The Value of Water—Estimating Water-Disruption Impacts on Businesses

, , ,

, , ,  and

and

Abstract

:1. Introduction

2. Materials and Methods

2.1. Data Collection

2.2. Data Analysis

3. Results

4. Discussion

5. Conclusions

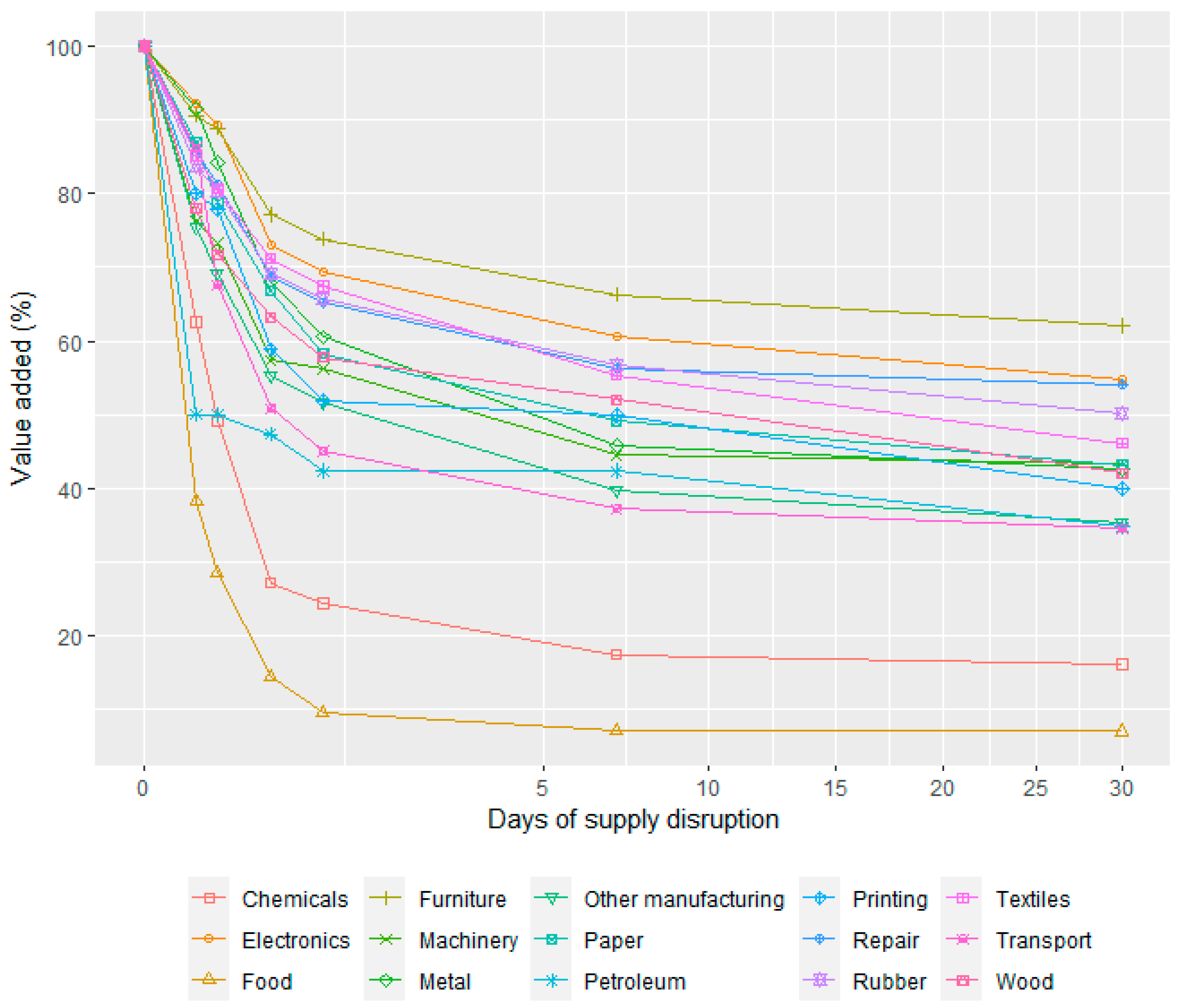

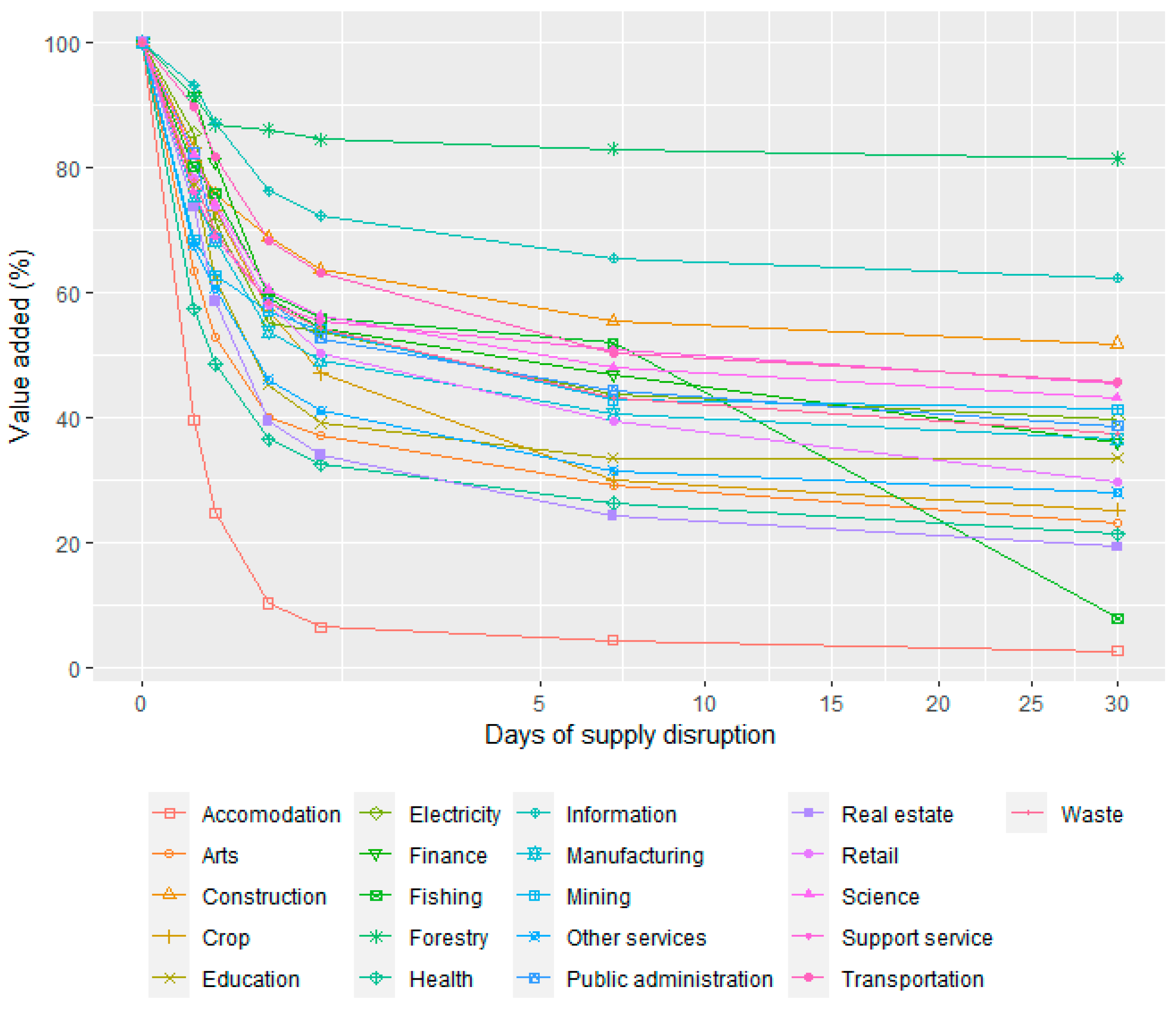

- The investigation of direct economic business losses of short and long-term water supply outages shows that Food, beverage and tobacco is the most severely affected manufacturing sector over all analyzed water disruption durations. The sector’s water resiliency factors range from 0.69 to 0.11 for the analyzed disruption durations (from two hours to one month). The Accommodation and food service sector is the most severely affected non-manufacturing sector, with resiliency factors ranging between 0.70 and 0.10. Forestry and logging is the least affected sector, with factors between 0.96 (two-hour disruption) to 0.83 (one-month disruption). The information provided by the resiliency factors can be used to improve assessments at the societal level, by for example, water providers or authorities who need to assess the annual risk of an existing water supply system or compare the (socio-economic) benefits of alternative risk mitigation measures. The stepwise procedure for estimating the annual risk (with consequences measured in costs) will include assessing which types of delivery failures that can occur in the supply system of interest, the likelihood of occurrence of these types of disruption events based on historical site-specific data or expert judgements, and which economic sectors are present in the region. For each type of disruption event, the cost per sector is calculated over disruption duration and recovery time as the product of the sector’s contribution to the regional GDP at normal business activity and the complement of the sector’s resiliency factor (1—resiliency factor). The total annual cost for businesses is then the aggregate product of the probability of each type of event and its respective costs for all present sectors.

