Monetary and Fiscal Policies for a Finite Planet

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

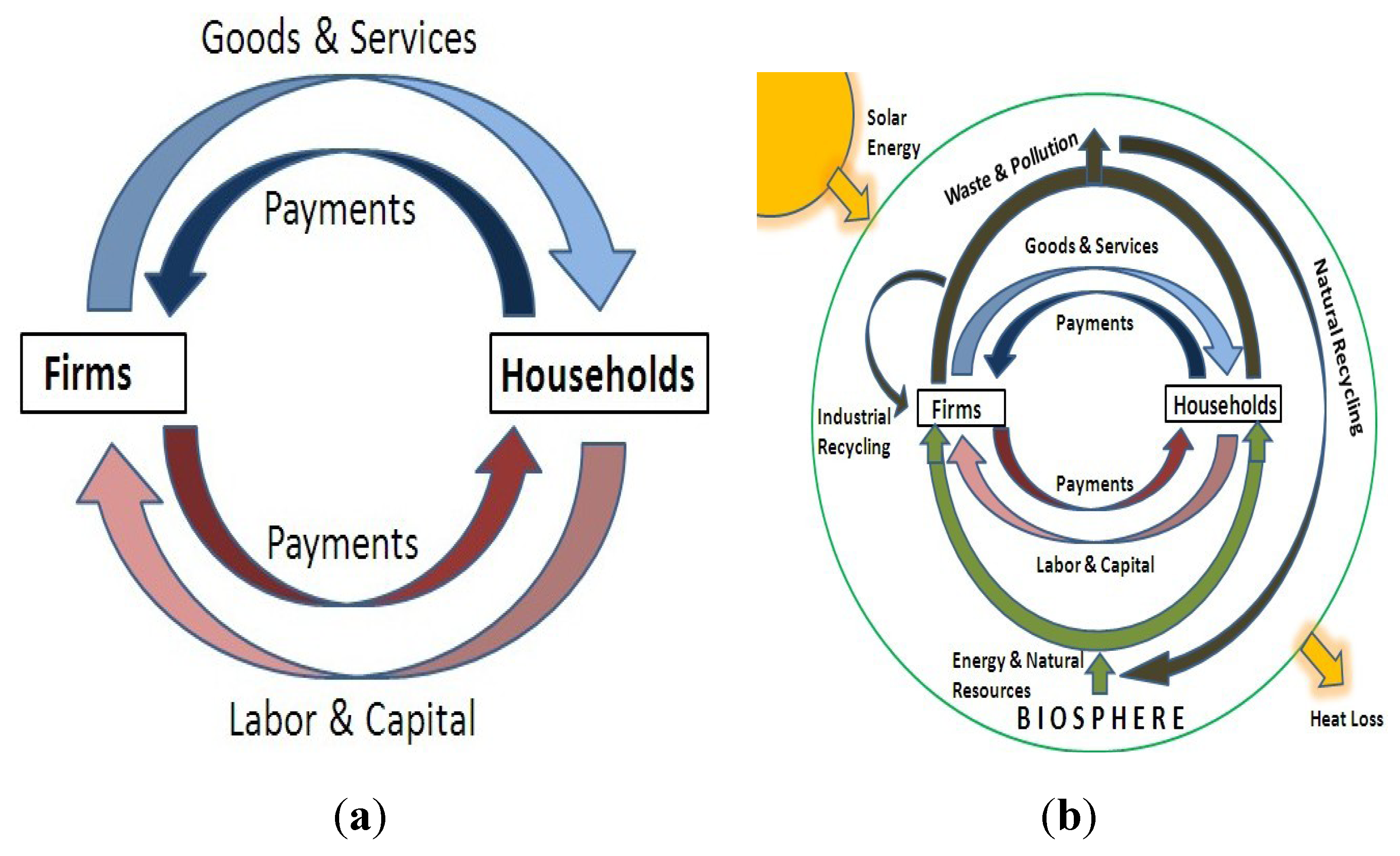

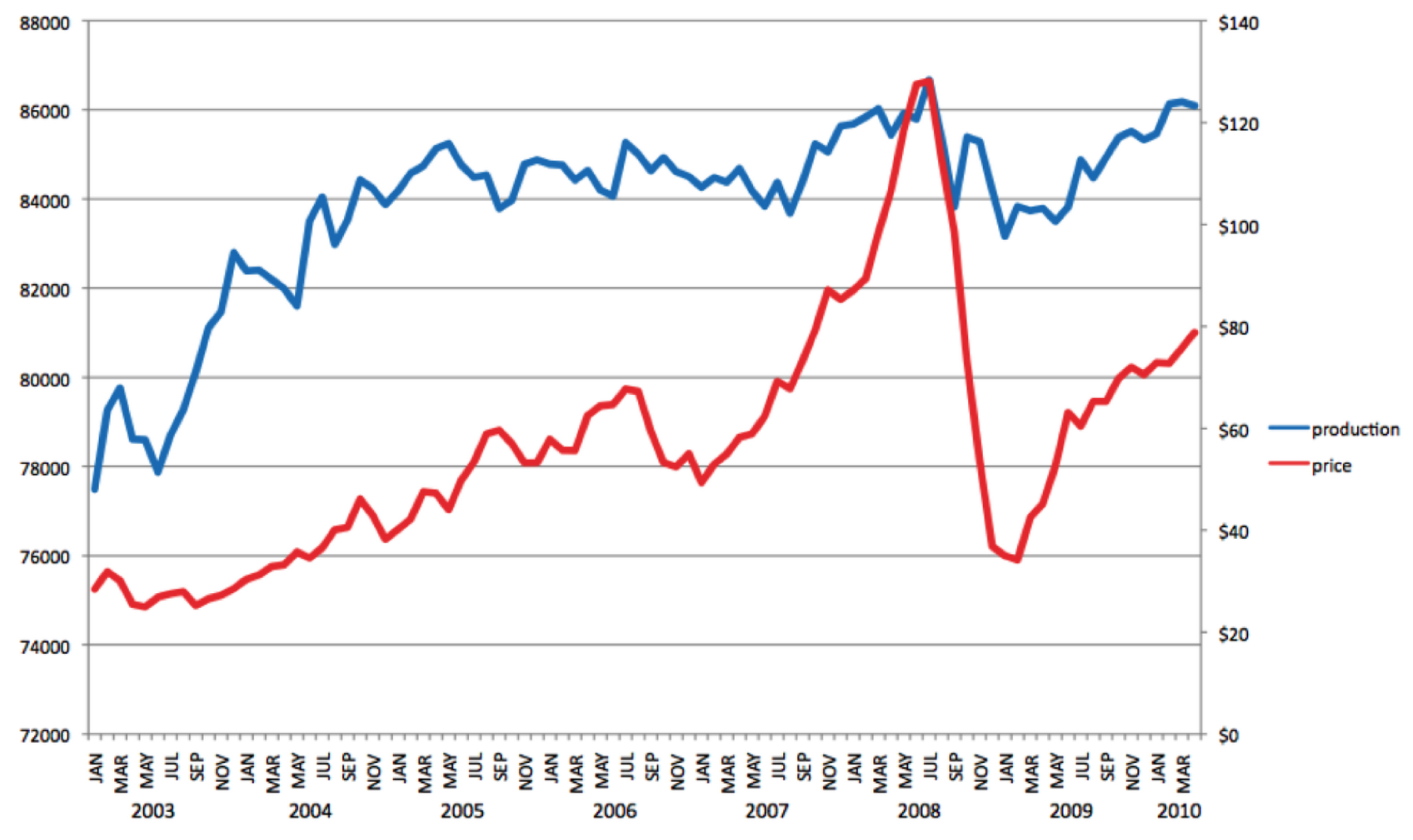

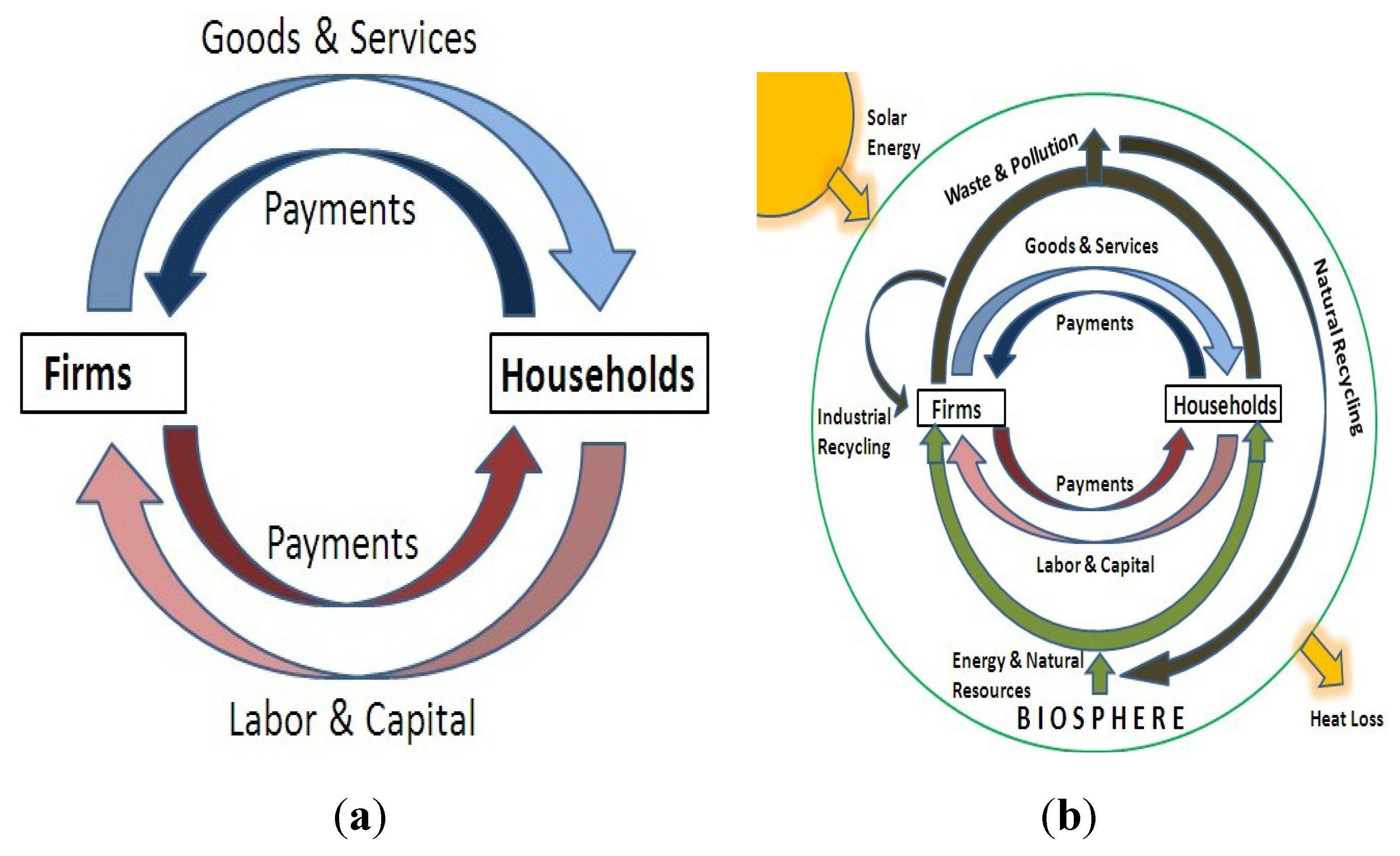

2. Biophysical Limits on a Finite Planet

2.1. The Laws of Physics

2.2. The Laws of Ecology

2.3. The Laws of Money

3. Building a Sustainable Macro-Economy

3.1. Problems with the Current System

