The Electricity Market in Greece: Current Status, Identified Challenges, and Arranged Reforms

Abstract

1. Introduction

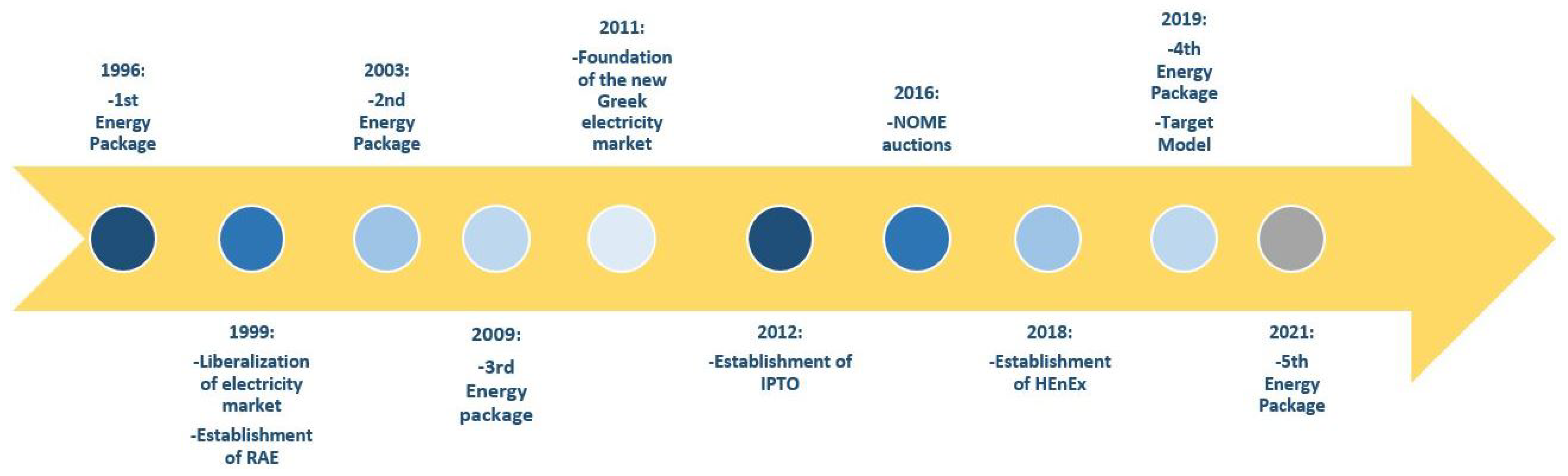

2. The Electricity Market Policy Framework

3. The Target Model Architecture

3.1. Forward Energy Market

3.2. Day-Ahead Market

3.3. Intra-Day Market

3.4. Balancing Market

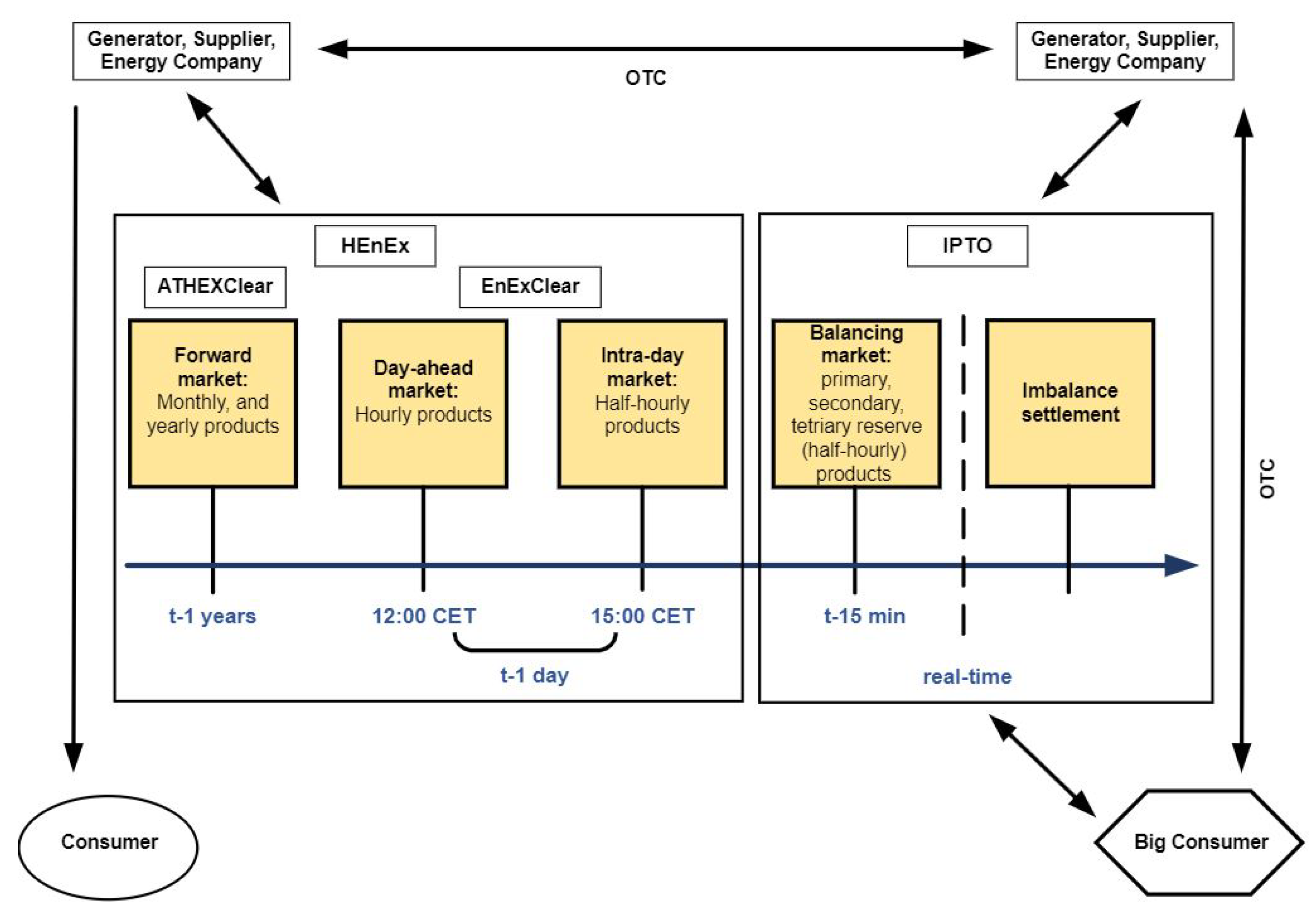

4. The Electricity Market in Greece

4.1. Forward Market in Greece

4.2. Day-Ahead Market in Greece

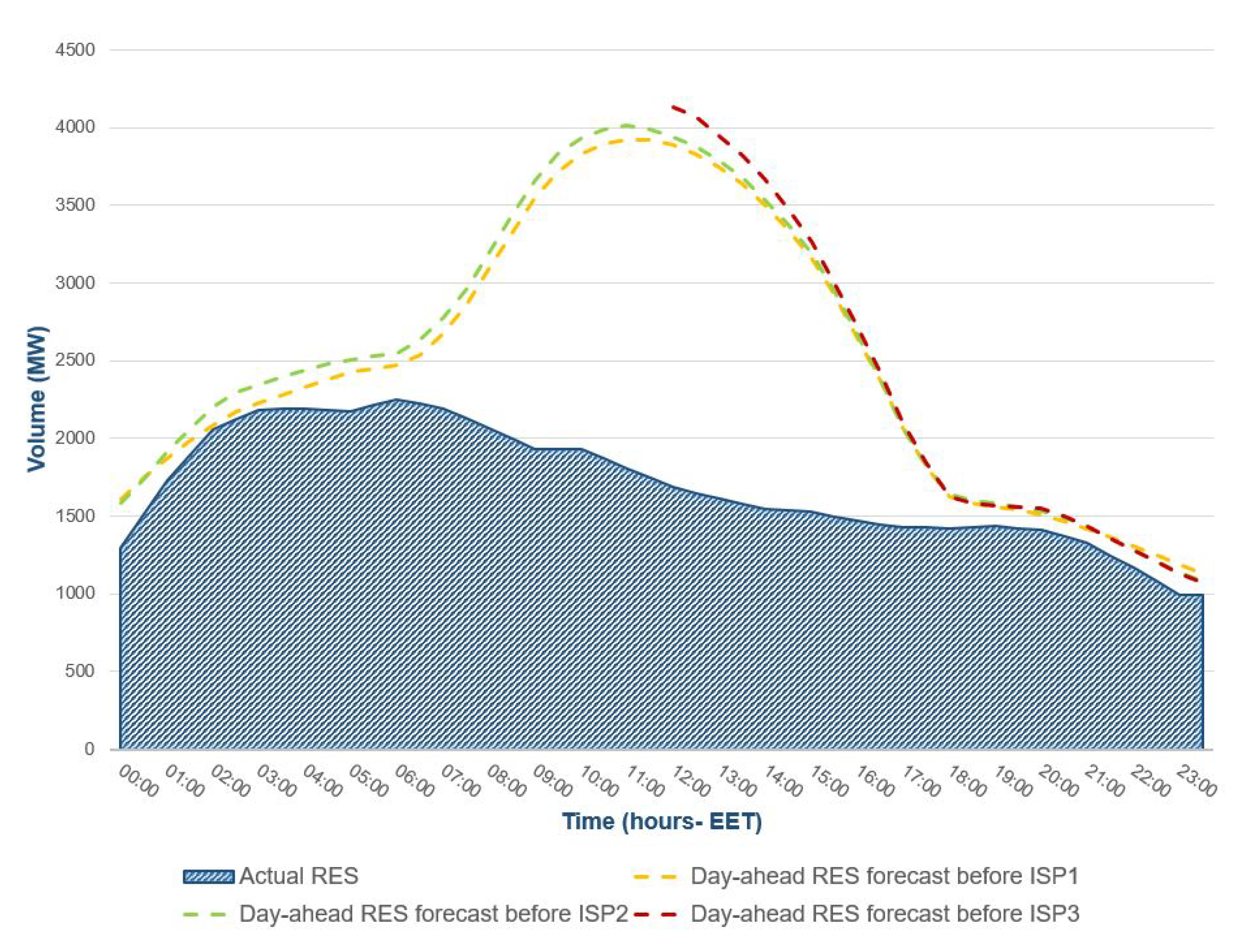

4.3. Intra-Day Market in Greece

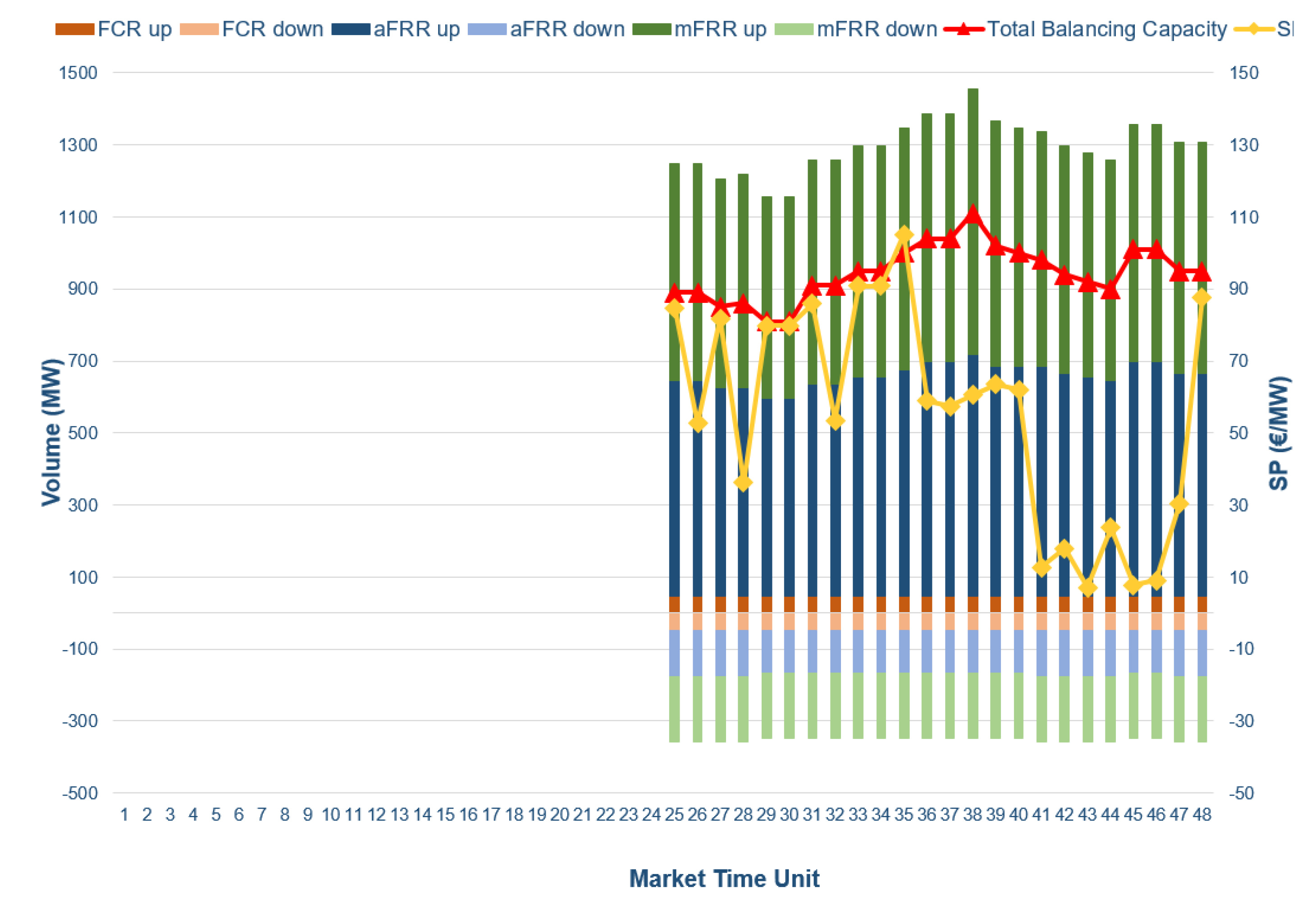

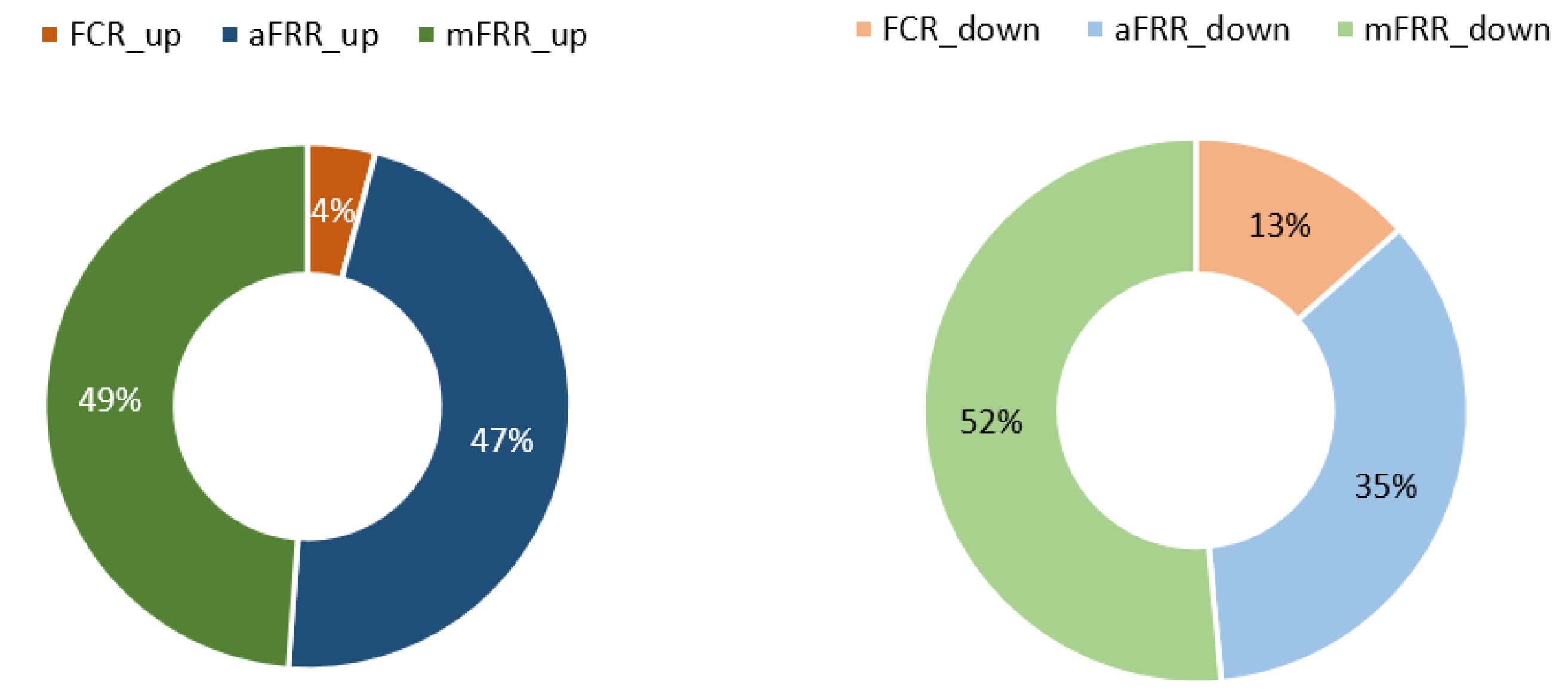

4.4. Balancing Market in Greece

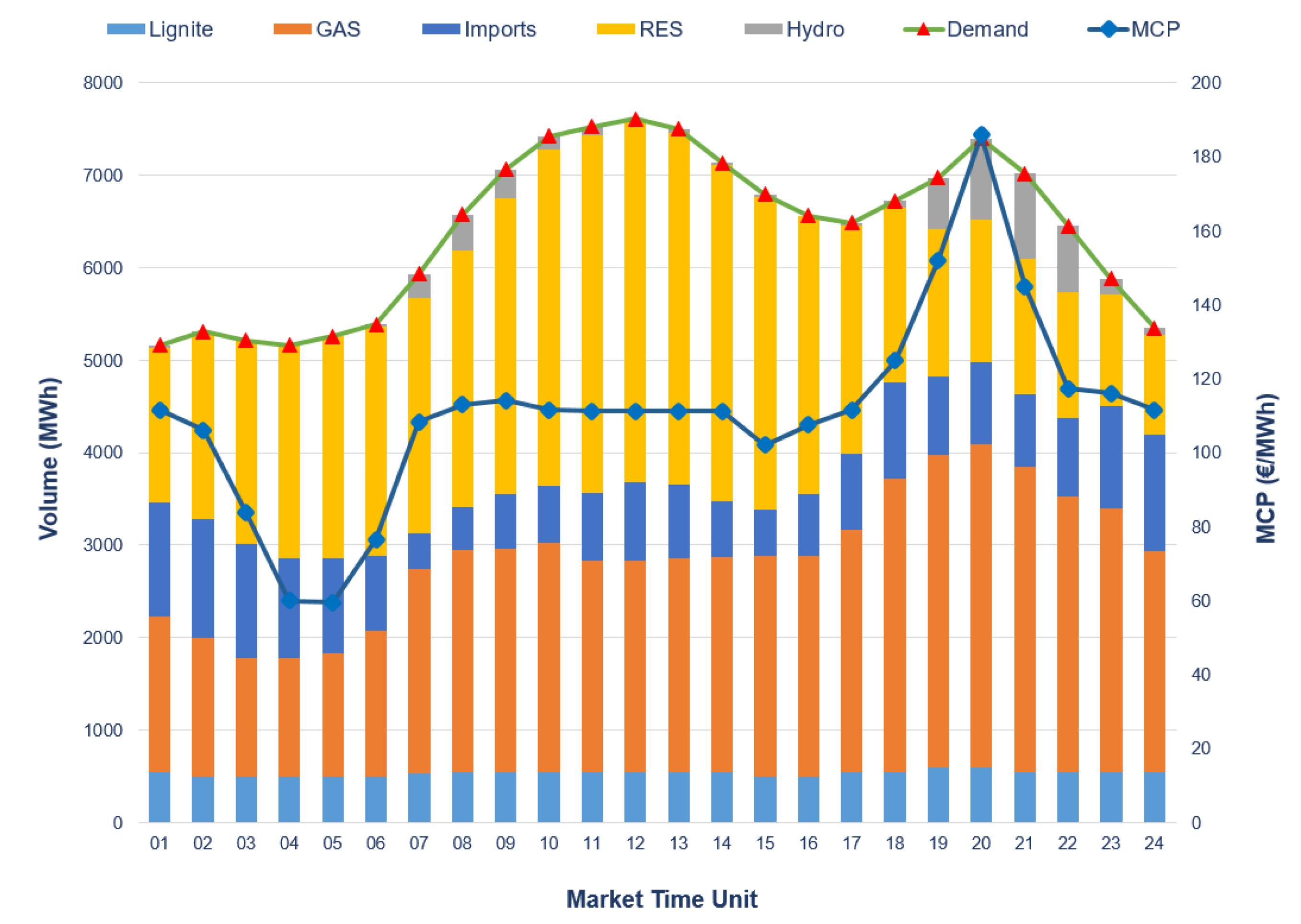

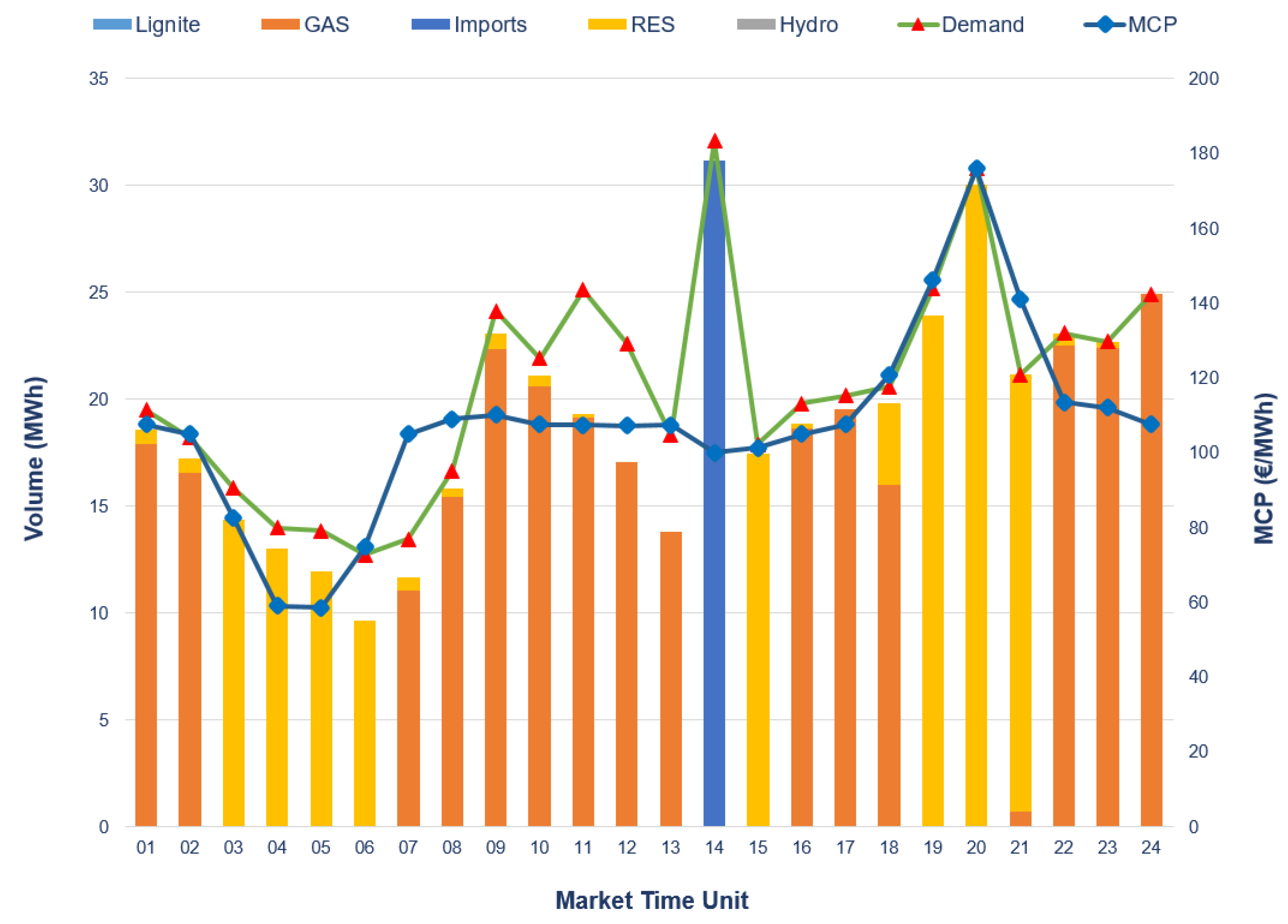

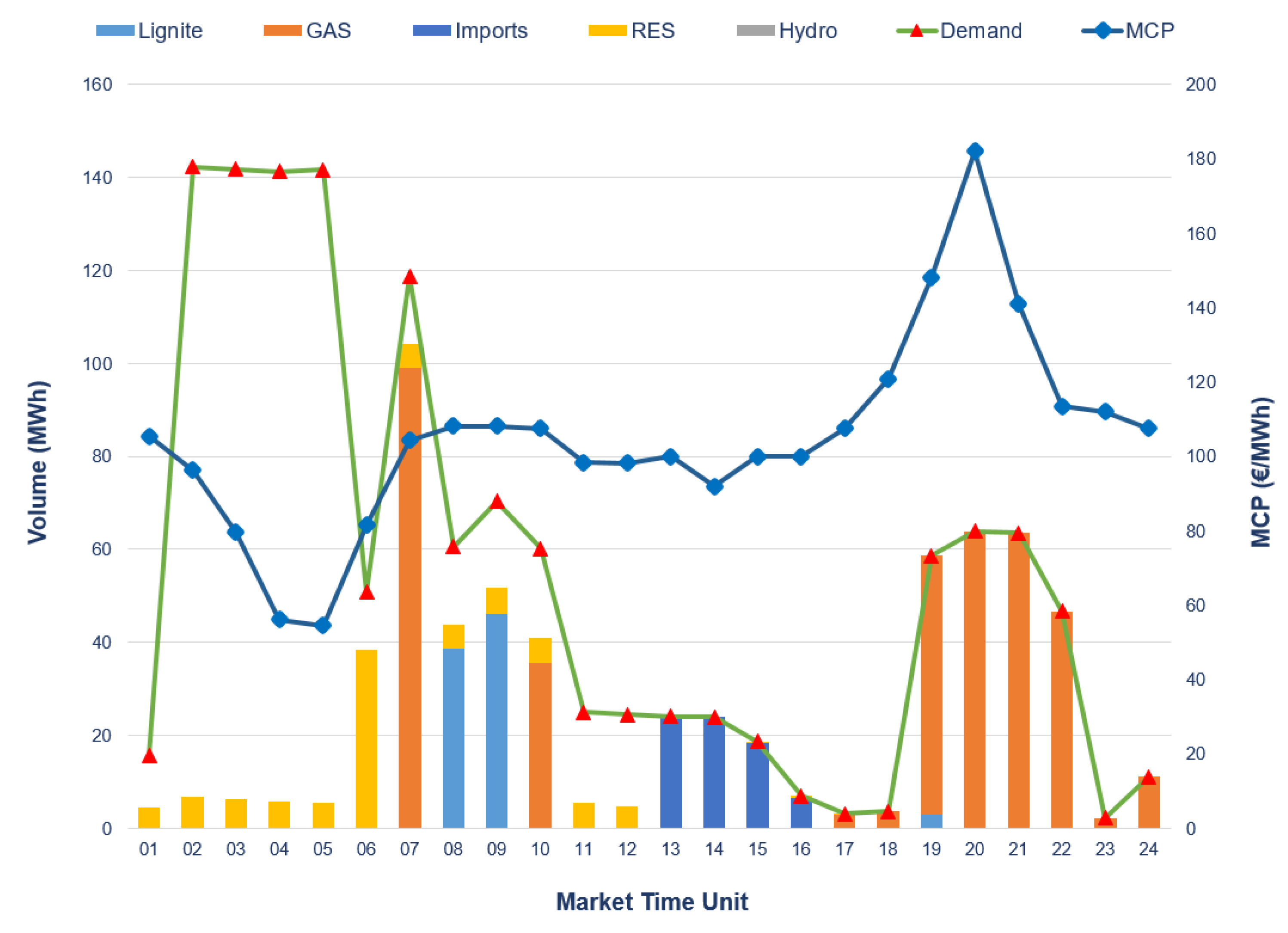

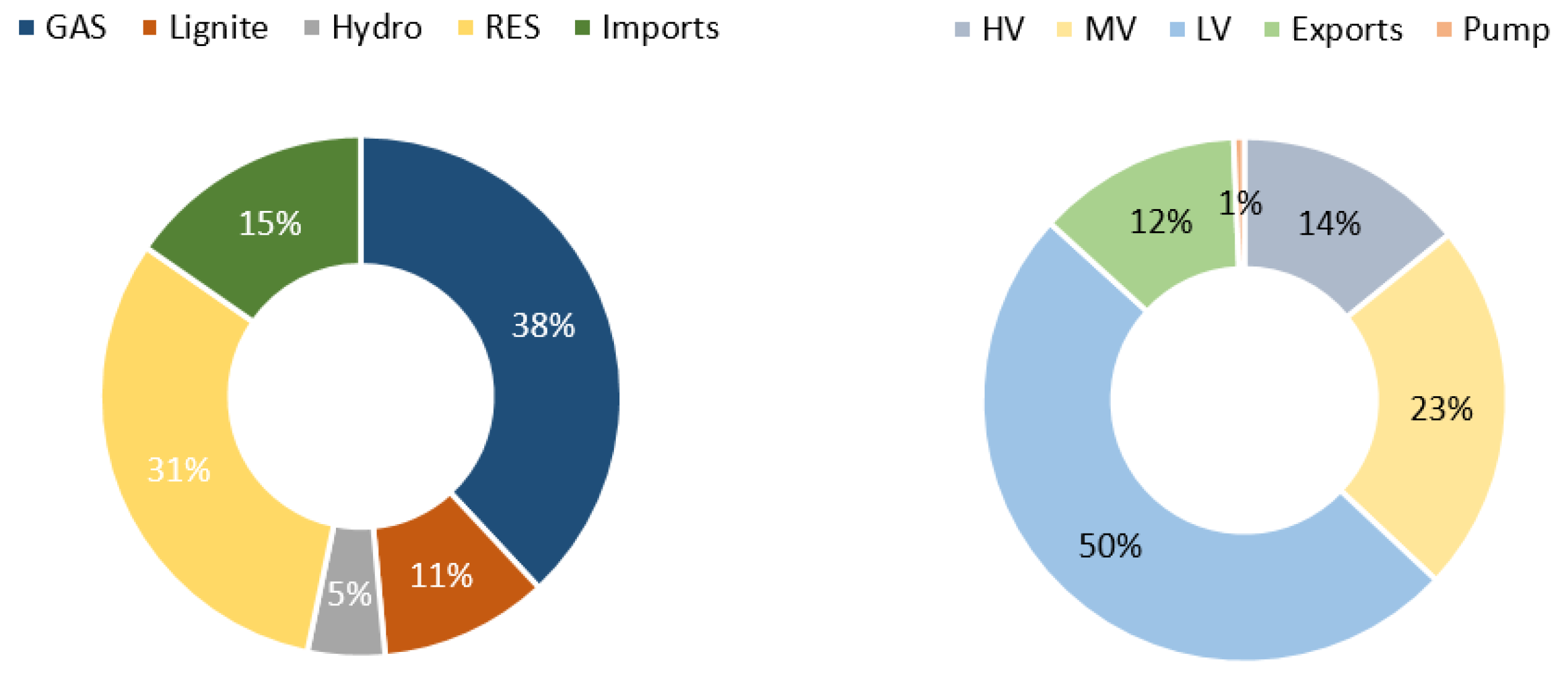

5. A Case Study of the Current Market Structure in Greece

6. The Identified Challenges in the Greek Electricity Market and the Proposed Reforms

7. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Abbreviations

| EU | European Union |

| CEP | clean energy package |

| FM | forward market |

| DAM | the day-ahead market |

| IDM | intra-day market |

| BM | balancing market |

| RES | renewable energy sources |

| DSR | demand side response |

| ACER | agency for the Cooperation of Energy Regulators |

| EB GL | electricity balancing guideline |

| TSOs | transmission system operators |

| DSOs | distribution system operators |

| SO GL | system operation guideline |

| CACM GL | capacity allocation and congestion management guideline |

| FCA GL | forward capacity allocation guideline |

| IPTO | Independent Power Transmission Operator |

| RAE | Regulatory Authority of Energy |

| HEnEx | Hellenic Energy Exchange |

| OTC | over-the-counter |

| EEX | European Energy Exchange |

| PTRs | physical transmission rights |

