Abstract

Climate change policies are affecting the economic and structural viability of European Union (EU) industries, particularly in the energy-intensive sector, with very challenging goals of EU Agenda 2030 in terms of CO2 reductions and energy efficiency. This ecological transition can be supported by the employment of innovative technologies, enabling production process efficiency, resource optimization and supply-chain integration. Nevertheless, it is still empirically unclear how energy-intensive industries will complete their ecological transition successfully, especially in terms of achieving environmental sustainability practices within the organization and in the supply-chain without endangering their economic availability. Moreover, the assessment of environmental sustainability performance is still not a unique standard framework, causing loss of transparency and traceability towards internal and external stakeholders, such as managers, investors and business partners. With 20 qualitative interviews of customers and experts of a company leader in the steel construction sector in Italy and Germany, the Feralpi Group, this paper explores the implications of strategic environmental sustainability indicators, which can transparently assess company performance. Preliminary results underline how shared standardized indicators are fundamental for a tighter supply-chain integration, giving impulse and significance to the steel producers’ efforts for environmental sustainability excellence. Future research should further investigate the connection between environmental sustainability strategies and performance indicators for a more integrated sustainability framework.

1. Introduction

Climate change has become a global challenge. The European Environment Agency has identified different economic and environmental vulnerabilities related to global warming: increased damages caused by unexpected storms and flooding, increased risk of biodiversity loss and of species extinction, and risk to the livelihoods of indigenous people [1]. A strategic containment of climate change is carbon neutrality, creating a balance between emitted and absorbed carbon in the atmosphere through the help of carbon sinks, such as forests and oceans [2]. The number of countries committing to carbon neutrality by 2050 and 2060 has increased, including India and China, [3]. The 26th United Nations (UN) Conference on Climate Change (Conference Of the Parties 26—COP26) was concluded on 12 November 2021 in Glasgow, focusing on four essential goals:

- (a)

- Mitigation: eliminating CO2 net emissions by 2050 and limiting the increase in planet temperature to no more than 1.5 degrees;

- (b)

- Adaptation: supporting the most vulnerable countries to reduce the impacts on climate change;

- (c)

- Finance for the climate: supporting financing to developing countries, reaching the goal of USD 100 billion per year;

- (d)

- Operational finalization of the United Nations (UN) Paris Agreement (December 2015 on climate change): focusing on the methods for reporting on greenhouse gas emissions and monitoring the commitments of the different countries [4].

The European Union (EU) started its commitment for climate change in 2008, aiming at reducing gas emissions by 20% (compared to 1990) and at increasing renewable energy and energy efficiency by 20% [5]. In 2014, the commitment went a step further: with the 2030 climate and energy framework, the EU set the more ambitious target to reduce gas emissions by 40% by 2030 [6]. In December 2019, the European Commission presented the European Green Deal, committing to achieving a carbon-neutral economy and society by 2050, with even more ambitious goals: a 55% reduction in greenhouse gas emissions, a 32% increase in renewable energy and a 32.5% increase in energy efficiency [7]. The EU Green Deal is a growth strategy which aims to “protect, conserve and enhance the EU’s natural capital, and protect the health and well-being of citizens from environment-related risks and impacts.” [8] (p.2). This strong ecological transition should foster the competitive advantage of European manufacturers, also supported by the EUR 1.8 trillion of the NextGenerationEU Recovery Plan to help them recover from the COVID-19 pandemic [9]. A pillar of this environmental sustainability should be digital technologies, which should boost innovative sustainable business models [10]. Each member state has to dedicate at least 37% of its national expenditure to the reduction of climate impact [11]. Italy has presented a total investment plan of EUR 248 billion, with 40% dedicated to the ecological transition. Core drivers of the ecological transition should be energy efficiency, renewable energy and the reuse of regenerated and recycled materials [12]. In addition, Germany has pledged to invest 90% of resources on green technologies, although with a smaller amount compared to Italy (EUR 11.5 billion and EUR 14 billion, respectively) [13].

Nevertheless, from a theoretical and empirical point of view, it is still unclear how EU manufacturers will manage their economic viability while achieving this ecological transition [14]. Green transition implies a complete transformation of the global economy, accounting for USD 3.5 trillion a year of additional investments to support this change [15]. Moreover, industries need standardized metrics and indicators in the supply-chain to measure the durable benefits of environmental sustainability strategies [16]. In this research, we decide to focus on energy-intensive industries, which are highly impacted in their business models by the ecological transition. There are three main, and sometimes radical, changes required in the production cycles of energy-intensive industries to reach a successful ecological transition: electrification of production processes to reduce the consumption of fossil fuels, use of biomasses to optimize product carbon footprint and energy efficiency practices through the use of the Best Available Techniques (BATs) [17]. Energy-intensive industries are steel, cement and petrochemical producers and are responsible for more than 20% of global CO2 emissions [18]. Energy-intensive companies are pushed to invest significant resources in order to achieve a zero-emission production [19]. Our research is focused on the steel sector, the backbone of the EU economy, which is required to apply profound sustainable environmental strategies for the ecologic transition to succeed. Steel could become from 20 to 40 percent more expensive if produced with other energy resources (such as hydrogen) [20], and the steel supply-chain itself is put under pressure to increase resource efficiency and Circular Economy (CE) practices [21]. The ecological transition pushed by the EU focusing on the three pillars of decarbonization—CO2 reduction measures, energy efficiency and Circular Economy (CE)—will enforce significant interconnected changes into the steel sector, both in the environmental strategies of steel producers and of their business partners [22]. With an exploratory approach, simultaneously, we analyze which environmental sustainability practices and key performance indicators are used to fulfill carbon neutrality strategies, not only considering a single firm but also looking at the integration in the steel supply-chain [23], since collaboration between suppliers and customers fosters reciprocal environmental strategies [24]. We will address these issues focusing on the innovative perspective of steel customers, which is still largely unexplored in the research, with the steel market being more a business-to-business sector.

To summarize, the main explorative research questions are the following:

- (1)

- What is the current environmental strategy in the supply-chain of steel industries, in particular looking at the customers’ perspective?

- (2)

- What are the environmental key performance indicators (KPIs) mainly used in order to measure environmental sustainability in the steel sector and with which goal?

These two research questions will be addressed directly with a specific semi-structured questionnaire, which will be further explained in Section 3. Focusing on the perspective of customers can complete the perspective of research on two relevant points, which are the practicability of environmental sustainability strategies and the measurability of environmental sustainability performance. The article consists of four main sections: in Section 2, the literature review, we will explore the paradigms of different environmental sustainability strategies in the steel sector and the most meaningful metrics to exchange information on environmental performance in the supply-chain; in Section 3, the methodology, we will present both the company case and the interview panel for the exploration of the single case study; in Section 4, we will present and discuss results; lastly, in Section 5, we will give insight into further research and conclusions.

2. Literature Review

2.1. Environmental Sustainability Strategies in the Steel Sector

The research on decarbonization strategies and metrics in the steel sector has to be first understood in the current research of environmental practices and performance indicators in sustainable business models of manufacturing industries.

The steel industry’s sustainable environmental practices have to be first contextualized in the main research framework of sustainable business models. Sustainable business models fulfill company performance by considering interests of various stakeholders on three intertwined dimensions: economic, social and environmental [25,26]. Sustainable economic activities encourage an optimized use of resources, such as raw materials and energy, and integrate social and environmental scopes, rather than only prioritizing consumeristic growth [27]. Sustainability reshapes the financial and organizational architecture of firms and can characterize the firm in new business archetypes [28].

- (a)

- Technological dimension: energy efficiency best practices (e.g., low carbon production);

- (b)

- Social dimension: servitization (service-oriented contracts rather than ownership);

- (c)

- Organizational dimension: repurpose for society and environment (hybrid businesses, such as social enterprises).

