Comparing Price Transmissions between a High Blend Ethanol Fuel and a Conventional Fuel: An Application of Seemingly Unrelated Regressions

Abstract

:1. Introduction

2. Literature

3. Empirical Methodology

3.1. Testing for Price Pass-Through Symmetry Using the Error Correction Model

3.2. Granger Causality

3.3. Lag Order Analysis

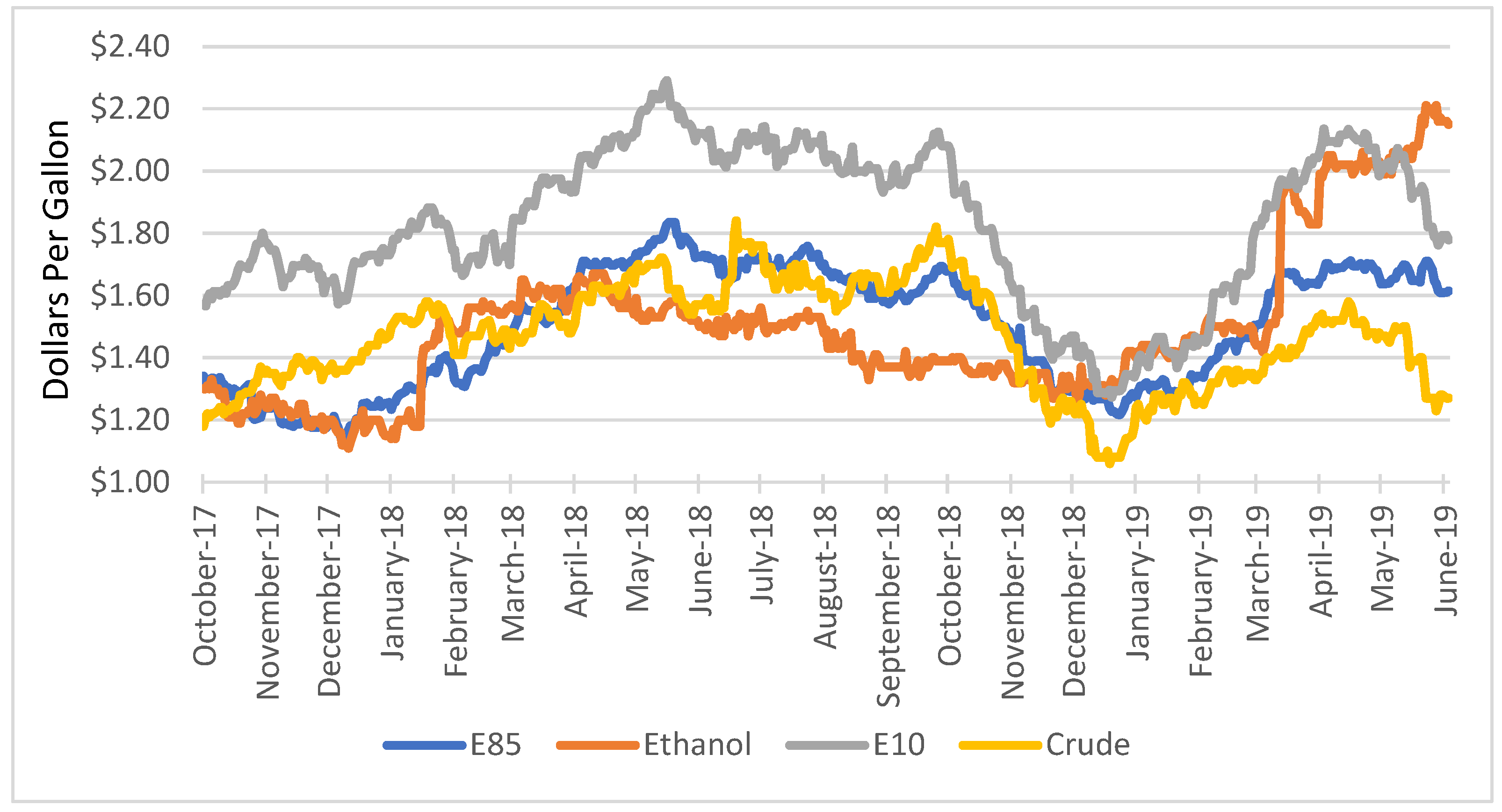

3.4. Data

4. Results

4.1. Econometric Models

4.2. Symmetry Analysis

5. Conclusions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Contín-Pilart, I.; Correljé, A.F.; Palacios, M.B. Competition, regulation, and pricing behaviour in the Spanish retail gasoline market. Energy Policy 2009, 37, 219–228. [Google Scholar] [CrossRef]

