Actual Quality Changes in Natural Resource and Gas Grid Use in Prospective Hydrogen Technology Roll-Out in the World and Russia

,

,  ,

,

Abstract

:1. Introduction

2. Obstacles to Producing Hydrogen

- Organize production using a method of hydrogen production that would be cost-effective, allow the production of fuel on an industrial scale and not have a significant carbon footprint [2].

- Significantly reduce the cost of manufacturing engines and systems based on hydrogen fuel cells and increase their motor life period and integrated efficiency factor or coefficient of operational productivity (IEF/COP).

- Ensure safety throughout the entire chain from the production to consumption of hydrogen, including storage and transport systems, with gradual improvements in their kinematic and thermodynamic characteristics, and reduce the content of special metal per kg of hydrogen transport fittings of hydrogen pipelines and storage facilities for its safe storage [26].

- Improve the efficiency of hydrogen transportation and (or) reduce the distance from the places of production to the places of consumption.

- Overcome the lack of feasible technologies for capturing and storing carbon dioxide in countries striving to become significant producers of “low-carbon” hydrogen.

- Find a way to overcome the freshwater deficit in a number of countries planning large-scale hydrogen production by electrolysis by building expensive desalination plants.

- Develop an international system of standards and regulations in the field of hydrogen energy based on optimal technological solutions.

3. Brief Information about the Development of Hydrogen Energy in Leading Countries

3.1. Europe

3.2. USA

3.3. Japan

3.4. South Korea

3.5. China

3.6. India

- Measures are adopted to allow sales (distribution) companies to supply electricity to producers of green hydrogen and ammonia at reduced tariffs.

- Producers of green hydrogen and ammonia are exempted from paying tariffs for the transmission of electricity between states for 25 years if the project is commissioned before 30 June 2025.

- Green hydrogen/ammonia producers and renewable energy production facilities should be provided with a connection to the electricity grid in a prioritized (accelerated) manner.

4. Results

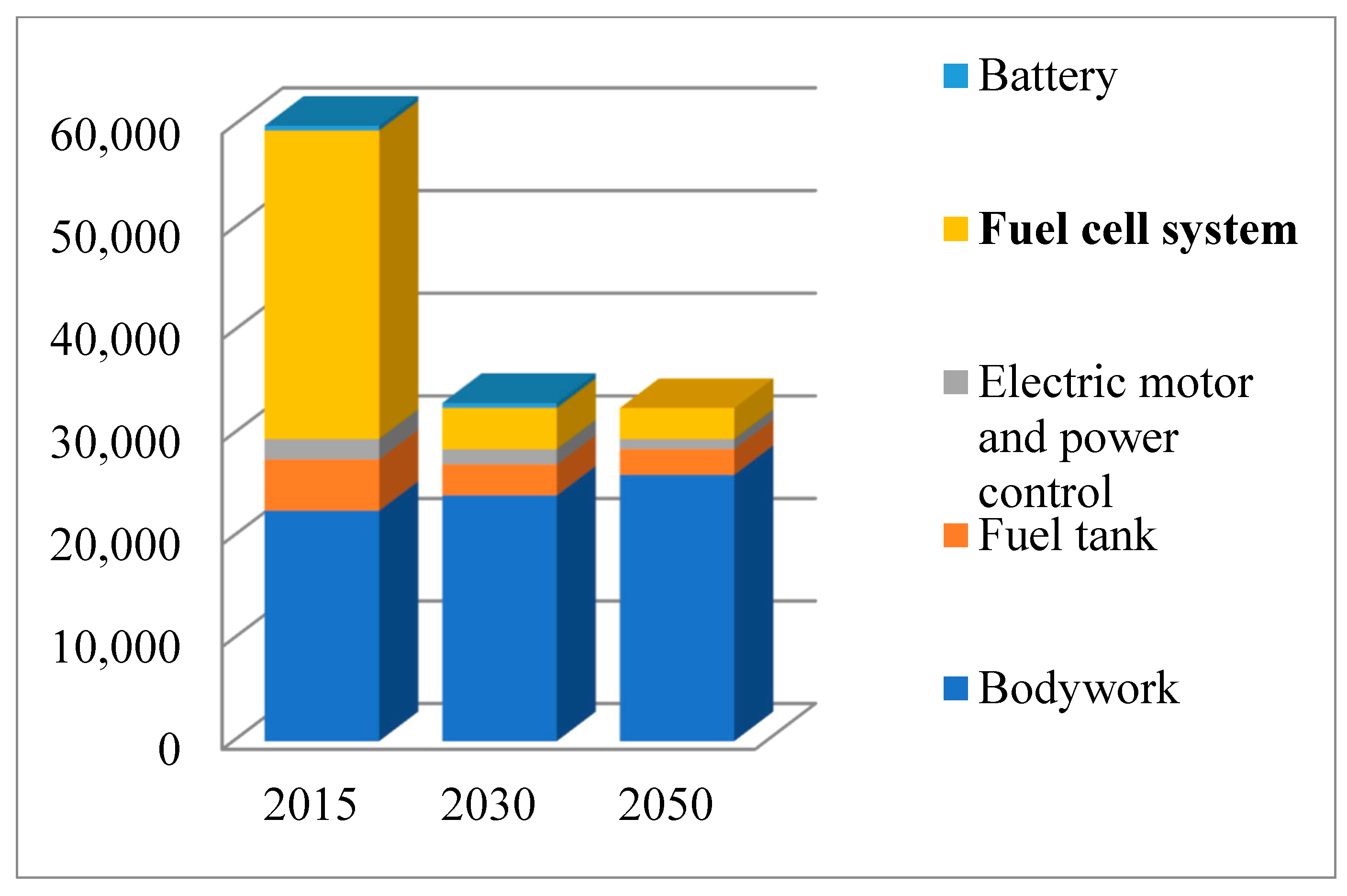

4.1. The Growing Number of HFCVs and Hydrogen Filling Stations Worldwide as a Visible Consumer Achievement in the Field of Hydrogen Energy

