Sustainable Leadership Practices Driving Financial Performance: Empirical Evidence from Thai SMEs

Abstract

:1. Introduction

2. Sustainable Leadership: A Theoretical Framework

3. Relationship between Sustainable Leadership and Corporate Financial Performance

4. Methodology

5. Measures

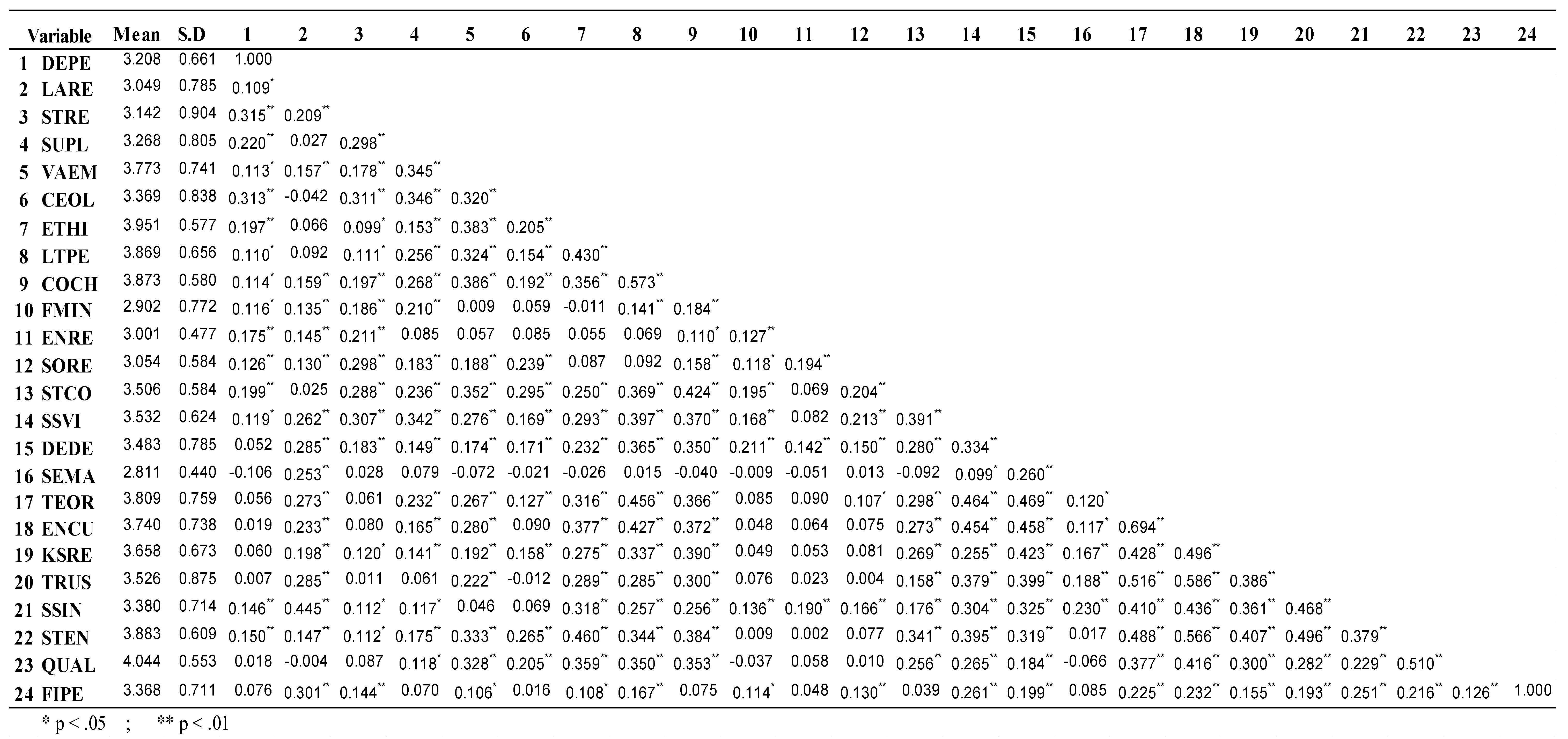

