Abstract

This study investigates the factors that affect farmers’ access to Food Security and Agricultural Credit (FSAC) services for the farmers of Pakistan who have no access to banking but have a feasible farm business. Using multiple regressions and logistic analysis, the authors revealed the determinants of farmers’ financial literacy and analyzed the variables which affected the farmers’ accessibility to FSAC. Results indicated that the average financial literacy of respondents was at a moderate level. It was affected by the age of respondents, length of their education, distance to nearby cities, ownership of bank accounts, annual income, and financial education experience. The FSAC accessibility was also impacted by the area of cultivated land, interest rate, collateral, farms’ income, financial literacy index, credit accessibility experiences, the legal status of farmer groups, and the amount of a loan. Some of the issues that prevent farmers from having widespread access to the FSAC include the lack of loan need, lack of FSAC awareness, lack of collateral, loan usury perspective, loan rejection experience, fear of borrowing from the bank, and inactive farmer groups. The study contributes to the existing literature on the determinants of farmers’ access and choice of credit sources by using a primary data set.

1. Introduction

1.1. Financial Literacy and Access to Capital

Food security is a form of state defense. All nations will be in danger if the food supply is endangered. Economic resilience is a prerequisite for national resilience [1]. Food and energy security, financial tenacity, and physical endurance make up the foundations of economic resilience [2]. Food security is the most significant pillar of the economic resilience framework. Food availability, access, stabilization, and distribution are the four pillars of food security [3]. Therefore, governments devote particular attention to securing the long-term growth of the nation’s food security through a related fiscal policy, providing funds, subsidies, and other means of support to domestic farmers and rural people. Businesses engaged in agriculture require some money as well as modern, technologically updated farm equipment. Although small businesses play a significant role in the development of many developing nations, they are always constrained by a lack of financial resources to meet a variety of operational and investment needs [4]. Lader [5] claimed that one of the major issues small businesses face is access to capital. Although in most of the developed countries and many developing markets, agribusiness subsidies have accelerated agricultural output, productivity, and output [6], rural residents still have restricted access to credit, particularly micro-credit (as demonstrated by Etonihu et al. [7] for African countries, Gao et al. [8] for China, and Sikandar et al. [9] for Pakistan).

According to Akram et al. [10], Constantin et al. [11], and Panait et al. [12], the availability of formal credit in rural areas is deteriorated by stringent guidelines and procedures, a lack of collateral, and high-interest rates. Many scholars also named the lack of financial literacy among the major barriers to obtaining funds for farmers [9,13]. According to Robb and James [14], having sufficient financial literacy would promote a favorable effect on financial behavior. Klapper et al. [15] evidenced that an improvement in financial literacy could substantially improve access to credit and savings in low-income environments. Specifically in Pakistan, a lack of formal loan availability results from several factors, including a low level of income in rural areas, complex bank operations, a lack of education in the spheres of finance and banking, high administrative costs, and difficulty in accessing the bank locations. The general level of Pakistanis farmers’ knowledge, understanding, and awareness of financial institutions, their related products, and services are quite low [15]. These circumstances contributed to the low adoption of financial services and products. In 2013, only 21.8% of respondents reported sufficient financial literacy. The government of Pakistan (GoP) has launched the interest subsidy program in an effort to alleviate the financial shortages faced by small and medium-sized businesses related to agriculture. The interest subsidy is the interest that the government pays at the current rate of interest for the applicable participants. This credit is given to those who lack access to capital in banking yet have viable businesses. The Food Security and Agriculture Credit’s (FSAC) interest subsidy is one of the credit program’s schemes started by the GoP to facilitate farmers with low income.

A sort of investment credit and working capital, known as FSAC, is provided to aid in the operation of the food stability program and the program for the development of food crops by the Ministry of National Food Security and Research (MNFSR) [16,17,18,19]. The primary targets of FSAC are (a) farmers of food crops like rice, corn, soybeans, cassava, sweet potatoes, and sorghum; (b) farmers of horticulture like onions, chilies, potatoes, ginger, and bananas; (c) farmers of sugarcane cultivation; (d) farmers of dairy products like dairy cattle, cattle breeding, race cock, domestic chickens, ducks, and quail; and (e) cooperatives for the purchase of grains, corn, and soybeans.

For the purpose of distributing FSAC to eligible farms, the GoP collaborates with local and international banks. It focuses on investing in improving infrastructure for farming communities. In this context, the Agriculture Credit Advisory Committee (ACAC) has set indicative agricultural credit disbursement targets of PKR 700 billion for the financial year 2016–2017 to 52 participating institutions. The institutions include twenty commercial banks, two specialized banks, four Islamic banks, and 26 microfinance institutions. Five major banks as a group have disbursed PKR 236.6 billion, or 69.6% of their annual target. Zarai Taraqiati Bank Limited (ZTBL) disbursed PKR 57.5 billion or 56.1% of its target [19,20,21]. At one of its sessions, ACAC noted that agricultural credit provided by Nationalized Commercial Banks (NCBs) was being used for non-agricultural purposes and that the situation regarding loan recovery was not sufficient. The Committee also believed that the growth of supervised credit schemes was the key to finding a solution to the issue. The Pakistan Banking Council would create a model scheme that NCBs would use going forward to distribute agricultural loans. A draught model scheme for the agricultural loan was created by the Pakistan Banking Council in cooperation with NCBs and several agricultural credit specialists. By 31 December 2021, ZTBL provided over PKR 40.7 billion to farmers in terms of loans, cash credits, running finance, etc., in the non-performing category. This amount is just 30–32% of the total budget allocated to ZTBL by the State bank of Pakistan (SBP). Because of the limited absorption, FSAC supported by ZTBL and MNFSR is not easily accessible to farmers [22,23,24]. Based on the foregoing context, this study aims at assessing financial literacy among Pakistani farmers, revealing the factors that affect financial literacy, and examining the impact of financial literacy, interest subsidy, and other variables on rice farmers’ access to FSAC.

The main purpose of this research is to explore the factors influencing farmers’ financial literacy index status and their access to credit for two regions of Pakistan, i.e., Central Punjab and Khyber Pakhtunkhwa. As the GoP aims to reduce poverty by providing facilities for affordable access to credit for farmers, the study uses multiple regressions and logistic analysis to analyze the variables impacting farmers’ accessibility to the Food Security and Agricultural Credit program.

1.2. The Role of the Agricultural Sector in Pakistan

The Pakistani economy has been growing steadily over the last 60 years at an average annual rate of 4.9%. Within only a decade, Pakistan’s GDP nearly doubled from $137 billion in 2006 to over $270 billion in 2015. The country’s growth, however, has been inconsistent, with many cycles of booms and busts. Pakistan is considered an emerging market economy, but it lags behind in many development parameters. Agriculture is the second largest sector in Pakistan (approximately 25% of the GDP [23] and about 42% of the labor, mainly women [24]). The sector generates over 75% of export revenue through agri-based textiles (cotton) and agri-food products [25]. Pakistan is among the world’s largest exporters of textiles and rice. It imports significant quantities of palm oil used in cooking. Despite its critical importance to food security, livelihoods, economic growth, and export revenues, agricultural productivity remains low, with significant yield gaps compared to global averages in key crops like wheat, rice, and sugarcane. The average farm size in Pakistan is 2.6 ha, with approximately 43% of the farmers categorized as smallholders with holdings of less than one ha, while only 22% of farmers own more than 3 ha of land [26]. In 2016, for the first time since 2000, the sector experienced a decline of 0.2%, primarily due to the impact of extreme events on key crops, a lack of access to key inputs, and a global downturn in commodity prices [24]. Critical investments in improved seeds, farming technology and techniques, and water infrastructure are needed to tackle the emerging challenges to the sector’s development, especially in the context of declining water availability and climate change impacts.

Pakistan is the sixth most populous country in the world, with an estimated population of 190 million [23]. Over 60% of the population still resides in rural areas despite rapid urbanization in the past few decades. Applying pro-poor strategies—including a focus on the development of smallholder farmers—the country has made significant progress in reducing the national poverty incidence, from 64.0% in 2001 to 29.5% in 2013. However, about 40% of the population is still deprived of some of the basic necessities, a phenomenon known as multidimensional poverty [27]. This is predominantly a rural phenomenon, with 55% of the rural population affected by multidimensional poverty. Agriculture provides employment for roughly 25 million people in Pakistan. The agricultural sector is the major source of income for 34% and 74% of economically active men and women, respectively. Yet women have limited access and control over productive resources (e.g., land, irrigation infrastructure, and agricultural inputs), low awareness of improved technologies and skills for value addition and marketing, and limited access to extension and financial services. Their role in the household and in daily agricultural activities, however, varies across regions according to local customs and traditions [28].

Pakistan is a natural resource-based economy, with almost half of its total land area (36 million ha) dedicated to agriculture [29]. Approximately 84% of the land is classified as arable and 14% as permanent meadows or pastures. The country’s forested area represents only 2% of the total land—compared to the world average of over 30% [23]—and is declining at a rate of 0.2–0.5% per year [30]. Deforestation—driven by urbanization, a rural reliance on fuelwood, and poor land planning—has been linked with socioeconomic vulnerability and a lack of effective policy and monitoring mechanisms to protect forests. The area of land under production has remained relatively stable over the last four decades at approximately 36 million ha. Since most of the arable land in Pakistan is already cultivated, productivity gains in the country are achieved through increased cropping intensity and the higher use of fertilizers. The average annual fertilizer use in Pakistan across all cropping systems is estimated at 159.9 kg/ha.

