Driving Mechanism of Greening Corporate Environmental Behaviour Under the “Dual-Carbon” Goal: A Study Based on Grounded Theory Study

Abstract

1. Introduction

2. Literature Review

3. Method and Data

3.1. Research Method

3.2. Data Sources

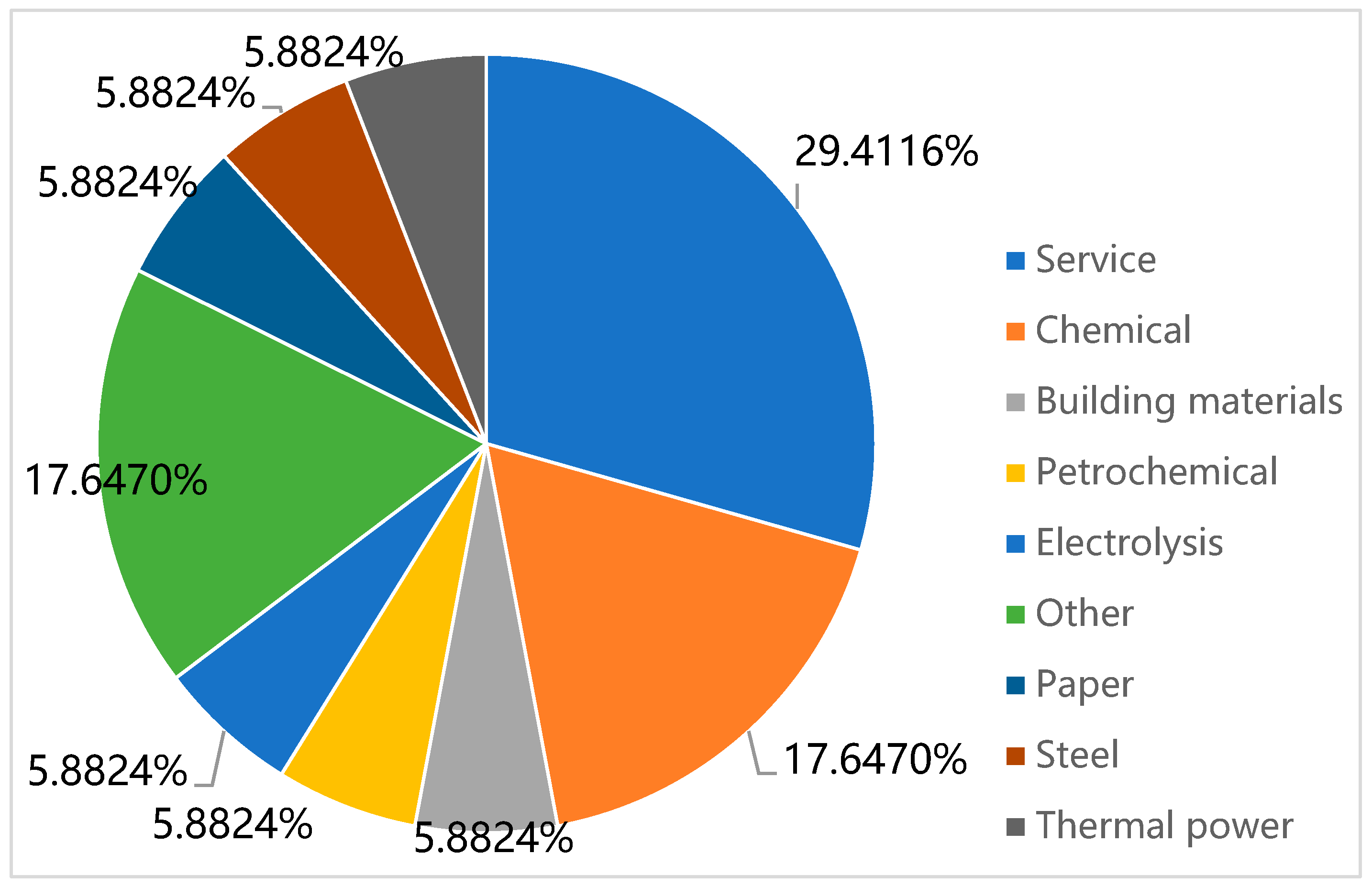

3.2.1. Acquisition of Data

3.2.2. Organisation of Data

3.3. Data Analysis

3.3.1. Open Coding

3.3.2. Axial Coding

3.3.3. Selective Coding

3.3.4. Saturation Test

4. Result Analysis

4.1. Macro to Micro Multidimensional Drivers

- Micro-firm level factors

- 2.

