1. Introduction

The structure of the agricultural sectors of the countries of Central and Eastern Europe (CEE) has been shaped historically, although the current directions of its changes have been determined by economic transformation and accession to the European Union (EU). The economic transition has determined the ownership structure of the agricultural sector in these countries, establishing small private farms, most often family farms, as the minimum form of land ownership or use [

1,

2]. With their accession to the EU, the CEE countries began the process of adapting agriculture and food production to the requirements of the common agricultural market and the Common Agricultural Policy (CAP) [

3,

4]. Decisions made by farms at the time were fraught with risk due to the new market situation in which the farms found themselves, and required knowledge and understanding of the new conditions of their operation.

The EU’s common agricultural market has provided CEE farms with many opportunities, including those related to the flow of goods, the common agricultural policy, but it has also imposed obligations including regulatory harmonization, compliance with sanitary standards, and food safety [

5]. With accession to the EU, farms in Central and Eastern Europe were able to benefit from financial support mechanisms under the CAP, but at the same time faced external competition. For farms in these countries, this has meant modernization and investment, often using CAP funds. As a natural consequence of agricultural modernization, the structure of the agricultural sector in CEE countries is changing. Agricultural sectors in these countries have progressively begun to increase the scale and specialization of production, as investments in the agricultural sector tend to be made on farms with larger economic size [

6,

7,

8].

At the time of accession to the EU in 2004, the agricultural sectors of the CCE countries (the Czech Republic, Estonia, Hungary, Lithuania, Latvia, Poland and Slovakia), and in 2007, the agricultural sectors of Bulgaria and Romania, were significantly different from those of the EU countries. The most important differences are the greater economic and social importance of agriculture in their economies, the dominance of small farms, and the slight tendency toward collectivization of agricultural production [

9], and lower, compared to the rest of the EU countries, technical efficiency [

10,

11]. Since accession to the EU, farms in Central and Eastern Europe have been adapting to the standards of member countries, taking advantage of financial support mechanisms that allow the farms to narrow the existing gap with agriculture in France, Germany, and Italy, among others. However, it is important to state that after almost two decades under the common agricultural market, the agricultural sectors of most CEE countries still differ in many respects from the agricultural sectors of other EU countries. A constant feature of farms is the high fragmentation of agriculture. Agricultural activities are carried out on small farms, and the only exceptions are the agricultural sectors of the Czech Republic and Slovakia. Although the process of adjustment of CEE agriculture in the EU agricultural market has not ended, new challenges have been posed.

The current operating conditions for farms in the EU, including CEE, have changed. Observed in most countries in the world, including the EU, climate change, environmental degradation, and lost biodiversity are increasingly resulting in catastrophes, i.e., drought, fires, and floods [

12], and have a direct negative impact on the economy and society. The European Commission has set specific and concrete targets to halt climate change and restore ecosystems and biodiversity. Climate and environmental awareness has occupied, and continues to occupy, much of the space in the EU’s formulated policy documents, the most widely described of which is the European Green Deal 2019 strategy (EGD) [

13].

The EGD [

13] is the European Union’s strategy to build a modern, resource-efficient, and competitive economy by 2050 that will achieve zero net greenhouse gas emissions and whose economic growth is decoupled from the use of natural resources [

13,

14]. Document [

13] corresponds to the development goals set out in Transforming Our World: 2030 Agenda for Sustainable Development [

15]. The EGD’s formulated efforts to return natural resources and protect the environment are also reflected in proactive climate diplomacy and the EU’s involvement in programs and initiatives beyond its borders. The European Commission finances projects related to environmental protection and combating climate change, promoting sustainable development in many areas, including energy, agriculture, and transport, under such programs as EU4Climate [

16], Union for the Mediterranean [

17], or SWITCH to Green [

18].

The overall climate neutrality goals outlined in the EGD commit each member country to directly join the initiative. Each EU country was required to create its first national long-term strategy for climate neutrality (Long-Term Strategy) by 1 January 2021 [

19], compliance with the National Energy and Climate Plan 2021–2030 [

20], and the following one: until 1 January 2029, and every 10 years thereafter. National Long-Term Strategy Plans must mandatorily set ambitious, measurable, and feasible goals for national economies, including for reducing greenhouse gas emissions and improving their removal by sinks in all sectors, i.e., electricity, industry, transport, heating and cooling, the construction sector, agriculture, waste management, land use, land use change, and forestry. All actions are taken at the EU and the national level to support the transformation of the EU economy towards a sustainable, climate-neutral, and resilient economy by 2050. One important area of these actions is agriculture and food production, as well as biodiversity protection.