- Farkas, R.; Yontcheva, B. Price transmission in the presence of a vertically integrated dominant firm: Evidence from the gasoline market. Energy Policy 2019, 126, 223–237. [Google Scholar] [CrossRef]

- Zellner, A. An Efficient Method of Estimating Seemingly Unrelated Regressions and Tests for Aggregation Bias. J. Am. Stat. Assoc. 1962, 57, 348–368. [Google Scholar] [CrossRef]

- Borenstein, S.; Cameron, A.C.; Gilbert, R. Do gasoline prices respond asymmetrically to crude oil price changes? Q. J. Econ. 1997, 112, 305–339. [Google Scholar] [CrossRef]

- Bachmeier, L.J.; Griffin, J.M. New evidence on asymmetric gasoline price responses. Rev. Econ. Stat. 2003, 85, 772–776. [Google Scholar] [CrossRef]

- Galeotti, M.; Lanza, A.; Manera, M. Rockets and Feathers Revisited: An International Comparison on European Gasoline Markets. Energy Econ. 2003, 25, 175–190. [Google Scholar] [CrossRef]

- Bettendorf, L.; van der Geest, S.A.; Varkevisser, M. Price asymmetries in the Dutch retail gasoline market. Energy Econ. 2003, 25, 669–689. [Google Scholar] [CrossRef]

- Kaufmann, R.K.; Laskowski, C. Causes for an asymmetric relation between the price of crude oil and refined petroleum products. Energy Policy 2005, 33, 1587–1596. [Google Scholar] [CrossRef]

- Remer, M. An empirical investigation of the determinants of asymmetric pricing. Int. J. Ind. Organ. 2015, 42, 46–56. [Google Scholar] [CrossRef]

- Chesnes, M. Asymmetric pass-through in US gasoline prices. Energy J. 2016, 37, 153–180. [Google Scholar] [CrossRef]

- Cha, K.; Lee, C.-Y. Rockets and Feathers in the Gasoline Market: Evidence from South Korea. Sustainability 2023, 15, 3815. [Google Scholar] [CrossRef]

- Raeder, F.T.; Rodrigues, N.; Losekann, L.D. Asymmetry in Gasoline Price Transmission: How do Fuel Pricing Strategy and the Ethanol Addition Mandate Affect Consumers? Int. J. Energy Econ. Policy 2022, 12, 517–527. [Google Scholar] [CrossRef]

- Cui, J.; Yang, H.; Wang, Y.; Yang, C. Dynamics of the gas retail market under China’s price cap regulation. Energy Policy 2023, 174, 113424. [Google Scholar] [CrossRef]

- Grasso, M.; Manera, M. Asymmetric error correction models for the oil-gasoline price relationship. Energy Policy 2007, 35, 156–177. [Google Scholar] [CrossRef]

- Bagnai, A.; Ospina, C.A.M. Asymmetries, outliers and structural stability in the US gasoline market. Energy Econ. 2018, 69, 250–260. [Google Scholar] [CrossRef]

- Bakhat, M.; Rosselló, J.; Sansó, A. Price transmission between oil and gasoline and diesel: A new measure for evaluating time asymmetries. Energy Econ. 2022, 106, 105766. [Google Scholar] [CrossRef]

- Engle, R.; Granger, C.W.J. Co-Integration and error correction: Representation, estimation, and testing. Econometrica 1987, 55, 251–276. [Google Scholar] [CrossRef]

- Blair, B.F.; Campbell, R.C.; Mixon, P.A. Price pass-through in US gasoline markets. Energy Econ. 2017, 65, 42–49. [Google Scholar] [CrossRef]

- Granger, C.W.J. Investigating causal relations by econometric models and crossspectral methods. Econometrica 1969, 37, 424–438. [Google Scholar] [CrossRef]

- Radchenko, S. Oil price volatility and the asymmetric response of gasoline prices to oil price increases and decreases. Energy Econ. 2005, 27, 708–730. [Google Scholar] [CrossRef]