- Macro-environmental level factors

- 3.

- Meso-industry level factors

4.2. Willingness of Enterprises to Make Green Changes

4.3. Corporate Green Change Behaviour

5. Conclusions and Discussion

5.1. Conclusions

- Under the “dual-carbon” goal, the green change of heavily polluting and high-energy-consuming enterprises is taking the form of specific behaviours. These behavioural changes are the responses of Chinese enterprises which are seeking to achieve the “dual-carbon” goal and satisfy high-quality development requirements. Changes come in the form of two specific behaviours: the strategic change of green management and the development and optimisation of cleaner production practices. Moreover, green changes in corporate environmental behaviour can be both active and passive. The ultimate goal is to achieve the long-term, sustainable green and low-carbon development goals of the enterprise itself.

- Under the “dual-carbon” goal, the willingness of enterprises to make green changes is driven by the interaction of internal and external factors on multiple levels. Influencing factors on the macro-, meso-, and micro-levels jointly influence enterprises’ willingness to make green changes. The current state of an enterprise, including resources, financial situation, the awareness of the enterprise’s management of low-carbon transition, and the enterprise’s own technological capability, greatly influence the enterprise’s willingness to change. This works in synergy with external policies, regulation, and other factors that are necessary for the development of the industry.

- Under the “dual-carbon” goal, enterprises’ green change willingness leads to the emergence of green change behaviour. An enterprise as an independently developing whole can often be seen as an individual with a collective consciousness. In the Theory of Planned Behaviour, it is believed that an individual’s behaviour is primarily influenced by willingness; the stronger his or her willingness, the higher the likelihood that he or she will perform a particular behaviour [48]. In an individual or in a business, behaviour is easily and directly influenced by a willingness to grow. If enterprises are to take prompt actions, promote low-carbon behavior, and achieve long-term transformation, they must maintain and enhance their determination to make changes.

5.2. Management Implications

- Taking into account green market demand and competition and in efforts to meet the expectations of the public, the concept of green consumption should be promoted at the level of the whole society. By fulfilling their social responsibilities (such as green brand marketing), enterprises can shape their public image, which can enhance consumer loyalty, making green and low-carbon products the preferred choice for consumers. At the same time, companies would build a green and low-carbon image to attract green cooperation.

- Institutions exert a binding influence on organisations, forcing firms located in the same system and influenced by the same external institutional factors to converge in terms of their behaviour. Therefore, policy incentives and constraints could be strengthened. On the one hand, policy regulations should be used to guide enterprises in changing their development direction. This would stimulate them to independently favour a lower-carbon and greener way of development by means of financial subsidies and tax incentives. On the other hand, responsibility for carbon emissions has been clarified through the enactment of laws. Legislation has further provided control requirements. Enterprises are required to comply with the carbon emissions data reporting, verification, and quota system and face administrative penalties or financial liabilities for violations. Enterprises need to embed emission reductions targets in their strategic planning or risk losing market access.

- Based on the Theory of Resource Allocation, enterprises should enhance their willingness to carry out green transformation. They should invest more funds in energy-saving and emission-reduction projects to ensure that resources are directed towards sustainable business. In this way, bridges for the research and development cooperation among schools and enterprises could be established. A channel would be opened up for technical exchanges and learning between schools and enterprises, or among enterprises.