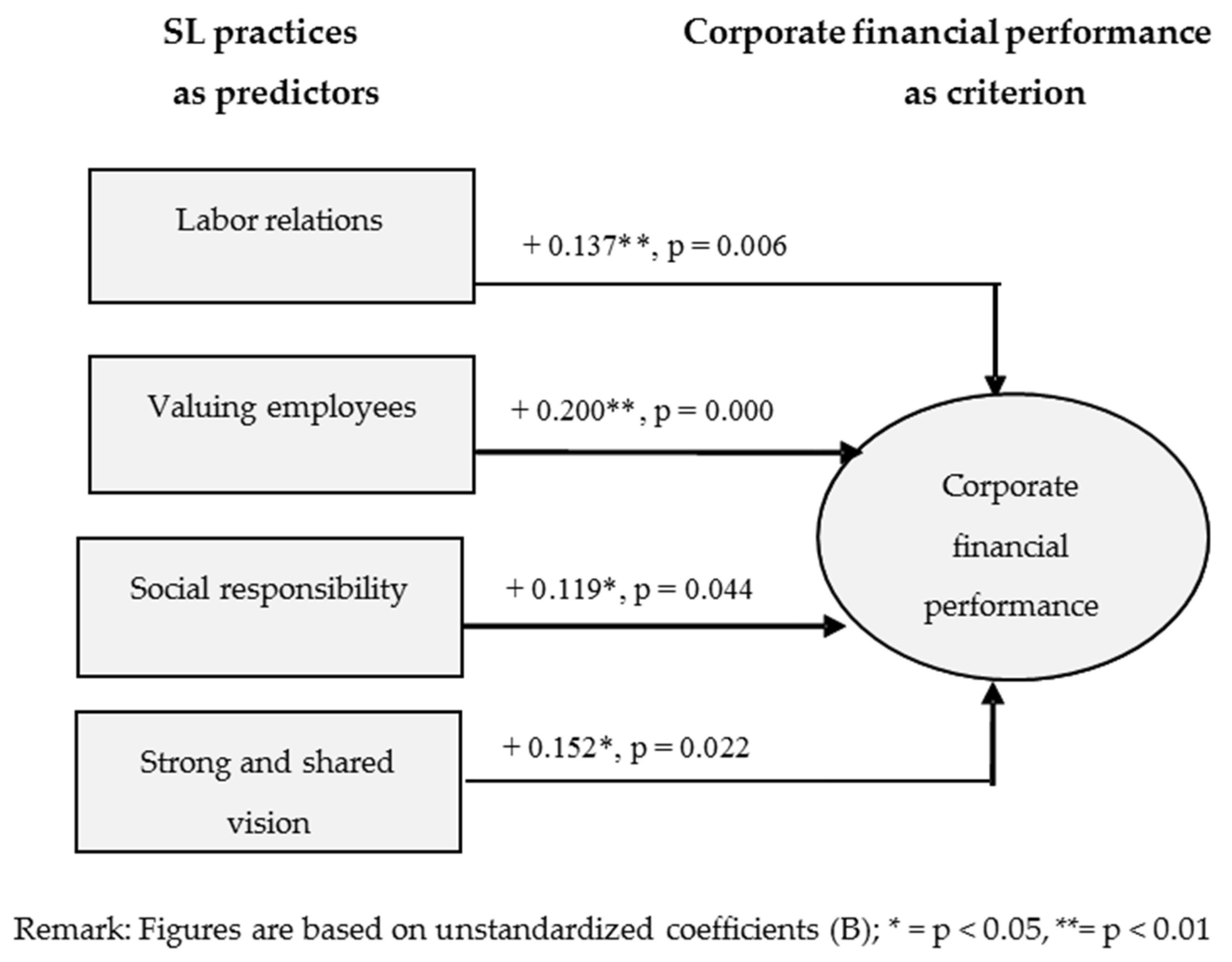

6. Results

7. Discussion

8. Implications

9. Limitations

10. Future Research

Acknowledgments

Author Contributions

Conflicts of Interest

References

- Smith, P.A.C.; Sharicz, C. The shift needed for sustainability. Learn. Organ. 2011, 18, 73–86. [Google Scholar] [CrossRef]

