Examining Diverse Investors in the Clean Energy and Environmental Technology Sector: A Network Analysis from Japan

Abstract

1. Introduction

2. Literature Review

3. Materials and Methods

3.1. Research Context

3.2. Dataset and Data Cleaning

3.3. Social Network Analysis

3.4. Community Analysis

4. Results

4.1. Historical Evolution of the CEET Investor Network

4.2. The Characteristics of the Diverse Investors

4.3. Community Analysis to Understand the Role of GVCs

5. Discussion and Conclusions

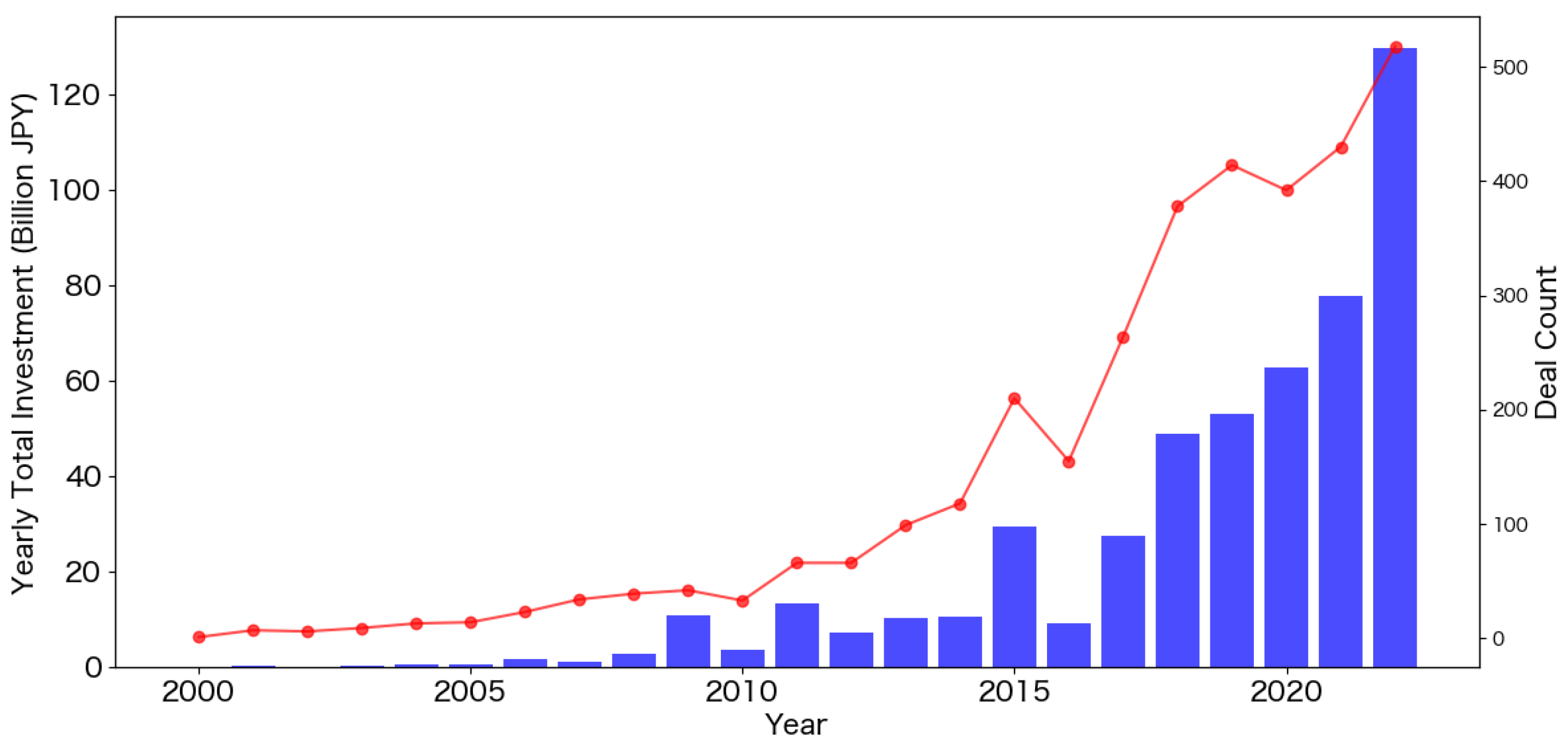

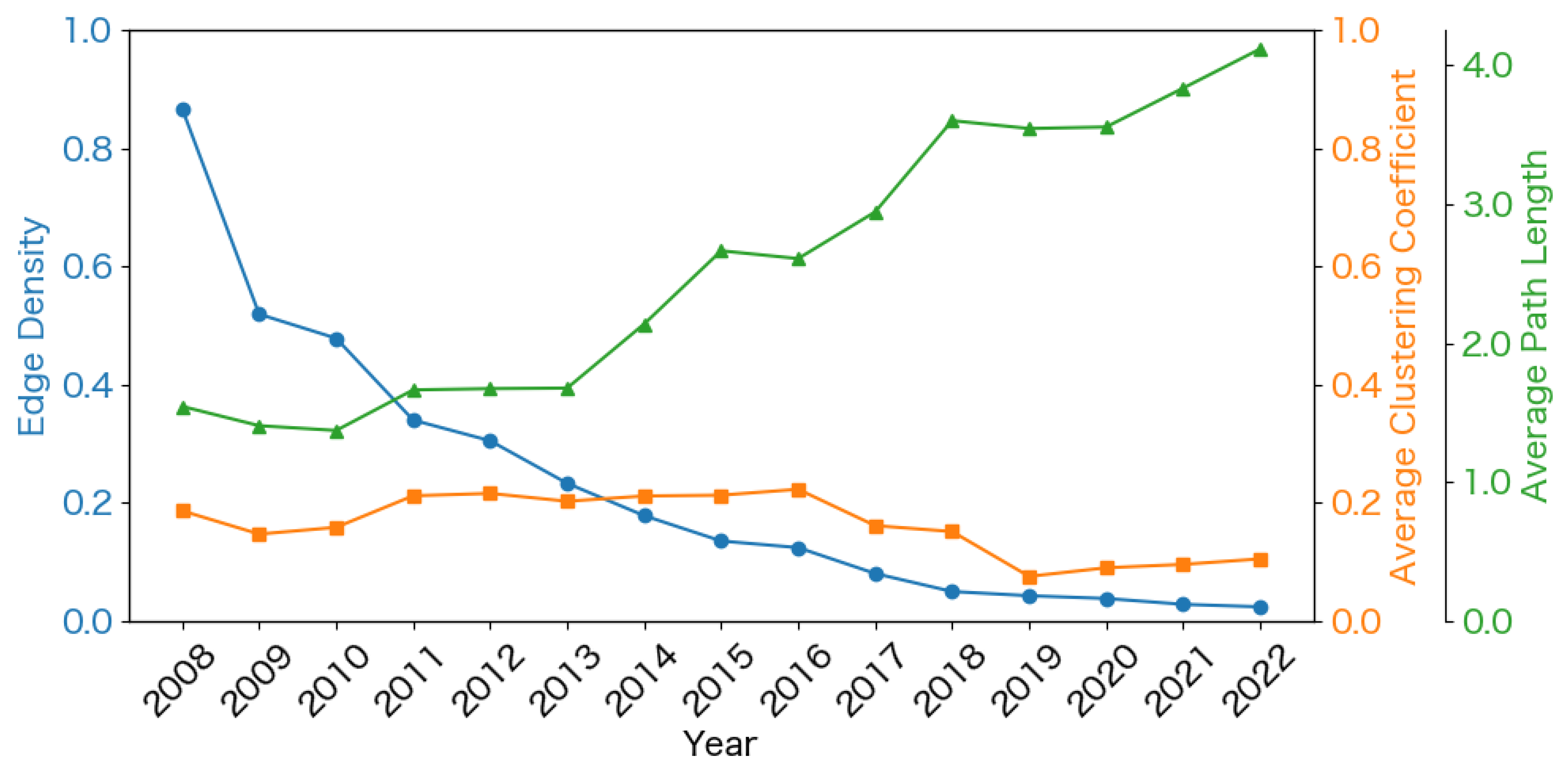

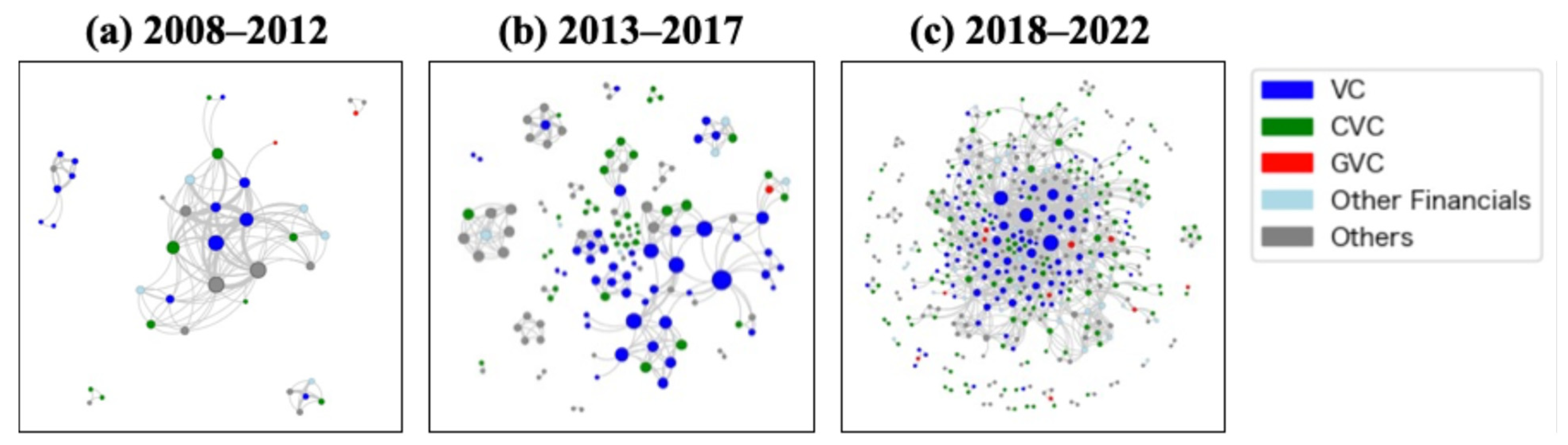

- Formative stage: This stage corresponds to the period from 2008 to 2012. A close-knit network was formed, characterized by a comparatively small number of investors. From 2010 onwards, the entry of investors continued, and the first signs of network cohesion appeared. During this period, energy deregulation could be associated with an increase in startup entry [68]; however, the energy market had not yet been sufficiently open to investor entry.

