Abstract

The field of CSR has witnessed considerable growth and established itself as a significant subject in family business studies. However, despite previous reviews exploring this topic from various angles, there remains a crucial gap in understanding the influence of diverse regulatory frameworks and social, environmental, and managerial values on the development of literature production and research streams across different regions. This gap holds particular significance for comprehending the latest advancements in this dynamic research field, particularly in emerging economies, where cultural and regulatory environments play a substantial role in shaping the attitude of family firms toward CSR. To bridge this gap, this paper conducts a comprehensive review of empirical studies focusing on sustainability in family firms. These studies are organized based on the country of study, and our review, based on a conjunct database derived from the Scopus and World of Science, encompasses 308 articles published between 1996 and 2023. Utilizing bibliometric software and adhering strictly to our inclusion criteria, we systematically grouped these articles into three distinct clusters: North American studies, European studies, and Asian studies. We found significant differences among areas regarding the main objectives, methodologies, and results of the research. This study comprehensively maps key themes and findings in family business sustainability, aiding researchers in organizing knowledge and guiding future investigations. Recognizing regional influences is crucial to ensuring representative and applicable research outcomes.

1. Introduction

Over the past decade, sustainability has garnered significant attention across various spheres—media, institutions, policy-making bodies, and both national and international organizations such as the United Nations. Corporate social responsibility (CSR) has emerged as a crucial tool in enterprise management, recognized for its pivotal role in tackling social issues [1].

While the exploration of sustainability in management studies traces back to the 1950s [2,3], the literature on CSR has experienced a recent, rapid expansion. CSR is now under investigation within diverse contexts, geographical regions, and business types, including state-owned firms [4,5], privately owned companies [6], and family-owned enterprises [7,8,9]. Understanding how CSR strategies evolve in distinct organizational settings and how sustainability drives competitive advantage and value creation has indeed become a focal point.

Family firms have drawn particular attention from practitioners and academics for several reasons. Firstly, their economic significance is noteworthy since they constitute almost two-thirds of all private businesses globally [10] and contribute significantly to GDP and employment, especially in countries like Brazil and the USA and in Europe (especially Italy and Germany), where they account for over 90% of the national economy [10]. Secondly, family firms possess unique characteristics that set them apart from other private entities. The intimate connection between family values and interests and a business significantly influences a firm’s culture, operational traits, and social conduct [11], potentially leading to different CSR practices. Moreover, there is a common belief that family-owned enterprises are deeply ingrained in their communities compared to non-family firms, impacting their societal influence.

The connection between family involvement and sustainability practices has been extensively explored in the literature, often through theoretical frameworks such as the resource-based view theory, social capital theory, organizational identity theory, socioemotional wealth theory, and inference theory [12].

Among the various theories interpreting this relationship, the socioemotional wealth theory and institution-based view stand out as the most commonly referenced [9]. According to the socioemotional wealth theory, families develop CSR policies to uphold their intrinsic values and, notably, the societal standing established by the family. Contrastingly, within the institution-based view, the behavior of family firms is significantly influenced by both formal and informal institutions, encompassing cultural values, norms, and the broader societal environment.

Therefore, corporate social responsibility in family firms unveils different and fascinating areas of study, as these firms often offer unique dynamics that influence their approach to CSR. The literature has increasingly explored CSR in family firms, investigating growing lines of research using different methodologies and approaches and referring to different geographical areas.

In recent years, scholars have progressively proposed a number of studies that have extensively outlined the evolving landscape of knowledge in this field, delineating various themes and approaches. From a methodological point of view, it is possible to identify studies that use bibliometric or systematic approaches (e.g., [13,14,15,16,17]), studies that rely on meta-analysis [9], and more qualitative approaches [18].

Ferreira et al. [16] identified four distinct clusters within the realm of family business studies: family business capital, strategy, social responsibility, and succession. These clusters denote pivotal areas that have garnered significant attention in the literature.

Mariani et al. [13] highlighted family involvement, corporate governance, and sustainability as recurring themes in family business studies.

Concurrently, Hidalgo et al. [19] delved into the main theories and approaches to CSR in family firms, offering insights into temporal trends and the evolution of CSR-related topics within the field.

With a similar approach, De las Heras-Rosas and Herrera [14] conducted a temporal analysis across three distinct periods (2003–2009; 2010–2014; 2015–2019), unveiling a diverse range of themes over time. Despite the escalating interest in this field, they observed fluctuating centrality in topics, indicating significant room for the further development and evolution of the literature.

Recent contributions have also highlighted the strong influence of cultural norms and regional contexts on the relationship between family firms and CSR, especially in diverse regulatory environments [20,21]. Cultural values and norms significantly shape corporations’ roles in addressing societal concerns [22,23] and influence the decision-making process of family owners regarding CSR strategies. These findings align with the meta-analysis conducted by Chen and Liu [9], demonstrating that the association between family firms and corporate social performance is contingent upon national cultural values, such as ingroup collectivism, human orientation, and future orientation. Additionally, social pressure on sustainability issues varies across regions, being historically higher in North American and European countries with a growing stakeholder orientation and lower in Eastern countries with a more pronounced shareholder-oriented culture [24].

Institutional theory suggests that “firms adapt to the regulations, incentive structures, and enforcement mechanisms within a country’s institutional environment” [25]. Consequently, the influence of stakeholders on firms’ strategies is intricately tied to the institutional environment, which exhibits significant disparities between developed and developing countries. Factors such as law enforcement, bureaucratic inconsistencies, property rights insecurity, and corruption may weaken stakeholders’ maturity and diminish their legitimacy [26,27]. Given the pivotal role of these factors in shaping stakeholders’ perceptions and their ability to influence firms’ strategies, it becomes pertinent to explore whether and to what extent these disparities have influenced the scientific approach to sustainability within family firms.

Despite several reviews and contributions [14,15,16,17,18,19], little focus has been placed on the influence of regional contexts and norms on literature production.

This study endeavors to bridge this gap by conducting a comprehensive bibliometric review employing social network analysis, co-citations, and co-words. This methodology involves categorizing and analyzing papers based on their respective countries of analysis. This technique not only encompasses the entirety of scientific field activities but also furnishes summaries that offer a broad perspective on research activities and their impacts, including insights into researchers, journals, universities, and countries [28]. Bibliometric analyses stand as a common and valuable tool for comprehensively analyzing the existing literature on a global scale [29]. Our objective is to shed light on corporate social responsibility (CSR) within family firms, drawing from a dataset of 308 papers spanning from 1996 to 2023 sourced from the Scopus and Web of Science (WoS) databases. Through this review, we seek to provide an updated and comprehensive analysis of CSR’s evolution within family firms in different regional contexts. We specifically aim to highlight the potential impact of varied regional contexts—identified by homogenous countries in terms of regulatory environments and social values—on literature production. Additionally, our analysis incorporates an assessment of the influence of the COVID-19 pandemic.

