Analysis on the Relationship between Green Accounting and Green Design for Enterprises

Abstract

:1. Introduction

2. Literature Review

{kind=link}

{kind=link}

| Country and name | Regulations or definitions |

|---|---|

| Denmark, 1995 Green Accounts Act [2] | About 1200 high-pollution enterprises must announce green accounting report. Besides, 200 enterprises voluntarily provide the reports. |

| Netherlands, 1999 Environmental Management Act [2] | About 260 enterprises are compelled to disclose the environmental report. Besides, 40 enterprises voluntarily provide the reports. |

| U.S. Environmental Protection Agency, 1995 An Introduction to Environmental Accounting As A Business Management Tool [3] | Environmental cost accounting means adding environmental cost information to the current cost accounting system, identifying hidden environmental cost and allocating it to proper products or manufacturing. |

| UN Division for Sustainable Development 2001 Environmental Management Accounting (EMA) [4] | Regarding corporate cost, product design production and investment decision-making, EMA can provide immediate and visionary information. EMA is also the decision-making and support tool. The information system allows the firms to manage environmental lifecycle and economic information and to acquire better information and environmental protection strategies. |

| International Federation of Accountants, 2005 Environmental Management Accounting Guidelines [5] | Environmental management accounting manages environmental and economic performance by development and execution of a proper environmental accounting system, including reports and auditing of corporate information and environmental management accounting. Generally speaking, it includes lifecycle accounting, total cost accounting, an effective process and strategic planning of environmental management. |

| Ministry of the Environment, Japan, 2005 Environmental Accounting Guidelines [6] | Green accounting is a quantitative assessment of the cost and effectiveness of enterprises in environmental protection activities. Enterprises are required to have systematic records and reports and are guided to maintain a positive relationship with ecological environment to implement effective and efficient environmental activities. The final goal is to accomplish sustainable development. |

| Environmental Protection Administration, Taiwan, 2008 Industrial Environmental Accounting Guidelines | By measurement, records, analyses and explanation, enterprises’ resources invested in environmental improvement and protection and executive outcomes are completely and consistently reorganized, and the outcomes are provided to stakeholders of enterprises. |