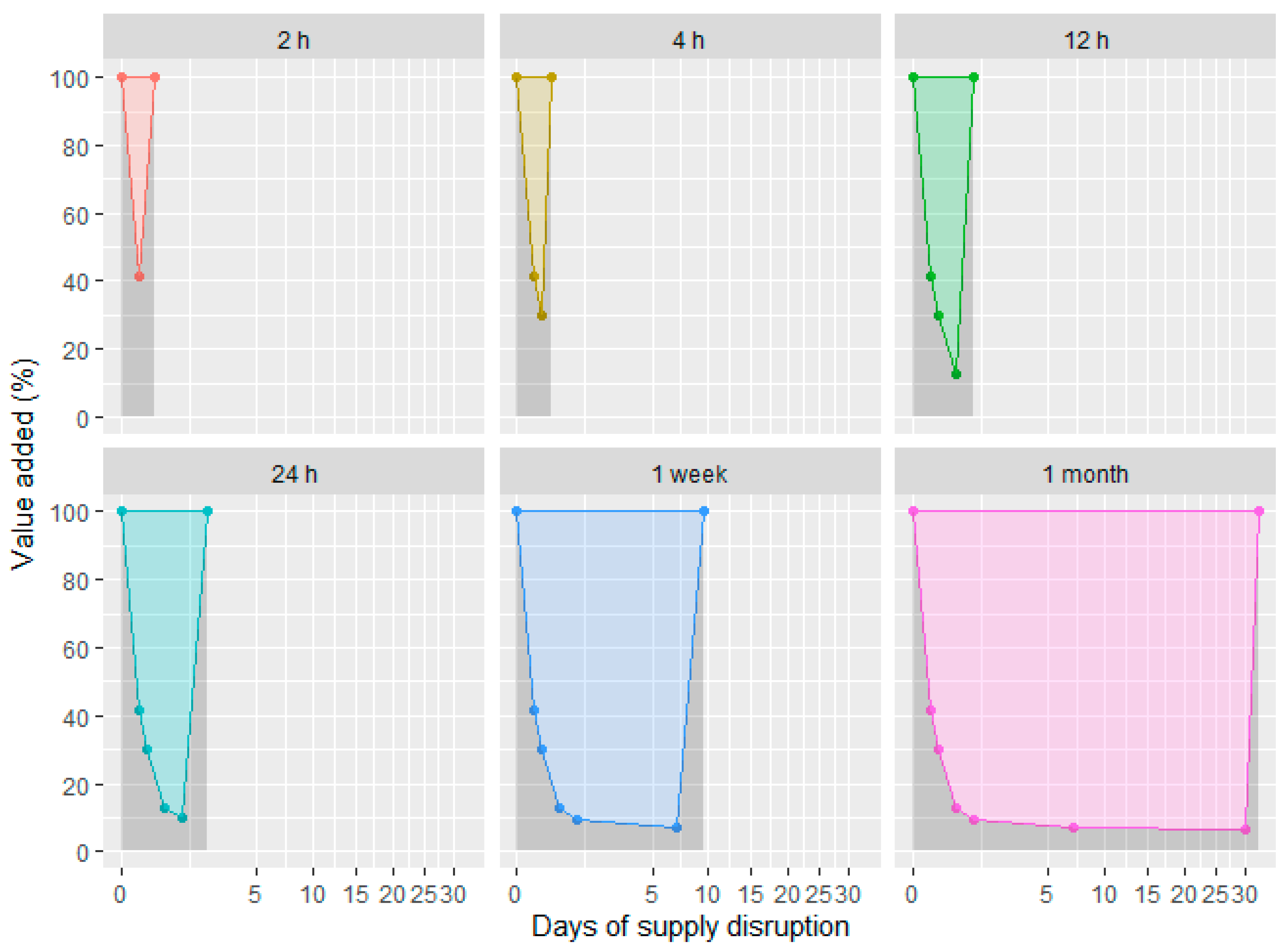

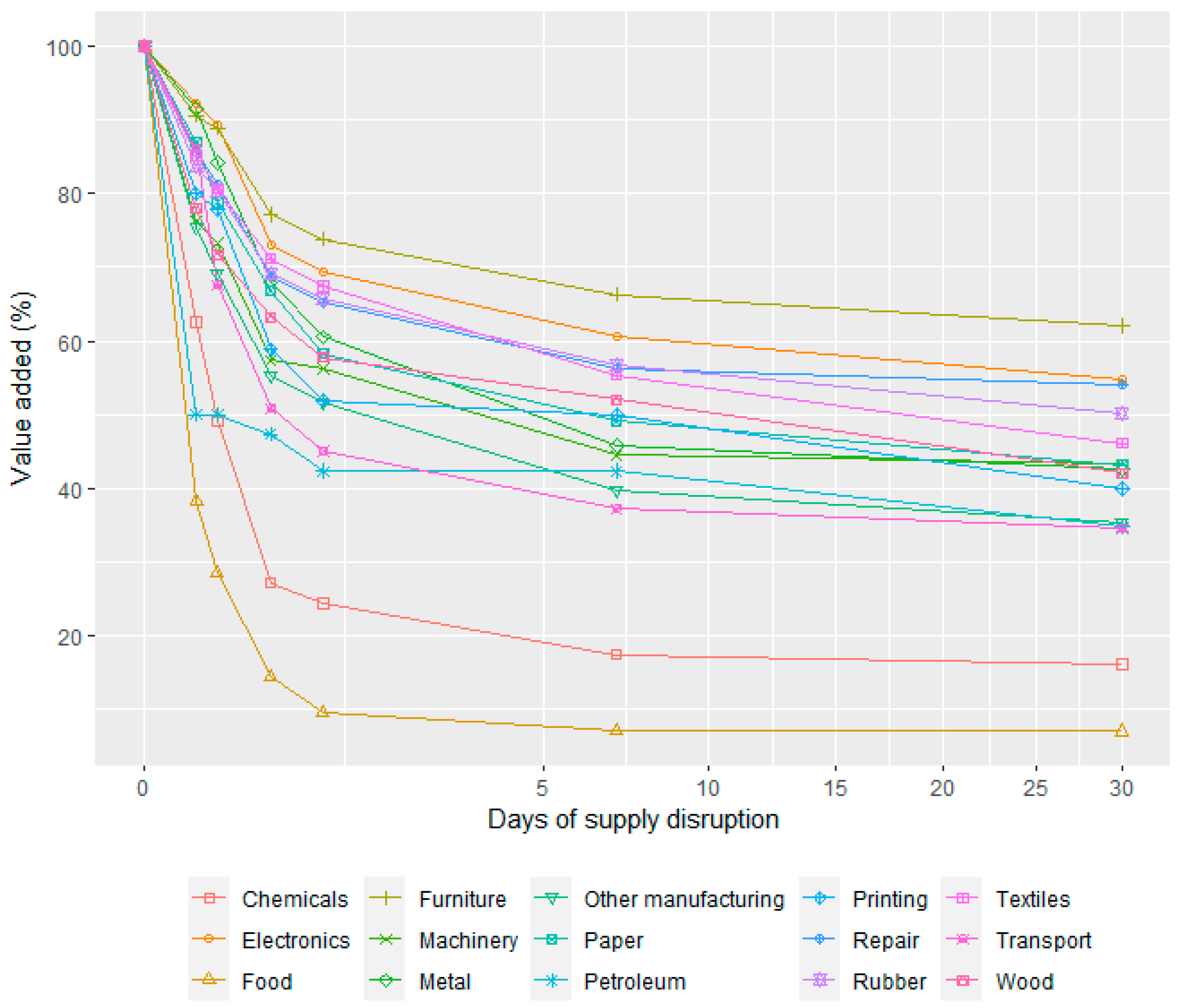

- It is worth noting that all sectors are affected already by a two-hour disruption, ranging from 7% reduction in value added in the Information and communication sector to 62% reduction in the Food, beverage and tobacco sector (mean values). The reduction in value added increases with the disruption duration, with sector-wise mean values varying between 13 and 75% for a four-hour disruption, 23 and 90% for a 12-h disruption, 26 and 94% for a one-day disruption, 34 and 96% for a one-week disruption; and 38 and 97% for a one-month disruption. However, a fairly large proportion of the companies can maintain a normal business activity (100% value added) throughout a water outage: 48% of all companies during a two-hour disruption, 34% during a four-hour disruption, 25% during a 12-h disruption, 23% during a one-day disruption; 18% during a one-week disruption; and 16% of all companies during a one-month disruption.

- The mean recovery time was less than a day for most sectors following disruptions lasting 24 h or less. The recovery time after week-long or month-long disruptions varied between a few hours and six days. However, several companies responded that they could not recover at all from those longer disruptions and would have to file for bankruptcy. When estimating the total business-related effects of water supply disruptions, effects of bankruptcy should thus be considered in addition to the lost value added.

- The business resilience factors provided here contribute with information to help respond to the challenges arising from water disruption risks. With a better understanding of the value of water to all water users, a good, effective and efficient water governance is made possible. The results can be used for better economic impact assessments and evaluations of mitigation strategies, hence facilitating the managing of risks at the least cost to society. By illustrating the economic benefit of a reliable water provision, the results can thus be used to justify measures aimed at strengthening water security and by that contributing to ensuring a long-term sustainable use of our water resources.

