Does the Water Resource Tax Reform Bring Positive Effects to Green Innovation and Productivity in High Water-Consuming Enterprises?

Abstract

1. Introduction

2. Literature Review

2.1. Water Resource Tax

2.2. Corporate Green Innovation

2.3. Total Factor Productivity of Enterprises

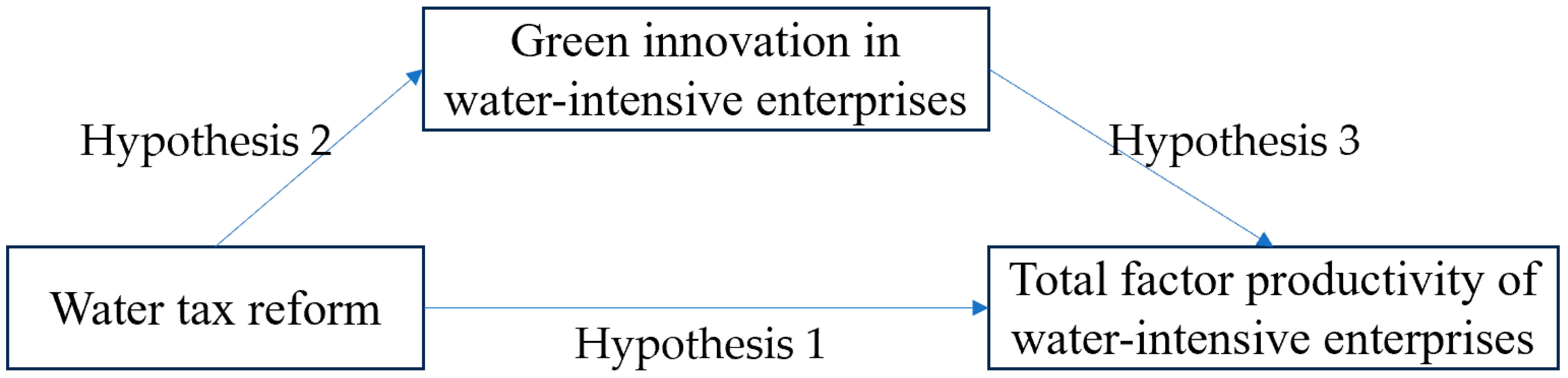

3. Theoretical Analysis and Research Hypothesis

4. Research Design

4.1. Sample Selection

4.2. Variable Measurement

4.3. Model Setup

5. Empirical Results and Analysis

5.1. Descriptive Statistics and Pearson Correlation Analysis

5.2. Benchmark Regression Analysis

5.3. Robustness Tests

5.3.1. Fixed Effects Model

5.3.2. Substitution of Key Variables

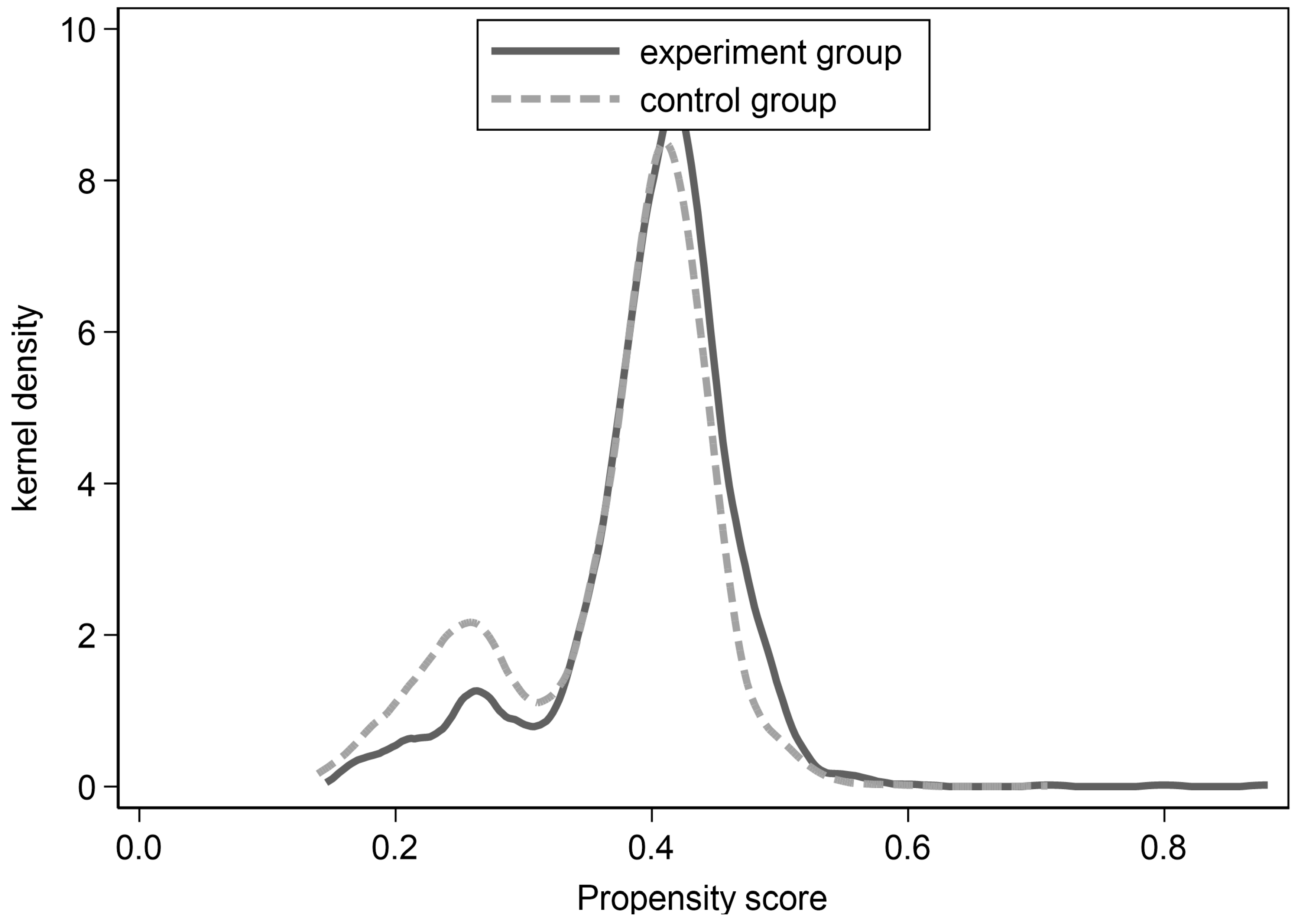

5.3.3. PSM-DID Model

5.4. Intrinsic Mechanism of Action Test

5.5. Heterogeneity Analysis

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Yao, P.; Li, J. Determining industry by water: Fee to tax of water resources and industrial transformation and upgrading. Stat. Res. 2023, 40, 135–148. [Google Scholar]

- Lv, Y.; Ge, Y.; Geng, Y. Has the water resource tax reform improved the green efficiency of water resource? J. Arid Land Resour. Environ. 2022, 36, 77–83. [Google Scholar]

- Huang, B. An exhaustible resources model in a dynamic input–output framework: A possible reconciliation between Ricardo and Hotelling. J. Econ. Struct. 2018, 7, 8. [Google Scholar]

- Ing, J. Adverse selection, commitment and exhaustible resource taxation. Resour. Energy Econ. 2020, 61, 101161. [Google Scholar]

- Welsch, H. Resource dependence, knowledge creation, and growth: Revisiting the natural resource curse. J. Econ. Dev. 2008, 33, 45–70. [Google Scholar] [CrossRef]

- Liu, H.; Ruebeck, C.S. Knowledge spillover and positive environmental externality in agricultural decision making under performance-based payment programs. Agric. Resour. Econ. Rev. 2020, 49, 270–290. [Google Scholar] [CrossRef]

- Thomas, A.; Zaporozhets, V. Bargaining over environmental budgets: A political economy model with application to French water policy. Environ. Resour. Econ. 2017, 68, 227–248. [Google Scholar]

- Höglund, L. Household demand for water in Sweden with implications of a potential tax on water use. Water Resour. Res. 1999, 35, 3853–3863. [Google Scholar] [CrossRef]