| JAO | Joint Allocation Office |

| SDAC | single day-ahead coupling |

| PCR | Price Coupling of Regions |

| EUPHEMIA | Pan-European Hybrid Electricity Market Integration Algorithm |

| NEMOs | Nominated Electricity Market Operators |

| XBID | cross-border intra-day |

| SIDC | single intra-day coupling |

| CRIDAs | complementary intra-day auctions |

| BRPs | balancing responsible parties |

| BSPs | balance service providers |

| RRs | restoration reserves |

| FCRs | frequency containment reserves |

| mFRR | manual frequency restoration reserve |

| aFRR | automatic frequency restoration reserve |

| FRRs | frequency restoration reserves |

| IN | imbalance netting |

| TERRE | Trans—European Replacement Reserves Exchange |

| MARI | Manually Activated Reserves Initiative |

| PICASSO | Platform for the International Coordination of Automated Frequency |

| Restoration and Stable System Operation | |

| IGCC | International Grid Control Cooperation |

| ATHEXClear | Athens Exchange Clearing House |

| MiFID II | Financial Instruments Directive |

| EMIR | European market infrastructure regulation |

| ETSS | Energy Trading Spot Market System |

| MRC | multi-regional coupling |

| IBWT | Italian Borders Working Table |

| HVDC | high voltage DC |

| SEleNe CC | Southeast Electricity Network Coordination Center |

| RCC | Regional Coordination Center |

| MCP | market clearing price |

| FiT | feed-in-tariff |

| VoLL | value of lost load |

| SEE CAO | South East Europe |

| ISP | Integrated Scheduling Programming |

| AGC | Automatic General Control |

| RTBM | Real-time Balancing Market |

| CBT | cross-border electricity trading |

| LV | low voltage |

| MV | medium voltage |

| HV | high voltage |

| SP | settlement price |

| IP | imbalance price |

| FiP | feed-in-premium |

| RES-PPAs | Renewable Energy Systems—Power Purchase Agreements |

