Economic and Environmental Consequences of the ECJ Genome Editing Judgment in Agriculture

Abstract

1. Introduction

2. The Economic Impact Model and Scenario

3. Results and Discussion

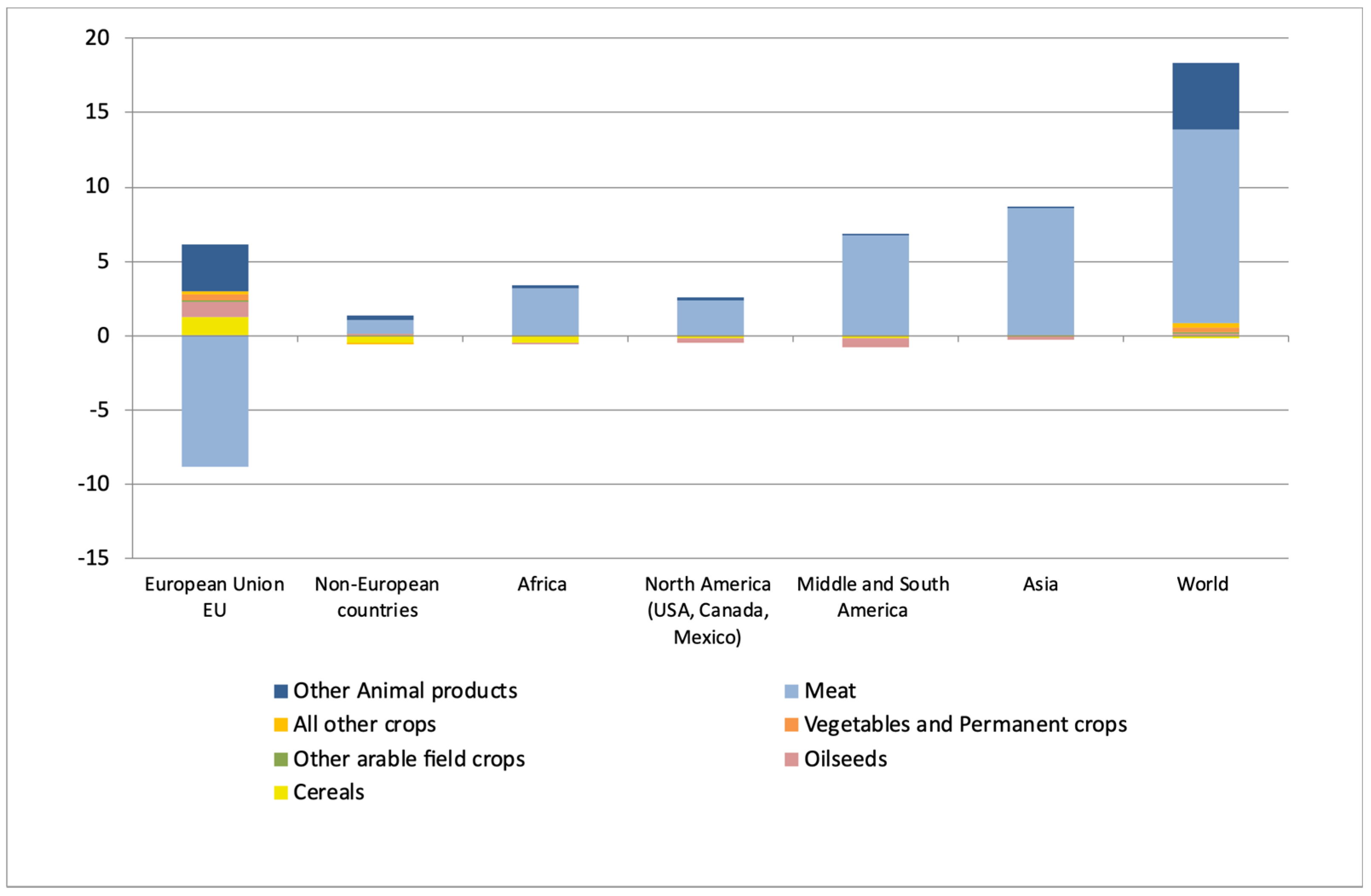

3.1. Economic Analysis

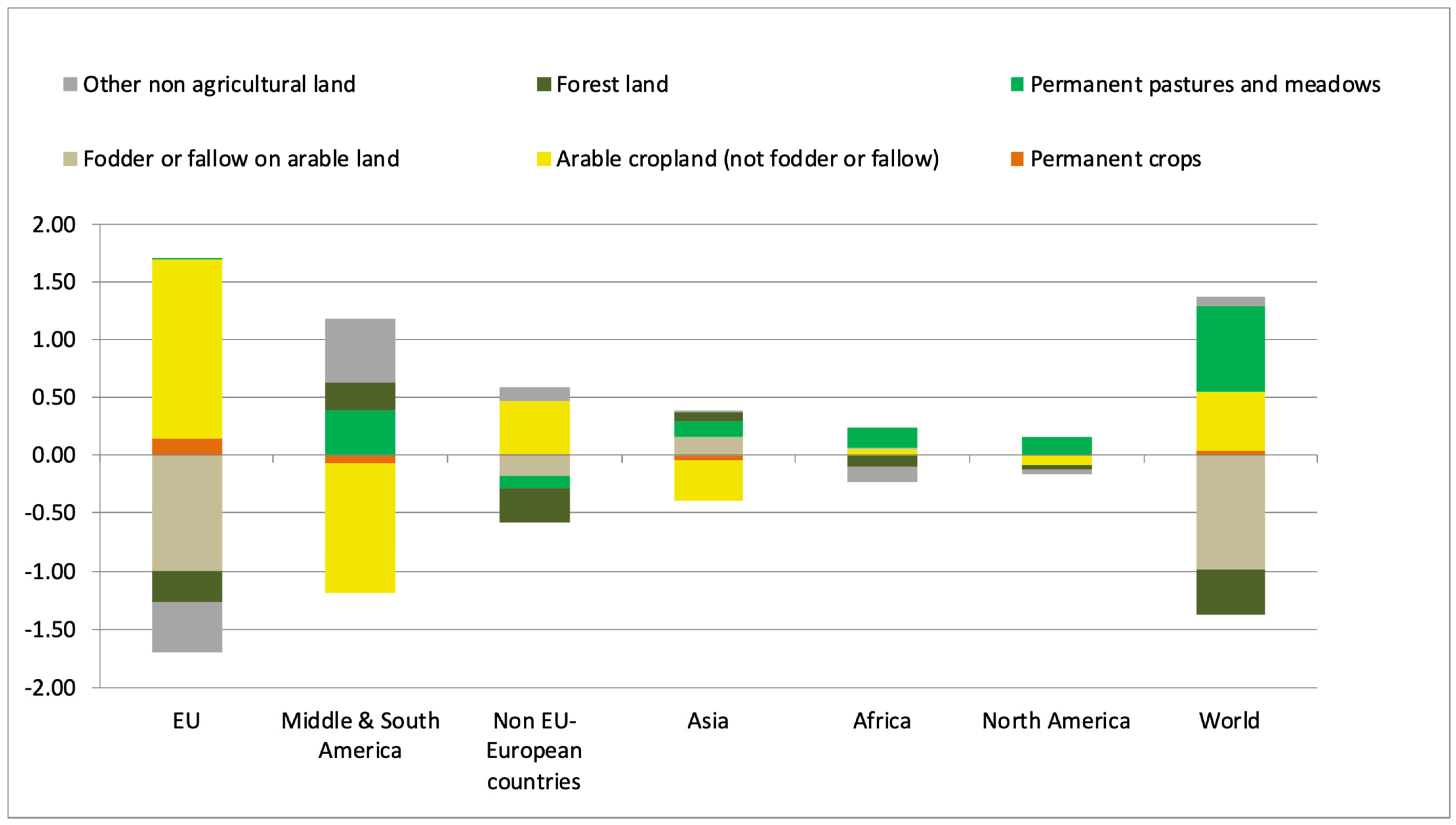

3.2. Land Use Change and Environmental Effects

3.3. Sensitivity Analysis

4. Discussion and Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| No. | Plant | Trait/Specification | Technological Specification | Developer, Producer, Country | Probably Traded as… |

|---|---|---|---|---|---|

| 1 | Potato | Product quality, non-browning | TALENs SDN1 | Calyxt, USA | IP |

| 2 | Potato | Product quality, reduced black spottiness | TALENs SDN1 | Simplot Plant Science, USA (Calyxt) | n.a. |

| 3 | Maize | Product quality, waxy corn | CRISPR/Cas9 SDN1 | Du Pont Pioneer, USA in Koop. China | IP—grown under contract Might occur in processed products |

| 4 | Maize | Product quality, higher starch levels | Meganuklease SDN1 | Agrivida, USA | IP |

| 5 | Maize | Product quality, reduced phytate production + herbicide tolerance | ZFN SDN3 | DowAgroScience, USA | IP |