- Clinch, J.P.; Dunne, L.; Dresner, S. Environmental and wider implications of political impediments to environmental tax reform. Energy Policy 2006, 34, 960–970. [Google Scholar]

- Berbel, J.; Borrego-Marin, M.M.; Exposito, A.; Giannoccaro, G.; Montilla-Lopez, N.M.; Roseta-Palma, C. Analysis of irrigation water tariffs and taxes in Europe. Water Policy 2019, 21, 806–825. [Google Scholar] [CrossRef]

- van Heerden, J.H.; Blignaut, J.; Horridge, M. Integrated water and economic modelling of the impacts of water market instruments on the South African economy. Ecol. Econ. 2008, 66, 105–116. [Google Scholar] [CrossRef]

- Porcher, S. The ‘hidden costs’ of water provision: New evidence from the relationship between contracting-out and price in French water public services. Util. Policy 2017, 48, 166–175. [Google Scholar]

- Porter, M.E.; Linde, C. Toward a new conception of the environment-competitiveness relationship. J. Econ. Perspect. 1995, 9, 97–118. [Google Scholar] [CrossRef]

- Fan, T. Research on the reform and perfection of resource Tax system. Open J. Soc. Sci. 2021, 9, 107943. [Google Scholar] [CrossRef]

- Jia, Z.; Lin, B. CEEEA2. 0 model: A dynamic CGE model for energy-environment-economy analysis with available data and code. Energy Econ. 2022, 112, 106117. [Google Scholar] [CrossRef]

- Chen, X.; Yi, N.; Zhang, L.; Li, D. Does institutional pressure foster corporate green innovation? Evidence from China’s top 100 companies. J. Clean. Prod. 2018, 188, 304–311. [Google Scholar] [CrossRef]

- Ambec, S.; Cohen, M.A.; Elgie, S.; Lanoie, P. The Porter hypothesis at 20: Can environmental regulation enhance innovation and competitiveness? Rev. Environ. Econ. Policy 2013, 7, 2–22. [Google Scholar] [CrossRef]

- Mikhno, I.; Koval, V.; Shvets, G.; Garmatiuk, O.; Tamošiūnienė, R. Green economy in sustainable development and improvement of resource efficiency. Cent. Eur. Bus. Rev. 2021, 10, 99–113. [Google Scholar] [CrossRef]

- Munguía-López, A.C.; González-Bravo, R.; Ponce-Ortega, J.M. Evaluation of carbon and water policies in the optimization of water distribution networks involving power-desalination plants. Appl. Energy 2019, 236, 927–936. [Google Scholar]

- Ouyang, R.; Mu, E.; Yu, Y.; Chen, Y.; Hu, J.; Tong, H.; Cheng, Z. Assessing the effectiveness and function of the water resources tax policy pilot in China. Environ. Dev. Sustain. 2022, 9, 1–17. [Google Scholar] [CrossRef]