3.2. Solutions 1: Monetary Policy

3.2.1. Banks with 100% Fractional Reserves

3.2.2. Public Creation and Destruction of Money

3.2.2.1. Lending and Repayment

3.2.2.2. Spending and Taxing

3.2.2.3. Purchasing Bonds from State and Local Governments

3.3. Solutions 2: Fiscal Policy

3.3.1. Public Expenditures in a SSE

3.3.2. Tax Bads, Not Goods

3.3.3. Tax What We Take, Not What We Make

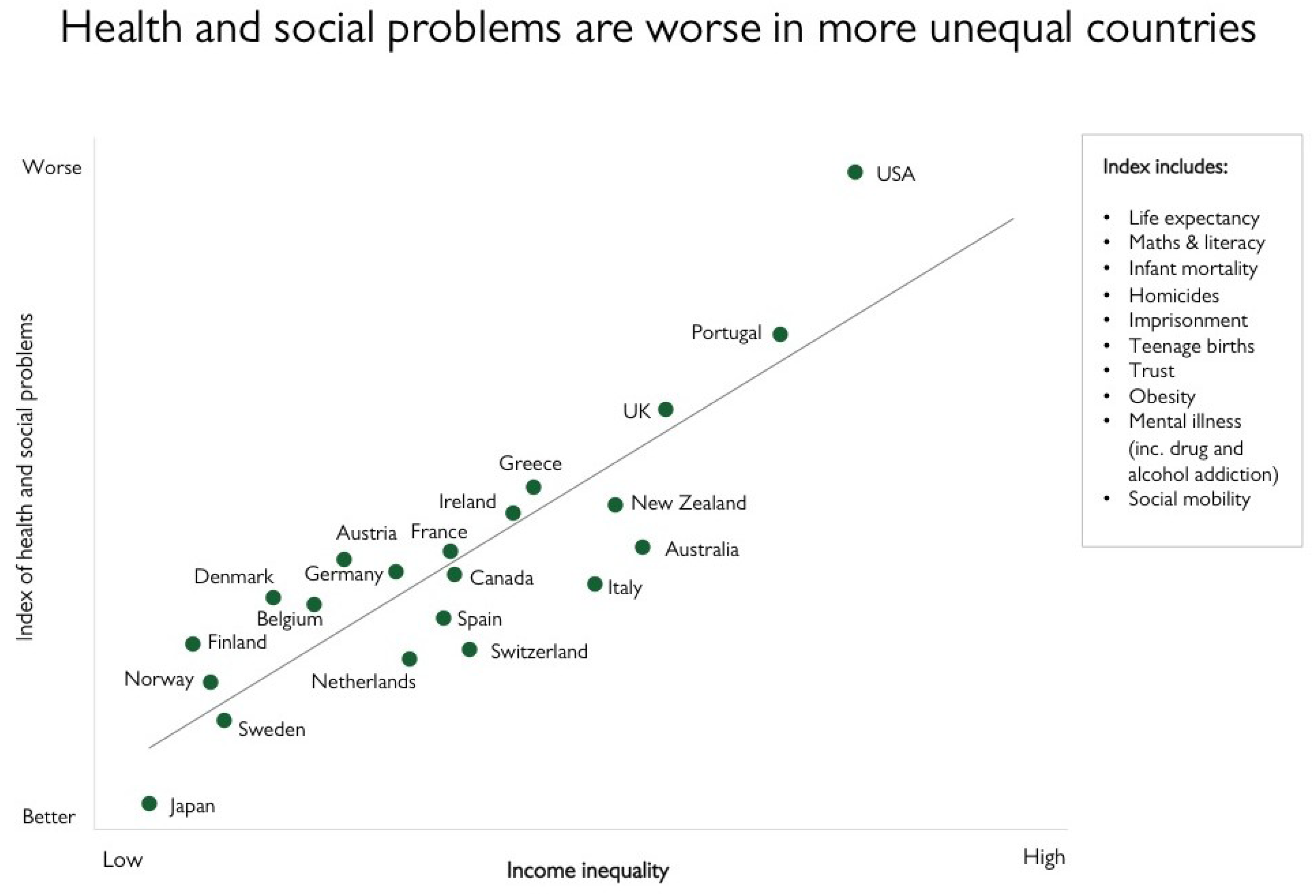

3.3.4. Taxation to Reduce Inequality

3.3.5. Cap and Auction and a Commons Asset Trust

3.4. Solutions 3: Monetary Trust

4. Transition

4.1. Paying off Existing Debt

4.2. Taking Advantage of Crisis

5. Conclusions

Acknowledgments

Conflict of Interest

References

- Harris, J.M.; Codur, A.-M. Macroeconomics and the Environment; Global Development and Environment Institute: Boston, MA, USA, 2004. [Google Scholar]

- Daly, H.E. Economics in a full world. Sci. Am. 2005, 293, 100–107. [Google Scholar] [CrossRef]

- Daly, H.E. Steady-State Economics: The Political Economy of Bio-Physical Equilibrium and Moral Growth; W. H. Freeman and Co.: San Francisco, CA, USA, 1977. [Google Scholar]

- Georgescu-Roegen, N. Energy and economic myths. South. Econ. J. 1975, 41, 347–381. [Google Scholar] [CrossRef]