| 6 | Maize | Fungal resistance, Northern Leaf Blight (NLB) | CRISPR/Cas9 (Cisgenesis) SDN3 | Du Pont Pioneer, USA | Commodity |

| 7 | Maize | Increased yield, increased photosynthesis efficiency | Meganuklease SDN3 | Benson Hill Biosystems, USA | Commodity |

| 8 | Mushroom | Product quality, non-browning | CRISPR/Cas9 SDN1 | Penn State University, USA | IP |

| 9 | Wheat | Product quality, increased nutritional value | TALENs SDN1 | Calyxt, USA | IP |

| 10 | Wheat | Fungal resistance, resistance to powdery mildew | CRISPR/Cas9 TALENs SDN1 | u.a. Calyxt, USA | Commodity |

| 11 | Soybean | Abiotic stress, drought and salt tolerance | CRISPR/Cas9 SDN1 | USDA-ARS, USA | Commodity |

| 12 | Soybean | Product quality, high oleic content, low linoleic content | TALENs SDN1 | Cellectis Plant Science, USA | IP |

| 13 | Rice | Fungal resistance, resistance to powdery mildew | TALENs SDN1 | Iowa State University, USA | Commodity |

| 14 | Tomato | Growth characteristics, easy separation of fruit from stem | CRISPR/Cas9 SDN1 | University of Florida, USA | n.a |