3. Research Design

3.1. Research Method

3.2. Research Process

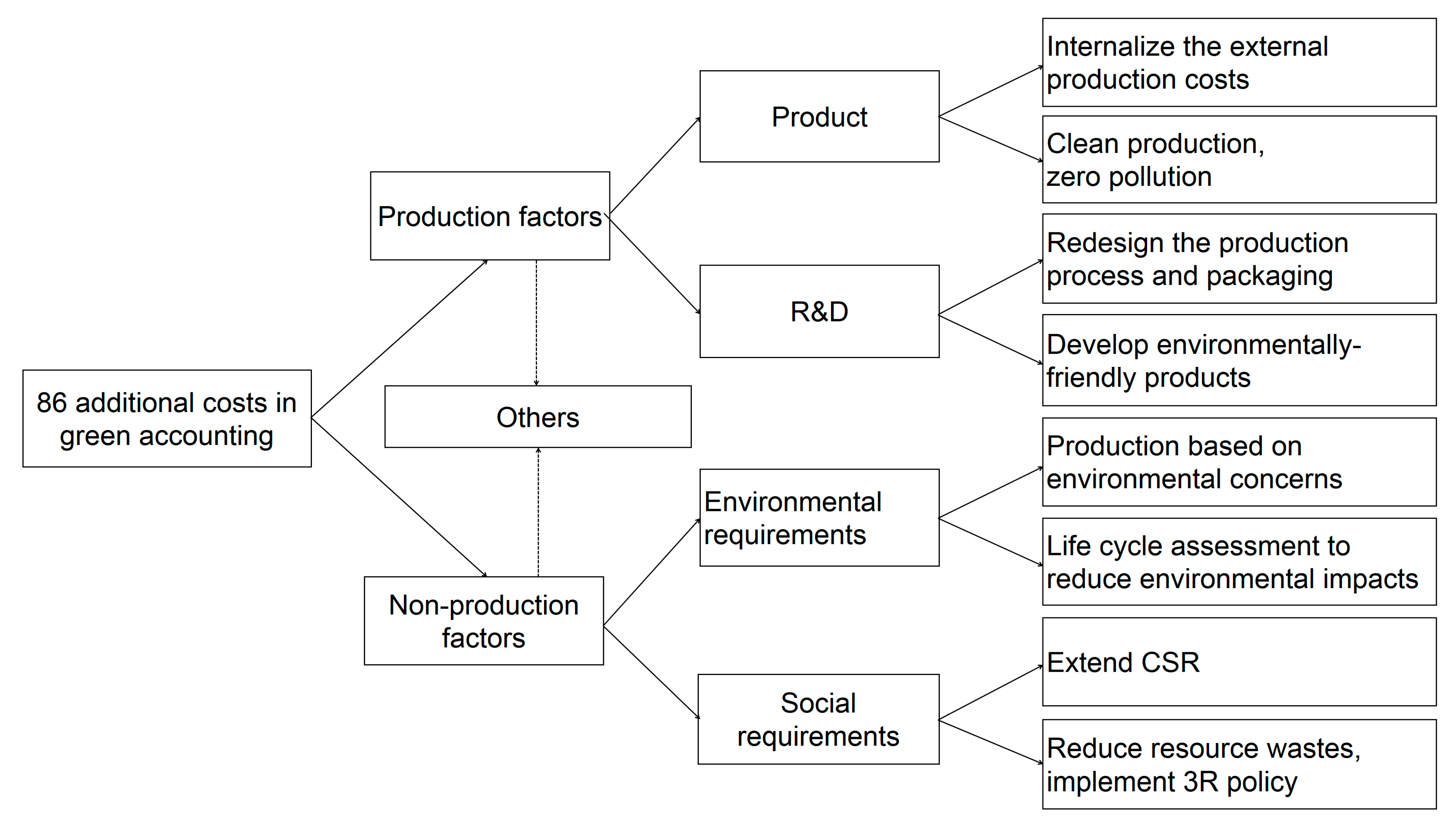

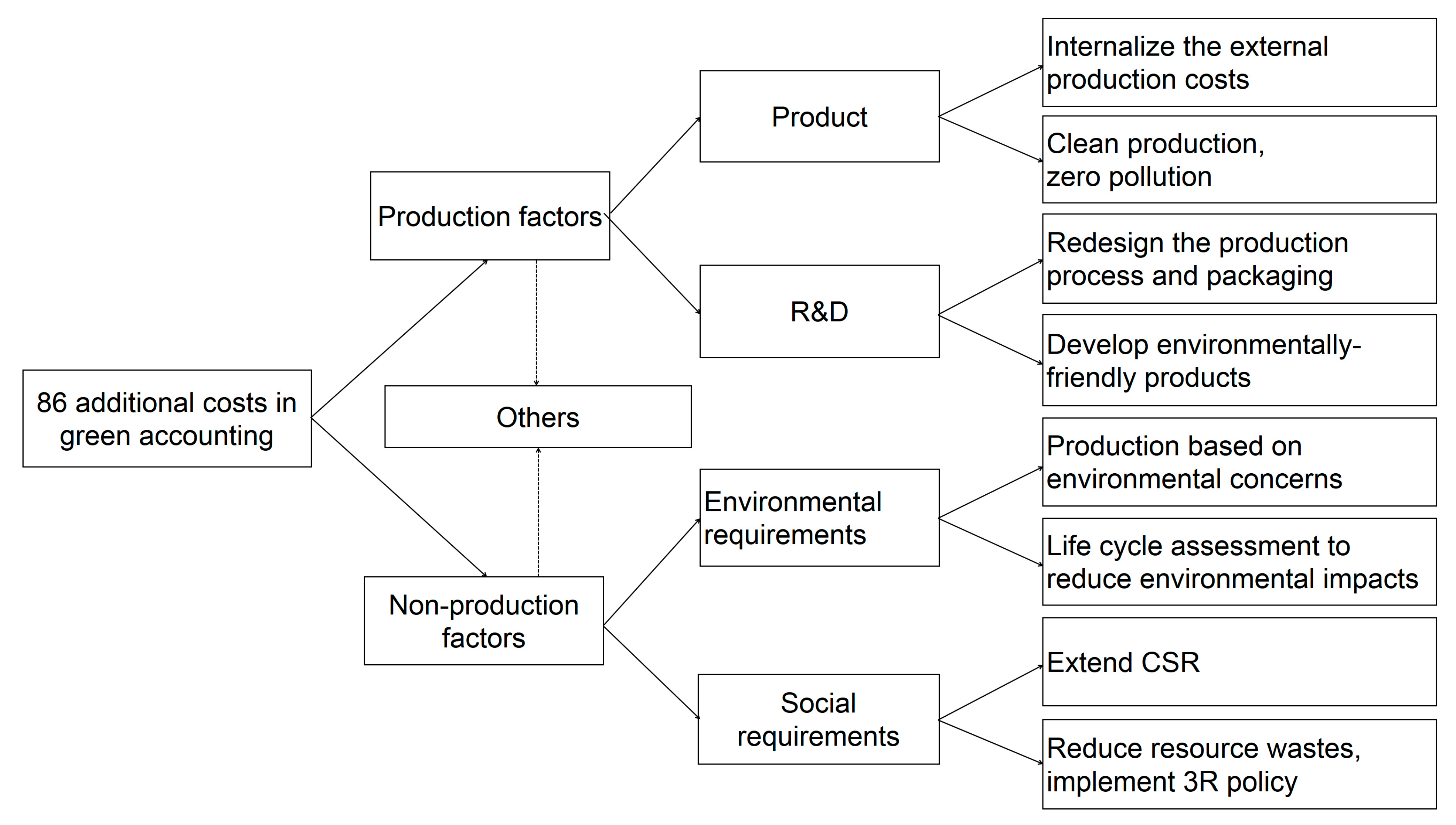

- (1)

- Internalize the external production costs: the enterprises should be responsible for the pollution that has been neglected or handled by the government.

- (2)

- Clean production, zero pollution: the product should not be harmful to the human body, nor produce pollution during the production process.

- (3)

- Redesign the production process and packaging: reduce the environmental impact during production and marketing.

- (4)

- Develop environmentally-friendly products: the production and disposal processes should not generate pollution.

- (5)

- Production based on environmental concerns: the production process that neglects pollution is not allowed.

- (6)

- Lifecycle assessment to reduce environmental impacts: assessment should be conducted during production, use and after use.

- (7)

- Extend CSR: the disposal of waste product should be extended from consumers to extended producer responsibility.

- (8)

- Reduce resource wastes, implement 3R policy: improve production efficiency and increase the reuse or recycling of resources.

4. Analysis and Discussion

- (1)

- Green accounting will lead a more proactive environmental planning through the recognition and the reduction of environmental cost and, consequently, the improvement of the profitability of enterprises [12].

- (2)

- Based on pubic corporate environmental information, the review of corporate performance on the environment and society by construction of an environmental accounting system has become the trend. In the future, we should be devoted to R&D and try to improve environmental pollution [13].

- (3)

- In Australia, a study on large corporations found that the adoption of environmental accounting is positively correlated with process innovation; in other words, green accounting leads to new changes to the production process [14].

- (4)

- Properly-designed environmental standards can promote innovation, lower the total product cost, and enhance product value. Innovation can lead enterprises to use more productive raw materials, resources and labor, as well as reduce the cost incurred due to environmental improvement. By doing so, enterprises can enhance the resource productivity and competitiveness [15].