1.3. Challenges for the Agricultural Sector

Despite the importance of agriculture to the economy and people, the sector faces a number of challenges, such as rising population, spurring urbanization, scarcity of water resources, and gender disparity. It is anticipated that Pakistan’s population will reach 244 million by 2030 and 300 million by 2050, having more than doubled during the preceding two decades at a pace of almost 2% per year [31]. Life expectancy is projected to rise from 66 to 71 years by 2050. Such exponential expansion will significantly strain the agricultural sector (which is already stretched thin and vulnerable) and increase food consumption. In Pakistan, the current per capita calorie availability is 2432 kcal/day. If the food supply does not keep up with predicted population growth, this number is likely to decrease. Rapid urbanization and industrial growth are projected to go hand in hand with population growth in Pakistan. Agricultural areas located close to industrial and urban development sites are exposed to dangerous chemicals, which have an impact on both the quality and safety of food items. Heavy metal-containing wastewater is frequently used to irrigate fields in peri-urban regions, where it may be absorbed by vegetables and other cash crops and enter the food chain. As evidenced by many studies, urban agriculture has a significant impact on waterborne illnesses and human health, particularly in developing economies.

Additional dangers to Pakistan’s food security include a lack of readily available water, deteriorating soil, and a diet that is more and more animal-based. These dangers are multiplied by shifting climatic conditions, such as rainfall, temperature, and humidity, which can alter natural resource availability and quality and make a sector more vulnerable. The majority of the country’s land is categorized as arid or semi-arid. About 20% of this area receives less than 120 mm of rainfall each year, whereas three-quarters of the nation receives less than 250 mm [32]. Therefore, rainfall is typically insufficient for sustaining pastures, cultivating agricultural products, and raising fruit trees. Due to poor weather, almost 8 million hectares of land in Pakistan are idle and underutilized. In Pakistan, additional water is needed for agricultural output to be successful, either by irrigation or water harvesting. Water resource management in Pakistan is seriously threatened by a rise in the demand for water for agriculture. Crop production can be directly impacted by droughts, floods, warming, and variations in precipitation. Only a few crops, including wheat and barley, are more resilient to climate change. For instance, a study on wheat production in the Swat and Chitral districts’ mountainous regions advises that short-duration, high-yielding varieties that can resist climatic anomalies be introduced there [33].

Meanwhile, the rural population, which serves as the foundation of the agricultural industry, is primarily made up of small-scale, underprivileged farmers who do not have access to contemporary farming techniques, equipment, fertilizer inputs, or crops that can withstand adverse weather conditions. Farmers are further prevented from implementing better practices by the high cost of seeds and a lack of government support. Rural areas lack well-constructed roads, storage and transportation facilities, electricity, and health and educational services. Each of these attributes is now insufficient to satisfy the needs of an expanding agricultural industry. Small farm size and ongoing poverty constrain farmers’ capacity to take risks and diversify their incomes, and their access to credit markets is further restricted by their low asset ownership and lack of collateral. The agricultural industry in Pakistan also exhibits prejudice and gender disparity. Women are less likely to possess income-generating assets like land, machinery, or equipment than men are, and they do not have equal influence in terms of making financial or economic decisions, despite the fact that 74% of employed women depend on agriculture, compared to 34% of employed males. Additional difficulties for women in agriculture are brought on by their limited access to cutting-edge farming methods and technologies, a lack of effective extension services, and high rates of illiteracy among rural women [34].

In this paper, the authors explore the effect of different socioeconomic, technical, and institutional factors on farmers’ access to credit and their FLI (financial literacy index) status for two different regions of Pakistan quantitatively. This information will ultimately help form policies that aim to reduce rural poverty by facilitating farmers’ easy and affordable access to credit. Specifically, this study focuses on the following objectives: (1) to determine the factors that influence farmers’ access to agricultural credit; (2) to use multiple regressions and logistic analysis to analyze the variables impacting farmers’ financial literacy; (3) analyze the variables which can have an impact on the farmers’ accessibility to FSAC.

The structure of the paper is as follows: Section 2 discusses the related research work related to subsidy and micro-credit provided by GoP, agricultural credit in Pakistan, and farmers’ access to credit sources. The system modeling is presented in Section 3, which includes the area, time, and nature of data related to this study. The data analysis method used in this research work is also discussed in this section. In Section 4, performance evaluation in terms of FLI and variables impacting credit accessibility results are demonstrated using financial behavior indicators and logistic regression modeling. Section 5 summarizes the authors’ recommendations in light of previous studies both on national and international levels. Finally, Section 6 concludes the paper.

2. Related Research Work

2.1. Subsidy

One of the fiscal policy tools available to any government to ensure access equitable to the economy and development is subsidies. The purpose of subsidies is to adjust for flaws in the market. The fundamental objective of Pakistan’s subsidy policy is to ensure that the poor have access to public services and that there is social and economic advancement. The goal of the subsidy is to increase domestic market share in addition to supporting domestic manufacturing. According to Milton and Orley [35], a government subsidy is a payment made to a company or household in order to accomplish specific goals that allow them to manufacture or consume the good in greater quantities or at a lower price. Subsidies have an economic goal of lowering prices or raising output. Todaro and Stephen [34] noted that a subsidy (sometimes known as a subvention) is a sort of financial assistance given to an enterprise or economic sector. The government provides some subsidies to producers and distributors in some industries to either encourage those companies’ efforts to hire additional workers or to prevent those industries from failing or from seeing their product prices rise [12]. A subsidy can also be considered as a budget allocation given to businesses or organizations that create, market, and sell products and services that meet the needs of many people while also allowing them to pay the asking price.

2.2. Microcredit

Microcredit has always been an integral component of agriculture, particularly for smallholder farmers. Farmers need loans to operate their farms, both for investments in capital and technology to increase production quantity and productivity. Farmers employ their own funds or obtain credit from a microfinance firm to suit their needs. A microfinance organization is the same as giving small loans to those with low incomes so they can start their own businesses. Wadud [36] found that in Bangladesh, farmers who received loans were able to boost their revenue by 9.46% more than those who did not. According to Quach et al. [37], microcredit for a household in Vietnam increased both food and non-food consumption per capita and had a favorable and significant influence on welfare. In the case of Pakistan, Montgomery [38] demonstrated that microcredit had a favorable effect on the economy, society, and income, especially for low-income families. The effects of microcredit can be assessed from two angles: whom do they reach, and how do they affect individual and household welfare? According to Karlan and Goldberg [39], evaluating an impact requires not just determining if the program has benefited the credit borrower in the present but also taking the borrower’s future into account.

A small-scale business generally obtains a higher return on investment than a larger-scale business because it has less capital [12,40]. This statement is founded on the law of declining marginal return to capital. A business unit’s marginal output declines as its capital level rises. According to Ibrahim and Bauer [41], microcredit had a considerable influence on the effect of access to microcredit on farmer income. Those who were successful in obtaining microcredit had better income and profits than those who were unsuccessful. Therefore, farmers’ income increased in direct proportion to the amount of credit accessed by farmers. This finding is supported by Angioloni et al. [42], who found that while increased credit had a negative impact on food consumption in Kyrgyzstan, it affected households’ ability to purchase new homes, lots, and businesses. In Morocco, microcredit gave a rise in household income and the demand for microfinance, expanded local businesses, and contributed to mitigating poverty [43].

Dewi et al. [44] conducted research on how FSAC helped rice farmers in the Kampar Regency of Riau Province increase their yields and profits. It was found that 46.98% of farms, 29.43% of consumers, and 23.57% of other enterprises adopted FSAC. Farmers used FSAC to buy and supply inputs, including seeds, fertilizer, pesticides, and agricultural equipment. The 18.93% increase in rice yield due to FSAC had a major impact on farm profit. In the Pati Regency of Central Java Province, Farida et al. [45] conducted an analysis of the performance of micro business credit and its effect on the income of the micro business. The study showed that FSAC had an impact on rising profit and total income, falling food expenditure share, growing labor force, and growing asset ownership. In a cow farm in Central Java, Dahri et al. [46] conducted an analysis of the program’s accessibility, economic impact, and degree of loan repayment. The majority of cattle farmers utilized the FSAC for cattle farm operations, specifically to purchase feeder cattle or pregnant cattle, feed, medicine, and cage repairs. In the case of an organic rice farm in Bogor Regency, Wati et al. [47] revealed that microcredit had a favorable effect on labor, input usage, and organic rice production, all of which increased. Arief and Rosmiati [48] discovered that the restriction of access to the source of credit had a significant and detrimental impact on a number of factors, including the adoption of technology, agricultural output, food safety, nutrient, health, and overall household welfare. A family that was able to access a source of credit was successful in boosting its welfare, productivity, and usage of labor from outside the family, as well as consumption and revenue [8].

