1. Introduction

Reputation is a complex and multidimensional concept [

1] that, following the study of Reference [

2], may be organized in downside and upside reputational risk. On the other hand, there is a growing political and academic interest in the use of information as a quasi-regulatory mechanism and its relation to organizational reputation [

3,

4,

5], with the recent case of Volkswagen being a prominent one [

6]. In this context, companies must be prepared to increase their reporting of non-financial information and to manage the impact of this information provision on their reputation. Environmental management can be defined as a set of corporate decisions and actions that aim to develop, deploy, execute, and control the corporate environmental policy. Environmental management is presented in this paper as a specific tool for reputational risk hedging, assuming that environmental management influences corporate reputation and customers’ satisfaction [

7,

8]. It is also assumed that for this idea to be true, environmental management has to improve corporate environmental performance and that this has to be effectively communicated to society, either directly (through company reporting and public relations) or indirectly (through governments and media coverage).

We developed a formal modelling to address the hedging capabilities of environmental management and reporting over reputational risk, using the flexibility granted by the options theory to consider different levels of information transparency. When considering a scenario of voluntary reporting, we show that environmentally concerned companies can reduce the cost of environmental management as a reputational risk strategy, as well as reduce the potential loss of reputational value from reputational threats and increase the potential profit from reputational opportunities. In the context of mandatory reporting, we highlight the role of assurance companies as bearers of the risk of bad reputations for non-concerned companies.

The rest of the manuscript is organized as follows.

Section 2 discusses the relation between environmental management and corporate reputation, pointing out how environmental reporting mediates in this relation.

Section 3 presents the method and formalizes the hedging role of good and bad environmental practices over reputational risk using results from the options theory.

Section 4 elaborates on the hedging capabilities of environmental management over reputational risk along different levels of information transparency. Finally,

Section 5 concludes and outlines recommendations for future research.

2. Environmental Management as a Driver of Corporate Reputation: The Importance of Environmental Reporting

Environmental performance is related to corporate reputation and customers’ satisfaction [

7,

8], and normally it can be expected that bad environmental performers will be penalised with a bad reputation and that good environmental performers will be rewarded with a good reputation [

9]. In this context, and assuming that environmental management leads to improved environmental performance [

10], environmental management can be thought of as a specific tool for reputational risk management.

It is possible that environmental management in itself can contribute to the improvement of corporate reputation if some signalling option is in use, for example, certification [

11]. Yet, obviously, as long as reputation depends on the information available and public perception, the effect of environmental management on reputation will be mediated by the reporting efforts of the company and other institutions (such as governments or mass media), as well as by how these efforts are perceived by the public. There is a risk that environmental reporting can be understood as green-washing [

12]. In fact, some studies have examined the level and nature of the environmental information voluntarily disclosed by firms and found that they may not be indicative of their underlying environmental performance [

13], pointing to the need to establish some mandatory framework to promote environmental reporting and even its assurance. The use of environmental disclosure or, more generally, Corporate Social Responsibility (CSR) disclosure to acquire greater legitimacy has already been analysed and considered as a long-term investment in reputation [

14,

15]; some authors even point out that corporate reputation can be more influenced by what companies report than by what they actually do [

9].

If corporate environmental management and reporting have an impact on corporate reputation, the regulatory authorities could promote the use of information about the environmental performance of companies as an environmental policy instrument. In this sense, Arora and Gangopadhyay [

16] conclude that the public image of a company is a key driving force of voluntary over-compliance with environmental regulations. Additionally, Caplan [

3] considers that under certain circumstances polluting firms self-regulate by internalizing the forward effect of their environmental reputation, and Banerjee and Shogren [

17] advance that firms concerned about their reputation would exert at least the optimal level of effort in environmental protection. Johnstone and Labonne [

11] consider that the environmental management area is characterized by strong information asymmetries, as its quality is not readily observable. The requirement to disclose information on the environmental performance of companies is a vehicle that environmental regulation could use in order to reduce these information asymmetries [

5], encouraging stakeholders to exercise disciplinary pressure on the behaviour of firms. Mitchell [

18] acknowledges also that disclosure-based policies can influence corporate behaviour, making targeted actors aware of their own behaviours and moving them to alter these behaviours in positive ways prior to (and independent of) the public disclosure process itself.

The relation between environmental performance and environmental reporting has also been studied, although offering mixed results depending on the theory applied to explain managerial behaviour [

13]. In this paper, we adopt the perspective of the voluntary disclosure theory, which predicts that firms with superior environmental performance will have incentives to disclose in order to differentiate themselves. In addition, even in a mandatory reporting context, firms with better environmental records (measured by toxic emissions) have higher levels of environmental disclosures [

19]. However, nowadays a credibility gap is acknowledged regarding sustainability reports, and assurance can play a valuable role in helping to ensure that the environmental information provided is reliable and credible. The concept of assurance includes not only reports verification, but also advice on environmental performance, corporate governance, stakeholder engagement, and other areas central to corporate responsibility, with the aim of reinforcing the credibility and quality of corporate sustainability strategies. The assurance market is a competitive and mainly unregulated market with various types of assurance suppliers from inside and outside the accounting profession [

20], and it has two principal reference standards which try to ensure the quality of the assurance work: the International Standard on Assurance Engagement (lSAE) 3000, and the Account-Ability 1000 Assurance Standard (AA 1000AS). However, some individual countries’ accounting authorities have also issued specific standards for the auditing of sustainability reports. We refer to the work of Manetti and Becatti [

21] to examine some critical points of present assurance services on sustainability reports, as well as a number of suggested improvements for future assurance standards. Ackers, Eccles, and Parker [

22] state also that voluntary CSR assurance has resulted in the inconsistent application of CSR assurance practices, and argue that this deficiency may be overcome through the imposition of a mandatory CSR assurance regime. Furthermore, assurance is acquiring importance in the context of the expanding use of integrated reporting, which needs specific assurance standards for reports that combine financial and non-financial information.

3. An Options Theory Approach to Reputational Risk Hedging Through Environmental Management

3.1. Methods

Since the proposal of the Black-Scholes equation to calculate the premium of a European option [

23], the method originally conceived for valuing financial options has been widely used for the analysis of different managerial decisions, including corporate valuation [

24,

25,

26], investment projects [

27,

28,

29,

30], research and development [

31,

32], and budgeting [

33].