For agriculture, the EGD is complemented by A Farm to Fork Strategy [

21] and the EU Biodiversity Strategy 2030 [

22]. The first focuses on reducing greenhouse gas emissions from the agricultural sector, developing sustainable farming practices, reducing the use of chemical fertilizers and crop protection products, and promoting ecological food production. In turn, the EU Biodiversity Strategy for 2030 [

22] describes ways to restore natural ecosystems and protect land from degradation, and formulates goals for creating and enhancing natural areas on agricultural land. Thus, the EGD, along with the mentioned strategies, set new goals for the agricultural sector, and, thus, CAP actions also needed to be reformulated—focused on supporting food production on sustainable or ecological farms [

23,

24,

25]. A total of 40% of the CAP 2023–2027 [

26] budget has been allocated to support the implementation of climate goals that will bring the EU closer to achieving the EGD goals. Modified financial support mechanisms have also been linked to the promotion of other agricultural ecosystem services [

27,

28]. Among the important changes in the CAP 2023–2027, of interest is the change in the approach to financial support for small- and medium-sized farms, most of which are located in CEE countries, including Poland and Romania. Small- and medium-sized farms received additional funding, for example, to promote sustainable and ecological production practices, or to finance the modernization and adaptation of production practices to climate changes.

In light of these facts, it is interesting to discuss the current and future structure of the agricultural sectors in the CEE countries, as well as the financial mechanisms supporting and developing food production methods on the farms of these countries. This is because it may turn out that the structure of the agricultural sector based on small-sized farms may now be one of the main assets in building the ecological position of CEE farms.

The main purpose of this article is to learn about the situation of the agricultural sectors in the countries of Central and Eastern Europe and to discuss the future directions of their development. It was assumed that the goals of the European Green Deal should influence the directions of transformation of agricultural sectors in the countries of Central and Eastern Europe. In order to realize the main purpose of the article, empirical research was conducted to assess the structural changes of agriculture in CEE countries in 2004–2021. The analyses assumed that the CEE countries consist of a group of nine countries, namely, Bulgaria, the Czech Republic, Estonia, Hungary, Lithuania, Latvia, Poland, Romania, and Slovakia. To estimate the structure of agricultural sectors, data on the number of farms grouped by agricultural type of farming and the economic size of farms were used separately for each of the CEE countries analyzed. The source of the data was the Farm Accountancy Data Network—FADN Database [

29].

This article is divided into four main parts. The second part contains a description of the empirical research, defines the research procedure, and presents the data and data sources. The third part of the article presents the results of the research on the structure of agriculture of the CEE countries by types of farming and economic size classes of farms, which forms the basis of the discussion in the last and fourth part of this article. This article ends with a conclusion, in which the main conclusions of the literature study, the study of strategic documents, and the results of the empirical research are formulated.

2. Materials and Methods

The purpose of the empirical research is to assess the structural changes in agriculture in the CEE countries that took place between 2004 and 2021. The background for the discussion of the observed changes is the assumptions of the European Green Deal. The questions to which answers were sought were formulated as follows:

What is the current structure of the agricultural sector in the CEE countries, taking into account types of farming and economic size classes of farms, and does it differ from the current structure of the agricultural sectors of the EU countries?

How might changes in the structure of the agricultural sector in Central and Eastern Europe affect the implementation of the European Green Deal?

The scope of this research, therefore, is to estimate the structure of the agricultural sectors in the CEE countries in terms of types of farming and economic size classes, and to compare and evaluate them against the agricultural sectors of the selected EU countries. This analysis assumes that CEE countries are a group of nine countries located in Central and Eastern Europe, members of the EU, which formed the so-called Eastern Bloc of Europe after World War II and were Bulgaria, the Czech Republic, Estonia, Hungary, Lithuania, Latvia Poland, Romania, and Slovakia. A group of six EU agricultural sectors (the founders of the EU) was used for comparison, namely, the agricultural sectors of Belgium, The Netherlands, France, Germany, Italy, and Luxembourg, which played a key role in shaping the CAP and continues to set its direction today. This outlines the object and spatial scope of the research.