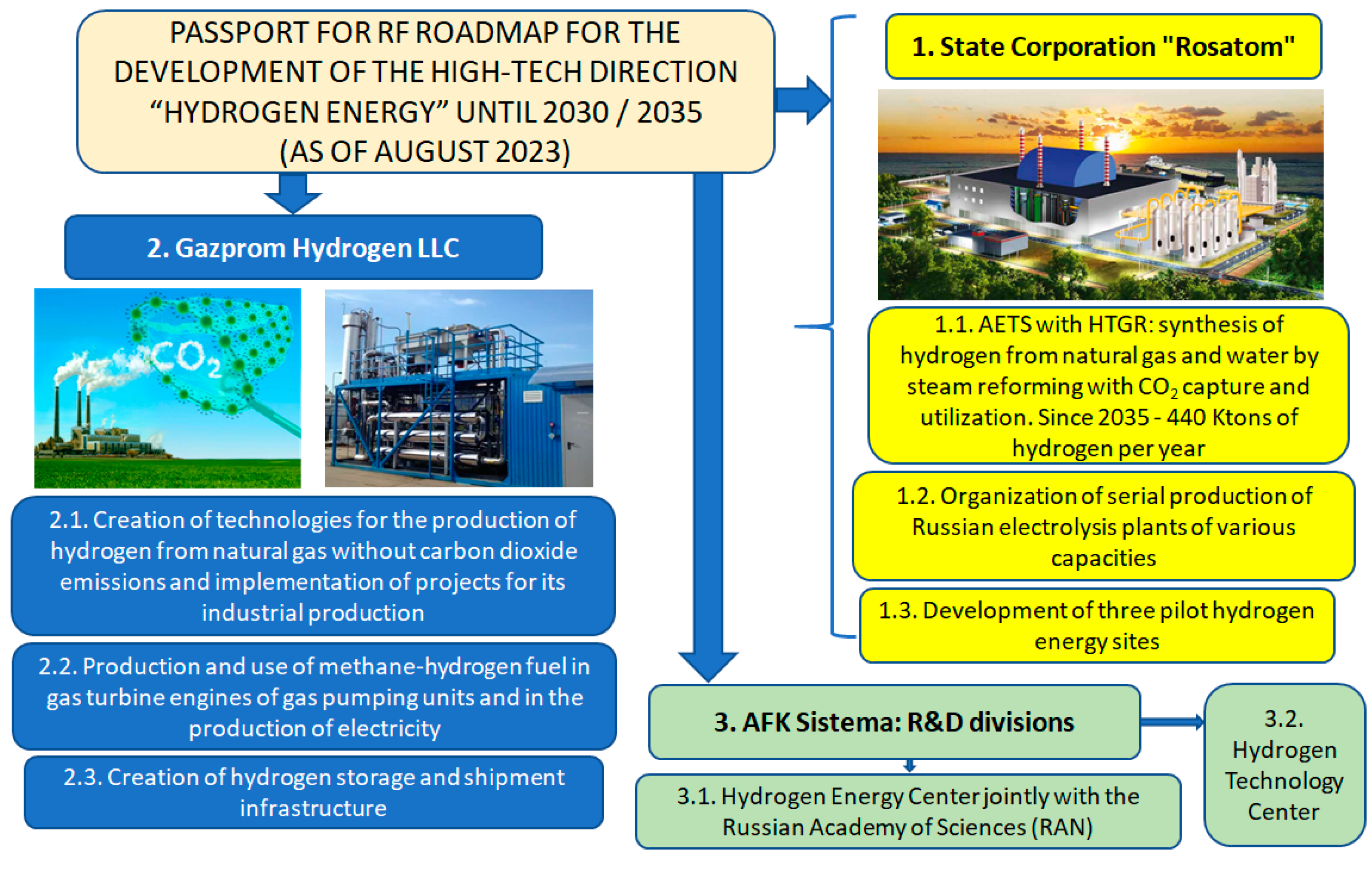

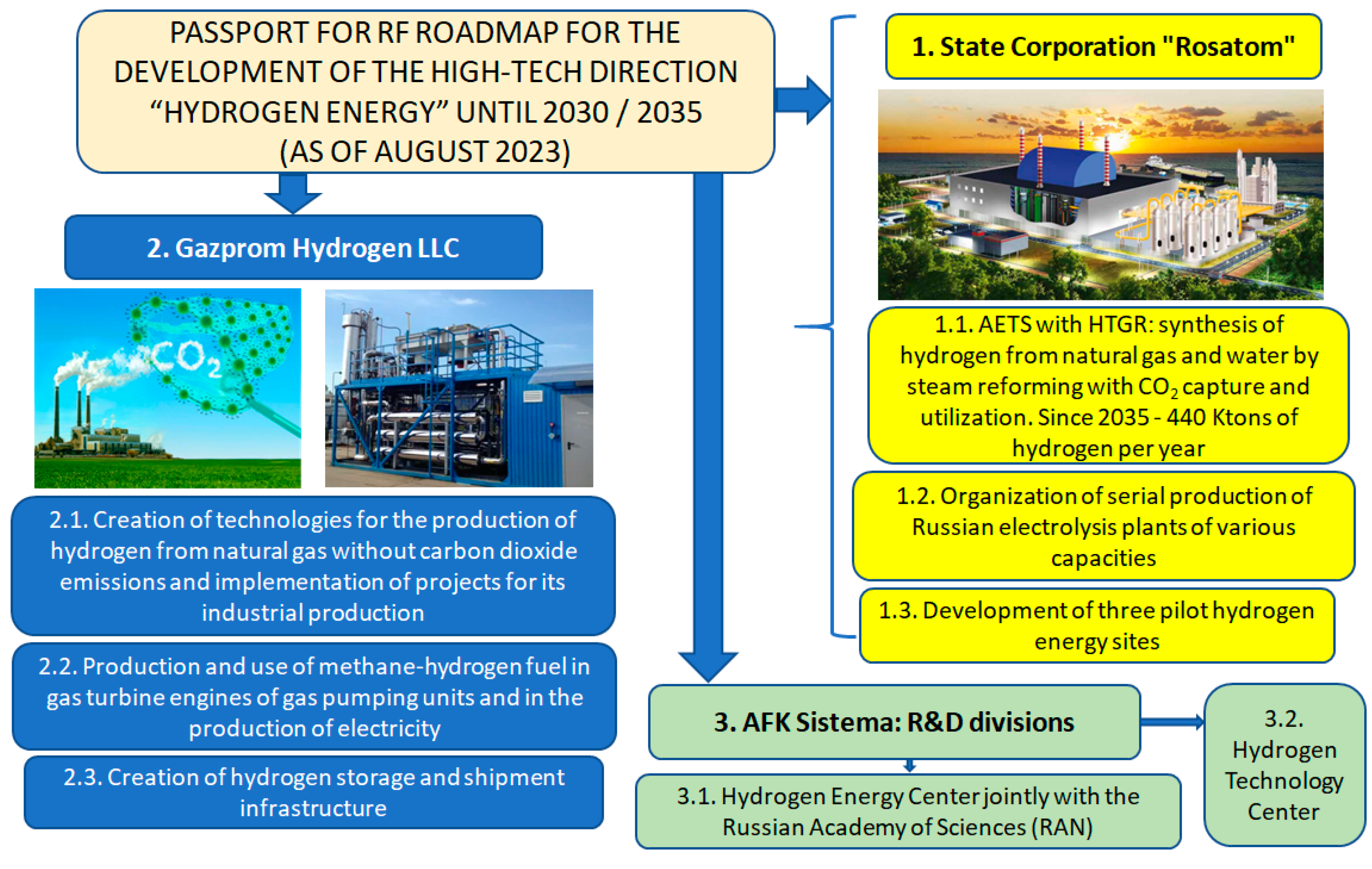

4.2. Development of Hydrogen Energy in Russia

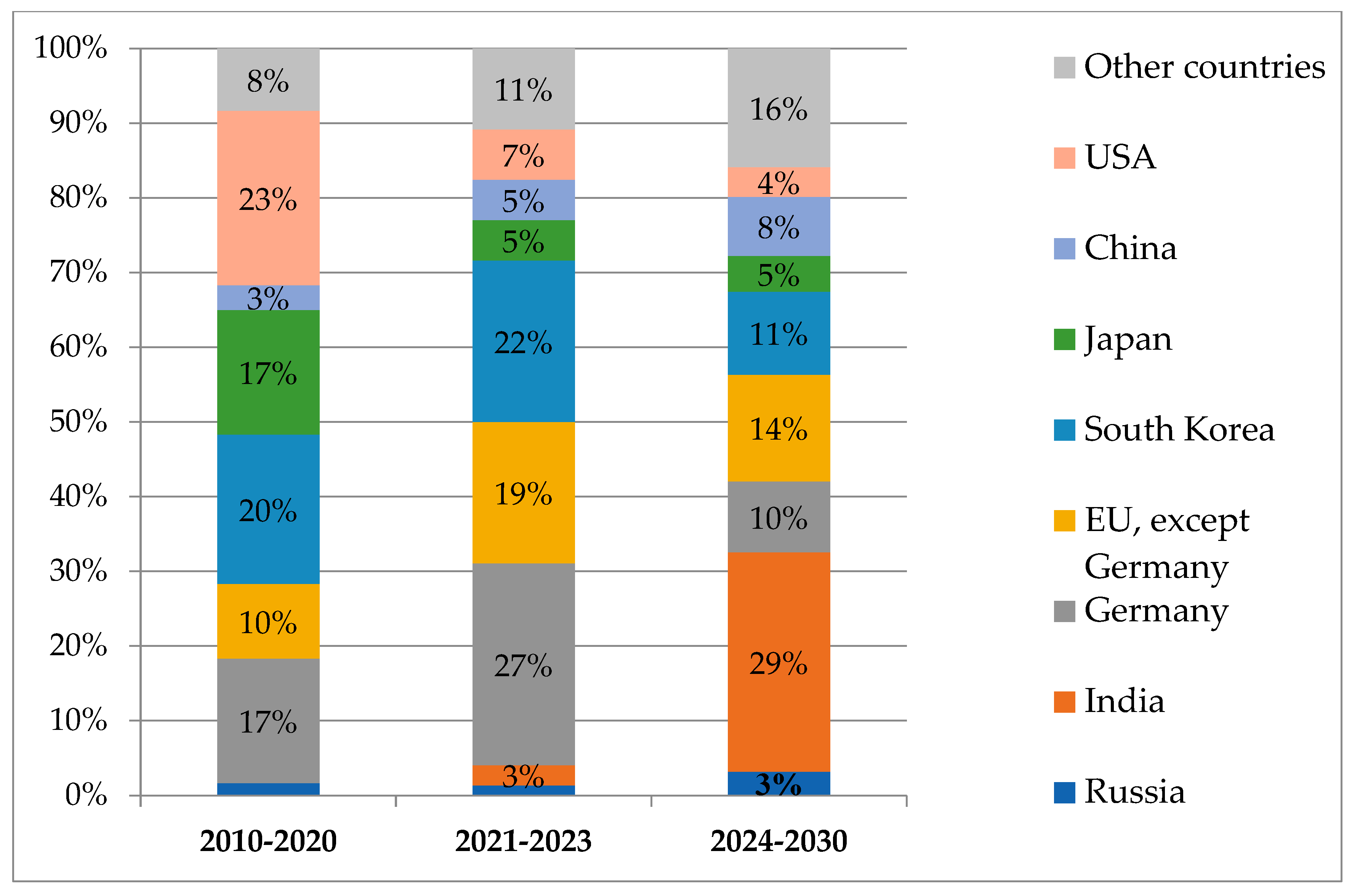

4.3. Estimation of Investments in the Development of Hydrogen Energy and Hydrogen Transport

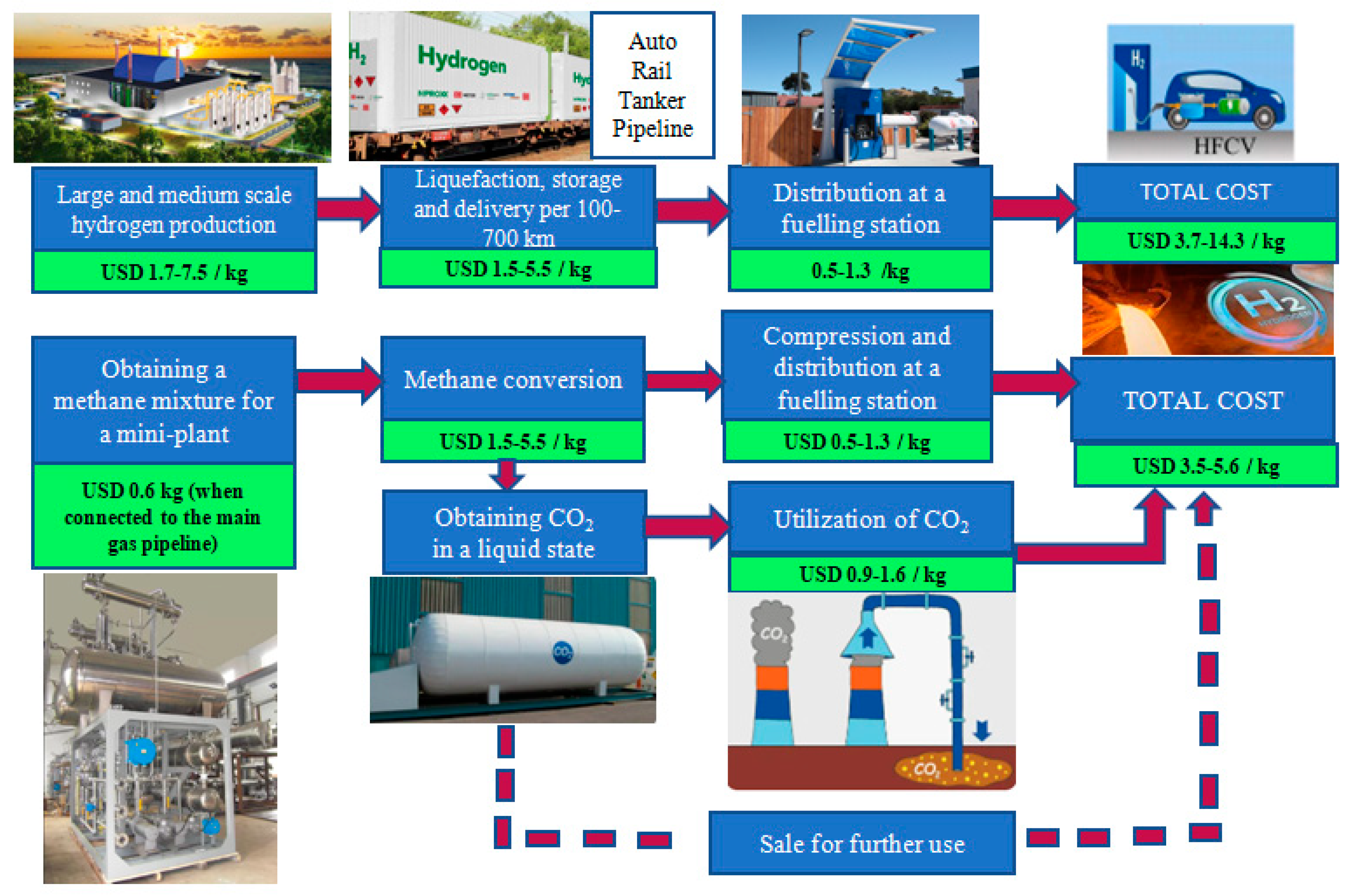

5. Major Technological Solutions for Hydrogen Energy in Russia until 2030

- Hydrogen production in a plant at the “regional level”, with subsequent delivery of fuel to filling stations in a liquefied or compressed state;

- Technological solutions for the storage and transportation of hydrogen fuel;

- Samples of trucks and buses powered by hydrogen fuel cells submitted by Kamaz PJSC, GAZ Group and other minor car manufacturers;