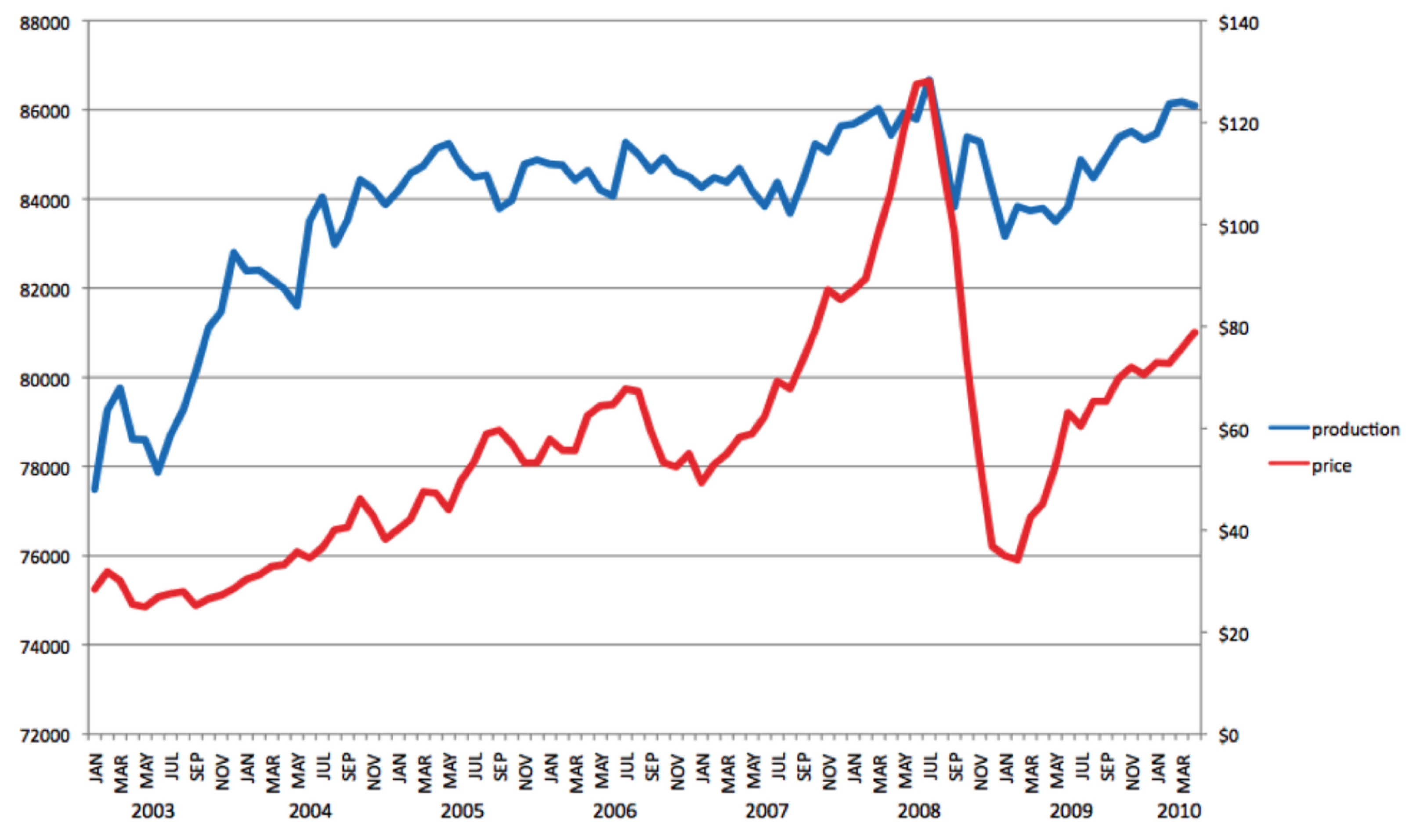

- British Petroleum, Statistical review of world energy, full report 2012. Available online: http://www.bp.com (accessed on 13 June 2013).

- Georgescu-Roegen, N. The Entropy Law and the Economic Process; Harvard University Press: Cambridge, MA, USA, 1971. [Google Scholar]

- Hall, C.A.S.; Cleveland, C.J.; Kaufmann, R. Energy and Resource Quality; Wiley Interscience: New York, NY, USA, 1986. [Google Scholar]

- Wackernagel, M.; Schulz, N.B.; Deumling, D.; Linares, A.C.; Jenkins, M.; Kapos, V.; Monfreda, C.; Loh, J.; Myers, N.; Norgaard, R.; et al. Tracking the ecological overshoot of the human economy. Proc. Natl. Acad. Sci. USA 2002, 99, 9266–9271. [Google Scholar] [CrossRef]

- Rockstrom, J.; Steffen, W.; Noone, K.; Persson, A.; Chapin, F.S.; Lambin, E.F.; Lenton, T.M.; Scheffer, M.; Folke, C.; Schellnhuber, H.J.; et al. A safe operating space for humanity. Nature 2009, 461, 472–475. [Google Scholar] [CrossRef]

- Malghan, D. A dimensionally consistent aggregation framework for biophysical metrics. Ecol. Econ. 2011, 70, 900–909. [Google Scholar] [CrossRef]

- Ekins, P. Identifying critical natural capital: Conclusions about critical natural capital. Ecol. Econ. 2003, 44, 277–292. [Google Scholar] [CrossRef]

- Farley, J. The role of prices in conserving critical natural capital. Conserv. Biol. 2008, 22, 1399–1408. [Google Scholar] [CrossRef]

- Meadows, D. Leverage points: Places to intervene in a system. Solutions 2009, 1, 41–49. [Google Scholar]

- Millennium Ecosystem Assessment, Ecosystems and Human Well-Being: Synthesis; Island Press: Washington, DC, USA, 2005.

- Daly, H.E.; Farley, J. Ecological Economics: Principles and Applications, 2nd ed.; Island Press: Washington, DC, USA, 2010; p. 537. [Google Scholar]

- Greco, T. Money: Understanding and Creating Alternatives to Legal Tender; Chelsea Green Publishing: White River Junction, VT, USA, 2001. [Google Scholar]

- Note that the US Federal Reserve Bank is actually a quasi-public central bank designed to be largely independent from the government. Also, in the EU zone, it is the European Central Bank that has a monopoly on money supply, not the national governments. National governments in the EU zone function much like states in the US: they must tax or borrow before they can spend. This paper will nonetheless discuss the situation in which the central bank and treasury are controlled by national government.