The analyzed countries of Central and Eastern Europe show great similarities geographically, historically, and economically [

30]. The political order in these countries was established relatively recently and was directly related to the Solidarity Revolution in Poland and the withdrawal of Lithuania, Latvia, and Estonia from the USSR federation; these countries are still characterized by less-stable political and institutional systems. Accession to the EU began the process of adapting their economies to EU structures, resulting in increased productivity, causing a rapid economic acceleration. Thanks to investment, including direct investment, the economic distance between the CEE countries and the rest of the EU has narrowed, and there has been a change in the sectoral structure of these economies. The increase in investment has had a positive impact on the condition of the labor market. Access to EU funds improved the state of technical, energy, and technological infrastructure [

31]. Despite the narrowing of the economic and social gap between CEE countries and the rest of the EU, their GDP per capita levels are still significantly lower compared to countries such as Germany, France, and Italy, and research and development spending is also lower.

This analysis covered the years 2004–2021. The year 2004 was the year of EU accession for most of the countries analyzed, with the exception of Bulgaria and Romania, which acceded to the EU in 2007. The year 2021 was the last year for which FADN collected and published a full set of data.

To estimate the structure of agricultural sectors, data on the number of farms grouped by type of farming and economic size classes separately for each of the CEE and selected EU countries analyzed were used, along with their overall characteristics. The source of the data was the Farm Accountancy Data Network—FADN database [

29], which annually publishes data characterizing farms operating in the EU.

FADN groups data on the number of farms by various classification criteria, including types of farming and economic size classes [

32]. The overall classification by type of farming divides farms into eight agricultural types: 1. farms specializing in field crops, 2. farms specializing in horticulture, 3. farms specializing in wine production, 4. farms specializing in other permanent crops, 5. farms specializing in milk cows, 6. farms specializing in raising other grazing livestock, 7. farms specializing in raising granivores, and 8. farms without specialization, engaged in mixed farming operations.

The classification of economic size classes of farms divides them into six economic size classes: 1. very small farms with annual income expressed in euros in the range of EUR 2000 to 7999, 2. small farms with annual income expressed in euros in the range of EUR 8000 to 24,999, 3. medium-small farms with annual income expressed in euros in the range of EUR 25,000 to 49,999, 4. medium-large farms with annual income expressed in euros in the range of EUR 50,000 to 99,999, 5. large farms with annual income expressed in euros in the range of EUR 100,000 to 499,999, and 6. very large farms with annual income of more than EUR 500,000.

Data on the number of farms according to the above-mentioned classifications were used to assess the structure of the agricultural sector in CEE countries in terms of types of farming and economic size classes, which were then compared over time and between countries.

3. Results

Over the past two decades, the EU’s agricultural sector has seen a trend toward fewer farms [

33,

34]. According to FADN data [

29], the total number of farms of interest to the FADN in the EU countries (EU-27) in 2021 was 3,562,962 farms, down by 456,308 farms compared to the number of farms in 2004. In 2021, the largest number of farms in the EU was in Poland (693,880 farms), then Italy (534,547 farms), and then Romania (390,026 farms).

In CEE countries, as in the EU, the number of farms has declined. In 2021, the number of farms in CEE countries was 1,344,783 farms, a decrease of 1,020,138 farms compared to 2007, when Romania and Bulgaria acceded to the EU. The largest number of farms was in Poland (693,880 farms) and the smallest in Slovakia (4466 farms). A downward trend in the number of farms was observed in eight of the nine countries analyzed, with the exception of the agricultural sector in Slovakia, where the number of farms increased by about 25% compared to 2004, when Slovakia acceded to the EU.

Selected EU countries (Belgium, The Netherlands, France, Germany, Italy, and Luxembourg) also saw a trend toward fewer farms. The number of farms in 2021 in these countries was 1,033,082 farms, down by 447,475 farms compared to 2004. In 2021, the largest number of farms was in Italy, with 534,547 farms, and the smallest in Luxembourg, with 1355 farms. The trend toward a decrease in the number of farms was observed in all EU countries analyzed.

A graphical representation of changes in the number of farms in CEE and selected EU countries between 2004 and 2021 is shown in

Figure 1.

Changes in the number of farms in the CEE countries affected structural changes in their agriculture. The collected FADN data made it possible to determine the structure of the CEE countries’ sectors in terms of the types of farming of the farms and by their economic size classes, and made it possible to assess the observed structural changes over time and in comparison with the structural changes observed in the agricultural sectors of the EU countries selected for analysis.