- Expansion and diversification stage: This stage corresponds to the period from 2013 to 2017. With the rapid growth of new investors, the CEET investor network has expanded and diversified. This growth trend was likely related to the total expansion of the Japanese startup investment market [19]. In addition, the rise of capital-intensive deep-tech startups may have increased the need for mutual collaboration among investors to allocate risk and secure funding.

- Stable growth stage: This stage corresponds to the period 2018–2022. The investor network was growing steadily, and the efficiency of the network was continuously improving. During this period, not only was the Japanese startup investment market growing, but also the promotion of sector-specific transition policies and the global trend of rapid investment growth in climate tech [69] were likely to be associated with this trend. As VC funds specializing in decarbonization were established and partnered with GVCs and CVCs [70,71], more diverse investors entered the CEET sector.

Supplementary Materials

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Abbreviations

| CEET | Clean Energy and Environmental Technology |

| VC | Venture Capital |

| CVC | Corporate Venture Capital |

| GVC | Governmental Venture Capital |

| R&D | Research and Development |

| GHG | Greenhouse Gas |

| SNA | Social Network Analysis |

| METI | Ministry of Economy, Trade and Industry |

| FIT | Feed-in Tariff |

| GX | Green Transformation |

| AI | Artificial Intelligence |

| IPO | Initial Public Offering |

| M&A | Mergers and Acquisitions |

References

- Boons, F.; Montalvo, C.; Quist, J.; Wagner, M. Sustainable Innovation, Business Models and Economic Performance: An Overview. J. Clean. Prod. 2013, 45, 1–8. [Google Scholar] [CrossRef]

- Cillo, V.; Petruzzelli, A.M.; Ardito, L.; Del Giudice, M. Understanding Sustainable Innovation: A Systematic Literature Review. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 1012–1025. [Google Scholar] [CrossRef]

- Anadon, L.D. Transforming U.S. Energy Innovation; Cambridge University Press: New York, NY, USA, 2014; ISBN 978-1-107-04371-8. [Google Scholar]

- Grubler, A.; Wilson, C. Energy Technology Innovation: Learning from Historical Successes and Failures; Cambridge University Press: Cambridge, UK; New York, NY, USA, 2013; ISBN 978-1-107-02322-2. [Google Scholar]

- Polzin, F. Addressing Barriers to Low-Carbon Innovation: Essays on Structures and Policies to Mobilise Private Finance; Peter Lang: Frankfurt am Main, Germany, 2015; ISBN 978-3-631-66981-5. [Google Scholar]