Circular Economy (CE) has been considered as part of the sustainability strategy. In contrast to the traditional linear economy, CE is based on three fundamental concepts: designing out waste (materials are designed to be used again with lowest energy consumption and highest quality retention); diverse systems based on renewable resources (resilient systems adapting and evolving in uncertain conditions); and eco-effectiveness (material flow is cradle-to-cradle, where resources are reusable and accumulate intelligence over time) [29,30].

Furthermore, research on sustainable business models has underlined how digital technologies are a powerful enabler of sustainable business strategies [31,32,33,34], in particular of sustainable company performance on an environmental, economic and social level [35,36,37]. Digitization enables CE practices, enhancing collaboration in the supply-chain for the reuse of resources, reduction of waste and material renewability [38,39], empowering information exchange and tracking [40,41,42].

Among manufacturing industries, the energy-intensive sector is the most impacted domain by the ecological transition, in terms of CO2 emissions reduction, energy efficiency [43] and CE economy practices [44]. Particularly, the EU steel industry will be affected by the decarbonization strategy in terms of rising CO2 emissions costs and needed technological and organization investments to reach carbon neutrality, such as the use of innovative energy sources such as hydrogen or renewable ones, such as solar or wind power, or increasing the rate of recyclable scrap as raw material [45,46]. The steel sector is responsible for 5% of CO2 emissions in the EU and 7% globally. CO2 emissions and energy use in European steel production have decreased by 50% since 1960, and the sector aims to achieve further reductions up to 95% by 2050 [47]. Due to their supply-chain structure and product life cycle, steel industries have been engaged in different projects with the objective of zero waste impact, reusing apparently finished processed materials [48]. Steel industries are often developing practices of Industrial Symbiosis (IS), exchanging materials and/or information to achieve reciprocal advantages with companies of different sectors [49]. The IS of steel industries focuses on CE practices with businesses’ viability [50] at different levels. From the steel production, materials (such as slags) can become valuable sources for other industries, including the chemical and cement sector, or exceeding steam can deliver energy for district heating in cities [51]. CE and IS are not only sources of important benefits, such as new revenues, increased life cycle of landfills and compliance to legislation, but also bring with themselves some challenges, such as high costs and mismatch between offer and demand [52]. Steel industries are still an open empirical research field to investigate environmental sustainability practices linked to economic and organizational feasibility [53,54]. If the first focus of our research is to explore the environmental strategies in the steel sector, we will use an innovative perspective, that of external stakeholders, such as customers, who have direct knowledge of market trends and changes [55,56].

2.2. Metrics for Environmental Sustainability

Another important aspect regarding research on decarbonization strategy is the definition of targets and indicators measuring the success of the sustainability performance and leading to achievable and feasible targets [57]. Particularly, standardized metrics estimating sustainability benefits are still an open issue [58], since different frameworks exist simultaneously without integration [59]. Different metrics affect the assessment of environmental sustainability benefits and company performance both for internal managers and external investors [60,61,62,63]. We found a gap in the current research on environmental sustainability, which urges to deepen the exploration of the standardization and harmonization of common metrics in the supply-chain [64], a fundamental factor to enhance efficient supply-chain integration [65]. We reviewed the different frameworks representing environmental indicators, focusing our attention on the three domains that we explored in the environmental strategies of steel industries: CO2 emissions, energy efficiency and CE practices. We concentrated on a main set of key performance indicators (KPIs) after a benchmarking with competitors in the sector and different internal evaluation sessions with managers and experts of the sustainability committee of the analyzed single firm. From this practical benchmarking, it has also clearly emerged how a standardized set of comparable indicators is still a challenge for the market.

The main structure for sustainability indicators lies in Agenda 2030, a framework launched in 2017 by the United Nations, which contains 17 strategic sustainable goals and 169 targets: (1) no poverty; (2) zero hunger; (3) good health and well-being; (4) quality education; (5) gender equality; (6) clean water and sanitation; (7) affordable and clean energy; (8) decent work and economic growth; (9) industry, innovation and infrastructure; (10) reduced inequalities; (11) sustainable cities and communities; (12) responsible consumption and production; (13) climate action; (14) life below water; (15) life on land; (16) peace, justice and strong institutions; (17) partnership for the goals [66]. Indicators of assessment of company sustainable performance did not come originally from a settled accounting association, such as the International Financial Reporting Standard (IFRS) Foundation, which recognizes standards of financial statements for companies listed on the stock exchange internationally (https://www.ifrs.org/ (accessed on 10 January 2022)). Sustainability indicators have been defined by four main voluntary frames, determining different guidelines:

- (1)

- The Global Reporting Initiative (GRI—https://www.globalreporting.org/ (accessed on 20 January 2022)): The GRI was founded in Boston in 1997, after the environmental scandal of the Exxon Valdez oil spill, with the goal to create a transparent framework to assess environmental, social and governance sustainability; in 2016, GRI guidelines became global standards for sustainability reporting, also starting to provide specified sector standards.

- (2)

- The Climate Disclosure Standards Board (CDSB—https://www.cdsb.net/ (accessed on 2 February 2022)): The CDSB was set up at the World Economic Forum in 2007 as a specific climate-related standard. Its main goal is to explain to investors the risks and opportunities that climate change has on organization strategy and financial performance.

- (3)

- The International Integrated Reporting Council (IIRC—https://integratedreporting.org/ (accessed on 23 January 2022)): In 2009, an International Integrated Reporting Committee was set up, including the GRI and the International Federation of Accountants (IFAC), in order to create a globally accepted integrated framework. The goal is to make companies disclose strategy, governance and performance in a clear and transparent format.

- (4)

- The Sustainability Accounting Standards Board (SASB—https://www.sasb.org/ (accessed on 15 January 2022)): The SASB was founded in 2011 to help disclose company financial material sustainability information to the market, identifying a subset of environmental, social and governance issues relevant for investors. It develops specific guidelines for 77 industries. In 2021, the SASB and the IIRC merged into the Value Reporting Foundation (VFR), as a step towards framework simplification. In 2022, with the goal to create a unified base of high-quality standard framework, the IFRS merged with the VFR and the CDSB to create the International Sustainability Standard Board (ISSB).

Moreover, four additional specific frameworks on climate change have been developed in recent years:

- (1)

- The framework of the Task-Force on Climate Related Financial Disclosures (TFCD—https://www.fsb-tcfd.org/ (accessed on 20 January 2022)): In 2017, the Financial Stability Board created the TFCD recommendations structured in four areas (metrics and targets, risk management, and strategy and governance) to support investors in the assessment on risks related to climate change.

- (2)

- The Carbon Disclosure Project framework (CDP—https://www.cdp.net/en (accessed on 2 February 2022)): Created in 2000, the CDP has focused climate disclosure on three main environmental sustainability topics—climate, forest and water—for companies, cities, regions, governments and investors. Focusing on targets and plans to mitigate climate change, the CDP aligned to the recommendation of the TFCD to guide businesses to a transition to a carbon-neutral global economy.

- (3)

- The Science Based Targets Initiative (https://sciencebasedtargets.org/ (accessed on 15 January 2022)): The Science Based Targets Initiative is a collaboration since 2015 between the CDP, the United Nations Global Compact, the World Resources Institute (WRI) and the World Wide Fund for Nature (WWF), aiming to support companies of various sectors to achieve the net zero emission goal by 2050. This is a precise pathway to reduce greenhouse gas emissions, in line with the latest climate science pursuing efforts to limit warming to 1.5 °C [67].

