Assessing the Economic Viability of the Plastic Biorefinery Concept and Its Contribution to a More Circular Plastic Sector

Abstract

:

1. Introduction

2. Materials and Methods

2.1. Simulation and Assumptions

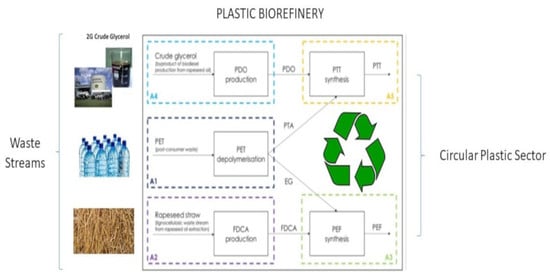

2.2. Process Design

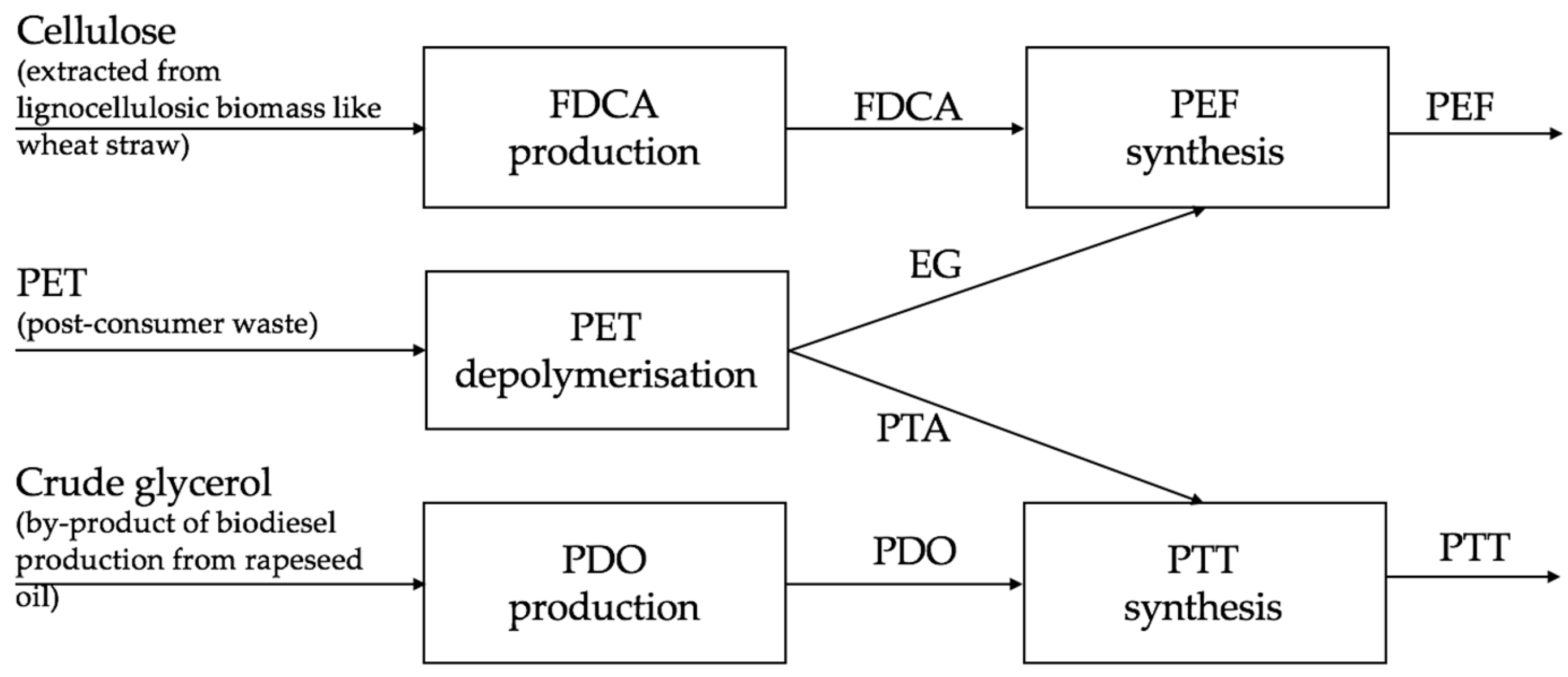

2.2.1. Area 1: PET Depolymerisation

2.2.2. Area 2: FDCA Synthesis

2.2.3. Area 3: PEF Synthesis

2.2.4. Area 4: PDO Synthesis

2.2.5. Area 5: PTT Synthesis

2.3. Cost Estimations and Cash-Flow Analysis

3. Results and Discussion

3.1. Minimum Selling Price

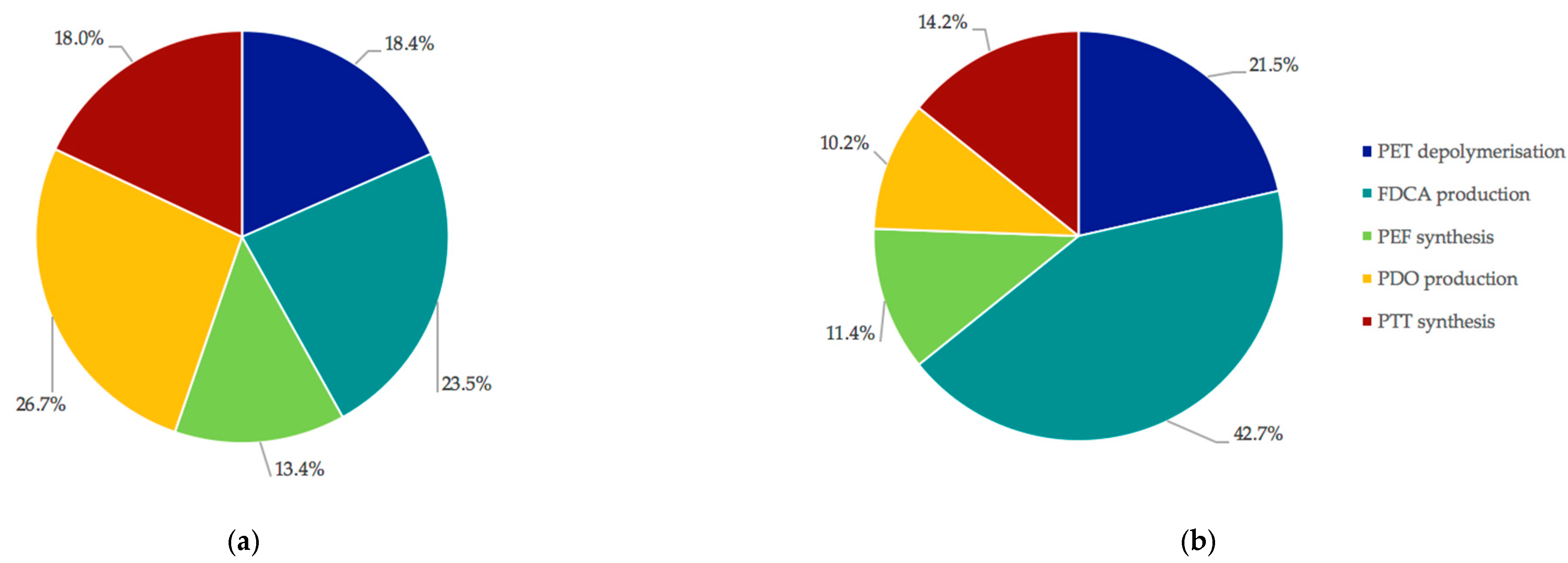