- (5)

- Green barriers can enhance the environmental performance of enterprises. Green barriers refer to the environmental requirement on product design, production, packaging and disposal, as mandated by the country of import on the importers [16].

- (6)

- Green innovation performances of the enterprises have a positive influence on corporate competitiveness. When the competitors have lower capability, green innovation yields higher positive influence on the corporate competitiveness [17].

- (7)

- Full control of environmental financial information can improve the production and design processes that are detrimental to environmental protection, thus reducing wastes, lowering environmental costs and avoiding risks [18].

- (8)

- Modern perspectives suggest that efficient resource utilization and reduction of wastes could save cost [19]

- (9)

- From the perspective of the resource-based view, new methods to reduce pollution include equipment operation, raw material recycling, product design and environmental awareness when creating market demands and lowering costs. This environmentally-oriented new thinking is based on end treatment. In other words, the concepts of lowering cost, increasing sales volume and reducing pollution should be incorporated in product design [20].

- (10)

- A study on 29 manufacturers that have implemented resource savings found that using technological innovation to increase resource productivity could offset environmental expenditure [21].

- (1)

- Less to produce more: more effective energy use and less waste output can reduce resource exhaustion. In other words, technological innovation can increase resource productivity and design more products with less raw material to reduce total cost.

- (2)

- Prevent pollution: shift from end treatment to pollution prevention; product design should be environmental oriented. The processing, production design and process going against environmental protection should be effectively improved. Saving can reduce waste.