2.3. Agricultural Credit in Pakistan

The agricultural sector is one of the key drivers of economic development in Pakistan. Its share in Pakistan’s GDP is 18.9%. It employs 42.3% of the nation’s laborers [22]. Pakistan, on the other hand, is the sixth-most populous nation in the world, and its population is growing by 2.4% annually [49]. Every aspect of life revolves around money. Thus farmers require credit in order to buy new technological tools, seeds, fertilizers, input materials, and land for agricultural development. Farmers can obtain loans from two sources: financial institutions and their peers who have money [50]. Farmers in underdeveloped nations like Pakistan rarely have savings; thus, institutional and informal lenders, including commercial banks, cooperatives, and commercial agents, as well as specialist financial institutions like ZTBL, serve as the primary sources of credit for Pakistani farmers. The Pakistani government built a vast network of agricultural credits after realizing the critical need of the agricultural sector. Numerous micro-credit institutions, small businesses, and the country’s 26 commercial banks, with a network of more than 3900 branches, all provide financial services to farmers across the nation [50].

According to the Pakistan Bureau of Statistics [51], from 1981–2021, the total amount of credit distributed by Pakistan’s commercial banks increased from PKR 40.42 billion to PKR 51.35 billion. Commercial banks dispersed PKR 326 billion as an agriculture loan, while the State Bank of Pakistan established an annual outstanding inductive objective and farm loans to climb from PKR 28.1 billion to PKR 312.7 billion. The Pakistani state bank established a goal to distribute PKR 1.35 trillion in the fiscal year 2019–20, which is more than the record-high farm credit of 1 trillion it recorded in the fiscal year 2018–19 [52].

In addition, the government has suggested that loan insurance programs be made available for small farmers who have lost money due to crop damage. In this context, the 2019–20 budgets include a proposal for PKR 2.5 billion [53]. Pakistani farmers continue to face numerous issues with agricultural financing, notwithstanding numerous increases and sources. The majority of farmers live in rural areas, where they are unable to get credit since they are far from cities and the locations of credit-granting institutions [54]. The big farmers have access to more financial options than the tiny, illiterate farmers since they have access to larger tracts of agricultural land and education [55]. For improved agricultural advancements in Pakistan, specialized banks like ZTBL and other commercial banks must therefore enhance the loan facility policies.

2.4. Farmers’ Access to Credit Sources

Recent studies have emphasized farmers’ needs for funds, access to formal credit sources, investment in agricultural inputs, and long-term welfare of farmers and rural dwellers by tracking changes in farm productivity, agricultural output, and household consumption in rural areas. In the case of Sindh province in Pakistan, Chandio and Jiang [56] found the availability of official agricultural credit to be comparatively low. This was partly because of the province’s remoteness from formal credit sources, challenging lending requirements, and high-interest rates. Furthermore, as evidenced by Amanullah et al. [57], Chandio et al. [58], Nouman et al. [59], and Rasheed et al. [60], farmers’ access to credit is significantly influenced by a number of socioeconomic characteristics, including gender, age, household size, educational attainment, farming experience, farm size, and income. Furthermore, Karaivanov and Kessler [61] revealed that the majority of farmers largely relied on unofficial loan sources due to their limited access to formal finance, which had a negative impact on their investments in agricultural inputs. Saleem and Jan [62], Rehman et al. [63], and Chandio et al. [55], among others, examined the influence of credit on agricultural risk management, farm productivity, and agricultural output and found all three components to be positively and significantly impacted by each other. According to Amanullah et al. [57], low access to credit has a detrimental impact on farmers’ well-being and income, while a lack of proper access to credit facilities renders farmers unable to obtain prospective farming earnings.

According to Hussain and Thapa [64], the size of landholding and the availability of agricultural finance are interrelated. Therefore, the size of the farm is a crucial consideration for classifying farmers into large, medium, and small groups. Moreover, classifications of farmers vary from country to country and from part to section [64]. Akram et al. [10], Amjad and Hasnu [65], and Dzadze et al. [66] showed conclusively that having substantial landholding increased one’s access to agricultural loans.

According to Saqib et al. [13], farmers’ ages are inversely correlated with their ability to acquire official agricultural loans in Pakistan. In this way, farming experience has no particularly significant impact. In low-income nations, access to credit is especially important for addressing the issues of food security, socioeconomic welfare, and poverty among agricultural communities [67,68]. Since it influences farmers’ ability to adopt new agronomic technologies, access to credit is a crucial component of farm management to increase agricultural output. The agricultural industry employs 42.3% of the workforce, contributes around 19% to the national economy, and provides the raw materials for a number of value-added industries [19,20]. The nation requires a higher degree of production for grain crops, fruits, vegetables, dairy products, and meat due to an exponentially rising population. To increase the productivity of the agriculture industry, more focus is needed. Improving financial support for farmers in the form of agricultural finance is a crucial strategy in this respect.

The links between better agricultural technologies and farmers’ sources of credit in rain-fed areas and their socioeconomic effects have not yet been quantified. The goal of the current study is to determine the effects of farmers’ socioeconomic features on their access to and choice of financing sources, as well as the relationship between these factors and the adoption of technology in Pakistan’s rain-fed agriculture. Planning and implementing agricultural finance-related policies and program is crucial for addressing the difficulties of food security in developing nations. This includes understanding the factors that affect farmers’ adoption of contemporary technology and their choice of financing sources. Table 1 depicts the previous empirical research and their outcomes for both national and international levels.

Table 1.

Previous empirical research and their outcomes for both national and international levels.

Table 1.

Previous empirical research and their outcomes for both national and international levels.

| Source | Topic | Outcome | Type | Location |

|---|---|---|---|---|

| Wadud [36] | Impact of microcredit on agricultural farm performance and food security in Bangladesh | Bangladeshi farmers boost their revenue by 9.46%. | International | Bangladesh |

| Quach et al. [37] | Access to credit and household poverty reduction in rural Vietnam | Increased food and non-food consumption per capita, significant influence on welfare. | International | Vietnam |

| Ibrahim and Bauer [41] | Access to microcredit and its impact on farm profit among rural farmers in dryland of Sudan | Farmers’ income increased in direct proportion to the amount of credit accessed by farmers. | International | Sudan |

| Ankrah Twumasi et al. [69] | Financial literacy and its determinants: The case of rural farm households in Ghana | Respondents’ socioeconomic and demographic characteristics, such as gender, income, age, and education, significantly affect financial literacy. | International | Ghana |

| Crepon et al. [43] | Impact of microcredit in rural areas of Morocco: evidence from a randomized evaluation | Microcredit gave a rise in households’ income, expanded local businesses, mitigated poverty. | International | Morocco |

| Dewi et al. [44] | Roles of food security and energy credit in increasing rice production and profits in Kampar Regency, Riau Province | 46.98% of farms, 29.43% of consumers, and 23.57% of other enterprises adopted FSAC. | International | Indonesia |

| Farida et al. [45] | An impact estimator using propensity score matching: People’s business credit program to micro-entrepreneurs in Indonesia | FSAC had an impact on rising profit and total income, falling food expenditure share, growing labor force, and growing asset ownership. | International | Indonesia |

| Dahri et al. [46] | Determinants of the KKPE credit program repayment of cattle farmers in Central Java, Indonesia | Majority of cattle farmers utilized the FSAC for cattle farm operations, specifically to purchase feeder cattle or pregnant cattle, feed, medicine, and cage repairs. | International | Indonesia |

| Wati et al. [47] | Microcredit access and impact on production and revenue of organic rice farming in Bogor regency | Microcredit had a favorable effect on labor, input usage, and organic rice production. | International | Indonesia |

| Zakic et al. [70] | Significance of financial literacy for the agricultural holdings in Serbia | Continuous education programs through agricultural extension services are critically important for upgrading financial literacy skills among farmers. | International | Serbia |

| Ravikumar et al. [71] | Assessment of farm financial literacy among jasmine growers in Tamilnadu, India | Financial literacy in rural areas is significantly affected by such variables as age, education, experience, farm income, years of relationship with the bank, size of landholding, and frequency of bank visits. | International | India |

| Chandio and Jiang [56] | Determinants of credit constraints: Evidence from Sindh, Pakistan | Availability of agricultural credit is comparatively low due to Sindh province’s remoteness from formal credit sources, challenging lending requirements, and high-interest rates. | National | Sindh, Pakistan |

| Amanullah et al. [57] | Credit constraints and rural farmers’ welfare in an agrarian economy | Low access to credit has a detrimental impact on farmers’ well-being and income, while a lack of proper access to credit facilities renders farmers unable to obtain prospective farming earnings. | National | KP, Pakistan |

| Hussain and Thapa [64] | Smallholders’ access to agricultural credit in Pakistan | Size of landholding and the availability of agricultural finance are interrelated. Therefore, the size of the farm is a crucial consideration for classifying farmers into large, medium, and small groups. | National | Sindh & Punjab, Pakistan |

| Saqib et al. [13] | Factors influencing farmers’ adoption of agricultural credit as a risk management strategy: The case of Pakistan. | Farmers’ ages are inversely correlated with their ability to acquire official agricultural loans in Pakistan. | National | Pakistan |

| Ullah et al. [72] | Factors determining farmers’ access to and sources of credit: Evidence from the rain-fed zone of Pakistan | The results indicate a moderate positive association between farmers’ access to agricultural credit and their adoption of improved agricultural technologies. The binary logit model’s results indicate that farmers with a large-sized farm, high farm income, better access to information, and large physical asset ownership showed a positive influence on credit access. | National | KP, Pakistan |

Source: authors’ development.