- Based on the Resource-Based view, enterprises can internalise green changes into their strategic resources and maximise differentiated advantages in terms of their development. By conducting research and development of clean production technologies and optimising energy efficiency, the carbon emissions per unit output can be reduced, thereby creating a cost advantage. Companies could also participate in the carbon trading market and obtain profit through excess quotas. Additionally, the carbon universal mechanism could be utilised to attract green investment and enhance capital market valuation. Within an enterprise, the establishment of a long-term strategic plan, rational allocation of resources, and the active training of professionals would all promote green change.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Yu, B.; Ding, P. Coal utilization’s impact on the negative externalities of urban environment. Environ. Eng. 2016, 34, 1166–1168. [Google Scholar]

- Yu, F.W.; Lin, S. Promotion Strategies of Green Transformation and Development of Enterprises Under the “Dual Carbon” Goal. Reform 2022, 2, 144–155. [Google Scholar]

- Hariyani, D.; Mishra, S.; Sharma, M.K.; Hariyani, P. Organizational Barriers to the Sustainable Manufacturing System: A Literature Review. Environ. Chall. 2022, 9, 100606. [Google Scholar] [CrossRef]

- Zhuang, G.Y. The Consumption Responsibility and Policy Suggestions under the Guidance of the Target of Carbon Neutralization. People’s Forum-Acad. Front. 2021, 14, 62–68. [Google Scholar]

- Li, Y.H.; Wang, H.G.; Xiao, X.W. Research on Carbon Emission Prediction and Emission Reduction Pathways in Jiangxi Province Based on System Dynamics. Ecol. Environ. Sci. 2025. Available online: http://kns.cnki.net/kcms/detail/44.1661.x.20250402.1438.010.html (accessed on 3 April 2025).

- Yan, J.; Li, M.; Han, H.P. Green Development and Carbon Reduction: Interprovincial Pathways in China Based on Dynamic Time Planning. Price Theory Pract. 2024, 11, 38–43. [Google Scholar]

- Jens, H.; Christian, R.; Klaus, R.N. Determinants of eco-innovations by type of environmental impact—The role of regulatory push/pull, technology push and market pull. Ecol. Econ. 2014, 78, 112–122. [Google Scholar]

- Jin, G.; Guo, B.S.; Deng, X.Z. Is there a decoupling relationship between CO2 emission reduction and poverty alleviation in China? Technol. Forecast. Soc. Change 2020, 151, 119856. [Google Scholar] [CrossRef]

- Liu, Y.; Du, M.; Yang, L.; Cui, Q.; Liu, Y.; Li, X.; Zhu, N.; Li, Y.; Jiang, C.; Zhou, P.; et al. Mitigation policies interactions delay the achievement of carbon neutrality in China. Nat. Clim. Change 2025, 15, 147–152. [Google Scholar] [CrossRef]

- Nazir, M.J.; Li, G.L.; Nazir, M.M.; Zulfiqar, F.; Siddique, K.H.M.; Lqbal, B.; Du, D.L. Harnessing soil carbon sequestration to address climate change challenges in agriculture. Soil Tillage Res. 2024, 237, 105959. [Google Scholar] [CrossRef]

- Zhang, Y.; Huang, Q.Z.; Li, D.D.; Deng, W. A Configuration Analysis of Corporate Environmental Information Disclosure and Low-carbon Production Behavior from the Perspective of Stakeholders. Soft Sci. 2024, 38, 15–21. [Google Scholar]

- He, Z.X.; Xu, S.C.; Shen, W.H.; Long, R.Y.; Chen, H. Factors that influence corporate environmental behavior Lempieial analysis based on panel data in China. J. Clean. Prod. 2016, 133, 531–543. [Google Scholar] [CrossRef]

- Li, W.A.; Wang, Q.; Niu, J.B. Research Review and Prospect on Driving Forces of Corporate Green Behavior. East China Econ. Manag. 2023, 37, 1–10+137. [Google Scholar]

- Li, C.F. Corporate environmental management motivation, behaviour and performance-A literature-based institutional analysis framework construction. Financ. Account. Mon. 2023, 44, 23–31. [Google Scholar]