- Faber, N.; Jorna, R.J.; van Engelen, J. The sustainability of ‘sustainability’. J. Environ. Assess. Pol. Manag. 2005, 7, 1–33. [Google Scholar] [CrossRef]

- Dobson, A. Environmental sustainabilities: An analysis and a typology. Environ. Pol. 1996, 5, 401–428. [Google Scholar] [CrossRef]

- Avery, G.C.; Bergsteiner, H. Honeybees and Locusts: The Business Case for Sustainable Leadership; Allen and Unwin: Sydney, Australia, 2010. [Google Scholar]

- Avery, G.C.; Bergsteiner, H. Sustainable Leadership: Honeybee and Locust Approaches; Routledge: New York, NY, USA, 2011. [Google Scholar]

- Székely, F.; Knirsch, M. Responsible leadership and corporate social responsibility: Metrics for sustainable performance. Eur. Manag. J. 2009, 23, 628–647. [Google Scholar] [CrossRef]

- Schaltegger, S.; Lüdeke-Freund, F.; Hansen, E. Business cases for sustainability—The role of business model innovation for corporate sustainability. Int. J. Innov. Sus. Dev. 2012, 6, 95–119. [Google Scholar] [CrossRef]

- Handy, C. What’s a business for? Harv. Bus. Rev. 2002, 80, 48–55. [Google Scholar]

- Harris, D.; Twomey, D. The enterprise perspective: A new mind-set for competitiveness and sustainability. Compet. Rev.: An Int. Bus. J. 2008, 6, 258–266. [Google Scholar] [CrossRef]

- Kramar, R. Beyond strategic human resource management: Is sustainable human resource management the next approach? Int. J. Hum. Res. Manag. 2014, 25, 1069–1089. [Google Scholar] [CrossRef]

- Dunphy, D.; Griffiths, A.; Benn, S. Organizational Change for Corporate Sustainability; Routledge: London, UK, 2003. [Google Scholar]

- Robèrt, K. Strategic Leadership for Sustainability; Blekinge Institute of Technology: Karlshamn, Sweden, 2007. [Google Scholar]

- Dyllick, T.; Hockerts, K. Beyond the business case for corporate sustainability. Bus. Strategy Environ. 2002, 11, 130–141. [Google Scholar] [CrossRef]

- Gibson, K. Stakeholder and sustainability: An evolving theory. J. Bus. Ethics 2012, 109, 15–25. [Google Scholar] [CrossRef]

- Mariappanadar, S. A conceptual framework for cost measures of harm of HRM Practices. Asia Pac. J. Bus. Admin. 2013, 5, 21–45. [Google Scholar] [CrossRef]

- Albert, M. The Rhine model of capitalism: An investigation. Eur. Bus. J. 1992, 4, 8–22. [Google Scholar]

- D’Amto, A.; Roome, N. Leadership of organizational change toward an integrated model of leadership for corporate responsibility and sustainable development: A process model of corporate responsibility beyond management innovation. Corp. Gov. 2009, 9, 421–434. [Google Scholar]

- Hind, P.; Wilson, A.; Lessen, G. Developing leaders for sustainable business. Corp. Gov. 2009, 9, 7–20. [Google Scholar]

- Kantabutra, S.; Suriyankietkaew, S. Sustainable leadership: Rhineland practices at a Thai small enterprise. Int. J. Entrep. Small Bus. 2013, 19, 77–94. [Google Scholar] [CrossRef]

- Winston, A. Corporate Sustainability Efforts: Feast or Famine. Available online: https://hbr.org/2012/03/corporate-sustainability-effor.html (accessed on 15 November 2015).

