2050 Scenarios for Long-Haul Tourism in the Evolving Global Climate Change Regime

Abstract

:1. Introduction

2. The Scenario-Building Approach

2.1. Methodological Underpinnings

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

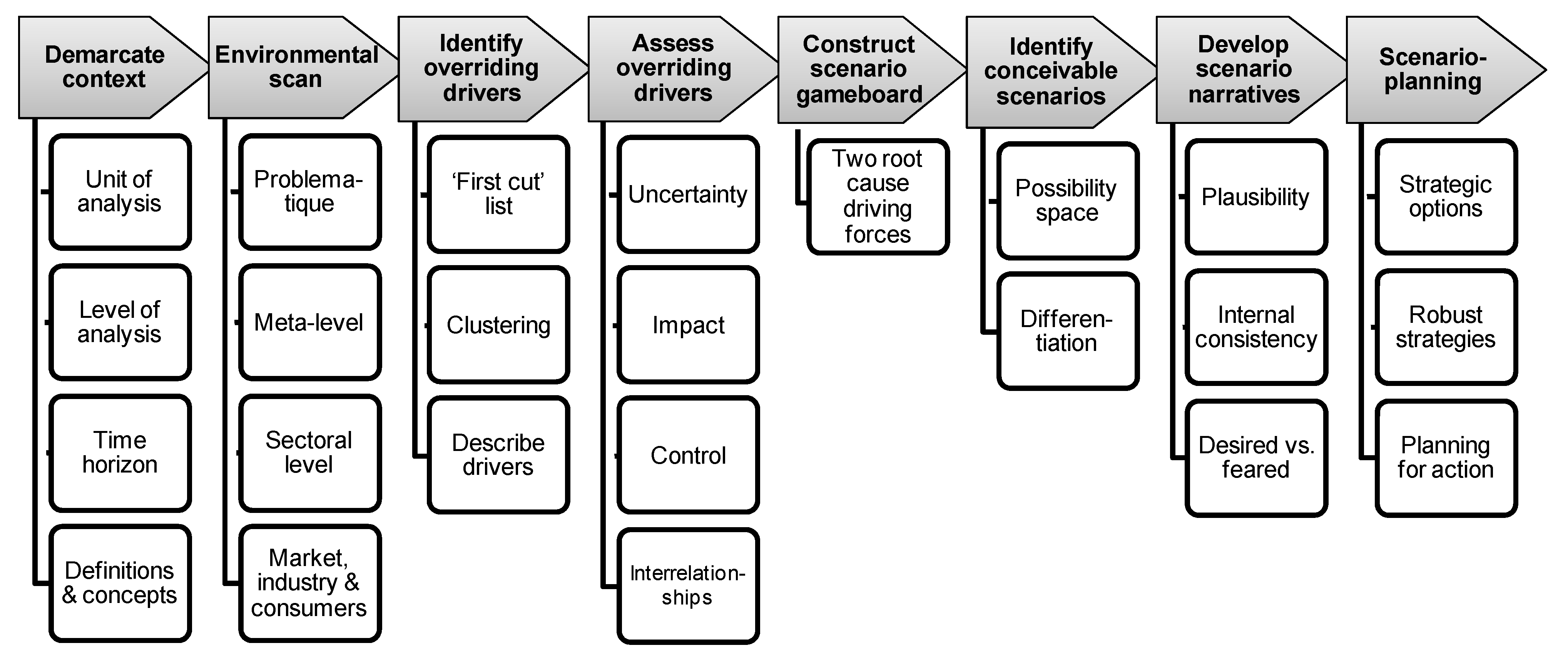

| Steps | Description |

|---|---|

| 1 | Demarcate the context of the scenario exercise, including the unit of analysis, level of analysis, time horizon and key concepts. |

| 2 | Describe the problematique, and brainstorm critical aspects or external drivers of change at the meta-level and in the contextual and transactional environments that could affect the prospects for LHT over the next four decades. These may include “predetermined” trends or phenomena [24] “already in the pipeline of the future” [28], but the focus is on “uncontrollable” uncertainties in the contextual environment, with “high potential impacts”. |

| 3 | Based on the environmental analysis, cluster the first-cut list of drivers and/or uncertainties, towards identifying a limited number of overriding driving forces “that set the pattern of events and determine outcomes” [27]. |

| 4 | Assess the overriding drivers in terms of their degree of uncertainty, potential impact and controllability, using a two-dimensional ranking space technique as well as an interrelationship diagram. |

| 5 | On this basis, identify and describe the two “root cause” driving forces, and construct a two-dimensional matrix-type scenario gameboard [7], which will form the basis of the scenario logics. |

| 6 | Identify the conceivable scenarios in the possibility space, and do a first-cut assessment of their plausibility and differentiation. Within this “possibility space” [29], now eliminate “combinations that are not credible”, while maintaining “a reasonable range of uncertainty” [26]. |

| 7 | Develop the scenario narratives or “rehearsals of the future” [24] by fleshing out the scenario logics. In the process, continuously assess the plausibility, internal consistency and relevance of each narrative, refining the storylines as required. To enhance decision-making utility, identify signposts (also referred to as “lead indicators” or “turning points”) for the alternative scenarios [19], and explicitly state any assumptions that underpin the scenario narratives. The narrative should also include indications of strategic imperatives, be they opportunities or risks, from the perspective of the unit of analysis. To challenge the limits of the mental models that underpin these narratives, identify any “wild cards” that may quite significantly disrupt a given scenario [28,30]. |

| 8 | Finally, in moving from scenario-building to integrated scenario-planning, or from “visualisation to realisation” [18], articulate the most desired future and ways of achieving this future, both at a strategic level and by identifying critical actions that could assist to realise it. Use Ringland’s [20] scenario options and scenario-positioning matrices to translate scenarios into a broad strategic orientation, positioning and planning framework for action. |

2.2. The Process

3. Demarcation of the Context (Step 1 in Figure 2)

3.1. The Unit of Analysis and Focus

3.2. The Level of Analysis

3.3. The Time Horizon

3.4. Definitions and Concepts

4. Environmental Scan (Step 2 in Figure 3)

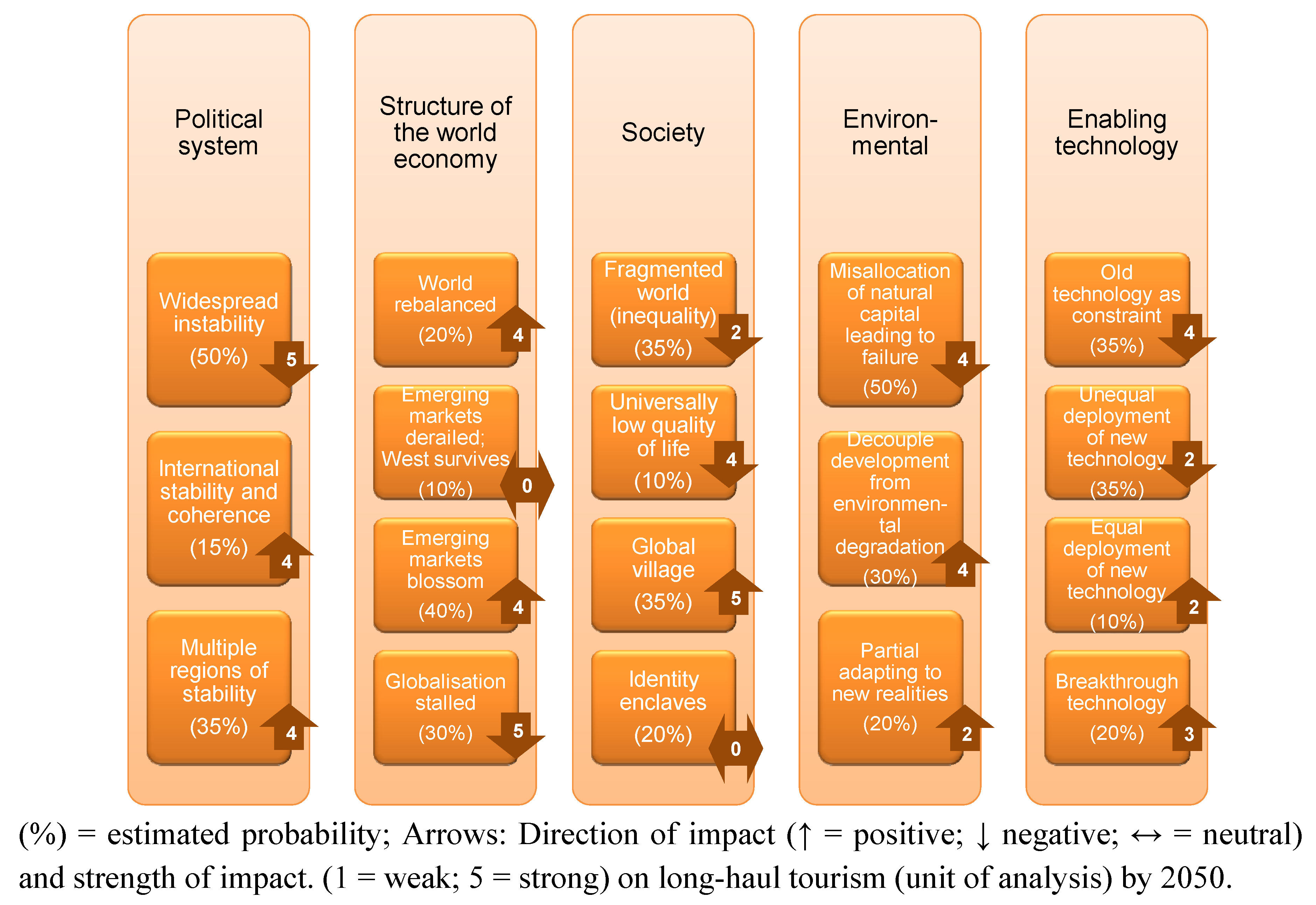

4.1. The Meta-level Contextual Environment

4.2. The Contextual and Transactional Environments (Sectoral Level)

4.2.1. The Contextual Environment

Political and Legal Influences

Economic and Demographic Influences

Social Influences

Technological Influences

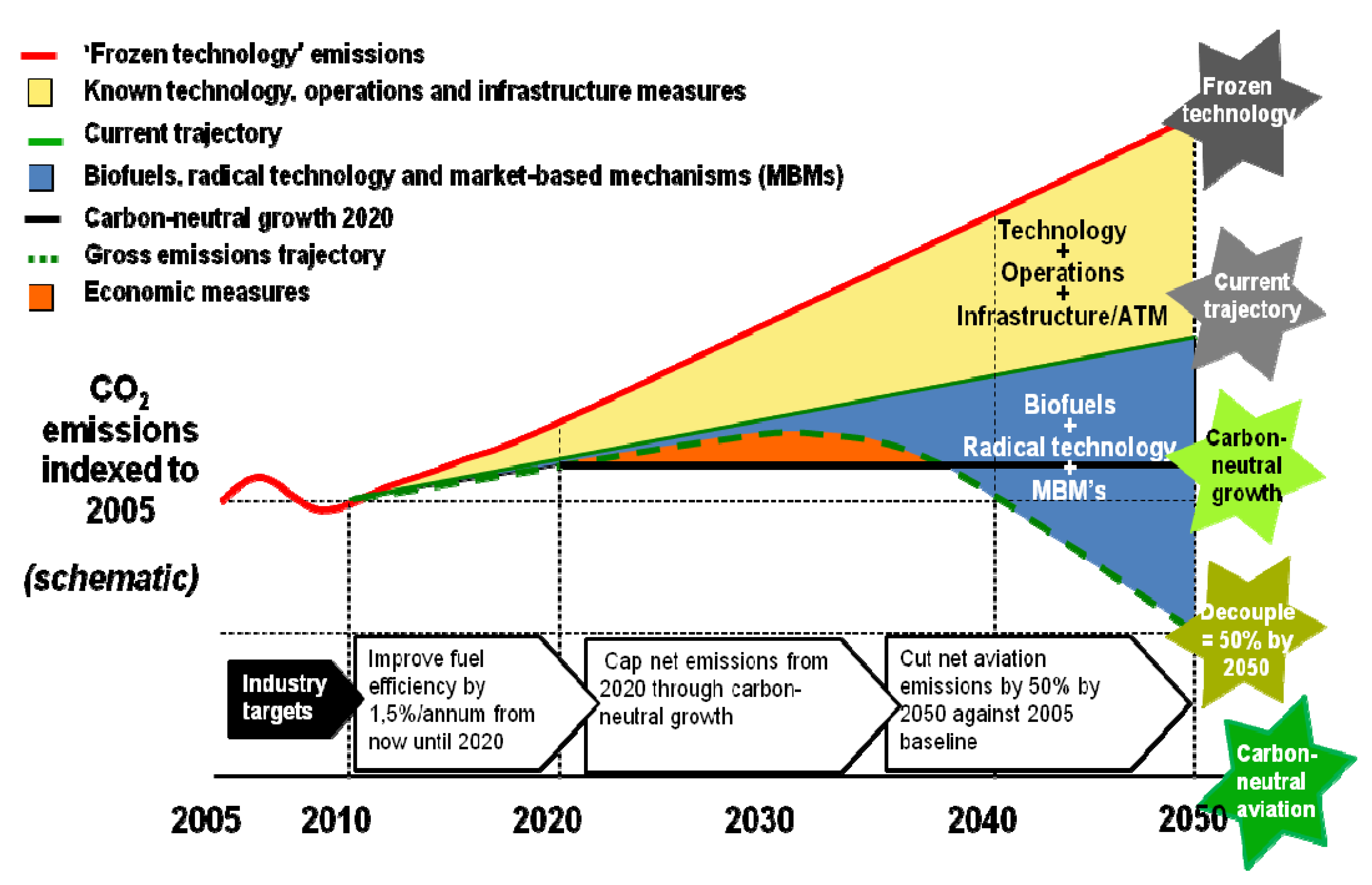

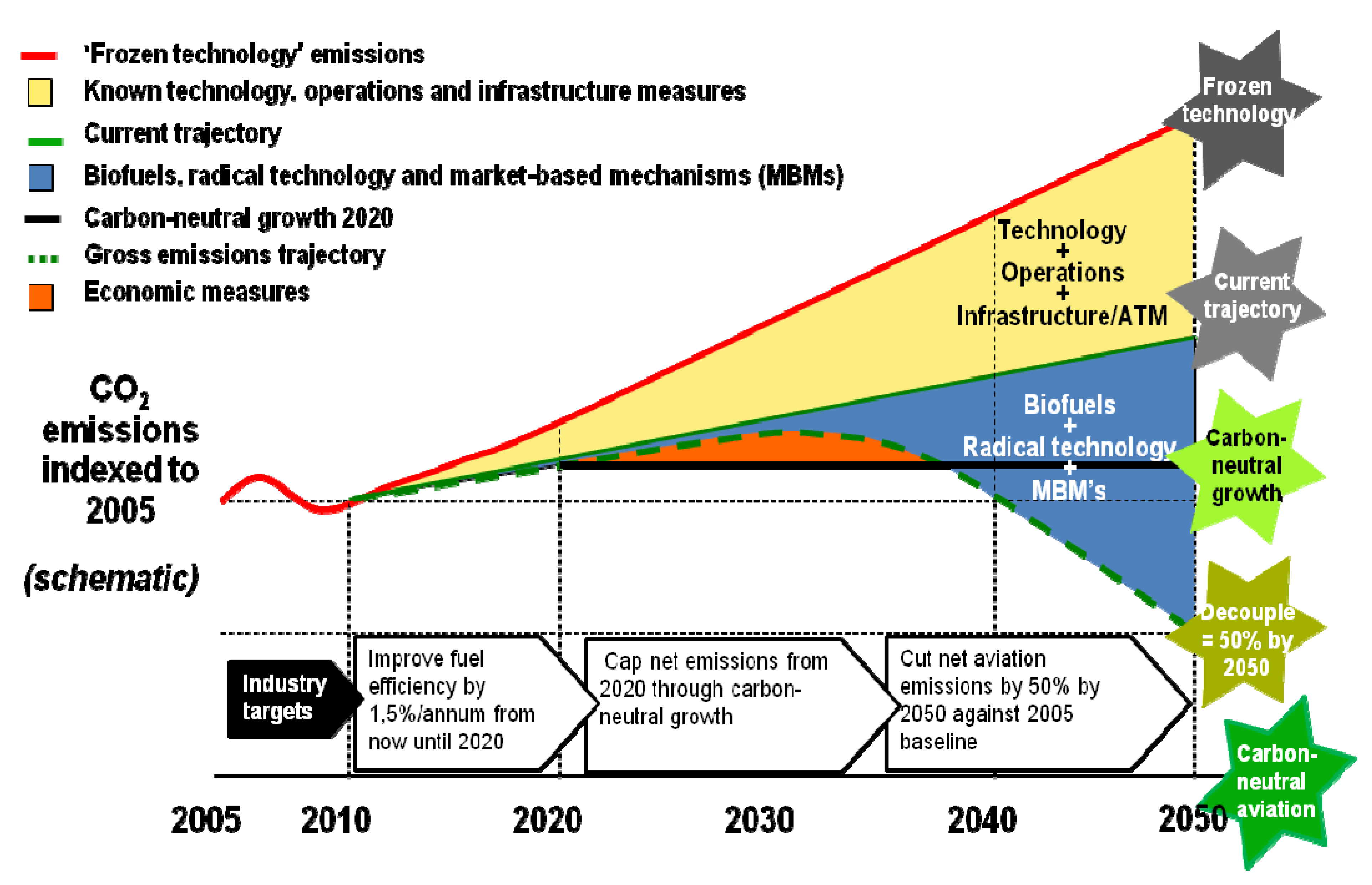

- Technological improvements: These interventions include (i) short-term improvements that enhance existing and new fleet efficiencies (for example retrofitting and production updates); (ii) medium-term innovations (for example new aircraft and engine design efficiencies in the pipeline), and (iii) long-term step changes (for example blended-wing design, the deployment of super-lightweight materials that emerge from the nanotechnology revolution, radical new technologies and airframe designs, and the drop-in of low-carbon aviation biofuels).

- Operational improvements: These interventions are by and large aimed at fuel savings, and include the spread of best practices for fuel conservation, greater use of fixed electrical ground power at airport terminals, centre-of-gravity optimisation, improved take-off and landing procedures (for example single-engine taxiing and the continuous-descent approach), and higher load factors (inter alia achieved through yield management).

- Infrastructural improvements: These interventions are aimed at removing inefficiencies in the utilisation of airports and airspace, including the transition to more flexible airspace use, reorganising the airspace, shortening flight routes, and improving airport and air traffic management infrastructure and technology.

- Economic measures: In IATA’s lexicon, these are positive economic measures as part of a global, sectoral, market-based approach, and could include direct offsetting/emissions trading. However, in reality, these could also include punitive economic measures, such as carbon or bunker fuel taxes and passenger or “per plane” carbon levies.

Environmental Influences

Resource Depletion

4.2.2. Market, Industry and Consumer Trends in the Transactional Environment

Market Overview

Industry Overview

- equally affected by archaic global legal frameworks that govern the airspace and ownership of airlines, and that limit competition in the skies as well as capital mobility [73];

- equally vulnerable to terrorist attacks in tourist destinations, cyber-terrorism (for example the threat of sabotage of air traffic navigation systems), geo-political tensions in key hot spots, pandemics such as the H1N1 influenza, natural disasters (for example the 2010 Icelandic volcanic eruption), and extreme weather conditions; and

- equally exposed to global exchange rate volatility, rising oil prices, new security concerns, non-tariff trade barriers (for example visa requirements, discriminatory travel taxes and travel advisories) and external economic shocks.