- (3)

- Clean production: the basic requirements for green design are products without toxicity and production without pollution of the environment; for example, the EU has the requirement of three instructions of Directive on the Waste Electronics and Electrical Equipment (WEEE), Directive on the Restriction of Hazardous Substances (RoHS) and Energy-using Products (Eup) in antiviruses. Although clean production looks like a green barrier, nowadays, it is also the global consensus in carrying out environmental protection.

- (4)

- Reduce impacts: it is the requirement of green design; use lifecycle assessment to evaluate the environmental impact; design and employ recyclable and renewable resources; ignore exhausting the limited resources of the Earth; produce an impact on the Earth’s ecological balance.

- (5)

- Environmental performance: improving processing design to make the environmentally external positive performance be greater than that of negative performance; showing environmental friendliness; increasing the corporate competitive advantage and environmental maintenance.

- (6)

- Input equals output: the production costs at every stage are analyzed and recorded by means of material flow cost accounting, from the cost of raw material to the system costs and the remaining and waste material cost, which are provided to engineering personnel as the basis for redesigning. It is required that the raw input equals the product output, trying best to make remaining and wasted material tend to zero.

5. Conclusions

- (1)

- The impact of green accounting on enterprises: Due to the CSR of enterprises, green accounting is the unavoidable trend. Production should not neglect environmental production and the production of low-cost and low-pollution products. Production and product design will be impacted. Based on the green accounting guidelines of the U.S., Japan and Taiwan, the results of the content analysis are as follows: (1) internalize the external production costs; (2) clean production, zero pollution; (3) redesign the production process and packaging; (4) develop environmentally-friendly products; (5) production based on environmental concerns; (6) lifecycle assessment to reduce environmental impacts; (7) extend CSR; and (8) reduce resource wastes and implement 3R policy. Thus, Factor 8 should be adopted as a measure of environmental awareness and pollution alleviation.

- (2)

- Efforts of green design in environmental protection: Green design has been developing for more than 30 years so far and has obtained positive affirmation in many studies, also including the quote in this paper. It has been the consensus around the whole world that green design is helpful for environmental protection. Based on the research results in recent years, six key points were concluded and sorted out in this study: (1) less to produce more; (2) prevent pollution; (3) clean production; (4) reduce impacts; (5) environmental performance; (6) input equals output; to prove that green design can produce benefits in enterprises, reduce environmental pollution and increase production efficiency.

- (3)