To address our research questions, we categorized countries into macro-regions based on two distinct criteria. Firstly, our objective was to establish homogeneous macro-regions considering regional and geographical contexts, regulatory approaches, and social environments. Secondly, we aimed to create sufficiently sized subsamples for conducting bibliometric analyses, encompassing thematic maps, keyword analyses, and co-occurrence networks. In our decision-making process, several pivotal choices shaped our approach:

- Grouping Western European countries based on their shared regulatory and social environments, despite occasional differences in sustainable development and perception [30]. This group was separated from Eastern European countries, which are characterized by less mature but recently evolving studies on CSR in family firms.

- Distinguishing North American countries from Latin American countries.

- Considering Asian countries collectively, a decision founded on various factors. Firstly, prior studies illuminate distinctive ownership and control patterns in Asian companies compared to the Western norm, highlighting specific pertinent issues [24]. Additionally, the existing literature underscores historical differences in stakeholder pressure for corporate social responsibility (CSR) between the USA, Europe, and Asian countries [24,31]. This variation is tied to the distinct social contexts wherein family firms operate: Western nations lean toward a stronger stakeholder orientation, exerting more considerable institutional pressure on firms to meet stakeholder demands [32,33,34]. Conversely, Asian countries exhibit a more shareholder-centric culture. As a result, family enterprises in Asia often prioritize their personal financial well-being, subsequently perceiving corporate social responsibility (CSR) as relatively inconsequential [35,36,37].

Despite the increasing research focus on sustainability in family firms, bibliometric studies on this topic are still limited. To our knowledge, this is the first updated bibliometric review delving into national and regional influences on literature production.

In our opinion, a notable strength of this contribution lies in its systematic approach, which categorizes research samples by region or country of analysis and assesses how regulatory and environmental factors impact literature production. A key finding refers to the relatively recent growth of CSR research in family firms, especially after 2000. Moreover, our contribution tries to focus on the global growth of sustainability awareness; the rising significance of sustainability is especially evident in Asian markets, albeit with a delayed trajectory compared to Europe and North America.

We expect our findings will bear substantial implications for both researchers and policymakers, providing valuable insights for family businesses and sustainability researchers. Our study has the potential to contribute to the literature by not only highlighting the most relevant trends but also by proposing a research agenda for future studies in this domain.

2. Methodology

To answer our research question and to gain insights into the current debate and identify leading trends in the literature, this study employs a combination of bibliometric techniques, such as citations, keyword analysis, and content analysis [38,39]. A bibliometric analysis is a widely used tool for globally analyzing the existing literature. It involves applying quantitative and statistical analysis to publications and their citations to assess the state of the literature and providing comprehensive data on the activities and impacts of research in a specific field. The study employs both the Scopus and Web of Science (WoS) databases, which are recognized as reliable tools extensively used in previous bibliometric research [40,41,42]. There has been substantial debate in the literature regarding the comparison between Scopus and Web of Science. While Scopus is acknowledged for its broader coverage compared to WoS, especially suitable for smaller research areas [43], such as the focus of sustainability within family firms, WoS offers superior graphics and more detailed citation analysis than Scopus [44]. Scopus and WoS are also widely acknowledged for their great compatibility in combination with Vos Viewer and Bibliometrix, along with the Biblioshiny package in the R program [42,45], which we have used as a primary tool to comprehend the structure of the literature. Consequently, the inclusion of both databases enables us to minimize the risk of overlooking relevant publications on the topic and capitalize on the strengths of each.

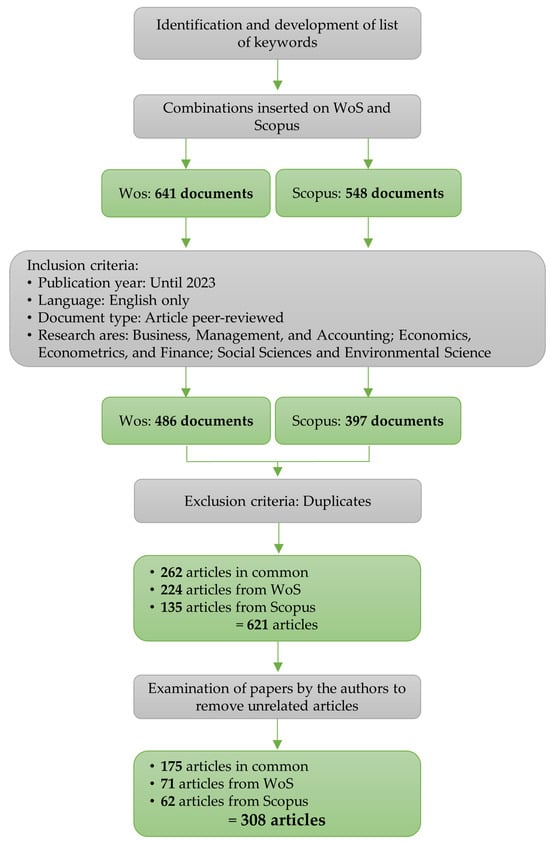

To conduct the bibliometric review, we performed the methodological process summarized in Figure 1. In the first step, we developed a keyword search in the Scopus and WoS databases and executed it in December 2023. These keywords were identified after a thorough review of the seminal papers in the field of CSR in the family firm’s environment. The resulting search included two set of keywords. The first set dealt with the identification of sustainability-relevant research using: “CSR” or “Environment* social* and governance” or “ESG” or “Corporate* social* responsib*” or “social* responsib*” or “corporate social initiative*” or “corporate responsib*” or “ethic”. The second set focused on the literature on family firms: “family firm*” or “family business*” or “family governance” or “family owner*” or “family CEO*” or “family enterprise” or “family control” or “family owned business*” or “family owned compan*” or “family owned firm*” or “family run business*” or “family managed business*” or “family owned enterprise*”. By screening all search results that included both a keyword from the two groups in the title, abstract, and author’s keywords, we identified 641 studies in WoS and 548 documents in Scopus. In the second step, we only included peer-reviewed articles in the English language and belonging to the areas of business, management, and accounting; economics, econometrics, and finance; social sciences; and environmental science. Considering our objective to comprehensively review the entire body of literature and gain insight into the latest developments in a highly dynamic field, our search was not constrained by a specific date. Consequently, we retrieved papers written up to the year 2023. The second step resulted in the identification of 486 documents in WoS and 397 in Scopus. The third step consisted of merging the two samples by removing duplicates. In the last step, each author performed an independent, one-to-one, detailed examination of each paper in the dataset in order to remove unrelated and not relevant articles, resulting in a final sample of 308 papers.

Figure 1.

Methodological process and results. Source: authors’ elaboration.

We further conducted a comprehensive examination of each paper to detect their research methods, which were categorized as quantitative, qualitative/conceptual, or reviews (bibliometric, systematic, or meta-analyses), and the countries of study. The results, as presented in Table 1, reveal that the majority of papers employed a quantitative approach, while about 10% were qualitative or conceptual, and 3% were reviews. Regarding the research-originating study, our analysis indicates that research on corporate social responsibility in family firms encompasses both developed and emerging economies. The most frequently studied countries were China (12.4%), followed by the USA (12.0%) and Italy (7.5%). Of the studies obtained, 14.3% refer to an international sample.