- Biancardi, M.; Maddalena, L.; Villani, G. Water taxes and fines imposed on legal and illegal firms exploiting groundwater. Discret. Contin. Dyn. Syst.-Ser. B 2021, 26, 5787–5806. [Google Scholar]

- Guo, J.; Chen, Z.; Nie, P. Discussion of the tax scheme for cleaner water use. Water Conserv. Sci. Eng. 2022, 7, 475–490. [Google Scholar] [CrossRef]

- Chen, Y.; Li, J.; Lu, H.; Yang, Y. Impact of unconventional natural gas development on regional water resources and market supply in China from the perspective of game analysis. Energy Policy 2020, 145, 111750. [Google Scholar] [CrossRef]

- Oltra, V.; Saint Jean, M. Sectoral systems of environmental innovation: An application to the French automotive industry. Technol. Forecast. Soc. Chang. 2009, 76, 567–583. [Google Scholar] [CrossRef]

- Vasileiou, E.; Georgantzis, N.; Attanasi, G.; Llerena, P. Green innovation and financial performance: A study on Italian firms. Res. Policy 2022, 51, 104530. [Google Scholar]

- Frondel, M.; Horbach, J.; Rennings, K. What triggers environmental management and innovation? Empirical evidence for Germany. Ecol. Econ. 2008, 66, 153–160. [Google Scholar] [CrossRef]

- Horbach, J. Determinants of environmental innovation—New evidence from German panel data sources. Res. Policy 2008, 37, 163–173. [Google Scholar] [CrossRef]

- Borsatto, J.M.L.S.; Bazani, C.L. Green innovation and environmental regulations: A systematic review of international academic works. Environ. Sci. Pollut. Res. 2021, 28, 63751–63768. [Google Scholar] [CrossRef]

- Stucki, T. Which firms benefit from investments in green energy technologies?–The effect of energy costs. Res. Policy 2019, 48, 546–555. [Google Scholar] [CrossRef]

- Fernando, Y.; Tseng, M.-L.; Sroufe, R.; Abideen, A.Z.; Shaharudin, M.S.; Jose, R. Eco-innovation impacts on recycled product performance and competitiveness: Malaysian automotive industry. Sustain. Prod. Consum. 2021, 28, 1677–1686. [Google Scholar]

- Zhang, Y.; Zhang, J.; Cheng, Z. Stock market liberalization and corporate green innovation: Evidence from China. Int. J. Environ. Res. Public Health 2021, 18, 3412. [Google Scholar] [PubMed]

- Segarra-Ona MD, V.; Peiró-Signes, A.; Verma, R.; Miret-Pastor, L. Does environmental certification help the economic performance of hotels? Evidence from the Spanish hotel industry. Cornell Hosp. Q. 2012, 53, 242–256. [Google Scholar] [CrossRef]

- Sáez-Martínez, F.J.; Díaz-García, C.; Gonzalez-Moreno, A. Firm technological trajectory as a driver of eco-innovation in young small and medium-sized enterprises. J. Clean. Prod. 2016, 138, 28–37. [Google Scholar] [CrossRef]

- Keskin, D.; Diehl, J.C.; Molenaar, N. Innovation process of new ventures driven by sustainability. J. Clean. Prod. 2013, 45, 50–60. [Google Scholar] [CrossRef]

- Ogbeibu, S.; Emelifeonwu, J.; Senadjki, A.; Gaskin, J.; Kaivo-Oja, J. Technological turbulence and greening of team creativity, product innovation, and human resource management: Implications for sustainability. J. Clean. Prod. 2020, 244, 118703. [Google Scholar]

- Scarpellini, S.; Marín-Vinuesa, L.M.; Portillo-Tarragona, P.; Moneva, J.M. Defining and measuring different dimensions of financial resources for business eco-innovation and the influence of the firms’ capabilities. J. Clean. Prod. 2018, 204, 258–269. [Google Scholar] [CrossRef]

- da Cunha Bezerra, M.C.; Gohr, C.F.; Morioka, S.N. Organizational capabilities towards corporate sustainability benefits: A systematic literature review and an integrative framework proposal. J. Clean. Prod. 2020, 247, 119114. [Google Scholar] [CrossRef]

- Shahzad, M.; Qu, Y.; Zafar, A.U.; Rehman, S.U.; Islam, T. Exploring the influence of knowledge management process on corporate sustainable performance through green innovation. J. Knowl. Manag. 2020, 24, 2079–2106. [Google Scholar] [CrossRef]

- Triguero, A.; Moreno-Mondéjar, L.; Davia, M.A. Drivers of different types of eco-innovation in European SMEs. Ecol. Econ. 2013, 92, 25–33. [Google Scholar] [CrossRef]

- Wang, C.L.; Ahmed, P.K. Dynamic capabilities: A review and research agenda. Int. J. Manag. Rev. 2007, 9, 31–51. [Google Scholar] [CrossRef]

- Lončar, D.; Paunković, J.; Jovanović, V.; Krstić, V. Environmental and social responsibility of companies cross EU countries–Panel data analysis. Sci. Total Environ. 2019, 657, 287–296. [Google Scholar] [CrossRef] [PubMed]

- Sumrin, S.; Gupta, S.; Asaad, Y.; Wang, Y.; Bhattacharya, S.; Foroudi, P. Eco-innovation for environment and waste prevention. J. Bus. Res. 2021, 122, 627–639. [Google Scholar] [CrossRef]