- (4)

- GHG (Greenhouse Gases) Protocol Corporate Accounting and Reporting Standard: This standard is a multi-stakeholder partnership, including the World Business Council for Sustainable Development (WBCSD), aiming to provide a procedure to quantify and report GHG emissions worldwide [68,69].

In Table 1, we provide a summary of main sustainability frameworks and scope.

Table 1.

Summary of main sustainability frameworks and scope.

The various set of indicators to fulfill sustainability goals is thought to apply to different sectors. However, companies not only have to select which indicators are more relevant for their organization, but, more importantly, those indicators are not able to fully measure the sustainable performance of organizations, also in environmental performance terms. In many cases, ratings of those voluntary frameworks are diverging in measurement [58]. Since the interest of capital investors has increasingly grown about companies with low environmental impact, at the beginning of 2022, the EU better defined a taxonomy framework classifying environmentally friendly economic activities more clearly, which can be applied for all industrial sectors. EU taxonomy is intended to award companies’ practices and investments above all in climate change mitigation, transition to circularity, pollution prevention and sustainable use of water resources; among the main criteria to contribute to climate change mitigation, there are use, generation, transmission of renewable energy, increase in climate-neutral mobility and switch to the use of renewable resources [70]. Specifically, an EU taxonomy was also directed to CE practices to cope with the lack of a common foundation to define circularity activities; nevertheless, taxonomic criteria should be more quantitatively and qualitatively determined, especially for sectors such as steel production, with a focus on the environmental performance of the entire value chain [71].

Concerning CE, different frameworks developed in order to come to a more standardized setting, but without success. In particular, two frameworks have been created in an optic of supply-chain integration: Circulytics and Circular Transition Indicators (CTIs). Circulytics was launched in 2020 by the Ellen MacArthur Foundation; it categorizes enabling factors such as strategy, innovation, skills and external engagement, focusing on the specificity of products and materials. CTIs have also been active since 2020 and belong to the World Business Council for Sustainable Development (WBCD); it is a quantitative analysis, giving insights and links between resource optimization and business performance [72]. A further step in the sustainability framework has lastly been the Benefit Corporation metrics system, which covers the same area of the triple-bottom-line approach, as in GRI and SASB, but where the rules of the game of capitalistic business are changed in a vision of just economy and ethical growth, meeting high standards of social and environmental performance through transparent accountability [73]. We acknowledge a literature gap in finding a transparently comparable framework of environmental sustainability indicators, in terms of decarbonization strategy, in an integrated supply-chain perspective [74].

3. Methodology: Exploring the Steel Sector with a Single Case Study

3.1. Presentation of the Case Study

Through qualitative analysis, we focus on a representative single company case; we found the use of a case study particularly helpful to have an extensive analysis in a real-life context for a research topic which needs more practical insights [75].

Based on the production process, steel industries can be divided into two main groups: electric arc furnace (EAF) and blast furnace (BF) steel producers. The significant difference consists in the main raw material used by these two production processes: EAF producers start from recyclable materials, scrap. The use of scrap causes a decrease of 40% in energy requirements and 60% less CO2 emissions, compared to the BF system, exploiting mostly iron ore. This is the reason why big steel producers, such as in China, are considering reshaping their production process towards the EAF system [76].

We focus our explorative research in the context of EAF producers. We put our attention on the Feralpi Group, which is an internationalized leader in steel production both in Italy and in Germany, with an historical commitment in environmental sustainability and technological innovation: its first sustainability report is dated 2004 [77]. Starting from a practical case analysis can help to enrich the theoretical framework of the existing literature, by observing reality patterns and trying to connect them inductively to a more abstract framework [78].

The history of the Feralpi Group is rooted in the initiative of one family, the Pasini family, and a group of related shareholders. In 1949, Carlo Pasini, the founder, took over the family forge in Odolo, a small city in the province of Brescia. From that moment the business continued to grow until Carlo Pasini himself in 1968 decided to build, together with other partners, the first new steel complex in Lonato del Garda. After the investment at the Lonato hub, the Feralpi Group expanded, with the establishment of Acciaierie di Calvisano in 1972. From the beginning, this reality has been characterized by an Industrial Symbiosis: harnessing the residual heat from the steel plant to raise fish with a high commercial profile (hence, even today, the caviar of the Agroittica brand is exported all over the world). The founder’s untimely death in 1983 saw the takeover of the management of Feralpi by his wife Camilla, together with their sons Giuseppe, Giovanni and Cesare, supported by other partners. The internationalization of the Feralpi Group took place in 1992, with the acquisition of a massive steel mill in the former Democratic Republic of Germany, leading the company to expand its national borders and increase its competitive advantage. Feralpi’s technological developments continued over time, including investing in the verticalization of production, through the manufacture of derivative products and the production diversification, with the acquisition of Nuova Defim and Orsogrill in the area of gratings and then with Caleotto in the area of special steels. The process of evolution of business of the Feralpi Group is completed with the acquisition of Presider, active in the field of large contracts for construction companies. The Feralpi Group focused its development into three streams: verticalization (integration of all possible products cycle, starting from billets, semi-products of EAF, to the very final products, meshes, being next to the final consumers in the business-to-business market), internationalization (with the acquisition of strategic production sites in one of the most important EU steel markets, Germany) and diversification (with the production of special steel, with the opportunity to go into more customized markets with possibly higher margins) [77].

In May 2020, the Feralpi Group published its first voluntary consolidated non-financial reporting, together with its consolidated financial statements [79]. The Feralpi Group is committed to six UN Sustainable Development Goals, which are integrated in its industrial plan: affordable and clean energy (Goal 7); decent work and economic growth (Goal 8); industry, innovation and infrastructure (Goal 9); sustainable city and communities (Goal 11); responsible consumption and production (Goal 12); and climate action (Goal 13) [80]. In 2021, the Feralpi Group defined a five-year group climate strategy, which aims at reducing CO2 emissions beyond 90,000 tons/year, fulfilling investments for EUR 100 million and covering 20% of its own energy consumption in Italy with renewable resources, in particular through the newly founded Feralpi Power On energy company [81]. Concerning CE practices, Feralpi initiatives cover different waste typologies in a concept of closing-the-loop strategy: recovery of black slag for the use in the construction industry, warm recovery to generate electric energy, recovery of rolling-mill scale to reuse in the construction sector and recovery of non-ferrous materials from the scrap selection [81].

From an industrial, innovation and sustainability point of view, the Feralpi Group represents an insightful case study to deepen the topic of environmental sustainability strategies and metrics.

3.2. Development of Qualitative Interviews

The first phase of this qualitative study was in 2021. We conducted the first interviews (19 in total) in May 2021, with managers from the Italian parent company and the German subsidiary, to have a first exploratory insight into the sustainability strategy on the three bottom-line dimensions (social, environmental and economic). Managers’ answers were counterbalanced by interviews of four business partners of the Feralpi Group to complete the perspective on the topic in a more unbiased way [82]. Focusing on market perspective, especially on the point of view of customers, who are pushed under pressure to fulfill environmental goals, we started a second qualitative analysis phase by pursuing a total of 20 semi-structured interviews [83] in the period of June–August 2022. Feralpi’s single case study offers a broad picture on the environmental sustainability practices and indicators in the sector, since the company operates both in the commodity market (construction) and in the special steel production. We selected strategic customers of Feralpi both from construction and special steel. The steel construction market is often characterized by cyclical resource shortages and tough deadlines, affecting the sustainability of the construction phase [84]. In the special steel market, which also serves the automotive sector, customers are more demanding concerning the use of environmentally friendly technologies and materials by their suppliers [85]. In order to obtain data triangulation and more objectivity in results, we selected representatives of various phases of Feralpi’s supply-chain in the commodity and special steel sector. We identified four areas of qualitative interviews in order to get a more amplified and complete view on the topic from the different perspectives of the market:

- (a)

- Construction sector, intermediates: These are significant customers of Feralpi who are in the intermediate phase of product commercialization; either they are reshaping final products of Feralpi and selling them to the final stage of product delivery, the construction site, or they are commercial partners selling steel products to service centers for product transformation. This point of view in the supply-chain is important, since it is an intermediate one before the final step in the value chain, so being influenced both by steel producers and final customers constraints. We conducted a total of 5 interviews.