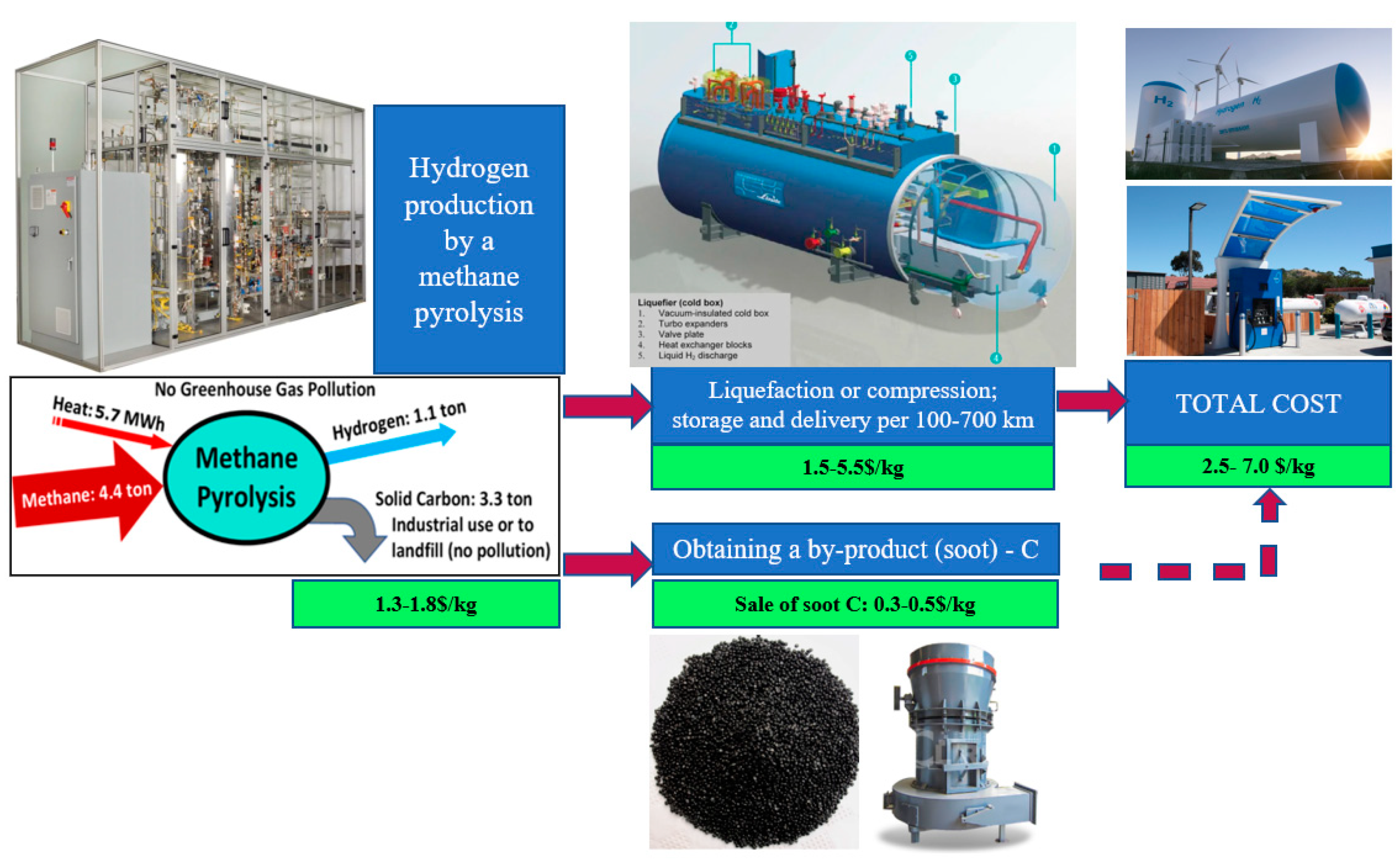

- Implemented pilot projects using methane conversion and pyrolysis methods with the possibility of capturing CO2 for plants for the synthesis of “turquoise” hydrogen (from natural gas) at small and medium scales.

- The launch of the serial production of models of passenger and freight vehicles, including railroad ones, using compressed hydrogen as fuel (it is advisable to use the current standards of 35 and 70 MPa). Notably, according to the conclusions of the IWG, in the car and truck sectors, as well as railway transport, hydrogen transport will not reach economic parity with current technologies until 2030 [116].

- The adaptation of technological solutions for equipment for the storage and transportation of hydrogen from large- and medium-scale production sites.

- The creation of a network of “turquoise” hydrogen mini-factories based on the existing gas filling infrastructure and medium-scale plants based on methane conversion and pyrolysis methods, including those that capture or neutralize CO2 emissions.

- The creation of domestic analogs or the purchase of Chinese equipment for filling stations.

6. Provisions

7. Conclusions

- ✓

- The most promising method to realize hydrogen energy use by 2030 in Russia and some countries rich in gas mineral resources seems to be the adaptation of existing technological solutions for storage and transportation equipment from large- and medium-scale hydrogen synthesis sites and the creation of a network of “turquoise” hydrogen mini-factories based on the existing gas filling infrastructure, as described in [22], and medium-scale plants based on methane conversion and pyrolysis methods, including those that capture or neutralize CO2 emissions.

- ✓

- The use of natural gas as a primary raw material for the development of hydrogen energy technologies in Russia for the period up to 2030 makes it necessary to develop appropriate technologies for its storage and transportation. The early formation of regional and sectoral priorities for the use of hydrogen as a fuel or energy raw material for energy-intensive technological processes in Russia may contribute to the reorientation of the supply of some of the natural gas to hydrogen generators in the coming years.

- ✓

- In the event of a decrease in the volume of shipments of pipeline gas and LNG to traditional markets abroad, it is expedient to ensure the possibility of using the resulting “surplus” in the territory of the country. Hydrogen technologies in transport and metallurgy can at least partly act as a rational direction for such purposes in the coming years.

- ✓

- The inevitable quality changes in natural resource and gas grid use in the prospective hydrogen technology expansion in Russia will affect science, technology, standardization, certification, accreditation and some other issues.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Dvoynikov, M.V.; Buslaev, G.V.; Kunshin, A.A.; Sidorov, D.A.; Budovskaya, M.E. New Concepts of Hydrogen Production and Storage in Arctic Region. Resources 2021, 10, 3. [Google Scholar] [CrossRef]

- Tcvetkov, P.S.; Cherepovitsyn, A.E.; Fedoseev, S.V. The Changing Role of CO2 in the Transition to a Circular Economy: Review of Carbon Sequestration Projects. Sustainability 2019, 11, 5834. [Google Scholar] [CrossRef]

- Litvinenko, V.S.; Tsvetkov, P.S.; Dvoynikov, M.V.; Buslaev, G.V. Barriers to implementation of hydrogen initiatives in the context of global energy sustainable development. J. Min. Inst. 2021, 244, 428–438. [Google Scholar] [CrossRef]

- Bezyk, Y.; Sówka, I.; Górka, M. Assessment of urban CO2 budget: Anthropogenic and biogenic inputs. Urban Clim. 2021, 39, 100949. [Google Scholar] [CrossRef]

- Cordroch, L.; Hilpert, S.; Wiese, F. Why renewables and energy efficiency are not enough—The relevance of sufficiency in the heating sector for limiting global warming to 1.5 °C. Technol. Forecast. Soc. Chang. 2022, 175, 121313. [Google Scholar] [CrossRef]

- IEA. Global Hydrogen Review. 2023. 176p. Available online: https://iea.blob.core.windows.net/assets/8d434960-a85c-4c02-ad96-77794aaa175d/GlobalHydrogenReview2023.pdf (accessed on 5 October 2023).

- Mastepanov, A. Hydrogen energy in Russia: Status and prospects. Energeticheskaya Polit. [Energy Policy] 2020, 12, 54–65. (In Russian) [Google Scholar] [CrossRef]

- World Energy Council. Hydrogen on the Horizon: National Hydrogen Strategies. 2021. Available online: https://www.worldenergy.org/publications/entry/working-paper-hydrogen-on-thehorizon-national-hydrogen-strategies (accessed on 5 October 2023).

- Ashari, P.A.; Blind, K.; Koch, C. Knowledge and technology transfer via publications, patents, standards: Exploring the hydrogen technological innovation system. Technol. Forecast. Soc. Chang. 2022, 187, 122201. [Google Scholar] [CrossRef]

- Ishimoto, Y.; Wulf, C.; Kuckshinrichs, W. Life cycle costing approaches of fuel cell and hydrogen systems: A literature review. Int. J. Hydrogen Energy 2023, in press. [CrossRef]

- Khan, T.; Yu, M.; Waseem, M. Review on recent optimization strategies for hybrid renewable energy system with hydrogen technologies: State of the art, trends and future directions. Int. J. Hydrogen Energy 2022, 47, 25155–25201. [Google Scholar] [CrossRef]

- Abu, S.M.; Hannan, M.; Ker, P.J.; Mansor, M.; Tiong, S.K.; Mahlia, T.I. Recent progress in electrolyser control technologies for hydrogen energy production: A patent landscape analysis and technology updates. J. Energy Storage 2023, 72, 108773. [Google Scholar] [CrossRef]

- Pérez-Vigueras, M.; Sotelo-Boyás, R.; González-Huerta, R.d.G.; Bañuelos-Ruedas, F. Feasibility analysis of green hydrogen production from oceanic energy. Heliyon 2023, 9, e20046. [Google Scholar] [CrossRef] [PubMed]

- Han, D.G.; Erdem, K.; Midilli, A. Investigation of hydrogen production via waste plastic gasification in a fluidized bed reactor using Aspen Plus. Int. J. Hydrogen Energy, 2023; in press. [Google Scholar] [CrossRef]

- Li, R.; Cao, J.; Xie, Y. Perovskite oxides successfully catalyze the electrolytic hydrogen production from oilfield wastewater. Int. J. Hydrogen Energy 2023, 48, 28061–28069. [Google Scholar] [CrossRef]

- Rubio, F.; Llopis-Albert, C.; Besa, A.J. Optimal allocation of energy sources in hydrogen production for sustainable deployment of electric vehicles. Technol. Forecast. Soc. Chang. 2023, 188, 122290. [Google Scholar] [CrossRef]

- Anticaglia, A.; Balduzzi, F.; Ferrara, G.; De Luca, M.; Carpentiero, D.; Fabbri, A.; Fazzini, L. Feasibility analysis of a direct injection H2 internal combustion engine: Numerical assessment and proof-of-concept. Int. J. Hydrogen Energy 2023, 48, 32553–32571. [Google Scholar] [CrossRef]

- Carayannis, E.G.; Ilinova, A.A.; Cherepovitsyn, A.E. The Future of Energy and the Case of the Arctic Offshore: The Role of Strategic Management. J. Mar. Sci. Eng. 2021, 9, 134. Available online: https://www.mdpi.com/2077-1312/9/2/134 (accessed on 5 October 2023). [CrossRef]

- Ilyushin, Y.V. Development of a Process Control System for the Production of High-Paraffin Oil. Energies 2022, 15, 6462. [Google Scholar] [CrossRef]

- AlHumaidan, F.S.; Halabi, M.A.; Vinoba, M. Blue hydrogen: Current status and future technologies. Energy Convers. Manag. 2023, 283, 116840. [Google Scholar] [CrossRef]

- Council, H. Hydrogen Decarbonization Pathways. A Life-Cycle Assessment. Hydrogen Council. 2021. 22p. Available online: https://hydrogencouncil.com/wp-content/uploads/2021/01/Hydrogen-Council-Report_DecarbonizationPathways_Part-1-Lifecycle-Assessment.pdf (accessed on 5 October 2023).