| 15 | Pennycress | Product quality, altered oil composition | CRISPR/Cas9 SDN1 | Illinois State University, USA | n.a. |

| 16 | Tobacco | Product quality, reduced nicotine content | Meganuklease SDN1 | North Carolina State University | n.a. |

| 17 | Rapeseed | Herbicide tolerance | ODM | Cibus, Kanada; USA | Commodity |

| Scenario | Commodity | Production | Human Consumption | Feed | Imports | Exports | Commodity | Production | Human Consumption | Feed | Imports | Exports |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10% | Wheat | 1 | 2 | 6 | −100 | −23 | Rapeseed oil | 2 | 2 | 34 | 10 | −5 |

| 25% | 1 | 2 | 6 | −100 | −23 | 3 | 3 | 37 | 11 | −4 | ||

| 50% | 0 | 2 | 6 | −100 | −23 | 3 | 3 | 42 | 12 | −4 | ||

| cease | 0 | 2 | 5 | −100 | −26 | 5 | 4 | 66 | 14 | −2 | ||

| 10% | Barley | 0 | 0 | 5 | −100 | −18 | Sunflower oil | −1 | 2 | 28 | 14 | −10 |

| 25% | 0 | 0 | 5 | −100 | −18 | −1 | 3 | 30 | 15 | −10 | ||

| 50% | 0 | 0 | 4 | −100 | −18 | −1 | 3 | 34 | 16 | −11 | ||

| cease | −1 | 0 | 4 | −100 | −19 | 1 | 4 | 51 | 18 | −10 | ||

| 10% | Maize | 7 | 0 | −13 | −100 | −27 | Soya oil | −6 | −7 | −28 | −94 | −83 |

| 25% | 7 | 0 | −13 | −100 | −27 | −7 | −7 | −29 | −96 | −86 | ||

| 50% | 6 | 0 | −14 | −100 | −28 | −9 | −8 | −30 | −98 | −88 | ||

| cease | 5 | 0 | −15 | −100 | −28 | −19 | −15 | −37 | −100 | −96 | ||

| 10% | Other Cereals | 8 | 23 | −22 | −99 | −52 | Palm oil | 0 | 4 | 0 | 4 | 0 |

| 25% | 8 | 24 | −22 | −100 | −53 | 0 | 4 | 0 | 4 | 0 | ||

| 50% | 8 | 24 | −22 | −100 | −53 | 0 | 4 | 0 | 4 | 0 | ||

| cease | 9 | 25 | −21 | −100 | −55 | 0 | 6 | 0 | 4 | 0 | ||

| 10% | Rapeseed | −3 | −2 | 5 | 13 | −13 | Rapeseed cake | 2 | −2 | 8 | 39 | −40 |

| 25% | −3 | −2 | 6 | 14 | −14 | 3 | −2 | 9 | 42 | −42 | ||

| 50% | −4 | −2 | 7 | 15 | −15 | 3 | −3 | 10 | 47 | −45 | ||

| cease | −5 | −4 | 9 | 23 | −22 | 5 | −4 | 15 | 69 | −56 | ||

| 10% | Sunflower seed | −12 | −3 | −9 | 46 | −16 | Sunflower cake | −1 | −1 | 22 | 46 | −40 |

| 25% | −13 | −4 | −10 | 49 | −17 | −1 | −1 | 24 | 50 | −42 | ||

| 50% | −14 | −4 | −11 | 53 | −18 | 0 | −1 | 27 | 55 | −45 | ||

| cease | −17 | −5 | −14 | 73 | −25 | 1 | −2 | 40 | 79 | −54 | ||

| 10% | Soya seed | 137 | −13 | −29 | −55 | −98 | Soya cake | −6 | 0 | −53 | −77 | −99 |