3.1. Structure of Agricultural Sectors by Types of Farming in CEE Countries

The agricultural sectors of the CEE countries at the time of accession to the EU, i.e., in 2004, and in the case of Bulgaria and Romania in 2007, were characterized by a large share of farms without a specific specialization, the so-called mixed farms (the exceptions were the agricultural sectors in Estonia and Slovakia, which already specialized in field crops at the time of accession), while in the agricultural sector of the other EU countries analyzed, there was a tendency to define the specialization of farm activities; for example, farms in France specialized in wine production and raising other grazing livestock, or olive production and wine in Italy, or milk farming in Luxembourg and The Netherlands.

In the agricultural sectors of the CEE countries in 2004, the highest share of farms engaged in mixed farming without specialization was in Lithuania (53% of farms), Poland (53% of farms), Latvia (45% of farms), and Romania (46% of farms). At the same time, on average, the share of farms without specialization engaged in mixed farming in the agricultural sectors of the EU countries analyzed was several times lower—the lowest in Italy and The Netherlands (6% of farms). In 2021, it is noteworthy that the agricultural sectors of the CEE countries have changed their structure in terms of types of farming. All CEE countries have seen a shift in agricultural activity toward greater specialization. Farms in CEE countries have evolved into agricultural sectors specializing in field crops (Type 1 farms)—in Hungary, 57% of farms are field crop farms, and in Slovakia, a similar 51% of farms are field crop farms. A significant profile of farm specialization in the CEE countries, in addition to field crops, was milk farming (type 5 farms) and raising granivores farming (type 7 farms). In 2021, the share of mixed farms without specialization was relatively high in the Czech Republic (18%), Lithuania (21%), Latvia (22%), Poland (20%), and Romania (27%). In the remaining CEE countries, i.e., Bulgaria, Estonia, Hungary, and Slovakia, the share of farms without specialization was similar to their share in the EU countries analyzed. In addition, in Belgium, The Netherlands, France, Germany, Italy, and Luxembourg, during the period under analysis, there was a tendency to continue the adopted specialization of production.

Detailed changes in the structure of agricultural sectors by types of farming in CEE and selected EU countries in 2004/2007 and in 2021 are shown in

Table 1.

