Value Chain Opportunities for Pacific Coastal Resources

Abstract

1. Introduction

2. Method

3. Results and Discussion

3.1. Beche-de-Mer (Sea Cucumber)

3.2. Ornamental Black Pearls and Trochus Shell

3.3. Coastal Fisheries for the Domestic Market

3.4. Reef Fish Exports

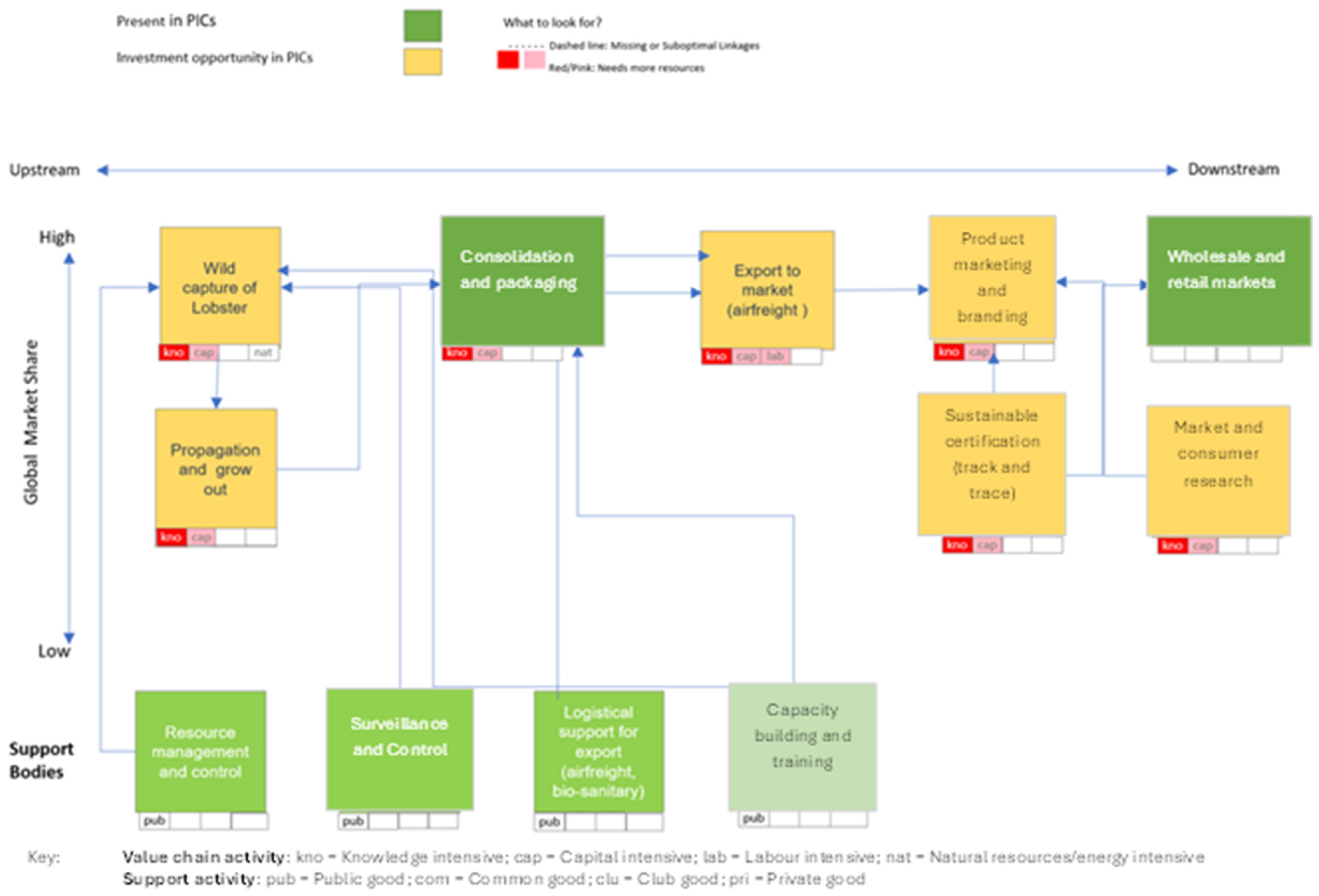

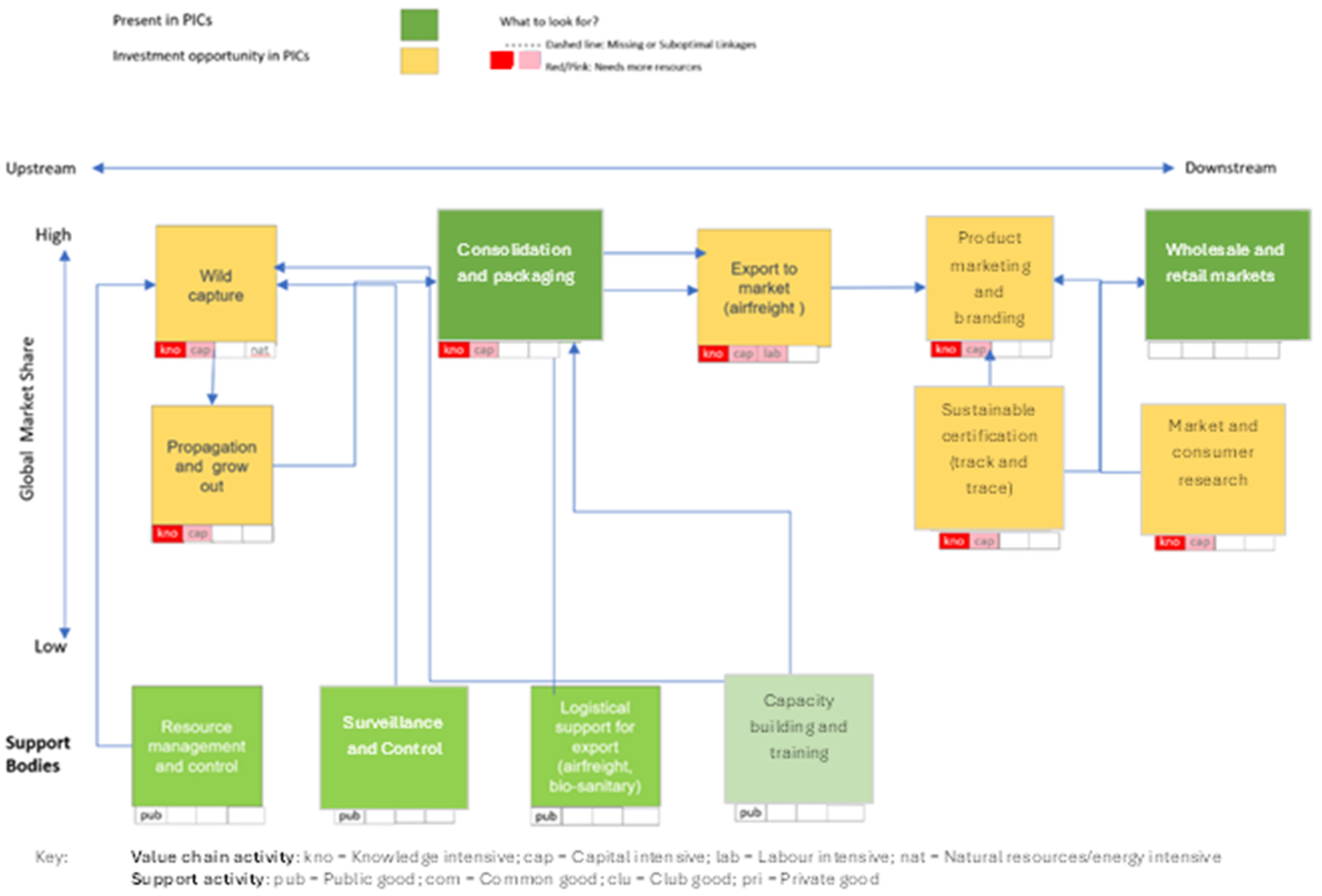

3.5. Live Lobster Export to Premium Markets

3.6. Export of Aquarium Products

3.7. Strategic Repositioning

3.7.1. Data Limitation for Sustainable Management

3.7.2. Governance and Management

3.7.3. Reallocation of Public Finance for Fisheries Management

3.7.4. Increasing Production from Coastal Fisheries for Food Security

3.7.5. Aquaculture, Cultivation, and Fishery Supplementation Programmes

3.7.6. Facilitating Market Access for Exports

3.8. Recommendations for External Development Support

- (i)

- Beche-de-mer: Efforts and initiatives that address the boom-and-bust exploitation of fisheries should be supported, particularly efforts concerning sustainable management and restocking and aquaculture programmes. Developing standardisation and training programmes surrounding the specific processing involved with the production of premium beche-de-mer is recommended.