- Federal Reserve Economic Data, U.S. Available online: http://research.stlouisfed.org/fred2/ series/TREAST (accessed on 13 June 2013).

- Egnal, M. Clash of Extremes: The Economic Origins of the Civil War; Hill and Wang: New York, NY, USA, 2009. [Google Scholar]

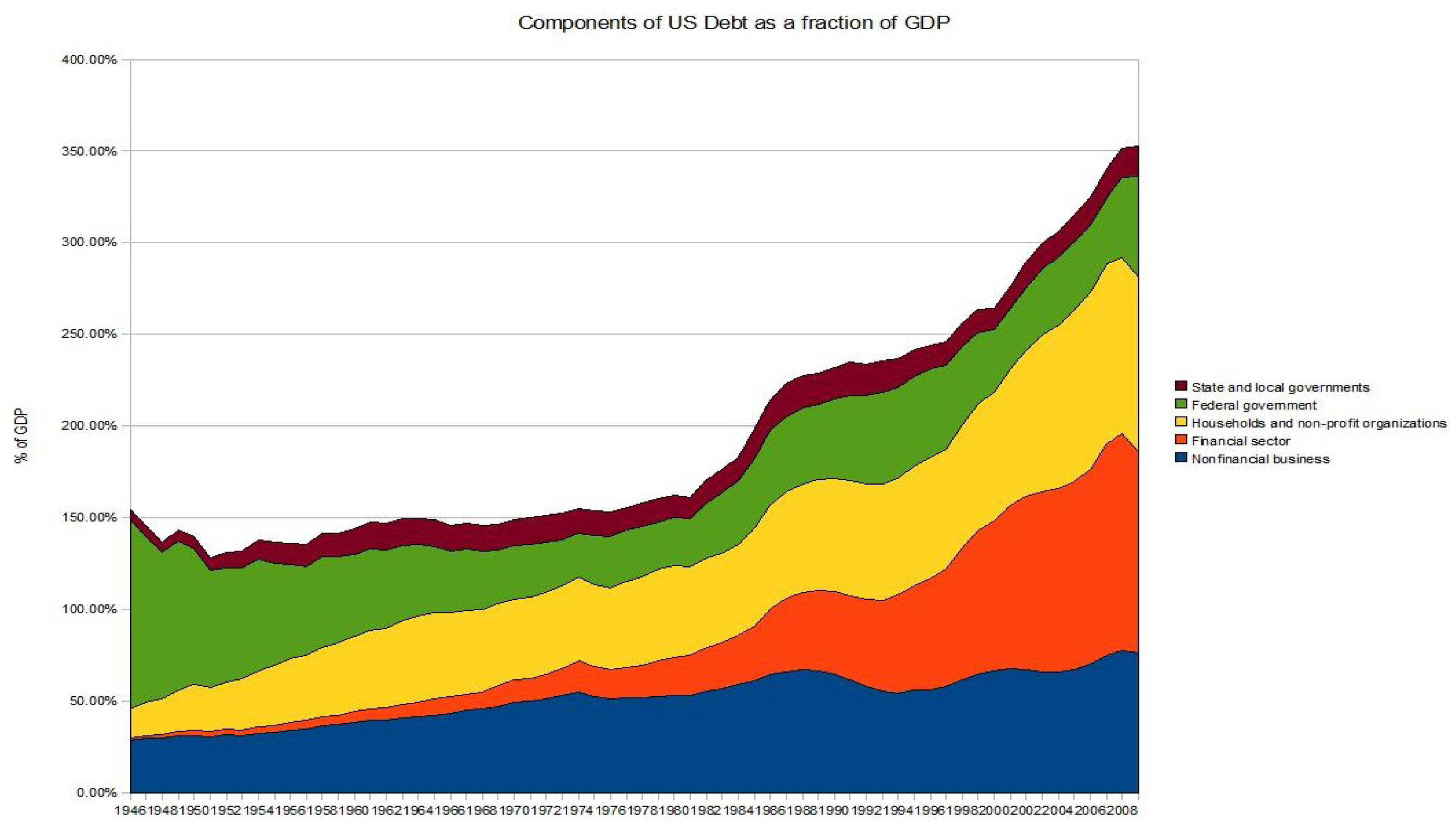

- Components of total united states debt. Wikimedia Commons: 2010. Available online: http://commons.wikimedia.org/wiki/File:Components-of-total-US-debt.jpg (accessed on 5 May 2012).