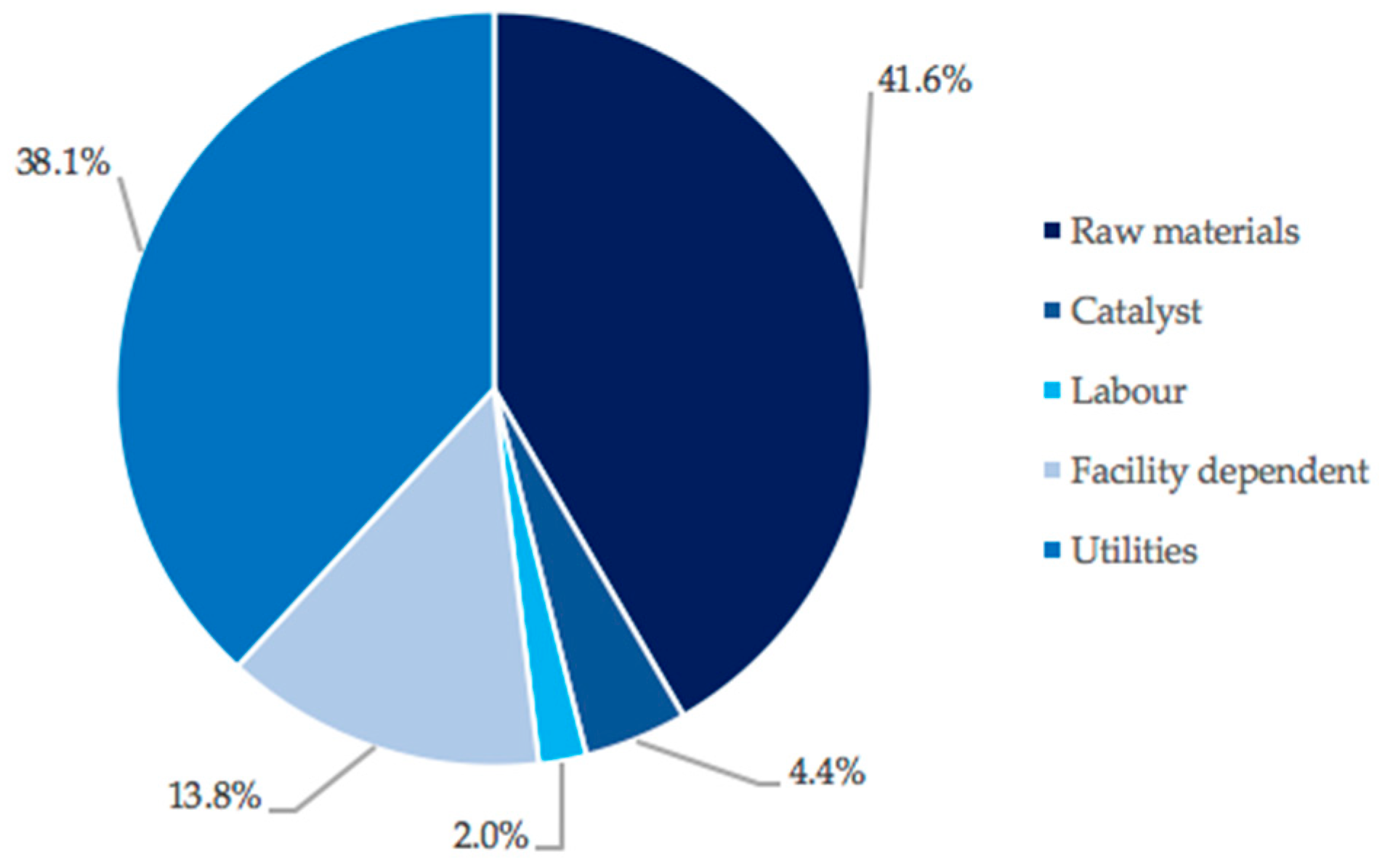

3.2. Capital and Operating Costs in Scenario 1

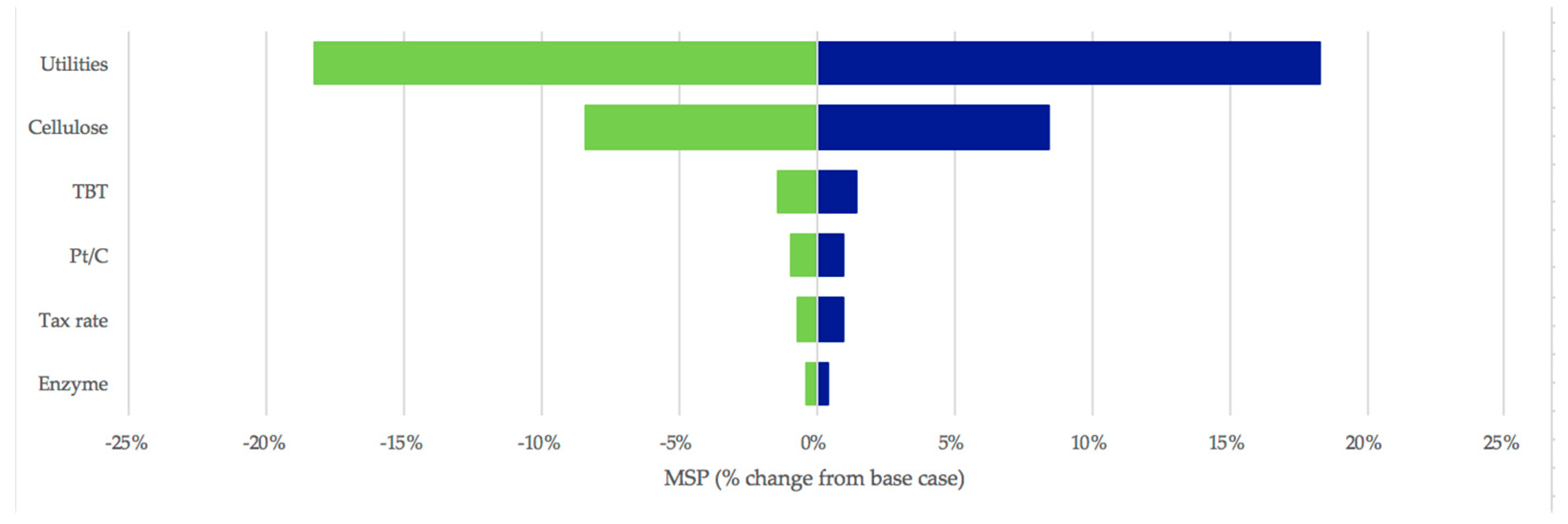

3.3. Sensitivity Analysis

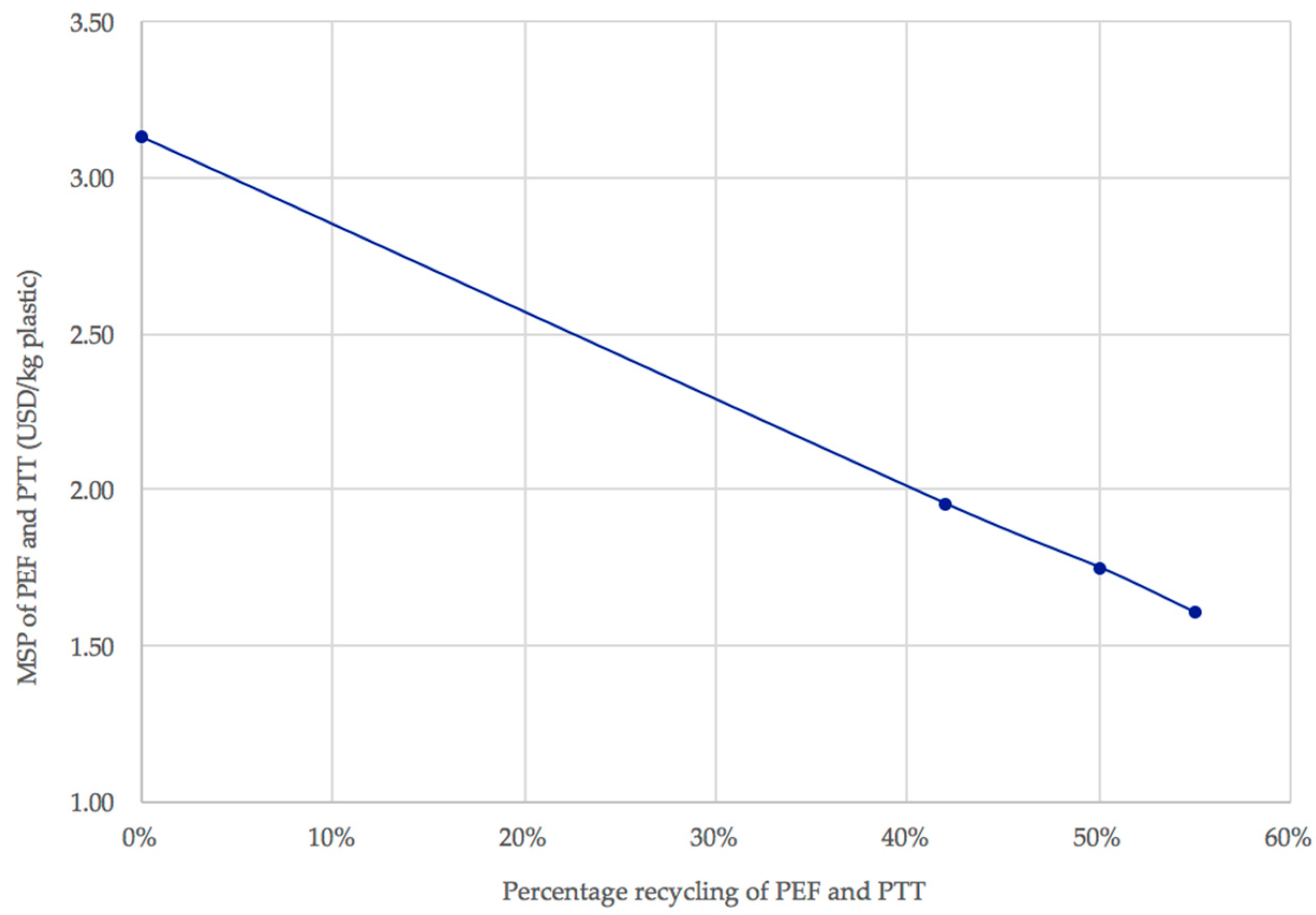

3.4. The Contribution of Policies to a More Circular Plastic Sector

- -

- PEF and PTT are depolymerised and the monomers purified in the same way as PET;

- -

- Less PET is produced (and therefore recycled) as PEF and PTT replace it;

- -

- Area 1 functions as normal;

- -

- Area 2 and 4 have less throughput (adjusted to meet the EG and PTA output from PET depolymerisation);