- Kotek, P.; Tóth, T.B.; Selei, A. Designing a future-proof gas and hydrogen infrastructure for Europe—A modelling-based approach. Energy Policy 2023, 180, 113641. [Google Scholar] [CrossRef]

- Bui, M.; Sunny, N.; Mac Dowell, N. The prospects of flexible natural gas-fired CCGT within a green taxonomy. iScience 2023, 26, 107382. [Google Scholar] [CrossRef]

- Bhattacharyya, R. Enabling the clean energy transition: An assessment of the role of sustainable and green finance taxonomies. Ref. Modul. Soc. Sci. 2023, in press. [CrossRef]

- Larin, V.N. Hypothesis of the Originally Hydride Earth; Nedra publishing: Moscow, Russia, 1980; 216p. (In Russian) [Google Scholar]

- Zagashvili, Y.; Kuzmin, A.; Buslaev, G.; Morenov, V. Small-scaled production of blue hydrogen with reduced carbon footprint. Energies 2021, 14, 5194. [Google Scholar] [CrossRef]

- Yang, Y.; Xu, H.; Lu, Q.; Bao, W.; Lin, L.; Ai, B.; Zhang, B. Development of Standards for Hydrogen Storage and Transportation. E3S Web Conf. 2020, 194, 02018. [Google Scholar] [CrossRef]

- Langmi, H.W.; Engelbrecht, N.; Modisha, P.M.; Bessarabov, D. Hydrogen Storage. In Electrochemical Power Sources: Fundamentals, Systems, and Applications; Chapter 13—Hydrogen storage. Hydrogen Production by Water Electrolysis; Elsevier: Amsterdam, The Netherlands, 2022; pp. 455–486. [Google Scholar] [CrossRef]

- AlZohbi, G.; Almoaikel, A.; AlShuhail, L. An overview on the technologies used to store hydrogen. Energy Rep. 2023, 9, 28–34. [Google Scholar] [CrossRef]

- Molaeimanesh, G.R.; Torabi, F. Chapter 4—Hydrogen Storage Systems. In Fuel Cell Modeling and Simulation: From Microscale to Macroscale; Elsevier: Amsterdam, The Netherlands, 2023; pp. 269–282. [Google Scholar] [CrossRef]

- Abreu, J.F.; Costa, A.M.; Costa, P.V.; Miranda, A.C.; Zheng, Z.; Wang, P.; Goulart, M.B.; Bergsten, A.; Ebecken, N.F.; Bittencourt, C.H.; et al. Large-scale storage of hydrogen in salt caverns for carbon footprint reduction. Int. J. Hydrogen Energy 2023, 48, 14348–14362. [Google Scholar] [CrossRef]

- Abreu, J.F.; Costa, A.M.; Costa, P.V.; Miranda, A.C.; Zheng, Z.; Wang, P.; Ebecken, N.F.; de Carvalho, R.S.; dos Santos, P.L.; Lins, N.; et al. Carbon net zero transition: A case study of hydrogen storage in offshore salt cavern. J. Energy Storage 2023, 62, 106818. [Google Scholar] [CrossRef]

- Zhu, S.; Shi, X.; Yang, C.; Li, Y.; Li, H.; Yang, K.; Wei, X.; Bai, W.; Liu, X. Hydrogen loss of salt cavern hydrogen storage. Renew. Energy 2023, 218, 119267. [Google Scholar] [CrossRef]

- El-Eskandarany, M.S. Chapter 9—Solid-State Hydrogen Storage Nanomaterials for Fuel Cell Applications. Energy Storage Prot. Coat. Med. Appl. 2020, 1, 229–261. [Google Scholar] [CrossRef]

- Desai, F.J.; Uddin, M.N.; Rahman, M.M.; Asmatulu, R. A critical review on improving hydrogen storage properties of metal hydride via nanostructuring and integrating carbonaceous materials. Int. J. Hydrogen Energy 2023, 48, 29256–29294. [Google Scholar] [CrossRef]

- Tang, D.; Tan, G.-L.; Li, G.-W.; Liang, J.-G.; Ahmad, S.M.; Bahadur, A.; Humayun, M.; Ullah, H.; Khan, A.; Bououdina, M. State-of-the-art hydrogen generation techniques and storage methods: A critical review. J. Energy Storage 2023, 64, 107196. [Google Scholar] [CrossRef]

- Plötz, P. Hydrogen technology is unlikely to play a major role in sustainable road transport. Nat. Electron. 2022, 5, 8–10. [Google Scholar] [CrossRef]

- IEA. Energy Technology Perspectives, Technology Roadmap: Hydrogen and Fuel Cells; IEA: Paris, France, 2015; 80p. [Google Scholar] [CrossRef]

- IEA. Energy Technology Perspectives 2020; IEA: Paris, France; 400p, Available online: https://iea.blob.core.windows.net/assets/7f8aed40-89af-4348-be19-c8a67df0b9ea/Energy_Technology_Perspectives_2020_PDF.pdf (accessed on 5 October 2023).

- IEA (April 2021), Global Hydrogen Review 2021. 224p. Available online: https://iea.blob.core.windows.net/assets/3a2ed84c-9ea0-458c-9421-d166a9510bc0/GlobalHydrogenReview2021.pdf (accessed on 5 October 2023).

- Bicer, Y.; Khalid, F. Life cycle environmental impact comparison of solid oxide fuel cells fueled by natural gas, hydrogen, ammonia and methanol for combined heat and power generation. Int. J. Hydrogen Energy 2020, 45, 3670–3685. [Google Scholar] [CrossRef]

- Zhang, W.; Fang, X.; Sun, C. The alternative path for fossil oil: Electric vehicles or hydrogen fuel cell vehicles? J. Environ. Manag. 2023, 341, 118019. [Google Scholar] [CrossRef] [PubMed]

- Park, C.; Lim, S.; Shin, J.; Lee, C.-Y. How much hydrogen should be supplied in the transportation market? Focusing on hydrogen fuel cell vehicle demand in South Korea: Hydrogen demand and fuel cell vehicles in South Korea. Technol. Forecast. Soc. Chang. 2022, 181, 121850. [Google Scholar] [CrossRef]

- IEA. Global Hydrogen Review 2022. 284p. Available online: https://iea.blob.core.windows.net/assets/c5bc75b1-9e4d-460d-9056-6e8e626a11c4/GlobalHydrogenReview2022.pdf (accessed on 5 October 2023).

- World Energy Council (WEC). Working Paper: Hydrogen on the Horizon: National Hydrogen Strategies, (September 2021). Available online: https://www.worldenergy.org/assets/downloads/Working_Paper_-_National_Hydrogen_Strategies_-_September_2021.pdf (accessed on 5 October 2023).

- U.S. Department of Energy Hydrogen Program. Available online: https://www.hydrogen.energy.gov/ (accessed on 5 October 2023).

- European Commission. EUR 21241—European Hydrogen and Fuel Cell Projects; Office for Official Publications of the European Communities: Luxembourg, 2004; 66p. [Google Scholar]

- FCHJU. Hydrogen Roadmap Europe: A sustainable pathway for the European Energy Transition. Available online: https://www.fch.europa.eu/news/hydrogenroadmap-europe-sustainable-pathway-european-energy-transition (accessed on 5 October 2023).

