1. Introduction

Manufacturing is an important cornerstone for countries to participate in global competition as a symbol of national competitiveness and overall strength. Despite their contribution to our economic development, manufacturing companies also hurt the environment. Environmental pollution incidents occur frequently, thus making environmental concerns a hotspot repeatedly. Green innovation and green transition have become top priorities in China’s “peak carbon dioxide emissions, carbon neutrality” strategic goal [

1]. The manufacturing industry, which consumes energy and resources and emits pollutants, should achieve high-quality development through green transition to improve its competitiveness under the “double carbon” target. Manufacturers are facing real constraints from the environment and limited resources, making the green transition a real dilemma.

In response to manufacturing companies’ struggles to achieve a green transition, the state will implement environmental tax and regulation policies. As the core subject of independent innovation, companies play a central role in enhancing innovation capability. Manufacturing companies have become increasingly focused on the green transition through green innovation [

2].

In practice, green innovation and green transition have aroused extensive attention. Green transition research places a focus on macro-level policy changes and micro-level changes within companies. At the macro level, the green transition of countries and regions is analyzed primarily from the perspective of policy research [

3]. There are three aspects to a micro-level corporate green transition: corporate executives [

4], corporate social responsibility [

1], and environmental regulation [

5]. However, studies focus on the direct correlation between “Internet plus” and green transition. There is a lack of literature that examines how “Internet plus” improves the green transition of manufacturing companies and what are factors for its effectiveness.

Environmental regulation and green technology innovation can be considered from four general perspectives. First, Porter’s hypothesis states that company innovation can be fostered by appropriate environmental regulation [

6]. Even after the short-term increase in costs, companies can obtain a long-term innovation compensation effect, thus facilitating innovation [

7]. Second, some scholars argue that environmental regulations increase company costs, which inhibits companies from developing green technologies [

8]. Third, some research has suggested that environmental regulation and technological progress are non-linear due to time-scale changes. In the short run, pollution-control investments crowd out green technology R&D investments, whereas innovation can generate additional profits to boost technological progress in the long run [

9]. Fourth, some empirical research has suggested that there is no significant correlation between the two based on an analysis of the calculations [

10]. Most literature on this topic focuses on the theoretical framework of “environmental regulation-green innovation-company performance” [

11,

12] and lacks a discussion on differentiated green transition models for companies.

Existing research on the economic consequences of sewage fee-to-tax places a focus on the “double dividend” of environmental taxes, i.e., the environmental and social dividends [

13,

14,

15]. As a result of environmental taxes, the quality of the environment can be improved, while reducing distortions are reduced, employment is encouraged, and even economic growth is stimulated. Studies on environmental taxes have largely focused on the macro level. The effect of sewage fee-to-tax on the green transition of manufacturing companies should be investigated in depth.