References

- European Palriament. The Internal Market: General Principles, Fact Sheet. 2021. Available online: https://www.europarl.europa.eu/factsheets/en/sheet/33/the-internal-market-general-principles (accessed on 7 February 2023).

- Next Kraftwerke. The European Energy Market—Liberalization & Unbundling. 2021. Available online: https://www.nextkraftwerke.be/en/knowledge-hub/liberalized-european-energy-market/ (accessed on 7 February 2023).

- EPEX SPOT. Basics of the Power Market. 2021. Available online: https://www.epexspot.com/en/basicspowermarket#electricity-a-unique-commodity (accessed on 7 February 2023).

- Florence School of Regulation. The Clean Energy for All Europeans Package. 2020. Available online: https://fsr.eui.eu/the-clean-energy-for-all-europeans-package/ (accessed on 7 February 2023).

- European Wind Energy Association. Creating the Internal Energy Market in Europe. 2012. Available online: http://www.ewea.org/uploads/tx_err/Internal_energy_market.pdf__cf_chl_f_tkv3WZT_WBpg2e8heaibT_AdtOkcj5XUlSWnuguuaj618-1642499273-0-gaNycGzNA1E (accessed on 7 February 2023).

- Kambouris, Y.; The Balancing Market. Proceedings of RAE Conference on Target Model, Athens. 2018. Available online: http://oldsite.rae.gr/site/file/system/docs/various/anartiseis/2207_1;jsessionid=0ac113f330d974196418896d4310bdedd1f4afc92bd9.e34Lah0LbNqMe38NaxqLch0Lci1ynknvrkLOlQzNp65In0 (accessed on 7 February 2023).

- Belyaev, L.S. Electricity Market Reforms: Economics and Policy Challenges; Springer: Berlin/Heidelberg, Germany, 2011. [Google Scholar]

- European Parliamentary Research Service. Understanding Electricity Markets in the EU. 2016. Available online: http://www.easyres-project.eu/wp-content/uploads/2019/02/understanding-elecricity-markets-in-the-eu.pdf (accessed on 7 February 2023).