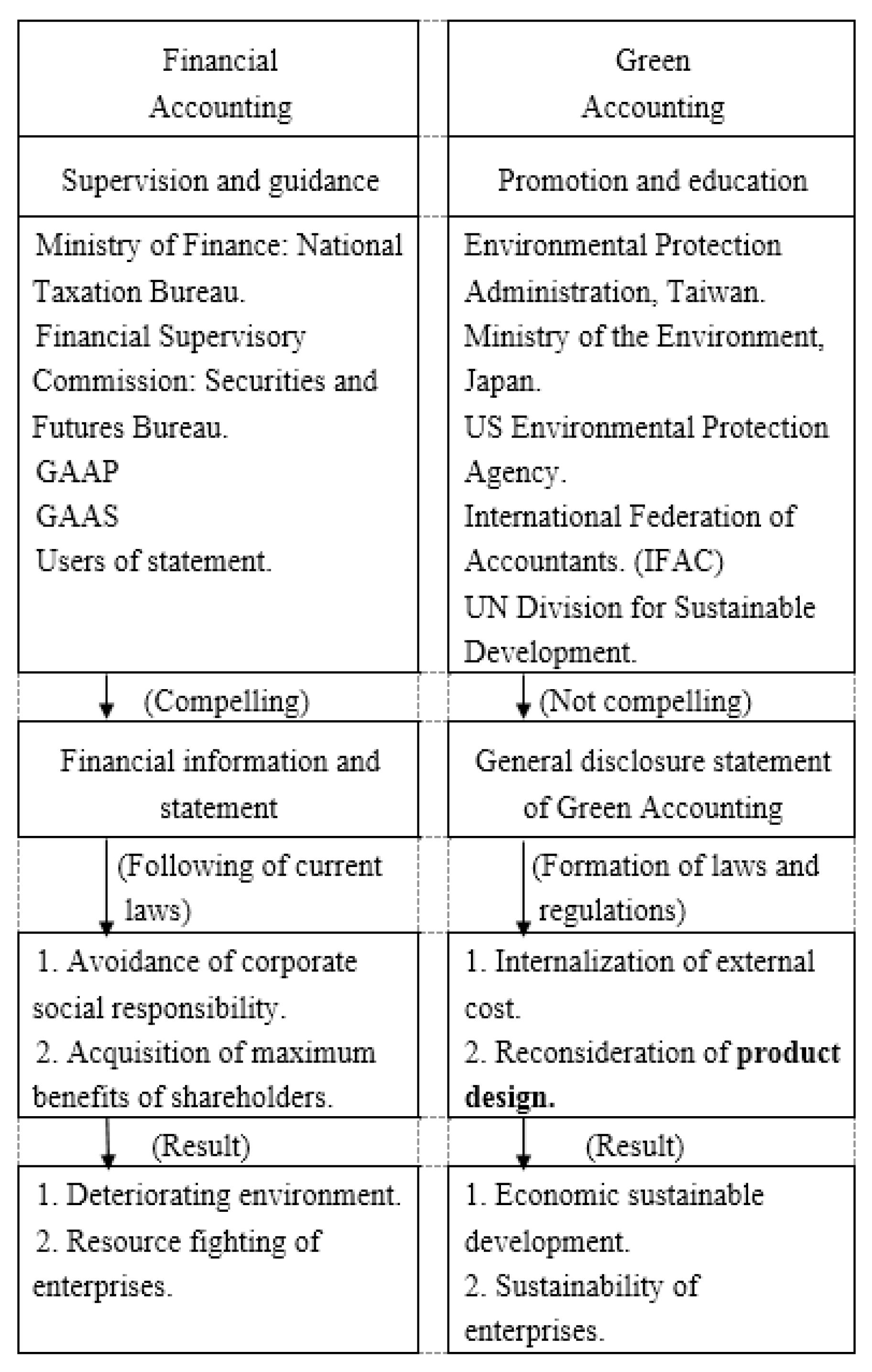

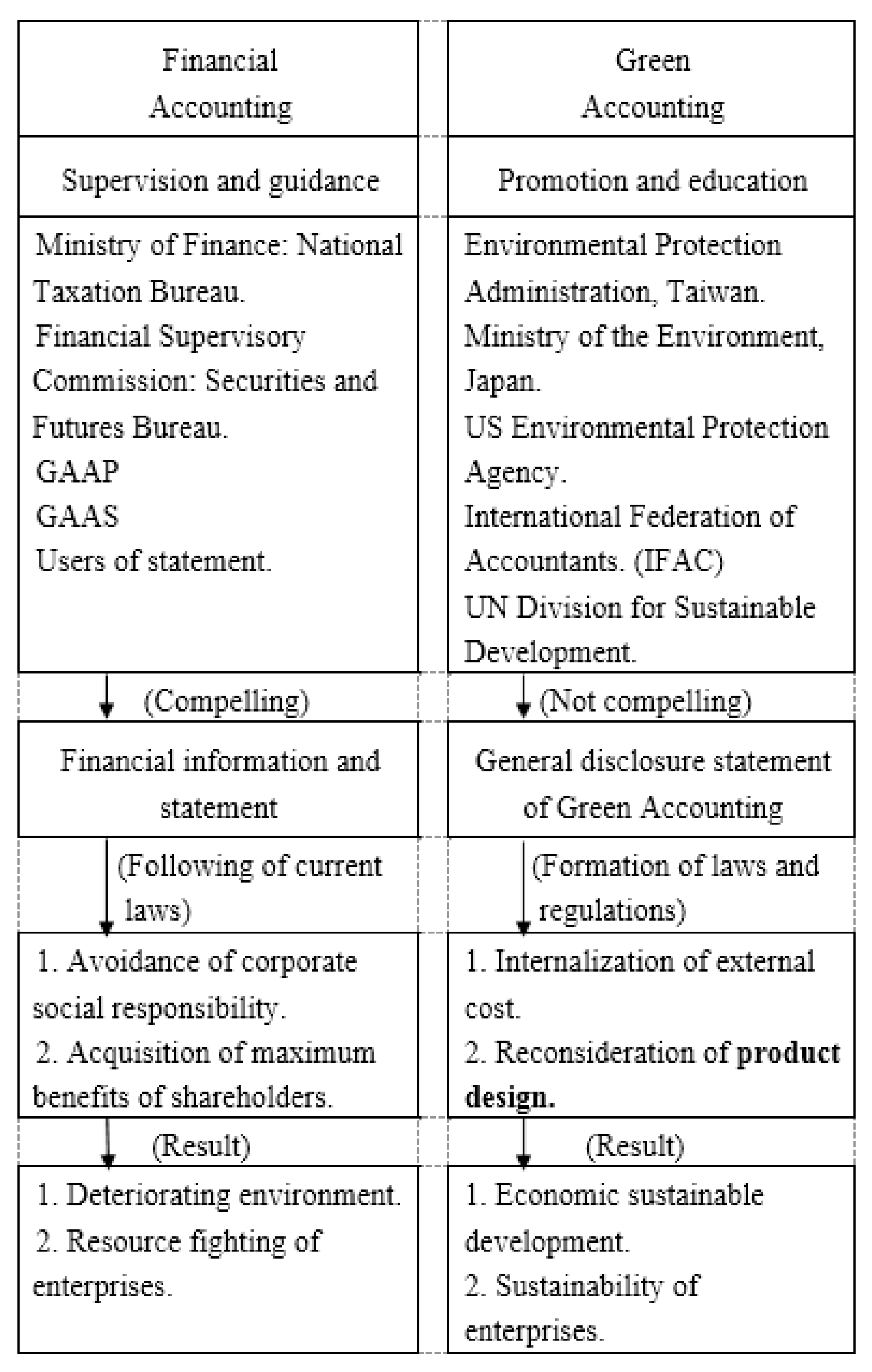

- The aspects of system and technology complement each other: Green accounting is the system aspect, that is the government makes policies about what enterprises should do. If enterprises implement green accounting completely in accordance with policies, it is inferred from the eight factors that many costs increase and the production technology is to be solved. In order to deal with the problem of energy savings plus production increasing and to prevent environmental degradation, the technology aspect needs to be deal with. During the process of corporate business activities, green design can provide technology support for dealing with the negative externalities problem. The method of innovative technology can also increase the resource productivity. It is suggested in the study: if enterprises are willing or are required by the government to implement green accounting in the future, a green design method can be adopted. It can deal with the problem of energy savings plus production increasing. In addition, it can achieve the goal that has been recognized of green design in preventing environment deterioration and maintaining sustainable corporate operation.