- Soddy, F. The Role of Money: What it Should Be, Contrasted with What It Has Become; Harcourt, Brace and Co.: New York, NY, USA, 1935. [Google Scholar]

- Daly, H.E. The economic thought of frederick soddy. Hist. Polit. Econ. 1980, 12, 469–488. [Google Scholar] [CrossRef]

- Daly, H.E.; Cobb, J.B., Jr. For the Common Good: Redirecting the Economy toward Community, the Environment, and a Sustainable Future, 2nd ed.; Beacon Press: Boston, MA, USA, 1994. [Google Scholar]

- Minsky, H.P. Stabilizing an Unstable Economy; Yale University Press: New Haven, CT, USA, 1986. [Google Scholar]

- Daly, H.E.; Townsend, K. Valuing the Earth: Economics, Ecology, Ethics; MIT Press: Cambridge, MA, USA, 1993; pp. 22–23. [Google Scholar]

- Costanza, R.; Fisher, B.; Ali, S.; Beer, C.; Bond, L.; Boumans, R.; Danigelis, N.L.; Dickinson, J.; Elliott, C.; Farley, J.; et al. An integrative approach to quality of life measurement, research, and policy. Surv. Perspect. Integr. Environ. Soc. 2008, 1, 11–15. [Google Scholar] [CrossRef]

- López, R.; Galinato, G.I. Should governments stop subsidies to private goods? Evidence from rural latin america. J. Public Econ. 2007, 91, 1071–1094. [Google Scholar] [CrossRef]

- Farley, J. Rethinking gnp: From welfare to cost. Al Jazeera 2001. [Google Scholar]

- Farley, J.; Perkins, S. Economics of Information in a Green Economy. In Building a Green Economy; Robertson, R., Ed.; Michigan State University Press: East Lansing, MI, USA, 2013. [Google Scholar]

- Dyson, B.G.T.; Ryan-Collins, J.; Werner, R. Towards a 21st Century Banking and Monetary System: Submission to the Independent Commission on Banking; New Economics Foundation: London, UK, 2011; pp. 1–39. [Google Scholar]

- Lawn, P. Facilitating the transition to a steady-state economy: Some macroeconomic fundamentals. Ecol. Econ. 2010, 69, 931–936. [Google Scholar] [CrossRef]

- Misch, F.; Wolff, P. The returns on public investment: Concepts, evidence and policy challenges. Available online: http://edoc.vifapol.de/opus/volltexte/2011/3272/pdf/DP_25.2008.pdf (accessed on 14 June 2013).

- The authors agree with the comments of one anonymous reviewer that the policies recommended here will require revisiting the traditional conception of full employment. Although there is insufficient space to explore this topic here, additional scholarship is encouraged into such topics as: What is the meaning of work? How are jobs defined as a subset of work? How is useful work rewarded? What is classified as work?

- Durning, A.T.; Bauman, Y. Tax Shift: How to Help the Economy, Improve the Environment, and Get the Tax Man off Our Backs; Northwest Environment Watch: Seattle, WA, USA, 1998. [Google Scholar]

- Gaffney, M. The hidden taxable capacity of land: Enough and to spare. Int. J. Soc. Econ. 2008, 36, 328–411. [Google Scholar] [CrossRef]