- Kreibiehl, S.; Jung, T.Y.; Battiston, S.; Carvajal, P.E.; Clapp, C.; Dasgupta, D.; Dube, N.; Jachnik, R.; Morita, K.; Samargandi, N.; et al. Investment and Finance. In IPCC Climate Change 2022: Mitigation of Climate Change. Contribution of Working Group III to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change; Cambridge University Press: Cambridge, UK; New York, NY, USA, 2022; ISBN 978-1-00-915792-6. [Google Scholar]

- Gaddy, B.E.; Sivaram, V.; Jones, T.B.; Wayman, L. Venture Capital and Cleantech: The Wrong Model for Energy Innovation. Energy Policy 2017, 102, 385–395. [Google Scholar] [CrossRef]

- Ivashina, V.; Lerner, J. Patient Capital: The Challenges and Promises of Long-Term Investing; Princeton University Press: Princeton, NJ, USA, 2019; ISBN 978-0-691-21708-6. [Google Scholar]

- Berger, M.; Dechezleprêtre, A.; Fadic, M. What Is the Role of Government Venture Capital for Innovation-Driven Entrepreneurship? OECD Science, Technology and Industry Working Papers, No. 2024/10; OECD Publishing: Paris, France, 2024. [Google Scholar] [CrossRef]

- Ghosh, S.; Nanda, R. Venture Capital Investment in the Clean Energy Sector. 2010. Available online: https://www.hbs.edu/ris/Publication%20Files/11-020_0a1b5d16-c966-4403-888f-96d03bbab461.pdf (accessed on 29 March 2025).

- Goldstein, A.; Doblinger, C.; Baker, E.; Anadón, L.D. Patenting and Business Outcomes for Cleantech Startups Funded by the Advanced Research Projects Agency-Energy. Nat. Energy 2020, 5, 803–810. [Google Scholar] [CrossRef]

- van den Heuvel, M.; Popp, D. The Role of Venture Capital and Governments in Clean Energy: Lessons from the First Cleantech Bubble. Energy Econ. 2023, 124, 106877. [Google Scholar] [CrossRef]

- Nicholas, T. VC: An American History; Harvard University Press: Cambridge, MA, USA, 2019; ISBN 978-0-674-98800-2. [Google Scholar]

- Hopp, C. When Do Venture Capitalists Collaborate? Evidence on the Driving Forces of Venture Capital Syndication. Small Bus. Econ. 2010, 35, 417–431. [Google Scholar] [CrossRef]

- Lockett, A.; Wright, M. The Syndication of Venture Capital Investments. Omega 2001, 29, 375–390. [Google Scholar] [CrossRef]

- Barabási, A.-L. Network Science; Cambridge University Press: Cambridge, UK; New York, NY, USA,, 2016; ISBN 978-1-107-07626-6. [Google Scholar]

- Wang, D.; Barabási, A.-L. The Science of Science, 1st ed.; Cambridge University Press: Cambridge, UK, 2021; ISBN 978-1-108-61083-4. [Google Scholar]

- Ministry of Economy, Trade and Industry (METI). Japan Startup Ecosystem 2024; Ministry of Economy, Trade and Industry: Tokyo, Japan, 2024; Available online: https://www.meti.go.jp/policy/newbusiness/global_promotion.pdf (accessed on 29 March 2025).

- Venture Enterprise Center (VEC). VEC YEARBOOK 2022 (Annual Report on Japanese Startup Businesses); Venture Enterprise Center: Tokyo, Japan, 2024; Available online: https://www.vec.or.jp/vec-whitepaper (accessed on 29 March 2025).

- Satz, E. Why Time Horizon Matters: The Key To Successful Venture Capital Investing. Available online: https://www.forbes.com/councils/forbesfinancecouncil/2024/12/05/why-time-horizon-matters-the-key-to-successful-venture-capital-investing/ (accessed on 13 March 2025).

- Cornelli, G.; Frost, J.; Gambacorta, L.; Merrouche, O. Climate Tech 2.0: Social Efficiency versus Private Returns; BIS Working Papers No. 1072; Bank for International Settlements: Basel, Switzerland, 2023; Available online: https://www.bis.org/publ/work1072.htm (accessed on 29 March 2025).

- PwC State of Climate Tech 2024. PwC. 2024. Available online: https://www.pwc.com/gx/en/issues/esg/climate-tech-investment-adaptation-ai.html (accessed on 29 March 2025).

- PwC State of Climate Tech 2021. PwC. 2021. Available online: https://www.pwc.com/gx/en/services/sustainability/publications/state-of-climate-tech.html (accessed on 29 March 2025).