- (ii)

- Coastal fisheries (fresh for domestic market): Efforts and initiatives that support fisheries data collection is essential for the required stock assessments for fisheries management to improve the supply of the resource. Support for infrastructure related to the development of the cold chain across PICs will improve supply by reducing post-production losses and spoilage while satisfying consumer preferences.

- (iii)

- Export of live reef fish: The establishment of sustainable fisheries management programmes is needed (including data on the fisheries). Initiatives that centre on habitat restoration to increase fish biomass are recommended due to the potential variety of reef species preferred by offshore markets. Further support can be directed to facilitating collaboration between local fishing stakeholders and foreign operators for market access.

- (iv)

- Export of aquarium products: The establishment of community management plans is needed to manage resources and prevent over exploitation. The establishment of efficient air freight connections can facilitate value chain participation where it does not exist. Further support in facilitating market connections and relationships with buyers in the USA has significant potential for success.

Supplementary Materials

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- FFA. FFA 2023 Tuna Economic Indicators Brochure. 2023. Available online: https://www.ffa.int/publications-and-statistics/statistics/ (accessed on 26 September 2024).

- SPC. Future of Fisheries: Coastal Fishery Report Card 2023. The Pacific Community. 2023. Available online: https://www.spc.int/DigitalLibrary/Doc/FAME/Brochures/SPC_2023_Coastal_Fishery_Report_Card.pdf (accessed on 26 September 2024).

- Gillett, R.; Fong, M. Fisheries in the Economies of Pacific Island Countries and Territories (Benefish Study 4); Digital Resource; Pacific Community: Noumea, New Caledonia, 2023; Available online: https://www.spc.int/DigitalLibrary/Doc/FAME/Manuals/Gillett_23_Benefish4.html (accessed on 30 September 2024).

- Siaosi, F.; Huang, H.W.; Chuang, C.T. Fisheries development strategy for developing Pacific Island Countries: Case study of Tuvalu. Ocean Coast. Manag. 2012, 66, 28–35. [Google Scholar] [CrossRef]

- Breckwoldt, A.; Seidel, H. The need to know what to manage—Community-based marine resource monitoring in Fiji. Curr. Opin. Environ. Sustain. 2012, 4, 33–337. [Google Scholar] [CrossRef]

- Friedlander, A.M.; Nowlis, J.; Koike, H. Improving fisheries assessments using historical data. Mar. Hist. Ecol. Conserv. Appl. Past Manag. Future 2014, 24, 91. [Google Scholar]

- Teh, L.C.; Teh, L.S.; Starkhouse, B.; Sumaila, U.R. An overview of socio-economic and ecological perspectives of Fiji’s inshore reef fisheries. Mar. Policy 2009, 33, 807–817. [Google Scholar] [CrossRef]

- Dick, E.J.; MacCall, A.D. Estimates of Sustainable Yield for 50 Data-Poor Stocks in the Pacific Coast Groundfish Fishery Management Plan; NMFS (National Marine Fisheries Service): Silver Spring, MD, USA, 2010. [Google Scholar]

- Lapres, B.E. A Strategic Segmentation of the Horticulture Sector Fruits and Vegetables; Global Value Chain Policy Series Report; World Bank: Washington, DC, USA, 2018. [Google Scholar]

- Mckenna, J.M. Strategic Segmentation Analysis: Nepal: Medicinal and Aromatic Plants (English); World Bank Group: Washington, DC, USA, 2019; Available online: http://documents.worldbank.org/curated/en/496421556737648658/Medicinal-and-Aromatic-Plants (accessed on 3 November 2024).

- Lapres, B.E. Report on Strategic Segmentation: Health Services and New Methods of Preventive Medicine and Diagnostics (English); World Bank Group: Washington, DC, USA, 2021; Available online: http://documents.worldbank.org/curated/en/962501632387221549/Report-on-Strategic-Segmentation-Health-Services-and-New-Methods-of-Preventive-Medicine-and-Diagnostics (accessed on 3 November 2024).