- (b)

- Construction sector, final customers: These are engineering and construction companies, leading projects by public or private hands in the civil construction sector. Their point of view is determinant to understand the trends and pressure of the market, which is pushed by ESG (environmental social governance) ratings of financial funds and investors. We conducted a total of 5 interviews.

- (c)

- Special steel: Producers or traders who deal directly with the automotive sector or sector of special steel products; in this sector, environmental sustainability is pushed by high sensibilization of final customers, who want more tailor-made products with specific and transparent environmental information. We conducted a total of 5 interviews.

- (d)

- Experts: Technical experts in the field of green sustainable steel, who can give a more detached and objective view on the trend of decarbonization strategies and metrics, and they can contextualize Feralpi customers’ responses in a more neutral and comprehensive way. We conducted a total of 5 interviews.

We used all the aggregate results from those different perspectives to complete the vision on the current environmental sustainability strategies and metrics in the steel sector.

Moreover, we managed to create focus groups with different participants (technical experts both of interviewed customers and of the Feralpi Group) in order to obtain more heterogeneous perspectives on the topic. We additionally organized a feedback session with managers of the Feralpi Group on the aggregated results to complete data saturation [86]. We also used diversified documentation sources (financial balance sheets, sustainability reporting, website information and press release articles) in order to counterbalance interviewees answers. Lastly, in the interview panel, we selected neutral experts on the topic in order to check and integrate the contribution given by customers [75].

In Table 2, we present more detailed information on interviewees:

Table 2.

List of all interviewees, with unit, company size and reference market.

Interviews were made with the help of a seven-point semi-structured questionnaire, adapted for customers and experts. The questionnaire was validated by experts of the field in order to have an unbiased base to start digging in the topic. In Appendix A, we will provide the two questionnaires for transparency. The questionnaire is made up of three main parts: (a) which sustainability strategy is enrolled in the organization, in particular which environmental sustainability approach; (b) which indicators are mainly used to measure the internal and the external performance in the supply-chain of environmental sustainability; (c) possible internal and external impacts in the organization due to data transparency, e.g., in Scope 1 (direct emissions from owned sources), 2 (indirect emissions from the generation, e.g., of purchased electricity) and 3 (all other indirect emissions) emissions traceability. Interviews were transcribed and openly coded, at first with more detailed concepts and then with more synthetized themes [86,87].

3.3. Selected Metrics

As a thorough preparation for interviews, we identified the most meaningful KPIs in the decarbonization strategy of the steel sector. We compared the main existing frameworks in terms of environmental sustainability performance, and we added further details from the analyses of competitors in the steel sector. We had different moments of discussions with strategic managers of Feralpi, responsible for environmental sustainability and decarbonization, to determine the most critical indicators for the company. We also took into account the environmental indicators defined by the World Steel Organization, founded in 1967 and representing 85% of world steel production [88]. We further compared and integrated those indicators with the framework of the Global Reporting Initiative (GRI), which is the mainly used framework in the steel sector both for listed and for non-listed companies, such as the Feralpi Group. We identified this set of indicators in the three main field of environmental sustainability strategy of steel industries, which are CO2 emissions reduction, energy efficiency and Circular Economy:

| 1. | CO2 emissions: | Tons CO2 /ton crude steel cast |

| (comparable to GRI 305-1, Scope 1, direct emissions | ||

| and GRI 305-2, Scope 2, indirect emissions) | ||

| 2. | Energy intensity: | GJ/ton crude steel cast |

| (comparable to GRI 302-3) | ||

| 3. | Material efficiency: | % of materials converted to products & co-products |

| (comparable to GRI 306) |

In the comparison with other steel industries’ sustainability reports and with Federacciai, the Italian Federation for Steel Industries, we considered two more indicators, which could be useful in the investigation through our supply-chain interviews:

| 4. | CO2 emissions: | GRI 305-3 indirect transport emissions Scope 3 |

| (ton/year) | ||

| 5. | Energy intensity: | GRI 302-1 energy from renewable sources |

We looked how those indicators are represented in the main sustainability frameworks analyzed in Section 2.2 in order to have a more complete and solid insight into the current status of the main sustainability metrics. In Table 3, we show these selected indicators synthetically in the main frameworks we analyzed.

Table 3.

Selected environmental performance indicators within the main existing sustainability frameworks.

Another confirmation of those indicators is given by the Italian Steel Industries Association (Federacciai), focusing the environmental transition on the three main areas of CO2 emissions, energy and material efficiency [89]:

- Climate change: absolute and specific data of CO2 yearly;

- Energy efficiency: yearly consumption of electrical energy, in specific numbers;

- CE: percentage of recycled steel (use of scrap or iron ore).

In the framework of the Italian steel producers association, water is a fourth topic concerning environmental sustainability, although in different sustainability reports of steel industries, water consumption is still not considered relevant in the materiality matrix, used to identify the most critical sustainability topics in the organization [89]. The topic of water is also deployed in a wider way in the Benefit Corporation framework and in the mainly used CE framework. In Table 4, we give more insights into the main CE frameworks, which were useful to construct a complete picture to prepare the background for interviews.

Table 4.

Focus on Circularity metrics.

4. Findings

4.1. Environmental Sustainability: The Market Point of View on Achievable Decarbonization Goals

It is very interesting how environmental sustainability is immediately identified by the majority of the respondents, with the highly standard environmental certifications. Environmental sustainability and decarbonization are actually impacting not only the quality of products but the entire organization, a point which is really becoming important for final business partners too [90,91]: “Customers, especially abroad, begin to appreciate and require highly standard environmental certifications. Product quality is not the only important thing. Actually customers want to see that your organization itself is structured and certified” (CEO, Customer L, special steel); “Customers, more abroad than on the Italian market, appreciate certifications on organizational and procedure efficiency. You should think for example, that if, on the German market, 700 companies are EMAS certified, 300 companies only have ISO 14001” (Expert A, vice president, special steel).

Nevertheless, among customers, traders have a different response. They do not need specific environmental organization certification, since they are only commercial intermediators and not producers. They need the quality product certifications of their suppliers. Moreover, traders and dealers do not have a sustainability reporting system, although some of them are committed to sustainability leadership: “Our mission: sustainable supply-chain excellence delivered” (Customer O, international trader).

Environmental sustainability and decarbonization strategies push companies to achieve higher standards of certifications on the structural and organizational level: “It is the customer that determines a company’s environmental sustainability” (Customer D, civil and commercial engineering). Different certifications were mentioned by respondents, with the goal of certifying product quality and environmental sustainability. Usually, organizations start from the most basic certification to strive for higher quality standards, especially if those are recognized by their customers. UNI ISO 9001 is the quality management certification, which is principally focused to satisfy customers’ expectations [92]. ISO 14001 is the main certification for environmental management and focuses on the continuous improvement of companies in the environmental approach [93]. EMAS is the Eco-Management and Audit Scheme developed by the European Commission as the highest certification to report environmental performance, transparency and management, enforcing upon manufacturers the three pillars of decarbonization: CO2 emissions reduction, energy efficiency and circularity [94]. Customers underlined how more specific ISO energy efficiency certifications have become fundamental to be competitive on the market, such as ISO 50001, which supports fixing targets and measures in order to reach energy efficiency [95]. Safety is another important aspect for sustainability performance, such as ISO 45001, setting the standards for the occupational and safety protection of employees, where OHSAS 18001 was the initial base for this development [96]. SOA (Società Organismo di Attestazione certifying body) certification is an official recognition in order to participate in public procurement projects [97], which is needed by construction and engineering industries. For special steel customers, IATF (International Automotive Task Force) 16949 is a specific certification to ensure high-quality products for the automotive industry, with risk management, information-technology-guaranteed procedures and subsupplier management [98].