- Migendt, M.; Polzin, F.; Schock, F.; Täube, F.A.; Von Flotow, P. Beyond Venture Capital: An Exploratory Study of the Finance-Innovation-Policy Nexus in Cleantech. Ind. Corp. Change 2017, 26, 973–996. [Google Scholar] [CrossRef]

- Polzin, F.; Sanders, M.; Täube, F. A Diverse and Resilient Financial System for Investments in the Energy Transition. Curr. Opin. Environ. Sustain. 2017, 28, 24–32. [Google Scholar] [CrossRef]

- Polzin, F. Mobilizing Private Finance for Low-Carbon Innovation—A Systematic Review of Barriers and Solutions. Renew. Sustain. Energy Rev. 2017, 77, 525–535. [Google Scholar] [CrossRef]

- Wyne, J. How To Fund High-Impact Climate Innovations. Available online: https://www.forbes.com/sites/jamilwyne/2024/07/24/how-to-fund-high-impact-climate-innovations/ (accessed on 13 March 2025).

- Du, Q.; Li, Z.; Du, M.; Yang, T. Government Venture Capital and Innovation Performance in Alternative Energy Production: The Moderating Role of Environmental Regulation and Capital Market Activity. Energy Econ. 2024, 129, 107196. [Google Scholar] [CrossRef]

- Owen, R. Lessons From Government Venture Capital Funds to Enable Transition to a Low-Carbon Economy: The U.K. Case. IEEE Trans. Eng. Manag. 2023, 70, 1040–1054. [Google Scholar] [CrossRef]

- Kirihata, T. Japanese Government Venture Capital: What Should We Know? Asia Pac. J. Innov. Entrep. 2018, 12, 14–31. [Google Scholar] [CrossRef]

- Bygrave, W.D. The Structure of the Investment Networks of Venture Capital Firms. J. Bus. Ventur. 1988, 3, 137–157. [Google Scholar] [CrossRef]

- Abell, P.; Nisar, T.M. Performance Effects of Venture Capital Firm Networks. Manag. Decis. 2007, 45, 923–936. [Google Scholar] [CrossRef]

- Ferrary, M.; Granovetter, M. The Role of Venture Capital Firms in Silicon Valley’s Complex Innovation Network. Econ. Soc. 2009, 38, 326–359. [Google Scholar] [CrossRef]

- Hochberg, Y.V.; Ljungqvist, A.; Lu, Y. Whom You Know Matters: Venture Capital Networks and Investment Performance. J. Financ. 2007, 62, 251–301. [Google Scholar] [CrossRef]

- Carniel, T.; Halloy, J.; Dalle, J.-M. A Novel Clustering Approach to Bipartite Investor-Startup Networks. PLoS ONE 2023, 18, e0279780. [Google Scholar] [CrossRef]

- Gu, W.; Yang, A.; Lu, L.; Li, R. Unveiling Latent Structure of Venture Capital Syndication Networks. Entropy 2022, 24, 1506. [Google Scholar] [CrossRef]

- Jin, Y.; Zhang, Q.; Li, S.-P. Topological Properties and Community Detection of Venture Capital Network: Evidence from China. Phys. Stat. Mech. Its Appl. 2016, 442, 300–311. [Google Scholar] [CrossRef]

- Luo, X.; Yin, J.; Jiang, H.; Wei, D.; Xia, R.; Ding, Y. Venture Capital Syndication Network Structure of Public Companies: Robustness and Dynamic Evolution, China. Systems 2023, 11, 302. [Google Scholar] [CrossRef]

- Yao, Q.; Ma, S.; Liang, J.; Christensen, K.; Jing, W.; Li, R. Syndication Network Associates with Specialisation and Performance of Venture Capital Firms. J. Phys. Complex. 2023, 4, 025016. [Google Scholar] [CrossRef]

- Zhang, R.; McCarthy, K.J.; Wang, X.; Tian, Z. How Does Network Structure Impact Follow-On Financing through Syndication? Evidence from the Renewable Energy Industry. Sustainability 2021, 13, 4050. [Google Scholar] [CrossRef]

- Polzin, F. Venture Capital Investments in Cleantech Startups. In The Palgrave Encyclopedia of Private Equity; Cumming, D., Hammer, B., Eds.; Springer International Publishing: Cham, Switzerland, 2024; pp. 1–6. ISBN 978-3-030-38738-9. [Google Scholar]

- Ministry of Economy, Trade and Industry (METI). The 5th Strategic Energy Plan; Ministry of Economy, Trade and Industry: Tokyo, Japan, July 2018. Available online: https://www.enecho.meti.go.jp/en/category/others/basic_plan/ (accessed on 29 March 2025).