- Morsing, M.; Perrini, F. CSR in SMEs: Do SMEs matter for the CSR agenda? Bus. Ethics Eur. Rev. 2009, 18, 1–6. [Google Scholar] [CrossRef]

- Wong, L.; Avery, G.C. Transforming organizations for sustainable practices. Int. J. Interdiscip. Soc. Sci. 2009, 4, 397–408. [Google Scholar]

- Orlitzky, M.; Siegel, D.S.; Waldman, D.A. Strategic corporate social responsibility and environmental sustainability. Bus. Soc. 2011, 50, 6–27. [Google Scholar] [CrossRef]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Pitman: Boston, MA, USA, 1984. [Google Scholar]

- Freeman, R.E.; Wicks, A.C.; Parmar, B.L. Stakeholder theory and “the corporate objective revisited”. Organ. Sci. 2004, 15, 364–369. [Google Scholar] [CrossRef]

- Maak, T.; Pless, N.M. Responsible leadership in a stakeholder society—A relational perspective. J. Bus. Ethics 2006, 66, 99–115. [Google Scholar] [CrossRef]

- Porter, M.E.; Kramer, M.R. Creating shared values. Harv. Bus. Rev. 2011, 89, 62–77. [Google Scholar]

- Brown, M.E.; Trevino, L.K. Ethical leadership: A review and future directions. Lead. Quart. 2006, 17, 595–616. [Google Scholar] [CrossRef]

- Resick, C.J.; Hanges, P.J.; Dickson, M.W.; Mitchelson, J.K. A cross cultural of the endorsement of ethical leadership. J. Bus. Ethics 2006, 63, 345–359. [Google Scholar] [CrossRef]

- Avery, G.C.; Bergsteiner, H. Sufficiency Thinking: Thailand’s Gift to an Unsustainable World; Allen & Unwin: Sydney, Australia, 2016. [Google Scholar]

- Puntasen, A.; Premchuen, S.; Keitdejpunya, P. Application of the Royal Thought about the Sufficiency Economy in SMEs; Thailand Research Fund: Bangkok, Thailand, 2003. [Google Scholar]

- Kantabutra, S.; Ractham, V.; Gerdsri, N.; Nuttavuthisit, K.; Kantamara, P.; Chiarakul, T. Sufficiency Economy Leadership Practices; Thailand Research Fund: Bangkok, Thailand, 2010. [Google Scholar]

- Boal, K.B.; Hooijberg, R. Strategic leadership research: Moving on. Lead. Quart. 2001, 11, 515–549. [Google Scholar] [CrossRef]

- Bennis, W.; Nanus, B. Leaders: The Strategies for Taking Charge; HarperCollins: New York, NY, USA, 2003. [Google Scholar]

- Covey, S. The habits of effective organizations. In Leader to Leader; Hesselbein, F., Cohen, P., Eds.; Jossey-Bass: San Francisco, MA, USA, 1999; pp. 215–226. [Google Scholar]

- Drucker, P.F. Management Challenges for the 21st Century; Harper Business: New York, NY, USA, 1999. [Google Scholar]

- Ott, U.F. The art and economics of international negotiations: Haggling meets hurrying and hanging on in buyer-seller negotiations. J. Innov. Knowl. 2016, 1, 51–61. [Google Scholar]

- International Monetary Fund. World Economic Outlook Database. Available online: http://www.imf.org/external/pubs/ft/weo/2015/02/weodata/weorept.aspx?sy=2014&ey=2014&scsm=1&ssd=1&sort=subject&ds=.&br=1&pr1.x=65&pr1.y=8&c=512%2C668%2C914%2C672%2C612%2C946%2C614%2C137%2C311%2C962%2C213%2C674%2C911%2C676%2C193%2C548%2C122%2C556%2C912%2C678%2C313%2C181%2C419%2C867%2C513%2C682%2C316%2C684%2C913%2C273%2C124%2C868%2C339%2C921%2C638%2C948%2C514%2C943%2C218%2C686%2C963%2C688%2C616%2C518%2C223%2C728%2C516%2C558%2C918%2C138%2C748%2C196%2C618%2C278%2C624%2C692%2C522%2C694%2C622%2C142%2C156%2C449%2C626%2C564%2C628%2C565%2C228%2C283%2C924%2C853%2C233%2C288%2C632%2C293%2C636%2C566%2C634%2C964%2C238%2C182%2C662%2C453%2C960%2C968%2C423%2C922%2C935%2C714%2C128%2C862%2C611%2C135%2C321%2C716%2C243%2C456%2C248%2C722%2C469%2C942%2C253%2C718%2C642%2C724%2C643%2C576%2C939%2C936%2C644%2C961%2C819%2C813%2C172%2C199%2C132%2C733%2C646%2C184%2C648%2C524%2C915%2C361%2C134%2C362%2C652%2C364%2C174%2C732%2C328%2C366%2C258%2C734%2C656%2C144%2C654%2C146%2C336%2C463%2C263%2C528%2C268%2C923%2C532%2C738%2C944%2C578%2C176%2C537%2C534%2C742%2C536%2C866%2C429%2C369%2C433%2C744%2C178%2C186%2C436%2C925%2C136%2C869%2C343%2C746%2C158%2C926%2C439%2C466%2C916%2C112%2C664%2C111%2C826%2C298%2C542%2C927%2C967%2C846%2C443%2C299%2C917%2C582%2C544%2C474%2C941%2C754%2C446%2C698%2C666&s=PPPGDP&grp=0&a=#download (accessed on 30 March 2016).

- Bangkok Bank. Moving Ahead with AEC: Opportunities and Challenges. Available online: http://www.set.or.th/th/news/thailand_focus/2012/Day2/ 20120830_0930_Charnsak_BBL.pdf (accessed on 20 January 2013).

- Eccles, R.G.; Ioannou, I.; Serafeim, G. The Impact of a Corporate Culture of Sustainability on Corporate Behavior and Performance. Available online: http://trippel.sdg.no/wp-content/uploads/2014/09/Eccles-HBR_The-Impact-of-a-Corporate-Culture-of-Sustainability1.pdf (accessed on 30 March 2016).

- White, R.J.; D’Souza, R.R.; McIlwraith, J.C. Leadership in venture backed companies: Going the distance. J. Lead. Organ. Stud. 2007, 13, 121–132. [Google Scholar] [CrossRef]

- Rujirawanich, P.; Addison, R.; Smallman, C. The effects of cultural factors on innovation in a Thai SME. Manag. Res. Rev. 2011, 34, 1264–1279. [Google Scholar] [CrossRef]

- Chittithaworn, C.; Islam, A.; Kaewchana, T.; Yusuf, D.H.M. Factors affecting business success of small and medium enterprises (SMEs) in Thailand. Asian Soc. Sci. 2011, 7, 180–190. [Google Scholar] [CrossRef]

- Jenkins, H. Small business champions for corporate social responsibility. J. Bus. Ethics 2006, 67, 241–256. [Google Scholar] [CrossRef]

- Kantabutra, S. Putting Rhineland principles into practice in Thailand: Sustainable leadership at Bathroom Design company. Glob. Bus. Organ. Excel. 2012, 31, 6–19. [Google Scholar] [CrossRef]

- Suriyankietkaew, S.; Avery, G.C. Employee satisfaction and sustainable leadership practices in Thai SMEs. J. Glob. Responsib. 2014, 5, 160–173. [Google Scholar] [CrossRef]

- Suriyankietkaew, S.; Avery, G.C. Leadership practices influencing stakeholder satisfaction in Thai SMEs. Asia Pac. J. Bus. Admin. 2014, 6, 247–261. [Google Scholar] [CrossRef]

- Avery, G.C. Leadership for Sustainable Futures: Achieving Success in a Competitive World; Edward Elgar: Cheltenham, UK, 2005. [Google Scholar]

- Bassi, L.; Frauenheim, E.; McMurrer, E.; Costello, L. Good Company: Business Success in the Worthiness Era; Berrett-Koehler: San Francisco, CA, USA, 2011. [Google Scholar]

- El-chaarani, H. The success keys for family firms: A comparison between Lebanese and French systems. J. Bus. Retail Manag. Res. 2013, 8, 1–14. [Google Scholar]

- Jing, F.F.; Avery, G.C.; Bergsteiner, H. Enhancing performance in small professional firms through vision communication and sharing. Asia Pac. J. Manag. 2014, 31, 599–620. [Google Scholar] [CrossRef]

- Harrison, J.S.; Wicks, A.C. Stakeholder theory, value, and firm performance. Bus. Ethics Quart. 2013, 23, 97–124. [Google Scholar] [CrossRef]

- Lu, W.M.; Wang, W.K.; Lee, H. The relationship between corporate social responsibility and corporate performance: Evidence from the US semiconductor industry. Int. J. Prod. Res. 2013, 51, 5683–5695. [Google Scholar] [CrossRef]

- Moser, D.V.; Martin, P.R. A broader perspective on corporate social responsibility research in accounting. Account. Rev. 2012, 87, 797–806. [Google Scholar] [CrossRef]

- Sung, S.Y.; Choi, J.N. Effects of team knowledge management on the creativity and financial performance of organizational teams. Organ. Behav. Hum. Decis. Process. 2012, 118, 4–13. [Google Scholar] [CrossRef]

- Zack, M.; McKeen, J.; Singh, S. Knowledge management and organizational performance: An exploratory analysis. J. Knowl. Manag. 2009, 13, 392–409. [Google Scholar] [CrossRef]

- Kantabutra, S.; Rungruang, P. Perceived vision-based leadership effects on staff satisfaction and commitment at a Thai energy provider. Asia Pac. J. Bus. Admin. 2013, 5, 157–178. [Google Scholar] [CrossRef]

- Dotzel, T.; Shankar, V.; Berry, L.L. Service innovativeness and firm value. J. Mark. Res. 2013, 50, 259–276. [Google Scholar] [CrossRef]

- Slater, S.F.; Mohr, J.J.; Sengupta, S. Radical product innovation capability: Literature review, synthesis, and illustrative research propositions. J. Prod. Innov. Manag. 2014, 31, 552–566. [Google Scholar] [CrossRef]

- Joyce, W.; Slocum, J.W. Top management talent, strategic capabilities, and firm performance. Organ. Dyn. 2012, 41, 183–193. [Google Scholar] [CrossRef]

- Collins, J.; Porras, J. Built to Last; HarperCollins: New York, NY, USA, 1994. [Google Scholar]

- Hair, J.F., Jr.; Black, W.C.; Babin, B.J.; Anderson, R.E.; Tatham, R.L. Multivariate Data Analysis, 7th ed.; Prentice Hall: Upper Saddle River, NJ, USA, 2010. [Google Scholar]

- Brown, D.M.; Laverick, S. Measuring corporate performance. Long Range Plan. 1994, 27, 89–98. [Google Scholar] [CrossRef]

- Kaplan, R.S.; Norton, D.P. The balanced scorecard. Harv. Bus. Rev. 2005, 70, 71–79. [Google Scholar]

- Ensley, M.D.; Hmieleski, K.M.; Pearce, C.L. The importance of vertical and shared leadership within new venture top management teams: Implications for the performance of startups. Lead. Quart. 2006, 17, 217–231. [Google Scholar] [CrossRef]

- Perera, S.; Baker, P. Performance measurement practices in small and medium size manufacturing enterprises in Australia. Small Enterp. Res. 2007, 15, 10–30. [Google Scholar] [CrossRef]

- Sian, S.; Roberts, C. UK small owner-managed businesses: Accounting and financial reporting needs. J. Small Bus. Enterp. Dev. 2009, 16, 289–305. [Google Scholar] [CrossRef]

- Jing, F.F. An Investigation of the Relationship between Leadership Paradigms and Organizational Performance in Pharmaceutical Sales Organizations; Fudan University Press: Shanghai, China, 2012. [Google Scholar]

- Ellis, P.D. Distance, dependence and diversity of markets: Effects on market orientation. J. Int. Bus. Stud. 2007, 38, 374–386. [Google Scholar] [CrossRef]

- Murray, J.Y.; Kotabe, M.; Zhou, J.N. Strategic alliance-based sourcing and market performance: Evidence from foreign firms operating in China. J. Int. Bus. Stud. 2005, 36, 187–208. [Google Scholar] [CrossRef]

- McAdam, R.; Reid, R. SME and large organization perceptions of knowledge management: Comparisons and contrasts. J. Knowl. Manag. 2001, 5, 231–241. [Google Scholar] [CrossRef]

- Supyuenyong, V.; Islam, N. Influence of SME characteristics on knowledge management processes: The case study of enterprise resource planning service providers. J. Enterp. Inform. Manag. 2009, 22, 63–80. [Google Scholar]

- Williamson, D.; Lynch-Wood, G. A new paradigm for SME environmental practice. TQM Magaz. 2001, 13, 424–433. [Google Scholar] [CrossRef]

- Edwards, D.; Ram, G.; Black, J. Drivers of environmental behavior in manufacturing SMEs and the implications for CSR. J. Bus. Ethics 2006, 67, 317–330. [Google Scholar]

- Tocher, N.; Rutherford, M.W. Perceived acute human resource management problems in small and medium firms: An empirical examination. Entrep. Theory Pract. 2009, 33, 455–479. [Google Scholar] [CrossRef]

- Hofstede, G.; Hofstede, G.J.; Minkov, M. Cultures and Organizations: Software of the Mind, 3rd ed.; McGraw-Hill: New York, NY, USA, 2010. [Google Scholar]

- Gittell, J.H.; von Nordenflycht, A.; Kochan, T.A. Mutual gains or zero sum? Labor relations and firm performance in the airline industry. Ind. Lab. Relat. Rev. 2004, 57, 163–180. [Google Scholar] [CrossRef]

- DeVaro, J. Teams, autonomy, and the financial performance of firms. Ind. Relat. 2006, 45, 217–269. [Google Scholar] [CrossRef]

- Ameer, R.; Othman, R. Sustainability practices and corporate financial Performance: A study based on the top global corporations. J. Bus. Ethics 2012, 108, 61–79. [Google Scholar] [CrossRef]

- Sorensen, S. The strength of corporate culture and the reliability of firm performance. Admin. Sci. Quart. 2002, 47, 70–91. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Sustainable Leadership (SL) Practices | Descriptions of the SL Practices (Avery and Bergsteiner [4]) | Other Leadership Approaches |

|---|---|---|

| 1. Developing people | Develops everyone continuously | STL, SELP |

| 2. Labor relations | Seeks cooperation | STL, SELP |

| 3. Retaining staff | Values long tenure at all levels | STL, SELP |

| 4. Succession planning | Promotes from within wherever possible | SELP |

| 5. Valuing staff | Is concerned about employees’ welfare | STL, EL, SELP |

| 6. CEO and top team | CEO works as top team member or speaker | STL, SELP |

| 7. Ethical behavior | “Doing the right thing” as an explicit core value | RL, EL, SELP |

| 8. Long-term perspective | Prefers the long-term over short-term profits and growth | STL, SELP |

| 9. Organizational change | Change is an evolving and considered process | RL, SELP |

| 10. Financial independence | Seek maximum independence from others | RL, SELP |

| 11. Environmental responsibility | Protects the environment | STL, SELP |

| 12. Social responsibility | Values people and the community | STL, SELP |

| 13. Stakeholder consideration | Everyone matters | EL, SELP |

| 14. Strong, shared vision | Shared view of future is essential strategic tool | SELP |

| 15. Decision-making | Is consensual and devolved | STL, EL, SELP |

| 16. Self-management | Staff are mostly self-managing | - |

| 17. Team orientation | Teams are extensive and empowered | STL, SELP |

| 18. Culture | Fosters an enabling, widely shared culture | SELP |

| 19. Knowledge sharing and retention | Spreads throughout the organization | STL, SELP |

| 20. Trust | High trust through relationships and goodwill | STL, EL, SELP |

| 21. Innovation | Strong, systematic, strategic innovation at all levels | SELP |

| 22. Staff engagement | Values emotionally committed staff and the resulting commitment | STL, SELP |

| 23. Quality | Is embedded in the culture | SELP |

| Coefficients | |||||||

|---|---|---|---|---|---|---|---|

| Model | Unstandardized Coefficients | Standardized Coefficients | t | Sig. | 95.0% Confidence Interval for B | ||

| B | Std. Error | Beta | Lower Bound | Upper Bound | |||

| (Constant) | 1.644 | 0.455 | - | 3.617 | 0.000 | 0.751 | 2.537 |

| DEPE | 0.023 | 0.054 | 0.021 | 0.423 | 0.672 | −0.083 | 0.128 |

| LARE | 0.137 | 0.050 | 0.151 | 2.759 | 0.006 | 0.039 | 0.234 |

| STRE | 0.055 | 0.042 | 0.070 | 1.308 | 0.191 | −0.028 | 0.137 |

| SUPL | 0.018 | 0.047 | 0.021 | 0.390 | 0.697 | −0.074 | 0.110 |

| VAEM | 0.200 | 0.054 | 0.209 | 3.683 | 0.000 | 0.307 | 0.093 |

| CEOL | −0.025 | 0.045 | −0.030 | −0.565 | 0.573 | −0.114 | 0.063 |

| ETHI | 0.009 | 0.068 | 0.008 | 0.139 | 0.889 | −0.124 | 0.143 |

| LTPE | 0.122 | 0.065 | 0.113 | 1.882 | 0.060 | −0.005 | 0.250 |

| COCH | −0.135 | 0.074 | −0.110 | −1.835 | 0.067 | −0.280 | 0.010 |

| FMIN | 0.048 | 0.044 | 0.052 | 1.089 | 0.277 | −0.039 | 0.134 |

| ENRE | −0.044 | 0.070 | −0.029 | −0.627 | 0.531 | −0.181 | 0.094 |

| SORE | 0.119 | 0.059 | 0.098 | 2.017 | 0.044 | 0.003 | 0.235 |

| STCO | −0.109 | 0.067 | −0.090 | −1.642 | 0.101 | −0.240 | 0.022 |

| SSVI | 0.152 | 0.066 | 0.133 | 2.304 | 0.022 | 0.022 | 0.282 |

| DEDE | 0.040 | 0.052 | 0.044 | 0.767 | 0.443 | −0.062 | 0.141 |

| SEMA | −0.042 | 0.080 | −0.026 | −0.531 | 0.595 | −0.199 | 0.114 |

| TEOR | 0.014 | 0.063 | 0.015 | 0.221 | 0.825 | −0.110 | 0.138 |

| ENCU | 0.043 | 0.069 | 0.045 | 0.626 | 0.532 | −0.092 | 0.179 |

| KSRE | 0.015 | 0.058 | 0.014 | 0.256 | 0.798 | −0.099 | 0.129 |

| TRUS | 0.003 | 0.050 | 0.004 | 0.064 | 0.949 | −0.095 | 0.102 |

| SSIN | 0.033 | 0.058 | 0.033 | 0.563 | 0.573 | −0.082 | 0.148 |

| STEN | 0.146 | 0.075 | 0.125 | 1.960 | 0.051 | 0.000 | 0.293 |

| QUAL | 0.088 | 0.071 | 0.069 | 1.246 | 0.213 | −0.051 | 0.227 |

© 2016 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons by Attribution (CC-BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Suriyankietkaew, S.; Avery, G. Sustainable Leadership Practices Driving Financial Performance: Empirical Evidence from Thai SMEs. Sustainability 2016, 8, 327. https://doi.org/10.3390/su8040327

Suriyankietkaew S, Avery G. Sustainable Leadership Practices Driving Financial Performance: Empirical Evidence from Thai SMEs. Sustainability. 2016; 8(4):327. https://doi.org/10.3390/su8040327

Chicago/Turabian StyleSuriyankietkaew, Suparak, and Gayle Avery. 2016. "Sustainable Leadership Practices Driving Financial Performance: Empirical Evidence from Thai SMEs" Sustainability 8, no. 4: 327. https://doi.org/10.3390/su8040327

APA StyleSuriyankietkaew, S., & Avery, G. (2016). Sustainable Leadership Practices Driving Financial Performance: Empirical Evidence from Thai SMEs. Sustainability, 8(4), 327. https://doi.org/10.3390/su8040327