As underlined by our respondents, particularly for construction and engineering companies in the commodity steel sector, LEED and Breeam have become fundamental certifications in order to gain more points in the evaluation of sustainability projects and building. The United State Green Building Council (USGBC) was founded in 1993 and promotes sustainability in projecting, constructing and functioning of buildings for public and residential use. It promotes LEED certification (Leadership in Energy and Environmental Design), which is the world reference for certifying green building systems, with more than 100,000 buildings participating today [99]. Since 1990, Breeam is also a certification for the accomplishment of ESG (environment social governance) strategy in the building and construction sector [100]. Another important active framework, which was cited in interviews, was GRESB, which is a collector on ESG (environmental, social and governance) performance indicators on real estate, connecting investors and companies’ managers, and basing its scorecard on GRI and Science Based Targets Indicators, scoring GHG, energy, certifications and materials [101].

These schemes have increased their importance in recent years in the construction market, leading to a selection of suppliers, especially in public residential and civil engineering and construction. The financial strategy of investment funds has become more sustainable, obliging companies to demonstrate their environmental sustainability commitment: “Sustainability has become more important for investment funds. Your company can gain more market value for being more sustainable. Also the minimum environmental criteria (CAM- Criteri Ambientali Minimi) put more pressure on environmental sustainability” (Customer A, engineering and construction). The public construction sector is pushing the employment of green steel, being projects financed by ESG-rated funds, as final customers are more sensitive to environmental topics: “In the long-term, green steel could give marketing visibility to producers with the best environmental sustainability performance.” (Customer C, civil engineering and real estate).

Gradually, environmentally sustainability practices seem to become significant differentiation factors leveraging a competitive advantage among all levels of the supply-chain (producers, customers and suppliers): “Sustainability has gained importance in the last time. Customers are looking for material quality. They become more loyal. In the long-term, sustainability will praise a company’s competitive advantage. We also need to educate our suppliers about it” (Customer C, civil engineering and real estate).

We observe how environmental sustainability is not only an internal organizational process, but it is spread throughout the entire supply-chain, especially in the selection and involvement of suppliers [74]: “Sustainability is a must. With the new CSR (Corporate Sustainability Reporting) Directive, we will be obliged to report our sustainability strategy and also the control on the supply-chain will become tougher” (Customer M, fastener producer); “We can achieve our sustainability strategy also through our suppliers. We will deepen the selection of our suppliers, based on sustainability criteria” (Customer B, civil engineering and infrastructure).

External experts added an additional interesting element for the environmental strategy in the steel sector: beyond the market itself, norms are pushing the energy-intensive sector to make strong decisions, which can also affect economic viability [102]: “Steel companies are facing an accelerated transition towards decarbonization, due to a strong regulation push” (Expert E). Economic viability of manufacturers is pressured by the challenging carbon-neutral goals of the European Union, giving sometimes uncertainty on the feasibility of practical initiatives to reach them, even on a national level: “Looking at the environmental sustainability strategy, both in Italy and in Germany, we can observe that those challenging goals are in disagreement with the practical modalities to reach them concretely” (Expert B). As underlined by an expert point of view, in Germany, industrial plants are far away from energy sources. This implies that energy transportation and storage have to be organized in a safe way for the surrounding residential areas and to generate less environmental impact.

Another important underlined point emerged from experts’ perspective is the energy strategy suggested for steel industries. In the topic of decarbonization strategy for steel industries, it emerges clearly how one has to differentiate between the blast furnace sector and the electric arc furnace sector. According to a recent study by the U.S. Steel Manufacturers Association and the London CRU Group, an independent market analyst, EAF steelmakers have an average Scope 1 and 2 emission intensity (GRI 305-4: EU ETS direct emissions Scope 1 + indirect emissions resulting from electricity use/total final products) 75% lower than blast furnaces (BF) [103]. EAF technology exploits mainly scrap as raw material, making the production process more circular than in BF integrated production cycles. However, scrap is not the only source of recyclable material to reduce CO2 emissions: “In the short-term, carbon neutrality with hydrogen technology is not feasible, for technical and financial reasons. Also nuclear power results in a very cost intensive and long-time investment. The future of environmental sustainability in the steel sector will be biomasses, although we have to create a dedicated supply-chain from scratch, especially in Italy” (Expert C). The employment of biomasses (e.g., heated and dried sugar, cane sugar and pyrolyzed eucalyptus) instead of coke as chemical energy could enhance the decarbonization strategy of steel industries, meaning reducing CO2 emissions and enhancing CE practices [104]. Nevertheless, this would imply creating a completely new supply-chain, where biomass production is not too far away from steel manufacturing. It would mean generating new collaborations with suppliers beyond their own traditional value chain. In fact, this confirms the current literature underlying how supply-chain integration and collaboration are two fundamental bases for the fulfillment of environmental sustainability practices, in particular to close the loop in CE strategies [40]. From experts’ perspective, one observes how CE practices in the steel sector are useful steps to reach carbon neutrality goals. However, CE practices imply new organizational collaboration in the supply-chain and new experimental technologies [105]: “One key point in terms of CE practices is not to degrade the quality of the recycled material with a non-optimal reuse. For example, tin plates are especially used in Italy for the food industry. There is still no technical way to separate high quality material, like copper, from the rest. So copper goes as scrap in the commodity and special steel production, but it is not the optimal way to reuse resources” (Expert C). Achieving Industrial Symbiosis goals, integrated players are more focused on carbon capture solutions, which is a technology at the initial stadium. This process attempts to capture carbon to produce biofuel for other production processes [104]. Starting from mineral instead of recyclable material, i.e., scrap, integrated players have to invest in a broader set of initiatives to achieve carbon neutrality: “Blast furnace systems could optimize their emissions up to 66% with all this set of initiatives. In the case of EAF, both in terms of emissions and of energy consumption, it is hard to abate. Through scrap recycling, EAF is already a technology at high pace for decarbonization goals” (Expert C).

Concerning decarbonization strategies, a last focus was given by customers concerning energy efficiency strategies. Energy efficiency results in the use of renewable sources. Most interviewed customers are focusing on green energy sourcing, especially produced by photovoltaic or hydroelectric plants, with a strategic margin of profitability, especially in this period where energy prices are getting expensive due to the geopolitical situation: “We are gas and energy intensive. We invested in a photovoltaic system, to enforce our decarbonization strategy and to gain economic advantage, due to the current geo-political situation.” (Customer L, special steel); “We are investing in photovoltaic systems as a source of energy. For new plants. Next year, we will install a third photovoltaic system. It is important both for energy production and CO2 emissions balance.” (Customer H, construction and engineering).

In Table 5 we will give a summary of main results on decarbonization strategies in the steel sector.

Table 5.

Summary of main results on decarbonization strategies in the steel sector.

In Section 4.2, we will deepen the results concerning the topic of environmental KPIs, which are interestingly linked to the environmental supply-chain strategy.