- Wu, L.; Yu, Q.H.; Ping, L. The Roles and Limitations of Voluntary Environmental Regulation in the Green Transformation of Chinese Manufacturing Firms. Financ. Trade Econ. 2023, 44, 140–156. [Google Scholar]

- Wang, Y.L.; Ming, Z. The role of environmental justice: Environmental courts, analysts’ earnings pressure and corporate environmental governance. Environ. Impact Assess. Rev. 2023, 104, 107–299. [Google Scholar] [CrossRef]

- Wang, J.; Fan, M.Z.; Lin, H. Environmental Governance Effect of Executive Equity Incentive: Be Worthy of the Name or a Mere Facade? Empirical Evidence Based on A-share High-pollution Enterprises. J. Financ. Econ. 2023, 49, 50–64. [Google Scholar]

- Lin, C.Y.; Ho, Y.H. The influences of environmental uncertainty on corporate green behavior: An empirical study with small and medium-size enterprises. Soc. Behav. Personal. Int. J. 2010, 38, 691–696. [Google Scholar] [CrossRef]

- Zhong, X.M.; Lou, L.; Lu, J.K. China’s Environmental Protection Tax Law and Corporate Environmental Responsibility: Policy Effects and the Conditions. Economist 2023, 8, 107–116. [Google Scholar]

- Dimaggio, P.; Powell, W. The ironcage revisited: Institutional isomorphism and collective rationality in organizational fields. Am. Sociol. Rev. 1983, 48, 147–160. [Google Scholar] [CrossRef]

- Bian, C.; Chu, Z.P.; Sun, Z.L. Media Coverage and Earnings Management of Commercial Banks. Manag. Rev. 2022, 34, 122–133. [Google Scholar]

- Tian, J.Z.; Kam, C.C. Corporate social network and corporate social responsibility: A perspective of interlocking directorates. Int. Rev. Financ. Anal. 2023, 7, 102711. [Google Scholar]

- Lanioe, P.; Laplante, B.; Roy, M. Can capital markets create incentives for pollution control. Ecol. Econ. 1998, 26, 31–41. [Google Scholar] [CrossRef]

- Wang, J.X.; Liu, X.R.; Yin, N. Research on the Relationship between Public Supervision and Green Environmental Performance of Enterprises. Econ. Issues 2020, 8, 70–77. [Google Scholar]

- Yannick, B.; Paul, H. Ecological community logics, identifiable business ownership, and green innovation as a company response. Res. Policy 2023, 52, 104826. [Google Scholar]

- Fan, R.G.; Wang, Y.T.; Chen, F.Z.; Du, K.; Wang, Y.Y. How do government policies affect the diffusion of green innovation among peer enterprises?—An evolutionary-game model in complex networks. J. Clean. Prod. 2022, 364, 132711. [Google Scholar] [CrossRef]

- Li, Z.; Huang, Z.; Su, Y. New media environment, environmental regulation and corporate green technology innovation: Evidence from China. Energy Econ. 2023, 119, 106545. [Google Scholar] [CrossRef]

- Zhang, J.P.; Li, L.Z. An empirical study on the impact of green finance and green policies on the green transformation of entity enterprises. China Popul.·Resour. Environ. 2023, 33, 47–60. [Google Scholar]

- Sun, J.; Zhai, N.N.; Miao, J.C.; Sun, H.P. Can green finance effectively promote the carbon emission reduction in “local-neighborhood” areas?—Empirical evidence from China. Agriculture 2022, 12, 1550. [Google Scholar] [CrossRef]

- Cui, X.J. Carbon emissions trading policy, technological change and green transformation of iron and steel enterprises. Account. Newsl. 2023, 20, 76–80+120. [Google Scholar]

- Wu, M.Y.; Zhang, L.R. Research on Attributes of Top Management Team, Environmental Responsibility and Corporate Value. East China Econ. Manag. 2018, 32, 122–129. [Google Scholar]

- Xing, L.Y.; Yu, H.X. Research on the Impact of Green Dynamic Ability on Environmental Innovation—The Moderating Effect of Environmental Regulation and Top Managers’ Environ amental Awareness. Soft Sci. 2020, 34, 26–32. [Google Scholar]