- -

- Area 3 and 5 have slightly less throughput.

4. Conclusions

Supplementary Materials

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Abbreviations

| DCCF | Discounted cumulative cash flow |

| FDCA | 2,5-furandicarboxylic acid |

| HMF | 5-hydroxymethyl furfural |

| MSP | Minimum selling price |

| PDO | 1,3-propane diol |

| PEF | Polyethylene furanoate |

| PET | Polyethylene terephthalate |

| PTT | Polytrimethylene terephthalate |

References

- Andersen, P.H.; Duvold, T.; Frølund, B.; Lüneborg, J.; Toft-Petersen, K.; Vanthournout, H.; Witte, C. New Plastics Economy: A Research, Innovation and Business Opportunity for Denmark; McKinsey & Company: Copenhagen, Denmark, 2019. [Google Scholar]

- Narancic, T.; Cerrone, F.; Beagan, N.; O’Connor, K.E. Recent Advances in Bioplastics: Application and Biodegradation. Polymers 2020, 12, 920. [Google Scholar] [CrossRef]

- Syberg, K.; Nielsen, M.B.; Clausen, L.P.W.; van Calser, G.; van Wezel, A.; Rochman, C.; Koelmans, A.A.; Cronin, R.; Pahl, S.; Hansen, S.F. Regulation of plastic from a circular economy perspective. Curr. Opin. Green Sustain. Chem. 2021, 29, 1–7. [Google Scholar] [CrossRef]

- Bassi, S.A.; Boldrin, A.; Faraca, G.; Astrup, T.F. Extended producer responsibility: How to unlock the environmental and economic potential of plastic packaging waste? Resour. Conserv. Recycl. 2020, 162, 1–12. [Google Scholar] [CrossRef]

- World Economic Forum; Ellen Macarthur Foundation and McKinsey & Company. The New Plastics Economy: Rethinking the Future of Plastics; Ellen Macarthur Foundation: London, UK, 2019. [Google Scholar]

- Hatti-Kaul, R.; Nilsson, L.J.; Zhang, B.; Rehnberg, N.; Lundmark, S. Designing Biobased Recyclable Polymers for Plastics. Trends Biotechnol. 2019, 38, 1–18. [Google Scholar] [CrossRef]