Supplementary Materials

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- WWAP. The United Nations World Water Development Report 2016 Report: Water and Jobs; UNESCO: Paris, France, 2016. [Google Scholar]

- WWAP. The United Nations World Water Development Report 2015: Water for a Sustainable World; UNESCO: Paris, France, 2015. [Google Scholar]

- Vladimirova, I.; Nguyen, N.; Schellekens, J.; Vassileva, I. Assessment of the Water Productivity Index. Deliverable to Task A4a of the Blue2 Project “Study on EU Integrated Policy Assessment for the Freshwater and Marine Environment, on the Economic Benefits of EU Water Policy and on the Costs of Its Non-Implementation”; DG ENV: Brussels, Belgium, 2018. [Google Scholar]

- Contreras, D.; Voets, A.; Junghardt, J.; Bhamidipati, S.; Contreras, S. The drivers of child mortality during the 2012–2016 drought in la Guajira, Colombia. Int. J. Disaster Risk Sci. 2020, 11, 87–104. [Google Scholar] [CrossRef] [Green Version]

- Ding, Y.; Hayes Michael, J.; Widhalm, M. Measuring economic impacts of drought: A review and discussion. Disaster Prev. Manag. Int. J. 2011, 20, 434–446. [Google Scholar] [CrossRef] [Green Version]

- Nocera, F.; Gardoni, P. A ground-up approach to estimate the likelihood of business interruption. Int. J. Disaster Risk Reduct. 2019, 41, 101314. [Google Scholar] [CrossRef]

- KPMG. Sustainable Insight–Water Scarcity: A Dive into Global Reporting Trends; KPMG International Cooperative: Zurich, Switzerland, 2012. [Google Scholar]

- Buck, S.; Auffhammer, M.; Hamilton, S.; Sunding, D. Measuring welfare losses from urban water supply disruptions. J. Assoc. Environ. Resour. Econ. 2015, 3, 743–778. [Google Scholar] [CrossRef] [Green Version]