- Metaxas, A.; Mathioulakis, M.; Lykidi, M. Implementation of the Target Model: Regulatory Reforms and obstacles for the Regional Market Coupling. Eur. Energy J. (EEJ) 2019, 8, 24–39. [Google Scholar] [CrossRef]

- Dagoumas, A. Impact of Bilateral Contracts on Wholesale Electricity Markets: In a Case Where a Market Participant Has Dominant Position. Appl. Sci. 2019, 9, 382. [Google Scholar] [CrossRef]

- Ahlqvist, V.; Holmberg, P.; Tangerås, T. A survey comparing centralized and decentralized electricity markets Author links open overlay panel. Energy Strategy Rev. 2022, 40, 100812. [Google Scholar] [CrossRef]

- Pellini, E. Measuring the impact of market coupling on the Italian electricity market. Energy Policy 2012, 48, 322–333. [Google Scholar] [CrossRef]

- Do, H.X.; Nepal, R.; Jamasb, T. Electricity market integration, decarbonisation and security of supply: Dynamic volatility connectedness in the Irish and Great Britain markets. Energy Econ. 2022, 92, 104947. [Google Scholar] [CrossRef]

- Gaffney, F.; Deane, J.P.; Gallachóir, B.P.Ó. Reconciling high renewable electricity ambitions with market economics and system operation: Lessons from Ireland’s power system. Energy Strategy Rev. 2019, 26, 100381. [Google Scholar] [CrossRef]

- González, J.S.; Alonso, C.Á. Industrial electricity prices in Spain: A discussion in the context of the European internal energy market. Energy Policy 2021, 148, 111930. [Google Scholar] [CrossRef]

- Tanrisever, F.; Derinkuyu, K.; Jongen, G. Organization and functioning of liberalized electricity markets: An overview of the Dutch market. Renew. Sustain. Energy Rev. 2015, 51, 1363–1374. [Google Scholar] [CrossRef]

- Newbery, D. Tales of two islands—Lessons for EU energy policy from electricity market reforms in Britain and Ireland. Energy Policy 2017, 105, 597–607. [Google Scholar] [CrossRef]

- Di Cosmo, V.; Lynch, M. Competition and the single electricity market: Which lessons for Ireland? Util. Policy 2016, 41, 40–47. [Google Scholar] [CrossRef]