| 25% | 150 | −14 | −31 | −60 | −99 | −7 | 1 | −56 | −80 | −100 | ||

| 50% | 169 | −15 | −34 | −67 | −99 | −8 | 3 | −60 | −85 | −100 | ||

| cease | 265 | −17 | −51 | −100 | −100 | −19 | 23 | −73 | −100 | −100 | ||

| 10% | Pulses | 6 | −1 | 32 | 31 | −19 | Sugar | −2 | 0 | 0 | 2 | −1 |

| 25% | 7 | −1 | 35 | 34 | −19 | −2 | 0 | 0 | 1 | −1 | ||

| 50% | 8 | −1 | 39 | 38 | −21 | −2 | 0 | −1 | 1 | 0 | ||

| cease | 15 | −2 | 61 | 56 | −25 | −2 | 0 | −2 | −1 | 1 | ||

| 10% | Pork | −6 | −1 | 0 | 39 | −29 | Biodiesel | −2 | 0 | 0 | 8 | −7 |

| 25% | −7 | −1 | 0 | 42 | −30 | −2 | 0 | 0 | 8 | −7 | ||

| 50% | −7 | −1 | 0 | 47 | −33 | −2 | 0 | 0 | 8 | −7 | ||

| cease | −9 | −1 | 0 | 69 | −42 | −2 | 0 | 0 | 9 | −8 | ||

| 10% | Poultry | −7 | −1 | 0 | 70 | −29 | Bioethanol | 0 | 0 | 0 | 3 | −3 |

| 25% | −7 | −1 | 0 | 77 | −31 | 0 | 0 | 0 | 3 | −2 | ||

| 50% | −8 | −1 | 0 | 86 | −33 | 0 | 0 | 0 | 2 | −2 | ||

| cease | −10 | −1 | 0 | 130 | −42 | 1 | 0 | 0 | 0 | 1 | ||

| 10% | Fish | 0 | 0 | 21 | 3 | 0 | DDG | −1 | 0 | 0 | 426 | −51 |

| 25% | 0 | 0 | 23 | 3 | 0 | −1 | 0 | 1 | 474 | −53 | ||

| 50% | 0 | 0 | 25 | 4 | 0 | 0 | 0 | 1 | 546 | −55 | ||

| cease | 0 | 0 | 38 | 5 | 0 | 2 | 0 | 5 | 899 | −63 |

References

- Modrzejewski, D.; Hartung, F.; Sprink, T.; Krause, D.; Kohl, C.; Wilhelm, R. What is the available evidence for the range of applications of genome-editing as a new tool for plant trait modification and the potential occurrence of associated off-target effects: A systematic map. Environ. Evid. 2019, 8, 27. [Google Scholar] [CrossRef]

- Friedrichs, S.; Takasu, Y.; Kearns, P.; Dagallier, B.; Oshima, R.; Schofield, J.; Moreddu, C. An overview of regulatory approaches to genome editing in agriculture. Biotechnol. Res. Innov. 2019, 3, 208–220. [Google Scholar] [CrossRef]

- Ricroch, A. Global developments of genome editing in agriculture. Transgenic Res. 2019, 28, 45–52. [Google Scholar] [CrossRef] [PubMed]

- Kohl, C.; Modrzejewski, D.; Kopertekh, L.; Dietz-Pfeilstetter, A.; Fischer, M.; Menz, J.; Sprink, T.; Hartung, F.; Wilhelm, R. Anlage 4—Übersicht über Nutz- und Zierpflanzen, die Mittels Gentechnik und Neuer Molekularbiologischer Techniken für die Bereiche Ernährung, Landwirtschaft, Gartenbau, Arzneimittelherstellung und -Forschung Entwickelt Werden. BMEL. Available online: https://www.bmel.de/SharedDocs/Downloads/DE/_Landwirtschaft/Gruene-Gentechnik/NMT_Stand-Regulierung_Anlage4.pdf?__blob=publicationFile&v=3 (accessed on 14 May 2021).

- Menz, J.; Modrzejewski, D.; Hartung, F.; Wilhelm, R.; Sprink, T. Genome Edited Crops Touch the Market: A View on the Global Development and Regulatory Environment. Front. Plant Sci. 2020, 11, 586027. [Google Scholar] [CrossRef] [PubMed]

- European Commission; Joint Research Centre. Current and Future Market Applications of New Genomic Techniques; LU Publications Office: Geneva, Switzerland, 2021; Available online: https://data.europa.eu/doi/10.2760/02472 (accessed on 12 May 2021).

- Court of Justice of the European Union (ECJ). Press Release No 111/18. Luxembourg. July 2018. Available online: https://curia.europa.eu/jcms/upload/docs/application/pdf/2018-07/cp180111en.pdf (accessed on 14 June 2021).

- Hartung, F.; Schiemann, J. Precise plant breeding using new genome editing techniques: Opportunities, safety and regulation in the EU. Plant J. 2014, 78, 742–752. [Google Scholar] [CrossRef] [PubMed]

- European Parliament (EP); European Council (EC). Regulation (EC) No 1830/2003 of the European Parliament and of the Council of 22 September 2003 Concerning the Traceability and Labelling of Genetically Modified Organisms and the Traceability of Food and Feed Products Produced from Genetically Modified Organisms and Amending Directive 2001/18/EC. Available online: https://eur-lex.europa.eu/legal-content/EN/ALL/?uri=CELEX%3A32003R1830 (accessed on 14 May 2021).

- Grohmann, L.; Keilwagen, J.; Duensing, N.; Dagand, E.; Hartung, F.; Wilhelm, R. Detection and Identification of Genome Editing in Plants: Challenges and Opportunities. Front. Plant Sci. 2019, 10, 236. [Google Scholar] [CrossRef]

- Schmidt, S.M.; Belisle, M.; Frommer, W.B. The evolving landscape around genome editing in agriculture: Many countries have exempted or move to exempt forms of genome editing from GMO regulation of crop plants. EMBO Rep. 2020, 21. [Google Scholar] [CrossRef]

- Sprink, T.; Eriksson, D.; Schiemann, J.; Hartung, F. Regulatory hurdles for genome editing: Process- vs. product-based approaches in different regulatory contexts. Plant Cell Rep. 2016, 35, 1493–1506. [Google Scholar] [CrossRef]

- Tsuda, M.; Watanabe, K.N.; Ohsawa, R. Regulatory Status of Genome-Edited Organisms Under the Japanese Cartagena Act. Front. Bioeng. Biotechnol. 2019, 7, 387. [Google Scholar] [CrossRef]

- Eckerstorfer, M.F.; Engelhard, M.; Heissenberger, A.; Simon, S.; Teichmann, H. Plants Developed by New Genetic Modification Techniques—Comparison of Existing Regulatory Frameworks in the EU and Non-EU Countries. Front. Bioeng. Biotechnol. 2019, 7, 26. [Google Scholar] [CrossRef]

- Bömeke, O.; Kahrmann, J.; Matthies, A. Detaillierte Übersicht zum Regulatorischen Status der Neuen Molekularbiologischen Techniken (NMT) in Ausgewählten Drittstaaten. 2018. Available online: https://www.bvl.bund.de/SharedDocs/Downloads/06_Gentechnik/molekulare_techniken/molekulare_techniken_bericht_anlage1.pdf (accessed on 14 May 2021).