- Takeuchi, J.; Ito, T.; Okamoto, H.; Toda, N. The Energy Industry 2050: Game Change to Utility 3.0; Nikkei BP: Tokyo, Japan, 2017. [Google Scholar]

- Kuramochi, T. Review of Energy and Climate Policy Developments in Japan before and after Fukushima. Renew. Sustain. Energy Rev. 2015, 43, 1320–1332. [Google Scholar] [CrossRef]

- Tokyo Electric Power Company Holdings, Inc.; TEPCO Ventures, Inc. TEPCO Establishes Subsidiary to Turn New Businesses into Venture Companies—For Faster and More Effective Response to Deregulation and Other Market Changes. Available online: https://www.tepco.co.jp/en/hd/newsroom/press/archives/2018/180627-01-e.html (accessed on 28 March 2025).

- Cabinet Secretariat of Japan. Basic Policy for the Realization of Green Transformation: Roadmap for the Next 10 Years; Cabinet Secretariat: Tokyo, Japan, 2023; Available online: https://www.cas.go.jp/jp/seisaku/gx_jikkou_kaigi/pdf/kihon_en.pdf (accessed on 29 March 2025).

- Uzabase, Inc. Japan Startup Finance 2018; Uzabase, Inc.: Tokyo, Japan, 2019. [Google Scholar]

- Uzabase, Inc. Japan Startup Finance 2022; Uzabase, Inc.: Tokyo, Japan, 2023. [Google Scholar]

- Cabinet Secretariat of Japan. Startup Development Five-Year Plan; Cabinet Secretariat: Tokyo, Japan, 2022; Available online: https://www.cas.go.jp/jp/seisaku/atarashii_sihonsyugi/pdf/sdfyplan2022en.pdf (accessed on 29 March 2025).

- Kennedy, K.M.; Edwards, M.R.; Doblinger, C.; Thomas, Z.H.; Borrero, M.A.; Williams, E.D.; Hultman, N.E.; Surana, K. The Effects of Corporate Investment and Public Grants on Climate and Energy Startup Outcomes. Nat. Energy 2024, 9, 883–893. [Google Scholar] [CrossRef]

- Krishna, H.; Kashyap, Y.; Dutt, D.; Sagar, A.D.; Malhotra, A. Understanding India’s Low-Carbon Energy Technology Startup Landscape. Nat. Energy 2023, 8, 94–105. [Google Scholar] [CrossRef]

- Uzabase, Inc. Speeda Startup Information Research. Available online: https://initial.inc/ (accessed on 16 July 2024).

- For Startups, Inc. STARTUP DB. Available online: https://startup-db.com/ (accessed on 17 April 2023).

- Anai, H.; Shibazaki, R. Study on Startups Ecosystem Aggregation in Tokyo 23 Ward: Analysis of Co-Aggregation Using Bivariate Local Moran Statistics. J. City Plan. Inst. Jpn. 2020, 55, 1055–1062. [Google Scholar] [CrossRef]

- Kutsuna, K. Current Status of Startups in the Kansai Region. Kokumin Keizai Zasshi J. Econ. Bus. Adm. 2022, 226, 1–10. [Google Scholar] [CrossRef]

- HolonIQ. 2023 Global Climate Tech Outlook. Available online: https://www.holoniq.com/notes/2023-global-climate-tech-outlook (accessed on 29 March 2025).

- Barrat, A.; Barthélemy, M.; Pastor-Satorras, R.; Vespignani, A. The Architecture of Complex Weighted Networks. Proc. Natl. Acad. Sci. USA 2004, 101, 3747–3752. [Google Scholar] [CrossRef]

- Humphries, M.D.; Gurney, K. Network ‘Small-World-Ness’: A Quantitative Method for Determining Canonical Network Equivalence. PLoS ONE 2008, 3, e0002051. [Google Scholar] [CrossRef]

- Watts, D.J.; Strogatz, S.H. Collective Dynamics of ‘Small-World’ Networks. Nature 1998, 393, 440–442. [Google Scholar] [CrossRef] [PubMed]

- Clauset, A.; Shalizi, C.R.; Newman, M.E.J. Power-Law Distributions in Empirical Data. SIAM Rev. 2009, 51, 661–703. [Google Scholar] [CrossRef]