Indeed, the options theory framework has already been applied in the fields of corporate social responsibility [

34] and risk management [

35], with some recent results related to reputational risk [

36,

37]. Thus, and following a similar approach, this article elaborates on a novel theoretical analysis of environmental management as a hedging instrument over reputational risk, considering that the options theory provides the flexibility needed in order to capture its varying hedging capability through different levels of information transparency. The valuation of the corporate reputation offered by the market will be represented by

. Consequently, considering that corporate reputation can be understood as an underlying asset, the value of which needs to be protected, and given that environmental management can be thought of as a hedging instrument over that underlying asset, we will be denoting the result of this reputational risk management strategy with

V. The company that wants to get the protection has to pay a premium in terms of effort in environmental management. Moreover, this effort gives the company the right to reach a certain level of reputational valuation. From that strike valuation level onwards, the option results are activated and the company gets a reputational payoff.

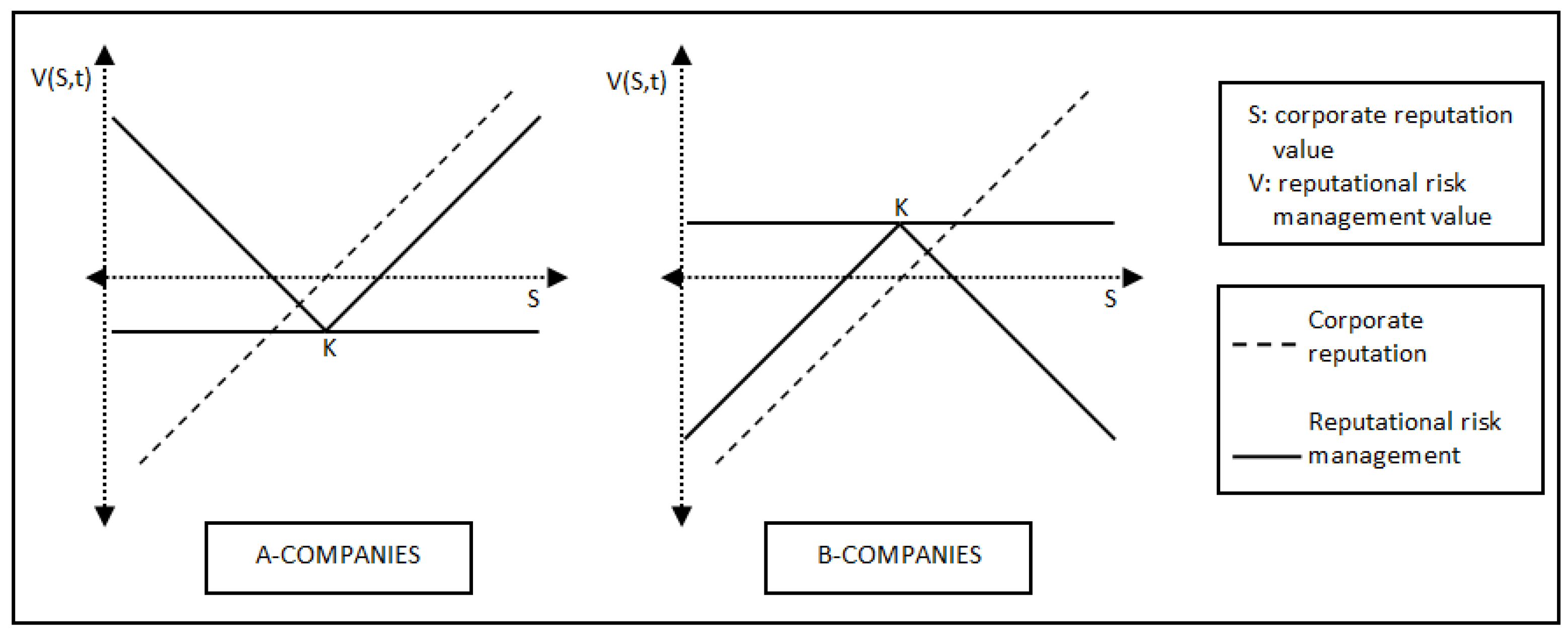

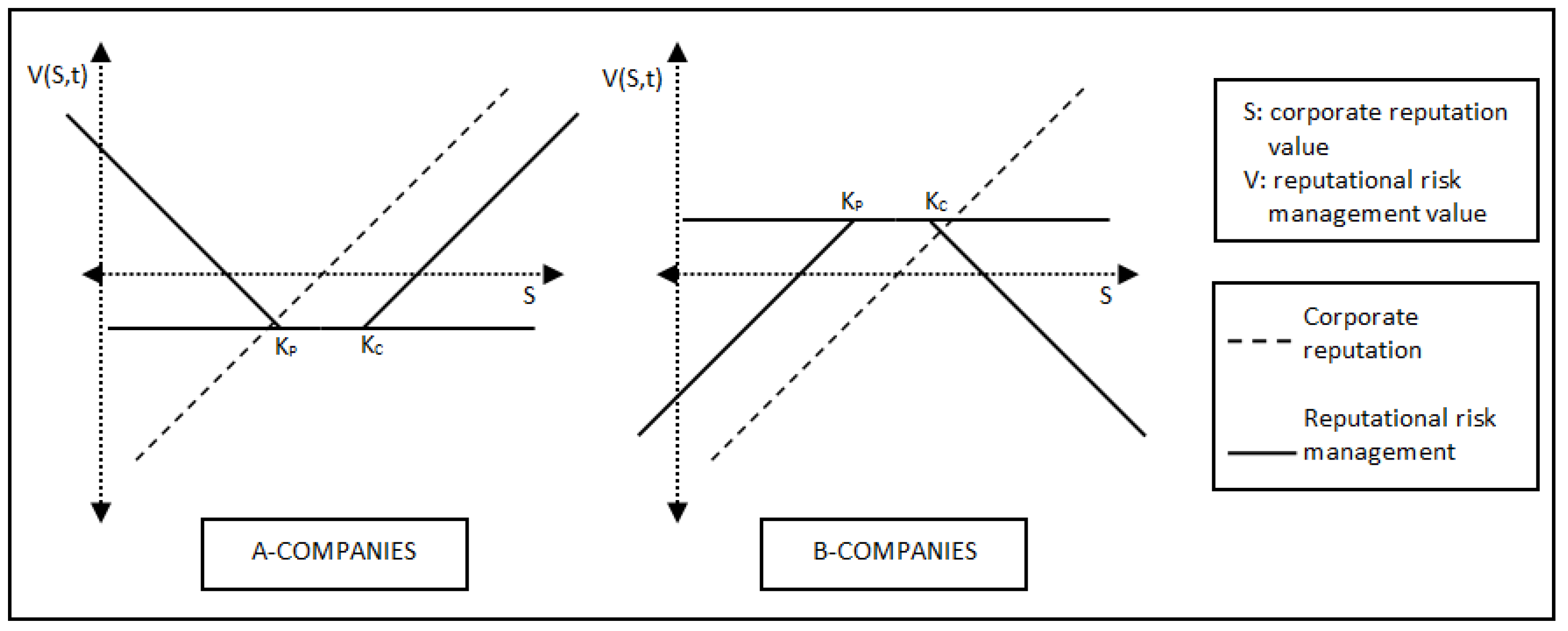

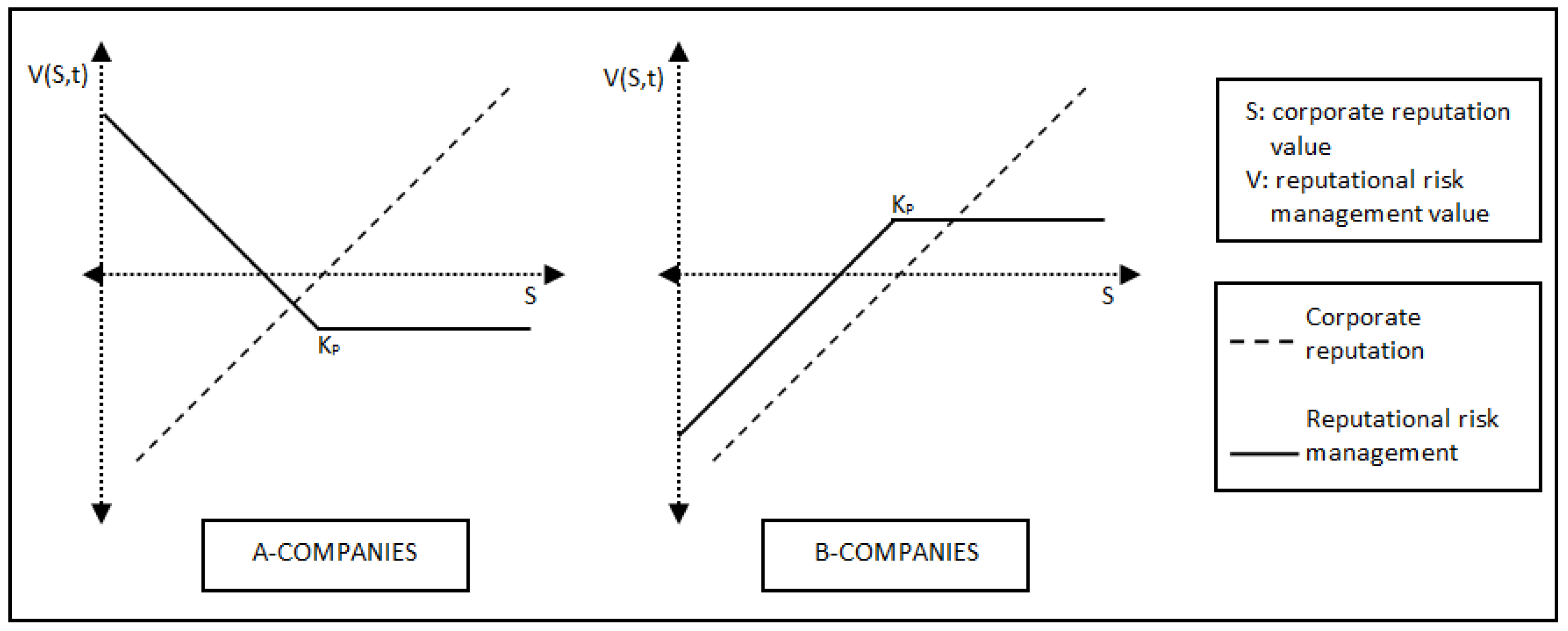

For clarity purposes, in order to understand how the protection offered by environmental management works and to determine the reputational result of this hedging strategy, the companies will be classified into two different groups: companies whose reputational risk is actively managed through environmental management (these ones will be called A-companies) and companies whose reputational risk is not actively managed through environmental management (these ones will be referred to as B-companies). The A-companies and the B-companies are the agents involved in the formalization of the environmental management hedging capabilities, and this formalization has two dimensions depending on whether the market rewards good environmental management practices or penalizes bad environmental management practices: In the first case, companies develop environmental management to take advantage of reputational opportunities in order to build a good reputation; and in the second case, companies invest in environmental management in order to protect against reputational threats and avoid a bad reputation.