Author Contributions

Appendix

| Country | Content | Factor | |

|---|---|---|---|

| A | 1. Monitoring or testing cost is required by law. | 5 | |

| 2. Research or simulation cost is required by law. | 3 | ||

| 3. Planning cost is required by law. | 3 | ||

| 4. Training cost is required by law. | 0 | ||

| 5. Testing cost is required by law. | 5 | ||

| 6. Environmental insurance cost is required by law. | 2 | ||

| 7. Pollution control cost is required by law. | 1 | ||

| 8. Waste fluid detection cost is required by law. | 1 | ||

| 9. Waste management cost is required by law. | 1 | ||

| 10. Environmental tax is required by law. | 5 | ||

| 11. R&D cost in the initial stage | 3 | ||

| 12. Retirement or closing cost when discarded | 2 | ||

| 13. Recovery cost after closing | 2 | ||

| 14. Voluntary addition of cost to strength community relations | 7 | ||

| 15. Voluntary addition of cost to strength monitoring or testing | 5 | ||

| 16. Voluntary addition of cost to increase auditing or training | 0 | ||

| 17. Voluntary addition of cost to find green suppliers | 6 | ||

| 18. Voluntary addition of cost to make improvements | 5 | ||

| 19. Voluntary addition of cost to strengthen recycling | 8 | ||

| 20. Voluntary R&D cost | 3 | ||

| 21. Cost to establish environmental groups or research institutes | 5 | ||

| 22. Cost to follow new regulations | 0 | ||

| 23. Loss from damaging natural resources | 0 | ||

| 24. Cost of maintaining corporate image | 7 | ||

| 25. Penalty or compensation cost | 1 | ||

| J | 26. Cost to prevent air pollution | 5 | |

| 27. Cost to prevent water pollution | 5 | ||

| 28. Cost to prevent soil pollution | 5 | ||

| 29. Cost to prevent noise pollution | 5 | ||

| 30. Cost to prevent vibration pollution | 5 | ||

| 31. Cost to prevent ozone pollution | 5 | ||

| 32. Cost to prevent land subsidence | 5 | ||

| 33. Cost to prevent other pollutions | 0 | ||

| 34. Cost to prevent global warming | 7 | ||

| 35. Cost to develop energy-saving production | 8 | ||

| 36. Cost to effectively use resources | 8 | ||

| 37. Cost to recycle industrial wastes | 2 | ||

| 38. Cost to dispose industrial wastes | 2 | ||

| 39. Cost to supplement recycling | 8 | ||

| 40. Additional cost for adopting green procurement | 6 | ||

| 41. Additional cost for producing environmentally-friendly products | 4 | ||

| 42. Additional cost for reducing packaging | 4 | ||

| 43. Cost of recycling discarded products | 8 | ||

| 44. Cost of disposing discarded products | 8 | ||

| 45. Cost to maintain environmental management | 5 | ||

| 46. Cost to monitor environmental impacts | 5 | ||

| 47. Cost to provide employee training on environmental management | 2 | ||

| 48. Cost of environmental improvement activities | 7 | ||

| 49. R&D cost on environmentally-friendly products | 4 | ||

| 50. R&D cost on reducing environmental impacts during production | 6 | ||

| 51. R&D cost on reducing environmental impacts during marketing | 6 | ||

| 52. Donations to environmental groups | 7 | ||

| 53. Donations to support community environmental activities | 7 | ||

| 54. Cost of environmental recovery | 1 | ||

| 55. Litigation cost on environmental protection | 0 | ||

| 56. Environmental insurance cost | 2 | ||

| T | 57. Cost of air pollution prevention | 5 | |

| 58. Water pollution prevention | 5 | ||

| 59. Soil and groundwater pollution prevention | 5 | ||

| 60. Noise pollution prevention | 5 | ||

| 61. Vibration pollution prevention | 5 | ||

| 62. Odor pollution prevention | 5 | ||

| 63. Land subsidence prevention | 5 | ||

| 64. Climate change prevention | 7 | ||

| 65. Ozone damage prevention | 7 | ||

| 66. Effective use of resources | 8 | ||

| 67. Reduce and recycle general wastes | 8 | ||

| 68. Reduce and recycle hazardous wastes | 8 | ||

| 69. Treatment and final disposal of general wastes | 8 | ||

| 70. Treatment and final disposal of hazardous wastes | 8 | ||

| 71. Additional cost of procuring raw materials with low environmental impact | 6 | ||

| 72. Cost of 3R and modification for product | 8 | ||

| 73. Cost of 3R and modification for container and packaging | 8 | ||

| 74. Cost of environmental education | 0 | ||

| 75. Cost of implementation and maintenance of environmental management system | 5 | ||

| 76. Cost of environmental monitoring | 5 | ||

| 77. R&D of products with low environmental impact | 6 | ||

| 78. R&D of production process with low environmental impact | 6 | ||

| 79. R&D of sales method with low environmental impact | 6 | ||

| 80. Cost of improving external environment | 1 | ||

| 81. Donations to environmental protection | 7 | ||

| 82. Cost of soil recovery | 1 | ||

| 83. Insurance cost on environmental protection | 2 | ||

| 84. Settlement or compensation cost on environmental disputes | 1 | ||

| 85. Penalty and litigation cost on environmental matters | 0 | ||

| 86. Energy tax | 5 |

- Product, 18.6%

- (1).

- Internalize the external production costs: eight items, 9.3%

- (2).

- Clean production, zero pollution: eight items, 9.3%

- R&D, 8.1%

- (3).

- Redesign the production process and packaging: four items, 4.6%

- (4).

- Develop environmentally-friendly products: three items, 3.5%

- Environmental requirements, 38.4%

- (5).

- Production based on environmental concerns: 25 items, 29.1%

- (6).

- Lifecycle assessment to reduce environmental impacts: eight items, 9.3%

- Social requirements, 25.6%

- (7).

- Extend CSR: nine items, 10.5%

- (8).

- Reduce resource wastes, implement 3R policy: 13 items, 15.1%

- Others, 9.3%

- (9).

- Irrelevant to production or operation: eight items, 9.3%

Conflicts of Interest

References

- Huy, P.Q. Exploring the Vietnamese Environment Accounting With an Introduction About the Green Accounting Information System. J. Mod. Acc. Audit. 2014, 10, 675–682. [Google Scholar]

- Ding, X.F. A Study of the Influences of Environmental Accounting and Environmental Protection to Financial Performance. Master’s Thesis, National Taiwan Ocean University, Keelung City, Taiwan, 2009. [Google Scholar]

- U.S. Environmental Protection Agency website. Available online: http://www.epa.gov/oppt/library/pubs/archive/acct-archive/resources.htm (accessed on 15 January 2015).