- Jenkins, S.; Quer, A.M.; Fonseca, C.; Varrone, C. Microbial degradation of plastics: New plastic degraders, mixed cultures and engineering strategies. In Soil Microenvironment for Bioremediation and Polymer Production; Chapter 12. Wiley Online Book; Jamil, N., Kumar, P., Batool, R., Eds.; John Wiley & Sons, Inc.: Hoboken, NJ, USA, 2019; pp. 215–238. ISBN 9781119592051. [Google Scholar]

- European Bioplastics. Position of European Bioplastics: Plastics Strategy—Contribution of Bioplastics to a Sustainable Circular Plastics Economy; European Bioplastics: Berlin, Germany, 2018. [Google Scholar]

- RameshKumar, S.; Shaiju, P.; O’Connor, K.E. Bio-based and biodegradable polymers—State-of-the-art, challenges and emerging trends. Curr. Opin. Green Sustain. Chem. 2020, 21, 75–81. [Google Scholar] [CrossRef]

- Ügdüler, S.; Van Geem, K.M.; Denolf, R.; Roosen, M.; Mys, N.; Ragaert, K.; De Meester, S. Towards closed-loop recycling of multilayer and coloured PET plastic waste by alkaline hydrolysis. Green Chem. 2020, 22, 5376–5394. [Google Scholar] [CrossRef]

- Tournier, V.; Topham, C.M.; Gilles, A.; David, B.; Folgoas, C.; Moya-Leclair, E.; Kamionka, E.; Desrousseaux, M.-L.; Texier, H.; Gavalda, S.; et al. An engineered PET depolymerase to break down and recycle plastic bottles. Nature 2020, 580, 216–219. [Google Scholar] [CrossRef]

- Dessbesell, L.; Souzanchi, S.; Rao, K.T.V.; Carrillo, A.A.; Bekker, D.; Hall, K.A.; Lawrence, K.M.; Tait, C.L.J.; Xu, C. Production of 2,5-furandicarboxylic acid (FDCA) from starch, glucose, or high-fructose corn syrup: Techno-economic analysis. Biofuels Bioprod. Biorefin. 2019, 13, 1234–1245. [Google Scholar] [CrossRef]

- Fei, X.; Wang, J.; Zhu, J.; Wang, X.; Liu, X. Biobased Poly(ethylene 2,5-furancoate): No Longer an Alternative, but an Irreplaceable Polyester in the Polymer Industry. ACS Sustain. Chem. Eng. 2020, 8, 8471–8485. [Google Scholar] [CrossRef]

- Loos, K.; Zhang, R.; Pereira, I.; Agostinho, B.; Hu, H.; Maniar, D.; Sbirrazzuoli, N.; Silvestre, A.J.D.; Guigo, N.; Sousa, A.F. A Perspective on PEF Synthesis, Properties, and End-Life. Front. Chem. 2020, 8, 1–18. [Google Scholar] [CrossRef] [PubMed]

- Eerhart, A.J.J.E.; Faaij, A.P.C.; Patel, M.K. Replacing fossil based PET with biobased PEF; process analysis, energy and GHG balance. Energy Environ. Sci. 2012, 5, 6407–6422. [Google Scholar] [CrossRef]

- Kurian, J.V. A New Polymer Platform for the Future—Sorona from Corn Derived 1,3-Propanediol. J. Polym. Environ. 2005, 13, 159–167. [Google Scholar] [CrossRef]

- Patel, M.; Angerer, G.; Crank, M.; Schleich, J.; Marscheider-Weidemann, F.; Wolf, O.; Hüsing, B. Techno-Economic Feasibility of Large-Scale Production of Bio-Based Polymers in Europe; Technical Report EUR 22103 EN; European Union Institute for Prospective Technological Studies Joint Research Commission: Seville, Spain, 2005; ISBN 92-79-01230-4. [Google Scholar]

- Kasmi, N.; Papageorgiou, G.Z.; Achilias, D.S.; Bikiaris, D.N. Solid-State Polymerization of Poly(Ethylene Furanoate) Biobased Polyester, II: An Efficient and Facile Method to Synthesize High Molecular Weight Polyester Appropriate for Food Packaging Applications. Polymers 2018, 10, 471. [Google Scholar] [CrossRef]