3.2. Structure of Agricultural Sectors by Farm Economic Size Classes in CEE Countries

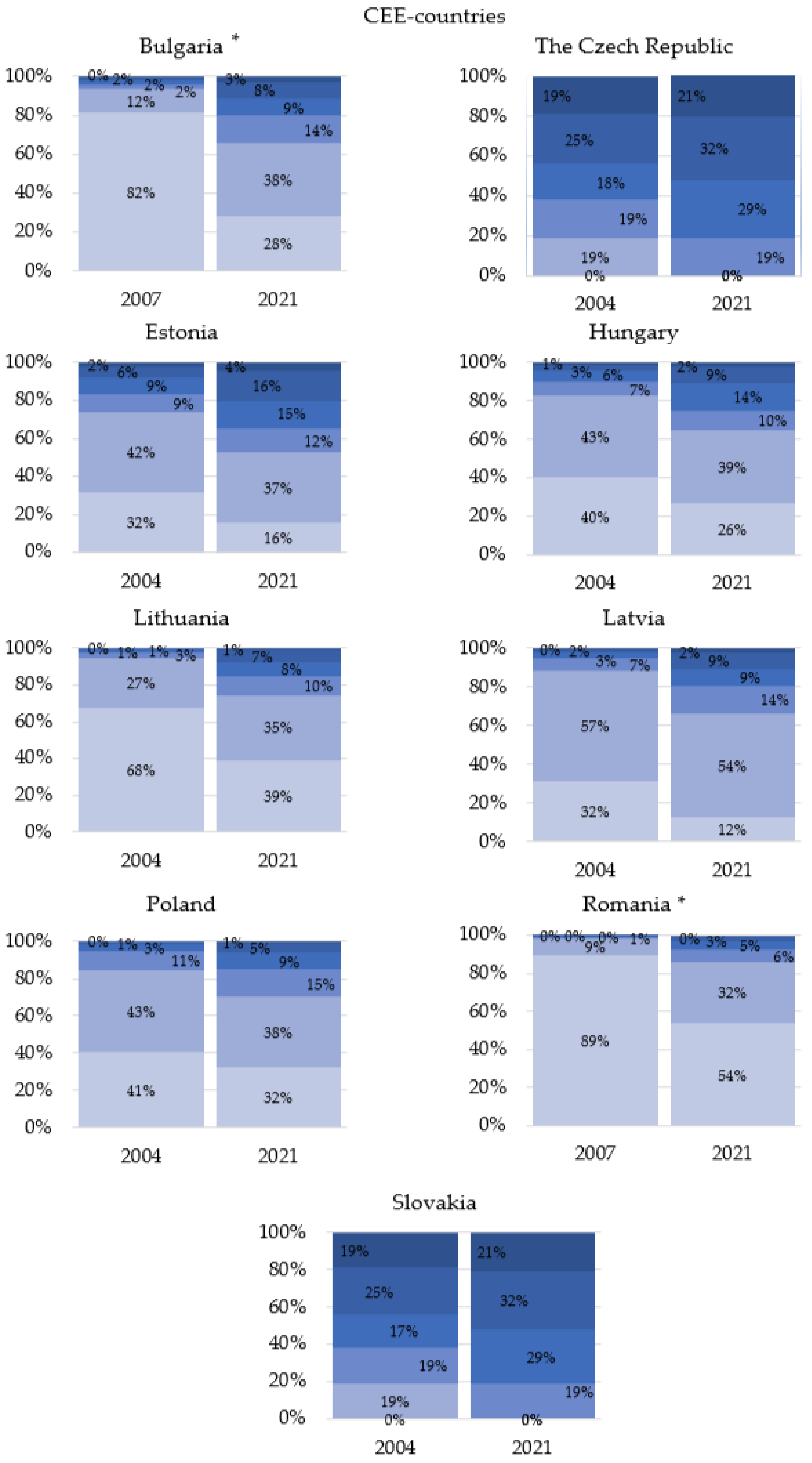

The second stage of the research determined the structure of agricultural sectors in CEE countries in terms of farm economic size classes.

Figure 2 shows the structures of the analyzed agricultural sectors of the CEE countries in terms of farm economic size classes in the year of their accession to the EU, i.e., 2004 or 2007, and in the last year of the analysis, i.e., 2021.

The agricultural sectors of the CEE countries at the time of accession to the EU differed significantly from the agricultural sectors of the EU countries (the founders of the EU) in terms of economic size classes of farms. The agricultural production of the CEE countries at the time of accession to the EU was mainly organized in economically very small and very small farms, with the exception of the agricultural sector of Slovakia. While agricultural production in EU countries was already organized in economically large and very large farms in 2004, the only exception was Italy, where the largest number of farms were very small and small farms (70% of farms in total).

In 2021, there have been small and slow changes in the structure of CEE countries’ agricultural sectors in terms of economic size classes—farms in CEE have increased their economic size. Although there is still an extraction of agricultural production in very small and small farms, the exception is the agricultural sector of Slovakia and the Czech Republic, where it is noted that the structure of agricultural sectors is becoming similar to the structure of agricultural sectors of EU countries in terms of economic classes of farms.

To summarize, the current structure of agricultural sectors in CEE countries is similar to that in EU countries in terms of types of farming. Farms in these countries specialize their production, specializing in field crops, milk production (dairy farming), and grazing livestock. In contrast, the analysis of the structure of the agricultural sectors of the CEE countries in terms of economic size classes did not allow confirmation that the farms of these countries have become similar to those of the EU countries. Thus, the results of the empirical research allow us to conclude that the current structure of agricultural sectors in CEE countries does not differ from the current structure of agricultural sectors in EU countries only partially, i.e., in terms of type of farming.

The EGD goals shed new light on the direction of structural transformation taken by farms in Central and Eastern Europe. The first years after the economic transformation and accession of these countries to the EU were motivated by raising the economic and technical efficiency of agriculture. Farms made changes in their structure, including the scale of size, and specialization of agricultural types along the lines of the agricultural sectors of EU countries, guided primarily by economic calculation. In the future, the changes initiated are likely to continue. However, after almost two decades of functioning within the EU agricultural market, when the transformation process has not been completed and a large number of farms are still in the stage of modernization, before the agricultural sector of CEE countries has achieved its goals, EGD has set new ones—changing the practices of farming practices and livestock breeding. This fact should be taken into account in further structural changes.

4. Discussion

EU agriculture, including the countries of Central and Eastern Europe, is now at a crucial point, facing new development paths, i.e., integrating the goals of reducing greenhouse gas emissions and promoting biodiversity into the existing strategy. The EU’s agricultural practices to date have ensured food security and provided the opportunity to produce enough food, and the financial support mechanisms under the CAP have guaranteed affordability for consumers and decent incomes for farmers [

35]. Since the 1980s, EU policy documents on agriculture and agricultural policy have emphasized the need to protect natural resources, at first discreetly and now directly, emphasizing sustainable and environmentally friendly farming practices. The EGD places EU agriculture in a new light, making it co-responsible for climate and environmental change and assigning it (the EU agricultural sector) a special role in bringing the EU back to climate neutrality.