- Graveline, N.; Grémont, M. Measuring and understanding the microeconomic resilience of businesses to lifeline service interruptions due to natural disasters. Int. J. Disaster Risk Reduct. 2017, 24, 526–538. [Google Scholar] [CrossRef]

- Brozović, N.; Sunding, D.L.; Zilberman, D. Estimating business and residential water supply interruption losses from catastrophic events. Water Resour. Res. 2007, 43, 14. [Google Scholar] [CrossRef]

- Chang, S.E. Socioeconomic impacts of infrastructure disruptions. Oxf. Res. Encycl. Nat. Hazard Sci. 2016, 31. [Google Scholar] [CrossRef]

- Rose, A.; Wing, I.S.; Wei, D.; Avetisyan, M. Total Regional Economic Losses from Water Supply Disruptions to the Los Angeles County Economy; Los Angeles County Economic Development Corporation: Los Angeles, CA, USA, 2012. [Google Scholar]

- ATC. Atc-25. Seismic Vulnerability and Impact of Disruption of Lifelines in the Conterminous United States; FEMA Federal Emergency Management Agency: Washington, WA, USA, 1991.

- FEMA. Fema Benefit-Cost Analysis Re-Engineering (Bcar). Development of Standard Economic Values; Federal Emergency Management Agency (FEMA): Washington, WA, USA, 2011.

- Chang, S.E.; Svekla, W.D.; Shinozuka, M. Linking infrastructure and urban economy: Simulation of water-disruption impacts in earthquakes. Environ. Plan. B Plan. Des. 2002, 29, 281–301. [Google Scholar] [CrossRef]

- Kajitani, Y.; Tatano, H. Estimation of lifeline resilience factors based on surveys of Japanese industries. Earthq. Spectra 2009, 25, 755–776. [Google Scholar] [CrossRef]

- Heflin, C.; Jensen, J.; Miller, K. Understanding the economic impacts of disruptions in water service. Eval. Program Plann. 2014, 46, 80–86. [Google Scholar] [CrossRef] [PubMed]

- Lizarraga, S.A. The Economic Consequences of Water Utility Disruptions; University of Missouri: Columbia, MO, USA, 2013. [Google Scholar]

- VASS. Swedish Water and Wastewater Associations Statistic’s System. Available online: http://www.vass-statistik.se/ (accessed on 23 September 2020).

- Lindhe, A.; Rosen, L.; Norberg, T.; Bergstedt, O. Fault tree analysis for integrated and probabilistic risk analysis of drinking water systems. Water Res. 2009, 43, 1641–1653. [Google Scholar] [CrossRef] [PubMed]

- Lindhe, A.; Norberg, T.; Rosén, L. Approximate dynamic fault tree calculations for modelling water supply risks. Reliab. Eng. Syst. Saf. 2012, 106, 61–71. [Google Scholar] [CrossRef] [Green Version]

- Sjöstrand, K.; Lindhe, A.; Söderqvist, T.; Rosén, L. Water supply delivery failures—A scenario-based approach to assess economic losses and risk reduction options. Water 2020, 12, 1746. [Google Scholar] [CrossRef]

- Malm, A.; Moberg, F.; Rosén, L.; Pettersson, T.J.R. Cost-benefit analysis and uncertainty analysis of water loss reduction measures: Case study of the gothenburg drinking water distribution system. Water Resour. Manag. 2015, 29, 5451–5468. [Google Scholar] [CrossRef]

- SFS. The Swedish Water Services Act (Lag (2006:412) om Allmänna Vattentjänster); The Ministry of the Environment: Stockholm, Sweden, 2006.

- Swedish Food Agency. Guide to Planning Emergency Water Supply; The Swedish Food Agency: Uppsala, Sweden, 2017.

- European Parliament. Regulation (Ec) No 1893/2006 of the European Parliament and of the Council of 20 December 2006 Establishing the Statistical Classification of Economic Activities Nace Revision 2 and Amending Council Regulation (Eec) No 3037/90 as Well as Certain Ec Regulations on Specific Statistical Domains. Available online: https://eur-lex.europa.eu/legal-content/EN/ALL/?uri=CELEX%3A32006R1893 (accessed on 7 April 2020).

- Rose, A. A framework for analyzing the total economic impacts of terrorist attacks and natural disasters. J. Homel. Secur. Emerg. Manag. 2009, 6, 27. [Google Scholar] [CrossRef]

- Atkinson, K.E. An Introduction to Numerical Analysis, 2nd ed.; John Wiley and Sons: New York, NY, USA, 1989. [Google Scholar]

- OECD. Oecd Sme and Entrepreneurship Outlook: 2005; OECD: Paris, France, 2005. [Google Scholar]

- Statistics Sweden. Current Statistics from the Business Register. Available online: https://www.scb.se/vara-tjanster/foretagsregistret/aktuell-statistik-fran-foretagsregistret/ (accessed on 4 May 2020).

- Swedish Water and Wastewater Association. Result Report for 2019 from Swedish Water and Wastewater Associations Statistic’s System; Swedish Water and Wastewater Association: Bromma, Sweden, 2020. [Google Scholar]

- Swedish Water and Wastewater Association. Sustainability Index for the Municipalities’ Water and Wastewater Operations; Swedish Water and Wastewater Association: Bromma, Sweden, 2020. [Google Scholar]

- Statistics Sweden. Gdp Quarter 1993–2020:1. Available online: https://www.scb.se/hitta-statistik/statistik-efter-amne/nationalrakenskaper/nationalrakenskaper/nationalrakenskaper-kvartals-och-arsberakningar/pong/tabell-och-diagram/tabeller/bnp-kvartal/ (accessed on 4 May 2020).