- Su, L.J.; Scott, R.S. Perceived corporate social responsibility’s impact on the well-being and supportive green behaviors of hotel employees: The mediating role of the employee-corporate relationship. Tour. Manag. 2019, 72, 437–450. [Google Scholar] [CrossRef]

- Wang, Y.; Li, X. Major Shareholders’ Shareholding and Corporate Environmental Protection Investment Methods: An Empirical Study Based on Listed Companies in China. Friends Account. 2022, 13, 76–81. [Google Scholar]

- Glaser, B.G.; Strauss, A.L. The Discovery of Grounded Theory: Strategies for Qualitative Research; Aldine Publishing Company: Chicago, IL, USA, 1967; pp. 1–282. [Google Scholar]

- Lv, J.; Zhang, S.Q.; Wang, Y.; Yang, M.J. Research on the Driving Mechanism of Green Innovation Intention of Energy Enterprises Based on Grounded Theory. Sci. Technol. Prog. Policy 2019, 36, 104–110. [Google Scholar]

- Suddaby, R. From the Editors: What Grounded Theory is Not. Acad. Manag. J. 2006, 49, 633–642. [Google Scholar] [CrossRef]

- Ren, X.W.; Sun, L.W.; Xing, L.Y. An Exploratory Research on the Two-Stages Evolutionary Process of Green Transformation of Resource-Based Enterprise Based on Grounded Theory: A Case of HBIS Group. Sci. Technol. Prog. Policy 2022, 39, 70–78. [Google Scholar]

- Zhou, D.L.; Yang, X. The Influencing Factors and Realization Path of the Digital Transformation of Enterprise Finance: An Exploratory Research Based on Grounded Theory. J. Manag. Case Stud. 2023, 16, 613–626. [Google Scholar]

- Eisenhardt, K.M. Building theories from case study research. Acad. Manag. Rev. 1989, 14, 532–550. [Google Scholar] [CrossRef]

- Guo, Y.X. Qualitative Research Data Analysis: Nvivo 8 Active Use Handbook; Higher Education Press: Taipei, Taiwan, 2009; pp. 1–147. [Google Scholar]

- Liu, J.H.; Pu, J.M. Research on New Energy Automotive Collaborative Innovation Strategy Based on the Grounded Theory: The Case Study of Yutong. Sci. Technol. Prog. Policy 2017, 34, 51–56. [Google Scholar]

- Han, L.L.; Wang, H.M. The Mechanism and Path of Green Transformation for Automobile Enterprises under High-Quality Development: A Case Study of BYD. Financ. Account. Mon. 2025, 46, 94–100. [Google Scholar]

- Yang, Y.M.; Huang, J.H.; Li, H.L. Environmental Protection Tax Law and Regional Green Transformation: Mechanisms and Effects. Financ. Account. Mon. 2024, 45, 102–109. [Google Scholar]

- Zhu, J.S.; Liu, Y.Y.; Zheng, X. Does Peers’ Green Transformation Force Enterprises Toward Green Innovation: A Text-Mining-Based Analysis on Spillover Effects. J. Syst. Manag. 2025. Available online: http://kns.cnki.net/kcms/detail/31.1977.N.20241227.1714.002.html (accessed on 30 December 2024).

- Bi, P.X. Executive-Level Green Awareness, Digital Transformation and Corporate Green Investments: An Analysis of Economic Consequences Based on ESG Performance. Commun. Financ. Account. 2025, 1, 50–53+58. [Google Scholar]

- Cooper, R.W.; Haltiwanger, J.C. On the nature of capital adjustment costs. Rev. Econ. Stud. 2006, 73, 611–633. [Google Scholar] [CrossRef]