- Yang, Y.-T.; Yang, T.-Y.; Chen, S.-H.; Tong, C.-V. Exploring the non-linearity of West Texas Intermediate crude oil price from exchange rate of US dollar and West Texas Intermediate crude oil production. Energy Strategy Rev. 2022, 41, 100854. [Google Scholar] [CrossRef]

- Li, J.; Stock, J.H. Cost pass-through to higher ethanol blends at the pump: Evidence from Minnesota gas station data. J. Environ. Econ. Mangement 2019, 93, 1–19. [Google Scholar] [CrossRef]

- Bacon, R. Rockets and feathers: The asymmetric speed of adjustment of UK retail gasoline prices to cost changes. Energy Econ. 1991, 13, 211–218. [Google Scholar] [CrossRef]

{kind=link}

| Variable | ADF Unit Root Tests | Long-Run Relationship | Johansen Cointegration Tests |

|---|---|---|---|

| E10 | −1.40 | Conventional Fuel | 151.01 *** |

| E85 | −1.06 | ||

| Crude | −0.06 | High-Blend Ethanol Fuel | 149.60 *** |

| Ethanol | 0.01 | ||

| ∆E10 | −12.48 *** | ||

| ∆E85 | −12.33 *** | ||

| ∆Crude | −13.43 *** | ||

| ∆Ethanol | −13.42 *** |

| Null Hypotheses | Causality F-Statistic |

|---|---|

| E10 does not cause Ct | 0.46 |

| Ct does not cause E10 | 57.07 *** |

| E10 does not cause Et | 0.76 |

| Et does not cause E10 | 2.52 ** |

| E85 does not cause Ct | 0.73 |

| Ct does not cause E85 | 9.34 *** |

| E85 does not cause Et | 1.74 |

| Et does not cause E85 | 2.50 ** |

| Standard | Coefficient of | ||||

|---|---|---|---|---|---|

| Variable | Observations | Mean | Range | Deviation | Variation |

| E10 | 524 | $1.83 | $1.27–$2.29 | 0.2457 | 13.40 |

| E85 | 524 | $1.50 | $1.15–$1.83 | 0.1908 | 12.70 |

| Crude Oil Spot | 524 | $1.47 | $1.06–$1.84 | 0.1688 | 11.48 |

| Ethanol | 524 | $1.50 | $1.11–$2.21 | 0.2459 | 16.43 |

| E10 | E85 | ||

|---|---|---|---|

| Coefficient | Estimate | Coefficient | Estimate |

| Ct | 1.129 *** | Ct | 0.738 *** |

| (0.022) | (0.023) | ||

| Et | 0.499 *** | Et | 0.359 *** |

| (0.021) | (0.022) | ||

| Trend | −0.093 *** | Trend | 0.032 *** |

| (0.008) | (0.008) | ||

| Constant | −0.375 *** | Constant | −0.188 *** |

| (0.036) | (0.038) | ||

| R2 | 0.892 | R2 | 0.80 |

| Coefficient | Estimate | Coefficient | Estimate |

|---|---|---|---|

| 0.202 *** | 0.194 *** | ||

| (0.07) | (0.05) | ||

| 0.475 *** | 0.890 *** | ||

| (0.068) | (0.038) | ||

| −0.216 | 0.280 *** | ||

| (1.148) | (0.082) | ||

| 0.130 * | 0.104 | ||

| (0.067) | (0.066) | ||

| 0.291 *** | −0.249 *** | ||

| (0.05) | (0.058) | ||

| 0.302 *** | 0.052 | ||

| (0.079) | (0.043) | ||

| −0.216 *** | 0.066 | ||

| (0.066) | (0.055) | ||

| 0.199 *** | 0.084 | ||

| (0.051) | (0.054) | ||

| 0.210 *** | −0.142 *** | ||

| (0.067) | (0.048) | ||

| −0.091 | −0.151 * | ||

| (0.063) | (0.087) | ||

| 0.093 | 0.092 | ||

| (0.068) | (0.08) | ||

| 0.162 *** | 0.258 *** | ||

| (0.033) | (0.058) | ||

| −0.007 | 0.031 | ||

| (0.031) | (0.056) | ||

| −0.236 *** | 0.377 *** | ||

| (0.044) | (0.099) | ||

| 0.080 | −0.122 | ||

| (0.061) | (0.092) | ||

| −0.077 *** | −0.164 ** | ||

| (0.022) | (0.067) | ||

| −0.073 *** | 0.102 | ||

| (0.018) | (0.068) | ||

| 0.038 | −0.084 * | ||

| (0.073) | (0.049) | ||

| −0.001 | −0.235 *** | ||

| (0.001) | (0.057) | ||

| Trend | 0.006 *** | ||

| (0.001) | |||

| Constant | −0.010 ** | ||

| (0.005) | |||

| System Weighted R2 | 0.728 |

| Coefficient | Estimate | Coefficient | Estimate |

|---|---|---|---|

| −0.282 *** | 0.015 | ||

| (0.058) | (0.033) | ||

| 0.156 *** | 0.131 *** | ||

| (0.049) | (0.039) | ||

| 0.101 ** | 0.075 *** | ||

| (0.04) | (0.028) | ||

| 0.065 | 0.065 ** | ||

| (0.062) | (0.026) | ||

| 0.092 *** | 0.149 *** | ||

| (0.034) | (0.036) | ||

| 0.136 *** | 0.026 | ||

| (0.045) | (0.029) | ||

| −0.017 | −0.035 | ||

| (0.049) | (0.034) | ||

| −0.078 * | −0.081 ** | ||

| (0.043) | (0.034) | ||

| −0.050 | 0.108 ** | ||

| (0.784) | (0.051) | ||

| 0.103 * | 0.368 *** | ||

| (0.058) | (0.064) | ||

| 0.094 *** | −0.017 | ||

| (0.019) | (0.032) | ||

| 0.150 *** | 0.050 | ||

| (0.039) | (0.046) | ||

| −0.012 | 0.069 | ||

| (0.041) | (0.045) | ||

| −0.049 *** | 0.202 *** | ||

| (0.017) | (0.054) | ||

| 0.135 ** | 0.026 | ||

| (0.057) | (0.054) | ||

| 0.114 *** | −0.287 *** | ||

| (0.043) | (0.06) | ||

| −0.240 *** | −0.022 | ||

| (0.038) | (0.041) | ||

| 0.017 | 0.044 | ||

| (0.02) | (0.042) | ||

| −0.150 *** | −0.071 * | ||

| (0.049) | (0.037) | ||

| Trend | 0.001 ** | ||

| (0.001) | |||

| Constant | 0.000 | ||

| (0.002) | |||

| System Weighted R2 | 0.728 |

| Short-Run Null Hypotheses | Long-Run Null Hypothesis |

|---|---|

| (Intra-model) | |

| (Intra-model) | |

| (Intra-model) | |

| ) (Intra-model) | |

| (Cross-model) | |

| (Cross-model) | |

| (Cross-model) | |

| (Cross-model) |

| Short-Run Null Hypotheses | T-Statistic | Long-Run Null Hypothesis | T-Statistic |

|---|---|---|---|

| E10 Intra-Model | |||

| 0.08 | |||

| Not Applicable | |||

| ) | 2.63 *** | ||

| ) | −2.11 ** | ||

| E85 Intra-Model | |||

| Not Applicable | |||

| −2.43 ** | |||

| ) | −2.54 ** | ||

| ) | 0.22 | ||

| Not Applicable | |||

| −1.15 | |||

| Cross-Model | |||

| 1.08 | |||

| −2.14 ** | |||

| ) | 6.26 *** | ||

| ) | 4.44 *** |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Parrott, S. Comparing Price Transmissions between a High Blend Ethanol Fuel and a Conventional Fuel: An Application of Seemingly Unrelated Regressions. Sustainability 2023, 15, 15974. https://doi.org/10.3390/su152215974

Parrott S. Comparing Price Transmissions between a High Blend Ethanol Fuel and a Conventional Fuel: An Application of Seemingly Unrelated Regressions. Sustainability. 2023; 15(22):15974. https://doi.org/10.3390/su152215974

Chicago/Turabian StyleParrott, Scott. 2023. "Comparing Price Transmissions between a High Blend Ethanol Fuel and a Conventional Fuel: An Application of Seemingly Unrelated Regressions" Sustainability 15, no. 22: 15974. https://doi.org/10.3390/su152215974

APA StyleParrott, S. (2023). Comparing Price Transmissions between a High Blend Ethanol Fuel and a Conventional Fuel: An Application of Seemingly Unrelated Regressions. Sustainability, 15(22), 15974. https://doi.org/10.3390/su152215974