- Arena, C.; Michelon, G.; Trojanowski, G. Big egos can be green: A study of CEO hubris and environmental innovation. Br. J. Manag. 2018, 29, 316–336. [Google Scholar]

- Zhang, Z.; Yang, L.; Peng, X.; Liao, Z. Overseas imprints reflected at home: Returnee CEOs and corporate green innovation. Asian Bus. Manag. 2023, 22, 1328–1368. [Google Scholar]

- Papagiannakis, G.; Voudouris, I.; Lioukas, S.; Kassinis, G. Environmental management systems and environmental product innovation: The role of stakeholder engagement. Bus. Strategy Environ. 2019, 28, 939–950. [Google Scholar] [CrossRef]

- Bernard, A.B.; Moxnes, A.; Saito, Y.U. Production networks, geography, and firm performance. J. Political Econ. 2019, 127, 639–688. [Google Scholar]

- Aghion, P.; Cai, J.; Dewatripont, M.; Du, L.; Harrison, A.; Legros, P. Industrial policy and competition. Am. Econ. J. Macroecon. 2015, 7, 1–32. [Google Scholar]

- Kiyota, K.; Okazaki, T. Industrial policy cuts two ways: Evidence from cotton-spinning firms in Japan, 1956–1964. J. Law Econ. 2010, 53, 587–609. [Google Scholar] [CrossRef][Green Version]

- Arizala, F.; Cavallo, E.; Galindo, A. Financial development and TFP growth: Cross-country and industry-level evidence. Appl. Financ. Econ. 2013, 23, 433–448. [Google Scholar] [CrossRef]

- Méon, P.G.; Weill, L. Does financial intermediation matter for macroeconomic performance? Econ. Model. 2010, 27, 296–303. [Google Scholar] [CrossRef]

- Caggese, A. Financing constraints, radical versus incremental innovation, and aggregate productivity. Am. Econ. J. Macroecon. 2019, 11, 275–309. [Google Scholar] [CrossRef]

- Habib, M.; Abbas, J.; Noman, R. Are human capital, intellectual property rights, and research and development expenditures really important for total factor productivity? An empirical analysis. Int. J. Soc. Econ. 2019, 46, 756–774. [Google Scholar] [CrossRef]

- Bennett, B.; Stulz, R.; Wang, Z. Does the stock market make firms more productive? J. Financ. Econ. 2020, 136, 281–306. [Google Scholar] [CrossRef]

- Hsieh, C.T.; Klenow, P.J. Misallocation and manufacturing TFP in China and India. Q. J. Econ. 2009, 124, 1403–1448. [Google Scholar] [CrossRef]

- Tian, G.Y.; Twite, G. Corporate governance, external market discipline and firm productivity. J. Corp. Financ. 2011, 17, 403–417. [Google Scholar] [CrossRef]

- Ahamed, M.M.; Luintel, K.B.; Mallick, S.K. Does local knowledge spillover matter for firm productivity? The role of financial access and corporate governance. Res. Policy 2023, 52, 104837. [Google Scholar] [CrossRef]

- Wang, H.; Yang, G.; Ouyang, X.; Tand, Z.; Long, X.; Yue, Z. Horizontal ecological compensation mechanism and technological progress: Theory and empirical study of Xin’an River Ecological Compensation Gambling Agreement. J. Environ. Plan. Manag. 2023, 66, 501–523. [Google Scholar]

- Hancevic, P.I. Environmental regulation and productivity: The case of electricity generation under the CAAA-1990. Energy Econ. 2016, 60, 131–143. [Google Scholar]

- Gray, W.B.; Shadbegian, R.; Wolverton, A. Environmental regulation and labor demand: What does the evidence tell us? Annu. Rev. Resour. Econ. 2023, 15, 177–197. [Google Scholar] [CrossRef]

- de Medeiros, J.F.; Vidor, G.; Ribeiro, J.L.D. Driving factors for the success of the green innovation market: A relationship system proposal. J. Bus. Ethics 2018, 147, 327–341. [Google Scholar]

- Magat, W.A. The effects of environmental regulation on innovation. Law Contemp. Probl. 1979, 43, 4–25. [Google Scholar]

- Weitzman, M.L. Optimal rewards for economic regulation. Am. Econ. Rev. 1978, 68, 683–691. [Google Scholar]

- Montero, J.P. Market structure and environmental innovation. J. Appl. Econ. 2002, 5, 293–325. [Google Scholar]

- Larson, D.M.; Helfand, G.E.; and House, B.W. Second-best tax policies to reduce nonpoint source pollution. Am. J. Agric. Econ. 1996, 78, 1108–1117. [Google Scholar] [CrossRef]

- Marriott, L.; Kraal, D.; and Singh-Ladhar, J. Tax as a solution for irrigation water scarcity, quality and sustainability: Case studies in Australia and New Zealand. Aust. Tax Forum 2021, 36, 369–402. [Google Scholar]

- Ambec, S.; Barla, P. A Theoretical foundation of the Porter hypothesis. Econ. Lett. 2002, 75, 355–360. [Google Scholar]

- Wang, K.; Wu, Y. Research on the promoting effect of green tax system on total factor productivity of rare earth enterprises—Empirical analysis based on resource tax reform. Price Theory Pract. 2023, 3, 116–119. [Google Scholar]

- Cannon, J.N. Determinants of ‘sticky costs’: An analysis of cost behavior using United States air transportation industry data. Account. Rev. 2014, 89, 1645–1672. [Google Scholar] [CrossRef]