- Cohen, J. Fields of dreams. Science 2019, 365, 422–425. [Google Scholar] [CrossRef]

- Roïz, J. Limits of the current EU regulatory framework on GMOs: Risk of not authorized GM event-traces in imports. OCL Ol. Corps Gras Lipides 2014, 21. [Google Scholar] [CrossRef]

- Kalaitzandonakes, N.; Kaufman, J.; Miller, D. Potential economic impacts of zero thresholds for unapproved GMOs: The EU case. Food Policy 2014, 45, 146–157. [Google Scholar] [CrossRef]

- Phillipson, M.; Smyth, S.J. Regulatory Lags for Genetically Modified Crops: Legal and Political Perspectives. In The Coexistence of Genetically Modified, Organic and Conventional Foods: Government Policies and Market Practices; Kalaitzandonakes, N., Phillips, P.W.B., Wesseler, J., Smyth, S.J., Eds.; Springer: New York, NY, USA, 2016; pp. 197–206. [Google Scholar] [CrossRef]

- Polansek, T. Syngenta Drops Lawsuit against Bunge over Biotech Viptera corn. Reuters. 17 December 2014. Available online: https://www.reuters.com/article/syngenta-ag-bunge-lawsuit-idUSL1N0U101I20141217 (accessed on 14 May 2021).

- Pearson, D.R. Cargill v. Syngenta: Biotechnology and Trade. Cato Institute. 1 October 2014. Available online: https://www.cato.org/blog/cargill-v-syngenta-biotechnology-trade (accessed on 14 May 2021).

- Polansek, T. Syngenta Faces Second Lawsuit over GMO Corn Rejected by China. Reuters. 2014. Available online: https://www.reuters.com/article/us-syngenta-seed-trans-coastal-idUSKBN0HB2OQ20140917 (accessed on 14 May 2021).

- NZZ. Syngenta Wird Auch von Trans Coastal Supply Wegen Maissaatgut Verklagt. Neue Zür. Ztg. 2014. Available online: https://www.nzz.ch/wirtschaft/newsticker/syngenta-wird-auch-von-trans-coastal-supply-wegen-maissaatgut-verklagt-1.18385369 (accessed on 14 May 2021).

- Reuters. REFILE-Syngenta Sues Cargill, ADM in GMO Corn Fight. Reuters. 2015. Available online: https://www.reuters.com/article/syngenta-seed-traders-idUSL1N13F18V20151120 (accessed on 14 May 2021).

- Fisher, M. Lack of Chinese Approval for Import of US Agricultural Products Containing Agrisure VipteraTM MIR 162: A Case Study on Economic Impacts in Marketing Year 2013/14; NGFA: Washington, DC, USA, 2014; Available online: http://ngfa.org/wp-content/uploads/Agrisure-Viptera-MIR-162-Case-Study-An-Economic-Impact-Analysis.pdf (accessed on 14 June 2021).

- Consmüller, N.; Vaasen, A.; Bartsch, D. Are genome edited products credence goods? Implications for regulation and governance. In Poster presented at the ISBR Symposium, Tarragona; ISBR: Karnataka, India, 2019. [Google Scholar]

- Eriksson, D.; Kershen, D.; Nepomuceno, A.; Pogson, B.J.; Prieto, H.; Purnhagen, K. A comparison of the EU regulatory approach to directed mutagenesis with that of other jurisdictions, consequences for international trade and potential steps forward. New Phytol. 2019, 222, 1673–1684. [Google Scholar] [CrossRef] [PubMed]

- Smyth, S.; Phillips, P. Product Differentiation Alternatives: Identity Preservation, Segregation, and Traceability. AgBioForum 2003, 5. [Google Scholar]

- Maaß, O.; Consmüller, N.; Kehlenbeck, H. Socioeconomic Impact of Genome Editing on Agricultural Value Chains: The Case of Fungal-Resistant and Coeliac-Safe Wheat. Sustainability 2019, 11, 6421. [Google Scholar] [CrossRef]

- FAOSTAT. Available online: http://www.fao.org/faostat/en/#data/ (accessed on 4 June 2021).

- Britz, W.; Witzke, P. CAPRI Model Documentation 2014. Bonn. Available online: https://www.capri-model.org/docs/capri_documentation.pdf (accessed on 14 May 2021).