Initially, the operation of the Common Agricultural Policy was focused on achieving the overall objectives of EU agriculture, including stabilizing markets for agricultural products, solving the problem of food overproduction in the 1980s. Farms, through access to direct payments under the CAP, were to be guaranteed a basic income and, more importantly, institutional support for investment planning, which provided the stimulus for mechanization of agricultural activities [

36]. Direct payments, in effect, allowed for an increase in the technical efficiency of agricultural production, and, combined with rural development funds, provided the basis for modernizing infrastructure and technology, driving the purchase of modern machinery and equipment by farms, introducing a range of organizational, process, and product innovations [

37].

On the one hand, the EU agricultural sector has seen a trend toward specialization and intensification of production on large farms, which have built their competitiveness on mass food production. This is primarily due to the fact that the CAP financial support mechanisms used to date have favored large farms [

38,

39,

40]. In addition, the economies of scale observed in the agricultural sector have motivated farms to increase the size of their farming operations [

11,

41,

42]. Such a model of agricultural activity is observed in France, Germany, Belgium, Luxembourg, and The Netherlands, but also in the Czech Republic and Slovakia, among others. On the other hand, farms in countries with a fragmented agrarian structure have developed farms producing on a smaller scale, spending less on modernization, basing the growth of their competitiveness on technologies that are more environmentally and socially friendly, often using support mechanisms for financing non-agricultural activities [

43] and shortening supply chains [

44,

45]. These practices are observed in most CEE countries, including Poland, Bulgaria, Estonia, Lithuania, Hungary, Latvia, and Romania, but also Italy. As a result, farms in the EU are diverse, including in terms of agrarian structure, economic strength, specialization, level of mechanization, and employment structure [

46].

Taking into account the conclusions of the literature review and the results of the above research, it is possible to identify special features that differentiate farms in Central and Eastern Europe from other farms in the EU [

46]. Farms in CEE are currently characterized by a similar level of production specialization to farms in other EU countries. In all CEE countries, there is a trend toward increasing specialization of agricultural activities, with the largest group of farms specializing in field crops and milk production. Compared to 2004, the share of farms without specialization engaged in mixed agricultural activities has decreased, although it is still higher compared to other EU countries. In addition, the agricultural sectors of CEE countries are characterized by a high share of small farms, i.e., farms of up to 5 hectares. In 2021, more than 60% of farms in CEE countries were small farms [

47]. Only the agricultural sectors of the Czech Republic, Slovakia, and Estonia were characterized by a structure in which the share of farms up to 5 hectares was significantly lower compared to the rest of the CEE countries, which were characterized by a significant share of farms over 100 hectares. The agrarian structure formed in this way is related to the economic size achieved by farms, as shown in the empirical research. Analysis of CEE farms in terms of economic size classes showed that all CEE countries (except the Czech Republic and Slovakia) are dominated by very small and small farms in terms of economic size classes. The dominance of very small and small farms in terms of economic size is a feature that permanently makes farms in CEE similar and distances them from farms in other EU countries, i.e., Germany and France. This is most likely strengthened by considerations of shared history and the aversion of farmers in CEE countries to collectivization of production [

48], and for this reason, the processes of increasing the scale of farm operations in CEE countries are slow. Most of the countries analyzed have seen only a slight increase in the number of large and very large farms. Farms in CEE countries, since joining the EU, have embarked on a period of technology and infrastructure modernization, developing production practices aimed at increasing productivity. As indicated by analyses by, among others, Fan et al. (2024) [

11] and Čechura et al. (2022) [

41], farms in Central and Eastern Europe, despite their small economic size, are now characterized by a high level of technical efficiency, have increasingly advanced technologies, growing capital potential, and are more specialized, mechanized, and innovative [

46].

In summary, farms in the countries of Central and Eastern Europe have embarked on a process of deep structural change since their accession to the EU, and at present, farms in these countries concentrate their agricultural activities in farms specializing in field crops and dairy farming, although still with a relatively high proportion of farms engaged in mixed activities. These farms are mainly small and very small farms in terms of area, with little economic strength. As the example of small farms in the Czech Republic, among others, shows, small farms support traditional farming methods, allowing regional production traditions to be preserved [

49]. Other research on small farms in EU countries, including in Central and Eastern Europe, indicates that carrying out production on small and very small farms is important for preserving and restoring biodiversity [

47]. In addition, it is becoming increasingly important that small mixed farms with farm characteristics in Central and Eastern Europe are strongly linked to local markets, which significantly shortens supply chains and affects food consumption patterns. Analyses of organizational and structural changes in the agricultural sectors in Poland, the Czech Republic, Hungary, Romania, Bulgaria, and Slovakia have revealed significant changes in the organization of supply chains that could permanently affect changes in the ways agricultural products are distributed [

46]. On the other hand, small and very small farms, despite being technically efficient, still achieve lower economic efficiency compared to large, specialized farms typical of EU countries, i.e., France, Germany, and The Netherlands [

49]. Therefore, they require separate treatment when determining financial support mechanisms under the CAP [

47].