- Yap, J. Intelligent Transport Systems and Logistics: Report on Strategic Segmentation (English); World Bank Group: Washington, DC, USA, 2021; Available online: http://documents.worldbank.org/curated/en/320221632394692662/Intelligent-Transport-Systems-and-Logistics-Report-on-Strategic-Segmentation (accessed on 3 November 2024).

- Onugha, I. A Strategic Segmentation of the Beef Sector; Global Value Chain Policy Series Report; World Bank: Washington, DC, USA, 2018. [Google Scholar]

- Yap, J.; Kilroy, A.; Trpkov, S.E.; Punda, P.; Duch Navarro, E.; De Paiva Dias, M.I.; Varlec, D.; Saric, D.; Bosnjak, K.; Micic, J.; et al. Report on Strategic Segmentation: Energy Technology, Systems, and Equipment-Croatia Competitiveness Reinforcement Initiative (English); World Bank Group: Washington, DC, USA, 2017; Available online: http://documents.worldbank.org/curated/en/946431632387017993/Report-on-Strategic-Segmentation-Energy-Technology-Systems-and-Equipment-Croatia-Competitiveness-Reinforcement-Initiative (accessed on 4 November 2024).

- Weber, M.; Salhab, J. Value Chain Development for Jobs in Lagging Regions-Let’s Work Program in Tunisia: Overview of the Approach, Impact, and Findings; World Bank: Washington, DC, USA, 2020. [Google Scholar]

- Porter, M.E. How Competitive Forces Shape Strategy. Harvard Business Review. Available online: https://hbr.org/1979/03/how-competitive-forces-shape-strategy (accessed on 7 January 2024).

- Porter, M. The Five Competitive Forces That Shape Strategy. Harvard Business Review. Available online: https://hbr.org/2008/01/the-five-competitive-forces-that-shape-strategy (accessed on 7 January 2024).

- Pringle, J.; Huisman, J. An Industry Analysis Using Porter’s Five Forces Framework. Ont. Univ. Anal. 2011, 41, 36–58. [Google Scholar]

- Purcell, S.W.; Lovatelli, A.; Pakoa, K. Constraints and solutions for managing Pacific Island sea cucumber fisheries with an ecosystem approach. Mar. Policy 2014, 45, 240–250. [Google Scholar] [CrossRef]

- Andréfouët, S.; Charpy, L.; Lo-Yat, A.; Lo, C. Recent research for pearl oyster aquaculture management in French Polynesia. Mar. Pollut. Bull. 2012, 65, 407–414. [Google Scholar] [CrossRef] [PubMed]

- Johnston, W.; Hine, D.; Southgate, P.C. Overview of the development and modern landscape of marine pearl culture in the South Pacific. J. Shellfish. Res. 2019, 38, 499–518. [Google Scholar] [CrossRef]

- Purcell, S.W.; Tiitii, S.; Aiafi, J.; Tone, A.; Tony, A.; Lesa, M.; Esau, C.; Cullis, B.; Gogel, B.; Seinor, K.D.C.; et al. Ecological and socioeconomic impacts of trochus introductions to Samoa. SFC Fish. Newsl. 2019, 160, 36–40. [Google Scholar]

- Cuetos-Bueno, J.; Houk, P. Disentangling economic, social, and environmental drivers of coral-reef fish trade in Micronesia. Fish. Res. 2018, 199, 263–270. [Google Scholar] [CrossRef]

- Gillett, R.; Tauati, M. Fisheries of the Pacific Islands: Regional and National Information; FAO: Rome, Italy, 2018. [Google Scholar]

- Gillett, R.; Lewis, A.; Cartwright, A. Coastal Fisheries in Fiji; David and Lucille Packard Foundation: Suva, Fiji, 2014. [Google Scholar]

- Gillett, R.; McCoy, M.A.; Bertram, I.; Kinch, J.; Desurmont, A.; Halford, A. Aquarium Products in the Pacific Islands: A Review of the Fisheries, Management and Trade; SPC: Noumea, New Caledonia, 2020; ISBN 978-982-00-1319-3. [Google Scholar]

- Barclay, K.M.; Satapornvanit, A.N.; Syddall, V.M.; Williams, M.J. Tuna is women’s business too: Applying a gender lens to four cases in the Western and Central Pacific. Fish Fish. 2022, 23, 584–600. [Google Scholar] [CrossRef]