- Cai, W.; Li, G. The drivers of eco-innovation and its impact on performance: Evidence from China. J. Clean. Prod. 2018, 176, 110–118. [Google Scholar] [CrossRef]

- Song, M.; Wang, S.; Zhang, H. Could environmental regulation and R&D tax incentives affect green product innovation? J. Clean. Prod. 2020, 258, 120849. [Google Scholar]

- Gilli, M.; Mancinelli, S.; Mazzanti, M. Innovation complementarity and environ-mental productivity effects: Reality or delusion? Evidence from the EU. Ecol. Econ. 2014, 103, 56–67. [Google Scholar] [CrossRef]

- Klette, T.J.; Griliches, Z. Empirical patterns of firm growth and R&D investment: A quality ladder model interpretation. Econ. J. 2000, 110, 363–387. [Google Scholar]

- Carrión-Flores, C.E.; Innes, R. Environmental innovation and environmental performance. J. Environ. Econ. Manag. 2010, 59, 27–42. [Google Scholar] [CrossRef]

- Fleming, L.; Sorenson, O. Science as a map in technological search. Strateg. Manag. J. 2004, 25, 909–928. [Google Scholar] [CrossRef]

- Wurlod, J.D.; Noailly, J. The impact of green innovation on energy intensity: An empirical analysis for 14 industrial sectors in OECD countries. Energy Econ. 2018, 71, 47–61. [Google Scholar] [CrossRef]

- Liu, B.; Cifuentes-Faura, J.; Ding, C.J.; Liu, X. Toward carbon neutrality: How will environmental regulatory policies affect corporate green innovation? Econ. Anal. Policy 2023, 80, 1006–1020. [Google Scholar] [CrossRef]

- Levinsohn, J.; Petrin, A. Estimating production functions using inputs to control for unobservables. Rev. Econ. Stud. 2003, 70, 317–341. [Google Scholar]

- Gramkow, C.; Anger-Kraavi, A. Could fiscal policies induce green innovation in developing countries? The case of Brazilian manufacturing sectors. Clim. Policy 2018, 18, 246–257. [Google Scholar] [CrossRef]

- Filson, A.; Lewis, A. Innovation from a small company perspective-an empirical investigation of new product development strategies in SMEs. In Proceedings of the 2000 IEEE Engineering Management Society, EMS-2000 (Cat. No. 00CH37139), Albuquerque, NM, USA, 15 August 2000; IEEE: Piscataway, NJ, USA, 2000; pp. 141–146. [Google Scholar]

- Amore, M.D.; Schneider, C.; Žaldokas, A. Credit supply and corporate innovation. J. Financ. Econ. 2013, 109, 835–855. [Google Scholar]

- Francis, J.; Smith, A. Agency costs and innovation some empirical evidence. J. Account. Econ. 1995, 19, 383–409. [Google Scholar] [CrossRef]

- De Cleyn, S.H.; Braet, J. Do board composition and investor type influence innovativeness in SMEs? Int. Entrep. Manag. J. 2012, 8, 285–308. [Google Scholar] [CrossRef]

- Belloc, F. Law, finance and innovation: The dark side of shareholder protection. Camb. J. Econ. 2013, 37, 863–888. [Google Scholar] [CrossRef]

- Zahra, S.A.; Ireland, R.D.; Hitt, M.A. International expansion by new venture firms: International diversity, mode of market entry, technological learning, and performance. Acad. Manag. J. 2000, 43, 925–950. [Google Scholar]

- Coles, J.L.; Daniel, N.D.; Naveen, L. Managerial incentives and risk-taking. J. Financ. Econ. 2006, 79, 431–468. [Google Scholar] [CrossRef]

- Miller, D.J.; Fern, M.J.; Cardinal, L.B. The use of knowledge for technological in-novation within diversified firms. Acad. Manag. J. 2007, 50, 307–325. [Google Scholar] [CrossRef]

- Yoo, Y.; Henfridsson, O.; Lyytinen, K. Research commentary—The new organizing logic of digital innovation: An agenda for information systems research. Inf. Syst. Res. 2010, 21, 724–735. [Google Scholar] [CrossRef]

- Mikalef, P.; Pateli, A. Information technology-enabled dynamic capabilities and their indirect effect on competitive performance: Findings from PLS-SEM and fsQCA. J. Bus. Res. 2017, 70, 1–16. [Google Scholar]

- Bronzini, R.; Piselli, P. The impact of R&D subsidies on firm innovation. Res. Policy 2016, 45, 442–457. [Google Scholar]

- Lokshin, B.; Mohnen, P. How effective are level-based R&D tax credits? Evidence from the Netherlands. Appl. Econ. 2012, 44, 1527–1538. [Google Scholar]

- Baron, R.M.; Kenny, D.A. The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. J. Personal. Soc. Psychol. 1986, 51, 1173–1182. [Google Scholar] [CrossRef] [PubMed]