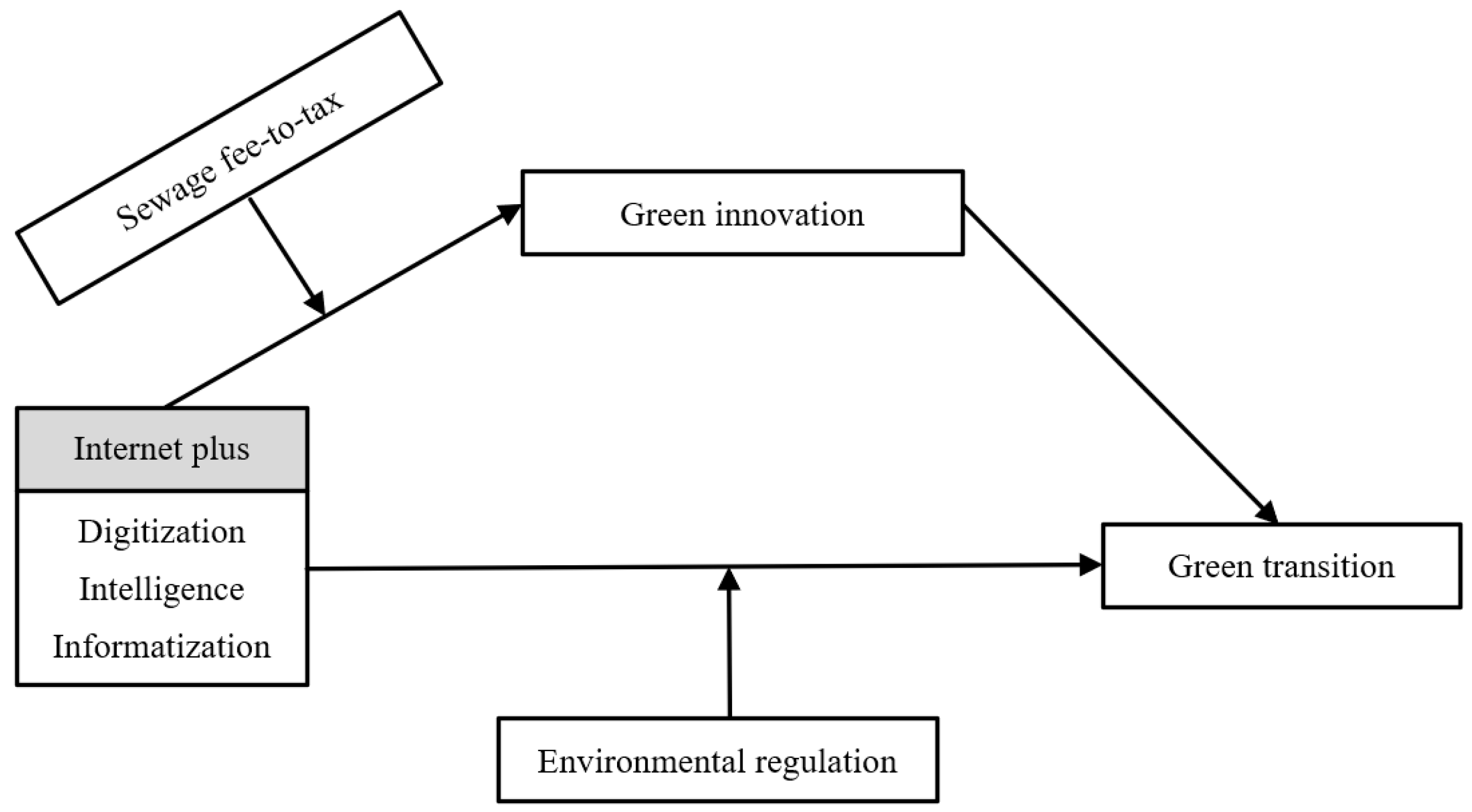

To solve the above research gaps, this study seeks to answer the following questions: Can “Internet Plus” with digitalization, intellectualization, and informatization promote the green transition of manufacturing companies? What role does green technology innovation play in the mechanism? Can environmental regulation and environmental protection taxes positively regulate the green transition of manufacturing companies?

In this study, “Internet plus” with its digitalization, intelligence, and informatization is first analyzed to facilitate the green transition mechanism of manufacturing companies from a theoretical perspective. An empirical analysis has been conducted on manufacturing companies listed on A-shares from 2015 to 2020 to verify the theoretical hypotheses. The results indicate that “Internet plus” is capable of significantly facilitating the green transition of manufacturing companies, and the reliability of the results is verified through endogeneity analysis and robustness tests. The result of the further analysis reveals that “Internet plus” with its digitalization and intelligence takes on a more critical significance in promoting green transition in private companies, while informatization is more important for state-owned companies. Moreover, there are significant regional and industry differences in the promotion effect, with a greater significance in the eastern region and high-tech industries. The result of the mechanism analysis indicates that “Internet plus” is capable of enhancing green transition through green technology innovation. Both environmental regulation and sewage fee-to-tax play a positive regulatory role. After 18 years of implementation, the environmental protection tax’s effect is stronger than before.

The main contributions of this study are as follows. First, research on green technology innovation and environmental regulation have contradictory findings (e.g., positive [

14], negative [

15], and U-shaped conclusions [

11]). Accordingly, how “Internet plus” has affected the green transition of companies is examined using Chinese manufacturing companies as an example, and how green technology innovation plays a mediating role is examined. The second contribution of this study is to complement the literature on China’s environmental tax by evaluating the comparative effect of the policy before and after its release. Third, this study presents “Internet plus” in three dimensions: digitalization, intelligence, and information, which provides more targeted guidance on green transition than simply measuring “Internet plus” in the past. Fourth, most research has focused on the direct correlation between “Internet plus” and green transition. However, this study breaks through previous studies that fail to incorporate the process mechanism, thus enriching theoretical results concerning “Internet plus” and green transition at the mechanism level. Furthermore, this study provides Chinese evidence for Porter’s hypothesis and extends its theoretical extension from the perspective of environmental regulation, thus providing reference value for the green transition and taking on practical significance for the global green era’s development.

The rest of this study is organized as follows. In

Section 2, the literature is reviewed, and the research hypotheses are proposed. In

Section 3, the research methods are described, and the research models are built. In

Section 4, the empirical research results are reported. In

Section 5, the in-depth analysis is presented. In

Section 6, a conclusion is drawn for this study.

6. Discussion

In the context of the rapid development of the Internet, the Internet and manufacturing companies should be integrated deeply to ensure high-quality development. Some scholars have focused on the integration between the Internet and the manufacturing industry, then studied the role of “Internet plus” in improving the competitiveness of companies. However, there is less literature that extends the research to green transition and explores the impact of “Internet plus” on the green transition of manufacturing companies. Due to this, it has become increasingly important to understand the mechanisms by which “Internet plus” can promote the green transition of manufacturing companies.

First and foremost, “Internet plus” with its digitalization, intelligence, and informatization have a significant effect in promoting green transition. In addition, “Internet plus” informatization plays a more significant role in the mechanism. Informatization technology promotes the mutual integration of all areas of society, improves the efficiency of resource allocation, and makes a significant contribution to the green transition of society. This study portrays “Internet plus” from three levels: digitalization, intelligence, and informatization, which is more comprehensive and breaks through the limitation of measuring “Internet plus” only from the overall perspective. It offers more targeted guidance in exploring the green transition of manufacturing companies and broadens the theoretical understanding of non-economic value creation in company transformation. The findings support and extend the perspectives of Peng et al. by introducing and confirming that digitalization inhibits and then promotes green transition in companies [

23].

Second, from a mechanism perspective, green technology innovation is selected as a mediating variable. The results support the transmission path of “Internet plus → green innovation → green transition”. Further, it is supplemented by Sun and Guo’s findings that digital transformation can significantly boost green technology innovation [

50].

Third, this study analyzes the regulatory effects of environmental regulation and sewage fee-to-tax. They have significant positive effects in regulating the above relationships. By exploring the effect of the release of China’s Environmental Protection Tax on manufacturing companies, this study complements the existing literature on environmental taxes in China by analyzing the comparative effect of the policy before and after its release. It provides evidence for Porter’s hypothesis in China [

6] and extends its theoretical application. It provides a reference value for the green transition of manufacturing companies and has some practical significance for the development of a new global green era.

In further research, considering that this mechanism of action can be influenced by external macroenvironmental factors and company factors, this study analyzes the heterogeneity in the nature of property rights, regional, and industry classification.

Despite its valuable insights, this study has limitations that should stimulate further research. The listed manufacturing companies in Shanghai and Shenzhen are examined to demonstrate the problem. However, it cannot be judged if the conclusion applies to non-listed companies, and its universality must be further demonstrated. Second, in the future, we can analyze and compare the green transition of manufacturing companies in different countries. Lastly, the heterogeneity of company size can be considered to analyze more comprehensively the effect of “Internet plus” on the green transition.

7. Conclusions and Policy Implications

Using A-share listed manufacturing companies from 2015–2020 as a research sample, this study examines “Internet plus” with its digitalization, intelligence, and informatization impact on the green transition, and draws the following conclusions. First, it is confirmed that “Internet plus” with its digitalization, intelligence, and information technology is capable of significantly boosting the green transition of manufacturing companies, and the results are verified through endogeneity analysis and robustness testing.

Second, “Internet plus” with its digitalization, intelligence, and informatization can enhance the green transition through green technology innovation.

Third, results indicate that environmental regulation strengthens the positive correlation between “Internet plus” with its digitalization, intelligence, informatization, and green transition. Sewage fee-to-tax bolsters the positive correlation between “Internet plus” with its digitalization, intelligence, informatization, and green transition. Further, the effect of implementing an environmental protection tax before and after 2018 is analyzed, and it is suggested that the effect is stronger after 2018.

Lastly, heterogeneity analysis indicates that “Internet plus” with its digitalization and intelligence is more effective in promoting the green transition in private companies, while information technology is more effective in the green transition of state-owned companies. There are obvious regional and industry differences in this promotion effect, with more significant effects in the eastern region. The positive effect in high-tech industries is larger than that of companies in non-high-tech industries. The above findings offer several policy implications.

Our findings also provide important practical implications. First, manufacturing companies should be guided by the government to accelerate the integration of “Internet plus” and carry out targeted green transitions. Through a new company ecosystem, manufacturing companies should develop digital platforms to create new product experiences and social value.

Second, environmental regulations should not only focus on government action, but also consider how markets allocate resources to drive green innovation.

Third, private companies should continue to focus on resource accumulation and improve resource utilization efficiency. To improve the industrial layout, the country needs to coordinate “Internet plus” and green development processes in the eastern and non-eastern regions. To promote green transition, non-high-tech companies should also cooperate in scientific research and cite advanced green innovation technologies.

Lastly, global economic growth is further inhibited by the effect of the pandemic. In the current economic environment, the government cannot reduce the strength of environmental regulations. The findings of this study further confirm Porter’s hypothesis [

6], which explains why environmental regulation should not be weakened, but rather be designed and implemented to encourage corporate green innovation.

{kind=link}