4.2. Strategic KPIs: Finding a Shared Path for Measurement and Implementation

Emissions reduction is undoubtedly the first prioritized goal of steel industries in their decarbonization strategy [57]. Measurement of Scope 1, 2 and 3 emissions is a central point for steel industries, as confirmed by qualitative and quantitative benchmarking we carried out among sustainability reports by the Feralpi Group and its market. Very interestingly, emissions measurement KPIs are important for steel customers, but especially the knowledge of the percentage of post-consumer recycled material, which means steel is not disposed of in landfill but it can be reused in another manufacturing process [106], is even more fundamental for the market. For engineering, construction industries and construction service centers, the percentage of recycled material is fundamental in order to get access to the market, and it becomes a discriminant element to be selected in tenders [53]: “The percentage of recycled material is fundamental in your sector. Compared to some competitors, you have 93%, while others declare 98.5% and 99%. A big competitor has only 88%. You should pay more attention to it. In some cases, you can lose access to contracts” (Customer E, steel service center).

The percentage of post-consumer recycled material is fundamental information for the construction market. It is derived from the framework of the Environmental Product Declaration (EPD). The EPD is a certification testifying manufacturers commitment to improve the environmental impact of their own products and services, as a result of a Life Cycle Assessment (LCA) study, estimating indicators of environmental pressure (e.g., climate change), which can be associated with environmental interventions linked to product life cycle [107,108]. The scope of this indicator is surely an external communication to the market in order to gain contracts and a signal of CE strategy inside steel manufacturing. The percentage of recycled material is also driving internal innovation in companies, such as in construction engineering and service centers. They are trying to employ recycled steel producers’ slags in their aggregates in order to increase the percentage of recycled material in their products, which is established by the law now to a minimum of 5%: “We are experimenting with new aggregates from recyclable materials coming from steel producers (slags). They are quite promising. So we could increase the percentage of recycled material from the current 5% to 20%” (Customer H, construction and engineering).

Another important element which emerged from interviews is that the percentage of recycled material is also driving a reduction of the carbon footprint of these aggregates, with the cement industry being a higher producer of CO2 emissions than steel products and waste. Nevertheless, the market does not have the same opinion on the positive reaction on the information on the percentage of recycled material. Especially from a point of view of a trader and service center, the positive reaction of the market could depend on the nature of the product: “If you communicate to customers that your product has a high percentage of recycled material, like steel, this could be perceived positively if you are talking to the commodity sector, but negative, if you are selling in a more niche market (e.g., steel radiators for furniture, our second business activity). Here it depends on the subjective reaction of the final consumer” (Customer G, dealer).

The origin and regionality of material, deriving from the LEED and Breeam frameworks, is a further significant indicator. Products bought next to the construction site are more praised, since one can spare emissions derived from transportation and enhance the local community market: “Customers have increased to request Leed certification, especially in the public sector and with big companies. The percentage of recycled material is important. But also the geographic distance (200 Km) has become important. For us this (we can take the example of Feralpi) is not a problem with our current suppliers” (Customer J, service center).

Emissions are also a fundamental KPI in the steel supply-chain. In particular, a growing traceability topic is emissions Scope 3. For emissions, the main frameworks are GRI, SAASB, TFCD, GHG protocol and ISO 14067 product carbon footprint certification [109], becoming fundamental information for sustainability reporting too. Emissions measurement has not only an internal scope for steel manufacturers to trace environmental performance, but it has become significant for some customers too, both in the commodity and in the special steel sector. Particularly, Scope 3 measurement is gaining significance, with some practical problems in the tracking of the related information, due to comparability issues (“Scope 3 emissions traceability is required. It depends on the project. Certainly, they are data difficult to retrieve”—Customer D, civil engineering).

From the commodity sector, public buyers push construction industries and then steel manufacturers to reveal their carbon footprint (“For sure, green steel could be a powerful trademark to obtain projects in public hands. Here you can find an advantage and demonstrate more value compared to your competitors”—Customer E, steel service center). In the special steel branch, the automotive sector is making pressure for a more transparent information exchange: “CO2 is the currency of the future. Emissions traceability is pushed by regulatory changes and is creating market adjustments. Tomorrow the market will obligatorily require your carbon footprint as a steel producer. Then this will have an impact on the final product price, like in the automotive sector. Governments are pushing on decarbonization. Producers could ask for a higher price for their green products” (Customer O, international trader).

Energy efficiency seems to be more of an internal indicator to measure production process optimization and effectiveness, as shown by the answers of some customers from special steels. It also emerges that currently non-material indicators (water and soil consumption) will be required by reporting norms and markets pushed by the public hand in the future.

A final aspect is relevant from customer interviews: environmental performance and measurability divide business partners in the supply-chain into two sustainability leadership categories: followers and leaders. In general, customers from the construction sector are waiting for producers to guide them in their sustainability strategy: “We have a follower approach. If producers push us to engage more in a sustainability strategy, like carbon footprint traceability, we will follow.” (Customer E, steel service center). In the follower approach of some customers, it is highlighted how the role of leadership should be taken by steel producers, also by explaining the economic value and strategic advantage of employing green steel in the market: “Steel EAF producers have to better communicate with their marketing the environmental advantage of their products made from recycled material, e.g., scrap. They have to better explain the economic advantages of those green products to their customers.” (Customer G, dealer). In the special steel sector, it is mostly the final customer who pushes a clear traceability of sustainable environmental practices: “It will be the first time for us. One customer asked us to make our product carbon footprint. If it works, we will extend this initiative to other supply-chain partners, e.g., Feralpi.” (Customer L, special steel). The leadership approach of some customers is characterized by facilitating steel producers in the path of making their decarbonization strategy economically valuable for the entire supply-chain: “Of course there are differences among sectors. Automotive is at a higher level of sustainability awareness, the construction sector still at a lower level. As a trader, we want to give an additional service. We have a facilitator role for producers. In the construction sector is the moment to anticipate. We want to chase opportunities. We would like to take the early mover advantage. Now it is time to take action” (Customer O, international trader).

In Table 6, we show strategic environmental KPIs in the steel sector.

Table 6.

Main strategic environmental KPIs in the steel sector.

Strategic environmental KPIs are still important in order to manage company successful performance internally: “Everything is monitored. There is a tight control. We can intercept anomalies predictively. Teams have access with their profile to specific environmental data (e.g., emissions, energy efficiency, waste management…)” (Expert A). However, successful KPIs should have a bottom-up more than a top-down approach, to be both used and understood concretely in daily work (“Benchmarking? It is a huge effort to put together numbers. Who will look at numbers? If something does not work at the shop floor, nothing can work. Workers need simple indicators. This is a big critical point: companies have to concentrate on strategic indicators for daily work, not only for reporting.”—Expert B) and in information exchange in the supply-chain (“We have a dedicated team to collect data. The point is: are these data really trustworthy? I collect data from the construction site and I have to trust the data they give me. There is a need to standardize indicators and data in the sector.”—Customer B, civil engineering and infrastructure). Transparency and comparability are fundamental elements for the significance and usability of KPIs, not only for the internal guidance of the company but also in the information exchange with business partners.

5. Discussion

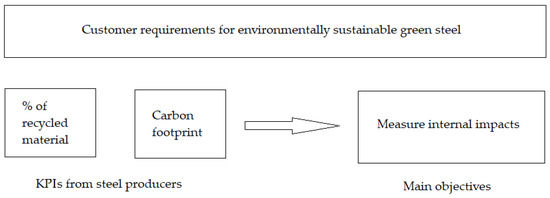

The creation of a comprehensive framework among environmental sustainability strategy and environmental performance KPIs is an important step of the research, which is useful both from an academic and practice perspective. This research gives impetus for further investigation on which sustainability indicators are strategic in the energy-intensive supply-chain. Results underlined how transparency, accountability and comparability are important factors for the usefulness of information exchange in the supply-chain [110]. In both steel commodities and special steel sectors, customers are more and more interested in environmental best practices of steel producers, and they are willing to award suppliers which are able to transparently demonstrate the carbon footprint of their products, which can become a selection criterion in business collaboration. Beyond clear normative European environmental constraints, the market is pushing both the commodity and the special steel sector to engage in green steel environmental strategies. As shown in Figure 1, customers of steel producers need environmental sustainability data mainly in two domains: CO2 emissions (carbon footprint) and CE practices (% of recycled material used in production processes). Those data are not only important internal drivers for strategic decisions in the organization, but they have become essential diversification points from competitors both in the construction and special steel market.

Figure 1.

Main KPIs and objectives for green steel.

It remains unclear how green characteristics could make steel products more praiseworthy in customers’ opinions, especially by commodity markets. Green materials currently have a green premium compared to the price of virgin materials [111]. From customers’ point of view, steel producers which are already sustainability leaders should take pace with more innovative technical marketing, which could explain the advantages and the added value of greener products. In this sense, comparable KPIs could foster information exchange and make evidence of environmental sustainability strategy from both a technical and economic perspective [112].

The reduction of the CO2 emissions is linked also to the employment of CE practices, which means the use of alternative recycled raw materials, whose carbon footprint can also be tracked by digital technologies. Smart circular supply-chains can give a competitive advantage to industries [113,114], such as those already experimented with in the automotive sector, where suppliers are selected and traced based on their environmental sustainability practices and the way they can demonstrate their environmental performance. Scope 3 emissions are monitored not only by the special steel industry but also by the commodity sector. We saw how final customers (construction sites), pushed by financial markets (investors), need green steel in order to access tenders and in the end to acquire new contracts. Nevertheless, the lack of easy, transparent and comparable environmental sustainability KPIs causes a void of regulation in the market, making steel producers and customers uncertain about the information to be given and on possible premium prices to be recognized as green steel [115]. Beyond the pressure of environmental regulations and markets, one can observe how customers embrace two different approaches: being a follower in green best practice or being a leader. This important decision is also guided by the presence of resources, both financial and human, in the organization, which can be dedicated to exploring the market more deeply and to engaging in collaborative partnerships with steel producers. CE practices are linked for the commodity steel market with the measurability of the percentage of recyclable material used in the process. CE practices, such as the reuse of apparently exhausted materials in current or new production processes, have been accelerated due to the new market interest towards green steel, both in the commodity and special steel sector. New recycled materials, such as biomass, can come from other sectors and be employed in steel production in a perspective of Industrial Symbiosis [38].

From a managerial point of view, this research suggests how fundamental it is, especially for producers far away from the final customer, to get in touch with their business partners and create a round table of discussions, where, beyond the commercial contractual conditions, other important aspects, such as environmental and supply efficiency can be identified in an optic of collaboration and integration. From an academic point of view, this research highlighted quite a new aspect: in the supply-chain collaboration, on average, suppliers are the initiators of green innovation technology initiatives [116]. Here, we focus on the point of view of customers, who, getting the needs and pains [117] of the final consumer, as especially happens in the automotive industry, can highlight important market trends and topics and offer the territory for future alliances in order to build more effective green supply-chains [118]. From an academic perspective, this research contributes additionally to the literature on environmental sustainability strategy and decarbonization, which is still an open field of discussion, especially in the steel sector [119,120]. In particular, we contribute to the research on strategic KPIs for environmental sustainability excellence, which is also a green field in terms of standardization and practicability, with the goal to enhance more effectiveness both on the shop floor and in the supply-chain [121,122].

6. Conclusions

Through our research, we put a starting point to further discover the perspective of the steel market on decarbonization strategies and sustainability environmental KPI. We think the perspective of the market is an important point of reference not only for steel producers, both in the case of special steel and commodities, but also in the whole energy-intensive sector. Decarbonization goals, including energy efficiency and Circular Economy practices, can be reached out only in a collaborative way through the supply-chain, preserving the economic viability of such environmental initiatives. Future research should also look at the suppliers’ perspective, who are also involved in decarbonization goals and strategies, such as ferroalloys, lime and coke suppliers, where reduction in CO2 emissions is also fundamental like it is for customers. In particular, research should explore how relevant information and strategic KPIs are not only communicated to business partners, but how they become relevant sources for energy-intensive producers in order to obtain further competitive advantage in the market. The further deepening of the use of digital and Industry 4.0 technologies could give more insights in information sharing and its impacts in the energy-intensive sector supply-chain. In the division of followers and leaders on green steel in the supply-chain, innovative steel producers could take the lead to influence the market and make the advantage of green steel more economically appealing for their customers. If information of CO2 emissions and CE practices is more communicated and perceived by the market as a key driver to differentiate standard products such as steel, energy efficiency is more monitored internally as a driver of production process optimization. Further research should investigate how energy efficiency information could be made more feasible for the market, as a further driver of competitive advantage. Moreover a more complete picture of the phenomenon will be given by looking for a more enlarged ethnographic perspective, by interviewing business partners in another context, such as Germany, which can be easily offered for example by the single case study of this research. This was a limitation of our current research, since we especially focused on the perspective of the Italian market. We are convinced that future research should further explore the connection between environmental sustainability and metrics, which are extremely important in order to assess the full potential of decarbonization strategy, also from an economical point of view.

Author Contributions

First author (L.T.) contributed to conceptualization, methodology, finding analysis and interpretation. Second author (E.D.M.) contributed to conceptualization, methodology, validation and finding analysis. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Ethical review and approval were waived for this study due to the complete anonymity of aggregated data.

Informed Consent Statement

Participant consent was waived due to the complete anonymity of aggregated data.

Data Availability Statement

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

A.1. Semi-Structured Interview Questionnaires for Customers and Experts

A.1.1. Questionnaire for Customers for Qualitative Interviews, June–August 2022

First part: Focus on the organization

What are the main actions of your sustainability strategy? And specifically in terms of CO2 emissions reduction, circular economy and energy efficiency?

What strategic indicators do you use in the company to check your performance in the field of CO2 reduction, circular economy and energy efficiency? Which framework (e.g., GRI, European taxonomy) do they belong to?

What are the objectives for using these indicators (internal, marketing, supply chain, …)?

Which of these indicators are critical for you to select your suppliers? Which ones are meaningful to your customers?

Second part: Projects in the supply-chain (especially with Feralpi, if relevant)

Considering the projects underway (or under development) with the Feralpi Group, which of these indicators are essential to verify the attractiveness of Feralpi compared to other competitors?

What are the projects that you would put in place to better integrate information with the Feralpi Group?

In your opinion, what is the future of the development of sharing and integration of strategic information in the supply chain to allow greater integration of the actors involved and better achieve the decarbonisation objectives?

A.1.2. Questionnaire for Experts for Qualitative Interviews, June–August 2022

In your opinion, what are the main actions of the sustainability strategy in the steel industry, specifically for electric arc furnace and blast furnace production? And in particular in terms of reducing CO2 emissions, circular economy and energy efficiency?

What are the strategic indicators used by manufacturers to check performance in the areas of CO2 reduction, circular economy and energy efficiency? Which framework (e.g., GRI, European taxonomy) do they belong to the most?

What are the objectives for using these indicators (internal, marketing, supply chain, …)?

Which of these indicators are a key to selecting suppliers? Which ones are meaningful to your customers?

In your opinion, what are the future/possible projects for the development of sharing and integration of strategic information in the supply chain to allow greater integration of the actors involved and better achieve the decarbonisation objectives?

References

- European Environment Agency. Climate Change, Impacts and Vulnerability in Europe 2016—Key findings; European Environment Agency: Copenhagen, Denmark, 2016.

- European Parliament. What is Carbon Neutrality and How Can It Be Achieved by 2050? 21 June 2021. Available online: https://www.europarl.europa.eu/news/en/headlines/society/20190926STO62270/what-is-carbon-neutrality-and-how-can-it-be-achieved-by-2050 (accessed on 1 January 2022).