The Consumer Landscape

4.3. Summary of the Problematique

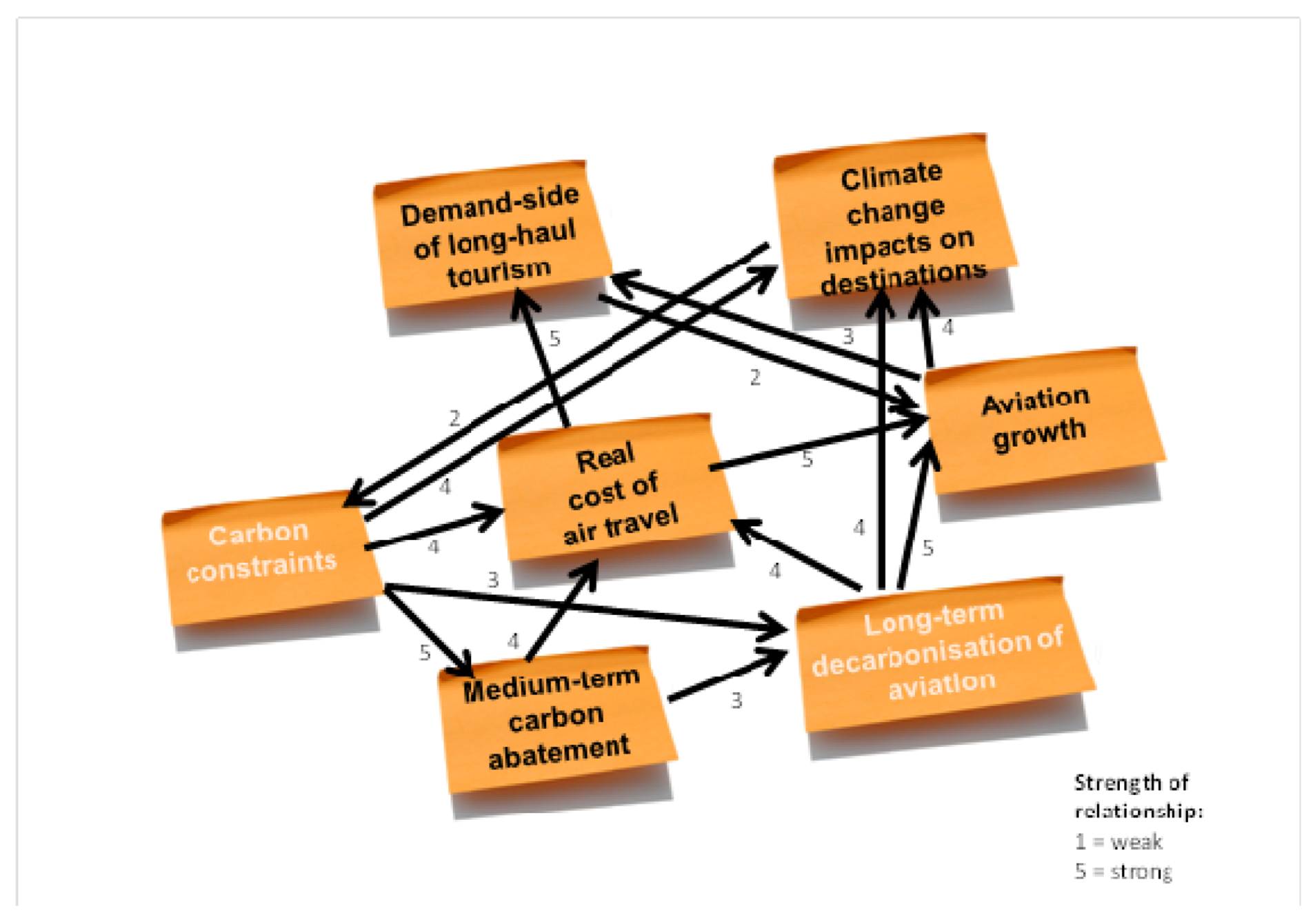

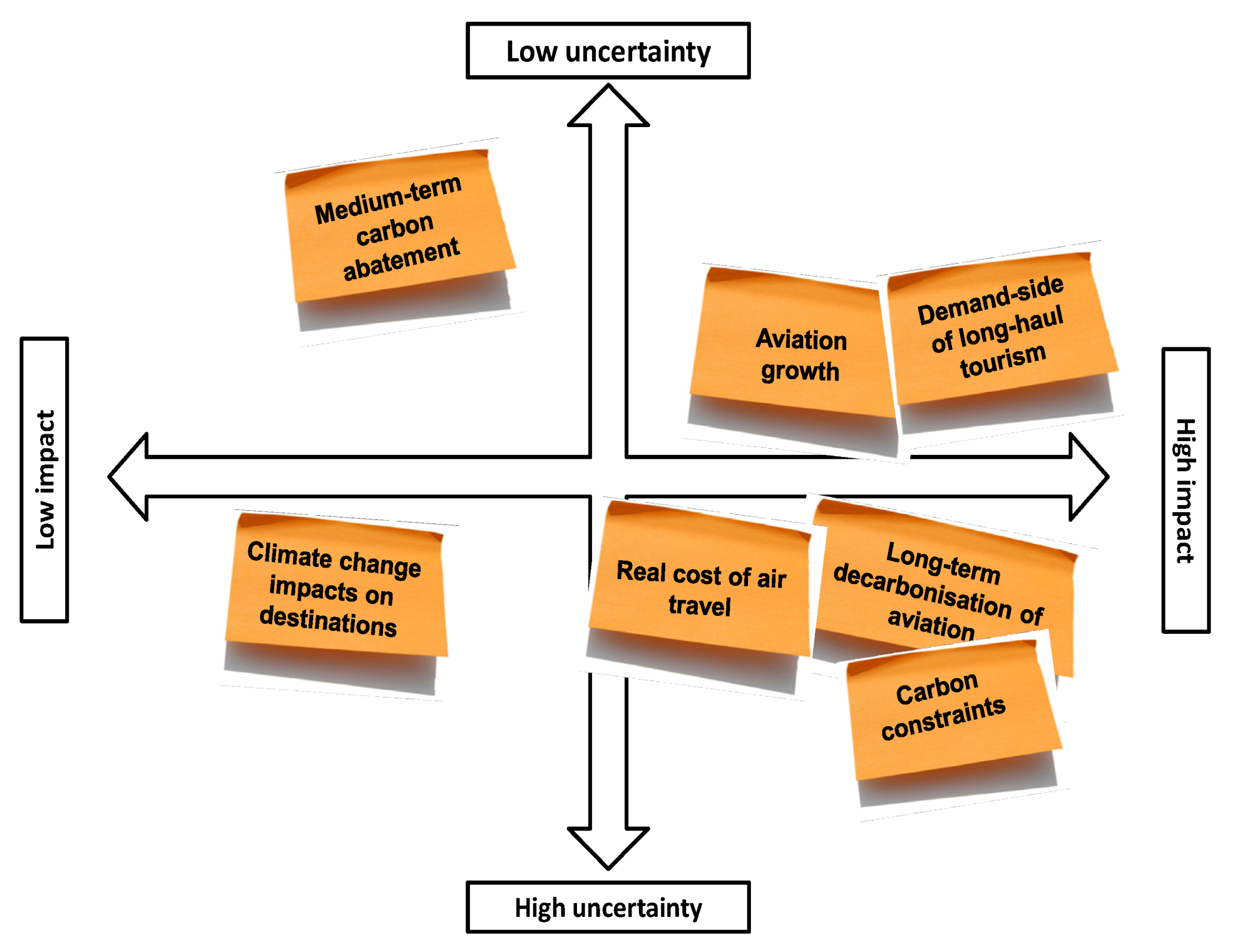

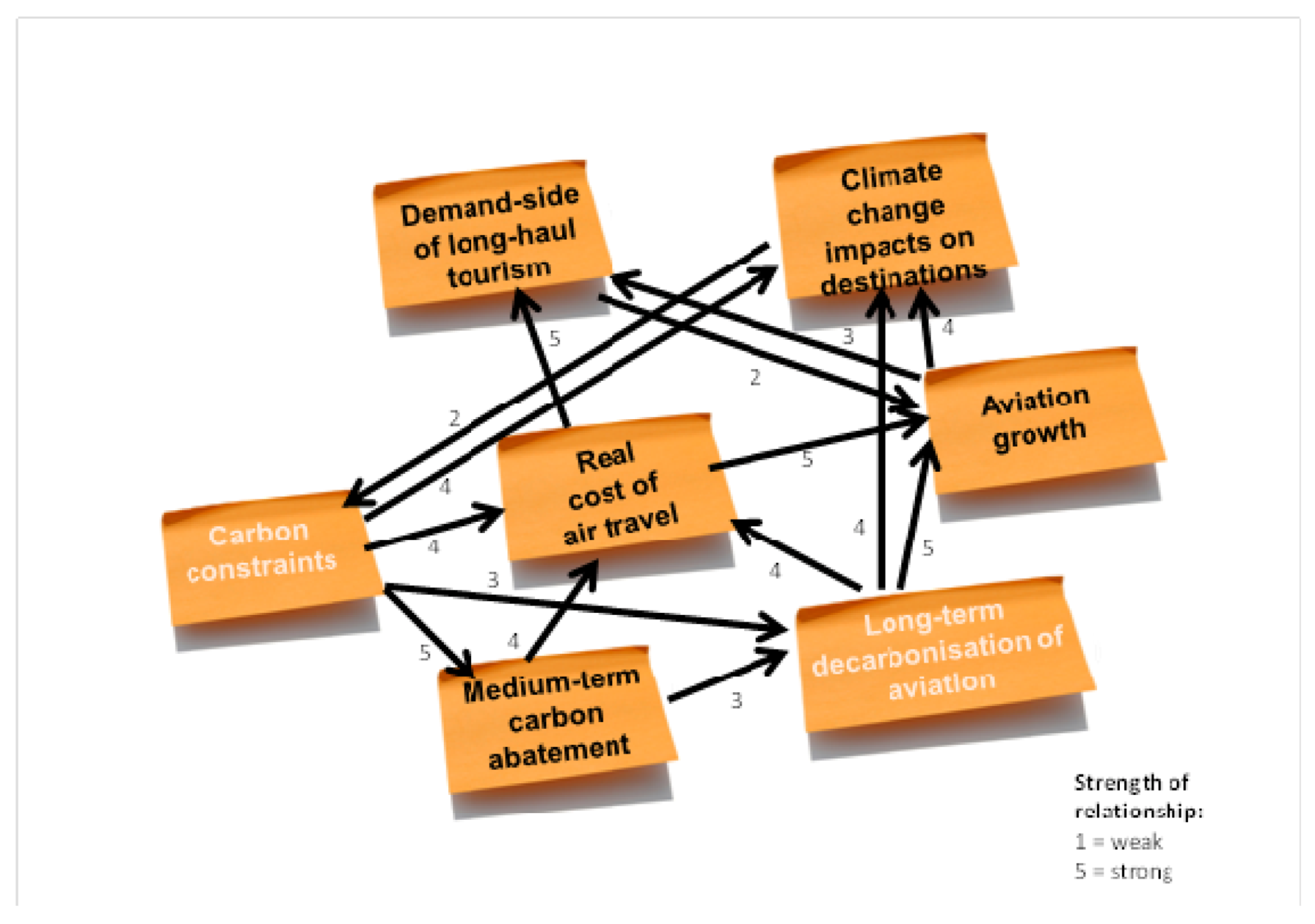

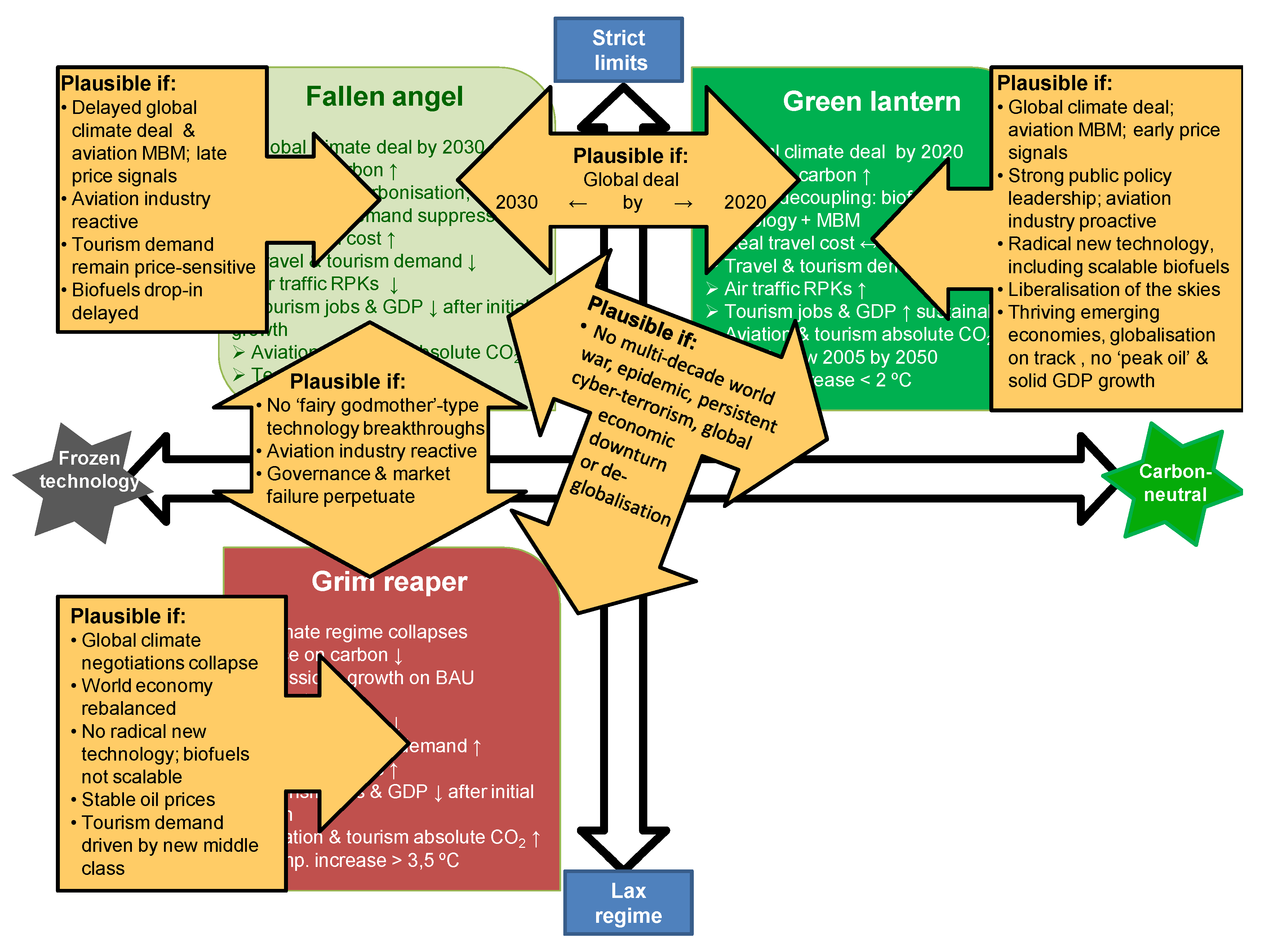

5. The Key Uncertainties, Overriding Drivers of Change and the Scenario Gameboard (Steps 3 to 5 in Figure 7)

| Overriding driver | Description |

|---|---|

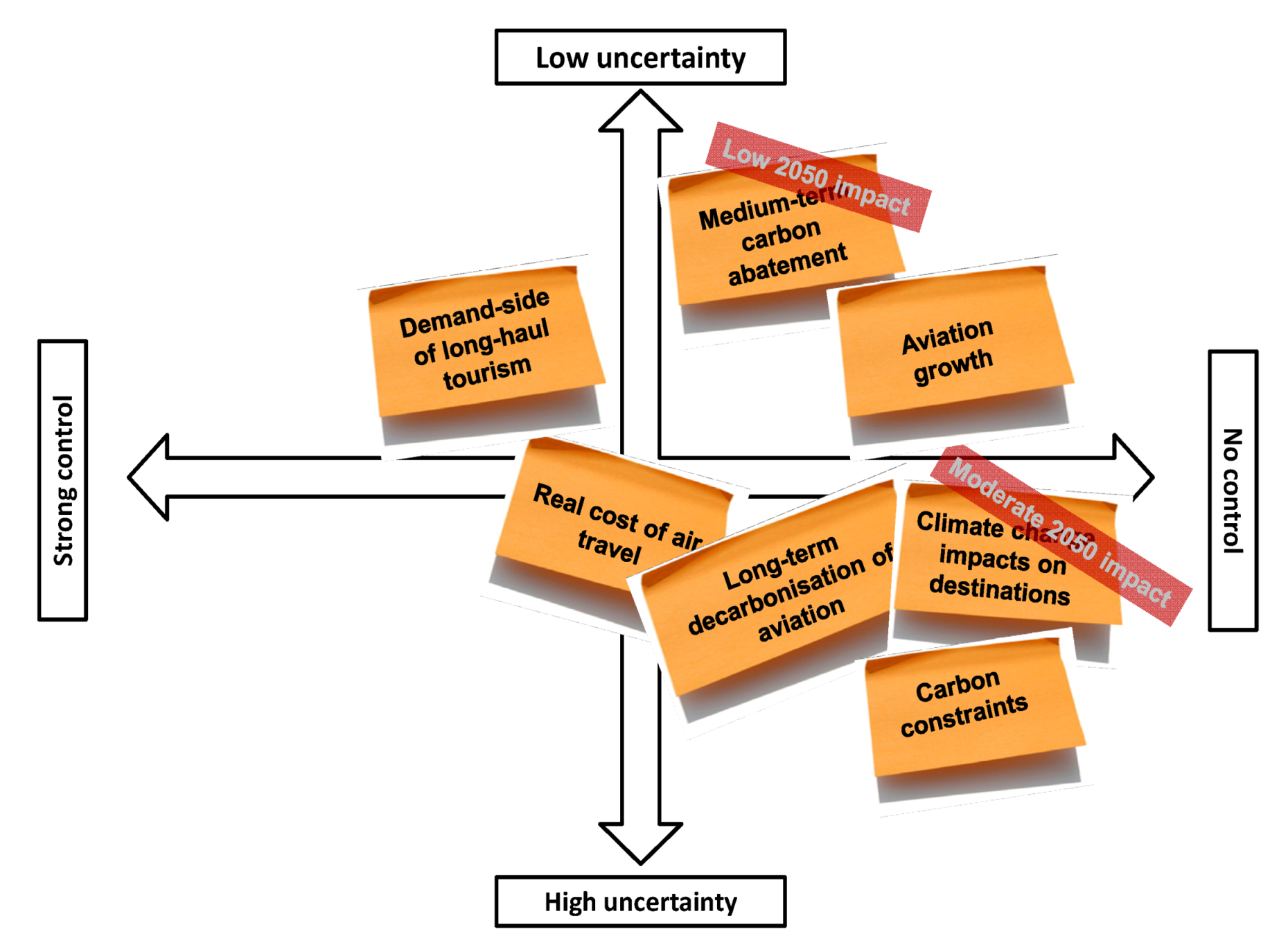

| 1 Climate change impacts on tourism destinations | Because tourism and aviation represent only five per cent of global emissions, and meeting “required by science” (RBS) mitigation targets for 2050 thus depends on many other economic sectors, this driving force is in the high-uncertainty, low-control quadrant. However, should the average global temperature increase move into dangerous territory by triggering critical ecosystem tipping points, the potential impacts on the tourism economy will likely enter the “high-impact” zone during the second half of the century, but not within the 2050 time horizon. |

| 2 Carbon constraints | This is by-and-large a political driver. A key uncertainty is whether multilateral negotiations will introduce carbon constraints. As will become evident in the scenario analysis, the timing of a political decision on carbon limits/carbon pricing could be a game changer in terms of decarbonisation—regardless of whether this involves a price instrument like carbon taxes or a quantity instrument like emissions trading (e.g. cap-and-trade, baseline-and-credit or offsetting). |

| 3 Medium-term carbon abatement levers (pre-2030) | These levers of change have low uncertainty, because many are already in the pipeline. These interventions may actually lead to further declines in the real cost of air travel. Even so, the impact on LHT would only be moderate to low, given that LHT growth also depends on a range of other variables. The tourism sector may be able to exert moderate influence towards implementing some of these measures—overall, though, control is low. |

| 4 Long-term decarbonisation (post-2030) | This is primarily a technological and behavioural driver. Decarbonisation through radically new (unknown) technologies, the drop-in of sustainable biofuels as jet fuel and/or the offsetting of unavoidable emissions through an MBM falls outside the tourism sector’s direct sphere of influence, and is highly uncertain for a number of reasons, including the political uncertainty about the nature and time frames for the introduction of carbon constraints (e.g. MBMs that act as price incentives), and the question marks over the scalability and costs of biofuels. The alternative to industry meeting RBS mitigation targets through technology deployment would be for governments to introduce physical constraints on the expansion of airport infrastructure, induce behavioural change among consumers, invest in infrastructure for passenger modal shifts, and incentivise information communication technology (ICT) alternatives to business travel. All these interventions fall within the high-uncertainty and no-control quadrants, and could impact on LHT through intermediary variables, such as aviation growth and the real cost of air travel. |

| 5 Real cost of air travel | Uncertainties relate to carbon pricing, other taxes and levies, oil prices and peak oil, scale economies and load factors, fuel-efficiency improvements (driven mainly by the medium-term carbon abatement levers outlined above) and the liberalisation (versus tighter regulation) of the airspace to allow for greater competition and growth of new business model, low-cost airlines. In terms of LHT demand as well as aviation growth, this is a high-impact, moderate-control driving force that also stands in direct relation to carbon constraints (read: carbon pricing) and the marginal cost of medium-term and long-term carbon abatement. |

| 6 Aviation growth | Aviation growth, or slowdown, will have a direct impact on LHT. By and large, because of institutional and regulatory silos that fragment the aviation-tourism value chain, aviation growth is a driving force outside the tourism sector’s sphere of direct influence. Aviation growth is exposed to a range of factors with various degrees of uncertainty attached to them, particularly the real cost of air travel (including oil prices), globalisation and the counter-trend of fragmentation, which could in turn have a negative impact on trade flows and business travel, the state and balance of forces in the global economy (e.g. emerging-market growth versus stagnation, the timing of global peak middle class, world trade and GDP), future consumer preferences (e.g. green consumerism), investment in airlift infrastructure versus mass-transit systems, and airline and airspace liberalisation. On balance, this driving force falls in the moderate-uncertainty zone. |

| 7 Demand side of long-haul tourism | Demand is highly correlated with aviation growth and trade volumes, and will have a definite impact on LHT. Although a range of driving forces within the organisational environment come into play, and are thus within the control of the tourism sector, tourism demand strongly depends on external variables very similar to those that drive aviation growth and the real cost of travel. This is thus a driving force of moderate uncertainty. |

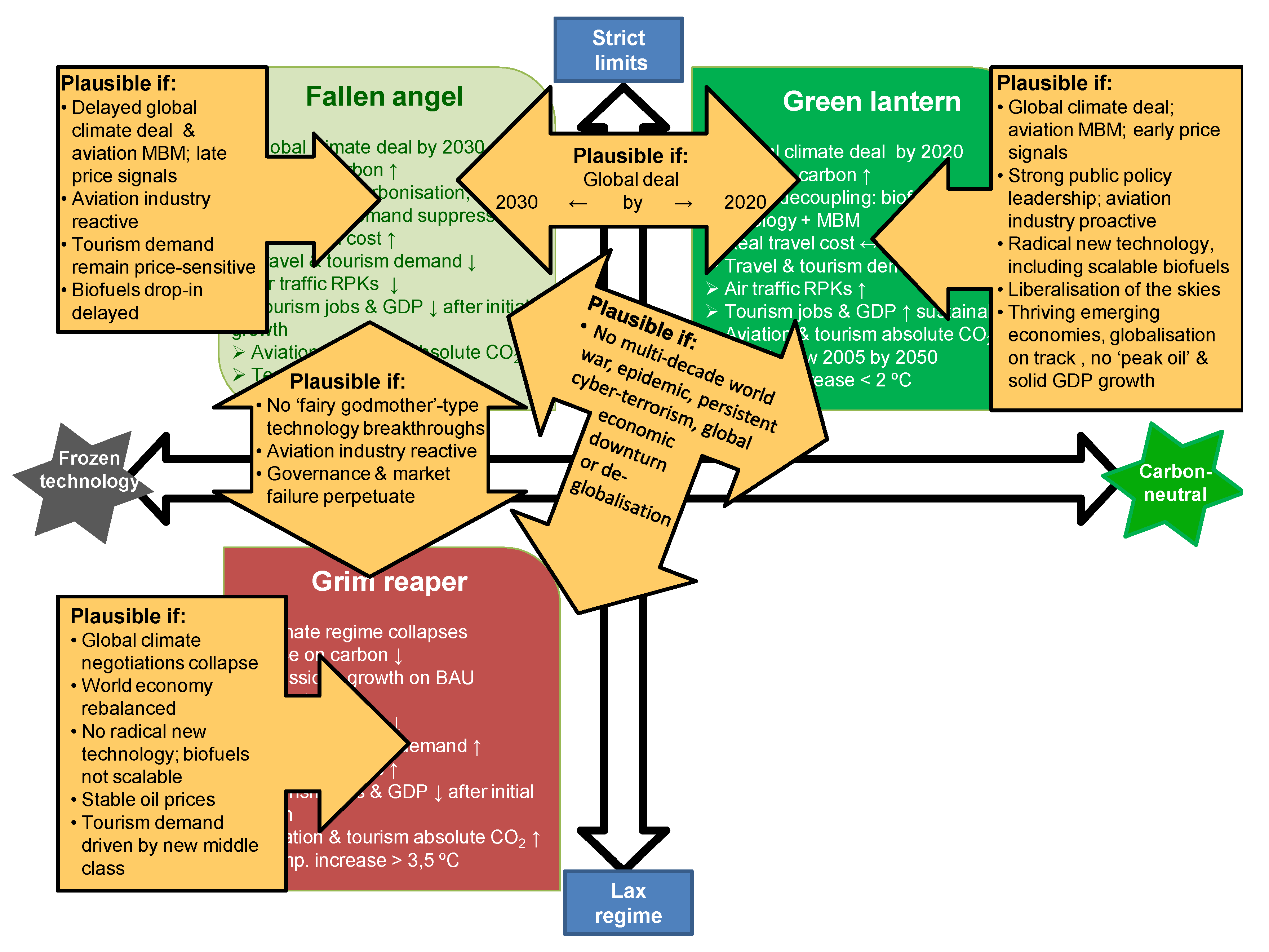

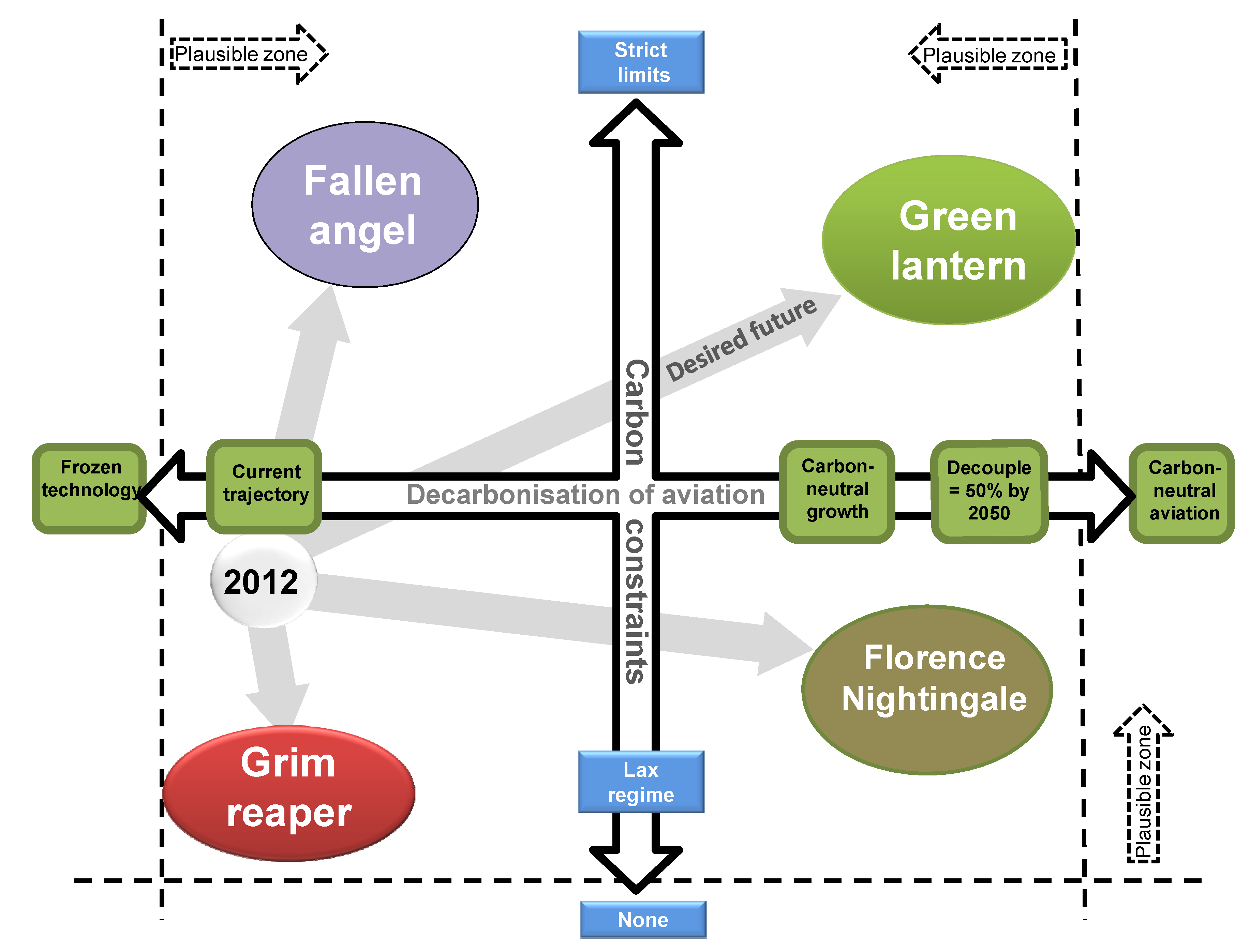

Vertical Axis: Carbon Constraints [Political Driver]

Horizontal Axis: Long-Term Decarbonisation of Dviation [Technological and Behavioural Driver]

6. 2050 Scenarios for Long-haul Tourism (Steps 6 and 7 in Figure 12)

6.1. Introduction

The Story of the Status Quo: Where Are We in 2012?

6.2. 2050 Futures: The Scenario Storylines

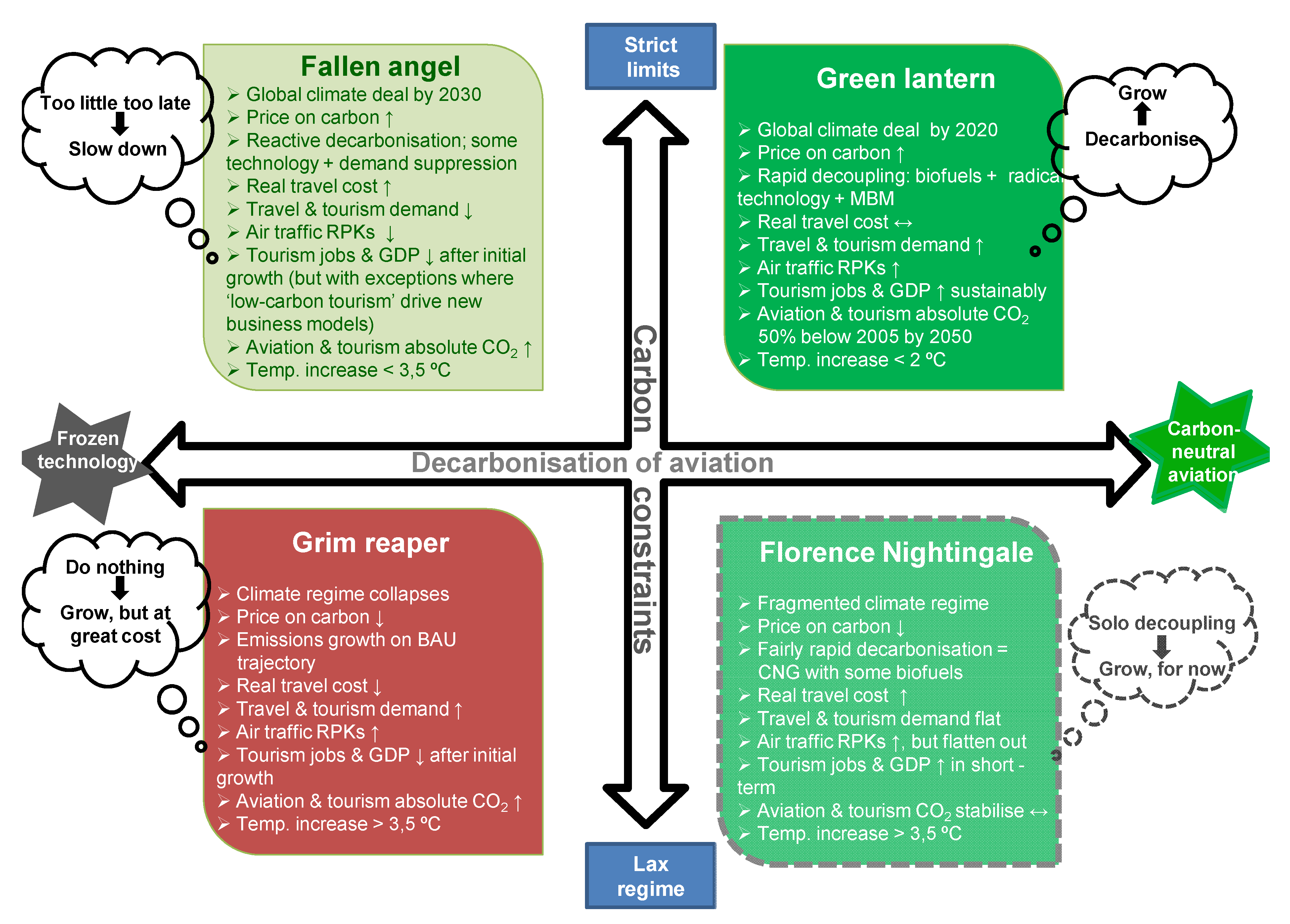

6.2.1. The “Green Lantern” Scenario

The Green Lantern: Where Are We in 2050?

How Did We Get Here?

2012 to 2020

2020 to 2030

2030 to 2050

What have been the Turning Points and Signposts over the last Four Decades? What is Assumed in this Scenario? And which “Wild Cards” could have Disrupted this Storyline?

What were the Implications for LHT Destinations? Any Risks and Opportunities? And, at a Strategic Level, how did Tourist Destinations Respond?

6.2.2. The “Fallen Angel” Scenario

The Fallen Angel: Where Are We in 2050?

How Did We Get Here?

2012 to 2030

2030 to 2050

What have Been the Turning Points and Signposts Over the Last Four Decades? What is Assumed in this Scenario? And which “Wild Cards” could have Disrupted this Storyline?

What were the Implications for LHT Destinations? Any Risks and Opportunities? And, at a Strategic Level, how did Tourist Destinations Respond?

6.2.3. The “Grim Reaper” Scenario

The Grim Reaper: Where Are We in 2050?

How Did We Get Here?

2012 to 2030

2030 to 2050

What Have Been the Turning Points and Signposts Over the Last Four Decades? What is Assumed in this Scenario? And which “Wild Cards” could have Disrupted this Storyline?

What Were the Implications for LHT Destinations? Any Risks and Opportunities? And, at a Strategic Level, How did Tourist Destinations Respond?

6.2.4. The “Florence Nightingale” Scenario

Florence Nightingale: Where Are We In 2050?

A Reality Check: Is this Scenario Plausible?

6.3. Summary of Strategic Choices

7. Strategic Choices: From Visualisation to Realisation (Step 8 in Figure 15)

7.1. Introduction

| Strategic thrust | Actions | Green Lantern | Fallen Angel | Grim Reaper |

|---|---|---|---|---|

| Future-robust core of strategy (All three scenarios) | ||||

| Adapt to climate change | Readiness: Develop tourism vulnerability assessment tools to understand and mitigate climate change risks* | ++ | ++ | ++ |

| Resilience: Adapt to unavoidable climate change and develop capacity to absorb climate impacts* | + | ++ | ++ | |

| Resistance: Develop climate resistant physical infrastructure** | + | ++ | ++ | |

| Hedge against uncertainty and risk | Demand-side: Follow portfolio approach to market segmentation (balanced portfolio of long-haul, regional and local tourism source markets, as well as business and leisure markets)* | ++ | + | O |

| Supply-side: Diversify tourism offerings beyond nature-based and climate exposed sectors* | + | ++ | ++ | |

| Decarbonise underlying activities | Government regulation and incentives for low-carbon transformation of tourism supply chain (e.g. land transport, accommodation); promote green consumerism through awareness campaigns* | ++ | ++ | - - |

| Low-carbon transformation of aviation supply chain (operational, infrastructural and technological efficiency improvements, as well as carbon off-setting/price incentives)** | ++ | + + | - | |

| New investment in regional, land-based mass-transit systems (e.g. high-speed rail connectivity)** | ++ | ++ | O | |

| Partly robust strategy (Fallen Angel & Green Lantern) | ||||

| Seize opportunities | Seize opportunities presented by low-carbon forms of tourism and green consumer sentiment (passenger modal shifts over short- to medium-haul, localised tourism, carbon-neutral accommodation and car rental, “green” branding/marketing)* | ++ | ++ | - |

| Focused contingent strategies (Fallen Angel) | ||||

| Decouple tourism from air transport | Switch to lower-volume, higher-value source markets* | - | ++ | - - |

| Develop land arrivals and local tourism as mainstays of sustainability* | O | + + | - - | |

| Focused contingent strategies (Grim Reaper and Fallen Angel) | ||||

| Decouple tourism from nature | Supply-side: Substitute nature-based tourist activities with new offerings* | - | + | ++ |

| Economic diversification | Diversify economy away from reliance on tourism receipts for GDP and jobs** | - - | + | ++ |

| Planning-oriented strategies | Reactive / preventative strategies | Proactive strategies | |||

|---|---|---|---|---|---|

| React to recognisable trends | Manage future risks | Stay flexible and hedge | Exploit future opportunities | Develop and reach own visions | |

| Focused contingency planning (based on reference scenario) | Decouple tourism from nature (Grim Reaper) Diversify economy away from tourism (Grim Reaper) | Predominantly land arrivals and local tourism (Fallen Angel) Lower-volume, higher value source markets (Fallen Angel) | |||

| Robust planning (based on several scenarios; at least desired “green lantern” scenario) | Deploy tourism vulnerability assessment tools Adapt to unavoidable climate change impacts | Build resilience capacity to deal with climate impacts Climate resilient infrastructure | Portfolio approach to market segmentation Diversify tourism offerings beyond nature-based and climate exposed sectors | Seize opportunities of low-carbon forms of tourism and green consumer sentiment | Create low-carbon competitive advantages by transforming tourism supply chain and consumer behaviour Accelerate decarbonisation of air transport Invest in regional, land-based mass-transit systems |

7.2. Adaptation

7.3. Market Development

7.4. Internal Decarbonisation

7.5. Low-Carbon Air Transport

7.6. Contingency Plans

8. Conclusion

Conflict of Interest

References

- Stern, N. The Economics of Climate Change: The Stern Review; Cambridge University Press: Cambridge, UK, 2006. [Google Scholar]

- United Nations Framework Convention on Climate Change (UNFCCC). Decision2/CP.15: Copenhagen Accord; COP Report, FCCC/CP/2009/11/Add.1; United Nations: Bonn, Germany, 2009. Available online: http://unfccc.int/documentation/documents/advanced_search/items/3594.php?rec=j&priref=600005735#beg (accessed on 7 April 2010).

- Intergovernmental Panel on Climate Change (IPCC), Climate Change 2007:Mitigation of Climate Change. Summary for Policy Makers; Contribution of Working Group III to the Fourth Assessment Report of the Intergovernmental Panel on Climate Change; Intergovernmental Panel on Climate Change: Geneva, Switzerland, 2007.

- Organization for Economic Cooperation and Development (OECD), Climate Change and Tourism Policy in OECD Countries; CFE/TOU(2010)10/FINAL; OECD: Paris, France, 2011.

- International Civil Aviation Organization (ICAO), ICAO Environmental Report 2010: Aviation and Climate Change; ICAO & FCM Communications Inc.: Montréal, Canada, 2010.

- Hichert, T. Business’ Contextual Environment, Presentation, University of Stellenbosch Business School, Bellville, South Africa, 2011.

- Ilbury, C.; Sunter, C. Scenario Gameboards. Available online: http://www.mindofafox.com/gameboard.php (accessed on 17 December 2012).

- Dubois, G.; Peeters, P.; Ceron, J.P.; Gössling, S. The future tourism mobility of the world population: Emission growth versus climate policy. Transport. Res. Pol. Pract. A 2011, 45, 1031–1042. [Google Scholar] [CrossRef]

- Yeoman, I. Our Sustainable Future—Looking Back from 2050. In Green Growth and Travelism—Letters from Leaders; Lipman, G., DeLacy, T., Vorster, S., Hawkins, R., Jiang, M., Eds.; Goodfellows: London, UK, 2012. [Google Scholar]

- Talwar, R. Forecasting the Future of Travel and Tourism: Scanning the Horizon. In Trends and Issues in Global Tourism 2010; Conrady, R., Buck, M., Eds.; Springer: Heidelberg, Germany, 2010. [Google Scholar]

- Feige, I. Forecasting the Future of Travel and Tourism: The Future of Mobility—Scenarios for the Year 2025. In Trends and Issues in Global Tourism 2010; Conrady, R., Buck, M., Eds.; Springer: Heidelberg, Germany, 2010. [Google Scholar]

- Davies, F.; Moutinho, L.; Hutcheson, G. Constructing a knowledge-based system to aid scenario-based strategic planning: An application to the European airline industry. Intell.Syst. Account Finance Manag. 2005, 13, 61–79. [Google Scholar] [CrossRef]

- Varum, C.A.; Melo, C.; Alvarenga, A.; de Carvalho, P.S. Scenarios and possible futures for hospitality and tourism. Foresight 2011, 13, 19–35. [Google Scholar] [CrossRef]

- Hay, B.; Yeoman, I. Turning scenarios into a strategy map: Our ambition for Scottish tourism. JVM 2005, 11, 89–102. [Google Scholar]

- Yeoman, I.; McMahon-Beattie, U. Developing a scenario planning process using a blank piece of paper. Tourism Hospit.Res. 2005, 5, 273–285. [Google Scholar] [CrossRef]

- Yong, Y.W.; Keng, K.A.; Leng, T.L. A Delphi forecast for the Singapore tourism industry: Future scenario and marketing implications. Eur. J. Market 1989, 23, 15–26. [Google Scholar]

- Fahey, L.; Randall, R.M. Learning from the Future: Competitive Foresight Scenarios; John Wiley: New York, NY, USA, 1998; p. 157. [Google Scholar]

- Walton, J.S. Scanning beyond the horizon: Exploring the ontological and epistemological basis for scenario planning. Adv. Develop. Hum. Resour. 2008, 10, 147–165. [Google Scholar]

- Mietzner, D.; Reger, G. Advantages and disadvantages of scenario approaches for strategic foresight. Int. J. Tech. Intell. Plann. 2005, 1, 220–239. [Google Scholar] [CrossRef]

- Ringland, G. Scenarios in Business; Wiley: Chichester, UK, 2002; pp. 167–174. [Google Scholar]

- Wilson, I. Mental Maps of the Future. In Scenario Building: A Suitable Method For Strategic Property Planning, The Cutting Edge 1999; Ratcliff, J., Ed.; St. John’s College, Cambridge, United Kingdom: 5–7 September 1999, The Property Research Conference of the RICS.

- National Department of Tourism (NDT), Shaping the Future of Tourism: 2030 Tourism Scenarios; NDT: Pretoria, South Africa, 2012.

- Bishop, P.; Hines, A.; Collins, T. The current state of scenario development: An overview of techniques. Foresight 2007, 9, 5–25. [Google Scholar] [CrossRef]

- Schwartz, P. The Art of the Long View: Planning for the Future in an Uncertain World; Doubleday Currency: New York, NY, USA, 1991. [Google Scholar]

- Schoemaker, P.L.H. When and how to use scenario planning: A heuristic approach with illustration. J. Forecast. 1991, 10, 549–564. [Google Scholar] [CrossRef]

- Schoemaker, P. Multiple scenario development: Its conceptual and behavioural foundation. Strat. Manag. J. 1993, 14, 193–213. [Google Scholar] [CrossRef]

- Ungerer, M.; Herholdt, J. Thinking about the Future. In Viable Business Strategies: A Fieldbook for Leaders, 3rd; Ungerer, M., Pretorius, M., Herholdt, J., Eds.; Knowres Publishing: Randburg, South Africa, 2011. [Google Scholar]

- Postma, J.B.M.; Liebl, F. How to improve scenario analysis as a strategic management tool? Technol. Forecast. Soc. Change 2005, 72, 161–173. [Google Scholar]

- Berkhout, F.; Hertin, J. Foresight Futures Scenarios: Developing and Applying a Participative Strategic Planning Tool; University of Sussex: Sussex, UK, 2002; p. 39. [Google Scholar]

- Von Reibnitz, U.H. Scenario Techniques; McGraw-Hill GmbH: Hamburg, Germany, 1988. [Google Scholar]

- United Nations World Tourism Organisation (UNWTO), Policy and Practice for Global Tourism; UNWTO: Madrid, Spain, 2011.

- Conrady, R.; Buck, M. Preface and Overview. In Trends and Issues in Global Tourism 2010; Conrady, R., Buck, M., Eds.; Springer: Heidelberg, Germany, 2010. [Google Scholar]

- Goldin, I. Tourism and the G20: T20 Strategic Paper; Background Paper; T20 Tourism Ministers’ Meeting, Buyeo, Republic of Korea, October 2010.

- International Tourism Exchange (ITB), ITB World Travel Trends Report 2009/2010; Messe Berlin GmbH.: Berlin, Germany, December 2009; Paper prepared by IPK International on behalf of ITB Berlin.

- Euromonitor. World Travel Market Trends. December 2009. Available online: http://www.euromonitor.com/World_Travel_Market_Trends (accessed on 14 September 2010).

- FutureBrand. 2009 Country Index. Available online: http://www.futurebrand.com/think/reports-studies/cbi/2009/download/ (accessed on 5 November 2010).

- Bode, A. Practical Aspects of Corporate Social Responsibility—Challenges and Solutions. In Trends and Issues in Global Tourism 2010; Conrady, R., Buck, M., Eds.; Springer: Heidelberg, Germany, 2010. [Google Scholar]

- Adlwarth, W. Corporate Social Responsibility—Customer Expectations and Behaviour in the Tourism Sector. In Trends and Issues in Global Tourism 2010; Conrady, R., Buck, M., Eds.; Springer: Heidelberg, Germany, 2010. [Google Scholar]

- Gasser, U.; Simun, M. Digital lifestyle and online travel: Looking at the case of digital natives. In Trends and Issues in Global Tourism 2010; Conrady, R., Buck, M., Eds.; Springer: Heidelberg, Germany, 2010. [Google Scholar]

- Willdorf, N. The Global Travel Consumer: Current and Emerging Trends. Presentation, WTTC Global Summit, Beijing, China, May 2010.

- Stupnytska, A. Global Economy, the BRICS and Beyond. Presentation, WTTC Global Summit, Beijing, China, May 2010.

- World Economic Forum (WEF). Outlook on the Global Agenda 2012. Available online: http://www3.weforum.org/docs/GAC11/WEF_GAC11_OutlookGlobalAgenda.pdf (accessed on 23 December 2011).

- Intergovernmental Panel on Climate Change (IPCC), Climate Change 2007: Synthesis Report; Report of the Intergovernmental Panel on Climate Change; Intergovernmental Panel on Climate Change: Geneva, Switzerland, 2007.

- Scott, D. Towards Climate Compatible Travelism. In Green Growth and Travelism—Letters from Leaders; Lipman, G., DeLacy, T., Vorster, S., Hawkins, R., Jiang, M., Eds.; Goodfellows: London, UK, 2012. [Google Scholar]

- World Economic Forum (WEF), Towards a Low Carbon Travel & Tourism Sector; Report; World Economic Forum, Booz & Company, WEF: Geneva, Switzerland, May 2009.

- World Economic Forum (WEF), Policies and Collaborative Partnership for Sustainable Aviation;Project White Paper; WEF: Geneva, Switzerland, 2011 January.

- International Air Transport Association (IATA), Aviation and Climate Change; IATA: Geneva, Switzerland, September 2010.

- Climate Change and Tourism: Responding to Global Challenges, 2008. Available online: http://www.unwto.org/sdt/news/en/pdf/climate2008.pdf (accessed on 14 March 2011).

- Scott, D.; Peeters, P.; Gössling, S. Can Tourism ‘Seal the Deal’ of its Mitigation Commitments? The Challenge of Achieving ‘Aspirational’ Emission Reduction Targets. September 2009. Available online: http://www.cstt.nl/userdata/documents/can%20tourism%20'seal%20the%20deal'%20of%20its%20mitigation%20commitments,%20paul.pdf (accessed on 19 November 2012).

- Air Transport Action Group (ATAG), Aviation: Benefits Beyond Borders; ATAG: Geneva, Switzerland, 2012.

- Fonta, P. Pushing the Technology Envelope, in International Civil Aviation Organization; ICAO Environmental Report 2010; Aviation and Climate Change, ICAO & FCM Communications Inc.: Montréal, Canada, 2010; p. 77. [Google Scholar]

- Air Transport Action Group (ATAG). UNFCCC Climate Talks: The Right Flightpath to Reduce Aviation Emissions. Available online: www.atag.org/component/downloads/downloads/72.html (accessed on 27 September 2011).

- International Air Transport Association (IATA) Economics, Aviation and Climate Change Mitigation; IATA: Geneva, Switzerland, 2010.

- United Nations World Tourism Organisation (UNWTO). International Recommendations for Tourism Statistics 2008, ST/ESA/STAT/SER.M/83/Rev.1. Available online: http://unstats.un.org/unsd/tradeserv/tourism/0840120%20IRTS%202008_WEB_final%20version%20_22%20February%202010.pdf (accessed on 20 March 2011).

- Long, B.L. Environmental regulation: The third generation. The OECD Observer 1997, June/July, 14–18. [Google Scholar]

- Keohane, N.O.; Revesz, R.L.; Stavins, R.N. The choice of regulatory instruments in environmental policy. Harv. Environ. Law Rev. 1998, 22, p. 313. Available online: http://www.hks.harvard.edu/fs/rstavins/Papers/The_choice_of_regulatory.PDF (accessed on 26 March 2012).

- Dietz, T.; Stern, P.C. Exploring New Tools for Environmental Protection. New Tools for Environmental Protection: Education, Information, and Voluntary Measures; Dietz, T., Stern, P.C., Eds.; National Academy Press: Washington, DC, USA, 2002. Available online: http://www.nap.edu/chapterlist.php?record_id=10401&type=pdf_chapter&free=1 (accessed on 26 March 2012).

- Organization for Economic Cooperation and Development (OECD). Regulatory Policies in OECD Countries: From Interventionism to Regulatory Governance; OECD Reviews of Regulatory Reform; OECD Publishing: Paris, France, 2002. Available online: http://www.oecdbookshop.org/oecd/display.asp?sf1=identifiers&st1=422002121P1 (accessed on 26 March 2012).

- Stavins, R.N. Experience with Market-Based Environmental Policy Instruments. In The Handbook of Environmental Economics; Mäler, K., Vincent, J., Eds.; Elsevier Science: Amsterdam, The Netherlands, 2002. [Google Scholar]

- Wilbanks, T.J.; Stern, P.C. New Tools for Environmental Protection: What we Know and Need to Know. New Tools for Environmental Protection: Education, Information, and Voluntary Measures; Dietz, T., Stern, P.C., Eds.; National Academy Press: Washington, DC, USA, 2002. Available online: http://www.nap.edu/chapterlist.php?record_id=10401&type=pdf_chapter&free=1 (accessed on 26 March 2012).

- Hichert, T. The Future of Tourism in South Africa: A Horizon Scan; Background Paper; National Department of Tourism’s Scenario-Building Process; Institute for Futures Research: Bellville, South Africa, 2012. [Google Scholar]

- Hichert, T. The Future of Tourism in South Africa: Trends and Driving Forces; Background Paper; National Department of Tourism’s Scenario-Building Process, Institute for Futures Research: Bellville, South Africa, 2012. [Google Scholar]

- Lipman, G. Report on Macro-Level Drivers that will Impact Future Tourism Scenarios; Background Paper; National Department of Tourism’s Scenario-Building Process, greenearth.travel: Brussels, Belgium, 2012. [Google Scholar]

- Saunders, G. NDT Tourism Scenario Planning to 2030/2050: Selected Key Drivers; Background Paper; National Department of Tourism’s Scenario-Building Process; GrantThornton: Sandton, South Africa, 2012. [Google Scholar]

- McKinsey. Global Economic Scenarios 2010–2020: Volatility in a Multi-Speed World; McKinsey Quarterly Global Executive Survey; McKinsey: Boston, MA, USA, 2011. Available online: http://www.amchamsineurope.com/file/613/competitiveness%20of%20EU%20and%20US%20companies.pdf (accessed on 27 May 2012).

- Earth Negotiations Bulletin (ENB). Summary of the Bonn Climate Change Conference, Bonn, Germany, 14–25 May 2012; International Institute for Sustainable Development: Geneva, Switzerland, 2012; 12, pp. 1–23.

- International Civil Aviation Organization (ICAO). Consolidated Statement of Continuing ICAO Policies and Practices Related to Environmental Protection—Climate Change. Resolution A37-19 adopted at the International Civil Aviation Organisation’s General Assembly, 37th Session, Montréal, Canada, 16–18 June 2010; Available online: http://www.icao.int/env/A37_Res19_en.pdf (accessed on 12 December 2010).

- International Civil Aviation Organization (ICAO). Emissions from fuel used for international aviation and maritime transport. Agenda item 6(a), FCCC/SBSTA/2010/MISC.14. Submission by the International Civil Aviation Organization (ICAO) at the 33rd Session of the United Nations Framework Convention on Climate Change (UNFCCC) Subsidiary Body for Scientific and Technological Advice (SBSTA33), Cancun, Mexico, 30 November–4 December 2010; Available online: http://www.icao.int/icao/en/env2010/Statements/sbsta-33_Item-6a.pdf (accessed on 12 December 2010).

- International Air Transport Association (IATA). Report of the Board of Governors; Agenda item 6, Document 1; Report presented at the 67th Annual General Meeting, Singapore, Singapore, June 2011.

- United Nations Framework Convention on Climate Change (UNFCCC). Kyoto Protocol to the United Nations Framework Convention on Climate Change; UNFCCC Secretariat: Bonn, Germany, 1997. Available online: http://unfccc.int/kyoto_protocol/items/2830.php (accessed on 6 March 2011).

- Havel, B.F. Briefing Paper 2: Do we need a new Chicago Convention? In Proceeding of the World Economic Forum Aviation, Travel and Tourism Industry Council, WEF, Geneva, Switzerland, 2011.

- Peterson, M. The Legality of the EU’s stand-alone approach to the climate impact of aviation: The express role given to the ICAO by the Kyoto Protocol. Reciel. 2008, 17, 196–204. [Google Scholar]

- Lyle, C. Breaking the Surly Bonds of Economic Regulation; Air Transport Economics: Québec Canada, 2011. [Google Scholar]

- Havel, B.F.; Sanchez, G.S. The emerging Lex Aviatica. Georgetown J. Int. Law. 2010, 42, 1. [Google Scholar]

- International Air Transport Association (IATA), Vision 2050; Report adopted in Singapore; IATA: Geneva, Switzerland, 2011 February 12.

- World Trade Organisation (WTO), Tourism Services; Background note by the Secretariat; S/C/W/51WTO: Geneva, Switzerland, 23 September 1998.

- World Travel and Tourism Council (WTTC), Travel and Tourism Economic Impact 2011; WTTC: London, United Kingdom, 2011.

- United Nations World Tourism Organisation (UNWTO). Provisional Agenda Item 5; Report of the Secretary-General, General Assembly, 19th session, Gyeongju, Republic of Korea, 8–14 October 2011; Available online: https://s3-eu-west-1.amazonaws.com/storageapi/sites/all/files/pdf/a19_05_report_sg_e.pdf (accessed on 3 October 2011).

- International Air Transport Association (IATA), International Air Transport Association Annual Report 2011; International Air Transport Association (IATA): Singapore, Singapore, June 2011.

- International Air Transport Association (IATA). A Global Framework for Addressing Aviation CO2 Emissions: Frequently asked Questions; Background Paper; ICAO 37th General Assembly, Montréal, Canada, 16–18 June 2010.

- World Travel and Tourism Council (WTTC), Travel and Tourism 2011; WTTC: London, UK, 2011.

- Scowsill, D. Speech by David Scowsill, President and CEO of the World Travel and Tourism Council, 2011. Available online: http://www.onecaribbean.org/content/files/WTTCDavidScowsill.pdf (accessed on 22 May 2012).

- United Nations Environment Programme (UNEP). Towards a Green Economy, Pathways to Sustainable Development and Poverty Eradication; UNEP: Nairobi, Kenya, 2011. Available online: http://www.unep.org/GreenEconomy/Portals/93/documents/Full_GER_screen.pdf (accessed on 22 February 2011).

- Dray, L.; Evans, A.; Schäfer, A. Fleet Renewal Policies—Initial Estimations. In Paper prepared for the World Economic Forum Aviation, Travel and Tourism Industry Agenda Council, WEF, Geneva, 2011; p. 1.

- Pearce, B. Analysis Behind the Air Transport Industry’s Global Sector Agreement on Climate Change; IATA: Geneva, Switzerland, 2010; pp. 6–7. [Google Scholar]

- Tyler, T. A Green Economy: The Contribution of Travel and Tourism—The Aviation Viewpoint. In Green Growth and Travelism—Letters from Leaders; Lipman, G., DeLacy, T., Vorster, S., Hawkins, R., Jiang, M., Eds.; Goodfellows: London, UK, 2012. [Google Scholar]

- Harbison, P. Sustainable Aviation and Green Growth—Blood, Sweat and Tears. In Green Growth and Travelism—Letters from Leaders; Lipman, G., DeLacy, T., Vorster, S., Hawkins, R., Jiang, M., Eds.; Goodfellows: London, UK, 2012. [Google Scholar]

- International Air Transport Association (IATA). A Global Approach to Reducing Aviation Emissions, 2009. Available online: http://www.iata.org/SiteCollectionDocuments/Documents/Global_Approach_Reducing_Emissions_251109web.pdf (accessed on 12 December 2010).

- International Air Transport Association (IATA), Fact Sheet: Environment; IATA: Geneva, Switzerland, June 2010.

- Air Transport Action Group (ATAG), Beginner’s Guide to Aviation Efficiency; ATAG: Geneva, Switzerland, 2010.

- Baljet, M. Aviation Biofuel. Presentation on behalf of IATA, Assistant Director Operations, IATA, Geneva, Switzerland, 2010.

- Air Transport Action Group (ATAG), Aviation Biofuels; ATAG: Geneva, Switzerland, 2011.

- O’Hanlon, S. Aviation Biofuels: From Fields to Wheels Up (R&D to Commercialization). Presentation at a World Biofuels Conference, London, UK, 2011. Available online: http://library.greenpowerconferences.com/abm/presentation.pdf (accessed on 14 November 2011).

- Air Transport Action Group (ATAG), Beginner’s Guide to Aviation Efficiency; ATAG: Geneva, Switzerland, 2009.

- International Air Transport Association (IATA). A Global Approach to Reducing Aviation Emissions; IATA: Montreal, Canada, 2009; p. 4. Available online: http://www.iata.org/SiteCollectionDocuments/Documents/Global_Approach_Reducing_Emissions_251109web.pdf (accessed on 12 December 2010).

- United Kingdom Committee on Climate Change (UKCCC), Meeting the UK Aviation Target—Options for Reducing Emissions; United Kingdom Committee on Climate Change: London, UK, 2009.

- Bauen, A.; Howes, J.; Bertucciolli, L.; Chudziak, C. Review of the Potential for Biofuels in Aviation; Final E4Tech Report; UK Committee on Climate Change: London, UK, August 2009. [Google Scholar]

- Hileman, J.I.; Ortiz, D.S.; Bartis, J.T.; Wong, H.M.; Donohoo, P.E.; Weiss, M.A.; Waitz, I.A. Near-Term Feasibility of Alternative Jet Fuels; Technical Report; RAND Corporation and Massachusetts Institute of Technology: Santa Monica, CA, USA, 2009. [Google Scholar]

- Caesar, W.K.; Riese, J.; Seitz, T. Betting on biofuels. The McKinsey Quarterly 2007, 2, 53–63. [Google Scholar]

- Aviation Global Deal Group (AGD group). A Sectoral Approach to Addressing International aviation Emissions; Discussion Note 2.0; Aviation Global Deal Group: London, UK, 9 June 2009. Available online: http://www.agdgroup.org/pdfs/090609_AGD_Discussion_Note_2.0.pdf (accessed on 28 February 2011).

- Aviation Global Deal Group (AGD group), A Coordinated Pathway Towards a Global Sectoral Agreement for International Aviation Emissions; AGD Group Discussion Paper; AGD Group: London, UK, 2011 December.

- Gössling, S.; Peeters, P.; Scott, D. Consequences of climate policy for international tourist arrivals in developing countries. Third World Q. 2008, 29, 874. [Google Scholar]

- Meinshausen, M. On the Risk of Overshooting 2 ºC. Paper presented at the Scientific Symposium Avoiding Dangerous Climate Change, MetOffice, Exeter, UK, 1–3 February 2005.

- United Nations World Tourism Organisation (UNWTO). 2010 International Tourism Results and Prospects for 2011. In Proceeding of the UNWTO News Conference, Madrid, Spain, 17 January 2011.

- World Travel Market (WTM), World Travel Market 2011: Industry Report; WTM: London, UK, November 2011.

- Scowsill, D. Travel & Tourism Leading the Way Towards Green Growth. In Green Growth and Travelism—Letters from Leaders; Lipman, G., DeLacy, T., Vorster, S., Hawkins, R., Jiang, M., Eds.; Goodfellows: London, UK, 2012. [Google Scholar]

- World Travel and Tourism Council (WTTC). Climate Change: A Joint Approach to Addressing the Challenge, 2010. Available online: http://www.wttc.org/bin/pdf/original_pdf_file/climate_change_final.pdf (accessed on 2 December 2010).

- Bisignani, G. The Mystery of Governments’ Aviation Policy. In Green Growth and Travelism—Letters from Leaders; Lipman, G., DeLacy, T., Vorster, S., Hawkins, R., Jiang, M., Eds.; Goodfellows: London, UK, 2012. [Google Scholar]

- Williams, K. Speech by British Airways CEO, Caribbean Tourism Organization Conference, Marigot, Saint-Martin, 16 September 2011; Available online: http://www.eturbonews.com/25264/british-airways-ceo-provides-world-view-state-tourism-industry (accessed on 19 September 2011).

- Gössling, S.; Broderick, J.; Upham, P.; Ceron, J.; Dubois, P.; Peeters, P.; Strasdas, W. Voluntary carbon offsetting schemes for aviation: Efficiency, credibility and sustainable tourism. J. Sustain. Tourism 2007, 15, 223–247. [Google Scholar] [CrossRef]

- Beaverstock, J.; Derudder, B.; Faulconbridge, J.; Witlox, F. International Business Travel in the Global Economy 2010. Available online: http://books.google.co.za/books?id=Z4wiZsqvm3sC&pg=PA118&lpg=PA118&dq=virtual+technology+video+conferencing+business+travel+substitute&source=bl&ots=23BjCBgxuP&sig=VImPFmxtFOqbNa0BXYC2XQsZbA0&hl=en&sa=X&ei=SyLFT6vGDsrBhAfH69zvCQ&redir_esc=y#v=onepage&q=virtual%20technology%20video%20conferencing%20business%20travel%20substitute&f=false (accessed on 29 May 2012).

- Mullich, J. The new face of face-to-face meetings efficiencies, technology, and better metrics bring freater ROI. Wall St. J. 2010. Available online: http://online.wsj.com/ad/article/globaltravel-face (accessed on 29 May 2012).

- Kennedy, D.; Combes, B.; Bellamy, O. Meeting the UK Aviation Target—Options for Reducing Emissions to 2050, in International Civil Aviation Organization; ICAO Environmental Report 2010: Aviation and Climate Change; ICAO & FCM Communications Inc.: Montréal, Canada, 2010. [Google Scholar]

- Gleaves, S.D. Potential for Modal Shift from Air to Rail for UK Aviation; Report; UK Committee on Climate Change: London, UK, 2008 September. [Google Scholar]

- United Kingdom Climate Change Committee (UKCCC), Government Response to the Committee of Climate Change Report on Reducing CO2 Emissions from UK Aviation to 2050; UK Department for Transport: London, UK, August 2011.

- Karlitekin, C. Forecasting the Future of Travel and Tourism: Future of Global Aviation. In Trends and Issues in Global Tourism 2010; Conrady, R., Buck, M., Eds.; Springer: Heidelberg, Germany, 2010. [Google Scholar]

- Scott, D.; Lemieux, C. Weather and Climate Information for Tourism; Report; World Meteorological Organisation and United Nations World Tourism Organization: Geneva, Switzerland, August 2009. Available online: http://www.unwto.org/climate/support/en/pdf/WCC3_TourismWhitePaper.pdf (accessed on 20 March 2011).

- United Nations World Tourism Organisation (UNWTO). International Tourism to Reach one Billion in 2012. Available online: http://media.unwto.org/en/press-release/2012-01-16/international-tourism-reach-one-billion-2012 (accessed on 11 April 2012).

- European Commission (EC). Draft Commission Decision on historical aviation emissions pursuant to Article 3c(4) of Directive 2003/87/EC of the European Parliament and of the Council establishing a scheme for greenhouse gas emission allowance trading within the Community. Available online: http://ec.europa.eu/clima/news/docs/decision_en.pdf (accessed on 2 April 2011).

- European Commission (EC). Inclusion of aviation in the EU ETS: Commission publishes historical emissions data on which allocations will be based, 11 March 2011. IP/11/259. Available online: http://europa.eu/rapid/pressReleasesAction.do?reference=IP/11/259&format=HTML&aged=0&language=EN&guiLanguage=fr (accessed on 2 April 2011).

- European Commission (EC). Questions & Answers on historic aviation emissions and the inclusion of aviation in the EU’s Emission Trading System (EU ETS). Memo/11/139, 2011c. Available online: http://europa.eu/rapid/pressReleasesAction.do?reference=MEMO/11/139&format=HTML&aged=0&language=EN&guiLanguage=fr (accessed on 2 April 2011).

- European Commission (EC). Reducing Emissions from the Aviation Sector. Fact Sheet, 2011. Available online: http://ec.europa.eu/clima/policies/transport/aviation/index_en.htm (accessed on 2 April 2011).

- International Energy Agency (IEA), Sustainable Production of Second-Generation Biofuels: Potential and Perspectives in Major Economies and Developing Countries; Information Paper; IEA: Paris, France, 2010.

- Steele, P. Aviation and Environment. Presentation, IATA’s Post-COP16, UNFCCC 16th Conference of the Parties, Cancun, Mexico, 29 November–10 December 2012; Media Briefing: Geneva, Switzerland, 2010.

- Siebert, A.; Rodrigues, C.A. SESAR and the Environment, in International Civil Aviation Organization; ICAO Environmental Report 2010: Aviation and Climate Change; ICAO & FCM Communications Inc.: Montréal, Canada, 2010; p. 109. [Google Scholar]

- Holsclaw, C.A. Development of an Aircraft CO2 Emissions Standard, in International Civil Aviation Organization; ICAO Environmental Report 2010: Aviation and Climate Change; ICAO & FCM Communications Inc.: Montréal, Canada, 2010. [Google Scholar]

- Strong, M. Facing down armageddon: Our environment at a crossroads. World Pol. J. 2009, 26, 25–32. [Google Scholar]

- Polsky, C.; Neff, R.; Yarnal, B. Building comparable global change vulnerability assessments: The vulnerability scoping diagram. Global Environ. Change 2007, 17, 472–485. [Google Scholar] [CrossRef]

- Birkmann, J. Vulnerability and Resilience of Coupled Human-Environmental Systems; Institute for Environment and Human Security: Tokyo, Japan, 2007. [Google Scholar]

- Lorenz, D.; Heard, B.; Hoekstra-Fokkink, L.; Orchard, J.; Valeri, S. Towards a City of Melbourne Climate Change Adaptation Strategy: A Risk Assessment and Action Plan; Discussion Paper; Maunsell Australia Pty Ltd.: Melbourne, Australia, 2008. [Google Scholar]

- Sivell, P.M.; Reeves, S.J.; Baldachin, L.; Brightman, T.G. Climate Change Resilience Indicators; South East United Kingdom Regional Assembly, Transport Research Laboratory: Berkshire, UK, 2008. [Google Scholar]

- Booz & Company, Green Tourism: A Road Map for Transformation; Booz & Company Inc.: Frankfurt, Germany, 2010.

- Fuller, E.D. Helping to Manage Change by Sitting at the Table. In Green Growth and Travelism—Letters from Leaders; Lipman, G., DeLacy, T., Vorster, S., Hawkins, R., Jiang, M., Eds.; Goodfellows: London, UK, 2012. [Google Scholar]

- World Travel and Tourism Council (WTTC), Durban Communiqué; WTTC: London, UK, 7 December 2011.

- Hotel Energy Solutions (HES), Analysis of Energy use by European Hotels; Online Survey and Desk Research; Hotel Energy Solutions project publications, 1st ed; UNWTO: Madrid, Spain, 2011.

- International Task Force on Sustainable Tourism Development (ITF-STD), A Three-Year Journey for Sustainable Tourism; UNEP & the Government of France: Paris, France, 2009.

- Taleb, N.N. The Black Swan: The Impact of the Highly Improbable; Allen Lane: London, UK, 2007. [Google Scholar]

© 2013 by the authors; licensee MDPI, Basel, Switzerland. This article is an open-access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/3.0/).

Share and Cite

Vorster, S.; Ungerer, M.; Volschenk, J. 2050 Scenarios for Long-Haul Tourism in the Evolving Global Climate Change Regime. Sustainability 2013, 5, 1-51. https://doi.org/10.3390/su5010001

Vorster S, Ungerer M, Volschenk J. 2050 Scenarios for Long-Haul Tourism in the Evolving Global Climate Change Regime. Sustainability. 2013; 5(1):1-51. https://doi.org/10.3390/su5010001

Chicago/Turabian StyleVorster, Shaun, Marius Ungerer, and Jako Volschenk. 2013. "2050 Scenarios for Long-Haul Tourism in the Evolving Global Climate Change Regime" Sustainability 5, no. 1: 1-51. https://doi.org/10.3390/su5010001

APA StyleVorster, S., Ungerer, M., & Volschenk, J. (2013). 2050 Scenarios for Long-Haul Tourism in the Evolving Global Climate Change Regime. Sustainability, 5(1), 1-51. https://doi.org/10.3390/su5010001