- Ajzen, I. The theory of planned behavior. Organ. Behav. Hum. Decis. Process. 1991, 50, 179–211. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Characteristics | Quantities | % | |

|---|---|---|---|

| Location (China) | Eastern | 10 | 58.82% |

| Western | 7 | 41.18% | |

| Years | ≤5 | 1 | 5.89% |

| 5–10 | 5 | 29.41% | |

| 10–20 | 5 | 29.41% | |

| ≥20 | 6 | 35.29% | |

| Ownership | Share-holding | 3 | 17.65% |

| Private | 6 | 35.29% | |

| State | 5 | 29.41% | |

| Mixed | 1 | 5.89% | |

| Sino-foreign joint venture | 2 | 11.76% | |

| Number of employees | ≤20 | 1 | 5.89% |

| 20–300 | 6 | 35.29% | |

| 301–1000 | 6 | 35.29% | |

| ≥1000 | 4 | 23.53% | |

| Asset size (Monetary unit: RMB) | ≤3 million | 0 | 0 |

| 300–20 million | 1 | 5.89% | |

| 20.1–400 million | 6 | 35.29% | |

| ≥400 million | 10 | 58.82% | |

| Selected Source Statements | Initial Concept |

|---|---|

| “Reduce production costs so that your product is competitive in the market”. “… Because competition is greater now. Originally, it was our factory that was doing it on its own, and a lot of factories didn’t do that. Now, they are also learning, taking the waste slag and grinding it into ash. So now in the market, the first grade of ash is competitive, and everyone down there is doing superfine ash”. | Product Market Competition |

| “The waste is uniformly disposed of by our purchasing department to a qualified supplier with full authority… We are all classified, this waste is to be classified periodically, and we then let the supplier, let the qualified supplier come over to dispose of it”. “Like that solid waste, itself to be disposed of without comprehensive utilisation, the disposal of that has some costs, generating carbon dioxide… Then we make products, and this carbon dioxide is equivalent to an emission reduction”. | Optimisation of waste disposal |

| “The downstream companies have environmentally friendly gradings. Or low-carbon products, that is, production is said to be “green”, including my production process, which is green. Cleaner production-oriented, downstream companies are willing to use such a product”. “And then also the manufacturers downstream have requirements for them, i.e., that you can only buy as much carbon as you can buy. In that case, it’s a reverse and forward push”. | Downstream business attitudes |

| “There’s the energy saving aspect, and then there’s through cooperation with other people’s companies… An energy enterprise puts solar panels on our side, and then sells us the electricity that’s generated from that, which is lower than the market price, …” “Like on our own, we basically work with other people. You pay money to invest in equipment and make technical improvements, and then I’ll use yours and just pay again…” | Inter-enterprise cooperation |

| “This business itself requires the business to be energy efficient”. “And then there’s also some of head office consistency, which is another requirement…” | Management requirements |

| Area | Source (Quantities) | Initial Concept (Frequency) |

|---|---|---|

| A01 Resource Base | 31 | Production conditions (18), Project transformation conditions (93), Financial conditions (31) |

| A02 Policy Regulation | 24 | Policy standards (42), National macro requirements (9), Emission requirements (7) |

| A03 Industry Pressures | 29 | Industry competitive pressures (31), Industry requirements (25), Peer green behaviour (15) |

| A04 Green Cooperation | 22 | Inter-enterprise cooperation (35), University-enterprise industry-academia-research cooperation (6), Third-party agency cooperation (7) |

| A05 Innovation Optimisation | 25 | Optimisation of waste disposal (23), Optimisation of energy recovery (10), Optimisation of recycling technologies (43) |

| A06 Regional level of green development | 10 | Regional energy base (7), Degree of regional promotion (4), Natural conditions (9) |

| A07 Management philosophy | 27 | Personnel management systems (17), Management requirements (39), Management decisions (7) |

| A08 Green competition in the marketplace | 12 | Product market competition (11), Green access requirements (4), Product verification requirements (3) |

| A09 Environmental Oversight | 30 | Public monitoring (32), Environmental policy (19), Environmental monitoring and verification (23) |

| A10 Strategic Change | 18 | Corporate identity (12), Procurement control (9), Transport control (3), Strategic development direction (72), Business strategy objectives (3), Business model planning (7) |