{kind=link}

{kind=link}

| Variable Type | Variable Name | Variable Symbol | Definition |

|---|---|---|---|

| Explained variable | Total factor productivity | TFP_LP | Total factor productivity calculated using the LP method |

| Mediator variable | Enterprise green innovation | GI | Add 1 to the number of invention patents applied for by the enterprise in the current year, taking the natural logarithm. |

| Explanatory variable | Water resource tax reform | TT | Whether to carry out pilot water resource tax reform, represented by the dummy variable TT, TTit = Treatedi × Timet |

| Control variable | Company profitability | ROA | Net profit margin on total assets |

| Company growth | Growth | Total assets growth rate | |

| Financial leverage | Lev | Asset–liability ratio | |

| Independent director governance | Id | The proportion of independent directors to the size of the board of directors | |

| Director board size | Bs | Total number of directors in the board of directors | |

| Governance of major shareholders | Msg | Shareholding ratio of the largest shareholder | |

| CEO duality | Pt | The value of the general manager concurrently serving as the chairman is 1; otherwise, the value is 0. | |

| Managerial ownership | MS | Proportion of shares held by company executives | |

| Executive compensation | MC | The total monetary compensation of company executives is calculated as the natural logarithm. | |

| Product market competition | HHI | HHI = represents the size of the i-th enterprise, and represents the total market size. | |

| Digital transformation | DT | Data calculation of text mining based on digital lexicon | |

| Financial subsidy | FS | (Government subsidies—returns of various taxes and fees received)/total assets | |

| Tax incentives | TI | Returns of various taxes and fees received/total assets | |

| Industry | Industry | Industry dummy variable | |

| Year | Year | Year dummy variable |

| Variable | Mean | Median | Max | Min | SD | Obs |

|---|---|---|---|---|---|---|

| TFP_LP | 10.9894 | 10.8418 | 14.7543 | 4.4336 | 1.2855 | 8949 |

| GI | 0.2082 | 0 | 6.6983 | 0 | 0.5843 | 8949 |

| TT | 0.1406 | 0 | 1 | 0 | 0.3476 | 8949 |

| ROA | 0.0410 | 0.0363 | 0.6271 | -0.6449 | 0.0709 | 8949 |

| Growth | 0.1326 | 0.0780 | 19.0954 | -0.8490 | 0.4286 | 8949 |

| Lev | 0.4453 | 0.4448 | 0.9970 | 0.0080 | 0.2014 | 8949 |

| Id | 0.3724 | 0.3333 | 0.8 | 0.1429 | 0.0555 | 8949 |

| Msg | 0.3661 | 0.3468 | 0.8999 | 0.0029 | 0.1559 | 8949 |

| Pt | 0.2206 | 0 | 1 | 0 | 0.4146 | 8949 |

| Bs | 8.9136 | 9 | 18 | 0 | 1.9163 | 8949 |

| MS | 0.0507 | 0.0001 | 0.7259 | 0 | 0.1216 | 8949 |

| MC | 14.7365 | 14.7958 | 18.5844 | 0 | 1.1287 | 8949 |

| HHI | 0.1248 | 0.1049 | 1 | 0.0144 | 0.1138 | 8949 |

| DT | 0.7037 | 0 | 5.0689 | 0 | 0.9758 | 8949 |

| FS | 0.0048 | 0.0023 | 0.4212 | 0 | 0.0166 | 8949 |

| TI | 0.0006 | 0 | 0.1132 | 0 | 0.0029 | 8949 |

| Variable | TFP_LP | GI | TT | ROA | Growth | Lev | Id |

|---|---|---|---|---|---|---|---|

| TFP_LP | 1 | ||||||

| GI | 0.3779 *** | 1 | |||||

| TT | 0.1292 *** | 0.1051 *** | 1 | ||||

| ROA | 0.1375 *** | −0.0017 | 0.0267 ** | 1 | |||

| Growth | −0.0140 | −0.0230 ** | −0.0273 *** | 0.1735 *** | 1 | ||

| Lev | 0.3670 *** | 0.1195 *** | −0.0223 ** | −0.3497 *** | −0.0057 | 1 | |

| Id | 0.0271 ** | 0.0287 *** | 0.0157 | 0.0080 | 0.0020 | −0.0521 *** | 1 |

| Msg | 0.3281 *** | 0.1503 *** | −0.0397 *** | 0.1236 *** | −0.0196 * | 0.0588 *** | 0.0551 *** |

| Pt | −0.1547 *** | -0.0693 *** | −0.0547 *** | 0.0394 *** | 0.0297 *** | −0.1432 *** | 0.1180 *** |

| Bs | 0.2549 *** | 0.1430 *** | −0.0026 | 0.0115 | −0.0265 ** | 0.2334 *** | −0.6101 *** |