- Singeo, A.; Ferguson, C.E.; Willyander, I.; Endress, R.; Bells, S.; Endress, B. Key Findings From Palau’s Gender and Marine Resources Assessment: Women and Men Both Important for Use, Management and Youth Empowerment. In Bulletin; Pacific: Noumea, New Caledonia, 2021; Volume 34, pp. 21–26. [Google Scholar]

- Fache, E.; Breckwoldt, A. Women’s Active Engagement with the Sea Through Fishing in Fiji. Anthropol. Forum 2024, 34, 186–208. [Google Scholar] [CrossRef]

- Gilchrist, H.; Rocliffe, S.; Anderson, L.G.; Gough, C.L. Reef fish biomass recovery within community-managed no take zones. Ocean Coast. Manag. 2020, 192, 105210. [Google Scholar] [CrossRef]

- Foo, S.A.; Walsh, W.J.; Lecky, J.; Marcoux, S.; Asner, G.P. Impacts of pollution, fishing pressure, and reef rugosity on resource fish biomass in West Hawaii. Ecol. Appl. 2021, 31, e2213. [Google Scholar] [CrossRef] [PubMed]

- Ceccarelli, D.M.; Lestari, A.P.; White, A.T. Emerging marine protected areas of eastern Indonesia: Coral reef trends and priorities for management. Mar. Policy 2022, 141, 105091. [Google Scholar] [CrossRef]

- Rojo, I.; Anadón, J.D.; García-Charton, J.A. Exceptionally high but still growing predatory reef fish biomass after 23 years of protection in a Marine Protected Area. PLoS ONE 2021, 16, e0246335. [Google Scholar] [CrossRef] [PubMed]

- Russ, G.R.; Rizzari, J.R.; Abesamis, R.A.; Alcala, A.C. Coral cover a stronger driver of reef fish trophic biomass than fishing. Ecol. Appl. 2021, 31, e02224. [Google Scholar] [CrossRef] [PubMed]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Commodity | Market Potential | Value Added | Job Creation | Competitiveness | Development Options | Priority |

|---|---|---|---|---|---|---|

| Beche-de-mer | Increased supply of premium product from sustainable fisheries from aquaculture | Considerable for superior processed product from preferred sea cucumber species; wide variation in the prices of the final product according to species, size, and quality | Low | High demand for a superior product | Standardisation of processing methods; supply of efficient targeted harvesting equipment; develop incentives for fishing methods and operations that conform to international standards for labour, health and safety, plastic waste management, sustainable fisheries management (certification); development of hatchery facilities to restock coastal fisheries with preferred species; provision of aquaculture facilities and supplies; support for regulation enforcement; support for sustainable management of fisheries; brand development through promotion of sustainably harvested products | High |

| Black pearls | Cultivated black pearls from the indigenous black-lipped oyster, largely marketed to tourists in French Polynesia and Fiji | High value added | Medium—management of farmed pearls is labour intensive | Black pearls compete with other pearl types internationally | Development and implementation of pearl farming community management plans and quality standards; oceanographic monitoring of environmental conditions for facilitating ideal culture conditions and developing sustainable farming practices; development of early warning systems to alert growers of adverse biological conditions and potential disease outbreaks; financial support for establishment of pearl farms; promotion and marketing of black pearls as a unique PIC product | Low |

| Trochus shell | Harvesting and export of Trochus shell for the manufacture of mother-of-pearl buttons | Low—most shell is exported in raw form as a low-value product | High—collection and handling of shell is labour intensive | Competition from other suppliers to a declining market | Community management plans to manage the resource and prevent over exploitation; regulation for sustainable fisheries management (permissible shell size, closed harvest seasons, permits, licencing); develop pilot projects, using existing knowledge in French Polynesia, that combine shell and algae production to tackle both biodiversity and climate change challenges | Low |

| Coastal fisheries (fresh) | Supply of fresh fish products from coastal fisheries to the domestic market threatened by over-exploitation | Support for data management and confirmation of resources, improved resource management, and support for fishing infrastructure to improve supply; cold chain to reduce post-production losses and facilitate transport and marketing | High—Large percentage of population involved with coastal fisheries; coastal fisheries largely local and artisanal | Low—The domestic market is self-contained | Support for data collection and analysis to accurately record production volumes and determine available resource for sustainable exploitation; support for community management of coastal fishery resource; support for fishing gear and fish aggregating devices (FADs), ice plants, and interventions to increase the supply and marketing of fishery products; supply of bycatch and trash fish from tuna oceanic fisheries to supplement domestic subsistence demand for fish in the PICs; development of pilot projects that create and regenerate natural habitats for increasing fish biomass production; enhanced awareness of interdependence between coastal habitats (and their quality) and fish abundance; enhanced coastal capacity to harvest higher value species (tuna and tuna-like species) | High |