3.2. Environmental Management as an Option to Build a Good Reputation

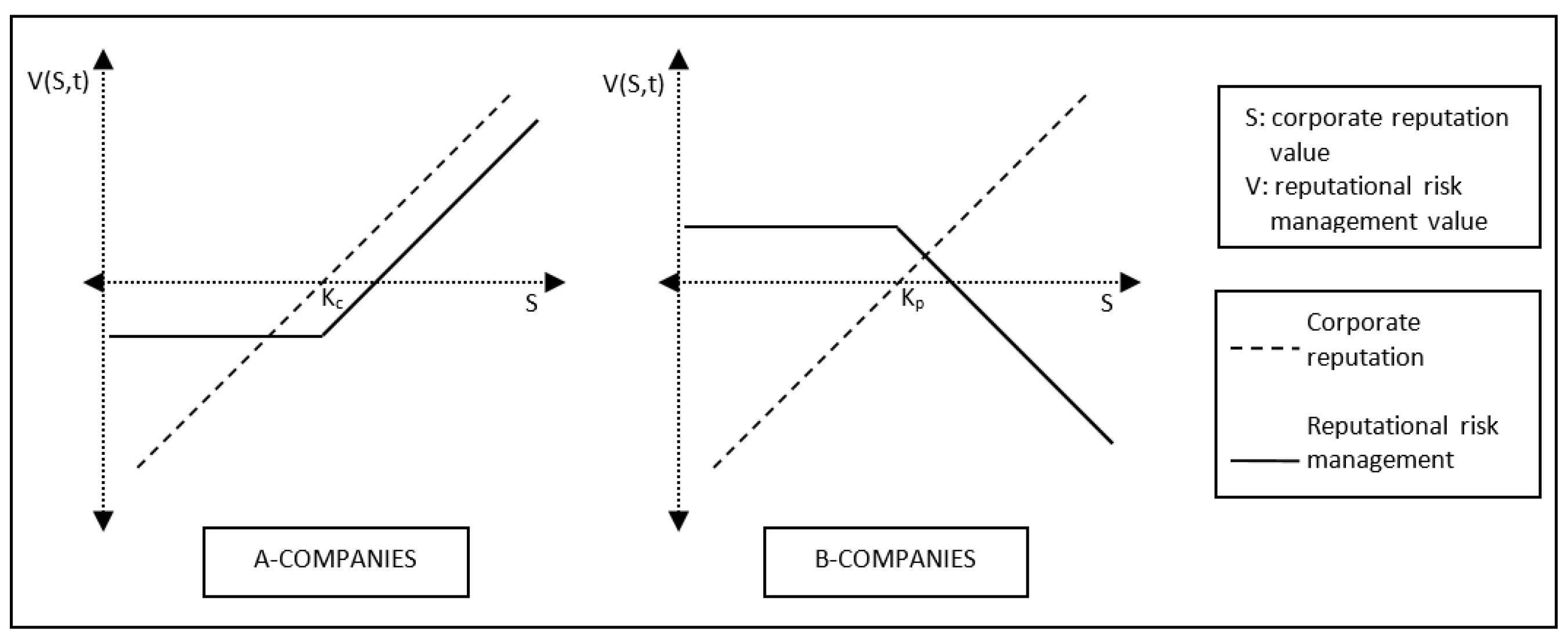

Regarding the first dimension, the A-companies invest in environmental management in order to build a good reputation. On the other side, the B-companies, which do not carry out environmental management, are not prepared to react in the appropriate manner when reputational opportunities arise, so the potential reputational advantages of these opportunities will be lost. From this point of view, it can be stated that the A-companies are buying the chance to get positive reputational consequences and build a good reputation, that is, they are taking a long position in a call contract over the underlying asset of corporate reputation. On the other side, as B-companies are wasting reputational opportunities in favour of A-companies, it can be affirmed that they are selling the chance of building a good reputation for A-companies, that is, they are taking the complementary short position in that call contract over the corporate reputation asset. The long and short positions of the call contract are presented in

Figure 1 [

38].

The option gets activated when the valuation of the corporate reputation offered by the market is above the valuation level that the A-companies have the right to get according to the investment in environmental management quantified through the premium. This valuation level corresponds to the strike price of the option and is represented by

. If the market is especially sensitive to good environmental management practices and offers a high valuation of good environmental management, the A-companies have complete interest in disclosing their environmental commitment in order to get the reputational reward in terms of this higher valuation. Otherwise, if the market offers a low valuation of these good environmental management practices, the A-companies get a null reputational result from their investment in environmental management. The premium of the call contract that collects the investment in environmental management carried out by the A-companies depends on the valuation of corporate reputation offered by the market, as well as the volatility over that valuation. Thus, the environmental management effort demanded of the company from the market is larger when the market offers a bigger reward to good environmental management practices, or when the volatility observed in the market around that valuation increases. On the other hand, if the market does not offer a high valuation of good environmental management practices or the volatility around this valuation is small, the required amount of investment in environmental management decreases. While the valuation of good environmental management practices gets higher, the A-companies get a bigger reputational reward that compensates the initial effort quantified through the premium, and the A-companies are driven to a region of potentially unlimited reputational profits. Otherwise, if the market does not reward good environmental management practices, the A-companies lose the investment represented by the premium, this quantity being the limit of their potential loss. The reputational result for B-companies is the opposite of the reputational result for A-companies. Thus, when the market offers a high valuation of good environmental management practices, the B-companies do not get the reputational reward and suffer a reputational loss in terms of the opportunity cost related to the wasted reputational opportunities. On the other hand, when the market does not reward good environmental management practices, the B-companies get the benefit corresponding to the premium invested by the A-companies. Given that this is an investment that the B-companies do not accomplish, it can be considered as a minor cost for them, so compared with the A-companies, the B-companies have a benefit in terms of the free funds corresponding to the non-undertaken investment in environmental management, and this is the only potential benefit that they could accomplish [

38].

Consequently, the call contract can be summarized by stating that it is a hedging instrument over the underlying asset of corporate reputation. When the reputational opportunities arise, the A-companies are in position of taking advantage of them, so their reputation improves. On the other hand, the B-companies have no chance to achieve the positive reputational consequences of those opportunities, so their reputation turns out to be poor compared with the reputation held by the A-companies. Thus, there is a transfer of good reputation in favour of the A-companies and to the detriment of the B-companies. It can be stated that the A-companies have the right to buy or get good reputation through the activation of the option, and when this occurs the B-companies have the obligation to sell and relinquish a good reputation.