- Jansson, T.; Heckelei, T. Estimating a Primal Model of Regional Crop Supply in the European Union: Regional Crop Supply in the EU. J. Agric. Econ. 2011, 62, 137–152. [Google Scholar] [CrossRef]

- Armington, P.S. A Theory of Demand for Products Distinguished by Place of Production. IMF Staff Pap. 1969, 1969. [Google Scholar] [CrossRef]

- European Commission; Joint Research Centre; Institute for Prospective Technological Studies. Methodology to Assess EU Biofuel Policies: The CAPRI Approach; LU Publications Office: Geneva, Switzerland, 2013; Available online: https://data.europa.eu/doi/10.2791/82235 (accessed on 14 May 2021).

- Golub, A.A.; Henderson, B.B.; Hertel, T.W.; Gerber, P.J.; Rose, S.K.; Sohngen, B. Global climate policy impacts on livestock, land use, livelihoods, and food security. Proc. Natl. Acad. Sci. USA 2013, 110, 20894–20899. [Google Scholar] [CrossRef] [PubMed]

- Hörtenhuber, S.J.; Lindenthal, T.; Zollitsch, W. Reduction of greenhouse gas emissions from feed supply chains by utilizing regionally produced protein sources: The case of Austrian dairy production: Greenhouse gas emissions from regional protein sources for dairy cows. J. Sci. Food Agric. 2011, 91, 1118–1127. [Google Scholar] [CrossRef]

- Weightman, R.M.; Cottrill, B.R.; Wiltshire, J.J.J.; Kindred, D.R.; Sylvester-Bradley, R. Opportunities for avoidance of land-use change through substitution of soya bean meal and cereals in European livestock diets with bioethanol coproducts: Substitution of soya and cereals with bioethanol coproducts. GCB Bioenergy 2011, 3, 158–170. [Google Scholar] [CrossRef]

- Sasu-Boakye, Y.; Cederberg, C.; Wirsenius, S. Localising livestock protein feed production and the impact on land use and greenhouse gas emissions. Animal 2014, 8, 1339–1348. [Google Scholar] [CrossRef] [PubMed]

- Henseler, M.; Piot-Lepetit, I.; Ferrari, E.; Mellado, A.G.; Banse, M.; Grethe, H.; Parisi, C.; Helaine, S. On the asynchronous approvals of GM crops: Potential market impacts of a trade disruption of EU soy imports. Food Policy 2013, 41, 166–176. [Google Scholar] [CrossRef]

- Muller, A.; Bautze, L. Agriculture and Deforestation: The EU Common Agricultural Policy, Soy, and Forest Destruction; Fern: Moreton in Marsh, UK, 2017. [Google Scholar]

- Weisser, W.W.; Roscher, C.; Meyer, S.T.; Ebeling, A.; Luo, G.; Allan, E.; Bebler, H.; Barnard, R.L.; Buchmann, N.; Buscot, F.; et al. Biodiversity effects on ecosystem functioning in a 15-year grassland experiment: Patterns, mechanisms, and open questions. Basic Appl. Ecol. 2017, 23, 1–73. [Google Scholar] [CrossRef]

- Kuiper, M.H.; van Tongeren, F.W. Using Gravity to Move Armington-an Empirical Approach to the Small Initial Trade Share Problem in General Equilibrium Models; OCED: Metta Fort, France, 2007. [Google Scholar]

- Gocht, A.; Britz, W.; Ciaian, P.; Paloma, S.G. Farm type effects of an EU-wide direct payment harmonisation. J. Agric. Econ. 2013, 64, 1–32. [Google Scholar] [CrossRef]

- Wasmer, M. Roads Forward for European GMO Policy—Uncertainties in Wake of ECJ Judgment Have to be Mitigated by Regulatory Reform. Front. Bioeng. Biotechnol. 2019, 7, 132. [Google Scholar] [CrossRef] [PubMed]

- European Commission. Study on the Status of New Genomic Techniques Under Union Law and in Light of the Court of Justice Ruling in Case C-528/16’, Brussels, COMMISSION STAFF WORKING DOCUMENT SWD(2021) 92 Final. April 2021. Available online: https://data.consilium.europa.eu/doc/document/ST-8285-2021-INIT/en/pdf (accessed on 14 June 2021).

- Eriksson, D.; Custers, R.; Björnberg, K.E.; Hansson, S.O.; Purnhagen, K.; Qaim, M.; Romeis, J.; Schiemann, J.; Schleissing, S.; Tosun, J.; et al. Options to Reform the European Union Legislation on GMOs: Scope and Definitions. Trends Biotechnol. 2020, 38, 231–234. [Google Scholar] [CrossRef]

| Production | Human con. | Processing | Biofuels | Feed Use | Imports | Exports | Market Volume * | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1000 t abs. | % | 1000 t abs. | % | 1000 t abs. | % | 1000 t abs. | % | 1000 t abs. | % | 1000 t abs. | % | 1000 t abs. | % | % | |

| Wheat | −465 | - | 960 | 2 | −307 | −8 | 232 | 6 | 2143 | 5 | −3312 | −100 | −6804 | −26 | −3 |

| Barley | −338 | −1 | 10 | - | 304 | 19 | 1112 | 4 | −421 | −100 | −2185 | −19 | −1 | ||

| Grain maize | 3080 | 5 | 15 | - | −967 | −15 | −469 | −14 | −8890 | −15 | −13,541 | −100 | −151 | −28 | −14 |

| Other cereals | 1201 | 9 | 316 | 25 | −2927 | −41 | −99 | −25 | −2288 | −21 | −6202 | −100 | −3 | −60 | −25 |