- Westling, K.; Kärrman, E.; Norström, A. A Vision for Water—Research and Innovation Agenda for the Swedish Water Sector. Available online: https://www.svensktvatten.se/forskning/vattenplattformen/vattenvisionen/ (accessed on 19 August 2019).

- Carlsson, H.; Haraldsson, M.; Kärrman, E.; Lidström, V.; Lundh, M.; Malm, A.; Malmström, H.; Pendrill, L.; Rönnbäck, M.; Sjögren, L.; et al. Investment Needs and Future Costs for Municipal Water and Sewage; Swedish Water and Wastewater Association: Stockholm, Sweden, 2017. [Google Scholar]

- Tierney, K.J. Businesses and Disasters: Vulnerability, Impacts, and Recovery. In Handbook of Disaster Research; Rodríguez, H., Quarantelli, E.L., Dynes, R.R., Eds.; Springer Science + Business Media: New York, NY, USA, 2007. [Google Scholar]

- The Government Offices of Sweden. National Strategy for Efficent and Sustainable Water Management. Available online: https://www.regeringen.se/pressmeddelanden/2021/02/en-efterfragad-strategi-for-effektiv-och-hallbar-vattenhushallning/ (accessed on 12 February 2021).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| NACE Code | Economic Activity | Number | Employees (%) | Water Source (%) | Disruption Experience * (%) | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| 0–9 | 10–49 | 50–199 | 200–9999 | Public | Public & Private | Private | ||||

| A 01 | Crop and animal production | 71 | 77 | 18 | 3 | 1 | 28 | 23 | 49 | 41 |

| A 02 | Forestry and logging | 13 | 62 | 38 | 0 | 0 | 15 | 38 | 46 | 23 |

| A 03 | Fishing and aquaculture | 5 | 80 | 20 | 0 | 0 | 60 | 20 | 20 | 20 |

| B 07–09 | Mining and quarrying | 7 | 43 | 43 | 14 | 0 | 71 | 14 | 14 | 57 |

| C 10–12 | Food, beverage and tobacco | 68 | 21 | 43 | 18 | 19 | 88 | 4 | 7 | 50 |

| C 13–15 | Textiles and leather | 38 | 65 | 19 | 14 | 3 | 76 | 3 | 21 | 27 |

| C 16 | Wood products | 26 | 58 | 35 | 8 | 0 | 85 | 4 | 12 | 42 |

| C 17 | Paper products | 20 | 10 | 60 | 5 | 25 | 60 | 30 | 10 | 45 |

| C 18 | Printing and recorded media | 10 | 80 | 20 | 0 | 0 | 100 | 0 | 0 | 10 |

| C 19 | Coke and petroleum | 4 | 75 | 0 | 0 | 25 | 75 | 25 | 0 | 25 |

| C 20–21 | Chemical and pharmaceutical | 53 | 9 | 43 | 34 | 13 | 89 | 11 | 0 | 40 |

| C 22–23 | Rubber and plastic | 33 | 41 | 38 | 19 | 3 | 79 | 9 | 12 | 38 |

| C 24–25 | Metal products | 63 | 44 | 38 | 16 | 2 | 89 | 5 | 6 | 17 |

| C 26–27 | Computer and electronics | 38 | 47 | 39 | 11 | 3 | 95 | 0 | 5 | 29 |

| C 28 | Machinery | 17 | 24 | 29 | 29 | 18 | 71 | 12 | 18 | 41 |

| C 29–30 | Transport equipment | 19 | 32 | 26 | 37 | 5 | 95 | 0 | 5 | 32 |

| C 31 | Furniture | 12 | 55 | 27 | 9 | 9 | 92 | 0 | 8 | 27 |

| C 32 | Other manufacturing | 27 | 56 | 30 | 15 | 0 | 85 | 7 | 7 | 41 |

| C 33 | Repair and installation | 28 | 82 | 14 | 4 | 0 | 86 | 0 | 14 | 11 |

| D 35 | Electricity, gas, steam and air | 30 | 17 | 47 | 30 | 7 | 77 | 20 | 3 | 40 |

| E 36–39 | Water, sewerage and waste | 26 | 27 | 54 | 12 | 8 | 69 | 15 | 15 | 62 |

| F 41–43 | Construction | 20 | 50 | 45 | 5 | 0 | 80 | 10 | 10 | 40 |

| G 45–47 | Wholesale and retail | 44 | 30 | 32 | 23 | 16 | 89 | 5 | 7 | 32 |

| H 49–53 | Transportation and storage | 50 | 34 | 34 | 22 | 10 | 92 | 6 | 2 | 32 |

| I 55–56 | Accommodation and food service | 59 | 39 | 37 | 14 | 10 | 92 | 0 | 8 | 63 |

| J 58–63 | Information and communication | 94 | 49 | 30 | 16 | 5 | 94 | 4 | 2 | 20 |