3. Materials and Methods

3.1. Area and Time

The present study is based on primary data collected from the Lakki Marwat and Karak districts of Khyber Pakhtunkhwa province and the Multan district of South Punjab. The area of cultivated land in the Lakki Marwat and Karak districts is 116,900 ha and 75,642 ha, respectively. The majority of the cultivated land is under rain-fed conditions, with sandy soil types and relatively hot weather. For both areas, agricultural production is the primary economic activity, with wheat and gram being the major crops. In Multan, the study covered five settlements (Loother, Qadir-purrawan, Lutafabad, Jodhpur, and Bua-pur), where the concentration of wheat and cotton growers is the highest.

3.2. Data

Well-structured questionnaires have been organized for collecting the primary data on the socioeconomic characteristics of the respondents, such as age, formal education, farming experience, credit availability, extension services, farm size, off-farm income, farm revenue per acre, own land, distance to the central city, availing FSAC or not. Secondary data was also collected from different official websites, including MNFSR, Pakistan bureau of statistics, Ministry of Agriculture and Livestock (MoAL), SBP, and scientific journals, as well as documents or publications from relevant institutions. This research has been designed specially to focus on the financial literacy of farmers and financial actors with reference to rural area farmers of Pakistan.

3.3. Sampling Method

Samples were collected using the multistage purposive sampling method. The first stage is taking Lakkimarwat and Karak as rain-fed agricultural regions and Multan as a dry region of Central Punjab as suitable research locations. The second stage is determining the three elected districts. The third stage is selecting five villages. The fourth stage is selecting 250 respondents within farmer groups. The questionnaires distributed to respondents amounted to 300 pieces, with details of 200 pieces for the respondent treatment and 100 pieces for the respondent control. Regarding agricultural technology adoption, farmers were specifically asked about the technology they had adopted during the previous two years. Any farmer who adopted at least one form of technology (from those recommended by the local agriculture extension department) was considered an adopter. The total sample size for the study was calculated using Yamane’s formula [73], which depends on the population size and the level of precision that has been widely used by researchers for data collection.

3.4. Data Analysis Method

Using multiple regression analysis, we should pertinently mention here that the financial literacy index is set as a dependent variable that depends on multiple independent variables such as gender, age, education duration, main occupation, distance to the capital regency, annual income, bank account ownership, and participation in financial education. The equation model inspired by the probit model mentioned [58,63] is as follows:

where = financial literacy index for which the score varies between 0 and 100; = intercept (constant); = coefficient regression of each variable; = gender (male = 1, female = 0); = age; = period of education (elementary = 6, junior high = 9, senior high = 12, college level > 12); = occupation (farmer = 1, non-farmer = 0); = distance to the nearby city, km; = annual income; = bank account ownership (owner = 1, others = 0); = financial education experience (experience = 1, no experience = 0).

The authors studied the effects of independent variables on FLI based on the results of the regression analysis. The second research aim was reached by using logistic regression analysis. The accessibility of FSAC was set as a dependent variable, while the independent ones included age, education duration, farm income, cultivated area, collateral, interest rate, FLI, farm group legal status, credit accessibility experience, and loan amount. The variables used in the regression refer to economic theories and previous studies related to microcredit accessibility [48,50]. The equation model is as follows:

where = subsidized microcredit accessibility (accessed microcredit = 1, others = 0); = intercept (constant); = coefficient regression of each variable; = age; = period of education (elementary = 6, junior high = 9, senior high = 12, college level > 12); = farmers income per season in PKR, million; = cultivated area, hectares; = collateral (hand over collateral = 1, other = 0); = interest rate on credit in terms of percent per annum; = financial literacy index for which score varies between 0 and 100; = legal status of farmer group (certificate holder = 1, other = 0); = credit accesses experience; = loan amount in PKR, million.

4. Results and Discussion

4.1. Financial Literacy Analysis

The variety of financial products available today reflects the financial sector’s tremendous expansion. To access contemporary financial goods, the general public should be sufficiently financially literate. Financial conduct will improve as a result of adequate public financial literacy, leading to a prosperous existence. According to Lusardi [74], financial education promotes more savings and enhances the standard of financial decision-making. People who are sufficiently financially literate on a micro level are more likely to access loans from regulated financial institutions, save more money, and manage risk better.

A country’s gross domestic product rises from the financial sector at the macro level if community financial behavior is acceptable. As evidenced by Garman et al. [75], 15% of workers in the USA exhibit poor financial practices. This circumstance demonstrated that rising manufacturing costs would result from declining productivity. In this study, financial literacy is assessed using an index value derived from questionnaires that have been methodically structured and adjusted for farmers’ circumstances in Pakistan. Thirty-one total questions covering personal money, savings and loans, insurance, and investments are included in our survey conducted in different regions of Pakistan.

4.2. Financial Literacy Characteristics of Respondents

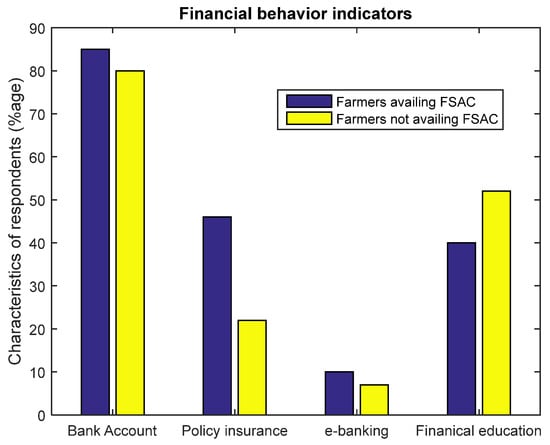

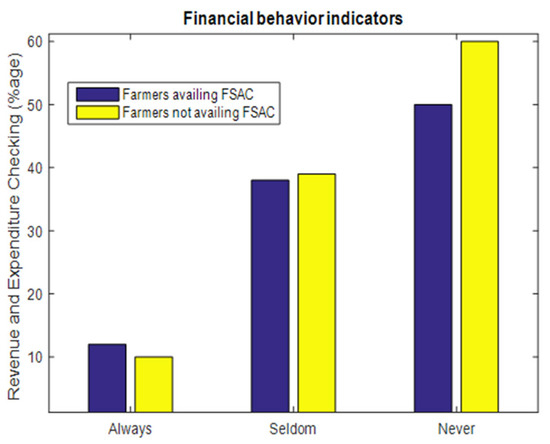

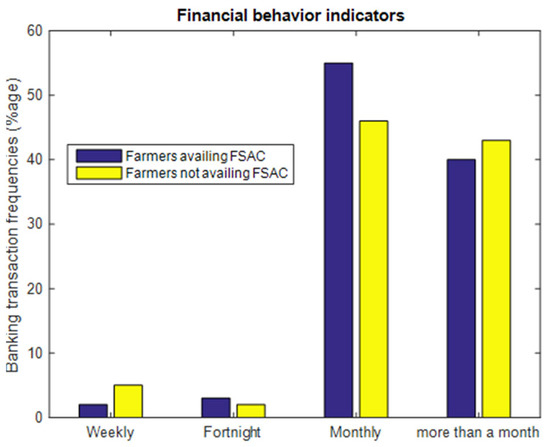

Good financial behavior is encouraged by adequate financial literacy. The financial behavior parameters include having a bank account, having insurance, using an electronic banking facility, having received financial education, being experienced in keeping track of income and expenses, and frequently using banking facilities. Figure 1, Figure 2 and Figure 3 provide information on the respondent’s financial behavior indicators.

Figure 1.

Financial behavior indicators in terms of bank account, policy insurance, e-banking, and financial education. Source: authors’ development.

Figure 2.

Financial behavior indicators in terms of revenue and expenditure checking routine. Source: authors’ development.

Figure 3.

Financial behavior indicators in terms of banking transaction frequencies. Source: authors’ development.

In the figures above, the data was segmented into two parts: farmers availing of FSAC services and those not availing of them. In the former group, 79% of respondents reported having a bank account. Respondents who own policies of insurance make up 22%, those who utilize electronic banking services make up 8%, and those with financial education experiences make up 51%. In terms of revenue and expenditure checking perspective, only 4% of respondents make a weekly transaction using banking services, while 9% of respondents actively track their income and expenses. Similarly, among farmers availing of FSAC, 86% of the respondents had bank accounts, 46% had insurance, 9% used electronic banking, 40% had experience with financial education, 9% always kept track of their income and outgoings, and 2% conducted banking transactions once a week. Among the respondents who did not avail of FSAC, 39% seldom check their revenues and expenditure details, and 46% conducted banking transactions once a month, whereas, for farmers availing of FSAC, 37% seldom check their revenues and expenditure details and 54% farmers perform banking transaction once a month.

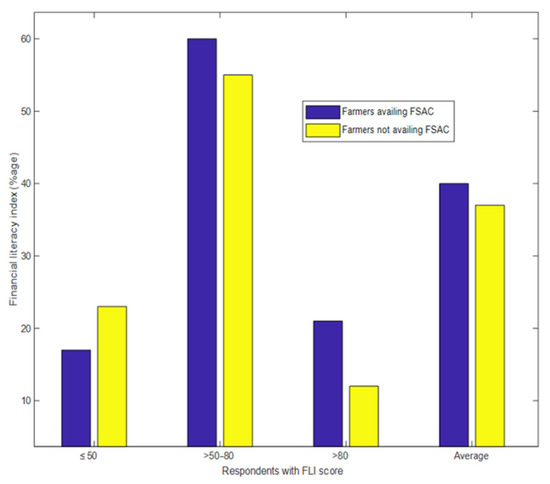

According to Servon and Kaetsner [76], financial and technology literacy are crucial for reducing poverty, and it is evident that respondents who availed of FSAC exhibited better financial behavior than respondents who did not. Because the introduction of electronic banking makes financial literacy instruction more effective, it will boost the degree of financial literacy. In this study, the number of accurate responses was divided by the total number of questions to determine the FLI. The three categories on the FLI are as follows. Low financial literacy is defined as having an index value of less than 50; moderate financial literacy is defined as having an index value between 50 and 80; and high financial literacy is defined as having an index value of more than 80.