| MS | −0.1822 *** | −0.0633 *** | −0.0630 *** | 0.1026 *** | 0.0461 *** | −0.2433 *** | 0.1246 *** |

| MC | 0.3162 *** | 0.1719 *** | 0.1081 *** | 0.1823 *** | 0.0099 | −0.0474 *** | −0.0033 |

| HHI | −0.0911 *** | −0.0116 | −0.0868 *** | −0.0891 *** | −0.0326 ** | 0.0177 | 0.0093 |

| DT | 0.0149 | −0.0194 | −0.0187 | 0.0144 | −0.0061 | 0.0153 | 0.0114 |

| FS | −0.0365 ** | −0.0599 *** | 0.0175 | 0.0504 *** | −0.0037 | −0.0074 | 0.0189 |

| TI | 0.1645 *** | 0.0590 *** | 0.0335 ** | −0.0261 * | 0.0237 | −0.0068 | 0.0956 *** |

| Variable | Msg | Pt | Bs | MS | MC | HHI | DT |

| Msg | 1 | ||||||

| Pt | 0.0518 *** | 1 | |||||

| Bs | 0.0806 *** | −0.0755 *** | 1 | ||||

| MS | −0.3995 *** | 0.0803 *** | −0.1653 *** | 1 | |||

| MC | 0.1003 *** | −0.0647 *** | 0.4409 *** | −0.1910 *** | 1 | ||

| HHI | 0.0408 *** | −0.0296 *** | 0.0534 *** | 0.0688 *** | 0.0514 *** | 1 | |

| DT | −0.0002 | −0.0015 | −0.0218 | 0.0446 *** | −0.0390 *** | 0.0148 | 1 |

| FS | 0.0458 *** | 0.0380 *** | −0.0441 *** | 0.0432 *** | 0.0369 ** | −0.0513 *** | −0.0015 |

| TI | 0.0331 ** | 0.0629 *** | −0.0717 *** | 0.0654 *** | 0.2166 *** | 0.0732 *** | −0.0077 |

| Variable | FS | TI | |||||

| FS | 1 | ||||||

| TI | 0.0358 ** | 1 |

| Variable | Model (1) | Model (2) | Model (3) |

|---|---|---|---|

| TT | 0.1147 *** (4.49) | 0.1029 *** (5.73) | |

| GI | 0.3547 *** (24.29) | ||

| ROA | 3.4274 *** (27.16) | −0.0214 (−0.24) | 3.4413 *** (28.14) |

| Growth | −0.0775 *** (−4.15) | −0.0189 (−1.44) | −0.0716 *** (−3.96) |

| Lev | 1.6378 *** (35.40) | 0.1726 *** (5.31) | 1.5783 *** (35.14) |

| Id | 0.9539 *** (6.07) | 0.6019 *** (5.45) | 0.7413 *** (4.85) |

| Msg | 1.3241 *** (24.11) | 0.4250 *** (11.02) | 1.1692 *** (21.83) |

| Pt | −0.1292 *** (−6.06) | −0.0361 ** (−2.41) | −0.1197 *** (−5.80) |

| Bs | 0.0644 *** (12.99) | 0.0365 *** (10.47) | 0.0522 *** (10.80) |

| MS | −0.3707 *** (−4.95) | −0.0710(−1.35) | −0.3620 *** (−5.00) |

| MC | 0.2051 *** (26.57) | 0.0594 *** (10.95) | 0.1834 *** (24.36) |

| HHI | 0.1317 (0.83) | 0.1510 (1.36) | 0.0730 (0.48) |

| DT | 3.7172 (1.36) | 2.1639 (1.13) | 2.9031 (1.09) |

| FS | −3.6460 *** (−7.71) | −0.4637 (−1.40) | −3.4948 *** (−7.62) |

| TI | 0.1054 *** (11.16) | 0.0069 (1.04) | 0.1019 *** (11.14) |

| Constant | 2.8642 *** (19.23) | −1.7303 *** (−16.54) | 3.4882 *** (23.80) |

| Year/industry | Yes | Yes | Yes |

| Adjust_R2 | 0.4800 | 0.2191 | 0.5113 |

| Obs | 8949 | 8949 | 8949 |

| Variable | Model (1) | Model (2) | Model (3) |

|---|---|---|---|

| TT | 0.1147 *** (4.49) | 0.1029 *** (5.73) | |

| GI | 0.3547 *** (24.29) | ||

| Controli,t | Yes | Yes | Yes |

| Constant | 3.1830 *** (21.53) | −1.6088 *** (−15.49) | 3.7774 *** (26.05) |

| Year/industry | Yes | Yes | Yes |

| Adjust_R2 | 0.4639 | 0.2048 | 0.4966 |

| Obs | 8949 | 8949 | 8949 |

| Variable | Replacing the Explanatory Variables | Replacing the Explained Variables | ||

|---|---|---|---|---|

| Model (2) | Model (3) | Model (1) | Model (3) | |

| TT | 0.3387 *** (13.49) | 0.0732 *** (3.83) | ||

| GI′ | 0.3135 *** (34.20) | |||

| GI | 0.1303 *** (10.57) | |||

| Controli,t | Yes | Yes | Yes | Yes |

| Constant | −2.7356 *** (−17.19) | 3.7379 *** (26.46) | 0.9412 *** (7.77) | 1.1697 *** (9.56) |

| Year/industry | Yes | Yes | Yes | Yes |

| Adjust_R2 | 0.2442 | 0.5264 | 0.2499 | 0.2580 |

| Obs | 8949 | 8949 | 8949 | 8949 |

| Column 1: TT → TFP_LP | |||||

| Weighted variable(s) | Mean control | Mean treated | Diff. | |t| | Pr (|T| > |t|) |

| TFP_OLS | 8.275 | 8.458 | 0.182 | 5.63 | 0.0000 *** |

| ROA | 0.037 | 0.039 | 0.002 | 0.88 | 0.3773 |

| Growth | 0.145 | 0.150 | 0.005 | 0.32 | 0.7504 |

| Lev | 0.493 | 0.491 | −0.002 | 0.33 | 0.7419 |

| Id | 0.364 | 0.364 | 0.000 | 0.13 | 0.8999 |

| Msg | 0.384 | 0.390 | 0.006 | 1.12 | 0.2642 |

| Pt | 0.117 | 0.112 | −0.004 | 0.45 | 0.6532 |

| Bs | 9.415 | 9.429 | 0.013 | 0.20 | 0.8416 |

| MS | 0.023 | 0.024 | 0.001 | 0.38 | 0.7046 |

| MC | 14.402 | 14.427 | 0.025 | 0.56 | 0.5783 |

| HHI | 0.134 | 0.139 | 0.005 | 1.02 | 0.3087 |

| TI | 0.001 | 0.001 | 0.000 | 0.18 | 0.8593 |

| FS | 0.004 | 0.004 | 0.000 | 0.35 | 0.7250 |

| DT | 0.311 | 0.310 | -0.001 | 0.06 | 0.9529 |

| Column 2: TT → GI | |||||

| Weighted variable(s) | Mean control | Mean treated | Diff. | |t| | Pr (|T| > |t|) |