- U.N. Division for Sustainable Development website. Available online: http://www.un.org/esa/sustdev/index.html (accessed on 15 January 2015).

- International Federation of Accountants website. Available online: http://www.ifac.org/ (accessed on 15 January 2015).

- Ministry of the Environment Government of Japan. Environmental Reporting Guidelines; Environment Agency Japan: Tokyo, Japan, 2005. [Google Scholar]

- Roozenburg, N.F.M.; Eekels, J. Product Design: Fundamentals and Methods; John Wiley & Sons Ltd.: Hoboken, NJ, USA, 1995; p. 83. [Google Scholar]

- Tu, J.C. Sustainable Design of Products—Theories and Practices of Green Design, 1st ed.; Asiapac Books Pte Ltd.: Taipei, Taiwan, 2005; p. 24. [Google Scholar]

- Guan, S.S. Methods of Design Research; Chuan Hwa Book: Taipei, Taiwan, 2010; pp. 85–93. [Google Scholar]

- Chang, S.S. Research Method, 2nd ed.; Tsang Hai Publishing: Taichung, Taiwan, 2007; p. 549. [Google Scholar]

- Huang, W.C. Study on the Use of Environmental Management by Enterprises to Enhance Competitiveness-Use ISO14000 as an Example. Master’s Thesis, Executive Master of Business Administration, College of Management, National Taiwan University, Taipei, Taiwan, 2004. [Google Scholar]

- Moorthy, K.; Yacob, P. Green accounting: Cost measures. Open J. Acc. 2013, 2, 4–7. [Google Scholar] [CrossRef]

- Chang, S.H.; Huang, S.Y.; Lin, Y.C. Study on Environmental Accounting Construction Process of Small and Medium Enterprises: Using Film Coating Company as an Example. J. Environ. Manag. 2012, 12, 1–25. [Google Scholar] [CrossRef]

- Aldónio, F.; Carly, M.; Bayu, H. Environmental management accounting and innovation: An exploratory analysis. Acc. Audit. Account. J. 2010, 23, 920–948. [Google Scholar] [CrossRef]

- Porter, M.E. Game Theory, 2nd ed.; Commonwealth Publishing Co. Ltd: Taipei, Taiwan, 2009. [Google Scholar]

- Wang, C.Y. The Latest Development and Prevention of Green Barriers. Market Mod. 2007, 07Z, 2–3. [Google Scholar]

- Chen, Y.S.; Lai, S.B.; Wen, C.T. The Influence of Green Innovation Performance on Corporate Advantage in Taiwan. J. Bus. Ethics 2006, 67, 331–339. [Google Scholar] [CrossRef]

- Kao, Y.S. Study on Factors of ISO14001 Manufacturers’ Adoption of Environmental Accounting System in Taiwan. Master’s Thesis, Graduate Institute of Business & Management, National Chiao Tung University, Hsinchu City, Taiwan, 2004. [Google Scholar]

- Berry, M.A.; Rondinelli, D.A. Proactive Corporate Environmental Management: A New Industrial Revolution. Acad. Manag. Exec. 1998, 12, 38–50. [Google Scholar]

- Nehrt, C. Maintainability of First Mover Advantages When Environmental Regulations Differ Between Countries. Acad. Manag. Rev. 1998, 23, 77–97. [Google Scholar]

- Porter, M.E.; Claas, V.D.L. Green and competitive: Ending the stalemate. Harv. Bus. Rev. 1995, 73, 120–134. [Google Scholar]

© 2015 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tu, J.-C.; Huang, H.-S. Analysis on the Relationship between Green Accounting and Green Design for Enterprises. Sustainability 2015, 7, 6264-6277. https://doi.org/10.3390/su7056264

Tu J-C, Huang H-S. Analysis on the Relationship between Green Accounting and Green Design for Enterprises. Sustainability. 2015; 7(5):6264-6277. https://doi.org/10.3390/su7056264

Chicago/Turabian StyleTu, Jui-Che, and Hsieh-Shan Huang. 2015. "Analysis on the Relationship between Green Accounting and Green Design for Enterprises" Sustainability 7, no. 5: 6264-6277. https://doi.org/10.3390/su7056264

APA StyleTu, J.-C., & Huang, H.-S. (2015). Analysis on the Relationship between Green Accounting and Green Design for Enterprises. Sustainability, 7(5), 6264-6277. https://doi.org/10.3390/su7056264