The European Green Deal has set new rules for the EU agricultural sector, setting ambitious goals for reducing greenhouse gas emissions and improving the environment. By 2050, the EU’s agricultural sector, including those in CEE countries, must undergo a transformation toward sustainable and green agricultural production practices that make a trade-off between agricultural production and climate and environmental protection. The logic of implementing the EGD obliges each member country to create a series of related strategies at the national level, focused on achieving EU climate neutrality by 2050 across all sectors of the economy [

19,

20].

One of the areas that is able to achieve climate neutrality for the EU by 2050 is agriculture and food production and biodiversity protection. A strategy to reduce greenhouse gas emissions from the agricultural sector, develop sustainable agricultural practices, reduce the use of chemical fertilizers and pesticides, and promote organic food production is enshrined in the A Farm to Fork Strategy [

21]. The strategy assumes that by 2030, the EU agricultural sector will have a 50% reduction in the use of chemical pesticides and 20% of chemical fertilizers in field crops, and a 50% reduction in the use of antibiotics in animal husbandry. In addition, the strategy calls for 25% of the cultivated area to be farmed eco-logically by 2030. Complementing the EGD in the area of agriculture is, among other things, the EU Biodiversity Strategy for 2030 [

22], which, for the agricultural sector, sets out ways to restore natural ecosystems and protect land from degradation, and formulates goals for creating and enhancing natural areas on agricultural land.

In the past, farms in the EU, including in the countries of Central and Eastern Europe, concentrated food production around intensive farming practices, thereby increasing their economic efficiency, but food production was not sustainable. As the European Environment Agency points out [

50], agriculture is responsible for 11% of the EU’s greenhouse gas emissions. The 2019 European Green Deal [

13] assigns the agricultural sector a role in achieving EU climate neutrality. Changing agricultural production to be more sustainable and environmentally friendly is key to reducing greenhouse gas emissions from the agricultural sector.

The CAP actions to date have been effective, and the food security of EU citizens has been ensured. The agricultural sector has the conditions to provide enough food, and the existing financial support mechanisms for farms guarantee the affordability of the food produced. At present, CAP activities focus on supporting food production on sustainable or ecological farms, which is one way to achieve climate neutrality and environmental protection in the EU [

23,

24,

25]. This equires the creation of financial support mechanisms that promote other agricultural ecosystem services in addition to agricultural products, i.e., soil re-tention, food production in a manner consistent with nature, and water supply from surface water—ecosystems that integrate agricultural and natural ecosystems [

27,

28]. In the case of the CAP, this means a complete change in approach to the farm evaluation system from one based on achieving ever higher economic efficiency to one based on environmental efficiency. CAP 2023–2027 [

26] combines financial support for farms with the use of environmentally friendly farming practices, and uses a system of additional incentives for climate and environmentally friendly farming practices. A total of 40% of the CAP 2023–2027 budget has been allocated to support the implementation of climate goals that will bring the EU closer to achieving the EGD goals. An important element of the CAP 2023–2027, from the point of view of farms in the CEE countries, is the point about increasing financial support for small- and medium-sized farms by reducing the amount of subsidies for the largest farms.

The characteristics of farms in Central and Eastern Europe, particularly their small scales of operation, indicate that in light of the European Green Deal and updated farm financial support mechanisms under the CAP 2023–2027, these farms could be potential sources of competitive advantage for their agriculture and should now be the starting point for actualizing their agricultural development paths.

Up until now, the farms of the CEE countries have been modeled on the farm solutions of selected EU countries, i.e., France and Germany, which build their competitiveness on the increase in the scale of operations. The experience of these countries shows that the achievement of higher technical and economic efficiency is achieved in large farms and invested—technologically developed, innovative, and having the technical means for production agility. To date, CAP financial support mechanisms have promoted farms that achieve high crop and livestock productivity. As a result, field and animal farming are carried out on specialized large-scale farms with strong technological capabilities. Specialized and intensive agriculture helps achieve food security for EU citizens; it provides food in sufficient quantities and at an affordable price. However, for large-scale farms, EGD has set an ambitious goal—sustainability of agricultural practices and sustainable intensification [

51,

52]. Large-scale food farms are, in the broadest terms, mechanized, techno-innovative farms. The use of technology and technological advances, i.e., drones, sensors, and artificial intelligence, should help maintain or achieve higher levels of productivity while minimizing water waste and reducing fertilizer and crop protection product use [

53]. Similarly, in the case of livestock farming [

48], the use of technology to monitor animal welfare should improve productivity while reducing the environmental impact of livestock farming. As a result, there should be positive external environmental effects; in particular, there should be a significant reduction in greenhouse gases. Artificial intelligence used on large farms in a decade’s time should improve the production agility of large farms and enable climate-beneficial crop management. Large farms have, in fact, the potential to periodically allocate resources and yields [

54,

55,

56]. Research on the economic and ecological efficiency of lettuce cultivation in the UK conducted experimentally by the University of Cambridge, among others [

57], confirms that the use of precision agriculture is a promising method for reducing greenhouse gas emissions in the agricultural sector. A report by the European Parliament [

58] outlines good precision farming practices that are already in use in EU countries, including dairy farms in The Netherlands, Germany, and France. The efficiency of field crops and animal husbandry achieved through precision agriculture should become a major factor of environmental sustainability in agricultural production

Farms in Central and Eastern Europe, motivated by economies of scale, have followed a growth-based development path since accession to the EU, but the transformation process has not been completed. In Central and Eastern Europe, agricultural production is still carried out on small and very small farms, with the exception of the Czech Republic and Slovakia. Farms in Central and Eastern Europe achieve a high level of technical efficiency, but still require investment. These are characterized by higher labor force participation, less specialization, and less-intensive production practices. Agricultural production on small farms has been an obstacle to the development of CEE farms so far, but it may now become their greatest advantage.

EGD points out that small farms in some countries are key to the transformation of the EU agricultural sector. The direction of development of small farms supported in EU regulations is ecological farming [

59]; it is emphasized that small-scale farming can be a competitive advantage for some agricultural sectors [

60]. The concept of ecological agricultural intensification focuses its attention on indicating the economic, ecological, and social benefits of using ecological processes on farms [

61,

62]. The primary environmental and social benefits relate to optimizing resource use, increasing biodiversity at the farm and regional level, and reducing greenhouse gas emissions. As a result, there is a long-term increase in the resilience of agriculture to climate change; the quality of the environment improves—there are economic benefits on a global scale.

Small farms have a natural tendency to avoid synthetic fertilizers and chemical pesticides; instead, using their natural counterparts, i.e., compost, bone meal, and spraying with plant extracts, is common. In addition, they show less mechanization of production, with more field and human labor. Similarly, ecological animal husbandry introduces pasture in place of intensive agriculture [

63,

64]. In addition, feeds with a low carbon footprint are introduced into the animals’ diets, and manure is used, resulting in reduced methane and nitrous oxide emissions. The consequence of small-scale farming and animal husbandry is to reduce their impact on the climate and environment and contribute to the biodiversity of their crops and livestock, as well as to significantly improve the water management of the land. Small farms focus their operations on local, resistant varieties of plants and animals. In addition, small farms use regenerative farming practices to improve soil quality, including intercropping to reduce erosion and enrich soils with organic matter, and crop rotation [

23,

65]. They also follow the practice of combining agriculture with forestry elements [

62], making use of natural wind barriers, thus providing a microclimate conducive to biodiversity of species. They maintain natural markers of crop boundaries, i.e., hedgerows and water bodies. It is common practice to integrate pastures with orchards, such as raising animals in fruit orchard areas. An example of the use of green solutions and their impact on minimizing greenhouse gas emissions and improving biodiversity can be found on farms specializing in wine production. Abinandan et al. [

66] indicate that artificial wetlands and microalgae utilization systems are an effective method of minimizing the carbon footprint of the wine industry. The growing awareness of the negative environmental, social, and economic effects of intensive agriculture, both among the public and the farms themselves [

67,

68,

69,

70], is an additional motivation for the development of ecological agriculture. Small farms are increasingly selling their products directly, and producer cooperatives are being formed to support local agriculture. As a result, supply chains are shortened, environmental costs of transportation are reduced, and social ecosystems are improved.

_Li.png)

{kind=link}

{kind=link}

{kind=link}