| GI | 0.128 | 0.219 | 0.091 | 5.18 | 0.0000 *** |

| ROA | 0.037 | 0.039 | 0.002 | 0.88 | 0.3773 |

| Growth | 0.145 | 0.150 | 0.005 | 0.32 | 0.7504 |

| Lev | 0.493 | 0.491 | −0.002 | 0.33 | 0.7419 |

| Id | 0.364 | 0.364 | 0.000 | 0.13 | 0.8999 |

| Msg | 0.384 | 0.390 | 0.006 | 1.12 | 0.2642 |

| Pt | 0.117 | 0.112 | −0.004 | 0.45 | 0.6532 |

| Bs | 9.415 | 9.429 | 0.013 | 0.20 | 0.8416 |

| MS | 0.023 | 0.024 | 0.001 | 0.38 | 0.7046 |

| MC | 14.402 | 14.427 | 0.025 | 0.56 | 0.5783 |

| HHI | 0.134 | 0.139 | 0.005 | 1.02 | 0.3087 |

| TI | 0.001 | 0.001 | 0.000 | 0.18 | 0.8593 |

| FS | 0.004 | 0.004 | 0.000 | 0.35 | 0.7250 |

| DT | 0.311 | 0.310 | −0.001 | 0.06 | 0.9529 |

| Variable | Path c (Model with dv Regressed on iv) | Path a (Model with Mediator Regressed on iv) | Paths b and c’ (Model with dv Regressed on Mediator and iv) | |||

|---|---|---|---|---|---|---|

| TT | 0.2412 *** (9.64) | 0.1550 *** (9.02) | 0.1847 *** (7.59) | |||

| GI | 0.3646 *** (24.44) | |||||

| Controli,t | Yes | Yes | Yes | |||

| Constant | 2.4059 *** (17.11) | −1.9716 *** (-20.42) | 3.1247 *** (22.43) | |||

| Year/industry | Yes | Yes | Yes | |||

| Adjust_R2 | 0.3682 | 0.0903 | 0.4077 | |||

| Obs | 8949 | 8949 | 8949 | |||

| Column 1: Sobel–Goodman Mediation Tests | ||||||

| Est | Std_err | z | P > |z| | |||

| Sobel | 0.057 | 0.007 | 8.463 | 0.000 | ||

| Aroian | 0.057 | 0.007 | 8.457 | 0.000 | ||

| Goodman | 0.057 | 0.007 | 8.469 | 0.000 | ||

| Column 2: Indirect, Direct, and Total Effects | ||||||

| Est | Std_err | z | P > |z| | |||

| a_coefficient | 0.155 | 0.017 | 9.021 | 0.000 | ||

| b_coefficient | 0.365 | 0.015 | 24.441 | 0.000 | ||

| Indirect_effect_aXb | 0.057 | 0.007 | 8.463 | 0.000 | ||

| Direct_effect_c’ | 0.185 | 0.024 | 7.586 | 0.000 | ||

| Total_effect_c | 0.241 | 0.025 | 9.637 | 0.000 | ||

| Proportion of total effect that is mediated: 0.234 | ||||||

| Ratio of indirect to direct effect: 0.306 | ||||||

| Ratio of total to direct effect: 1.306 | ||||||

| Variable | SOEs | Non-SOEs | ||||

|---|---|---|---|---|---|---|

| Model (1) | Model (2) | Model (3) | Model (1) | Model (2) | Model (3) | |

| TT | 0.0484(1.17) | 0.0615 * (1.88) | 0.1149 *** (3.79) | 0.0640 *** (3.73) | ||

| GI | 0.3704 *** (19.84) | 0.1708 *** (6.63) | ||||

| Controli,t | Yes | Yes | Yes | Yes | Yes | Yes |

| Constant | 3.0283 *** (15.46) | −2.0909 *** (−13.49) | 3.8029 *** (19.88) | 3.4272 *** (13.03) | −0.6637 *** (−4.46) | 3.5634 *** (13.57) |

| Year/industry | Yes | Yes | Yes | Yes | Yes | Yes |

| Adjust_R2 | 0.5202 | 0.3210 | 0.5613 | 0.4537 | 0.0834 | 0.4571 |

| Obs | 4237 | 4237 | 4237 | 4712 | 4712 | 4712 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Xu, C.; Gao, Y.; Hua, W.; Feng, B. Does the Water Resource Tax Reform Bring Positive Effects to Green Innovation and Productivity in High Water-Consuming Enterprises? Water 2024, 16, 725. https://doi.org/10.3390/w16050725

Xu C, Gao Y, Hua W, Feng B. Does the Water Resource Tax Reform Bring Positive Effects to Green Innovation and Productivity in High Water-Consuming Enterprises? Water. 2024; 16(5):725. https://doi.org/10.3390/w16050725

Chicago/Turabian StyleXu, Chaohui, Yingchao Gao, Wenwen Hua, and Bei Feng. 2024. "Does the Water Resource Tax Reform Bring Positive Effects to Green Innovation and Productivity in High Water-Consuming Enterprises?" Water 16, no. 5: 725. https://doi.org/10.3390/w16050725

APA StyleXu, C., Gao, Y., Hua, W., & Feng, B. (2024). Does the Water Resource Tax Reform Bring Positive Effects to Green Innovation and Productivity in High Water-Consuming Enterprises? Water, 16(5), 725. https://doi.org/10.3390/w16050725