| Pork meat | −2094 | −9 | −239 | −1 | −138 | −30 | 34 | 67 | −1682 | −42 | −9 | ||||

| Poultry meat | −1452 | −10 | −155 | −1 | −1 | −50 | 241 | 130 | −1056 | −42 | −8 | ||||

| Sugar | −398 | −2 | 13 | - | 1 | - | −51 | −2 | −2 | −3 | −22 | −1 | 17 | 1 | −2 |

| Fish and aquatic products | 33 | - | −3 | −1 | 609 | 38 | 627 | 5 | −13 | − | 4 | ||||

| Production | Human con. | Processing | Biofuels | Feed Use | Imports | Exports | Market Volume * | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1000 t abs. | % | 1000 t abs. | % | 1000 t abs. | % | 1000 t abs. | % | 1000 t abs. | % | 1000 t abs. | % | 1000 t abs. | % | % | |

| Soybeans | 6.871 | 265 | −58 | −17 | −2.905 | −25 | 478 | - | −471 | −51 | −10.405 | −100 | −101 | −100 | −27 |

| Soy oil | −425 | −19 | −292 | −15 | −243 | −100 | −589 | −94 | −102 | −37 | −1.566 | −100 | −766 | −96 | −52 |

| Soy cake | −1.732 | −19 | 23 | 23 | −170 | −100 | −20.521 | −73 | −19.605 | −100 | −669 | −100 | −74 | ||

| Rapeseed | −750 | −5 | −33 | −4 | 1.108 | 5 | 1.229 | - | 69 | 9 | 1.885 | 23 | −8 | −22 | 5 |

| Rapeseed oil | 490 | 5 | 112 | 4 | 31 | 1 | 156 | 4 | 260 | 66 | 59 | 14 | −10 | −2 | 6 |

| Rapeseed cake | 625 | 5 | −3 | −4 | −120 | −43 | 1.630 | 15 | 293 | 69 | −589 | −56 | 7 | ||

| Sunflower seed | −1.677 | −17 | −33 | −5 | −371 | −6 | 53 | - | −45 | −14 | 499 | 73 | −730 | −25 | −11 |

| Sunflower oil | 33 | 1 | 107 | 4 | −2 | −1 | 19 | 5 | 85 | 51 | 148 | 18 | −28 | −10 | 5 |

| Sunflower cake | 45 | 1 | −2 | 2.558 | 40 | 2.448 | 79 | −65 | −54 | 38 | |||||

| Pulses | 379 | 15 | −25 | −2 | −8 | −20 | 990 | 61 | 512 | 55 | −67 | −25 | 25 | ||

| Palm oil | 53 | 6 | −10 | 222 | 13 | 265 | 4 | 0 | 4 | ||||||

| Bio ethanol | 44 | 1 | −1 | 0 | 1 | 1 | 1 | ||||||||

| Bio diesel | −182 | −2 | 108 | 9 | −73 | −8 | −1 | ||||||||

| DDG | 86 | 2 | 197 | 5 | 105 | 900 | −6 | −63 | 5 | ||||||

| Ruminants | Granivorous | |||||||

|---|---|---|---|---|---|---|---|---|

| For Dairy Production | Other Cows | Male Adult Cattle High | Male Adult Cattle Low | Sheep and Goat | Pig Fattening | Poultry Fattening | ||

| kg Dry Matter/Head | kg Dry Matter/Million Heads | |||||||

| Feed cereals | baseline | 997 | 390 | 580 | 145 | 11 | 212 | 4993 |

| % to baseline | 12 | −16 | −2 | 4 | −25 | - | 1 | |

| Protein-rich feed | baseline | 511 | 216 | 296 | 75 | 7 | 98 | 2246 |

| % to baseline | −32 | −54 | −39 | −55 | −36 | −2 | −1 | |

| Energy-rich feed | baseline | 63 | 24 | 30 | 7 | 1 | 9 | 156 |

| % to baseline | 1 | 1 | 2 | 1 | 4 | - | 2 | |

| Other feed (like DDG) | baseline | 133 | 101 | 67 | 30 | 5 | ||

| % to baseline | 0 | 5 | −2 | −2 | 1 | |||

| Gras | baseline | 8794 | 7682 | 6264 | 2928 | 157 | ||

| % to baseline | 18 | 14 | 17 | 12 | 24 | |||

| Fodder maize | baseline | 4315 | 1792 | 2470 | 1211 | 20 | ||

| % to baseline | −31 | −28 | −25 | −21 | −32 | |||

| Fodder grass from arable land | baseline | 2726 | 2649 | 1671 | 801 | 36 | ||

| % to baseline | 31 | 26 | 25 | 23 | 31 | |||

| European Union EU | Non-European Countries | North America (USA, Canada, Mexico) | Middle and South America | |||||

|---|---|---|---|---|---|---|---|---|

| Baseline in Euro/t | % | Baseline in Euro/t | % | Baseline in Euro/t | % | Baseline in Euro/t | % | |

