projects which is supported by a PPP Cell within the department. A Single Window Agency under the Chairmanship of Chief Secretary is set up for appraisal and approval of the projects. The State High-Level Committee chaired by the Chief Minister will approve Projects above Rs.50 Crores. GoK intends to put in mechanisms for expediting the land acquisition process and if necessary specific legislation would be passed in this regard. To enhance the commercial viability of projects, GoK may allow, wherever necessary, the Concessionaire/SPV to develop utilitarian services or other socially acceptable commercial activities, on the infrastructure project site.” |

| Land Value Capture Policy, MoUD, GoI | The policy provides for four steps for project-based VCF. (1) Initiation (2) Planning (3) Design and strategy and (4) Execution and Operation. The policy document also provides a Guidance Note for the inclusion of VCF in projects. The Guidance Note envisages that VCF should be an integral part of the DPR for Central Government projects as has been stated by the Ministry of Finance in its OM dated 7 March 2017. |

| Title | Contributors | Beneficiaries | Process | Financial Risks | Governance Actors |

|---|---|---|---|---|---|

| JNNURM | Landowners, property developers | ULBs (cities), development authorities, parastatal agencies | Not explicitly stated. Assumed to be part of the consolidated fund | ULBs, development authorities, parastatal agencies | State government and ULBs |

| Smart City | Landowners, property developers | ULBs, smart city SPVs | Income to consolidated fund; revenue to SPVs | ULBs, SPVs | State Government, ULB |

| AMRUT | Landowners, property developers | ULBs, development authorities, parastatal agencies | Not explicitly stated. Assumed to be part of the consolidated fund | ULBs, development authorities, and parastatal agencies | State government and ULBs |

| Land Acquisition Act, 2013 | Landowners, property developers | State Government | Proceeds go to the consolidated fund | State Government | State Government |

| The Andhra Pradesh Infrastructure Development Enabling Act, 2001 | Landowners, property developers | ULBs, development authorities, parastatal agencies | Proceeds go to consolidated fund; PPP projects can appropriate value | Project proponents (public/private) | State Government |

| GIDB Act | Landowners, property developers | ULBs, development authorities, parastatal agencies | Proceeds go to consolidated fund; PPP projects can appropriate value | Project proponents (public/nongovernment) | State Government |

| Infrastructure Policy, Government of Karnataka | Landowners, property developers | ULBs, development authorities, parastatal agencies | Proceeds go to consolidated fund; PPP projects can appropriate value | Project proponents (public/nongovernment) | State Government |

| Land Value Capture Policy, MoUD, GoI | Landowners, property developers | ULBs, development authorities, parastatal agencies | Proceeds go to consolidated fund; PPP projects can appropriate value | Project proponents (public/nongovernment) | State Government |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tirumala, R.D.; Tiwari, P. Land-Based Financing Elements in Infrastructure Policy Formulation: A Case of India. Land 2021, 10, 133. https://doi.org/10.3390/land10020133

Tirumala RD, Tiwari P. Land-Based Financing Elements in Infrastructure Policy Formulation: A Case of India. Land. 2021; 10(2):133. https://doi.org/10.3390/land10020133

Chicago/Turabian StyleTirumala, Raghu Dharmapuri, and Piyush Tiwari. 2021. "Land-Based Financing Elements in Infrastructure Policy Formulation: A Case of India" Land 10, no. 2: 133. https://doi.org/10.3390/land10020133

APA StyleTirumala, R. D., & Tiwari, P. (2021). Land-Based Financing Elements in Infrastructure Policy Formulation: A Case of India. Land, 10(2), 133. https://doi.org/10.3390/land10020133