| A11 Policy Incentives | 23 | Financial subsidies (39), Publicity incentives (5), Technical support (5) |

| A12 Expected Returns | 26 | Return on investment (33), Product upgrade advantage (10), Cost reduction (17) |

| A13 Market Greening Requirements | 31 | International market demand (44), Consumer demand (48), Downstream business attitudes (34) |

| A14 Technical Capability | 27 | Autonomous transformation capacity (28), Autonomous research and development capacity (24), Autonomous monitoring capacity (14) |

| A15 Management’s willingness to change | 8 | Management attitudes (14) |

| Main Categories | Sub-Categories | Connotation |

|---|---|---|

| Micro-firm level factors (F) | A01 Resource Base | In-house resource acquisition, support, and reserves are fundamental to green change. |

| A12 Expected Returns | The desire of companies to achieve the goals of improving the efficiency of resource utilisation, increasing profits, and reducing costs is an important motivation for green change. | |

| A09 Management philosophy | The philosophies of business managers regarding important procedures such as management, decision-making, and appraisal will directly affect whether or not an enteprise can make a green change. | |

| A14 Technical Capability | The research and development of green and low-carbon technologies, as well as the technical talent, achievements, and transformation experience of enterprises are important technical guarantees for the green change of enterprises. | |

| Macro-environmental level factors (E) | A02 Policy Regulation | A series of regulations issued by the government is an important external factor for green change. |

| A11 Policy Incentives | A range of subsidy-supporting policies enacted by the government are important externalities for green change. | |

| A09 Environmental Oversight | Social scrutiny triggered by environmental problems of high emissions and pollution is one of the factors influencing the green change of enterprises. | |

| Meso-industry level factors (P) | A13 Market Greening Requirements | The propensity of consumers and upstream and downstream vendors to buy low-carbon products. The creation of a market for low-carbon products is a major reference for companies in terms of making green changes. |

| A08 Green competition in the marketplace | With an increase in market maturity, a change of traditional concepts makes high pollution, high carbon emissions, and a lack of environmental protection awareness in the development of enterprises liabilities; green change will bring new opportunities for the development of enterprises, placing companies in a more powerful position. | |

| A03 Industry Pressures | The requirements of the industry in which the enterprise operates and the behaviour of its peers are the main factors influencing its green change | |

| A04 Green Cooperation | Cooperative resource and technology sharing among enterprises will enable them to achieve higher green returns with less investment. | |

| Willingness of businesses to make green changes (W) | A15 Management’s willingness to change | Enterprises are willing to assume social responsibility, purchase new equipment, invest in new technologies, reform the original production process, carry out pollution control, recycle and reuse resources, and bear the risks brought about by the reform. |

| Regional level of green development (R) | A06 Regional level of green development | With an increase in market maturity, a change of traditional concepts makes high pollution, high carbon emissions, and a lack of environmental protection awareness in the development of enterprises liabilities; green change will bring new opportunities for the development of enterprises, placing companies in a more powerful position. |

| Green change behaviour in business (B) | A10 Strategic Change | Strategic change in enterprises is an important means of internalising the will for green change into organisations and systems. Driven by micro-, meso-, and macro-level factors, corporate management will make disruptive changes to the development paradigm which will necessarily involve steps in strategic planning, formulation, implementation, and adjustment so that it can always be integrated with the environment. |

| A05 Innovation Optimisation | Innovation and optimisation are important means of implementing green change behaviours in enterprises, and only through continuous innovation in products, production, and management, and optimisation of production and management processes can enterprises truly adapt to the current economic environment and successfully promote green behaviours. |

| Relationship Structure | Connotations | ||

|---|---|---|---|

| ① The first half of the green change: antecedent motives | Will to change | Green change willingness refers to an enterprise’s green behaviour under the “dual-carbon” target. It is the subjective willingness of an enterprise’s management to seek green and carbon-reducing development. | |