| Products with price increase in all regions | ||||||||

| Rapeseed | 413 | 9 | 390 | 13 | 337 | 3 | 443 | 3 |

| Sunflower seed | 341 | 11 | 519 | 4 | 324 | 2 | 382 | 2 |

| Pulses | 296 | 11 | 660 | 5 | 902 | 1 | 711 | 1 |

| Pork meat | 1792 | 17 | 2366 | 1 | 1698 | 4 | 1647 | 2 |

| Other products | ||||||||

| Wheat | 208 | 5 | 411 | −5 | 237 | 0 | 202 | 0 |

| Barley | 183 | 4 | 305 | −4 | 184 | −1 | 163 | 1 |

| Grain maize | 210 | 6 | 288 | 0 | 197 | −1 | 191 | −3 |

| Other cereals | 165 | 9 | 199 | −2 | 168 | −2 | 176 | −6 |

| Soybeans | 396 | 169 | 380 | −8 | 407 | −4 | 340 | −3 |

| Poultry meat | 1781 | 12 | 3303 | −8 | 1414 | 1 | 1605 | 0 |

| Rapeseed oil | 847 | 2 | 934 | −10 | 845 | 1 | 837 | 1 |

| Soy oil | 772 | 59 | 764 | −8 | 822 | 0 | 832 | 1 |

| Rapeseed cake | 338 | 28 | 395 | 7 | 409 | −2 | 401 | −6 |

| Sunflower seed cake | 300 | 14 | 383 | 5 | 361 | −3 | 367 | −6 |

| Soy cake | 384 | 162 | 427 | −4 | 485 | −6 | 488 | −15 |

| Sugar | 506 | - | 614 | 2 | 452 | - | 257 | - |

| Bio ethanol | 1230 | - | 886 | 1 | 789 | - | 964 | - |

| DDG from bio-ethanol processing | 120 | 33 | 151 | −9 | 149 | −6 | 144 | −15 |

| Europe, Non-EU | Africa | North America | Middle and South America | Asia | Australia and New Zealand | Total | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| abs. | % | abs. | % | abs. | % | abs. | % | abs. | % | abs. | % | abs. | % | |

| Rapeseed | 318 | 11 | 1 | 74 | 1288 | 66 | 36 | 18 | 11 | 86 | 231 | 8 | 1884 | 23 |

| Sunflower seed | 207 | 84 | 20 | 135 | 17 | 103 | 66 | 90 | 188 | 56 | 0 | 92 | 499 | 73 |

| Pulses | 149 | 45 | 20 | 76 | 220 | 65 | 71 | 47 | 35 | 69 | 16 | 70 | 512 | 56 |

| Fish | 109 | 6 | 11 | 6 | 38 | 5 | 194 | 11 | 272 | 4 | 3 | 4 | 628 | 5 |

| Rapeseed cake | 287 | 68 | 6 | 2277 | 0 | 0 | 0 | 0 | 293 | 69 | ||||

| Sunflower seed cake | 1718 | 59 | 39 | 343 | 3 | 330 | 681 | 422 | 7 | 405 | 0 | 0 | 2447 | 79 |

| Total (in 1000 t) | Per ha (in kg) | ||||||

|---|---|---|---|---|---|---|---|

| Value in Baseline | abs. Change | % Change | Value in Baseline | abs. Change | % Change | ||

| source | Mineral fertilizer | 9552 | 1024 | 11 | 59 | 6 | 10 |

| Manure | 8144 | −607 | −7 | 50 | −4 | −7 | |

| Crop residues | 8543 | 805 | 9 | 53 | 5 | 9 | |

| Biological fixation | 1607 | 701 | 44 | 10 | 4 | 43 | |

| Atmospheric deposition | 1844 | 10 | 1 | 11 | 0 | 0 | |

| remains | Absorption by crop | −19,593 | 1412 | 7 | −121 | 8 | 7 |

| Surplus total | 10,097 | 459 | 5 | 63 | 3 | 4 | |

| Gaseous loss | −2794 | −107 | −4 | −17 | −1 | −4 | |

| Run off mineral | −395 | 35 | 9 | −2 | 0 | 9 | |

| Run off manure | −256 | −19 | −7 | −2 | −2 | −8 | |

| Surplus at soil level | 6543 | 541 | 8 | 41 | −44 | 8 | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Gocht, A.; Consmüller, N.; Thom, F.; Grethe, H. Economic and Environmental Consequences of the ECJ Genome Editing Judgment in Agriculture. Agronomy 2021, 11, 1212. https://doi.org/10.3390/agronomy11061212

Gocht A, Consmüller N, Thom F, Grethe H. Economic and Environmental Consequences of the ECJ Genome Editing Judgment in Agriculture. Agronomy. 2021; 11(6):1212. https://doi.org/10.3390/agronomy11061212

Chicago/Turabian StyleGocht, Alexander, Nicola Consmüller, Ferike Thom, and Harald Grethe. 2021. "Economic and Environmental Consequences of the ECJ Genome Editing Judgment in Agriculture" Agronomy 11, no. 6: 1212. https://doi.org/10.3390/agronomy11061212

APA StyleGocht, A., Consmüller, N., Thom, F., & Grethe, H. (2021). Economic and Environmental Consequences of the ECJ Genome Editing Judgment in Agriculture. Agronomy, 11(6), 1212. https://doi.org/10.3390/agronomy11061212