- Varrone, C.; Skiadas, I.V.; Gavala, H.N. Effect of hydraulic retention time on the modelling and optimization of joint 1,3 PDO and BuA production from 2G glycerol in a chemostat process. Chem. Eng. J. 2018, 347, 525–534. [Google Scholar] [CrossRef]

- Eberl, A.; Heumann, S.; Kotek, R.; Kaufmann, F.; Mitsche, S.; Cavaco-Paulo, A.; Gübitz, G.M. Enzymatic hydrolysis of PTT polymers and oligomers. J. Biotechnol. 2008, 135, 45–51. [Google Scholar] [CrossRef] [PubMed]

- Bertolini, F.A.; Soccio, M.; Weinberger, S.; Guidotti, G.; Gazzano, M.; Guebitz, G.M.; Lotti, N.; Pellis, A. Unveiling the enzymatic degradation process of bio-based thiophene polyesters. Front. Chem. 2021, in press. [Google Scholar]

- Kim, H.; Choi, J.; Park, J.; Won, W. Production of a sustainable and renewable biomass-derived monomer: Conceptual process design and techno-economic analysis. Green Chem. 2020, 22, 7070–7079. [Google Scholar] [CrossRef]

- Chatzifragkou, A.; Papanikolaou, S.; Dietz, D.; Doulgeraki, A.I.; Nychas, G.E.; Zeng, A. Production of 1,3-propanediol by Clostridium butyricum growing on biodiesel-derived crude glycerol through a non-sterilized fermentation process. Appl. Microbiol. Biotechnol. 2011, 91, 101–112. [Google Scholar] [CrossRef]

- Petrides, D.; Da Gama, R. Production of 1,3 Propanediol (PDO) via Fermentation—Process Modeling and Techno-Economic Assessment (TEA) Using SuperPro Designer; Intelligen, Inc.: Scotch Plains, NJ, USA, 2020. [Google Scholar] [CrossRef]

- Seider, W.D.; Seader, J.D.; Lewin, D.R.; Widago, S. Product and Process Design Principles: Synthesis, Analysis, and Evaluation, 3rd ed.; John Wiley & Sons, Inc.: Hoboken, NJ, USA, 2009; pp. 534–627. [Google Scholar]

- Davis, R.; Tao, L.; Tan, E.C.D.; Biddy, M.J.; Beckham, G.T.; Scarlata, C.; Jacobsen, J.; Cafferty, K.; Ross, J.; Lukas, J.; et al. Process Design and Economics for the Conversion of Lignocellulosic Biomass to Hydrocarbons: Dilute-Acid and Enzymatic Deconstruction of Biomass to Sugars and Biological Conversion of Sugars to Hydrocarbons; National Renewable Energy Laboratory (NREL): Golden, CO, USA, 2013. [Google Scholar]

- Intelligen, Inc. SuperPro Designer User Guide. 2020. Available online: https://www.intelligen.com/wp-content/uploads/2020/05/SuperPro_ManualForPrinting_v11.pdf (accessed on 1 August 2021).

- DalinYebo. FDCA to PEF: A Production Cost Analysis. 2019. Available online: https://dalinyebo.com/fdca-to-pef-polyethylene-furanoate_a-production-cost-analysis/ (accessed on 21 August 2021).

- Statista. Price of Polyethylene Terephthalate (PET) Worldwide from 2017 to 2021. 2021. Available online: https://www.statista.com/statistics/1171088/price-polyethylene-terephthalate-forecast-globally/ (accessed on 21 August 2021).

- Avantium. Investor Presentation H2. 2021. Available online: https://www.avantium.com/wp-content/uploads/2021/08/Avantium-Investor-Presentation_H2_compressed.pdf (accessed on 2 November 2021).

- Hann, S.; Scholes, R.; Lee, T.; Ettinger, S.; Jørgensen, H. Bio-Based and Biodegradable Plastics in Denmark: Market, Applications, Waste Management and Implications in the Open Environment; Environmental Project No. 2125; The Danish Environmental Protection Agency: Odense, Denmark, 2020; ISBN 978-87-7038-165-9. [Google Scholar]

- Van der Klis, F.; van Haveren, J.; van Es, D.S.; Bitter, J.H. Synthesis of Furandicarboxylic Acid Esters From Nonfood Feedstocks Without Concomitant Levulinic Acid Formation. ChemSusChem 2017, 10, 1460–1468. [Google Scholar] [CrossRef]

- Wang, W.; Mittal, A.; Pilath, H.; Chen, X.; Tucker, M.P.; Johnson, D.K. Simultaneous upgrading of biomass-derived sugars to HMF/furfural via enzymatically isomerized ketose intermediates. Biotechnol. Biofuels 2019, 12, 1–9. [Google Scholar] [CrossRef]

- Varrone, C.; Liberatore, R.; Crescenzi, C.; Izzo, G.; Wang, A.J. The valorization of glycerol: Experimentation and economic assessment of an innovative process for the bioconversion of crude glycerol into ethanol and hydrogen. Appl. Energy 2013, 105, 349–357. [Google Scholar] [CrossRef]

- Fernando-Foncillas, C.; Varrone, C. Potential of the sewage sludge valorization in Scandinavia by co-digestion with other organic wastes: A Techno-economic assessment. J. Clean. Prod. 2021, 324, 129–139. [Google Scholar] [CrossRef]

- European Commission. A European Strategy for Plastics in a Circular Economy; European Commission: Brussels, Belgium, 2018. [Google Scholar]

- Eurostat. Plastic Packaging Recycling Rate, Electronic Dataset. 2017. Available online: https://ec.europa.eu/eurostat/databrowser/view/ten00063/default/table?lang=en (accessed on 19 October 2021).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Parameter | Value | Source |

|---|---|---|

| PET flow rate | 67,853 tpa | Calculated |

| Enzyme loading | 0.2 wt.% | [11] |

| PET conversion | 90.0% | [11] |

| PTA yield | 86.3% | [11] |

| Parameter | Value | Source |

|---|---|---|

| Cellulose flow rate | 131,900 tpa | Calculated |

| Cellulose loading | 3.0 wt. % | [22] |

| HMF yield | 42 mol % | [22] |

| FDCA yield | 93.6 mol % | [22] |

| FDCA recovery | 95% | [22] |

| Parameter | Value | Source |

|---|---|---|

| FDCA conversion | 83% | [18] |

| PEF purity | 99.4% | Calculated |

| PEF flow rate | 59,150 tpa | Calculated |

| Parameter | Value | Source |

|---|---|---|

| Crude glycerol flow rate | 64,550 tpa | Calculated |

| Crude glycerol purity | 81% | [23] |

| Crude glycerol in feed | 75% | [23] |

| Crude glycerol flow rate | 64,550 tpa | [23] |

| PDO purity | 99.3% | Calculated |

| Scenario 1 | Scenario 2 | |

|---|---|---|

| SP (USD/kg) | 2.70 | 2.70 |

| PBP (years) | 23.3 | 5.15 |

| MSP (USD/kg) | 3.13 | 2.34 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Roux, M.; Varrone, C. Assessing the Economic Viability of the Plastic Biorefinery Concept and Its Contribution to a More Circular Plastic Sector. Polymers 2021, 13, 3883. https://doi.org/10.3390/polym13223883

Roux M, Varrone C. Assessing the Economic Viability of the Plastic Biorefinery Concept and Its Contribution to a More Circular Plastic Sector. Polymers. 2021; 13(22):3883. https://doi.org/10.3390/polym13223883

Chicago/Turabian StyleRoux, Megan, and Cristiano Varrone. 2021. "Assessing the Economic Viability of the Plastic Biorefinery Concept and Its Contribution to a More Circular Plastic Sector" Polymers 13, no. 22: 3883. https://doi.org/10.3390/polym13223883

APA StyleRoux, M., & Varrone, C. (2021). Assessing the Economic Viability of the Plastic Biorefinery Concept and Its Contribution to a More Circular Plastic Sector. Polymers, 13(22), 3883. https://doi.org/10.3390/polym13223883