- Heijden, T.V.; Lago, J.; Palensky, P.; Abraham, E. Electricity price forecasting in European Day Ahead Markets: A greedy consideration of market integration. IEEE Access 2021, 9, 119954–119966. [Google Scholar] [CrossRef]

- Andrianesis, P.; Biskas, P.; Liberopoulos, G. An overview of Greece’s wholesale electricity market with emphasis on ancillary services. Electr. Power Syst. Res. 2011, 81, 1631–1642. [Google Scholar] [CrossRef]

- Papaioannou, G.P.; Dikaiakos, C.; Evangelidis, G.; Papaioannou, P.G.; Georgiadis, D.S. Co-movement analysis of Italian and Greek electricity market wholesale prices by using a wavelet approach. Energies 2015, 8, 11770–11799. [Google Scholar] [CrossRef]

- Andrianesis, P.E.; Liberopoulos, G.; Papalexopoulos, A.D. Greek wholesale electricity market: Forthcoming market changes and bid/cost recovery. In Proceedings of the 8th Mediterranean Conference on Power Generation Transmission, Distribution and Energy Conversion (MEDPOWER 2012), Cagliari, Italy, 1–3 October 2012; pp. 1–6. [Google Scholar]

- Danias, N.; Swales, J.K.; McGregor, P. The Greek electricity market reforms: Political and regulatory considerations. Energy Policy 2013, 62, 1040–1047. [Google Scholar] [CrossRef]

- Venizelos, E.C. EU Target Model Implementation Towards Sustainability-The Case Study of Greek Power Market. Ph.D. Dissertation, University of Piraeus, Piraeus, Greece, 2021. [Google Scholar]

- Ioannidis, F.; Kosmidou, K.; Andriosopoulos, K.; Everkiadi, A. Assessment of the Target Model Implementation in the Wholesale Electricity Market of Greece. Energies 2021, 14, 6397. [Google Scholar] [CrossRef]

- RAE. Market Reform Plan for Greece—Ver. 8. 2021. Available online: https://ec.europa.eu/energy/sites/default/files/greece_market_reform_plan.pdf (accessed on 7 February 2023).