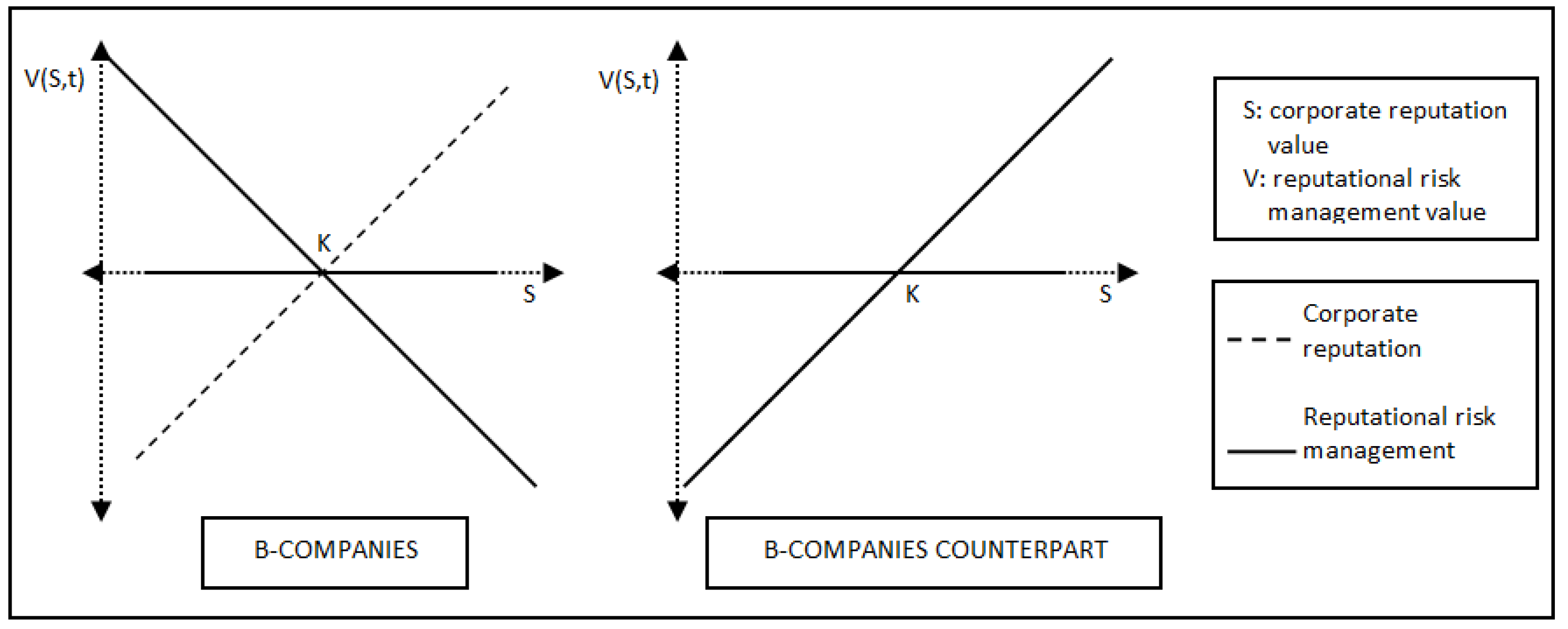

3.3. Environmental Management as an Option to Avoid a Bad Reputation

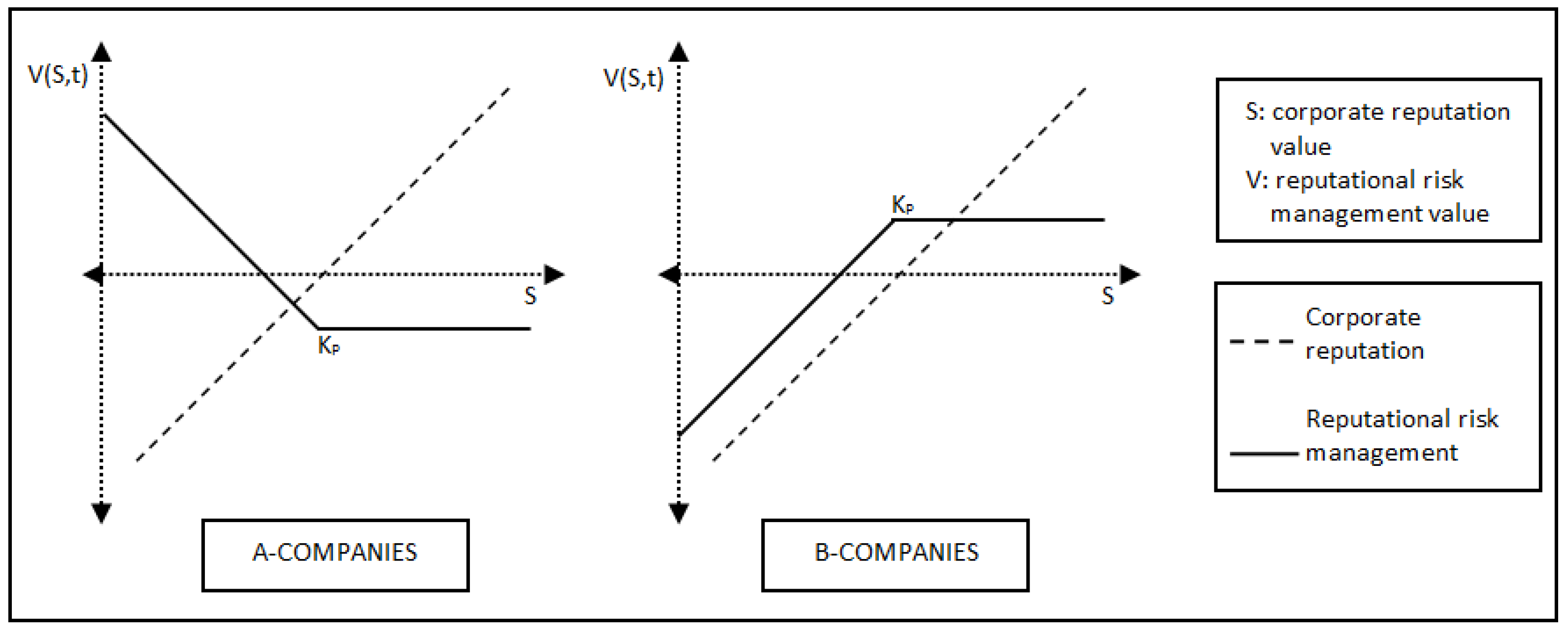

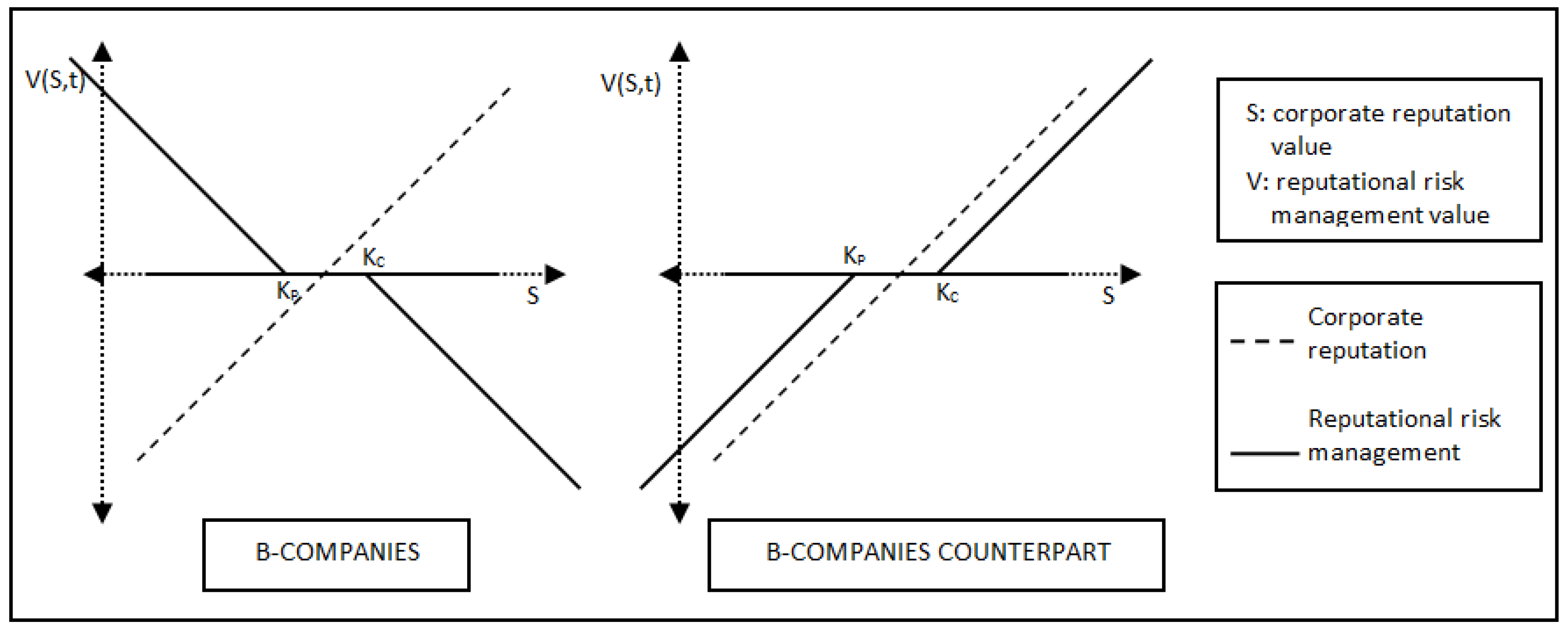

Regarding the second dimension of the environmental management strategy, which comprises the protection against damages derived from reputational threats, the A-companies invest in environmental management in order to get far away from a bad reputation. Meanwhile, the B-companies do not accomplish this investment, so when reputational threats show up (for instance, in the regulatory demand of disclosure of information on environmental performance) they are not ready to respond in a suitable way (they cannot communicate a good environmental performance), and they cannot avoid the reputational damage. From this point of view, it can be stated that the A-companies are buying the chance to sell the negative consequences of reputational threats and avoid a bad reputation, that is, they are taking a long position in a put contract over the underlying asset of corporate reputation. On the other side, if the B-companies are suffering damage from reputational threats, it can be said that they are buying the bad reputation that the A-companies are selling, that is, they are taking the complementary short position in that put contract over the corporate reputation asset. The long and short positions are presented in

Figure 2 [

38].

The option gets activated when the valuation of bad environmental management practices derived from the market is below the strike valuation level that the A-companies have the right to reach, according to their investment in environmental management. If the market is especially sensitive to bad environmental management practices and reacts by penalizing them by offering a low reputational valuation, the A-companies will disclose their environmental commitment in order to avoid this reputational penalty and get the correct reputational valuation according to their reputational effort. Otherwise, if the market does not penalize bad environmental management practices and offers a high valuation of bad reputations, the A-companies get a null reputational result from their investment in environmental management. The premium of the put contract, which represents the investment