- A Hydrogen Strategy for a Climate-Neutral Europe. Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions. Brussels, 8.7.2020. COM. 2020. № 301. 23p. Available online: http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=CELEX:52012DC0673:EN:NOT (accessed on 5 October 2023).

- Sustainable and Smart Mobility Strategy—Putting European Transport on Track for the Future COM/2020/789 Final. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A52020DC0789 (accessed on 5 October 2023).

- Hydrogen Energy in Russia and Europe: Market Prospects for $700 Billion. Available online: https://trends.rbc.ru/trends/green/5ef46e379a7947a89c25170d (accessed on 23 September 2023). (In Russian).

- Press Release on the Official Website of the Ministry of Economy and Energy of Germany Dated 17 October 2019. Available online: https://www.bmvi.de/SharedDocs/DE/Pressemitteilungen/2019/079-scheuer-nip-wasserstoff.html (accessed on 23 September 2023). (In German).

- Gils, H.C.; Gardian, H.; Schmugge, J. Interaction of hydrogen infrastructures with other sector coupling options towards a zero-emission energy system in Germany. Renew. Energy 2021, 180, 140–156. [Google Scholar] [CrossRef]

- Ministries of Economy and Transport of the North German Coastal States. Bremen, Hamburg, Mecklenburg-Western Pomerania, Lower Saxony and Schleswig-Holstein. Hydrogen strategy for North Germany. 7 November 2019; European Economic and Social Committee and the Committee of the Regions: Brussels, Belgium; Available online: http://carbonneutralcities.org/wp-content/uploads/2020/02/North-German-Hydrogen-Strategy.pdf (accessed on 5 October 2023).

- Bakhtina, O. Quantum Leap. Germany Adopts National Hydrogen Strategy. Available online: https://neftegaz.ru/news/ecology/553728-kvantovyy-skachok-germaniya-prinyala-natsionalnuyu-vodorodnuyu (accessed on 23 September 2023). (In Russian).

- U.S. Department of Energy. Office of Fossil Energy. July 2020. «Hydrogen Strategy—Enabling a Low-Carbon Economy». Available online: https://www.energy.gov/fecm/articles/hydrogen-strategy-enabling-low-carbon-economy (accessed on 5 October 2023).

- Mallapragada, D.S.; Gençer, E.; Insinger, P.; Keith, D.W.; O’sullivan, F.M. Can Industrial-Scale Solar Hydrogen Supplied from Commodity Technologies Be Cost Competitive by 2030? Cell Rep. Phys. Sci. 2020, 1, 100174. [Google Scholar] [CrossRef]

- Makaryan, I.A.; Sedov, I.V. Evaluation of the economic efficiency of the scale of hydrogen production by various methods. Russ. Chem. J. 2021, LXV, 62–76. [Google Scholar]

- Kopteva, A.; Kalimullin, L.; Tcvetkov, P.; Soares, A. Prospects and Obstacles for Green Hydrogen Production in Russia. Energies 2021, 14, 718. [Google Scholar] [CrossRef]

- Kumar, P.; Prasad, S.B.; Patel, D.; Kumar, K.; Dixit, S.; Nikolaevna, S.N. Optimization of cycle time assembly line for mass manufacturing. Int. J. Interact. Des. Manuf. 2023. [Google Scholar] [CrossRef]

- Multi-State ZEV Action Plan. Accelerating the Adoption of Zero Emission Vehicles 2018–2021. Available online: https://portal.ct.gov/-/media0/DEEP/air/mobile/EVConnecticut/2018---Multi-State-ZEV-Task-Force-Action-Plan.pdf (accessed on 23 July 2023).

- Iida, S.; Sakata, K. Hydrogen technologies and developments in Japan. Clean Energy. 2019, 3, 105–113. [Google Scholar] [CrossRef]

- Khan, U.; Yamamoto, T.; Sato, H. Consumer preferences for hydrogen fuel cell vehicles in Japan. Transp. Res. Part D Transp. Environ. 2020, 87, 102542. [Google Scholar] [CrossRef]

- Khan, U.; Yamamoto, T.; Sato, H. Understanding attitudes of hydrogen fuel-cell vehicle adopters in Japan. Int. J. Hydrogen Energy 2021, 46, 30698–30717. [Google Scholar] [CrossRef]

- METI (Minister of Economy, Trade and Industry of Japan), Ministerial Council on Renewable Energy, Hydrogen and Related Issues. Basic Hydrogen Strategy Determined. 2017. Available online: https://www.meti.go.jp/english/press/2017/1226_003.html (accessed on 5 October 2023).

- METI. Strategic Roadmap for Hydrogen and Fuel Cells. 2019. Available online: www.meti.go.jp/english/press/2019/pdf/0312_002a.pdf (accessed on 5 October 2023).

- Wang, J.; Matsumoto, S. Can subsidy programs lead consumers to select «greener» products?: Evidence from the Eco-car program in Japan. Res. Transp. Econ. 2021, 91, 101066. [Google Scholar] [CrossRef]

- Makwana, M.; Patel, A.M.; Oza, A.D.; Prakash, C.; Gupta, L.R.; Vatin, N.I.; Dixit, S. Effect of Mass on the Dynamic Characteristics of Single- and Double-Layered Graphene-Based Nano Resonators. Materials 2022, 15, 5551. [Google Scholar] [CrossRef] [PubMed]

- Ohno, T.; Nishida, Y.; Ishihara, T.; Hirose, A. Re-Examining Japan’s Hydrogen Strategy. Moving beyond the “Hydrogen Society” Fantasy (Sept. 2022). 25p. Available online: https://www.renewable-ei.org/pdfdownload/activities/REI_JapanHydrogenStrategy_EN_202209.pdf (accessed on 5 October 2023).

- Ishihara, T.; Ohno, T. Revised Basic Hydrogen Strategy Offers. No Clear Path to Carbon Neutrality (June 2023). 13p. Available online: https://www.renewable-ei.org/pdfdownload/activities/REI_Hydrogen_PositionPaper_2023_EN.pdf (accessed on 5 October 2023).

- Stangarone, T. South Korean efforts to transition to a hydrogen economy. Clean Technol. Environ. Policy 2021, 23, 509–516. [Google Scholar] [CrossRef]

- Lee, J.-H.; Woo, J. Green New Deal Policy of South Korea: Policy Innovation for a Sustainability Transition. Sustainability 2020, 12, 10191. [Google Scholar] [CrossRef]

- Ulsan Strives to Become Global Hydrogen Leader. Available online: https://www.koreaherald.com/view.php?ud=20181022000747 (accessed on 23 July 2023).

- Lee, Y.; Seo, I. Sustainability of a Policy Instrument: Rethinking the Renewable Portfolio Standard in South Korea. Sustainability 2019, 11, 3082. [Google Scholar] [CrossRef]

- Ministry of Trade, Industry and Energy of Korea. Hydrogen Economy Roadmap, 2019–2040. Available online: https://www.motie.go.kr/common/download.do?fid=bbs&bbs_cd_n=81&bbs_seq_n=161262&file_seq_n=2 (accessed on 5 October 2023).

- Kim, Y.; Yi, E.; Son, H. Russia’s Policy Transition to a Hydrogen Economy and the Implications of South Korea–Russia Cooperation. Energies 2022, 15, 127. [Google Scholar] [CrossRef]

- Upadhyay, G.; Saxena, K.K.; Sehgal, S.; Mohammed, K.A.; Prakash, C.; Dixit, S.; Buddhi, D. Development of Carbon Nanotube (CNT)-Reinforced Mg Alloys: Fabrication Routes and Mechanical Properties. Metals 2022, 12, 1392. [Google Scholar] [CrossRef]

- Lee, Y.; Lee, M.C.; Kim, Y.J. Barriers and strategies of hydrogen fuel cell power generation based on expert survey in South Korea. Int. J. Hydrogen Energy 2022, 47, 5709–5719. [Google Scholar] [CrossRef]

- Hyundai Motors Group Press Release. Available online: https://www.hyundai.news/eu/brand/hyundai-motor-group-reveals-fcev-vision-2030 (accessed on 5 October 2023).

- Matulucci, C. The Hydrogen Stream: South Korea Launching Hydrogen Bidding Market (13 June 2023). Available online: https://www.pv-magazine.com/2023/06/13/the-hydrogen-stream-south-korea-launching-hydrogen-bidding-market/ (accessed on 5 October 2023).