Table 1.

Sample description.

Regarding macro-regions, Asia led with 108 studies, followed by Western Europe with 67 studies and North America with 38 studies. Due to data constraints, we narrowed our comparison down to three specific clusters of papers focusing on Asia, Europe, and North America. Other regions exhibit relatively limited and recent scientific production. Consequently, using bibliometric techniques in these regions might yield misleading or non-generalizable results.

3. Results

We analyzed the four clusters of papers resulting from our research using VoS Viewer 1.6.20 and the R-package Biblioshiny 4.1.3, which provides comprehensive features, including conceptual structure and thematic analysis, as well as various tables and graphs [46].

3.1. Descriptive Analysis

As indicated in Table 2, the entire sample of quantitative papers (n = 308) was written by 732 authors and published in 129 journals, spanning from 1996 to 2023. The average citation level per document was 29.2. On average, each document had 2.46 authors, indicating that most articles had at least two authors. This is further supported by the average number of co-authors per document, which was 2.87. Notably, only 32 papers were authored by a single individual, comprising approximately 10% of the total, underscoring a significant level of collaboration in sustainability publications.

Table 2.

Summary of articles.

When examining the three subsamples, it became evident that the level of collaboration and the number of international co-authors were notably higher in the Western European sample. This subsample indeed exhibited a much lower percentage of single-authored documents compared to the entire sample.

Table 2 further demonstrates that pioneering studies in the late 1990s on sustainability in family firms were primarily focused on European and North American countries. This suggests that these regions historically placed more emphasis on sustainability issues compared to their Asian counterparts. Additionally, these studies show a higher number of citations (average of 38.27 and 64.71 for Western Europe and North America, respectively), suggesting that these papers are generally consulted by researchers investigating the topic.

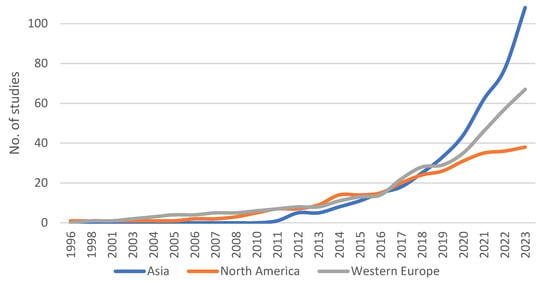

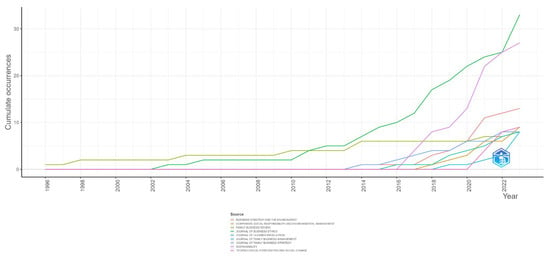

Figure 2 illustrates the evolution of the field in terms of the cumulative number of publications. The literature on sustainability in family firms emerges heterogeneously in the regions under analysis: research on western countries began to grow in the early 2000s, while studies in Asian countries show a delay of about eight years. It is noteworthy that nowadays Asia is becoming increasingly attractive for researchers, with an annual growth rate of 33.74%, compared to 9.65% and 2.6% for Western Europe and North America, respectively.

Figure 2.

Cumulative frequency of published documents. Source: authors’ elaboration using Biblioshiny package 4.1.3 in R.

The substantial difference in the growth rates of Western European and North American studies becomes more pronounced after the COVID-19 pandemic. Before the pandemic, studies in the two regions followed a similar pattern. However, after the crisis, the two lines diverged. This behavior could be explained by the interest raised around significant regulatory interventions by the European legislator, which has implemented various initiatives to strengthen the transparency of sustainability disclosures, develop responsible approaches, and regulate taxonomies and investments toward sustainability.

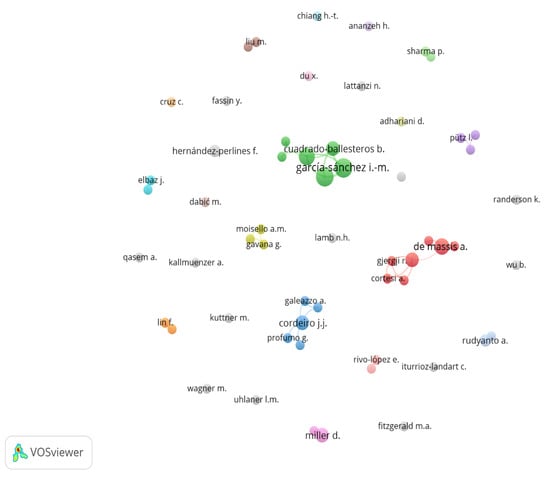

We analyze the network among researchers investigating sustainability in family firms. Figure 3 graphically represents the relationships among authors in the production of papers and the intensity of these relationships. The size of the nodes indicates the number of contributions by an author, and the thickness of the lines specifies the frequency of scientific collaborations in which scholars have worked together. First, the analysis reveals that only eleven authors have more than three publications on the topic and that such productive authors work in the same clusters. The most productive author is García-Sánchez I.-M., followed by Martínez-Ferrero J. and Rodríguez-Ariza L. Second, the figure shows a high number of authors with very few and weak relationships and limited relevance in terms of citations. This suggests that the majority of authors work in isolation, and there are no leading groups in this area of study. An exception is represented by the green, red, and blue groups, mainly composed of European authors. These results further highlight the intuition that Europe is currently leading research on these topics, particularly in Spain and Italy.

Figure 3.

Authors networks by normalized citations. Source: Vos Viewer 1.6.20.

A similar trend emerges when examining the top fifteen universities. Table 3 indicates that the University of Salamanca holds the most influential position, followed by the University of Granada and Erasmus University Rotterdam. Within the top fifteen, Spain boasts four institutions, while Italy is represented by three. Once more, countries like Spain and Italy demonstrate a higher concentration of production within a select few universities and research groups, while other nations display a greater dispersion of literature production. In support of the findings depicted in Figure 3, additional untabulated results reveal that only 28 institutions exhibit more than four affiliations, and a striking 63% of the universities (277 out of a total of 433) within the sample are associated with only one affiliation.

Table 3.

Most influential universities.

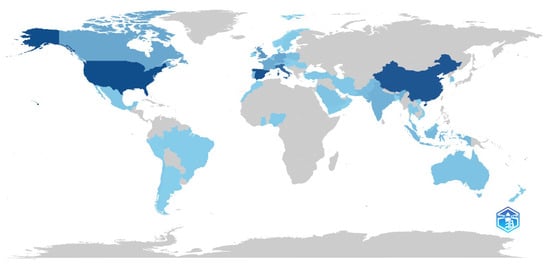

Figure 4 illustrates the countries where the theme of CSR in family firms has been explored. The intensity of the blue color corresponds to the scientific production level of each country. Leading the list is the USA, with the highest number of articles on the topic (85). Spain (81) and Italy (66) exhibit significant literature production in Europe and globally rank among the most prolific. China follows closely with 79 articles, while the United Kingdom (35), Canada, Germany (25), France (23), India (19), and the Netherlands (16) also contribute to the discourse.

Figure 4.

Countries’ scientific production. Source: Biblioshiny package 4.1.3 in R.

The figure notably highlights the theme’s development in specific regions, particularly in North America, Western Europe, and—more recently—Southeastern Asia. It is evident that several areas have recently begun participating in the scientific debate, such as the Middle East and Latin America.

The 308 reviewed studies were published in 129 journals until 2023. Table 4 lists the journals with the highest number of published articles and citations. The table reveals that articles on sustainability in family firms are predominantly featured in journals focused on general management, social responsibility, and ethics. The leading journals in terms of the most publications are the Journal of Business Ethics (33 articles) and Sustainability (27 articles), while other journals exhibit a lower number of published studies. Among the remaining 114 sources, 85 published only one article.

Table 4.

Most influential journals.

In terms of the number of citations, the Journal of Business Ethics outperforms other sources, covering 20.93% of the citations. The second most cited journal is Entrepreneurship: Theory and Practice. Despite this journal publishing only four articles on CSR in family firms, it hosts the most cited papers on the topic, namely works by Dyer and Whetten [47] and Cruz et al. [48].

Table 4 also indicates a certain degree of concentration among the most recurrent journals, as the first fifteen sources account for 50.97% and 65.82% of the total in terms of the number of articles and citations, respectively.

Figure 5 depicts the cumulative increase in the number of publications by each top journal. Since 2016, the number of publications by the Journal of Business Ethics and Sustainability has seen a significant increase. These journals have recently surpassed more specialized journals such as family business review, which is primarily devoted to the exploration of the dynamics of family firms. While Family Business Review was the primary outlet until 2011, in the last decade, Sustainability and the Journal of Business Ethics have emerged as the main sources for studies, becoming fundamental publications for academics and policymakers focused on sustainability disclosure topics. This suggests that topics related to family firms are no longer confined to specialized journals but are welcomed in a broader range of sources, indicating the increasing interest among scholars and editors.

Figure 5.

Cumulative source growth by total number of published documents. Source: Biblioshiny package 4.1.3 in R.

Untabulated results show that Sustainability is the preferred output for studies on European countries (18.12%), while the Journal of Business Ethics is the main source for Asian and North American research (8.2% and 23.44%, respectively).

3.2. Co-Occurrence Network

The primary topics and main research streams stem from the words integrated into the research strategy. They are a direct outcome of the initial decisions made during the sample definition. We have included the most important keywords and their similarities to optimize the sample composition for the analysis, enhancing the breadth of our coverage in the analysis process.

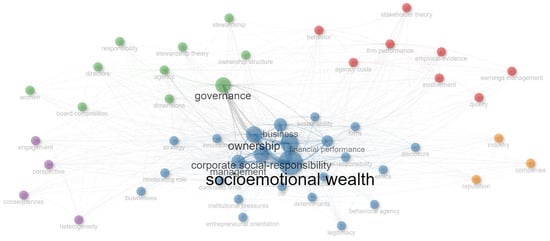

The aggregate representation of the co-occurrence network, as shown in Figure 6, unveils the presence of one larger research stream and four smaller clusters distinguished by distinct colors.

Figure 6.

Topics’ relevance as analyzed in the co-occurrence network. Source: Biblioshiny package 4.1.3 in R.

Firstly, the largest cluster encompasses a lot of diversified keywords that refer to the relationship between CSR and sustainability and firms’ financial performance, as expressed by several determinants related to innovation, CSR strategies, ethics, and entrepreneurial orientation. Among others, disclosure deserves a particular mention. This issue is declined according to different points of view: CSR disclosure and environmental disclosure are the most common. The quality and depth of the information provided to the financial markets, to the social communities, and to all the categories of shareholders are expected to increase over time to enhance the quality of social and economic reporting. Therefore, the markets’ evaluation will be related to a full and large set of data and qualitative information about firms’ businesses.

The smaller clusters are related to this one, representing more specific research streams. Among them, governance deserved large attention by researchers (green cluster). Governance issues highlight several factors expected to influence family firms’ management, with a clear focus on strategies, organization, ownership structure, and board composition. Also, issues about gender composition and board diversity are highlighted. Family firms are characterized by specific challenges, for example, family involvement and generational succession toward the future of a business.

Further, we detected a specific research stream that referred to performance (red cluster): the linkage with the first and largest cluster is very significant. The relationship between CSR and economic performance has become increasingly tight over time, but non-financial performance has also gained importance. So, regardless of a firm’s size and business model, the integration of a performance analysis related both to economic and non-financial contents offers a comprehensive overview of a firm, its governance, and its business. According to the increasing use of the integrated report, we may expect that the importance of this stream will grow in the next few years for family firms too. Among others, this cluster unveils the relevance of some issues referred to as earnings management, agency costs, and stakeholders’ theory, which can drive firms’ equilibria over time.

A further small research stream, even if limited in its diffusion, is tied to the role of reputation (yellow cluster). We believe that the focus in this area is particularly relevant for family firms, both considering reputation defense to be the most crucial element moving family firms in CSR and considering reputation as an element deriving from an effective system of values for a firm and its environment. Despite its relevance, empirical studies in this area seem relatively scarce.

The purple cluster appears less represented and quite diversified, and it does not show a clear and direct linkage with the largest one.

Among the untabulated results, we can observe that European studies highlight the presence and relevance of a larger research stream, where the most important issues are related to firms’ management. Despite the large size and diversification of the issues, some issues stand out as particularly relevant. Among the others, we highlight studies devoted to ownership structure, board composition, financial performance, and business strategies. Other subclusters are less represented and carry less significance in these studies.

Even if most cited keywords are similar to the rest of the sample, Asian studies—which are, on average, relatively newer—offer some specific focuses on the most relevant theories about firms’ management and governance. In further detail, several studies unveil issues related to socioemotional wealth, behavioral agency and disclosure, and agency costs. This research stream also delves into its relationship with CSR studies and its impact on a firm’s financial performance.

American studies are mainly focused on socioemotional wealth, business, performance, and the relationship with CSR. Despite the fact that the granularity of keywords is more limited, some specific research streams appear. They refer, for example, to “shareholder activism”, the relationship with financial performance, and long-term orientation as crucial components of a business strategy for future performance.

3.3. Thematic Evolution

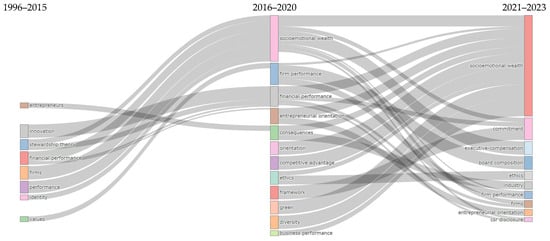

As often reported in other similar studies, Figure 7 summarizes the evolution of research and the history of themes over time using authors’ keywords. In order to analyze the differences in keywords’ relevance over time, we split the overall time horizon (1996–2023) into three segments: the first period, the longest one, ranges from 1996 to 2015, the second one is in the range 2016–2020, and the last one encompasses the last three years (2021–2023). We also tried different time limits, but we only noticed small differences.

Figure 7.

Thematic evolution. Source: Biblioshiny package 4.1.3 in R.

The identified “time windows” were established based on specific key dates. In 2015, for example, the Paris Climate Agreement was signed and the 17 SDGs were adopted by the United Nations; in 2020, we had the outbreak of the COVID-19 pandemic. We can expect that these milestones have pushed firms and scholars as well to devote more attention to the relationship between CSR and performance, as well as its impact on their business, in terms of risks, efficiency, and sustainability.

Moreover, it is worthy to mention that in recent years, the number of contributions has largely increased; these topics attracted a growing interest from researchers, but the mix of topics changed over time. Also, the geographical heterogeneity increased, with a higher number of papers coming from Asian countries or based on Asian firms.

In the first stage (1996–2015), among the most cited authors’ keywords, we can observe a major focus on “basic” topics, referring to firms’ identity, financial performance, and the role of innovation. In the second stage, as the number of contributions increased, we noted a greater diversification in keywords. Solid and basic profiles, however, are still relevant, i.e., the management of family firms and strategic decisions, the entrepreneurial orientation, the analysis of the market, and the competitive advantage. Socioemotional wealth theory rises in importance, as well as topics related to ethics, diversity, and green orientation. In the final stage (2021–2023), the words’ distribution remained similar, while socioemotional wealth, executive compensation, and board composition—related to financial performance—gained more attention. As is known, during the pandemic, global economies faced a severe recession, and firms had to face new challenges; new economic equilibria are required to face new risks. Sustainability is increasingly integrated into firms’ strategies, as evidenced by the growing significance of ethics and CSR disclosure. These aspects are among the most frequently cited items in the latest time segment, shaping entrepreneurial orientation.

3.4. Thematic Maps

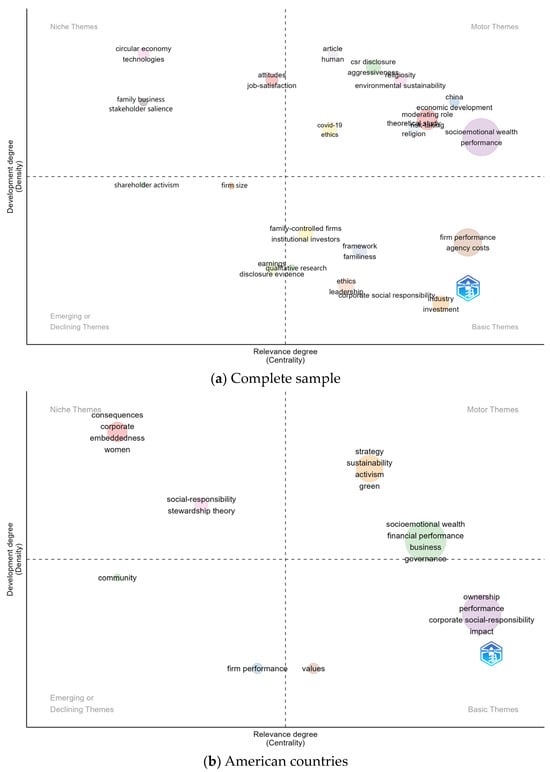

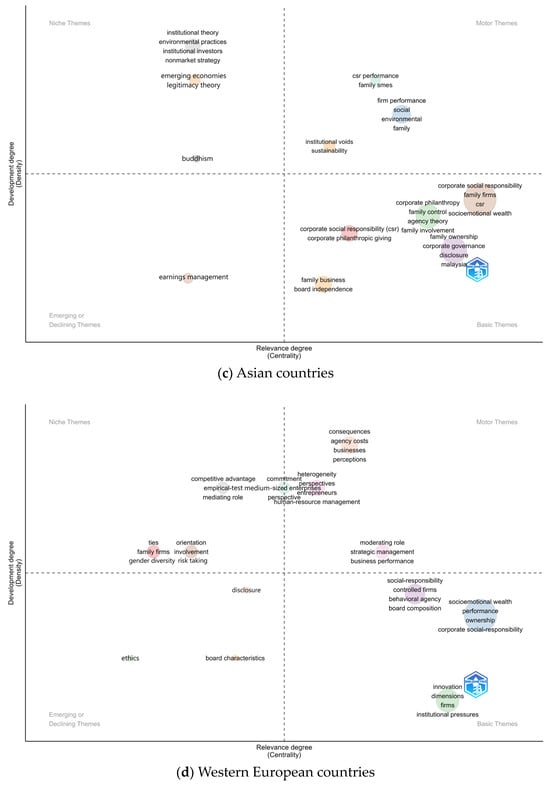

Figure 8, which summarizes the relevance degree (centrality) and the development degree (density), suggests four macro-types of themes to be analyzed: “motor themes” are characterized by high centrality and density, while—on the opposite end of the scale—we have “emerging or declining themes”. Intermediate sections encompass both themes that are central but have a low level of development (“basic themes”) and themes that are well developed but less central (“niche themes”). Some remarks are worth mentioning.

Figure 8.

Thematic maps. Source: Biblioshiny package 4.1.3 in R.

The “basic themes” section shows a high concentration of relevant topics, which characterize many contributions. The most important keywords refer to family business/family-controlled firms, agency costs, firms’ performance, and corporate social responsibility. These topics have remained central over time, and they are useful for building a general framework to analyze firms’ strategies with regards to CSR and sustainability. These basic themes are studied extensively in our sample.

“Niche themes” show low centrality and a high level of development; despite the small size of this section, the cited themes appear quite interesting and challenging, as they include—among others—circular economy, the role of technologies, and job satisfaction. The latter suggests closer attention to empirical studies about the “social role” of firms, especially with regards to policies toward employees and workers. This encompasses aspects such as the quality of the work environment and work–life balance. “Motor themes”, with high density and centrality, are heavily represented. They unveil high diversification by themes, ranging from socioemotional wealth and performance to CSR disclosure and environmental sustainability. This research stream emphasizes the increasing significance of information, encompassing both financial and non-financial data, available to shareholders, stakeholders, and financial markets.

A quite interesting point refers to the positioning, within this section, of empirical studies based on Chinese firms. This result appears consistent with the recent significant growth in the number of contributions analyzing China, India, and other Asian countries. In the last 3 years, the COVID-19 pandemic has represented a “motor theme”.

The diffusion of “emerging or declining themes” is quite limited, as suggested by the small size of the bubble.

The interpretation of the thematic map of the subsamples offers some interesting insights. The Asian contributions highlight the relevance of institutional voids as a “motor theme”, suggesting the necessity of a deeper regulatory intervention on sustainability issues, which is still mainly driven by the initiatives of individual companies, which are now using CSR to signal to foreign investors that they have more governance structures than other regional competitors [49]. Among others, the “motor themes” suggest the relevance of contributions addressing topics that explore the relationship between CSR and a firm’s environmental and financial performance. The centrality of these issues is further highlighted within the cluster labelled “basic themes”: research investigating Asian firms concerning their social role, particularly in corporate philanthropic giving, and their strategies aimed at establishing social reputation and developing a favorable business environment through comprehensive disclosure.

With regards to “basic themes”, European studies are primarily focused on CSR, business performance, and strategic issues related to ownership and board composition. The evolution of the latter is also a result of the regulatory framework, which in recent years has strengthened the criteria for assessing the effectiveness of firms’ governance. Actually, board characteristics are one of the emerging themes, and studies about gender diversity have gained importance over time. It is worthy to mention the relevance of studies dedicated to institutional pressures and their impact on firms. These studies delve into strategic responses, business orientation, and ownership, posing unique challenges for family firms.

American studies demonstrate a strong central focus on fundamental themes surrounding family business, the historical evolution of corporate social responsibility, and its impact on a firm’s performance. These studies particularly emphasize the relationship between sustainability performance and financial performance, underscoring a heightened focus on this correlation.

The themes covered in American studies are less diversified. Sustainability, green investments, and socioemotional wealth gained centrality (“motor themes”), while the characteristics of embeddedness and stewardship theory are “niche themes”.

3.5. Word Cloud

The word cloud depicted in Figure 9 is generated from the keyword plus, derived from the entire sample of selected studies. The size of the font corresponds to the frequency of the appearance of a specific keyword in the literature. Consistent with what has been observed in the previous sections, the main keywords reflect the themes that have received particular attention from authors. The three primary sets of keywords reflecting the main research themes can be summarized as follows.

Figure 9.

Words cloud. Source: Biblioshiny package 4.1.3 in R.

The first is characterized by the term “socioemotional wealth”, which is linked to qualitative and quantitative analyses regarding the interpretation of motivations and specific logics directed toward the involvement of family firms in sustainable activities. From this standpoint, it becomes evident that the socioemotional wealth theory is significantly the most established and studied theory in the literature.

The terms “management”, “governance”, and “ownership” reflect the particularly relevant role of managing family firms and the implications for sustainability policies. This is viewed in light of the specific relationships that may emerge in the presence of family CEOs or significant family influence in managerial decisions, as well as the close relationships these firms establish with their stakeholders and their surrounding environment.

The third group of keywords reflects the themes of “financial performance”, “performance”, and “business”, confirming that appropriate sustainability policies can only be promoted in the presence of adequate financial returns or if such sustainability policies enable achieving greater financial returns or increases in the market value of companies.

Within specific geographical clusters, notable keywords have been identified in the literature. European studies prominently feature themes like corporate social responsibility and sustainability. However, there is a distinct emphasis on governance approaches, decision-making processes, and environmental issues. Particularly, environmental management holds significant weight within the European context, driven by substantial regulatory emphasis.

The literature on this topic in Asian countries, while sharing the most common keywords, introduces several other terms such as firm ownership, firm size, religion, and corporate philanthropy. This highlights the traditional inclination of Asian firms to prioritize charity over cultivating a culture of social responsibility within their organizations [50].

American studies encompass a wide array of common keywords, like socioemotional wealth and corporate social responsibility. Additionally, there is notable attention toward issues concerning firms’ performance, ownership structure, and family businesses.

Upon comparing these three clusters, Europe emerges as the primary catalyst for the environmental revolution. This distinction arises due to the relatively lower importance placed on this issue in the other clusters, where the frequency of environmental topics is notably lower.

4. Discussion

Family businesses hold significant importance within society and as economic operators and have been extensively studied. Our bibliometric analysis spanned from 1996 to 2023, specifically focusing on sustainability within the context of family firms. We categorized our research sample into papers centered on Western European, North American, and Asian countries, aiming to assess the potential influence of diverse regulatory frameworks and cultural norms on literature production.

The analysis of trends in publications on CSR practices in family firms provides insights into the primary research directions and the evolving landscape across themes, authors, and, crucially, regional and regulatory contexts.

Our systematic literature review unveiled that corporate social responsibility (CSR) remains relatively limited within family firm research but is steadily gaining prominence. While early contributions date back to 1996, interest in CSR within family firms significantly expanded after 2000 and is notably evident in European and North American studies. On the other hand, Asian studies exhibit an approximate eight-year lag. While its inception stemmed from studies in Western Europe and North America, the focal point has now shifted. Many influential papers shaping future research trajectories concentrate on emerging markets. This shift mirrors the gradual diffusion of the demand for a more sustainable approach by firms, a critical factor given the substantial Co2 emissions attributed to these countries.

The analysis highlights the pivotal role of the COVID-19 pandemic, prompting significant regulatory interventions by the European legislator. These interventions aimed to enhance transparency in sustainability disclosures, foster responsible approaches, and regulate taxonomies and investments toward sustainability.

In addition, this study underscores the significant influence of diverse contexts, regulatory frameworks, and economic systems on family firms’ engagement in CSR practices, directing the literature production on this subject. This has vital implications, emphasizing the need to integrate the specific business environment contexts of family firms and acknowledge variances in normative influences within environments. For instance, within the EU context, the heightened awareness of sustainability and climate-related issues has led to regulatory interventions focusing on ESG (environmental, social, and governance) factors. Consequently, the literature has shifted markedly toward exploring managerial implications and the implications of broader transparency and disclosure.

Conversely, while the literature on this topic in Asia is experiencing rapid growth, it retains a foundational CSR approach, where philanthropic orientation remains significantly entrenched in local cultures. However, there is an increasing interest in CSR among firms and investors, calling for deeper regulatory intervention to signal better governance structures to foreign investors compared to regional competitors.

Overall, this subject has garnered substantial attention, diversifying thematically and geographically. While CSR and governance remain fundamental, emerging topics like disclosure and environmental concerns, especially in the European context, are gaining prominence within the broader scope of corporate responsibility.

4.1. Implications

This study holds significant implications for sustainability studies on family businesses by meticulously identifying the investigated issues, their contributions, and key findings. It serves as a valuable literature map, offering insights into the primary topics discussed, the findings, uncertainties, and future research directions. Our framework should aid researchers in organizing existing studies, facilitating a deeper comprehension of this phenomenon, and guiding future investigations to address impending issues and inquiries.

A crucial takeaway from this analysis is the recognition that when regional contexts, regulatory frameworks, and social environments shape the relationships between phenomena, research analyses must account for these factors. Failing to do so might yield outputs that lack representativeness or adequate generalizability.

Moreover, while this type of analysis might be more beneficial for academia than for regulators and policymakers, it is vital to note that certain results can have tangible implications. Specifically, the concerns raised regarding institutional voids highlight the necessity to intervene and eliminate barriers such as arbitrary law enforcement and bureaucratic inconsistencies. Addressing these obstacles is critical to maximizing the positive impact of promoting sustainable initiatives and strategies among firms.

4.2. Limitations and Future Research Agenda

Our study acknowledges several limitations, each suggesting potential avenues for future research.

Firstly, our use of specific databases might not encompass all relevant papers. However, this is mitigated to some extent by employing two widely used databases (Web of Science and Scopus), reducing the risk of missing references. Incorporating additional sources could further mitigate this limitation.

Our study is confined to exploring the narrative and bibliometric dimensions of the sustainability literature within family firms. To enhance this analysis, we urge scholars to employ more advanced tools like text mining. This approach would enable a deeper understanding of the connections and networks between documents and studies. Proposing new meta-analyses encompassing diverse countries and regions would further reinforce our findings. Therefore, additional research is imperative to advance and refine our analysis. Moreover, the absence of a universally accepted definition of family firms presents challenges for drawing conclusions with external validity. Establishing a comprehensive definition is crucial to reducing heterogeneity in this field.

Additionally, the limited sample sizes, especially in the American subsample, restrict comprehensive overviews and specific tests for robust results regarding thematic evolutions. This limitation might hinder the generalizability of our findings. However, it is intrinsic to the nature of this investigation. The output stems from a conscientious trade-off aiming to balance two conflicting needs: the necessity for relatively large subsamples and an overall homogeneous sample that effectively represents regional contexts with specific nuances. Future research endeavors should prioritize a robust methodological approach and ensure data quality to enhance the generalizability of the results. This step will significantly contribute to further theoretical advancements in understanding sustainability within the realm of family firms.

Moving forward, future research could focus on conducting longitudinal studies to analyze the evolution of CSR practices within specific regional contexts, comparing the effectiveness of CSR initiatives across diverse regulatory environments, exploring stakeholder engagement within varied regional landscapes, and conducting behavioral studies to comprehend how societal perceptions and cultural norms impact CSR adoption by corporations within different regional contexts.

Author Contributions

Conceptualization, A.C., R.L. and A.U.; methodology, A.C.; software, A.C.; validation, A.C.; formal analysis, A.C.; investigation, A.C., R.L. and A.U.; resources, A.C., R.L., A.U.; data curation, A.C.; writing—original draft preparation, A.C., R.L. and A.U.; writing—review and editing, A.C., R.L. and A.U.; visualization, A.C., R.L. and A.U.; supervision, R.L.; project administration, R.L.; funding acquisition, R.L. All authors have read and agreed to the published version of the manuscript.

Funding

This work is part of the project NODES, which received funding from the MUR—M4C2 1.5 of PNRR, funded by the European Union—NextGenerationEU (grant agreement no. ECS00000036) [A.C., R.L.].

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

No new data were created or analyzed in this study. Data sharing is not applicable to this article.

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Barnett, M.L. The Business Case for Corporate Social Responsibility. Bus. Soc. 2019, 58, 167–190. [Google Scholar] [CrossRef]

- Bowen, H. Social Responsibilities of the Businessman; University of Iowa Press: Iowa City, IA, USA, 1953. [Google Scholar]

- Carroll, A.B. Corporate Social Responsibility. Bus. Soc. 1999, 38, 268–295. [Google Scholar] [CrossRef]

- Tan, D.; Bilal; Gao, S.; Komal, B. Impact of Carbon Emission Trading System Participation and Level of Internal Control on Quality of Carbon Emission Disclosures: Insights from Chinese State-Owned Electricity Companies. Sustainability 2020, 12, 1788. [Google Scholar] [CrossRef]

- Komal, B.; Bilal; Ezeani, E.; Shahzad, A.; Usman, M.; Sun, J. Age Diversity of Audit Committee Financial Experts, Ownership Structure and Earnings Management: Evidence from China. Int. J. Financ. Econ. 2023, 28, 2664–2682. [Google Scholar] [CrossRef]

- Liu, Q.; Bilal; Komal, B. A Corpus-Based Comparison of the Chief Executive Officer Statements in Annual Reports and Corporate Social Responsibility Reports. Front. Psychol. 2022, 13, 851405. [Google Scholar] [CrossRef] [PubMed]

- Payne, G.T.; Brigham, K.H.; Broberg, J.C.; Moss, T.W.; Short, J.C. Organizational Virtue Orientation and Family Firms. Bus. Ethics Q. 2011, 21, 257–285. [Google Scholar] [CrossRef]

- Breton-Miller, I.L.; Miller, D. Family Firms and Practices of Sustainability: A Contingency View. J. Fam. Bus. Strategy 2016, 7, 26–33. [Google Scholar] [CrossRef]

- Chen, J.; Liu, L. Family Firms, National Culture and Corporate Social Performance: A Meta-Analysis. Cross Cult. Strateg. Manag. 2022, 29, 379–402. [Google Scholar] [CrossRef]

- International Family Enterprise Research Academy (IFERA). IFERA Family Businesses Dominate. Fam. Bus. Rev. 2003, 16, 235–240. [Google Scholar] [CrossRef]

- Daspit, J.J.; Chrisman, J.J.; Ashton, T.; Evangelopoulos, N. Family Firm Heterogeneity: A Definition, Common Themes, Scholarly Progress, and Directions Forward. Fam. Bus. Rev. 2021, 34, 296–322. [Google Scholar] [CrossRef]

- Bargoni, A.; Alon, I.; Ferraris, A. A Systematic Review of Family Business and Consumer Behaviour. J. Bus. Res. 2023, 158, 113698. [Google Scholar] [CrossRef]

- Mariani, M.M.; Al-Sultan, K.; De Massis, A. Corporate Social Responsibility in Family Firms: A Systematic Literature Review. J. Small Bus. Manag. 2023, 61, 1192–1246. [Google Scholar] [CrossRef]

- de las Heras-Rosas, C.; Herrera, J. Family Firms and Sustainability. A Longitudinal Analysis. Sustainability 2020, 12, 5477. [Google Scholar] [CrossRef]

- Stock, C.; Pütz, L.; Schell, S.; Werner, A. Corporate Social Responsibility in Family Firms: Status and Future Directions of a Research Field. J. Bus. Ethics 2023, 1–61. [Google Scholar] [CrossRef]

- Ferreira, J.J.; Fernandes, C.I.; Schiavone, F.; Mahto, R.V. Sustainability in Family Business—A Bibliometric Study and a Research Agenda. Technol. Forecast. Soc. Change 2021, 173, 121077. [Google Scholar] [CrossRef]

- Curado, C.; Mota, A. A Systematic Literature Review on Sustainability in Family Firms. Sustainability 2021, 13, 3824. [Google Scholar] [CrossRef]

- Chalkasra, L.S.P.S.; Rivera, J.P.R.; Basuil, D.A.T. A Review of Theoretical Perspectives on CSR Among Family Enterprises. Vis. J. Bus. Perspect. 2019, 23, 225–233. [Google Scholar] [CrossRef]

- Ramos-Hidalgo, E.; Orta-Pérez, M.; Agustí, M.A. Ethics and Social Responsibility in Family Firms. Research Domain and Future Research Trends from a Bibliometric Perspective. Sustainability 2021, 13, 14009. [Google Scholar] [CrossRef]

- Chapple, W.; Moon, J. Corporate Social Responsibility (CSR) in Asia. Bus. Soc. 2005, 44, 415–441. [Google Scholar] [CrossRef]