carried out by A-companies in environmental management in order to protect against reputational threats and avoid a bad reputation, depends on the valuation of bad environmental management practices offered by the market, and on the volatility over that valuation. The reputational effort demanded by the company from the market in order to avoid the reputational damage related to bad environmental management practices is larger when the market offers a low valuation of them, that is, when the reputational penalty imposed by the market is higher, or when the volatility observed in the market valuation of bad environmental management practices increases. On the other hand, if the market does not offer a poor valuation of bad environmental management practices, or the volatility around this valuation is small, the amount of investment in environmental management required to avoid reputational damages decreases. While the valuation of bad environmental management practices gets lower, the A-companies avoid more severe reputational damage, and this profit in terms of the non-suffered reputational loss compensates for the initial effort quantified through the premium, driving the A-companies to a region of potentially unlimited reputational profits (by avoiding potentially unlimited reputational losses). Otherwise, if the market does not penalize bad environmental management practices, the A-companies lose the investment in avoiding the reputational damage represented by the premium, this quantity being the limit of their potential loss. The reputational result for the B-companies is the opposite of the reputational result for A-companies. Thus, when the market offers a low valuation of bad environmental management practices, the B-companies suffer the reputational damage and get the subsequent reputational loss. On the other hand, when the market does not penalize bad environmental management practices, the B-companies get the benefit corresponding to the premium invested by the A-companies in avoiding reputational damage. Once again, it can be considered as a minor cost for the B-companies, because compared with the A-companies they have a benefit in terms of the non-accomplished investment in environmental management, and this is the only potential benefit that they could accomplish [

38].