- Ren, X.; Dong, L.; Xu, D.; Hu, B. Challenges towards hydrogen economy in China. Int. J. Hydrogen Energy 2020, 45, 34326–34345. [Google Scholar] [CrossRef]

- He, J.; Li, Z.; Zhang, X.; Wang, H.; Dong, W.; Chang, S.; Ou, X.; Guo, S.; Tian, X.; Gu, A.; et al. Comprehensive report on China’s Long-Term Low-Carbon Development Strategies and Pathways. Chin. J. Popul. Resour. Environ. 2020, 18, 263–295. [Google Scholar] [CrossRef]

- Zhao, F.; Mu, Z.; Hao, H.; Liu, Z.; He, X.; Victor Przesmitzki, S.; Ahmad Amer, A. Hydrogen Fuel Cell Vehicle Development in China: An Industry Chain Perspective. Energy Technol. 2020, 8, 2000179. [Google Scholar] [CrossRef]

- Shan, W.; Wang, F.-F. Challenges and Policy Suggestions on the Development of Hydrogen Economy in China. E3S Web Conf. 2020, 155, 01011. [Google Scholar] [CrossRef]

- Liu, Z.; Kendall, K.; Yan, X. China Progress on Renewable Energy Vehicles: Fuel Cells, Hydrogen and Battery Hybrid Vehicles. Energies 2019, 12, 54. [Google Scholar] [CrossRef]

- Li, F. Marks End of Support for Fuel Cell Cars. China Daily, (14 October 2019). 2020. Available online: http://global.chinadaily.com.cn/a/201910/14/WS5da406a7a310cf3e355705d5.html (accessed on 5 October 2023).

- Collins, L. China’s Green Hydrogen Boom (31 March 2023). Available online: https://www.hydrogeninsight.com/electrolysers/china-s-green-hydrogen-boom-domestic-electrolyser-demand-will-grow-from-more-than-2gw-this-year-to-40gw-in-2028/2-1-1429420 (accessed on 5 October 2023).

- Momade, M.H.; Durdyev, S.; Dixit, S.; Shahid, S.; Alkali, A.K. Modeling labor costs using artificial intelligence tools. Int. J. Build. Pathol. Adapt. 2022, in press. [Google Scholar] [CrossRef]

- Ediger, V.Ş.; Bowlus, J.V.; Dursun, A.F. State capitalism and hydrocarbon security in China and Russia. Energy Strategy Rev. 2021, 38, 100725. [Google Scholar] [CrossRef]

- Li, Y.; Taghizadeh-Hesary, F. The economic feasibility of green hydrogen and fuel cell electric vehicles for road transport in China. Energy Policy 2022, 160, 112703. [Google Scholar] [CrossRef]

- Mao, S.; Zhang, Y.; Bieker, G.; Rodriguez, F. Zero-emission bus and truck market in China: A 2021 update. Work. Pap. Int. Counc. Clean Transp. 2023, 4. Available online: https://theicct.org/wp-content/uploads/2023/01/china-hvs-ze-bus-truck-market-2021-jan23.pdf (accessed on 5 October 2023).

- Moon, S.; Kim, K.; Seung, H.; Kim, J. Strategic analysis on effects of technologies, government policies, and consumer perceptions on diffusion of hydrogen fuel cell vehicles. Energy Econ. 2022, 115, 106382. [Google Scholar] [CrossRef]

- Raab, M.; Maier, S.; Dietrich, R.-U. Comparative techno-economic assessment of a large-scale hydrogen transport via liquid transport media. Int. J. Hydrogen Energy 2021, 46, 11956–11968. [Google Scholar] [CrossRef]

- Litvinenko, V.S.; Dvoynikov, M.V.; Trushko, V.L. Elaboration of a conceptual solution for the development of the Arctic shelf from seasonally flooded coastal areas. Int. J. Min. Sci. Technol. 2021, 32, 113–119. [Google Scholar] [CrossRef]

- Harichandan, S.; Kar, S.K.; Bansal, R.; Mishra, S.K. Achieving sustainable development goals through adoption of hydrogen fuel cell vehicles in India: An empirical analysis. Int. J. Hydrogen Energy 2022, 48, 4845–4859. [Google Scholar] [CrossRef]

- Harichandan, S.; Kar, S.K.; Rai, P.K. A systematic and critical review of green hydrogen economy in India. Int. J. Hydrogen Energy 2023, 48, 31425–31442. [Google Scholar] [CrossRef]

- Singh, R.K.; Nayak, N.P. DIVE method integration for techno-economic analysis of hydrogen production techniques in India. Mater. Today Proc. 2023, in press. [CrossRef]

- Qureshi, F.; Yusuf, M.; Kamyab, H.; Zaidi, S.; Khalil, M.J.; Khan, M.A.; Alam, M.A.; Masood, F.; Bazli, L.; Chelliapan, S.; et al. Current trends in hydrogen production, storage and applications in India: A review. Sustain. Energy Technol. Assess. 2022, 53, 102677. [Google Scholar] [CrossRef]

- Litvinenko, V.S.; Petrov, E.I.; Vasilevskaya, D.V.; Yakovenko, A.V.; Naumov, I.A.; Ratnikov, M.A. Assessment of the role of the state in the management of mineral resources. J. Min. Inst. 2023, 259, 95–111. [Google Scholar] [CrossRef]

- Skobelev, D.O.; Cherepovitsyna, A.A.; Guseva, T.V. Carbon capture and storage: Net zero contribution and cost estimation approaches. J. Min. Inst. 2023, 259, 125–140. [Google Scholar] [CrossRef]

- Matrokhina, K.V.; Trofimets, V.Y.; Mazakov, E.B.; Makhovikov, A.B.; Khaykin, M.M. Development of methodology for scenario analysis of investment projects of enterprises of the mineral resource complex. J. Min. Inst. 2023, 259, 112–124. [Google Scholar] [CrossRef]

- Apostolou, D.; Xydis, G. A literature review on hydrogen refuelling stations and infrastructure: Current status and future prospects. Renew. Sustain. Energy Rev. 2019, 113, 109292. [Google Scholar] [CrossRef]

- Bolobov, V.I.; Latipov, I.U.; Popov, G.G.; Buslaev, G.V.; Martynenko, Y.V. Estimation of the influence of compressed hydrogen on the mechanical properties of pipeline steels. Energies 2021, 14, 6085. [Google Scholar] [CrossRef]

- H2station Map. Available online: https://www.h2stations.org/stations-map/?lat=49.139384&lng=11.190114&zoom=2 (accessed on 15 September 2023).

- IEA. Fuel Cell Electric Vehicle Stock by Segment; by Region. 2017–2020. IEA. Paris. Available online: https://www.iea.org/reports/hydrogen (accessed on 15 September 2023).

- Yurin, V.E.; Egorov, A.N. Predictive economic efficiency of combining nuclear power plants with autonomous hydrogen power complex. Int. J. Hydrogen Energy 2021, 46, 32350–32357. [Google Scholar] [CrossRef]

- Zhiznin, S.Z.; Timokhov, V.M.; Gusev, A.L. Economic aspects of nuclear and hydrogen energy in the world and Russia. Int. J. Hydrogen Energy 2020, 45, 31353–31366. [Google Scholar] [CrossRef]

- Romanova, T. Russia’s political discourse on the EU’s energy transition (2014–2019) and its effect on EU-Russia energy relations. Energy Policy 2021, 154, 112309. [Google Scholar] [CrossRef]

- Buslaev, G.; Tsvetkov, P.; Lavrik, A.; Kunshin, A.; Loseva, E.; Sidorov, D. Ensuring the Sustainability of Arctic Industrial Facilities under Conditions of Global Climate Change. Resources 2021, 10, 128. [Google Scholar] [CrossRef]

- Shulga, R.N.; Petrov, A.Y.; Putilova, I.V. The Arctic: Ecology and hydrogen energy. Int. J. Hydrogen Energy 2020, 45, 7185–7198. [Google Scholar] [CrossRef]

- Temiz, M.; Dincer, I. A unique ocean and solar based multigenerational system with hydrogen production and thermal energy storage for Arctic communities. Energy 2021, 239, 122126. [Google Scholar] [CrossRef]

- Konoplev, V.; Sarbaev, V.; Melnikov, Z. The main aspects of safety of hydrogen energy in relation to the motor transport process on gas engine fuels. Transp. Res. Procedia 2018, 36, 295–302. [Google Scholar] [CrossRef]

- Filippov, S.P.; Golodnitsky, A.E.; Kashin, A.M. Fuel cells and hydrogen energy. Energeticheskaya Politika [Energy Policy] 2020, 11, 28–39. (In Russian) [Google Scholar] [CrossRef]

- Hydrogen Economy—The Path to Low-Carbon Development. M: Energy Center of the Moscow School of Management SKOLKOVO. 2019. 63p. Available online: https://energy.skolkovo.ru/downloads/documents/SEneC/Research/SKOLKOVO_EneC_Hydrogen-economy_Rus.pdf (accessed on 5 October 2023). (In Russian).