| K 64–66 | Financial and insurance activities | 25 | 16 | 44 | 28 | 12 | 100 | 0 | 0 | 36 |

| L 68 | Real estate activities | 38 | 21 | 26 | 32 | 21 | 95 | 5 | 0 | 61 |

| M 69–75 | Scientific and technical activities | 81 | 46 | 37 | 15 | 2 | 91 | 2 | 6 | 28 |

| N 77–82 | Administrative and support service | 34 | 50 | 21 | 24 | 6 | 82 | 9 | 9 | 35 |

| O 84 | Public administration and defense | 36 | 3 | 19 | 42 | 36 | 89 | 11 | 0 | 47 |

| P 85 | Education | 39 | 33 | 33 | 26 | 8 | 90 | 5 | 5 | 44 |

| Q 86–88 | Human health activities | 86 | 40 | 28 | 24 | 8 | 86 | 8 | 6 | 38 |

| R 90–93 | Arts, entertainment and recreation | 82 | 45 | 41 | 10 | 4 | 88 | 4 | 9 | 34 |

| S 94–96 | Other service activities | 109 | 43 | 29 | 19 | 8 | 81 | 12 | 7 | 30 |

| Total | 1405 | |||||||||

| NACE Code | Economic Activity | 2 h | 4 h | 12 h | 24 h | 1 Week | 1 Month | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| r | t-Factor | r | t-Factor | r | t-Factor | r | t-Factor | r | t-Factor | r | t-Factor | ||

| A 01 | Crop and animal production | 0.92 | 13.97 | 0.90 | 10.95 | 0.73 | 7.12 | 0.65 | 3.77 | 0.44 | 1.25 | 0.32 | 1.09 |

| A 02 | Forestry and logging | 0.96 | 1.00 | 0.94 | 2.62 | 0.90 | 5.62 | 0.88 | 3.31 | 0.85 | 1.33 | 0.83 | 1.08 |

| A 03 | Fishing and aquaculture | 0.90 | 1.40 | 0.84 | 1.00 | 0.73 | 1.03 | 0.66 | 1.03 | 0.56 | 1.01 | 0.36 | 1.00 |

| B 07–09 | Mining and quarrying | 0.84 | 1.14 | 0.78 | 1.07 | 0.65 | 1.11 | 0.61 | 1.07 | 0.51 | 1.03 | 0.44 | 1.00 |

| C 10–12 | Food, beverage and tobacco | 0.69 | 3.41 | 0.68 | 2.28 | 0.40 | 2.73 | 0.32 | 2.66 | 0.18 | 1.46 | 0.11 | 1.10 |

| C 13–15 | Textiles and leather | 0.93 | 1.31 | 0.88 | 1.05 | 0.81 | 1.30 | 0.76 | 1.17 | 0.65 | 1.16 | 0.55 | 1.09 |

| C 16 | Wood products | 0.89 | 1.44 | 0.83 | 1.08 | 0.72 | 1.06 | 0.67 | 1.03 | 0.57 | 1.01 | 0.49 | 1.00 |

| C 17 | Paper products | 0.93 | 3.39 | 0.95 | 2.27 | 0.80 | 1.46 | 0.73 | 1.26 | 0.58 | 1.29 | 0.51 | 1.12 |

| C 18 | Printing and recorded media | 0.90 | 1.00 | 0.84 | 1.05 | 0.73 | 1.10 | 0.65 | 1.14 | 0.55 | 1.06 | 0.49 | 1.07 |

| C 19 | Coke and petroleum | 0.75 | 3.19 | 0.78 | 2.09 | 0.62 | 2.75 | 0.58 | 1.88 | 0.47 | 1.13 | 0.44 | 1.15 |

| C 20–21 | Chemical and pharmaceutical | 0.81 | 11.14 | 0.82 | 6.18 | 0.53 | 3.48 | 0.45 | 2.38 | 0.32 | 1.59 | 0.23 | 1.15 |

| C 22–23 | Rubber and plastic | 0.92 | 1.41 | 0.91 | 1.23 | 0.80 | 1.16 | 0.75 | 1.13 | 0.65 | 1.17 | 0.57 | 1.08 |

| C 24–25 | Metal products | 0.96 | 1.36 | 0.93 | 1.16 | 0.82 | 1.19 | 0.74 | 1.16 | 0.57 | 1.05 | 0.47 | 1.03 |

| C 26–27 | Computer and electronics | 0.96 | 1.03 | 0.94 | 1.05 | 0.85 | 1.05 | 0.78 | 1.51 | 0.67 | 1.08 | 0.60 | 1.04 |

| C 28 | Machinery | 0.88 | 1.24 | 0.83 | 1.15 | 0.71 | 1.10 | 0.65 | 1.06 | 0.53 | 1.05 | 0.47 | 1.05 |

| C 29–30 | Transport equipment | 0.93 | 1.21 | 0.86 | 1.08 | 0.67 | 1.14 | 0.57 | 1.08 | 0.41 | 1.15 | 0.34 | 1.06 |

| C 31 | Furniture | 0.95 | 1.08 | 0.93 | 1.04 | 0.86 | 1.08 | 0.81 | 1.09 | 0.72 | 1.02 | 0.66 | 1.01 |

| C 32 | Other manufacturing | 0.88 | 1.80 | 0.85 | 2.03 | 0.71 | 1.43 | 0.63 | 1.22 | 0.51 | 1.31 | 0.41 | 1.05 |

| C 33 | Repair and installation | 0.93 | 2.54 | 0.88 | 1.02 | 0.79 | 1.00 | 0.73 | 1.01 | 0.63 | 1.01 | 0.58 | 1.03 |

| D 35 | Electricity, gas, steam and air | 0.93 | 2.25 | 0.92 | 1.57 | 0.74 | 2.09 | 0.69 | 2.26 | 0.54 | 1.12 | 0.45 | 1.05 |

| E 36–39 | Water, sewerage and waste | 0.89 | 1.49 | 0.86 | 1.30 | 0.72 | 1.25 | 0.66 | 1.28 | 0.54 | 1.20 | 0.45 | 1.11 |

| F 41–43 | Construction | 0.91 | 1.78 | 0.86 | 1.19 | 0.77 | 1.15 | 0.72 | 1.25 | 0.64 | 1.26 | 0.57 | 1.07 |

| G 45–47 | Wholesale and retail | 0.89 | 2.07 | 0.83 | 1.58 | 0.71 | 1.08 | 0.63 | 1.06 | 0.48 | 1.10 | 0.38 | 1.06 |

| H 49–53 | Transportation and storage | 0.95 | 1.23 | 0.91 | 1.17 | 0.81 | 1.09 | 0.73 | 1.07 | 0.59 | 1.03 | 0.51 | 1.03 |

| I 55–56 | Accommodation and food service | 0.70 | 2.55 | 0.62 | 1.69 | 0.36 | 2.16 | 0.29 | 2.21 | 0.17 | 1.57 | 0.10 | 1.22 |

| J 58–63 | Information and communication | 0.97 | 1.58 | 0.94 | 1.09 | 0.86 | 1.11 | 0.80 | 1.08 | 0.71 | 1.04 | 0.66 | 1.00 |

| K 64–66 | Financial and insurance activities | 0.96 | 1.04 | 0.92 | 1.08 | 0.76 | 1.06 | 0.66 | 1.05 | 0.52 | 1.02 | 0.42 | 1.05 |

| L 68 | Real estate activities | 0.87 | 1.71 | 0.78 | 1.41 | 0.59 | 1.52 | 0.50 | 1.45 | 0.33 | 1.07 | 0.26 | 1.08 |

| M 69–75 | Scientific and technical activities | 0.91 | 2.24 | 0.86 | 1.34 | 0.74 | 1.24 | 0.67 | 1.17 | 0.56 | 1.09 | 0.48 | 1.03 |

| N 77–82 | Administrative and support service | 0.89 | 1.00 | 0.83 | 1.08 | 0.72 | 1.08 | 0.66 | 1.12 | 0.55 | 1.02 | 0.50 | 1.01 |

| O 84 | Public administration and defense | 0.91 | 2.51 | 0.86 | 1.83 | 0.71 | 1.29 | 0.64 | 1.16 | 0.51 | 1.04 | 0.44 | 1.02 |

| P 85 | Education | 0.90 | 1.54 | 0.84 | 1.27 | 0.66 | 1.34 | 0.56 | 1.20 | 0.41 | 1.04 | 0.37 | 1.03 |

| Q 86–88 | Human health activities | 0.79 | 4.11 | 0.71 | 1.28 | 0.53 | 1.32 | 0.45 | 1.25 | 0.35 | 1.21 | 0.28 | 1.11 |

| R 90–93 | Arts, entertainment and recreation | 0.82 | 5.69 | 0.77 | 4.00 | 0.58 | 2.17 | 0.51 | 1.90 | 0.38 | 1.21 | 0.31 | 1.10 |

| S 94–96 | Other service activities | 0.84 | 1.53 | 0.78 | 2.98 | 0.62 | 1.91 | 0.54 | 1.58 | 0.40 | 1.14 | 0.33 | 1.04 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sjöstrand, K.; Klingberg, J.; Zadeh, N.S.; Haraldsson, M.; Rosén, L.; Lindhe, A. The Value of Water—Estimating Water-Disruption Impacts on Businesses. Water 2021, 13, 1565. https://doi.org/10.3390/w13111565

Sjöstrand K, Klingberg J, Zadeh NS, Haraldsson M, Rosén L, Lindhe A. The Value of Water—Estimating Water-Disruption Impacts on Businesses. Water. 2021; 13(11):1565. https://doi.org/10.3390/w13111565

Chicago/Turabian StyleSjöstrand, Karin, Josefine Klingberg, Noor Sedehi Zadeh, Mattias Haraldsson, Lars Rosén, and Andreas Lindhe. 2021. "The Value of Water—Estimating Water-Disruption Impacts on Businesses" Water 13, no. 11: 1565. https://doi.org/10.3390/w13111565

APA StyleSjöstrand, K., Klingberg, J., Zadeh, N. S., Haraldsson, M., Rosén, L., & Lindhe, A. (2021). The Value of Water—Estimating Water-Disruption Impacts on Businesses. Water, 13(11), 1565. https://doi.org/10.3390/w13111565