- Manolopoulos, D.; Kitsopoulos, K.; Kaldellis, J.K.; Bitzenis, A. The evolution of renewable energy sources in the electricity sector of Greece. Int. J. Hydrogen Energy 2016, 41, 12659–12671. [Google Scholar] [CrossRef]

- Ibn Saif, A.U.N.; Khadem, S.K. Consumer-centric Electricity Market: Review of key European projects. In Proceedings of the 17th International Conference on the European Energy Market (EEM), Stockholm, Sweden, 16–18 September 2020; pp. 1–6. [Google Scholar]

- Forouli, A.; Bakirtzis, E.A.; Papazoglou, G.; Oureilidis, K.; Gkountis, V.; Candido, L.; Ferrer, E.D.; Biskas, P. Assessment of Demand Side Flexibility in European Electricity Markets: A Country Level Review. Energies 2021, 14, 2324. [Google Scholar] [CrossRef]

- Single Electricity Market (SEM) Committee. Consultation on Dispatch, Redispatch and Compensation Pursuant to Regulation (EU) 2019/943. 2021. Available online: https://www.semcommittee.com/sites/semc/files/media-files/SEM-21-026%20Consultation%20on%20Dispatch%2C%20Redispatch%20and%20Compensation%20Pursuant%20to%20Regulation%20EU%202019943.pdf (accessed on 7 February 2023).

- ACER. Market Monitoring Report 2020—Electricity Wholesale Market Volume. 2022. Available online: https://extranet.acer.europa.eu/Official_documents/Acts_of_the_Agency/Publication/ACER%20Market%20Monitoring%20Report%202020%20%E2%80%93%20Electricity%20Wholesale%20Market%20Volume.pdf (accessed on 7 February 2023).

- European Union. Directive 96/92/EC of the European Parliament and of the Council Concerning Common Rules for the Internal Market in Electricity; OJ L 027, 30.01.1997; European Union: Brussels, Belgium, 1997; pp. 20–29. [Google Scholar]

- European Union. Directive 98/30/EC of the European Parliament and of the Council Concerning Common Rules for the Internal Market in Natural Gas; OJ L 204, 21.07.1998; European Union: Brussels, Belgium, 1998; pp. 1–12. [Google Scholar]

- European Union. Directive 2003/55/EC of the European Parliament and of the Council Concerning Common Rules for the Internal Market in Natural Gas and Repealing Directive 98/30/EC; OJ L 176, 15.07.2003; European Union: Brussels, Belgium, 2003; pp. 57–78. [Google Scholar]

- European Union. Regulation (EC) No 1228/2003 of the European Parliament and of the Council on Conditions for Access to the Network for Cross-Border Exchanges in Electricity; OJ L 176, 15.7.2003; European Union: Brussels, Belgium, 2003; pp. 1–10. [Google Scholar]

- European Union. Directive 2009/72/EC of the European Parliament and of the Council Concerning Common Rules for the Internal Market in Electricity and Repealing Directive 2003/54/EC; OJ L 211, 14.8.2009; European Union: Brussels, Belgium, 2009; pp. 55–93. [Google Scholar]

- European Union. Regulation (EC) No 714/2009 of the European Parliament and of the Council on Conditions for Access to the Network for Cross-Border Exchanges in Electricity and Repealing Regulation (EC) No 1228/2003; OJ L 211, 14.8.2009; European Union: Brussels, Belgium, 2003; pp. 15–35. [Google Scholar]

- European Union. Regulation (EC) No 713/2009 of the European Parliament and of the Council Establishing an Agency for the Cooperation of Energy Regulators; OJ L 211, 14.8.2009; European Union: Brussels, Belgium, 2009; pp. 1–14. [Google Scholar]

- European Union. Regulation (EU) 2019/943 of the European Parliament and of the Council on the Internal Market for Electricity; OJ L 158, 14.6.2019; European Union: Brussels, Belgium, 2019; pp. 54–124. [Google Scholar]

- European Union. Directive (EU) 2019/944 of the European Parliament and of the Council on Common Rules for the Internal Market for Electricity and Amending Directive 2012/27/EU; OJ L 158, 14.6.2019; European Union: Brussels, Belgium, 2019; pp. 125–199. [Google Scholar]

- European Commission. Amendment to the Renewable Energy Directive to Implement the Ambition of the New 2030 Climate Target. 2021. Available online: https://commission.europa.eu/document/2caaf8e2-df20-4bdb-bde0-384599b1e82e_en (accessed on 7 February 2023).

- Wildgrube, T. Fit for 55? An Assessment of the Effectiveness of the EU COM’s Reform Proposal for the EU ETS. No. 22/04; EWI Working Paper; Institute of Energy Economics at the University of Cologne (EWI): Cologne, Germany, 2022. [Google Scholar]

- Marcu, A.; Maratou, A.; Mehling, M.; Cosbey, A. The EU Carbon Border Adjustment Mechanism (CBAM). In Preliminary Analysis of the European Commission Proposal for a Regulation Establishing a Carbon Border Adjustment Mechanism; CBAM: Amsterdam, The Netherlands, 2021; p. 564. [Google Scholar]

- Florence School of Regulation. Fit for 55: EU Rolls Out Largest Ever Legislative Package in Pursuit of Climate Goals. 2021. Available online: https://fsr.eui.eu/fit-for-55-eu-rolls-out-largest-ever-legislative-package-in-pursuit-of-climate-goals/ (accessed on 7 February 2023).

- ENTSO-E. Network Codes. 2016. Available online: http://annualreport2016.entsoe.eu/network-codes/ (accessed on 7 February 2023).

- European Union. Commission Regulation (EU) 2017/2195 Establishing a Guideline on Electricity Balancing; OJ L 312, 28.11.2017; European Union: Brussels, Belgium, 2017; pp. 6–53. [Google Scholar]

- European Union. Commission Regulation (EU) 2017/1485 Establishing a Guideline on Electricity Transmission System Operation; OJ L 220, 25.8.2017; European Union: Brussels, Belgium, 2017; pp. 1–120. [Google Scholar]

- European Union. Commission Regulation (EU) 2015/1222 Establishing a Guideline on Capacity Allocation and Congestion Management; OJ L 197, 25.7.2015; European Union: Brussels, Belgium, 2015; pp. 24–72. [Google Scholar]

- European Union. Commission Regulation (EU) 2016/1719 Establishing a Guideline on Forward Capacity Allocation; OJ L 259, 27.9.2016; European Union: Brussels, Belgium, 2016; pp. 42–68. [Google Scholar]

- Biskas, P.N.; Marneris, I.G.; Chatzigiannis, D.I.; Roumkos, C.G.; Bakirtzis, A.G.; Papalexopoulos, A. High-level design for the compliance of the Greek wholesale electricity market with the Target Model provisions in Europe. Electr. Power Syst. Res. 2016, 152, 323–341. [Google Scholar] [CrossRef]

- Fafaliou, I.; Polemi, M.L. Trends in the European electricity markets: The case of Greece. Int. J. Econ. Bus. Res. 2010, 2, 369. [Google Scholar] [CrossRef]

- Beus, M.; Pavić, I.; Štritof, I.; Capuder, T.; Pandžić, H. Electricity Market Design in Croatia within the European Electricity Market-Recommendations for Further Development. Energies 2018, 11, 346. [Google Scholar] [CrossRef]

- Hellenic Association for Energy Economics. Greek Energy Market Report. 2020. Available online: https://www.haee.gr/FileServer?file=ca430e84-31ec-4fa8-8153-ac3f6eb16b70 (accessed on 7 February 2023).