- Arutyunov, V.S.; Strekova, L.N. The Potential of Hydrogen Energy and Possible Consequences of Its Implementation. Neftegazokhimiya 2021, 1, 8–11. (In Russian) [Google Scholar] [CrossRef]

- Materials for Discussion with the Interdepartmental Working Group on the Development of Hydrogen Energy in the Russian Federation 17 February 2022. 29p. Available online: https://www.bigpowernews.ru/photos/0/0_RP3C6vWA0RtOsNlpa0jEVPQjtVDo3xAy.pdf?ysclid=limvjwvrrd249552974 (accessed on 5 October 2023). (In Russian).

- Safina, E.B.; Khokhlov, S.V. Paradox of alternative energy consumption: Lean or profligacy? Int. J. Qual. Res. 2017, 11, 903–916. [Google Scholar] [CrossRef]

- Ponomarenko, T.V.; Marinina, O.A.; Nevskaya, M.A. Developing Corporate Sustainability Assessment Methods for Oil and Gas Companies. Economies 2021, 9, 58. [Google Scholar] [CrossRef]

- Capurso, T.; Stefanizzi, M.; Camporeale, S.M. Perspective of the role of hydrogen in the 21st century energy transition. Energy Convers. Manag. 2021, 251, 114898. [Google Scholar] [CrossRef]

- Greene, D.L.; Ogden, J.M.; Lin, Z. Challenges in the designing, planning and deployment of hydrogen refueling infrastructure for fuel cell electric vehicles. eTransportation 2020, 6, 100086. [Google Scholar] [CrossRef]

- Ajanovic, A.; Haas, R. Prospects and impediments for hydrogen and fuel cell vehicles in the transport sector. Int. J. Hydrogen Energy 2021, 46, 10049–10058. [Google Scholar] [CrossRef]

- Hansen, O.R. Hydrogen infrastructure—Efficient risk assessment and design optimization approach to ensure safe and practical solutions. Process Saf. Environ. Prot. 2020, 143, 164–176. [Google Scholar] [CrossRef]

- Wickham, D.; Hawkes, A.; Jalil-Vega, F. Hydrogen supply chain optimisation for the transport sector—Focus on hydrogen purity and purification requirements. Appl. Energy 2021, 305, 117740. [Google Scholar] [CrossRef]

- Tcvetkov, P.S.; Fedoseev, S.V. Analysis of project organization specifics in small-scale LNG production. J. Min. Inst. 2020, 246, 678–686. [Google Scholar] [CrossRef]

- Fateev, V.N.; Alekseeva, O.K.; Korobtsev, S.V.; Seregina, E.A.; Fateeva, T.V.; Grigoriev, A.S.; Aliev, A.S. Problems of accumulation and storage of hydrogen. Chem. Probl. 2018, 4, 453–483. [Google Scholar] [CrossRef]

- Tarkowski, R.; Uliasz-Misiak, B.; Tarkowski, P. Storage of hydrogen, natural gas, and carbon dioxide—Geological and legal conditions. Int. J. Hydrogen Energy 2021, 46, 20010–20022. [Google Scholar] [CrossRef]

- Ponomarev-Stepnoy, N.N.; Alekseev, S.V.; Petrunin, V.V.; Kodochigov, N.G.; Kuznetsov, L.E.; Fateev, S.A.; Kodochigov, G.N. Nuclear energy technology complex with high-temperature gas-cooled reactors for large-scale environmentally friendly production of hydrogen and natural gas. Gazov. Promyshlennost [Gas Industry] 2018, 11, 94–102. (In Russian) [Google Scholar]

- Aksyutin, O.; Ishkov, A.; Romanov, K.; Teterevlev, R. The role of Russian natural gas in the development of hydrogen energy. Energeticheskaya Polit. [Energy Policy] 2021, 3, 6–19. [Google Scholar] [CrossRef]

- Development of Hydrogen Energy in Russia: New Energy Policy. Analytical Research of the Company “Business Profile” (9 June 2021). 16p. Available online: https://delprof.ru/press-center/open-analytics/razvitie-vodorodnoy-energetiki-v-rossii-novaya-energopolitika/1 (accessed on 5 October 2023). (In Russian).

- Hydrogen Energy: Growth Points—Expert Opinion. Neftegaz 2021, 20, 2–20. Available online: http://oilandgasforum.ru/data/files/20_web.pdf (accessed on 15 September 2023). (In Russian).

- Dawood, F.; Anda, M.; Shafiullah, G.M. Hydrogen production for energy: An overview. Int. J. Hydrogen Energy 2020, 45, 3847–3869. [Google Scholar] [CrossRef]

- Belov, V.B. Hydrogen energy is a new niche for Russian-German cooperation. Anal. Zap. [Analytical Note] 2020, 37, 220. [Google Scholar] [CrossRef]

- Goyal, D.; Dang, R.K.; Goyal, T.; Saxena, K.K.; Mohammed, K.A.; Dixit, S. Graphene: A Path-Breaking Discovery for Energy Storage and Sustainability. Materials 2022, 15, 6241. [Google Scholar] [CrossRef] [PubMed]

- Marinina, O.A.; Kirsanova, N.Y.; Nevskaya, M.A. Circular economy models in industry: Developing a conceptual framework. Energies 2022, 15, 9376–9386. [Google Scholar] [CrossRef]

- Parkinson, B.; Balcombe, P.; Speirs, J.F.; Hawkes, A.D.; Hellgardt, K. Levelized Cost of CO2 Mitigation from Hydrogen Production Routes. Energy Environ. Sci. 2019, 12, 19. [Google Scholar] [CrossRef]

- Nguyen, V.T.; Pham, T.V.; Rogachev, M.K.; Korobov, G.Y.; Parfenov, D.V.; Zhurkevich, A.O.; Islamov, S.R. A comprehensive method for determining the dewaxing interval period in gas lift wells. J. Petrol. Explor. Prod. Technol. 2023, 13, 1163–1179. [Google Scholar] [CrossRef]

- Duryagin, V.; Nguyen Van, T.; Onegov, N.; Shamsutdinova, G. Investigation of the Selectivity of the Water Shutoff Technology. Energies 2023, 16, 366. [Google Scholar] [CrossRef]

- ISO 11439:2013; Gas Cylinders—High Pressure Cylinders for the on-Board Storage of Natural Gas as a Fuel for Automotive Vehicles. ISO: Belgium, Brussels, 2013.

- Vasilev, Y.N.; Cherepovitsyn, A.E.; Tsvetkova, A.Y.; Komendantova, N.E. Promoting Public Awareness of Carbon Capture and Storage Technologies in the Russian Federation: A System of Educational Activities. Energies 2021, 14, 1408. [Google Scholar] [CrossRef]

- Hydrogen Insights May 2023 Hydrogen Council, McKinsey & Company. 27p. Available online: https://hydrogencouncil.com/wp-content/uploads/2023/05/hydrogen-insights-2023.pdf (accessed on 5 October 2023).

- Prather, M.J. Atmospheric science. An environmental experiment with H2? Science 2003, 302, 581–582. [Google Scholar] [CrossRef] [PubMed]

- Busch, P.; Kendall, A.; Lipman, T. A systematic review of life cycle greenhouse gas intensity values for hydrogen production pathways. Renew. Sustain. Energy Rev. 2023, 184, 113588. [Google Scholar] [CrossRef]

- Davies, A.J.; Hastings, A. