1. Introduction

Investor protection is prominent for the healthy development of the capital market [

1,

2,

3,

4]. However, the protection of minority shareholders is still poor in many emerging economies. In China, the shareholder structure of listed companies in the A-share market presents a highly concentrated feature, while most of the accounts in the market are held by individual investors [

5]. Minority shareholders lack the necessary professional knowledge and rational trading ability, leading to a weak ability to protect legal rights. Hence, they face greater investment losses due to issuers’ fraudulent issuance, internal trading, false statements, and market manipulation [

6]. Therefore, the development of an effective investor protection mechanism is urgent. To improve investor protection, the China Securities Investor Services Center (CSISC) was established by the China Securities Regulatory Commission (CSRC), which aims to exercise various shareholder rights to protect minority shareholders’ benefits.

The existing research exploring the impact of CSISC on the capital market is relatively limited, mainly focusing on the economic consequences of its establishment. CSISC shareholding encourages minority shareholders’ activism and plays a role in protecting the rights and interests of minority shareholders; therefore, the pilot reform of CSISC shareholding can significantly reduce the stock price crash risks, promote the smooth operation of the financial market [

7], reduce earnings management, and improve earnings quality [

5]. Based on the existing literature, this paper further focused on how CSISC can improve the long-term sustainability performance of companies, which means the impact on ESG performance. We found that the pilot reform of CSISC shareholding has a positive influence on the ESG performance of listed companies. The CSISC, as a minority shareholder, has a positive influence on the ESG through increased supervision capability and information transparency.

We focused on the impact of ESG performance mainly because minority shareholders have insufficient ability to exercise individual interests [

6]. In emerging economies with concentrated ownership structures, large shareholders, especially controlling shareholders, are likely to pose a negative influence in monitoring a firm’s opportunistic behaviors and, in turn, increase private short-term interest. Compared with large shareholders, benefiting from the short-term zero-sum game is hard for minority shareholders [

8], and they pay more attention to the long-term and sustainability development of companies [

9,

10]. Under CSISC shareholding, some of the short-term benefits obtained by large shareholders are redirected to projects that benefit all shareholders in the long run, such as ESG. Furthermore, we believe it is necessary to investigate how CSISC ensures long-term sustainable development, which is the ESG performance of listed companies, by exercising minority shareholder rights.

To analyze the relationship between CSISC shareholding and ESG performance, we constructed a difference-in-differences model. Due to the CSISC only buying and holding 100 shares of each listed company in Shanghai, Guangdong (excluding Shenzhen), and Hunan provinces during the pilot period in 2016, we use listed firms in the pilot regions as treatment firms and listed firms in other provinces as control firms. We performed a difference-in-differences (DID) approach and found that after the CSISC shareholding pilot reform, the ESG score in pilot regions increased, which confirmed our Hypothesis 1 that the pilot reform of CSISC shareholding has a positive influence on the ESG performance of listed companies. To validate our DID research design, we performed a parallel trend analysis, finding that the differences in ESG performance in the pilot period are not attributable to the trending differences between the treatment and control groups. Our DID research design is valid. We also conducted a placebo test, propensity score matching, controlling time and regional effects, and changing the control group to confirm the robustness of our results.

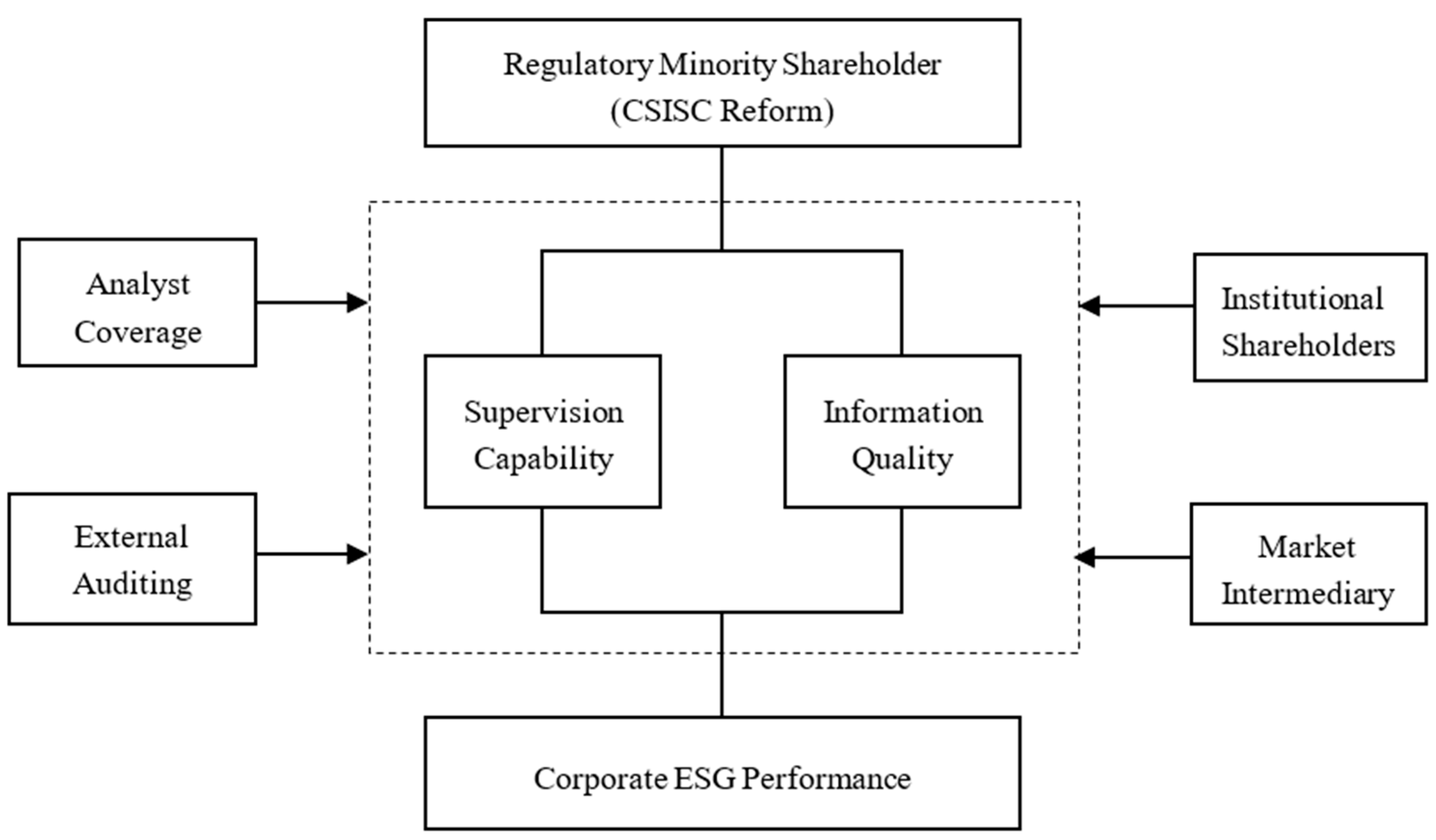

Furthermore, from heterogeneity analysis, CSISC shareholding has a positive influence on large companies and companies in non-high-polluting industries. From cross-sectional analysis, analysts’ attention, external auditing quality, institutional shareholding, and highly-developed market intermediary and legal system can strengthen the effect of CSISC shareholding on corporate ESG performance. The mechanism analysis shows that CSISC shareholding leads to a positive influence on ESG through increased supervision capability and information transparency.

Figure 1 shows the research framework of this paper.

Our study makes several contributions. Firstly, it contributes to the literature on minority shareholder protection and investigates the economic consequences of CSISC shareholding. Current research mainly focuses on the impact of CSISC shareholding on the short-term economic behavior of companies, including stock price crash risks [

7] and earnings management [

5]. However, only by improving the long-term value and focusing on the long-term sustainable development of listed companies can the investment value of minority shareholders be truly enhanced and their interests protected. Our findings can inspire regulators in emerging markets to establish suitable mechanisms to protect minority shareholder rights in the long run.

Secondly, now that the ESG score is a popular indicator for investors to select stocks, companies need to improve their ESG performance. Existing studies mainly focused on the economic consequences of the ESG [

11,

12,

13,

14] and rarely investigated how to improve ESG performance, especially from the perspective of a minority shareholder. This paper then adds to the research literature on minority shareholder protection.

Thirdly, previous studies on the relationship between minority shareholders’ activism and the long-term development of listed companies were primarily conducted in the context of developed markets. Our analysis also enhances the understanding of investor protection and ESG activities in China because lowering the high ownership concentration and protecting minority investors from improving market efficiency should be the key to solving agency problems in the Chinese capital market and for all emerging economies.

The remainder of this paper proceeds as follows:

Section 2 introduces the institutional background of the CSISC and the literature review.

Section 3 develops our hypothesis.

Section 4 describes the sample and research design.

Section 5 presents our main empirical results.

Section 6 concludes the paper.