- Hellenic Association for Energy Economics. Greek Energy Market Report. 2019. Available online: https://www.haee.gr/media/4858/haees-greek-energy-market-report-2019-upload-version.pdf (accessed on 7 February 2023).

- HEnEx. Spot Trading Rulebook: Day-Ahead & Intra-Day Markets Trading Rulebook—Ver. 1.4. 2021. Available online: https://www.enexgroup.gr/documents/20126/144557/Spot_Trading_Rulebook_v1.4_en.pdf (accessed on 7 February 2023).

- Biskas, P.N.; Chatzigiannis, D.I.; Bakirtzis, A.G. European electricity market integration with mixed market designs—Part I: Formulation. IEEE Trans. Power Syst. 2014, 29, 458–465. [Google Scholar] [CrossRef]

- KU Leuven Energy Institute. EI Fact Sheet: The Current Electricity Market Design in Europe. 2015. Available online: https://set.kuleuven.be/ei/images/EI_factsheet8_eng.pdf/ (accessed on 7 February 2023).

- Ashworth, P.; Baldwin, K.G.H.; Brear, M.; Chappel, T.; Garbutt, M.; Hernandez, C.A.; Jotzo, F.; MacGill, I.; Nelson, T. Overview of papers for the Special Issue of The Electricity Journal: The Future Electricity Market Summit. Electr. J. 2020, 33, 9. [Google Scholar] [CrossRef]

- Swin, G.P.; Natraj, A.; O’Mahoney, A. The European Target Model and the impact of implicit auctions on interconnection capacity prices. In Proceedings of the 13th International Conference on the European Energy Market (EEM), Porto, Portugal, 6–9 June 2016; pp. 1–6. [Google Scholar]

- ACER. European Electricity Forward Markets and Hedging Products—State of Play and Elements for Monitoring. 2015. Available online: https://www.acer.europa.eu/en/Electricity/Market%20monitoring/Documents_Public/ECA%20Report%20on%20European%20Electricity%20Forward%20Markets.pdf| (accessed on 7 February 2023).

- Ausubel, L.M.; Cramton, P. Using forward markets to improve electricity market design. Util. Policy 2010, 18, 195–200. [Google Scholar] [CrossRef]

- Florence School of Regulation. Electricity Markets in the EU. 2020. Available online: https://fsr.eui.eu/electricity-markets-in-the-eu/ (accessed on 7 February 2023).

- ENTSO-E. Single Day-Ahead Coupling (SDAC). 2021. Available online: https://www.entsoe.eu/network_codes/cacm/implementation/sdac/ (accessed on 7 February 2023).

- Koltsaklis, N.E.; Dagoumas, A.S. Incorporating unit commitment aspects to the European electricity markets algorithm: An optimization model for the joint clearing of energy and reserve markets. Appl. Energy 2018, 231, 235–258. [Google Scholar] [CrossRef]

- Koltsaklis, N.E.; Zenginis, I.; Dagoumas, A.S. Assessing new block order options of the EUPHEMIA algorithm: An optimization model for the economic dispatch problem in power exchanges. Energy Rep. 2020, 6, 3119–3140. [Google Scholar] [CrossRef]

- Zad, B.B.; Toubeau, J.F.; Vatandoust, B.; Bruninx, K.; De Grève, Z.; Vallée, F. Enhanced integration of flow-based market coupling in short-term adequacy assessment. Electr. Power Syst. Res. 2021, 201, 107507. [Google Scholar] [CrossRef]

- Vajdić, M.; Kelava, M. Development and Impact of Flow-Based Methodology in Core Region. J. Energy Energ. 2020, 69, 4. [Google Scholar] [CrossRef]

- European Commission, Directorate-General for Energy. The Future Electricity Intraday Market Design. Publications Office. 2019. Available online: https://data.europa.eu/doi/10.2833/004191 (accessed on 7 February 2023).

- 2020. Available online: https://data.efet.org//Files/Documents/Electricity%20Market/Spot%20and%20short-term%20markets/EFET_ID_MarketDesign_06052020.pdf (accessed on 7 February 2023).

- ENTSO-E. European Cross-Border Intraday (XBID) Solution Trades Exceed 2.5 Million Since Go-Live. 2018. Available online: https://www.entsoe.eu/news/2018/09/06/european-cross-border-intraday-xbid-solution-trades-exceed-2-5-million-since-go-live/ (accessed on 7 February 2023).

- NEMO Commitee. Single Intraday Coupling (SIDC). 2021. Available online: https://www.nemo-committee.eu/sidc (accessed on 7 February 2023).

- ENTSO-E. Single Intraday Coupling (SIDC). 2021. Available online: https://www.entsoe.eu/network_codes/cacm/implementation/sidc/ (accessed on 7 February 2023).

- ENTSO-E. Electricity Balancing in Europe—ENTSO-E Releases an Overview of the European Electricity Balancing Market and Guideline. 2018. Available online: https://www.entsoe.eu/news/2018/12/12/electricity-balancing-in-europe-entso-e-releases-an-overview-of-the-european-electricity-balancing-market-and-guideline/ (accessed on 7 February 2023).

- ENTSO-E. Balancing Report. 2020. Available online: https://eepublicdownloads.azureedge.net/clean-documents/Publications/Market%20Committee%20publications/ENTSO-E_Balancing_Report_2020.pdf (accessed on 7 February 2023).

- ACER. Decision No 11/2020 on the Methodology for a List of Standard Products for Balancing Capacity for Frequency Restoration Reserves and Replacement Reserves. 2020. Available online: https://documents.acer.europa.eu/Official_documents/Acts_of_the_Agency/Individual%20decisions/ACER%20Decision%2011-2020%20on%20standard%20products%20for%20balancing%20capacity.pdf (accessed on 7 February 2023).

- Single Electricity Market Committee. System Services-Future Arrangement Scoping Paper, SEM-20-044. 2020. Available online: https://www.semcommittee.com/sites/semc/files/media-files/SEM-20-044%20System%20services%20future%20arrangements%20scoping%20paper.pdf (accessed on 7 February 2023).

- ENTSO-E. All TSOs’ Proposal for the Implementation Framework for a European Platform for the Exchange of Balancing Energy from Frequency Restoration Reserves with Automatic Activation in Accordance with Article 21 of Commission Regulation (EU) 2017/2195 Establishing a Guideline on Electricity Balancing. 2018. Available online: https://eepublicdownloads.entsoe.eu/clean-documents/nc-tasks/EBGL/EBGL_A21_181218_ALL%20TSOs%20proposal_aFRRIF_explanatory_document_for%20submission.pdf?Web=0 (accessed on 7 February 2023).

- ENTSO-E. Explanatory Document of Proposals for Amendement of the Implementation Frameworks for the European Balancing Platforms in Accordance with Articles 20(1), 21(1) and 22(1) of Commission Regulation (EU) 2017/2195 Establishing a Guideline on Electricity Balancing. 2021. Available online: https://consultations.entsoe.eu/markets/mfrr_afrr_in_if_amendment/supporting_documents/PfA_IFs_Explanatory%20document.pdf (accessed on 7 February 2023).

- ENTSO-E. Automatic Frequency Restoration Reserve Process Implementation Guide. 2019. Available online: https://eepublicdownloads.entsoe.eu/clean-documents/EDI/Library/ERRP/Automatic_Frequency_Restoration_Reserve_Process_IG_v1.0.pdf (accessed on 7 February 2023).

- ENTSO-E. PICASSO Platform. 2021. Available online: https://www.entsoe.eu/network_codes/eb/picasso/ (accessed on 7 February 2023).

- ENTSO-E. MARI Platform. 2021. Available online: https://www.entsoe.eu/network_codes/eb/mari/ (accessed on 7 February 2023).

- ENTSO-E. TERRE Platform. 2021. Available online: https://www.entsoe.eu/network_codes/eb/terre/ (accessed on 7 February 2023).

- Florence School of Regulation. The EU Electricity Network Codes. 2017. Available online: https://www.scribd.com/document/364124461/FSR-NC-Course-Text (accessed on 7 February 2023).

- HEnEx. Towards the Integration of Greek and EU Energy Markets—Policy Briefs. 2019. Available online: https://www.haee.gr/media/4859/policy-brief-henex_-final-244201.pdf (accessed on 7 February 2023).

- IPTO. The European Target Model. 2017. Available online: https://www.admie.gr/en/market/general/description (accessed on 7 February 2023).

- EnEx. Derivatives Markets Trading. 2021. Available online: https://www.enexgroup.gr/derivatives_trading (accessed on 7 February 2023).

- Ioannidis, F.; Kosmidou, K.; Makridou, G.; Andriosopoulos, K. Market design of an energy exchange: The case of Greece. Energy Policy 2019, 133, 110887. [Google Scholar] [CrossRef]

- EnEx. Electricity Derivatives, Day-Ahead and Intra-Day Markets Operation under Target Model. 2019. Available online: https://energypress.gr/sites/default/files/media/002_-_papadionysiou_exe_-_final.pdf (accessed on 7 February 2023).

- EPEX SPOT. Extension of Single Day-Ahead Coupling (SDAC) to Greece—Go-Live Planned for 15 December 2020. 2020. Available online: https://www.epexspot.com/en/news/extension-single-day-ahead-coupling-sdac-greece-go-live-planned-15-december-2020 (accessed on 7 February 2023).

- Koltsaklis, N.; Dagoumas, A. Policy Implications of Power Exchanges on Operational Scheduling: Evaluating EUPHEMIA’s Market Products in Case of Greece. Energies 2018, 11, 2715. [Google Scholar] [CrossRef]

- NEMO Commitee. EUPHEMIA Public Description: Single Price Coupling Algorithm. 2020. Available online: https://www.nordpoolgroup.com/globalassets/download-center/single-day-ahead-coupling/euphemia-public-description.pdf (accessed on 7 February 2023).

- IPTO. Technical Limits for Bidding Prices and Clearing Prices in the Balancing Market—Ver. 1.0. 2020. Available online: https://www.admie.gr/sites/default/files/users/dda/KAE/TECHNICAL%20LIMITS_EN.pdf (accessed on 7 February 2023).

- ECCO International. Detailed Level Market Design of the Hellenic Forward, Day-Ahead and Intraday Markets and Respective Market Codes and High-Level IT. 2017. Intra-Day Market Code: JRC/PTT/2017/C.3/0017/OC, Vol. 4.. Available online: https://www.dapeep.gr/wpcontent/uploads/diavouleuseis/2017/2017.12.18INTRADAYMARKETCODEENGLISH.pdf (accessed on 7 February 2023).

- Vespucci, M.T.; Innorta, M.; Cervigni, G. A Mixed Integer Linear Programming model of a zonal electricity market with a dominant producer. Energy Econ. 2013, 35, 35–41. [Google Scholar] [CrossRef]

- IPTO. Balancing Market Rulebook—Ver. 3.0. 2020. Available online: https://www.admie.gr/sites/default/files/users/dda/KAE/Balancing%20Market%20Rulebook_v3.pdf (accessed on 7 February 2023).

- IPTO. System Balancing. 2021. Available online: https://www.admie.gr/en/market/general/capacity-calculation (accessed on 7 February 2023).

- HEnEx. Markets Archive. 2022. Available online: https://www.enexgroup.gr/web/guest/markets-archive (accessed on 7 February 2023).

- IPTO. Market Statistics—Data. 2022. Available online: https://www.admie.gr/en/market/market-statistics/detail-data (accessed on 7 February 2023).

- Makrygiorgou, D.I.; Andriopoulos, N.; Georgantas, I.; Dikaiakos, C.; Papaioannou, G.P. Cross-Border Electricity Trading in Southeast Europe Towards an Internal European Market. Energies 2020, 13, 6653. [Google Scholar] [CrossRef]

- Knaut, A.; Paschmann, M. Price volatility in commodity markets with restricted participation. Energy Econ. 2019, 81, 37–51. [Google Scholar] [CrossRef]

- RAE. RAE DECISION NO. 54/2021—Amendment of the Balancing Market Regulation: Adoption of Measures Aimed at the Smooth Operation of the Balancing Market and the Promotion of Effective Competition in It. 2021. Available online: https://www.rae.gr/apofaseis/8083/ (accessed on 7 February 2023).

- Agostini, M.; Bertolini, M.; Coppo, M.; Fontini, F. The participation of small-scale variable distributed renewable energy sources to the balancing services market. Energy Econ. 2021, 97, 105208. [Google Scholar] [CrossRef]

- Guo, B.; Weeks, M. Dynamic tariffs, demand response, and regulation in retail electricity markets. Energy Econ. 2022, 106, 105774. [Google Scholar] [CrossRef]

- Neetzow, P.; Pechan, A.; Eisenack, K. Electricity storage and transmission: Complements or substitutes? Energy Econ. 2018, 76, 367–377. [Google Scholar] [CrossRef]

- Polemis, M.L.; Dagoumas, A.S. The electricity consumption and economic growth nexus: Evidence from Greece. Energy Policy 2013, 62, 798–808. [Google Scholar] [CrossRef]

- EnergyPress. HEDNO preparing to Announce Latest Smart Meters Tender. 2020. Available online: https://energypress.eu/hedno-to-announce-new-smart-meters-tender-backed-by-recovery-fund/ (accessed on 7 February 2023).

- HEDNO. Metering Systems Modernization. 2021. Available online: https://deddie.gr/en/stratigiki-eksugxronismos/eksugxronismos/eksugxronismos-metritikwn-sustimatwn/ (accessed on 7 February 2023).

- Nicolli, F.; Vona, F. Energy market liberalization and renewable energy policies in OECD countries. Energy Policy 2019, 128, 853–867. [Google Scholar] [CrossRef]

- Andriopoulos, N.; Bachoumis, A.; Alefragis, P.; Birbas, A. Optimization of a Local Energy Market Operation in a Transactive Energy Environment. In Proceedings of the 17th International Conference on the European Energy Market (EEM), Stockholm, Sweden, 16–18 September 2020; pp. 1–6. [Google Scholar]

- Duch-Brown, N.; Rossetti, F. Digital platforms across the European regional energy markets. Energy Policy 2020, 144, 111612. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Instrument | Total Orders | Max Price | Min Price | AVG Price | Total Quotes |

|---|---|---|---|---|---|

| GREBM1021 | 2 | 157 | 154 | 155.5 | 1 |

| GREBM1121 | 2 | 171.5 | 167.5 | 169.5 | 1 |

| GREBQ421 | 49 | 160 | 150.4 | 158.3 | 7 |

| GREBY22 | 2 | 115 | 110 | 112.5 | 1 |

| GREPM1021 | 2 | 164.75 | 160.25 | 162.5 | 1 |

| GREPQ421 | 16 | 172.13 | 166.65 | 169.27 | 8 |

| GREPY22 | 2 | 122.75 | 116.25 | 119.5 | 1 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Makrygiorgou, J.J.; Karavas, C.-S.; Dikaiakos, C.; Moraitis, I.P. The Electricity Market in Greece: Current Status, Identified Challenges, and Arranged Reforms. Sustainability 2023, 15, 3767. https://doi.org/10.3390/su15043767

Makrygiorgou JJ, Karavas C-S, Dikaiakos C, Moraitis IP. The Electricity Market in Greece: Current Status, Identified Challenges, and Arranged Reforms. Sustainability. 2023; 15(4):3767. https://doi.org/10.3390/su15043767

Chicago/Turabian StyleMakrygiorgou, Jemma J., Christos-Spyridon Karavas, Christos Dikaiakos, and Ioannis P. Moraitis. 2023. "The Electricity Market in Greece: Current Status, Identified Challenges, and Arranged Reforms" Sustainability 15, no. 4: 3767. https://doi.org/10.3390/su15043767

APA StyleMakrygiorgou, J. J., Karavas, C.-S., Dikaiakos, C., & Moraitis, I. P. (2023). The Electricity Market in Greece: Current Status, Identified Challenges, and Arranged Reforms. Sustainability, 15(4), 3767. https://doi.org/10.3390/su15043767