- Witt, M.A.; Stahl, G.K. Foundations of Responsible Leadership: Asian Versus Western Executive Responsibility Orientations Toward Key Stakeholders. J. Bus. Ethics 2016, 136, 623–638. [Google Scholar] [CrossRef]

- Gelfand, M.J.; Nishii, L.H.; Raver, J.L. On the Nature and Importance of Cultural Tightness-Looseness. J. Appl. Psychol. 2006, 91, 1225–1244. [Google Scholar] [CrossRef] [PubMed]

- Garcia-Sanchez, I.-M.; Cuadrado-Ballesteros, B.; Frias-Aceituno, J.-V. Impact of the Institutional Macro Context on the Voluntary Disclosure of CSR Information. Long. Range Plan. 2016, 49, 15–35. [Google Scholar] [CrossRef]

- Welford, R. Corporate Governance and Corporate Social Responsibility: Issues for Asia. Corp. Soc. Responsib. Environ. Manag. 2007, 14, 42–51. [Google Scholar] [CrossRef]

- Peng, M.W. Institutional Transitions and Strategic Choices. Acad. Manag. Rev. 2003, 28, 275. [Google Scholar] [CrossRef]

- Kansal, M.; Joshi, M.; Batra, G.S. Determinants of Corporate Social Responsibility Disclosures: Evidence from India. Adv. Account. 2014, 30, 217–229. [Google Scholar] [CrossRef]

- Dobers, P.; Halme, M. Corporate Social Responsibility and Developing Countries. Corp. Soc. Responsib. Environ. Manag. 2009, 16, 237–249. [Google Scholar] [CrossRef]

- Hawkins, D.T. Bibliometrics of the Online Information Retrieval Literature. Online Rev. 1978, 2, 345–352. [Google Scholar] [CrossRef]

- Mutschke, P.; Mayr, P.; Schaer, P.; Sure, Y. Science Models as Value-Added Services for Scholarly Information Systems. Scientometrics 2011, 89, 349–364. [Google Scholar] [CrossRef]

- Lafortune, G.; Fuller, G.; Bermont-Diaz, L.; Kloke-Lesch, A.; Kandouri, P.; Riccaboni, A. Achieving the SDGs: Europe’s Compass in a Multipolar World. Europe Sustainable Development Report 2022; SDSN Europe: Paris, France, 2022. [Google Scholar]

- El Ghoul, S.; Guedhami, O.; Wang, H.; Kwok, C.C.Y. Family Control and Corporate Social Responsibility. J. Bank. Financ. 2016, 73, 131–146. [Google Scholar] [CrossRef]

- Amann, B.; Jaussaud, J.; Martinez, I. Corporate Social Responsibility in Japan: Family and Non-Family Business Differences and Determinants. Asian Bus. Manag. 2012, 11, 329–345. [Google Scholar] [CrossRef]

- Campopiano, G.; De Massis, A. Corporate Social Responsibility Reporting: A Content Analysis in Family and Non-Family Firms. J. Bus. Ethics 2015, 129, 511–534. [Google Scholar] [CrossRef]

- Dekker, J.; Hasso, T. Environmental Performance Focus in Private Family Firms: The Role of Social Embeddedness. J. Bus. Ethics 2016, 136, 293–309. [Google Scholar] [CrossRef]

- Biswas, P.K.; Roberts, H.; Whiting, R.H. The Impact of Family vs Non-Family Governance Contingencies on CSR Reporting in Bangladesh. Manag. Decis. 2019, 57, 2758–2781. [Google Scholar] [CrossRef]

- Du, X. Is Corporate Philanthropy Used as Environmental Misconduct Dressing? Evidence from Chinese Family-Owned Firms. J. Bus. Ethics 2015, 129, 341–361. [Google Scholar] [CrossRef]

- Muttakin, M.B.; Khan, A. Determinants of Corporate Social Disclosure: Empirical Evidence from Bangladesh. Adv. Account. 2014, 30, 168–175. [Google Scholar] [CrossRef]

- Stanley, T.D. Wheat from Chaff: Meta-Analysis as Quantitative Literature Review. J. Econ. Perspect. 2001, 15, 131–150. [Google Scholar] [CrossRef]

- Christofi, M.; Pereira, V.; Vrontis, D.; Tarba, S.; Thrassou, A. Agility and Flexibility in International Business Research: A Comprehensive Review and Future Research Directions. J. World Bus. 2021, 56, 101194. [Google Scholar] [CrossRef]

- Pham, H.-H.; Dong, T.-K.-T.; Vuong, Q.-H.; Luong, D.-H.; Nguyen, T.-T.; Dinh, V.-H.; Ho, M.-T. A Bibliometric Review of Research on International Student Mobilities in Asia with Scopus Dataset between 1984 and 2019. Scientometrics 2021, 126, 5201–5224. [Google Scholar] [CrossRef]

- Khan, M.A. ESG Disclosure and Firm Performance: A Bibliometric and Meta Analysis. Res. Int. Bus. Financ. 2022, 61, 101668. [Google Scholar] [CrossRef]

- Aria, M.; Cuccurullo, C. Bibliometrix: An R-Tool for Comprehensive Science Mapping Analysis. J. Inf. 2017, 11, 959–975. [Google Scholar] [CrossRef]

- Bretas, V.P.G.; Alon, I. Franchising Research on Emerging Markets: Bibliometric and Content Analyses. J. Bus. Res. 2021, 133, 51–65. [Google Scholar] [CrossRef]

- Falagas, M.E.; Pitsouni, E.I.; Malietzis, G.A.; Pappas, G. Comparison of PubMed, Scopus, Web of Science, and Google Scholar: Strengths and Weaknesses. FASEB J. 2008, 22, 338–342. [Google Scholar] [CrossRef] [PubMed]

- Derviş, H. Bibliometric Analysis Using Bibliometrix an R Package. J. Scientometr. Res. 2020, 8, 156–160. [Google Scholar] [CrossRef]

- Jalal, R.N.-U.-D.; Alon, I.; Paltrinieri, A. A Bibliometric Review of Cryptocurrencies as a Financial Asset. Technol. Anal. Strat. Manag. 2021, 1–16. [Google Scholar] [CrossRef]

- Dyer, W.G.; Whetten, D.A. Family Firms and Social Responsibility: Preliminary Evidence from the S&P 500. Entrep. Theory Pract. 2006, 30, 785–802. [Google Scholar] [CrossRef]

- Cruz, C.; Larraza–Kintana, M.; Garcés–Galdeano, L.; Berrone, P. Are Family Firms Really More Socially Responsible? Entrep. Theory Pract. 2014, 38, 1295–1316. [Google Scholar] [CrossRef]

- Cordeiro, J.J.; Galeazzo, A.; Shaw, T.S.; Veliyath, R.; Nandakumar, M.K. Ownership Influences on Corporate Social Responsibility in the Indian Context. Asia Pac. J. Manag. 2018, 35, 1107–1136. [Google Scholar] [CrossRef]

- Singh, S.; Mittal, S. Analysis of Drivers of CSR Practices’ Implementation among Family Firms in India. Int. J. Organ. Anal. 2019, 27, 947–971. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).