- Esposito, C.; Gortan, M.; Testa, L.; Chiaromonte, F.; Fagiolo, G.; Mina, A.; Rossetti, G. Venture Capital Investments through the Lens of Network and Functional Data Analysis. Appl. Netw. Sci. 2022, 7, 42. [Google Scholar] [CrossRef]

- Yamano, H.; Asatani, K.; Sakata, I. Evaluating Nodes of Latent Mediators in Heterogeneous Communities. Sci. Rep. 2020, 10, 8456. [Google Scholar] [CrossRef]

- Landherr, A.; Friedl, B.; Heidemann, J. A Critical Review of Centrality Measures in Social Networks. Bus. Inf. Syst. Eng. 2010, 2, 371–385. [Google Scholar] [CrossRef]

- Girvan, M.; Newman, M.E.J. Community Structure in Social and Biological Networks. Proc. Natl. Acad. Sci. USA 2002, 99, 7821–7826. [Google Scholar] [CrossRef]

- Blondel, V.D.; Guillaume, J.-L.; Lambiotte, R.; Lefebvre, E. Fast Unfolding of Communities in Large Networks. J. Stat. Mech. Theory Exp. 2008, 2008, P10008. [Google Scholar] [CrossRef]

- Danon, L.; Díaz-Guilera, A.; Duch, J.; Arenas, A. Comparing Community Structure Identification. J. Stat. Mech. Theory Exp. 2005, 2005, P09008. [Google Scholar] [CrossRef]

- Guimerà, R.; Nunes Amaral, L.A. Functional Cartography of Complex Metabolic Networks. Nature 2005, 433, 895–900. [Google Scholar] [CrossRef]

- Romero, T. As Japan Deregulates Electricity, This Startup Lets Consumers Compare Suppliers. Available online: https://www.techinasia.com/talk/yohei-kiguchi-enechange (accessed on 25 March 2025).

- PwC State of Climate Tech 2023. PwC. 2023. Available online: https://www.pwc.com/gx/en/issues/esg/state-of-climate-tech-2023-investment.html (accessed on 29 March 2025).

- Japan Investment Corporation. JIC Makes LP Investment in ANRI-GREEN No.1 2022. 2022. Available online: https://www.j-ic.co.jp/en/news/.assets/E_20220126_JIC_PressRelease.pdf (accessed on 27 April 2025).

- Segal, M. Mitsubishi Launches $1 Billion Climate Tech Growth Fund. Available online: https://www.esgtoday.com/mitsubishi-launches-1-billion-climate-tech-growth-fund/ (accessed on 25 March 2025).

- Gompers, P.A.; Lerner, J. The Venture Capital Cycle; MIT Press: Cambridge, MA, USA, 2004; ISBN 978-0-262-07255-7. [Google Scholar]

- Fels, G.; Kronberger, M.; Gutmann, T. Revealing the Underlying Drivers of CVC Performance—A Literature Review and Research Agenda. Ventur. Cap. 2021, 23, 67–109. [Google Scholar] [CrossRef]

- Hibara, N. Modeling New Categories of CVC Investments. Waseda Bull. Int. Manag. 2016, 47, 83–88. [Google Scholar]

- Bianchini, R.; Croce, A. The Role of Environmental Policies in Promoting Venture Capital Investments in Cleantech Companies. Rev. Corp. Financ. 2022, 2, 587–616. [Google Scholar] [CrossRef]

- Alperovych, Y.; Groh, A.; Quas, A. Bridging the Equity Gap for Young Innovative Companies: The Design of Effective Government Venture Capital Fund Programs. Res. Policy 2020, 49, 104051. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Tech Sector | Number of Nodes | Number of Edges | α Estimate (Scale-Free Parameter) | 95% Confidence Interval for α | Mean KS Statistic | Mean p-Value | Optimal Xmin |

|---|---|---|---|---|---|---|---|

| CEET | 525 | 1716 | 2.941 | [2.460, 3.778] | 0.870 | p < 0.001 | 14.0 |

| Drug Discovery | 250 | 1035 | 2.767 | [2.094, 4.507] | 0.924 | p < 0.001 | 30.0 |

| AI | 303 | 891 | 2.641 | [2.126, 4.248] | 0.650 | p < 0.001 | 5.0 |

| Investor Types | VC | CVC | GVC | Other Financials | Others |

|---|---|---|---|---|---|

| Degree Centrality | |||||

| Mean | 16.395 | 5.530 | 7.091 | 7.649 | 4.758 |

| Median | 8.000 | 4.000 | 6.000 | 6.000 | 3.000 |

| Min | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| Max | 104.000 | 22.000 | 21.000 | 24.000 | 38.000 |