3. Hypothesis Development

Minority shareholders have insufficient ability to exercise individual interests, often face information asymmetry, and are always victims of fraudulent issuance, internal transactions, false statements, and market manipulation by issuers [

6]. It is hard for minority shareholders to benefit from the short-term zero-sum game [

8], which means minority shareholders can only obtain benefits through long-term value investment. Hence, it is vitally important for minority shareholders to protect their legal rights and gain benefits by focusing on ESG performance as a long-term sustainable development of companies [

9,

10].

The CSISC, as a minority shareholder, has a positive influence on ESG from two aspects. On one hand, CSISC shareholders could increase the supervision capability. The CSISC is an established organization affiliated with the CSRC [

5], representing the attitude of the regulator as an innovative government regulation. Not only is the CSISC equipped with more competent professionals, but it is also able to cooperate deeply with regulators and the judicial system. Through judicial proceedings, the CSISC creates a deterrent effect on listed companies that attempt to violate the interests of minority shareholders through internal transactions and information fraud. Therefore, with strong external supervision, the CSISC can improve corporate governance and regulate the internal operating mechanisms of listed companies. Besides, the presence of the CSISC also arouses the awareness of minority shareholders to actively participate in the exercise of their rights and increases their chances of attending shareholders’ meetings. As outsider investors, minority shareholders cannot accurately realize the financial information of listed companies. Instead, they focus on the long-term sustainable development ability of a company through the information disclosed on social responsibility, environmental protection, innovation investment, and other aspects. Thus, the negative news of social responsibility and environmental protection is more likely to attract the attention of minority shareholders. This strong supervision creates reputational pressure on companies, which encourages insiders to engage in valuable long-term strategic plans and focus on sustainable development, especially by reducing corporate socially irresponsible activities and avoiding penalties for environmental violations [

31]. As ESG performance can reflect corporate long-term development and social and environmental responsibility by stimulating listed companies to pursue a more socially responsible approach and avoid misappropriation and opportunistic behavior to increase long-term value, we believe that the CSISC can prompt corporate ESG performance through its supervisory effect.

On the other hand, the CSISC would force firms to respond or disclose more information to avoid further investigation and penalties. The CSISC has filed some litigation cases involving information disclosure irregularities of listed companies, which shows that the quality of information disclosure of listed companies is a special concern of the CSISC at present. In the event of false statements, material omissions, and other illegal violations of listed companies, the CSISC can, through continuous tracking of the listed company’s information disclosure, expose the problems of the listed company, timely release signals to the market, and increase the cost of information disclosure violations. Information disclosure is not only a way to alleviate information asymmetry and agency problems to increase corporate governance but also an important channel to actively display the development direction and social responsibility behavior of enterprises. When listed companies have a high level of information transparency and voluntary disclosure of non-financial information, they are more willing to actively disclose information related to the company’s long-term development, including sustainability, corporate governance, and social and environmental responsibility, leading to a positive effect on ESG performance [

24,

41]. We believe that the CSISC can prompt corporate ESG performance by increasing information quality.

Based on the above discussion, we have developed the following hypothesis:

Hypothesis 1 (H1): The pilot reform of CSISC shareholding has a positive influence on the ESG performance of listed companies.

4. Research Design

4.1. Sample and Data

To construct the DID model to test and estimate the effect of the CSISC shareholding pilot reform in 2016, we selected a sample of listed firms registered in Shanghai, Zhejiang, Guangdong, Hunan, and Hubei provinces from 2013 to 2017, following the existing studies from Ge et al. [

5] and Chen et al. [

17]. According to these studies [

42,

43,

44], ESG performance is measured by Huazheng ESG evaluation. Based on the core connotation and development experience of ESG, combined with the actual situation of the domestic market, the Huazheng ESG evaluation system constructs a three-level index system from top to bottom. Specifically, there are 3 first-level indicators, 14 second-level indicators, 26 third-level indicators, and more than 130 underlying data indicators. Through the combination of quarterly regular evaluation and dynamic tracking, the ESG score level of all A-share listed companies in the past 10 years was systematically measured (with a total score of 100 points), and nine ratings of “AAA-C” were given accordingly. Other data came from the CSMAR (China Stock Market and Accounting Research Database).

To ensure the comparability and similarity between samples, we further screened the samples as follows. First, because of the differences between financial companies and manufacturing companies in the statement structure, accounting treatment, audit requirements, and regulatory provisions, we omitted the financial companies. Second, pure B shares are subscribed and traded in foreign currencies, so we only used data from companies listed in the A-share market. Third, as the securities of ST (special treatment) companies cannot be circulated and traded normally in the market, nor can they be held by CSISC, so we omitted data on ST companies. Forth, we omitted samples with missing data. After selection and screening, we obtained 5264 firm-year observations.

4.2. Research Methodology

The research model is designed as follows:

The dependent variable indicates the corporate ESG score in year t + 1, which is the comprehensive and quantitative measure of corporate ESG performance. Considering Huazheng ESG rating is divided into nine levels from AAA to C to reflect the corporate ESG performance, we assigned this variable from C to AAA as 1–9 according to the rating. As the policy may not have an immediate effect in that year, we used the ESG score of the next year to study the effects on corporate social responsibility performance. The independent variable × reflects the effect of the pilot reform of CSISC shareholding. is a dummy variable indicating whether the firm is in the pilot region (Shanghai, Guangdong excluding Shenzhen and Hunan). Considering the economic and geographic factors to make the other conditions of the control group and the treated group close to the natural experiment, we chose listed companies in Zhejiang, Shenzhen, and Hubei as the control group. So, equals one for companies located in Shanghai, Guangdong, excluding Shenzhen and Hunan, and equals zero for companies located in Zhejiang, Shenzhen, and Hubei. The coefficient is our main interest. If a significant positive coefficient is observed, our hypothesis is confirmed, which indicates that CSISC shareholding promotes corporate ESG performance.

Following existing literature in the corporate finance [

21,

32,

33,

44,

45], we controlled other variables influencing corporate social responsible behavior and ESG performance, including firm size (

Size), asset-liability ratio (

Lev), return on asset (

ROA), price/book value ratio (

PB), market performance (

TobinQ), board size (

Boardsize), board independence (

Indep), CEO duality (

Duality), ownership concentration (

Top10), profitability (

Loss), and firm age (

Age). We also controlled firm-fixed effects and year-fixed effects in our model to reduce estimation bias.

Appendix A provides a detailed definition of all the variables.

4.3. Descriptive Statistics

Table 1 shows the summary statistics of the main variables in the regression test. The mean of

Treat × Post is 0.214, which means that 21.4% of observations were affected by the CSISC shareholding. On average, 39.6% of sample companies’ assets are financed by liabilities; the market value is 2.066 times the book value. Approximately, each firm has a total number of seats on the Board of Directors on average, and 32.4% of the observations exist in the situation where the two positions of chairman and general manager are held by one person.

Table 2 reports the Pearson correlation matrix for the variables used in the regression test. The independent variable

Treat × Post is significantly and positively correlated with the ESG score, and the result is the preliminary validation of the hypothesis, but more accurate estimation and inference still need further empirical tests.

6. Conclusions

To improve investor protection, the China Securities Regulatory Commission (CSRC) aims to exercise various shareholder rights to protect minority shareholders’ benefits. Based on DID analysis, we found that after the CSISC shareholding pilot reform, the ESG score in pilot regions increased by 0.091 on average, which confirmed our hypothesis that the pilot reform of CSISC shareholding has a positive influence on corporate ESG score. Furthermore, we analyzed heterogeneity and cross-sectional perspectives and found that CSISC shareholding has a positive influence on large companies and companies in non-high-polluting industries. Analysts’ attention, external auditing quality, institutional shareholding, and highly-developed market intermediary and legal system can strengthen the effect of CSISC shareholding on corporate ESG performance. On the basis of previous research [

5,

7,

17], although CSISC is a minority shareholder for companies, its policy and regulatory characteristics make its role different from that of ordinary minority shareholders, which is of special significance for corporate governance and investor protection. Hence, our paper determined a positive relationship between the CSISC and the corporate ESG rating.

The paper affirms the deterrent and supervisory governance effects of CSISC, as well as the leading demonstration effect on minority shareholders. Our findings can inspire regulators in emerging markets to establish suitable mechanisms to protect minority shareholder rights in the long run. From a policy perspective, this paper suggests that CSISC can join other forces with external governance functions, such as auditors, financial analysts, and institutional investors, activating the awareness of minority shareholders themselves to defend their rights and actively guiding and providing more convenience for minority shareholders to exercise their rights. Then, the CSISC can improve the governance and information disclosure environment of listed companies and promote the healthy development of the capital market.

There are several limitations to this study. First, because capital market policy changes frequently in China, we used DID to test our research question and conducted a series of robustness tests; however, we cannot rule out potential endogeneity concerns. Second, we mainly focused on the influence of the CSISC in pilot areas, lacking data on specific actions taken by the CSISC. We hope future studies dig deep into this issue with more data and can also focus on the combined effect of the CSISC and other forces, such as auditors, financial analysts, and institutional investors. Moreover, because not all listed companies in China can provide accurate and detailed ESG information, we hope that with the establishment and improvement of the ESG index system, more samples can be obtained to enrich the research results, and we hope more interesting results can be found in ESG performance.

{kind=link}