| Micro-firm level factors → Willingness of businesses to make green changes | Resource Base → Green change behaviour in business | The resource base refers to the financial and equipment status of an enterprise, as well as the support in terms of energy and relationships. It is the material basis on which the enterprise’s willingness to make a green change is formed. | |

| Expected Returns → Green change behaviour in business | Expected return is an enterprise’s measurement and consideration of the return situation after the change; the level of return will directly affect the formation of the enterprise’s degree of willingness to affect a green change. | ||

| Management Philosophy → Green change behaviour in business | The management philosophy of an enterprise always affects the internal operation logic of the enterprise in daily management, operation, assessment, etc., and has an important influence on the formation of a will to make green changes. | ||

| Technical Capability → Green change behaviour in business | Technological capability refers to the R&D capability of an enterprise’s technical team and represents the technological self-confidence and guarantee that promotes the formation of the enterprise’s willingness to make green changes. | ||

| Macro-environmental level factors → Willingness of businesses to make green changes | Policy Regulation → Green change behaviour in business | Policy regulation is the government, through the law, norms, and other administrative means; this can stimulate green change willingness. | |

| Policy Incentives → Green change behaviour in business | The government stimulates willingness to make green changes through policy incentives, tax subsidies, and technical assistance. | ||

| Environmental Oversight → Green change behaviour in business | Environmental supervision mainly stems from the concerns of the public, the supervision and verification efforts of the relevant departments, etc., which have a strong influence on the willingness of enterprises to make green changes | ||

| Meso-industry level factors → Willingness of businesses to make green changes | Market Greening Requirements → Green change behaviour in business | The green demand of the market and the huge market space it creates have a distinctive guiding effect on the green change of enterprises. | |

| Green competition in the marketplace → Green change behaviour in business | The demand for green and low-carbon products and a lack of competitiveness of original products will have an important impact on the willingness of enterprises to make green changes. | ||

| Industry Pressures → Green change behaviour in business | The requirements of the development of the industry in which the enterprise is located and the green behaviour of peer enterprises will play roles in promoting the formation of an enterprise’s willingness to make green changes. | ||

| Green Cooperation → Green change behaviour in business | The strength of green cooperation as an enabler of corporate willingness to make green changes | ||

| ② Green changes the second half: the back path | Willingness of businesses to make green changes → Green change behaviour in business | Green change behaviour in business → Strategic Change | An enterprise’s willingness to make green changes will have a direct impact on the enterprise’s changes in the future development model, in which strategic planning, formulation, implementation, and adjustment are all specific green change behaviours of the enterprise. |

| Willingness of businesses to make green changes → Innovation Optimisation | An enterprise’s willingness to make green changes will allow it to innovate and optimise its production processes in terms of products, production, and management. | ||

| ③ Greening the whole process: moderating the impact | Willingness of businesses to make green changes → Green change behaviour in business Regional level of green development | The level of green development in the region where an enterprise is located will have a limiting and moderating effect on the transition from the enterprise’s willingness to make green changes to the actual process of generating green change behaviours. | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wu, H.; Du, J. Driving Mechanism of Greening Corporate Environmental Behaviour Under the “Dual-Carbon” Goal: A Study Based on Grounded Theory Study. Sustainability 2025, 17, 4708. https://doi.org/10.3390/su17104708

Wu H, Du J. Driving Mechanism of Greening Corporate Environmental Behaviour Under the “Dual-Carbon” Goal: A Study Based on Grounded Theory Study. Sustainability. 2025; 17(10):4708. https://doi.org/10.3390/su17104708

Chicago/Turabian StyleWu, Huan, and Jianguo Du. 2025. "Driving Mechanism of Greening Corporate Environmental Behaviour Under the “Dual-Carbon” Goal: A Study Based on Grounded Theory Study" Sustainability 17, no. 10: 4708. https://doi.org/10.3390/su17104708

APA StyleWu, H., & Du, J. (2025). Driving Mechanism of Greening Corporate Environmental Behaviour Under the “Dual-Carbon” Goal: A Study Based on Grounded Theory Study. Sustainability, 17(10), 4708. https://doi.org/10.3390/su17104708