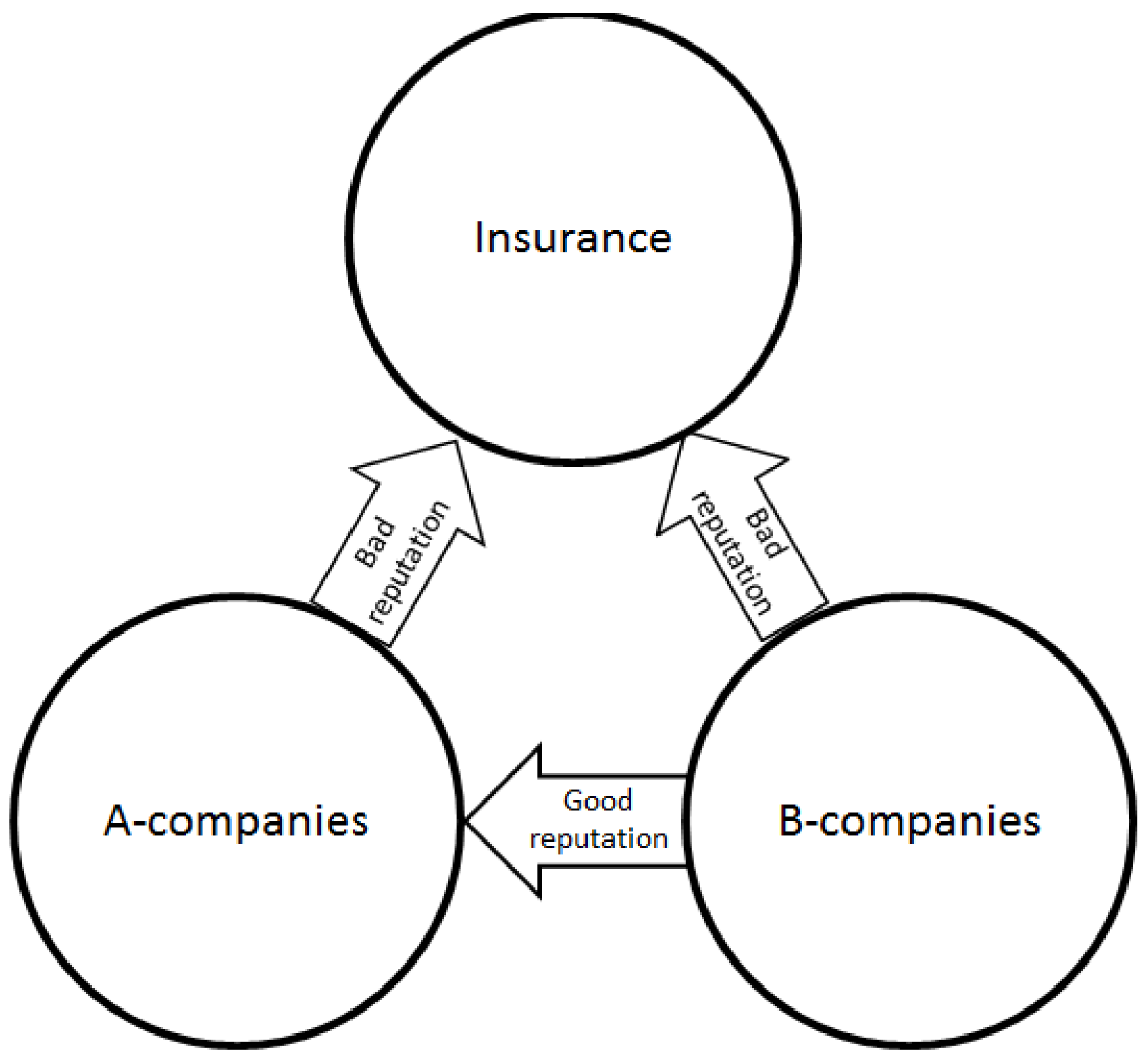

Consequently, the put contract can be summarized by stating that it is another hedging instrument over the underlying asset of corporate reputation. When the reputational threats arise, the A-companies are in position of getting protection against them, so their reputational valuations do not suffer. On the other hand, the B-companies have no chance to avoid the negative reputational consequences of those threats, so their reputation turns out to be poor when compared with the reputation held by the A-companies. Thus, there is a transfer of bad reputation from the A-companies to the B-companies. It can be stated that the A-companies have the right to sell or get rid of a bad reputation through the activation of the option, and when this occurs the B-companies have the obligation to buy or get a bad reputation.