The overall respondents’ average FLI for farmers availing of FSAC is 39.9, and for farmers not availing of FSAC is 38.3 (Figure 4). The index measuring financial literacy with reference to the low financial literacy group is 17% for farmers availing of FSAC and 23% for farmers not availing of FSAC. Similarly, for the moderate financial literacy group, 59% of the farmers fall into the category of respondents availing of FSAC and 53% of farmers not availing of FSAC. For the high financial literacy group, the FLI of respondents availing of FSAC is 20%, and the FLI of respondents not availing is 11.3%.

Figure 4.

FLI with respect to respondents’ FLI score. Source: authors’ development.

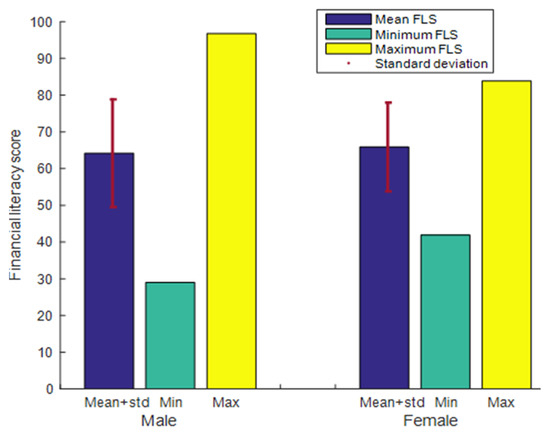

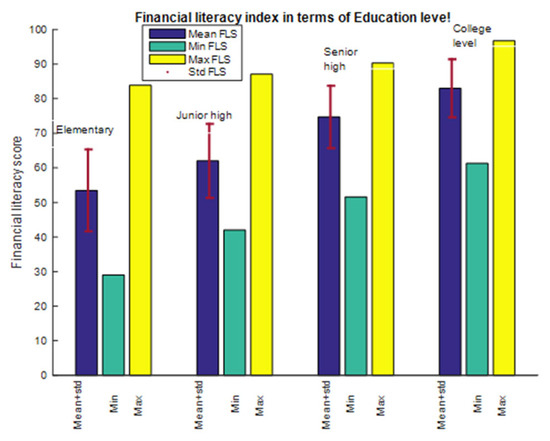

Comparing the average FLI of male and female respondents, the mean FLI of female respondents is marginally higher than that of male respondents (Figure 5). The mean FLI was significantly influenced by the respondents’ educational background (Figure 6). The mean FLI of the respondents increases with increasing educational achievement. For elementary school, junior high, senior high, and college, the mean FLI is 53.5, 62.05, 73.7, and 80.98, respectively.

Figure 5.

FLI in terms of gender. Source: authors’ development.

Figure 6.

FLI in terms of education level. Source: authors’ development.

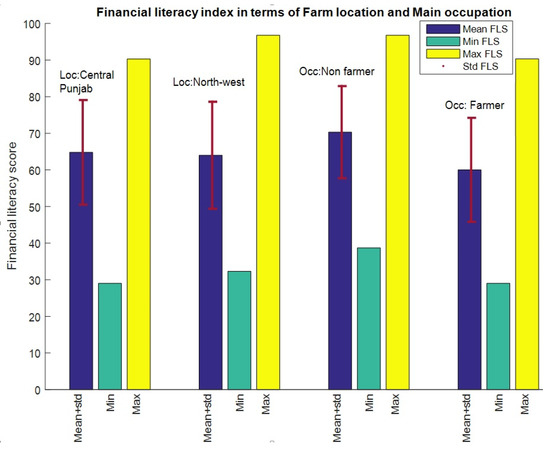

In Central Punjab, respondents’ FLI is measured on average at 65.2%, while in the northwestern Khyber Pakhtunkhwa province, it is measured on average at 64.3%. Apparently, there is no significant difference in the average value of FLI based on the farming locations. Moreover, as shown in Figure 7, we have also included the occupation of the respondents, i.e., whether they are full-time farmers or they are involved in other jobs, such as carpenters, construction workers, traders, public transportation drivers, taxi drivers, manufacturing employees, breeders, etc. Full-time farmers’ average FLI is almost 60%, and for non-farmers, it is around 69.4% based on the criteria that if respondents’ yearly income from agricultural operations accounts for more than 50% of their total income, then farming is their primary occupation. If their annual income is made up of more than 50% of other sources, then farming is not their primary occupation.

Figure 7.

FLI in terms of farm location and main occupation. Source: authors’ development.

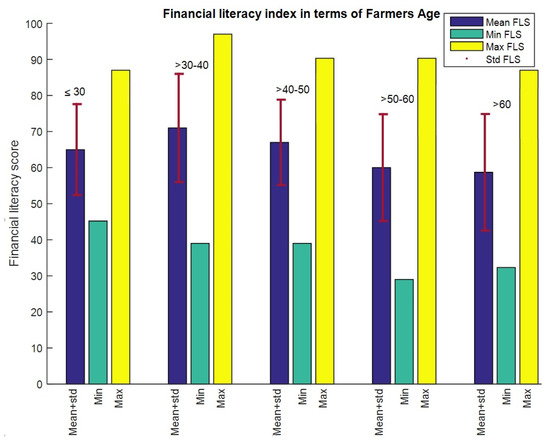

The FLI has been impacted by the age variable as well. Ages 31 to 40 had the greatest FLI among respondents (Figure 8). The average FLI among respondents under 30 years old is 63.97. The average FLI among respondents who are between the ages of 41 and 50 is 65.64. With respondents ranging in age from 51 to 60, the average FLI is 58.89. The lowest FLI is for those who are above 60.

Figure 8.

FLI in terms of farmers’ age. Source: authors’ development.

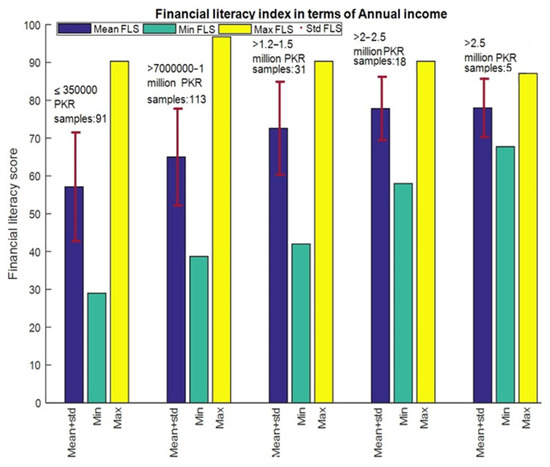

The annual income and the FLI are correlated (Figure 9). The FLI will rise in direct proportion to annual income. The respondents with the lowest FLI score of 57.12 were those with annual incomes under PKR 0.35 million. The average FLI for respondents with incomes within PKR 0.7–1.0 million is 64.00, whereas, for those with incomes within PKR 1.2–1.5 million, it is 72.33; for those with incomes within PKR 2.0–2.5 million, it is 76.98. Respondents with annual incomes over PKR 2.5 million have the highest FLI, which is 78.26.

Figure 9.

FLI in terms of annual income. Source: authors’ development.

4.3. Variables Affecting Financial Literacy

We applied the linear regression model to identify the factors that affected financial literacy. Two hundred sixty samples were used as observations in the regression, the number of variables evaluated was eight, and the number of observations minus the number of variables was 252. It is highly likely that independent factors have an impact on the FLI concurrently and considerably. The value of FLI was 52.8% affected by independent variables which exist in the regression model, while the remaining 47.2% percent value of FLI was influenced by additional variables that are not part of the regression model. The discrepancy between values (sample and population values) predicted by a model or estimator and the values actually observed is typically measured using the root mean square error (RMSE). If the RMSE is less than the dependent variable’s standard deviation, the regression model is considered to be accurate. The RMSE value and the standard deviation of financial literacy are 9.9625 and 14.4709, respectively. As a result, the model is deemed to be a good and fit model to predict the FLI. Furthermore, the t-value demonstrates how each independent variable has a limited impact on the dependent variable. The results of the regression analysis indicate that four variables, i.e., ED, D, AI, and FEEx, significantly affect the FLI at the significance level of 1%. Additionally, the FLI measure is highly influenced by variables A and Acc at a significance level of 10%. However, FLI is not greatly impacted by variables G and Occ.

Age is a factor that can negatively affect the FLI score at a 10% level of significance, which means that the younger generation has a tendency to be financially literate because the age variable’s coefficient is negative. It is pertinent to mention that the youngest respondent in this survey was 24 years old, and the oldest was 81. In the age of digital information, younger generations absorb new technologies more readily than older ones as information availability is growing rapidly in rural areas of Pakistan. The younger generations (below 50) can access more information since they are more accustomed to the capabilities of contemporary technological devices used online. As a result, the results of the regression show that younger generations are more financially literate than older generations. The age group of 31 to 40 years has the greatest FLI. The value of the FLI is lower in the age group under 30 than it is in the bracket of 31 to 40 years. The findings of this study are consistent with Usera [77], who discovered that the lowest age range (15–25 years) had a lower index of financial literacy value than the next age range (26–45 years) and that the lowest index is in the age range above 60 years. At a 1% level of significance, the length of formal schooling has a favorable and noticeable impact on the financial literacy score. Higher education is necessary to improve one’s financial literacy. Education, both formal and informal, has an impact on how people think, act, and solve problems. Higher-educated individuals will be more accepting of change, have more positive viewpoints, and be more adept at using information technology wisely.

According to Chen and Volpe [78], FLI should increase with the increase in education levels. At the significance level of 1%, the distance between a farm and the nearby city has a real and detrimental effect on the FLI score. The greater the distance to a location where one could easily access technology information in a nearby city, the lower the respondent’s level of financial literacy. The FLI is favorably impacted by annual income at the 1% level of significance. Higher-income earners are more likely to be financially literate than low-income earners due to access to and availability of contemporary information technology and agricultural advancement updates. At a significance level of 10%, farmers having bank accounts could positively influence the FLI score. To conduct daily financial transactions, it has become absolutely necessary for everyone to have a bank account. Opening a bank account has numerous advantages, including increased security, simpler financial operations, earning interest, and a government guarantee. The use of various banking services demonstrates a higher level of financial literacy. According to Lusardi [74], Garman et al. [75], Servon and Kaestner [76], and Wagner [79], among others, financial education increases the financial literacy score.

Moreover, the level of financial literacy is not significantly influenced by gender. Positively skewed coefficients suggest that men typically have higher levels of financial knowledge. However, it is equally probable for men and women to pursue financial education to raise their level of financial literacy. Foregoing in view, the FLI has not been considerably impacted by the primary source of occupation, i.e., respondents who identified as farmers as their primary occupation had lower financial literacy. The reason is that the person who works on a farm on a daily basis will learn less than a trader. Farmers will usually come into contact with other farmers, but the non-farmers will get a vast exposure as they meet different kinds of persons on a daily basis.

4.4. FSAC Accessibility

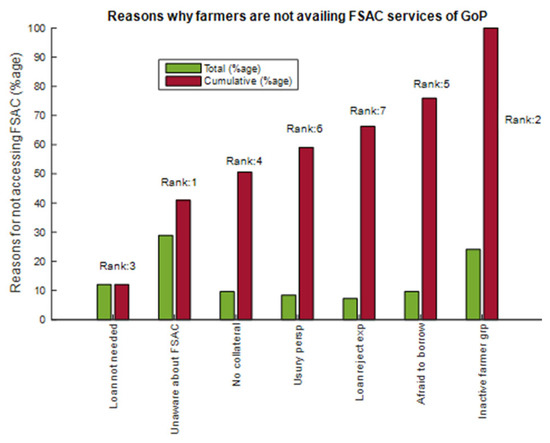

FSAC can be accessible either singly or in groups, both with their own benefits and drawbacks. A total of 36.5% of respondents used farmer groups to access FSAC, while the remaining 63.5% used individual access. Interest rates are the same whether you get them personally or through farmer groups. The number of loans obtained using the farmer group platform was relatively smaller, i.e., around PKR 100 thousand, whereas each loan obtained on an individual basis is an average of around PKR 140 thousand. In this investigation, 260 samples were used, of which 95 samples accessed FSAC and 165 samples did not, for a variety of reasons. There are seven factors that can be gathered to explain why FSAC is inaccessible: (1) Ignorance of the FSAC interest subsidy program, (2) Lack of Need for Loan, (3) Lack of Collateral, (4) Bank Loan considered as Usury, (5) Rejection when proposing FSAC, (6) Fear of Borrowing from Bank, and (7) Inactivity of farmer group. The highest percentage of respondents not availing of FSAC (28.89%) belongs to the ones who are unaware of any interest subsidies offered by the GoP (Figure 10).

Figure 10.

Reasons why farmers are not availing FSAC services of the GoP. Source: authors’ development.

The respondent’s participation in a farmer group that is inactive and rarely holds meetings has the second highest percentage of farmers (24.2%) who are not availing of FSAC. Meetings of farmer groups only take place when the government offers support in the form of seeds, fertilizer, and production machinery. The third most common reason for not using the FSAC is due to the reason that respondents do not necessarily require loans for their farming expenses. In light of the aforementioned circumstances, a portion of dispersed respondents did not use FSAC because they were unaware of the government’s initiative to subsidize interest in FSAC.

This suggests that in order to accomplish the purpose of the FSAC subsidy program, there is a greater need for widespread dissemination of information about government initiatives. Banks, affiliated offices, and farmer groups can disseminate information either individually or collectively. Furthermore, the agricultural regional office and other government entities should prioritize guiding farmer groups in order to increase their financial literacy.

According to the microfinance triangle developed by Zeller and Meyer [80], microfinance institutions must focus on three key goals: outreach, impact, and sustainability. This study suggests that the FSAC accessed by respondents is still quite small. ZTBL in Pakistan must innovate in order to connect with more FSAC participants, which will lead to increased revenues and the sustainability of bank enterprises. The FSAC participants’ good effects, growing profit made by the ZTBL and other banks, and the high sustainability will help in improving the well-being of the farmer, which will ultimately fuel the regional and national economies.

4.5. Loan Application

According to the respondent’s data, 36.5% of farmers accessed FSAC through farmer groups, and 63.5% accessed it individually. This implies that one of every four farms uses farmer organizations to apply for FSAC loans in Pakistan. Therefore, it is crucial for a farm to join a farmer group, and it is crucial for the farmer group to take an active role in serving its members’ interests. Table 2 summarizes the pros and cons of availing FSAC loan through the group.

Table 2.

Pros and cons of availing FSAC through farmer group.

4.6. The Impact Variables of FSAC Accessibility

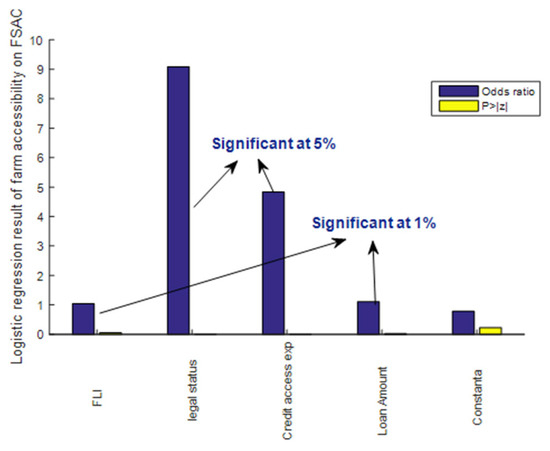

It is possible to conclude that the logistic regression model is a good and fit model that can help in making a decision about availing FSAC based on the likelihood ratio of 186.39, degree of freedom as 10, log-likelihood as 68.243, pseudo-R2 as 56.92%, and p = 0.000. The model uses a number of variables such as age, education level, farm income, cultivable area width, collateral, interest rate, FLI, the legal status of the farmer group, credit accessibility experience, and loan size. The estimation findings revealed that, at a significance level of 1%, six of the ten independent variables utilized in the model have a substantial influence on whether or not FSAC is accepted. These factors include farm revenue, the size of the cultivated area, collateral, interest rates, the legal status of the farmer group, and credit accessibility experience. The loan amount and FLI have a substantial impact at the 1% level of significance (Figure 11). The Z-values of FLI, LS, CAex, LA, and Constanta are 1.92, 3.57, 6.32, 2.26, and −1.2.

Figure 11.

Logistic regression results of farm accessibility of FSAC keeping in view variables like FLI, LS, CAex, LA, and Constanta. Source: authors’ development.

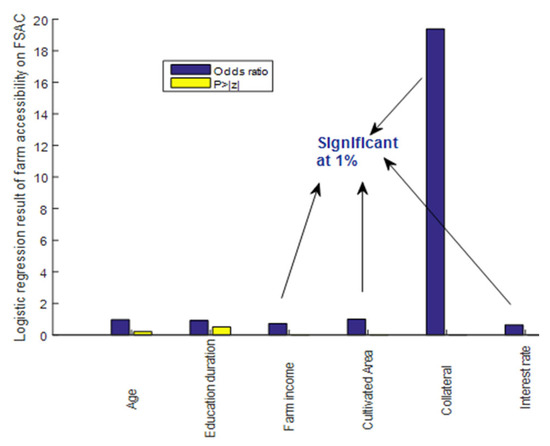

Age and education duration did not have a significant impact on FSAC accessibility (Figure 12). By multiplying the volume of rice production by the price of paddy, the farm revenue variable calculates the monetary worth of the commodity. The accessibility of FSAC is impacted by the respondent’s lowest income of 25,000 PKR. The central Punjab and Khyber Pakhtunkhwa farmers’ average farm revenue is 0.36 million PKR annually. The farm income variable’s Z value is negative, which means that obtaining FSAC is more likely if the farm income is lower. According to the ZTBL and ACAC statistics, the interest subsidy is given to low-income small farms so that high-income farms are less inclined to apply for FSAC. The Z-values of variables such as A, ED, FIS Area, C, and IR are −1.27, −0.66, −2.69, 2.74, 4.85, and −5.48, respectively.

Figure 12.

Logistic regression results of farm accessibility of FSAC keeping in view variables like A, ED, AI, Area, C, and IR. Source: authors’ development.

Farm income has a negative and significant impact on FSAC accessibility, according to the p-value of the farm income variable, which is significant at the 1% level. In rice farming, the primary productivity component is the area under cultivation. The likelihood of its production will be higher the wider the farmed area, while the likelihood will decrease the narrower the cultivated area. The scale of farming is shown by the breadth of the cultivated area; the larger the cultivated area, the larger the scale of farming. Each respondent in this study had a different farmed area. The largest cultivable area measures 5.6 hectares, while the smallest cultivable area measures 0.2 hectares. A bigger cultivated area is more likely to have access to FSAC, according to the regression results, which show that the Z value of the cultivated area variable has a positive sign. The chances ratio of 1.001 indicates that the chance of accessing FSAC increases by one for each hectare of cultivated land added.

According to Zhao et al. [81], the collateral asset is the debtor’s guarantee if the business is not lucrative. The debtor will work harder to expand his business in order to keep his assets, which increases the likelihood that his business will succeed. The collateral variable’s Z value is positive, indicating that there will be a higher chance of accessing FSAC if the collateral is pledged. The odds ratio is 19.4, and the collateral variable’s p-value is significant at the 1% level, showing that the collateral has a positive and significant impact on FSAC accessibility. The interest rate that must be paid by the debtor within a year is the variable interest rate. According to the regression, the value of Z for interest rate is negative, which means that the likelihood of the respondent accessing FSAC decreases as the interest rate rises. The interest rate considerably and negatively impacted the accessibility of FSAC, as shown by the odds ratio value of 0.634, and the p-value of the interest rate variable is significant at the 1% level.

The legal standing of farmer groups can give them many advantages, including the ability to register with the justice and human rights departments of the GoP, acquire official legal recognition, and perhaps even get government subsidies more frequently. The Z value of the farmer group’s variable determining its legal entity status has a positive sign based on the results of the regression. It implies that compared to farmer groups without legal status, farmers who belong to farmer groups with legal status are more likely to have access to FSAC. The legal status of the farmer group has a positive and significant impact on the accessibility of FSAC, according to the p-value of the variable, which is significant at the 1% level. As long as the last loan has been repaid in a timely way, FSAC participants who have previously accessed it will have a better chance of borrowing it again.

By vetting the FSAC candidates who have previously obtained credit, the Bank might make even more financial savings. The credit access experience variable has a positive Z value according to the regression’s findings. This indicates that farmers with prior credit access experience are more likely to use FSAC than farmers without such expertise. The odds ratios of the credit access experience variables have a value of 4.828, which indicates that every farmer with credit access experience has a 4.828 times larger chance of accessing FSAC than farming without credit access experience.

The odds ratio for the loan amount variable is 1.11, which means that a loan amount increase of PKR 14,400 will have the potential to access FSAC, which is 1.11 times larger. The loan amount has a positive and significant influence on the accessibility of FSAC, according to the p-value value of the variable for the loan amount, which is significant at the 5% level. We know that the youngest respondent in this study is 24 years old, while the oldest respondent is 81 years old. The respondents are 47 years old on average. The age variable’s Z value has a negative sign which suggests that the likelihood of an older person being able to obtain FSAC is decreasing. This is consistent with the hypothesis and is supported by the fact that lending to senior citizens puts financial institutions at a greater risk of default. The results of this study are different from those of Nguyen and Luu [82], who claimed that age significantly affects one’s ability to acquire loans. The age variable does not significantly affect the FSAC accessibility, according to the p-value of the age variable over 10% significance. As they receive FSAC loans through the group, some senior respondents can easily avail of FSAC services of the GoP.

The accessibility of FSAC is not significantly impacted by the education duration variable. This variable shows how long the respondent took to complete his formal schooling. According to those who have completed elementary school, junior high school lasts six years, senior high school twelve years, and college sixteen. Respondents who have been in school for a longer period of time will be more educated, obviously. The education duration variable shows that the majority of responders had only completed elementary school. The education duration variable’s Z value has a negative sign which means that the less schooling a person has, the more likely they are to get credit. The likelihood of respondents who can access FSAC at the primary level will be higher given that the majority of respondents have education at the elementary level. The accessibility of FSAC is not impacted by education duration. This finding differs from those of Pandula [83], who claimed that education is a significant impact since it will improve the debtor’s ability to seek out financial information.

5. Recommendations

The GoP, along with relevant organizations, including SBP, ZTBL, and ACAC, must step up efforts to broaden financial literacy through education, training, and exposure to the banking and finance industries. These initiatives aim to improve the community’s financial literacy. The ability to access financial institution products and services for the benefit of the community and to promote the expansion of the national economy through the financial sector will result from adequate financial literacy. We come to the conclusion that it is crucial to effectively disseminate information on financing and agricultural technology and that doing so calls for distinct policies that are targeted at various farmer groups with various socioeconomic and farm-related features.

6. Conclusions

In the rain-fed region of Khyber Pakhtunkhwa (KP), Pakistan, this study examines the variables that influence farmers’ access to agricultural loans and their involvement in adopting better agricultural technologies. We evaluate and analyze the relative contributions of farmers’ socioeconomic characteristics on their access to loans and adoption techniques using logistic models. According to the findings, farmers who have access to agricultural loans are more likely to adopt new agricultural technologies. The binary logit model’s findings reveal that farmers with a sizable farm, high farm revenue, greater information access, and ownership of sizable physical assets had a favorable impact on credit access. However, access to agricultural loans for farmers appeared to be negatively impacted by the farming experience. In terms of the sources of finance used by farmers, this study indicated that farmers with greater assets, experience, and information tended to rely more on banks than on informal and input suppliers. In a similar vein, older farmers with higher levels of education, larger farms, and higher farm incomes had a higher propensity to borrow from input suppliers rather than banks. The average FLI of the study’s respondents was at a moderate level, which is consistent with the poll conducted in existing benchmarks. Age, education duration, distance from the nearby city, annual income, ownership of bank accounts, and financial education experience are factors that have a major impact on financial literacy. 7.6% of all farmer groups in the research area were reached by FSAC distribution, and the total amount disbursed is still considerably below the maximum amount of loans that can be made accessible. Some of the issues that prevent farmers from having widespread access to the FSAC include the following: lack of loan need; lack of knowledge of the existence of the FSAC; lack of collateral; loan usury perspective; loan rejection experience; fear of borrowing from the bank; and inactive farmer groups. The width of the cultivated land, collateral, FLI, the legal status of the farmer group, experience with credit accessibility, and the loan amount are all factors that have a positive and significant impact on the accessibility of FSAC, whereas factors having a negative and considerable impact on FSAC accessibility are farm income and interest rates.

The overall findings in this research could be utilized and extrapolated to check the overall effect of FLI, SMA, and variables impacting both of them on national and global levels. We are specifically focusing on KP and Punjab regions in this work, but in the future, we will hopefully expand our sample space by collecting farmers’ data in Sindh, Baluchistan, Gilgit-Baltistan, and Azud-Jammu-Kahsmir regions. In that case, we can compute and compare the FSAC accessibility and FLI status of each province of Pakistan. Only then would we be able to compare the overall FLI and FSAC global benchmarks with that in Pakistan.

Author Contributions

Conceptualization, A.R. and G.T.; methodology, A.R.; software, F.S.; validation, A.R., Z.T., G.T. and V.E.; formal analysis, A.R.; investigation, G.T.; resources, A.R., Z.T. and V.E.; data curation, G.T.; writing—original draft preparation, A.R.; writing—review and editing, V.E. and F.S.; visualization, Z.T. and V.E.; supervision, G.T.; project administration, A.R. and V.E.; funding acquisition, G.T. All authors have read and agreed to the published version of the manuscript.

Funding

This research is funded by Northeast Forestry University and the Chinese Government Scholarship Council grant number 201741006.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data presented in this study are available on request from the corresponding author.

Acknowledgments

The guidance from Shakir Ullah from Northeast Forestry University is highly appreciated.

Conflicts of Interest

The authors declare no conflict of interest. The funders had no role in the design of the study; in the collection, analyses, or interpretation of data; in the writing of the manuscript; or in the decision to publish the results.

References

- Siregar, H. Micro-Based Macroeconomic Policy; IPB Press: Bogor, Indonesia, 2009. [Google Scholar]

- Erokhin, V.; Gao, T.; Chivu, L.; Andrei, J.V. Food security in a food self-sufficient economy: A review of China’s ongoing transition to a zero hunger state. Agricu. Econ. Czech 2022, 68, 476–487. [Google Scholar] [CrossRef]

- Kini, J. Multidimensional Food Security Index: A Comprehensive Approach. Asian J. Agric. Ext. Econ. Sociol. 2022, 40, 317–331. [Google Scholar] [CrossRef]

- Cook, P.; Nixson, F. Finance and Small and Medium-Sized Enterprise Development; Institute for Development Policy and Management: Manchester, UK, 2000. [Google Scholar]

- Lader, P. The public/private partnership. Springs Spring 1996, 35, 41–44. [Google Scholar]

- Tobias, R. A Closer Look at EU Agricultural Subsidies: Developing Modification Criteria; Germanwatch: Berlin, Germany, 2006. [Google Scholar]

- Etonihu, K.I.; Rahman, S.A.; Usman, S. Determinants of access to agricultural credit among crop farmers in a farming community of Nasarawa State, Nigeria. J. Dev. Agric. Econ. 2013, 5, 192–196. [Google Scholar] [CrossRef]

- Gao, T.; Ivolga, A.; Erokhin, V. Sustainable rural development in Northern China: Caught in a vice between poverty, urban attractions, and migration. Sustainability 2018, 10, 1467. [Google Scholar] [CrossRef]

- Sikandar, F.; Erokhin, V.; Xin, L.; Sidorova, M.; Ivolga, A.; Bobryshev, A. Sustainable agriculture and rural poverty eradication in Pakistan: The role of foreign aid and government policies. Sustainability 2022, 14, 14751. [Google Scholar] [CrossRef]

- Akram, W.; Hussain, Z.; Sial, M.H.; Hussain, I. Agricultural credit constraints and borrowing behavior of farmers in rural Punjab. Eur. J. Sci. Res. 2008, 23, 294–304. [Google Scholar]

- Constantin, M.; Radulescu, I.D.; Andrei, J.V.; Chivu, L.; Erokhin, V.; Gao, T. A perspective on agricultural labor productivity and greenhouse gas emissions in context of the common agricultural policy exigencies. Econ. Agric. 2021, 68, 53–67. [Google Scholar] [CrossRef]

- Panait, M.; Erokhin, V.; Andrei, J.V.; Gao, T. Implication of TNCs in agri-food sector—Challenges, constraints and limits—Profit or CSR? Strateg. Manag. 2020, 20, 33–43. [Google Scholar] [CrossRef]

- Saqib, S.; Ahmad, M.M.; Panezai, S.; Ali, U. Factors influencing farmers’ adoption of agricultural credit as a risk management strategy: The case of Pakistan. Int. J. Disaster Risk Reduct. 2016, 17, 67–76. [Google Scholar] [CrossRef]

- Robb, C.A.; James, R.N. Associations between individual characteristics and financial knowledge among college students. J. Pers. Financ. 2009, 8, 170–184. [Google Scholar]

- Klapper, L.; Lusardi, A.; Panos, G. Financial Literacy and the Financial Crisis; National Bureau of Economic Research: Cambridge, MA, USA, 2012. [Google Scholar]

- Ullah, A.; Arshad, M.; Kächele, H.; Zeb, A.; Mahmood, N.; Müller, K. Socio-economic analysis of farmers facing asymmetric information in inputs markets: Evidence from the rainfed zone of Pakistan. Technol. Soc. 2020, 63, 101405. [Google Scholar] [CrossRef]

- Elahi, E.; Abid, M.; Zhang, L.; ul Haq, S.; Sahito, J.G.M. Agricultural advisory and financial services; farm level access, outreach and impact in a mixed cropping district of Punjab, Pakistan. Land Use Policy 2018, 71, 249–260. [Google Scholar] [CrossRef]

- Ullah, A.; Arshad, M.; Kachele, H.; Khan, A.; Mahmood, N.; Müller, K. Information asymmetry, input markets, adoption of innovations and agricultural land use in Khyber Pakhtunkhwa, Pakistan. Land Use Policy 2020, 90, 104261. [Google Scholar] [CrossRef]

- Zada, M.; Shah, S.J.; Yukun, C.; Rauf, T.; Khan, N.; Shah, S.A.A. Impact of small-to-medium size forest enterprises on rural livelihood: Evidence from Khyber Pakhtunkhwa, Pakistan. Sustainability 2019, 11, 2989. [Google Scholar] [CrossRef]

- Zada, M.; Yukun, C.; Zada, S. Effect of financial management practices on the development of small-to medium size forest enterprises: Insight from Pakistan. GeoJournal 2021, 86, 1073–1088. [Google Scholar] [CrossRef]

- Government of Pakistan. Pakistan Economic Survey 2016–2017. Available online: https://www.finance.gov.pk/survey_1617.html (accessed on 21 December 2022).

- Government of Pakistan. Agriculture. Pakistan Economic Survey 2019–2020. Available online: https://finance.gov.pk/survey/chapters_18/02-Agriculture.pdf (accessed on 21 December 2022).

- World Bank. World Development Indicators. Available online: http://data.worldbank.org/ (accessed on 21 December 2022).

- Government of Pakistan. Pakistan Economic Survey 2015–2016. Available online: http://www.finance.gov.pk (accessed on 15 December 2022).

- Trade Development Authority of Pakistan. Statistics for 2015–2016. Available online: http://www.tdap.gov.pk/tdap-statistics.php (accessed on 21 December 2022).

- Pakistan Bureau of Statistics. Agricultural Census. Available online: http://www.pbs.gov.pk/ (accessed on 10 December 2022).

- Government of Pakistan. Multidimensional Poverty in Pakistan. Available online: https://www.undp.org/pakistan/publications/multidimensional-poverty-pakistan (accessed on 10 December 2022).

- Food and Agriculture Organization of the United Nations. Women in Agriculture in Pakistan. Available online: http://www.fao.org (accessed on 15 November 2022).

- Food and Agriculture Organization of the United Nations. Available online: http://www.fao.org/faostat/en (accessed on 15 November 2022).

- Qamer, F.M.; Shehzad, K.; Abbas, S.; Murthy, M.; Xi, C.; Gilani, H.; Bajracharya, B. Mapping deforestation and forest degradation patterns in Western Himalaya, Pakistan. Remote Sens. 2016, 8, 385. [Google Scholar] [CrossRef]

- United Nations Development Program. Climate Public Expenditure and Institutional Review. Available online: http://www.pk.undp.org (accessed on 15 November 2022).

- Qamar-uz-Zaman, C.; Mahmood, A.; Rasul, G.; Afzaal, M. Climate Change Indicators of Pakistan; Pakistan Metrological Department: Islamabad, Pakistan, 2009. [Google Scholar]

- Hussain, S.S.; Mudasser, M. Prospects for wheat production under changing climate in mountain areas of Pakistan: An econometric analysis. Agric. Syst. 2007, 94, 494–501. [Google Scholar] [CrossRef]

- Todaro, M.P.; Stephen, C.S. Economic Development; Addison Wesley: Harlow, UK, 2009. [Google Scholar]

- Milton, H.S.; Orley, M.A., Jr. Contemporary Economics; Worth Publishers: New York, NY, USA, 1993. [Google Scholar]

- Wadud, M.A. Impact of Microcredit on Agricultural Farm Performance and Food Security in Bangladesh; Institute for Inclusive Finance and Development: Dhaka, Bangladesh, 2013. [Google Scholar]

- Quach, M.H.; Mullineux, A.W.; Murinde, V. Access to Credit and Household Poverty Reduction in Rural Vietnam; The University of Birmingham: Birmingham, UK, 2005. [Google Scholar]

- Montgomery, H. Serving the Poorest of the Poor: The Poverty Impact of the Khushhali Banks Microfinance Lending in Pakistan; Asian Development Bank Institute: Tokyo, Japan, 2005. [Google Scholar]

- Karlan, D.; Goldberg, N. The Impact of Microfinance: A Review of Methodological Issues; NYU Wagner Graduate School: New York, NY, USA, 2006. [Google Scholar]

- Aghion, B.A.; Morduch, J. The Economics of Microfinance; MIT Press: Cambridge, MA, USA, 2005. [Google Scholar]

- Ibrahim, A.H.; Bauer, S. Access to microcredit and its impact on farm profit among rural farmers in dryland of Sudan. Glob. Adv. Res. J. Agric. Sci. 2013, 2, 88–102. [Google Scholar]

- Angioloni, S.; Kudabaev, Z.; Ames, G.C.W.; Wetzstein, M. Micro-credit impact in Kyrgyzstan: A study case. In Proceedings of the 2013 Annual Meeting of the Southern Agricultural Economics Association, Orlando, FL, USA, 2–5 February 2013. [Google Scholar]

- Crepon, B.; Devoto, D.; Duflo, E.; Pariente, W. Impact of Microcredit in Rural Areas of Morocco: Evidence from Randomizes Evaluation; Agence Francaise de Developpement: Paris, France, 2011. [Google Scholar]

- Dewi, I.S.; Dwi, R.; Netti, T. Roles of food security and energy credit in increasing rice production and profits in Kampar Regency, Riau Province. J. Din. Pertanian 2015, 30, 163–170. [Google Scholar] [CrossRef]

- Farida, F.; Siregar, H.; Nuryartono, N.; Intan, E.K.P. An impact estimator using propensity score matching: People’s business credit program to micro-entrepreneurs in Indonesia. Iran. Econ. Rev. 2016, 20, 599–615. [Google Scholar] [CrossRef]

- Dahri, T.; Hutagaol, P.; Siregar, H.; Simatupang, P. Determinants of the KKPE Credit Program Repayment of Cattle Farmers in Central Java, Indonesia. Glob. J. Commer. Manag. Perspect. 2015, 4, 17–22. [Google Scholar]

- Wati, D.R.; Nuryartono, N.; Anggraeni, L. Microcredit access and impact on production and revenue of organic rice farming in Bogor regency. J. Econ. Dev. Policy 2014, 3, 75–94. [Google Scholar]

- Arief, B.; Rosmiati, M. Impact of Credit Access on Rice Farmers Household Welfare; IKOPIN Press: Jatinangor, Indonesia, 2013. [Google Scholar]

- Pakistan Bureau of Statistics. 6th Population and Housing Census 2017. Available online: https://www.pbs.gov.pk/content/populationcensus (accessed on 15 December 2022).