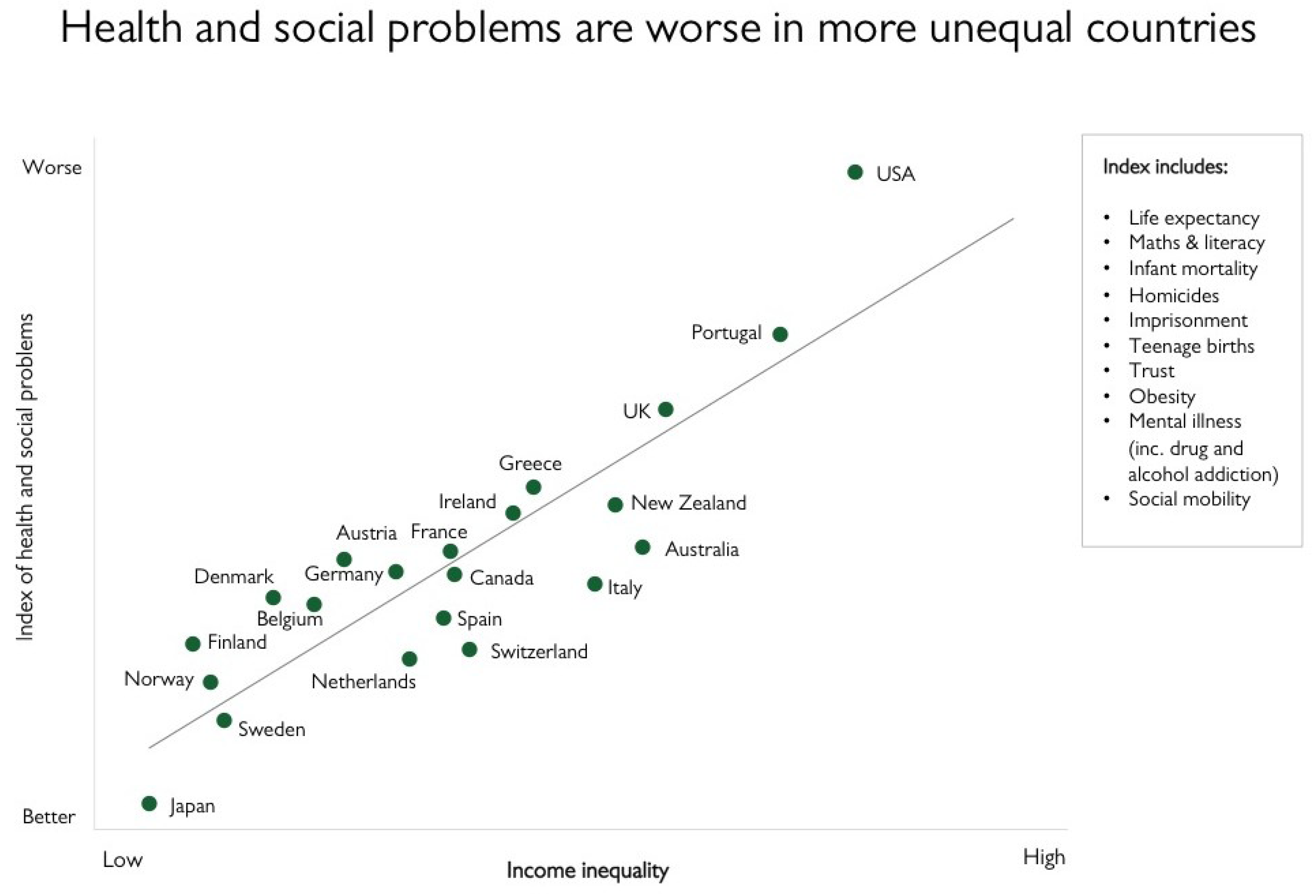

- Wilkinson, R.; Pickett, K. The Spirit Level: Why More Equal Societies Almost Always Do Better; Allan Lane/Penguin Press: London, UK, 2009. [Google Scholar]

- Barnes, P. Capitalism 3.0. A Guide to Reclaiming the Commons; Berrett-Koehler Publishers: San Francisco, CA, USA, 2006. [Google Scholar]

- Vermont Senate Bill 44. Vermont Common Assets Trust. Available online: www.leg.state.vt.us/DOCS/2008/BILLS/INTRO/S-044.DOC (accessed on 13 June 2013).

- Boulding, K.E. The Economics of the Coming Spaceship Earth. In Environmental Quality in a Growing Economy; Jarrett, H., Ed.; Resources for the Future/Johns Hopkins University Press: Baltimore, MD, USA, 1966; pp. 3–14. [Google Scholar]

- Moench, E.; Vickery, J.; Aragon, D. Why is the Market share of adjustablerate mortgages so low? Available online: http://www.newyorkfed.org/research/current_issues/ci16-8.html (accessed on 13 June 2013).

- Federal Reserve Economic Data, Excess Reserves of Depository Institutions (EXCRESNS). Federal Reserve Bank of St. Louis: St. Louis, MO, USA, 2013. Available online: http://research.stlouisfed.org/fred2/series/EXCRESNS (accessed on 13 June 2013).

- Friedman, M. Capitalism and Freedom; University of Chicago Press: Chicago, IL, 1982; p. ix. [Google Scholar]

© 2013 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/3.0/).

Share and Cite

Farley, J.; Burke, M.; Flomenhoft, G.; Kelly, B.; Murray, D.F.; Posner, S.; Putnam, M.; Scanlan, A.; Witham, A. Monetary and Fiscal Policies for a Finite Planet. Sustainability 2013, 5, 2802-2826. https://doi.org/10.3390/su5062802

Farley J, Burke M, Flomenhoft G, Kelly B, Murray DF, Posner S, Putnam M, Scanlan A, Witham A. Monetary and Fiscal Policies for a Finite Planet. Sustainability. 2013; 5(6):2802-2826. https://doi.org/10.3390/su5062802

Chicago/Turabian StyleFarley, Joshua, Matthew Burke, Gary Flomenhoft, Brian Kelly, D. Forrest Murray, Stephen Posner, Matthew Putnam, Adam Scanlan, and Aaron Witham. 2013. "Monetary and Fiscal Policies for a Finite Planet" Sustainability 5, no. 6: 2802-2826. https://doi.org/10.3390/su5062802

APA StyleFarley, J., Burke, M., Flomenhoft, G., Kelly, B., Murray, D. F., Posner, S., Putnam, M., Scanlan, A., & Witham, A. (2013). Monetary and Fiscal Policies for a Finite Planet. Sustainability, 5(6), 2802-2826. https://doi.org/10.3390/su5062802