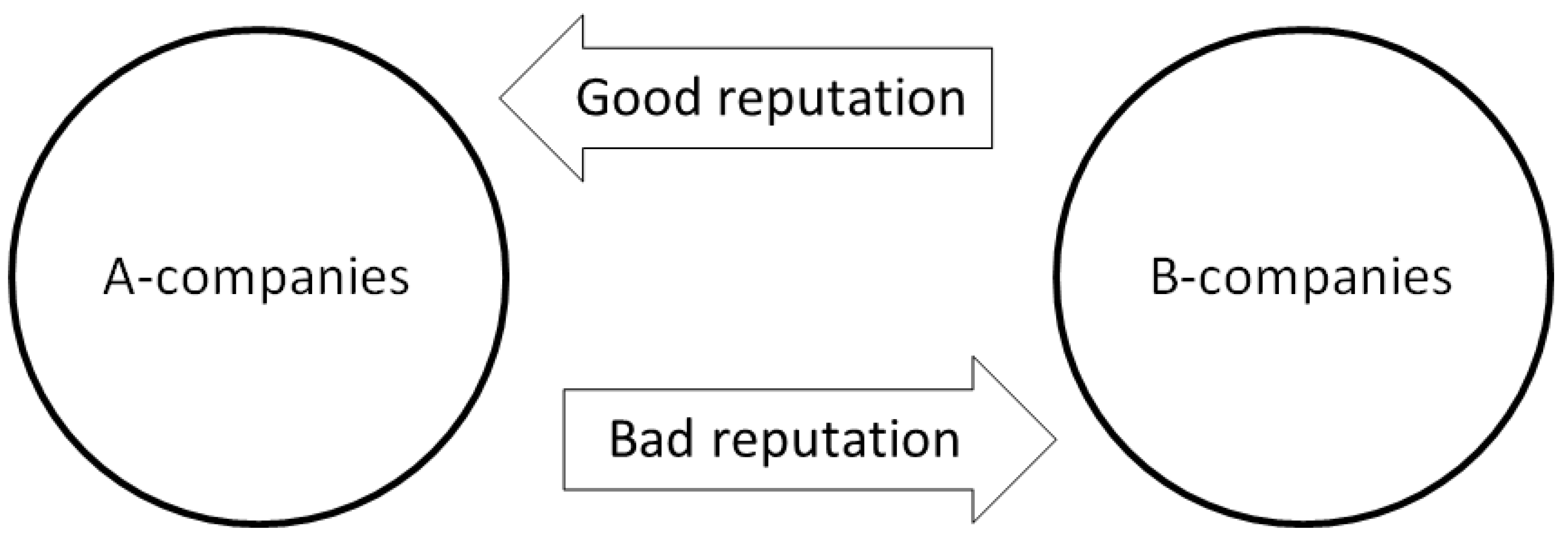

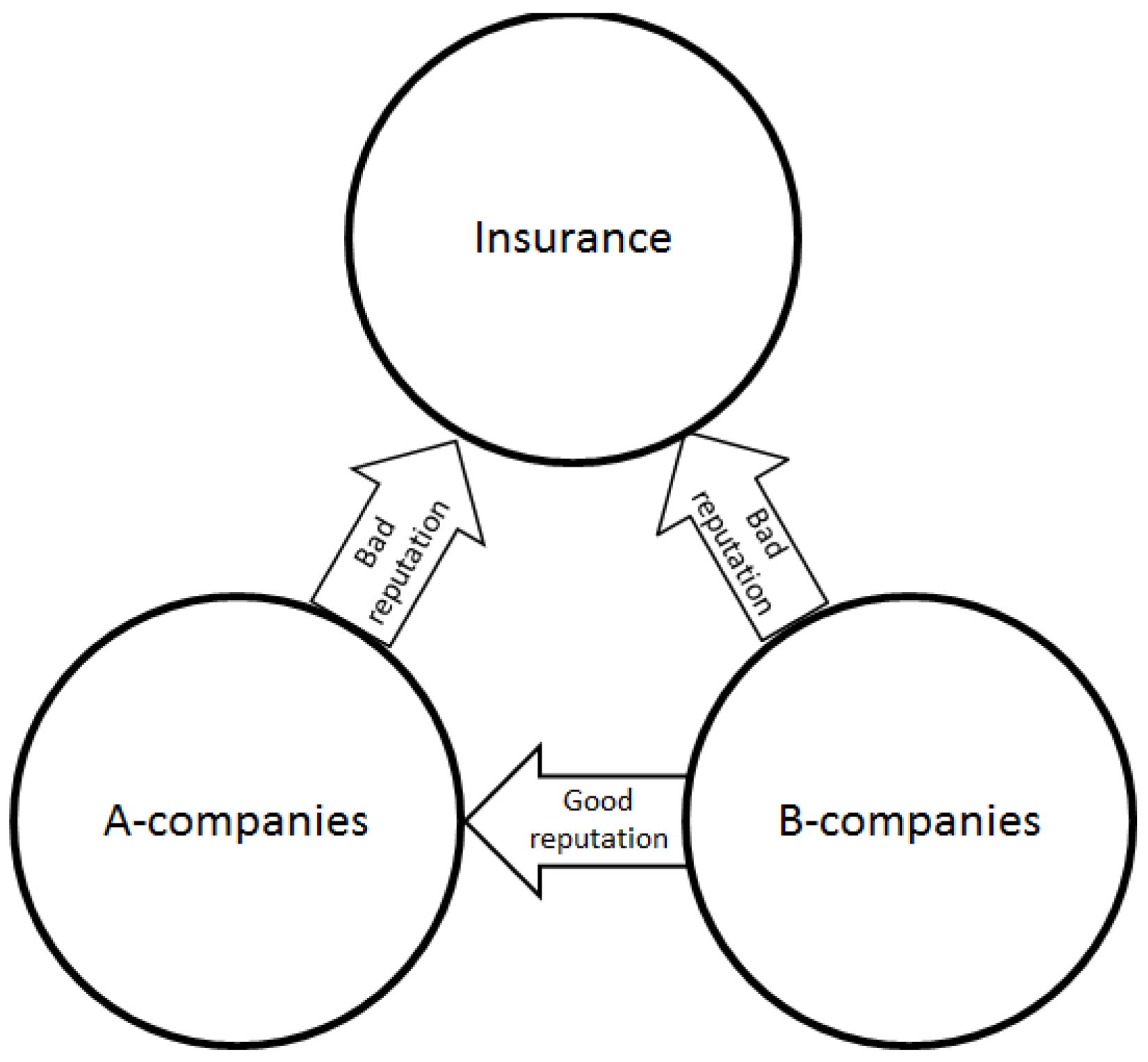

To sum up, the two dimensions of environmental management described above (to foster a good reputation or to avoid a bad reputation), it can be said that there is a bidirectional reputational flow between the companies in the market, where the A-companies have the right to get the good reputational consequences derived from reputational opportunities that the B-companies lose through a call contract, and simultaneously the A-companies have the right to avoid the bad reputational consequences derived from reputational threats that the B-companies are suffering through a put contract (

Figure 3).

5. Conclusions

The main objective of this essay has been proposing a formal modelling for the hedging capabilities of environmental management and reporting over reputational risk. The review of previous literature on the relationship between environmental management and reputation has revealed that some important issues mediate in this relationship: environmental reporting, its voluntary or mandatory nature, and the need of assurance. Consequently, the link between environmental management and reputation can be analysed under different levels of transparency.

The options theory has been proposed as a convenient methodology due to its flexibility that allows the consideration of different levels of information asymmetry and several scenarios, showing that environmental management acts like a hedging instrument over the company’s reputation, contributing to the achievement of its objectives. When considering a scenario of voluntary reporting, we show that the environmentally concerned companies can reduce the cost of environmental management as a reputational risk strategy, as well as reduce the potential loss of reputational value from reputational threats and increase the potential profit from reputational opportunities. In the context of mandatory reporting, we have highlighted the role of assurance companies as bearers of the risk of bad reputations for non-concerned companies, to the extent that assurance companies get involved both in the design and implementation of their client’s sustainability strategies as well as in the verification of their sustainability reports.

Table 1 summarizes the main findings for companies concerned with environmental management and reporting along with the different scenarios covered in the study.

In addition,

Table 2 summarizes the main findings for non-concerned companies along the different scenarios:

Given that reputational risk is becoming increasingly important for companies, the corporate management field could benefit from this paper’s contributions, taking them as a starting point to reach a full integration of environmental management into corporate management as a reputational risk hedging strategy. Moreover, the proposed methodological framework would help to reduce the overall exposure of a company to reputational risk and, therefore, it would positively contribute to the shareholder value creation. This is also a contribution to the academic field, as there is an absence of studies that analyse the issue of “whether or not it pays to be green” that consider the intermediate variables that influence the performance links, such as reputation [

8]. Consequently, there is an open avenue for further research to empirically examine the link between companies’ reputations and their corporate value, as well as to develop an empirical investigation of this paper’s theoretical propositions. From an academic perspective, this paper also advances the literature by integrating the consideration of environmental management, environmental reporting, and reputational risk under the framework provided by the options theory, something that to our knowledge has not been done yet. Finally, we have reviewed the concerns regarding the reliability of voluntary environmental disclosures, which signal a need for both enhanced mandatory reporting requirements and improved enforcement [

13], and also for assurance of CSR information. Consequently, policy makers could also find our framework useful to analyse the suitability of incentives for environmental disclosures, or the need for a mandatory disclosure, to promote corporate environmental behaviour, which might imply a less active and costly role for the regulating authorities [

3]. More concretely, national governments across the European Union that are having to transpose to their regulatory framework in accordance with the recent Directive on non-financial information disclosure, need to carefully analyse the implications of voluntary and mandatory reporting as well as the role of assurance, and could base such analysis on this paper’s contributions. As a final recommendation, corporate and public policies, as well as academic fields could take into account this paper’s contributions as a starting point to justify the need for demanding greater transparency and assurance on the environmental performance of companies, and the convenience of developing further research on the relationship between environmental management and reputational risk.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}