| Betweenness Centrality | |||||

| Mean | 0.010 | 0.001 | 0.002 | 0.001 | 0.001 |

| Median | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| Min | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| Max | 0.138 | 0.022 | 0.008 | 0.014 | 0.017 |

| Closeness Centrality | |||||

| Mean | 0.312 | 0.210 | 0.216 | 0.236 | 0.167 |

| Median | 0.308 | 0.262 | 0.267 | 0.266 | 0.225 |

| Min | 0.004 | 0.002 | 0.002 | 0.002 | 0.002 |

| Max | 0.504 | 0.397 | 0.398 | 0.414 | 0.430 |

| Eigenvector Centrality | |||||

| Mean | 0.041 | 0.007 | 0.014 | 0.012 | 0.007 |

| Median | 0.013 | 0.002 | 0.001 | 0.002 | 0.001 |

| Min | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| Max | 0.427 | 0.067 | 0.088 | 0.088 | 0.087 |

| Centrality Measure | H-Statistic | p-Value | Effect Size (ε2) | Significant Differences (p < 0.05) |

|---|---|---|---|---|

| Degree Centrality | 59.476 | p < 0.001 | 0.107 | VC-CVC, VC-Others |

| Betweenness Centrality | 88.642 | p < 0.001 | 0.163 | VC-CVC, VC-Other Financials, VC-Others, CVC-Others, GVC-Others |

| Closeness Centrality | 76.118 | p < 0.001 | 0.139 | VC-CVC, VC-Other Financials, VC-Others |

| Eigenvector Centrality | 73.702 | p < 0.001 | 0.134 | VC-CVC, VC-Other Financials, VC-Others |

| Metric | CEET |

|---|---|

| Number of GVC Communities | 10 |

| Number of Non-GVC Communities | 55 |

| Average Size of GVC Communities | 28.70 |

| Average Size of Non-GVC Communities | 4.33 |

| Median Size of GVC Communities | 29.00 |

| Median Size of Non-GVC Communities | 2.00 |

| Mann-Whitney U Test Result | Significant |

| U Statistic | 466.5 |

| p-value | p < 0.001 |

| Epsilon-Squared (ε2) | 0.348 |

| Investor Types | Number of Communities | Mean | Median | Min | Max |

|---|---|---|---|---|---|

| VC | 14 | 2.588 | 2.0 | 0.0 | 7.600 |

| CVC | 41 | 0.378 | 0.0 | 0.0 | 2.625 |

| GVC | 10 | 2.250 | 0.5 | 0.0 | 8.000 |

| Other Financials | 17 | 1.368 | 0.5 | 0.0 | 9.000 |

| Others | 53 | 0.201 | 0.0 | 0.0 | 2.286 |

| Investor Types | Count | Mean | Median | Min | Max |

|---|---|---|---|---|---|

| VC | 119 | 0.354 | 0.408 | 0.0 | 0.822 |

| CVC | 164 | 0.173 | 0.000 | 0.0 | 0.684 |

| GVC | 11 | 0.309 | 0.444 | 0.0 | 0.680 |

| Other Financials | 37 | 0.205 | 0.000 | 0.0 | 0.710 |

| Others | 194 | 0.104 | 0.000 | 0.0 | 0.720 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Iwata, H.; Kubo, K.; Yamano, H.; Sugiyama, M.; Tanaka, K. Examining Diverse Investors in the Clean Energy and Environmental Technology Sector: A Network Analysis from Japan. Sustainability 2025, 17, 4258. https://doi.org/10.3390/su17104258

Iwata H, Kubo K, Yamano H, Sugiyama M, Tanaka K. Examining Diverse Investors in the Clean Energy and Environmental Technology Sector: A Network Analysis from Japan. Sustainability. 2025; 17(10):4258. https://doi.org/10.3390/su17104258

Chicago/Turabian StyleIwata, Hiroyoshi, Kotaro Kubo, Hiroko Yamano, Masahiro Sugiyama, and Kenji Tanaka. 2025. "Examining Diverse Investors in the Clean Energy and Environmental Technology Sector: A Network Analysis from Japan" Sustainability 17, no. 10: 4258. https://doi.org/10.3390/su17104258

APA StyleIwata, H., Kubo, K., Yamano, H., Sugiyama, M., & Tanaka, K. (2025). Examining Diverse Investors in the Clean Energy and Environmental Technology Sector: A Network Analysis from Japan. Sustainability, 17(10), 4258. https://doi.org/10.3390/su17104258