| Coastal fishery products (processed) | Increase the shelf life and supply of fish for the local market through developing a cold chain and freezing, drying, and smoking | Low—Product for the domestic market | Medium | Low—Internal domestic market prefers fresh fish; processed fish products—canned fish and meat—compete with alternatives | Support for fishing gear and fish aggregating devices (FADs), ice plants, and interventions to increase the supply and marketing of fishery products; incentives for international businesses to set up processing facilities to supply the domestic market (duty-free access, tax holidays, repatriation of profits); develop community employment through training fish processing | Medium |

| Live reef fish exports | Large market in Hong Kong and China where favoured species (e.g., red coral trout) command high prices | Favoured species command high prices and high value-added potential | Fish are mostly captured by use of hand lines and traps to supply foreign carrier holding ships and foreign fishing vessels; good potential for involvement of local people | High competition among PICs despite small collective market share; competition with exports of coral trout from Australia from aquaculture | Sustainable local fisheries management programmes to develop resources (habitat restoration, establishment of protected areas and spawning grounds, closed seasons); non-destructive fishing methods or capture techniques that preserve the local environment and keep the resource intact; regulation of the fishery through public institutions for long-term extraction; establishment of licensing scheme to control extraction and for data collection to enable management; support monitoring and management of live fish capture through allocation of fishing access rights and observer programme; support for local fishing stakeholders to collaborate with foreign operators for market access; brand development when environmentally friendly or approved harvesting methodologies are used and for social benefit programmes that direct a portion of proceeds back to locals; marketing and promotion of PIC coastal fish as a unique product; sustainability certification of suppliers such as through the Marine Stewardship Council (MSC) | High |

| Lobster | Export of live lobsters to premium markets: China, Japan, and USA | Large value added for premium products | High level of job creation for local people in harvesting, transport, and marketing | High—Lobsters are also exported from New Zealand and Australia; PIC resources limited, of inferior quality, and vulnerable to over-exploitation | Efficient air freight connections and infrastructure; phytosanitary protocols and standards for export; support for the establishment of the resource and maximum sustainable yield for fisheries in local contexts; provision of training and support for the logistics of export of a live product to the marketplace; marketing and promotion of PIC lobsters as an attractive unique island product in the destination countries; consolidating regional export through a selected number of approved exporters to facilitate efficiency in the logistics and administration involved with exportation | Low |

| Aquarium products (ornamental fish, coral, live rock, and clams) | Strong global market with the USA as the main market | High value added to middlemen and exporters; important determinants of the cost structure are air freight costs, diver’s pay, electricity and holding and packaging costs. | Labour intensive for capture of wild fish | High—Major producers are Indonesia and the Philippines, accounting for most of USA imports; Pacific Islands’ competitive advantages are a relatively short supply chain, reputation for high quality, low mortality, and good availability | Training in knowledge of desired species and products; support for community management plans to manage the resource and prevent over exploitation; support for the facilitation of exports in compliance with CITES for some items (export certification); logistical support for establishment of efficient air-freight connections; facilitating good market connections and relationships with buyers in the USA | High |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bennett, M.; March, A.; Greer, R.; Failler, P. Value Chain Opportunities for Pacific Coastal Resources. Sustainability 2025, 17, 1103. https://doi.org/10.3390/su17031103

Bennett M, March A, Greer R, Failler P. Value Chain Opportunities for Pacific Coastal Resources. Sustainability. 2025; 17(3):1103. https://doi.org/10.3390/su17031103

Chicago/Turabian StyleBennett, Michael, Antaya March, Ray Greer, and Pierre Failler. 2025. "Value Chain Opportunities for Pacific Coastal Resources" Sustainability 17, no. 3: 1103. https://doi.org/10.3390/su17031103

APA StyleBennett, M., March, A., Greer, R., & Failler, P. (2025). Value Chain Opportunities for Pacific Coastal Resources. Sustainability, 17(3), 1103. https://doi.org/10.3390/su17031103