- García-García, P.; Carpintero, O.; Buendía, L. Just energy transitions to low carbon economies: A review of the concept and its effects on labour and income. Energy Res. Soc. Sci. 2020, 70, 101664. [Google Scholar] [CrossRef]

- United Nations. Climate Change Conference. COP26. The Glasgow Climate Pact. The Conference of the Parties Serving as the Meeting of the Parties to the Paris Agreement. 12 November 2021. Available online: https://unfccc.int/process-and-meetings/the-paris-agreement/the-glasgow-climate-pact-key-outcomes-from-cop26 (accessed on 20 January 2022).

- Senato della Repubblica. Pacchetto Clima-Energia. Atti Comunitari n. 11, 12, 13, 14, 15, 16. n. 13/DN. 7 November 2008. XVI Legislatura. Unione Europea. Available online: https://www.senato.it/documenti/repository/lavori/affarieuropei/dossier/XVI/Dossier%2013_DN.pdf (accessed on 25 January 2022).

- European Commission. 2030 Climate and Energy Framework. Available online: https://ec.europa.eu/clima/eu-action/climate-strategies-targets/2030-climate-energy-framework_en (accessed on 2 January 2022).

- European Commission. Delivering the European Green Deal. Available online: https://ec.europa.eu/info/strategy/priorities-2019-2024/european-green-deal/delivering-european-green-deal_en#leading-the-third-industrial-revolution (accessed on 2 January 2022).

- European Commission. Communication from the Commission to the European Parliament, the European Council, the Council, the European Economic and Social Committee and the Committee of the Regions. The European Green Deal. 11 December 2019. Available online: https://eur-lex.europa.eu/resource.html?uri=cellar:b828d165-1c22-11ea-8c1f-01aa75ed71a1.0002.02/DOC_1&format=PDF (accessed on 5 February 2022).

- European Commission. A European Green Deal. Available online: https://ec.europa.eu/info/strategy/priorities-2019-2024/european-green-deal_en (accessed on 3 January 2022).

- European Commission. Recovery and Resilience Scoreboard. Pillars. Available online: https://ec.europa.eu/economy_finance/recovery-and-resilience-scoreboard/pillar_overview.html?lang=en (accessed on 2 January 2022).

- European Commission. Recovery Plan for Europe. 2021. Available online: https://commission.europa.eu/strategy-and-policy/recovery-plan-europe_en (accessed on 1 December 2021).

- #Next Generation Italia. Piano Nazionale di Ripresa e Resilienza. Bozza Aggiornata al 12 gennaio. 2021. Available online: https://www.governo.it/sites/new.governo.it/files/PNRR_2021_0.pdf (accessed on 5 January 2022).

- Magnani, A. Next Generation EU, Cos’è e Come Funziona. Il Sole 24 Ore. 4 March 2021. Available online: https://www.ilsole24ore.com/art/next-generation-eu-cos-e-e-perche-l-europa-deve-correre-fondi-la-ripresa-covid-ADlKpzMB (accessed on 15 December 2021).

- Trainer, T. A technical critique of the Green New Deal. Ecol. Econ. 2022, 195, 107378. [Google Scholar] [CrossRef]

- McKinsey & Company. The Net Zero Transition. Report. What It Would Cost, What It Would Bring. McKinsey Global Institute in Collaboration with McKinsey Sustainability and McKinsey’s Global Energy & Materials and Advanced Industries Practices. January 2022. Available online: https://www.mckinsey.com/capabilities/sustainability/our-insights/the-net-zero-transition-what-it-would-cost-what-it-could-bring (accessed on 3 February 2022).

- Zumente, I.; Lace, N. ESG Rating—Necessity for the Investor or the Company? Sustainability 2021, 13, 8940. [Google Scholar] [CrossRef]

- Mobarakeh, M.R.; Kienberger, T. Climate neutrality strategies for energy-intensive industries: An Austrian case study. Clean. Eng. Technol. 2022, 10, 100545. [Google Scholar] [CrossRef]

- Bataille, C.G.F. Physical and Policy Pathways to Net-Zero Emissions Industry. WIREs Clim. Chang. 2020, 11, e633. [Google Scholar] [CrossRef]

- Baste, I.A.; Watson, R.T. Tackling the climate, biodiversity and pollution emergencies by making peace with nature 50 years after the Stockholm Conference. Glob. Environ. Chang. 2022, 73, 102466. [Google Scholar] [CrossRef]

- Vogl, V.; Åhman, M.; Nilsson, L.J. Assessment of Hydrogen Direct Reduction for Fossil-Free Steelmaking. J. Clean. Prod. 2018, 203, 736–745. [Google Scholar] [CrossRef]

- Mallet, A.; Pal, P. Green transformation in the iron and steel industry in India: Rethinking patterns of innovation. Energy Strategy Rev. 2022, 44, 100968. [Google Scholar] [CrossRef]

- Yu, X.; Tan, C. China’s pathway to carbon neutrality for the iron and steel industry. Glob. Environ. Chang. 2022, 76, 102574. [Google Scholar] [CrossRef]

- Toktaş-Palut, P. Analyzing the effects of Industry 4.0 technologies and coordination on the sustainability of supply chains. Sustain. Prod. Consum. 2022, 30, 341–358. [Google Scholar] [CrossRef]

- Majeed, M.A.A.; Rupasinghe, T.D. Internet of things (IoT) embedded future supply chains for industry 4.0: An assessment from an ERP-based fashion apparel and footwear industry. Int. J. Supply Chain Manag. 2017, 6, 5–40. [Google Scholar]

- Jensen, J.P.; Prendeville, S.M.; Bocken, N.M.P.; Peck, D. Creating sustainable value through remanufacturing: Three industry cases. J. Clean. Prod. 2019, 218, 304–314. [Google Scholar] [CrossRef]

- Mebratu, D. Sustainability and sustainable development. Environ. Impact Assess. Rev. 2018, 18, 493–520. [Google Scholar] [CrossRef]

- Jackson, T. Prosperity without Growth: Economics for a Finite Planet; Earthscan: London, UK, 2011. [Google Scholar]

- Bocken, N.M.P.; Short, S.W.; Rana, P.; Evans, R.S. A literature and practice review to develop sustainable business model archetypes. J. Clean. Prod. 2014, 65, 42–56. [Google Scholar] [CrossRef]

- Geissdoerfer, M.; Savage, P.; Bocken, N.M.P.; Hultink, E.J. The Circular Economy- A new sustainability paradigm? J. Clean. Prod. 2017, 143, 757–768. [Google Scholar] [CrossRef]

- Ellen MacArthur Foundation. Towards the Circular Economy. Economic and Business Rationale for an Accelerated Transition; Ellen MacArthur Foundation: Cowes, UK, 2013. [Google Scholar]

- Bag, S.; Yadav, G.; Dhamija, P.; Kataria, K.K. Key resources for industry 4.0 adoption and its effect on sustainable production and circular economy: An empirical study. J. Clean. Prod. 2021, 281, 125233. [Google Scholar] [CrossRef]

- Berg, H.; Bendix, P.; Jansen, M.; Le Blévennec, K.; Bottermann, P.; Magnus-Melgar, M.; Pohjalainen, E.; Wahlström, M. Unlocking the Potential of Industry 4.0 to Reduce the Environmental Impact of Production; Eionet Report—ETC/WMGE 2021/5; European Environment Agency, European Topic Center on Waste and Materials in a Green Economy: Boeretang, Belgium, 2021.

- Birkel, H.; Hartmann, E. Internet of Things—The future of managing supply chain risks. Supply Chain Manag. 2020, 25, 535–548. [Google Scholar] [CrossRef]