Towards Life Cycle Sustainability Assessment

Abstract

:1. Introduction

1.1. From Environmental Protection towards Sustainability

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Characteristics | “TRADITIONAL” environmental protection | “MODERN” environmental protection |

|---|---|---|

| political background | control of risks, dangers | sustainability (“triple bottom line”) |

| primary policy principle | command & control | push & pull |

| main actor | governments | society (“shared responsibility”) |

| policy setting | confrontation | cooperation |

| tasks | separation of tasks, individual solutions | integration of tasks, system solutions |

| principle for action | reactive | proactive |

| regional scope | local, national | international |

| focus | production (“single processes”) | products (“process networks”) |

| environment | single compartments and emissions | complete cross-media view over the complete life cycle |

| environmental technology | separate processes, end-of-pipe | integrated processes, innovations |

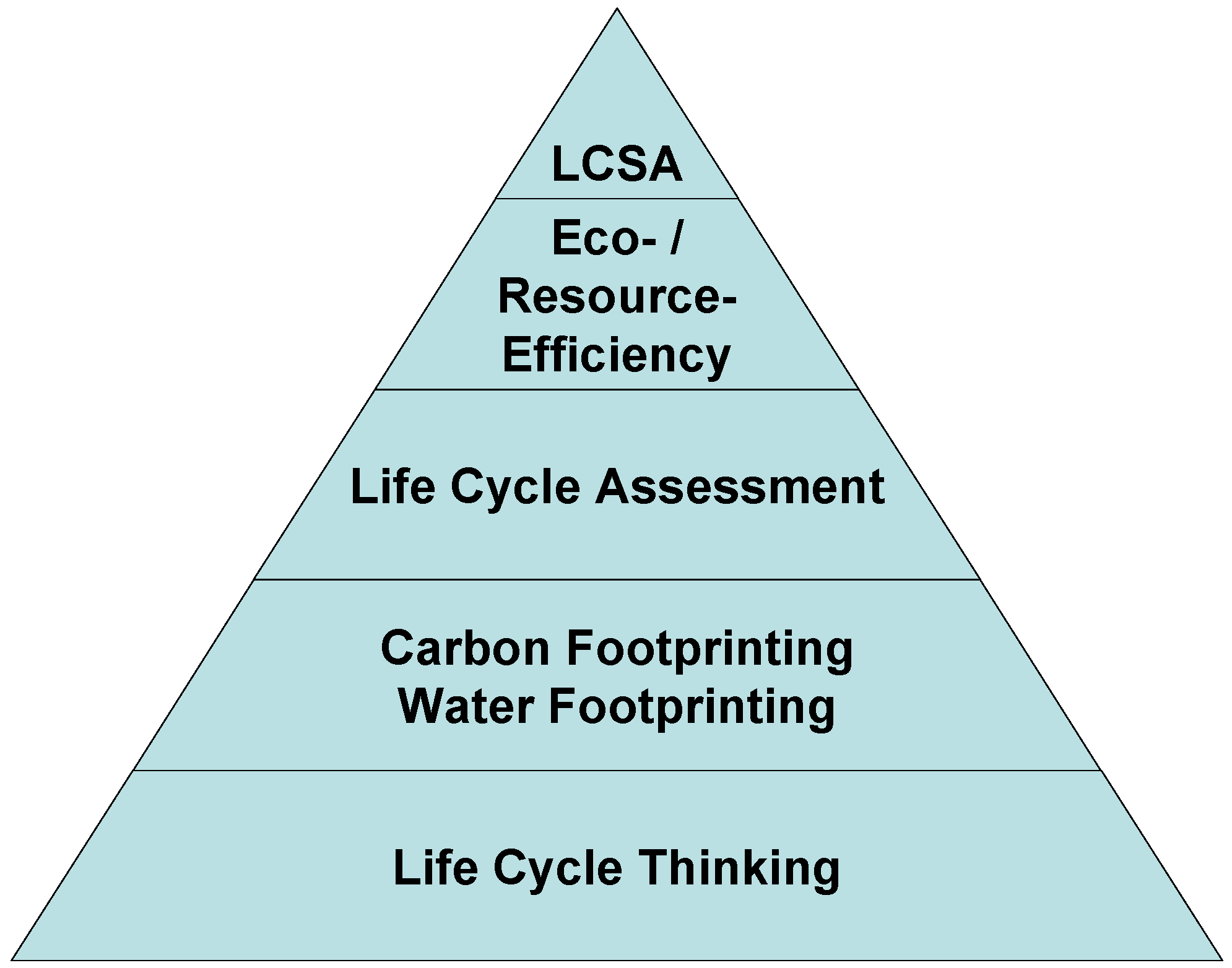

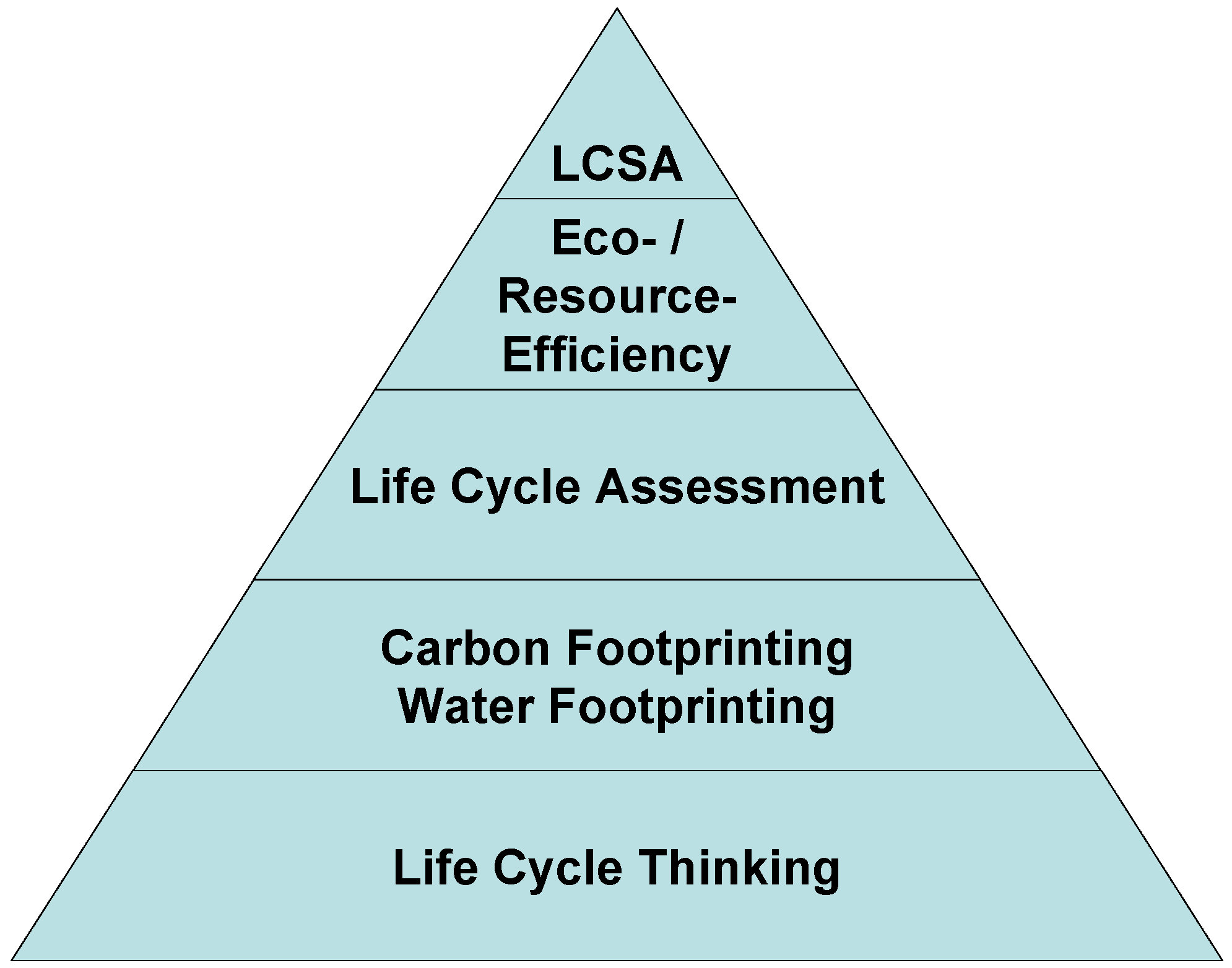

1.2. Maslow’s Pyramid of Environmental and Sustainability Assessment Tools

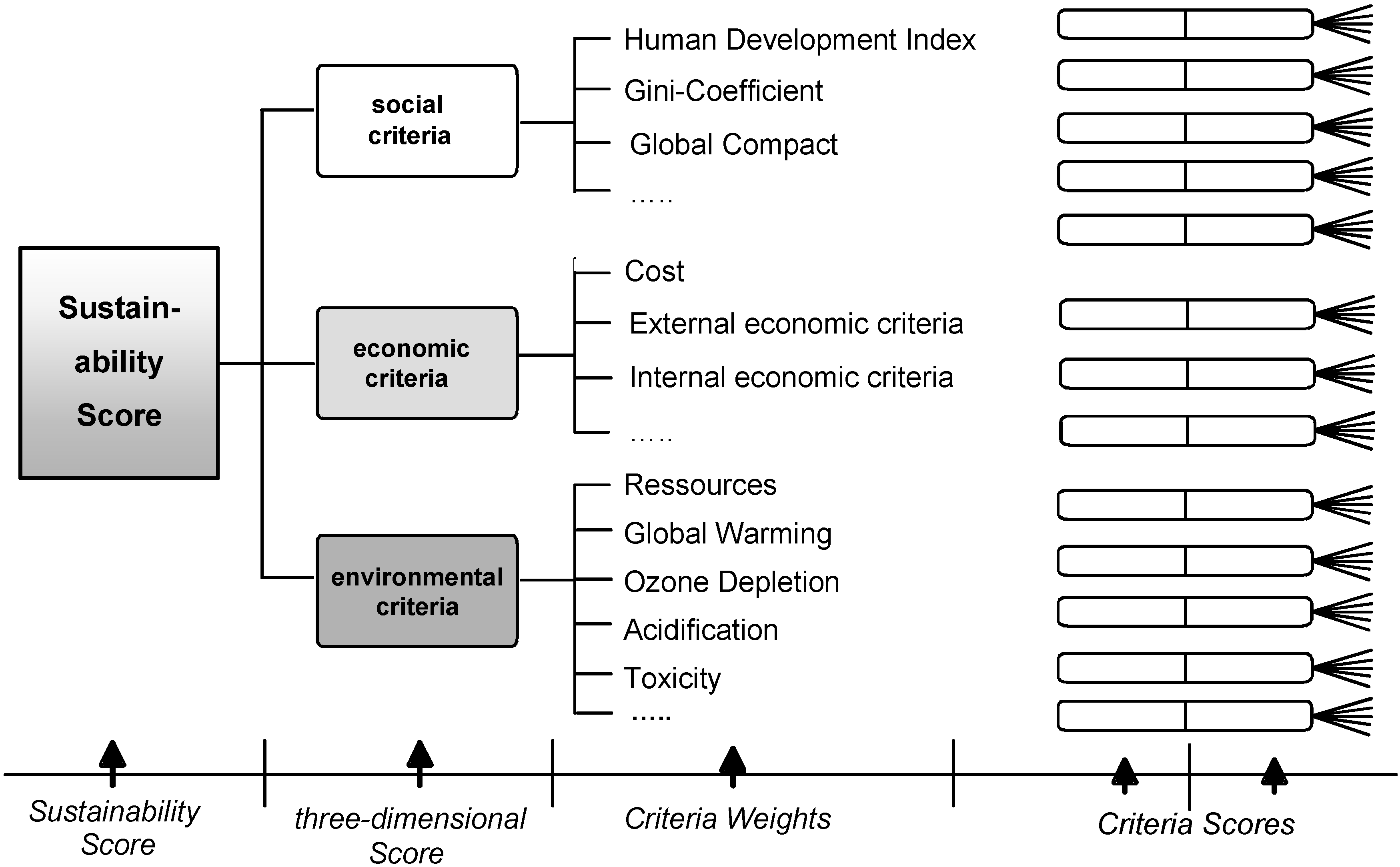

2. Life Cycle Sustainability Assessment Methodology

LCSA = Life Cycle Sustainability Assessment

LCA = Environmental Life Cycle Assessment

LCC = LCA-type Life Cycle Costing

SLCA = Social Life Cycle Assessment

2.1. Environmental Dimension

- Life cycle perspective:all phases (“from the cradle to the grave”) of the life cycle of a product (good or service)—from the extraction and processing of the resources, over production and further processing, distribution and transport, use and consumption to recycling and disposal—have to be assessed with regard to all relevant material and energy flows.

- Cross-media environmental approach:all relevant environmental impacts are taken into account, i.e., both on the input side (use of resources) and on the output side (emissions to air, water and soil, including waste).

2.2. Economic Dimension

2.3. Social Dimension

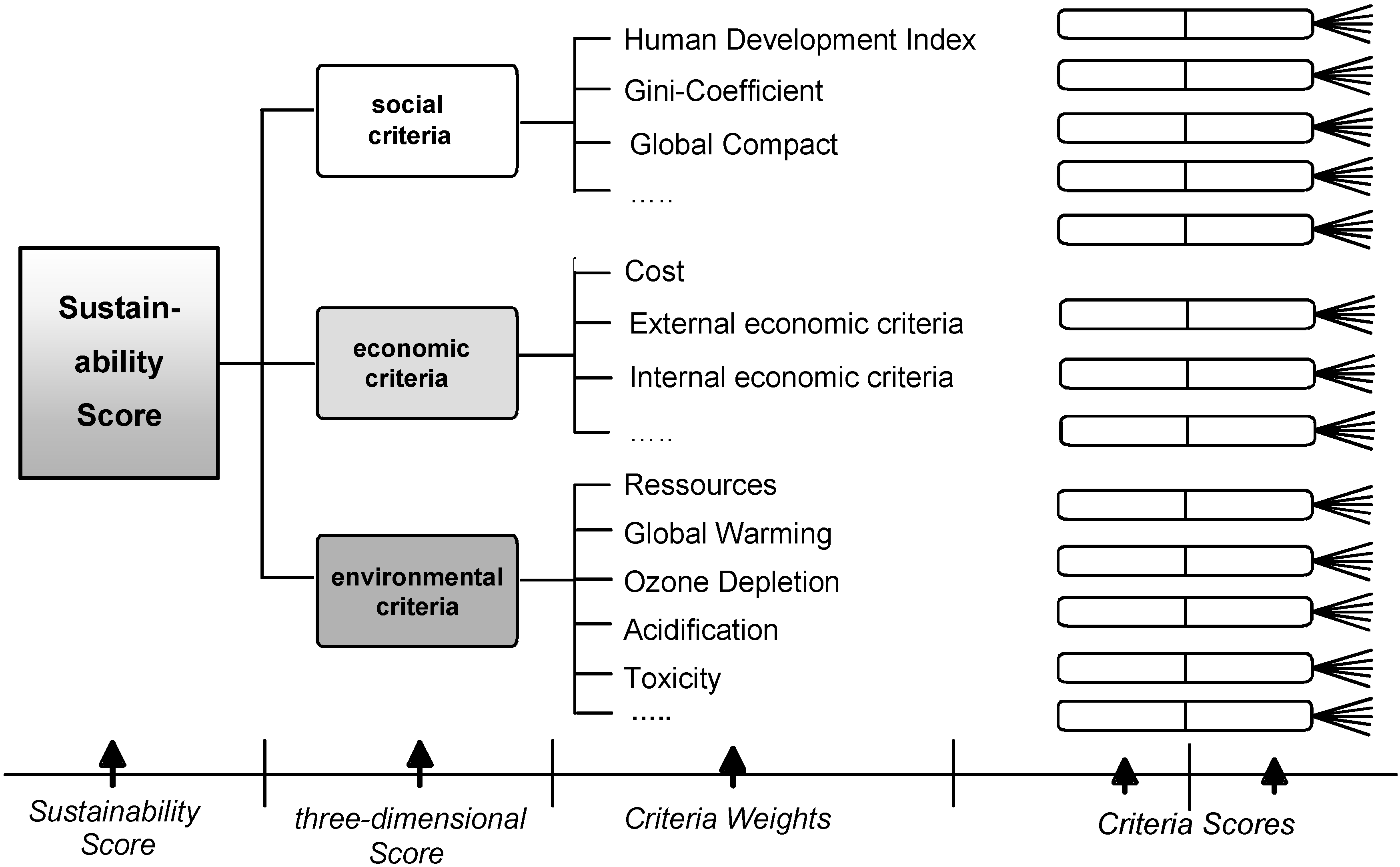

- Human Development Index (HDI) [32]: data accessible in the annual Human Development Reports.

- Gini-coefficient as a measure of inequality of wealth [33]: data accessible in the annual Human Development Reports (http://hdr.undp.org) and

- Commitment to comply with the criteria of the UN Global Compact [34]: data accessible in the weekly updated index.

3. Life Cycle Sustainability Assessment Evaluation Schemes

- weighting of individual indicators within each of the three sustainability dimensions, i.e., weighting between e.g., different environmental indicators like global warming potential and acidification potential (the same applies to social and economic indicators), and

- weighting among the three dimensions of sustainability (environmental, economic, social).

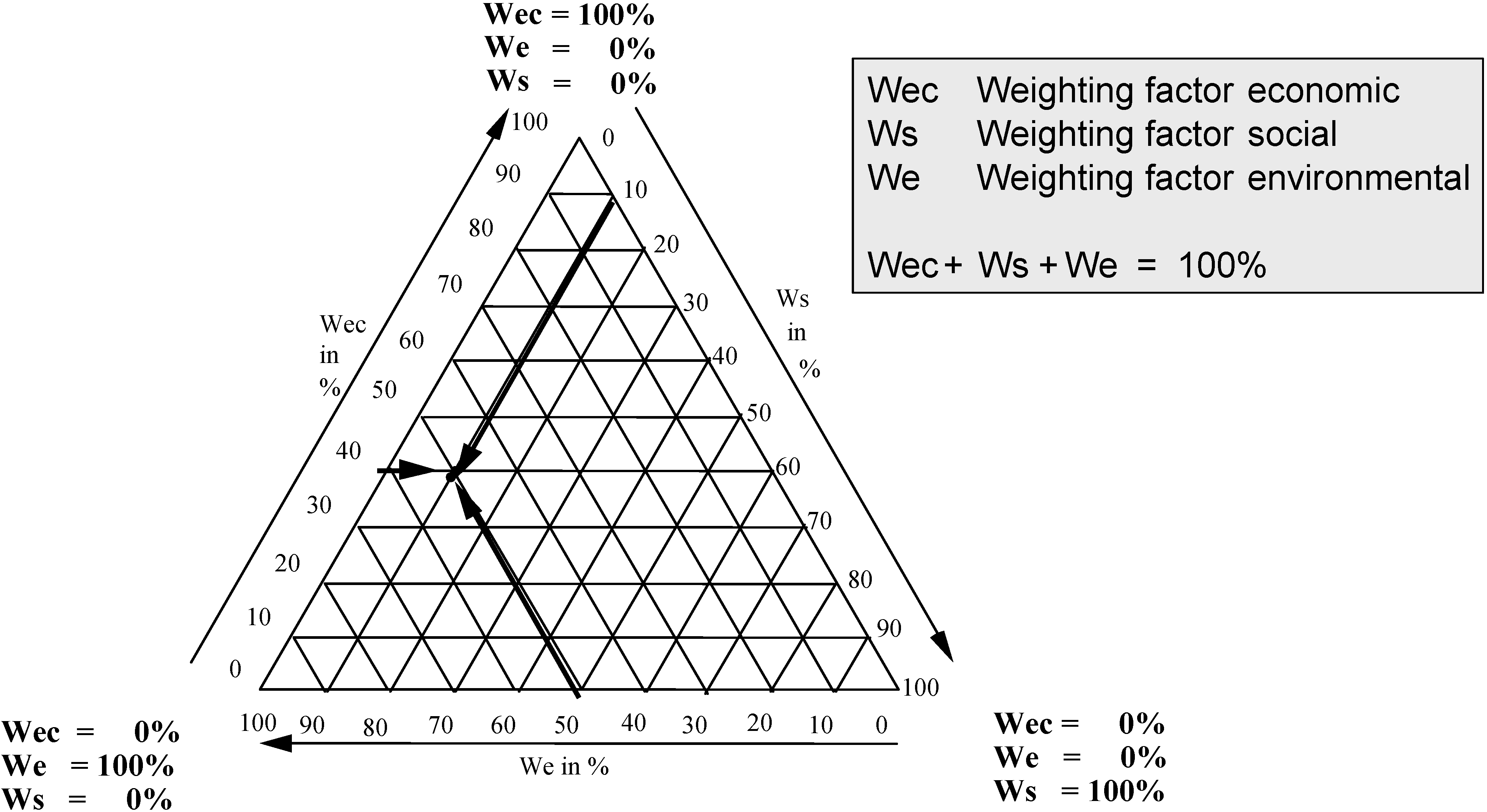

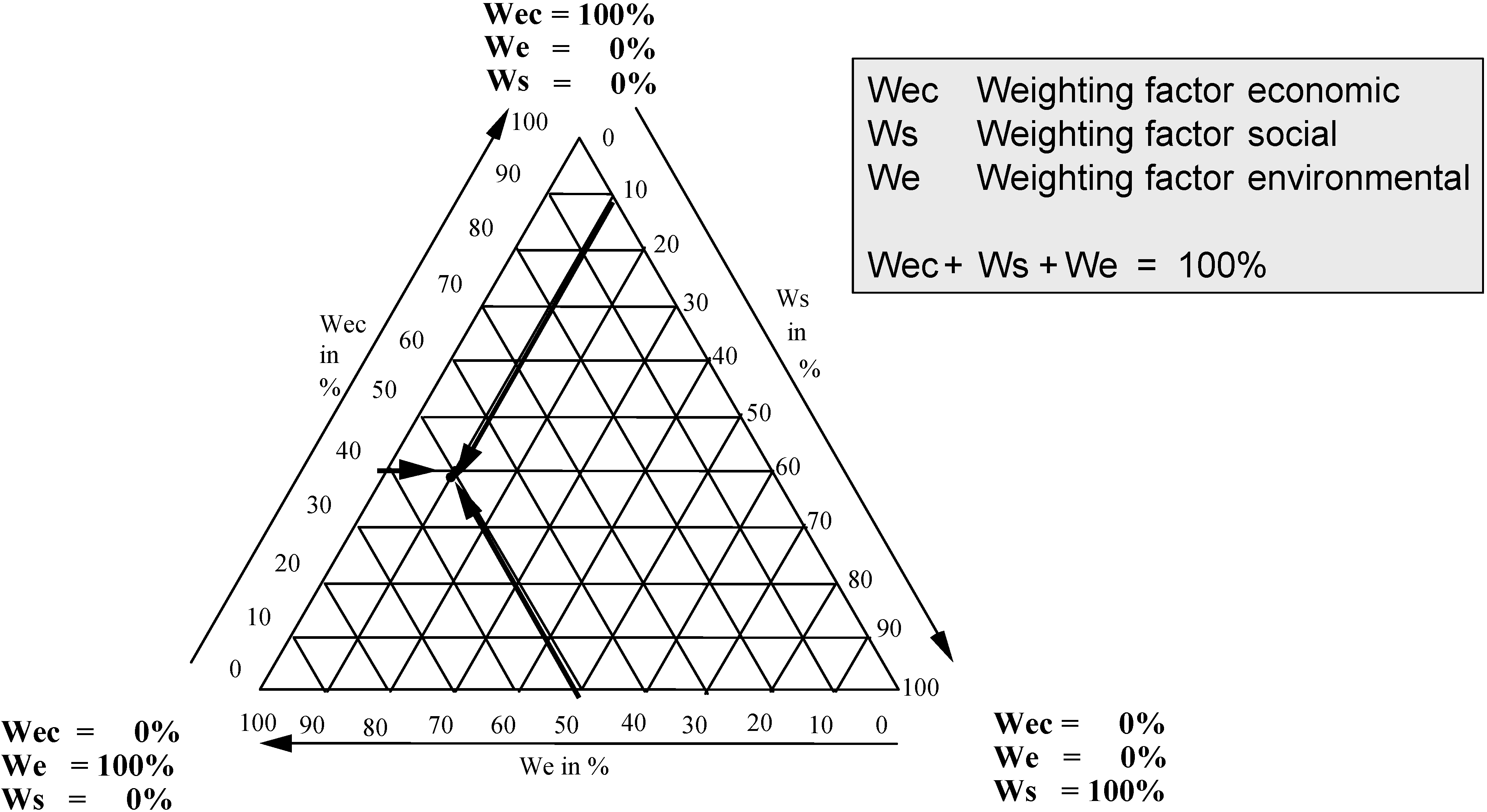

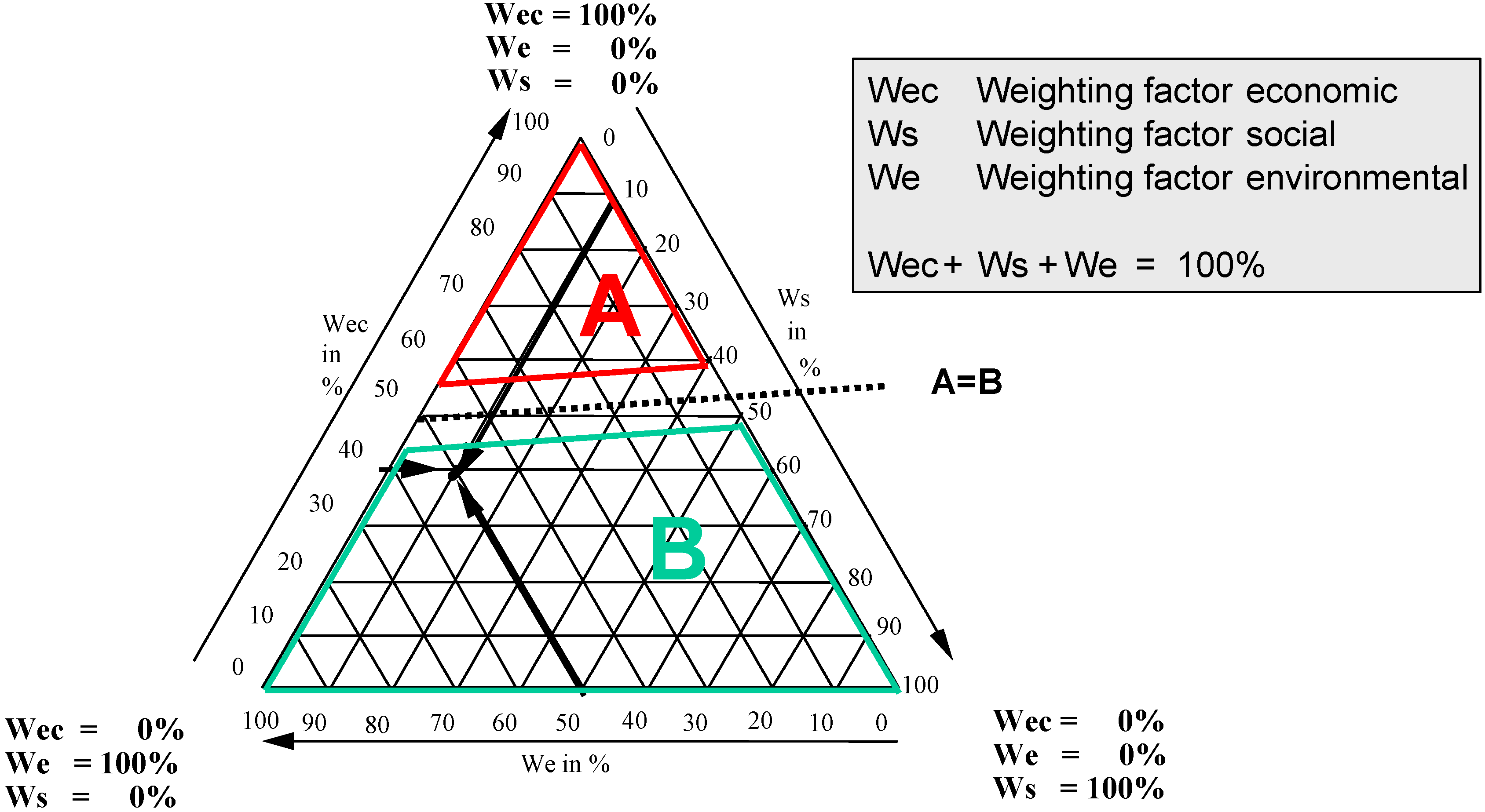

3.1. Life Cycle Sustainability Triangle (LCST)

- environmental value: Ei

- social value: Si

- economic value: Eci

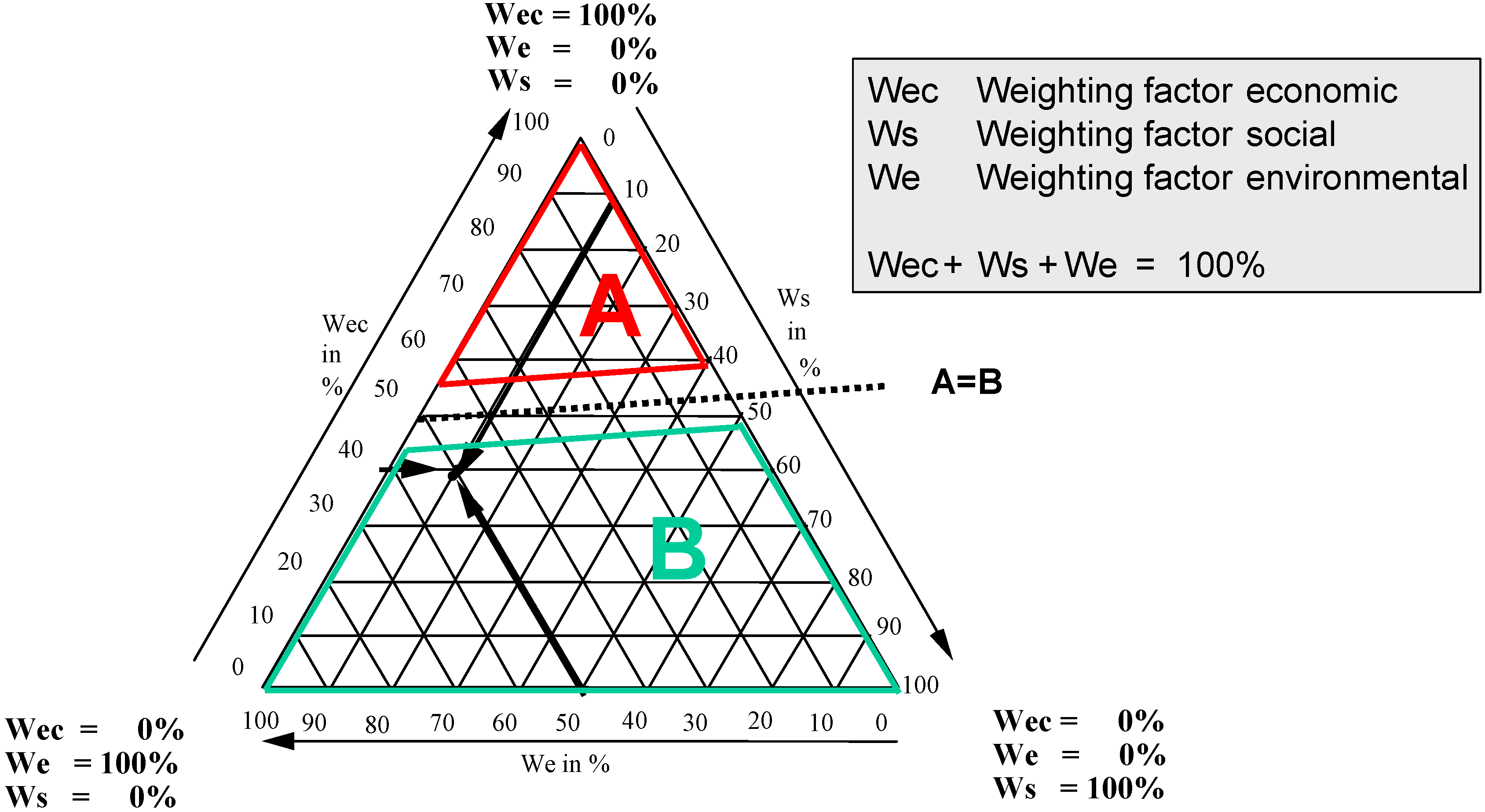

- Environmental PerformanceAt the upper corner (point 1) environment is weighted at 100%. If the decision is solely based on environmental criteria, alternative A is chosen. If one now follows the environmental axis up to point 2, the dominance changes, i.e., option A is now only preferred if environment is weighted at least 53%. At a lower weighting of environmental performance alternative B always dominates.

- Social PerformanceAt the right corner (point 3) the social dimension is weighted at 100%. If the decision is solely based on social criteria, alternative B is chosen. If one now follows the social axis up to point 4 the dominance field changes, i.e., in a purely socio-environmental weighting a social weighting of below 43% would lead to a preference of option A. If one includes the economic dimension, option B can also dominate with a social weighting of only 10% if the economic performance is weighted by more than 50% (point 5).

- Economic PerformanceOn the left corner (point 6) economic performance is weighted at 100%. If the decision is solely based on economy, alternative B is chosen. A weighting of 47% corresponds to point 7 on the economy axis. If economic performance is weighted at least with this value alternative B always dominates.

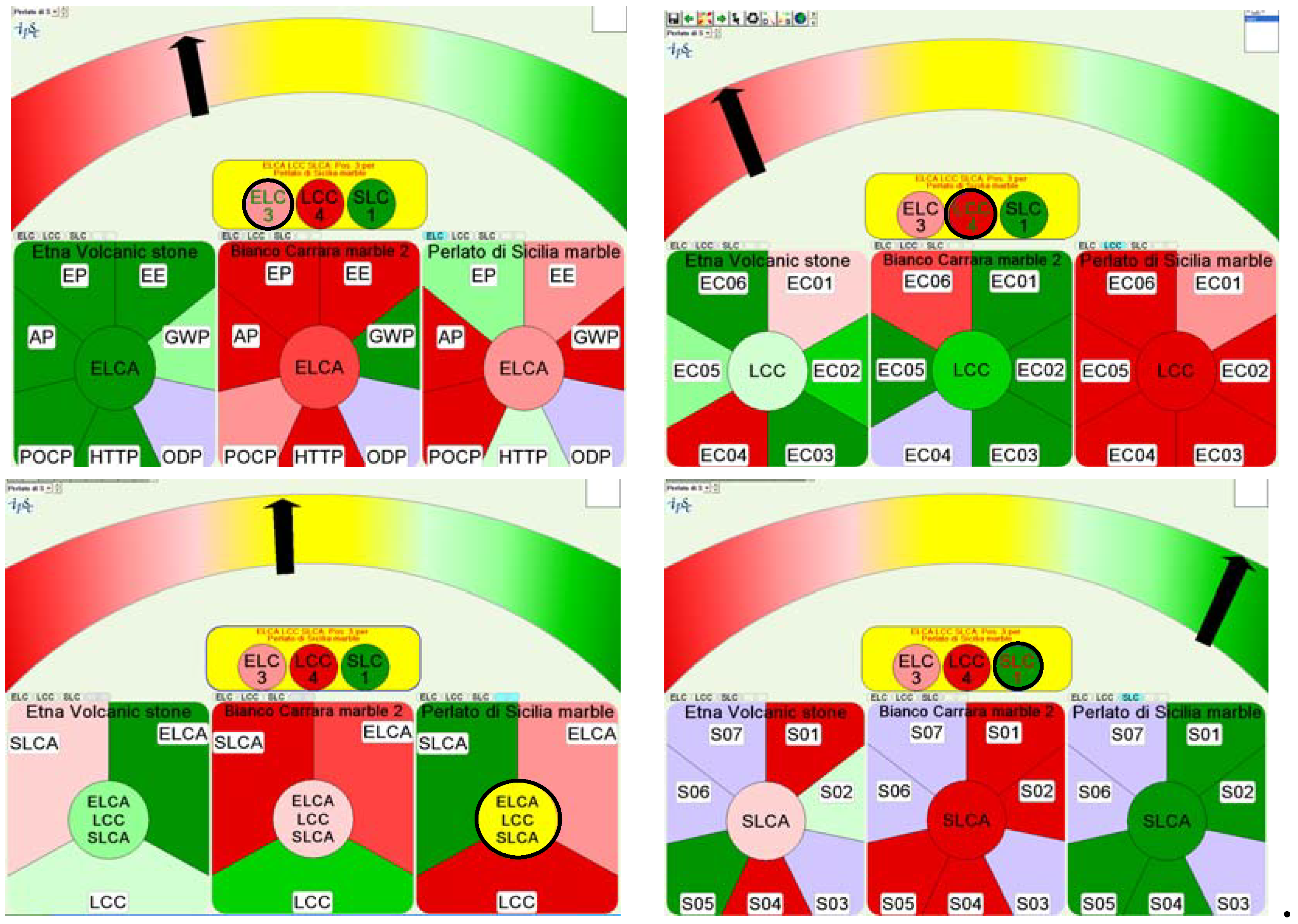

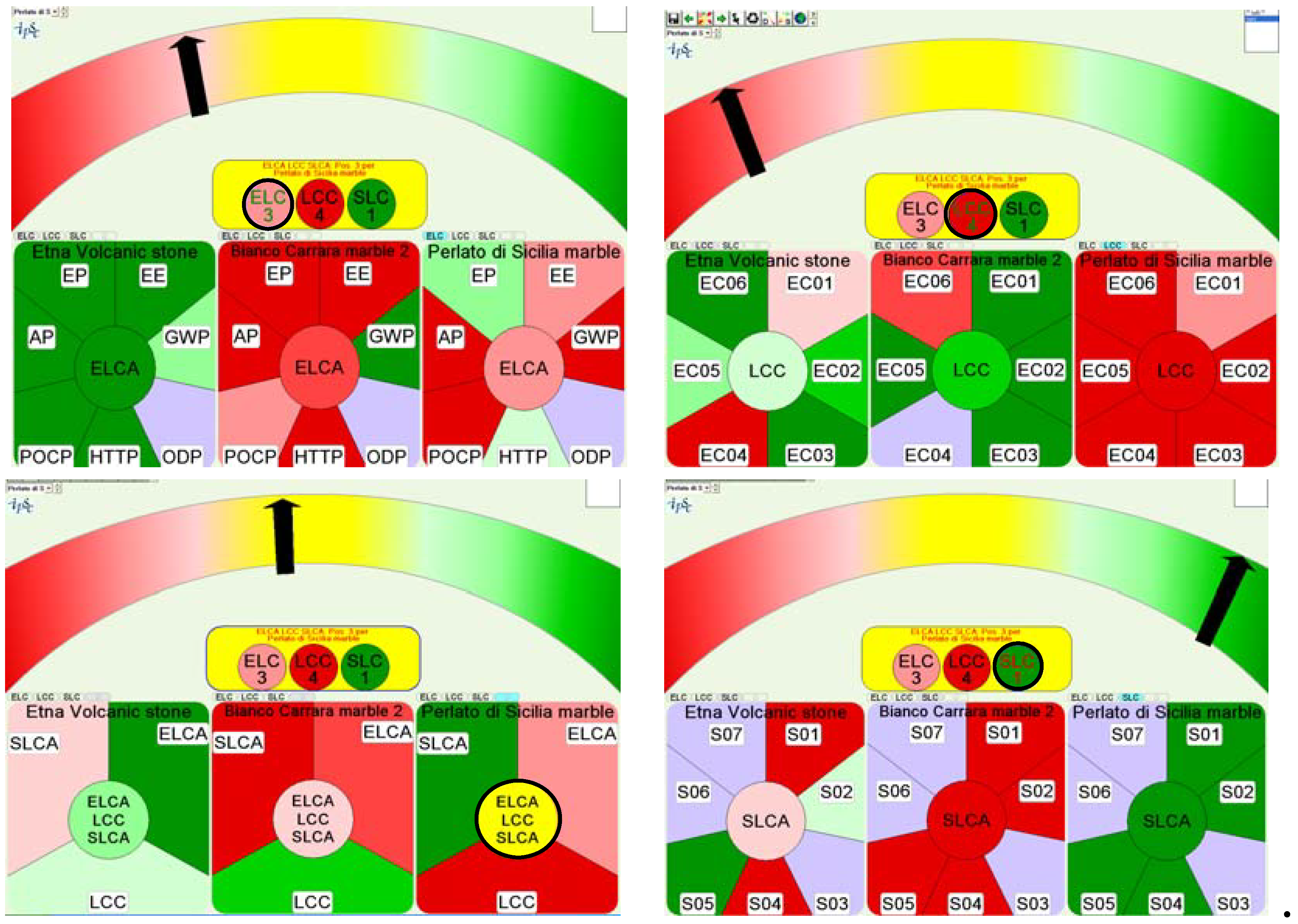

3.2. Life Cycle Sustainability Dashboard (LCSD)

4. Conclusions

Acknowledgements

References and Notes

- Brand, K.W. Politik der Nachhaltigkeit; Edition sigma: Berlin, Germany, 2002. [Google Scholar]

- Bruntland, G.H. Our Common Future: The World Commission on Environment and Development; Oxford University Press: Oxford, UK, 1987. [Google Scholar]

- Rubik, F. Integrierte Produktpolitik; Metropolis: Marburg, Germany, 2002. [Google Scholar]

- Maslow, A.H. A Theory of Human Motivation. Psychol. Rev. 1943, 50, 370–396. [Google Scholar] [CrossRef]

- Communication on Integrated Product Policy; European Commission: Brussels, Belgium, 2003.

- Finkbeiner, M. Carbon Footprinting—Opportunities and threats. Int. J. Life Cycle Assess. 2009, 14, 91–94. [Google Scholar] [CrossRef]

- Berger, M.; Finkbeiner, M. Water footprinting: How to address water use in life cycle assessment? Sustainability 2010, 2, 919–944. [Google Scholar] [CrossRef]

- Finkbeiner, M.; Inaba, A.; Tan, R.B.H.; Christiansen, K.; Klüppel, H.J. The New International Standards for Life Cycle Assessment: ISO 14040 and ISO 14044. Int. J. Life Cycle Assess. 2006, 11, 80–85. [Google Scholar] [CrossRef]

- Environmental Management—Life Cycle Assessment—Principles and Framework (ISO 14040); ISO: Geneva, Switzerland, 2006.

- Environmental Management—Life Cycle Assessment—Requirements and Guidelines (ISO 14044); ISO: Geneva, Switzerland, 2006.

- Oeko-Institut. Produktlinienanalyse; Kölner Volksblatt Verlag: Cologne, Germany, 1987. [Google Scholar]

- O’Brian, M.; Doig, A.; Clift, R. Social and Environmental Life Cycle Assessment (SELCA). Int. J. Life Cycle Assess. 1996, 1, 231–237. [Google Scholar] [CrossRef]

- Kloepffer, W. Life-Cycle Based Sustainability Assessment as Part of LCM. In Proceedings of the 3rd International Conference on Life Cycle Management, Zurich, Switzerland, 27–29 August 2007.

- Kloepffer, W. Life Cycle Sustainability Assessment of Products. Int. J. Life Cycle Assess. 2008, 13, 89–95. [Google Scholar] [CrossRef]

- Finkbeiner, M. Produkt-Ökobilanzen—Methode und Anwendung. In TÜV-Umweltmanagement-Berater; Myska, M., Ed.; TÜV Media: Cologne, Germany, 1999; pp. 1–20. [Google Scholar]

- Publications of the UNEP/SETAC Life Cycle Initiative; UNEP: Nairobi, Kenya, 2010; Available online: http://lcinitiative.unep.fr (accessed on 15 August 2010).

- Publications of the European Platform of LCA Including the ILCD Handbook; European Commission: Brussels, Belgium, 2010; Available online: http://lct.jrc.ec.europa.eu/publications (accessed on 15 August 2010).

- Eyerer, P. Ganzheitliche Bilanzierung—Werkzeug zum Planen und Wirtschaften in Kreisläufen; Springer: Heidelberg, Switzerland, 1996. [Google Scholar]

- Finkbeiner, M.; Saur, K. Ganzheitliche Bewertung in der Praxis. In Ökologische Bewertung von Produkten, Betrieben und Branchen; Symposium Bundesministerium für Umwelt, Jugend und Familie Österreich: Vienna, Austria, 1999. [Google Scholar]

- Wübbenhorst, K.L. Konzept der Lebenszykluskosten. Grundlagen, Problemstellungen und technologische Zusammenhänge; Verlag für Fachliteratur: Darmstadt, Germany, 1984. [Google Scholar]

- Kaufman, R.J. Life cycle costing: A decision-making tool for capital equipment acquisition. Cost Manag. 1970, March-April, 21–28. [Google Scholar]

- Zehbold, C. Lebenszykluskostenrechnung; Gabler: Wiesbaden, Germany, 1996. [Google Scholar]

- Franzeck, J. Methodik der Lebenszykluskostenanalyse und-planung (Life Cycle Costing) für die Entwicklung technischer Produktsysteme unter Berücksichtigung umweltlicher Effekte; University Stuttgart: Stuttgart, Germany, 1997. [Google Scholar]

- Hunkeler, D.; Lichtenvort, K.; Rebitzer, G. Environmental Life Cycle Costing; CRC Press: Boca Raton, FL, USA, 2008. [Google Scholar]

- Bubeck, D. Life Cycle Costing (LCC) im Automobilbau; Verlag Dr. Kovac: Hamburg, Germany, 2002. [Google Scholar]

- Global Reporting Initiative: Sustainability Reporting Guidelines; GRI: Boston, MA, USA, 2002.

- Jørgensen, A.; Le-Boqc, A.; Nazakina, L.; Hauschild, M. Methodologies for social life cycle assessment. Int. J. Life Cycle Assess. 2008, 13, 96–103. [Google Scholar] [CrossRef]

- Jørgensen, A.; Hauschild, M.; Jørgensen, M.; Wangel, A. Relevance and feasibility of social life cycle assessment from a company perspective. Int. J. Life Cycle Assess. 2009, 14, 204–214. [Google Scholar] [CrossRef]

- Jørgensen, A.; Finkbeiner, M.; Jørgensen, M.S.; Hauschild, M.Z. Defining the baseline in social life cycle assessment. Int. J. Life Cycle Assess. 2010, 15, 376–384. [Google Scholar] [CrossRef]

- UNEP. Guidelines for Social Life Cycle Assessment of Products; UNEP-SETAC Life-Cycle Initiative: Paris, France, 2009. [Google Scholar]

- Finkbeiner, M.; Günzel, U. Analyse von Methoden zur sozialen Produktbewertung und Verwendbarkeit im Kontext von Ökobilanzen; DaimlerChrysler AG: Stuttgart, Germany, 2005. [Google Scholar]

- UNDP. Human Development Report 2010. Available online: http://hdr.undp.org. (accessed on 20 August 2010).

- Gini, C. Measurement of inequality of incomes. Econ. J. 1921, 31, 124–126. [Google Scholar] [CrossRef]

- United Nations Global Compact Homepage. http://www.unglobalcompact.org (accessed on 20 August 2010).

- Schuh, H. Entscheidungsverfahren zur Umsetzung einer nachhaltigen Entwicklung; Dresdner Beiträge zur Betriebswirtschaftslehre: Dresden, Germany, 2001. [Google Scholar]

- Günther, E.; Schuh, H. Nachhaltige Entwicklung—eine Herausforderung für unternehmerische Entscheidungen: Wahrnehmung von Verantwortung als Voraussetzung einer nachhaltigen Entwicklung. In Quantitative Modelle und nachhaltige Ansätze der Unternehmungsführung; Physica: Heidelberg, Germany, 2003; pp. 199–214. [Google Scholar]

- Traverso, M.; Finkbeiner, M. Life Cycle Sustainability Dashboard. In Proceedings of the 4th International Conference on Life Cycle Management, Cape Town, South Africa, 6–9 September 2009.

- Hofstetter, P.; Braunschweig, A.; Mettier, T.; Müller-Wenk, R.; Tietje, O. The Mixing Triangle: Correlation and Graphical Decision Support for LCA-based Comparisons. J. Ind. Ecol. 1999, 3, 97–115. [Google Scholar]

- Hardi, P.; Semple, P. The Dashboard of Sustainability—From a Metaphor to an Operational Set of Indices. In Proceedings of the Fifth International Conference on Social Science Methodology, Cologne, Germany, 3–6 October 2000.

- Jesinghaus, J. On the Art of Aggregating Apples & Oranges; Fondazione Eni Enrico Mattei: Milan, Italy, 2000. [Google Scholar]

© 2010 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/3.0/).

Share and Cite

Finkbeiner, M.; Schau, E.M.; Lehmann, A.; Traverso, M. Towards Life Cycle Sustainability Assessment. Sustainability 2010, 2, 3309-3322. https://doi.org/10.3390/su2103309

Finkbeiner M, Schau EM, Lehmann A, Traverso M. Towards Life Cycle Sustainability Assessment. Sustainability. 2010; 2(10):3309-3322. https://doi.org/10.3390/su2103309

Chicago/Turabian StyleFinkbeiner, Matthias, Erwin M. Schau, Annekatrin Lehmann, and Marzia Traverso. 2010. "Towards Life Cycle Sustainability Assessment" Sustainability 2, no. 10: 3309-3322. https://doi.org/10.3390/su2103309

APA StyleFinkbeiner, M., Schau, E. M., Lehmann, A., & Traverso, M. (2010). Towards Life Cycle Sustainability Assessment. Sustainability, 2(10), 3309-3322. https://doi.org/10.3390/su2103309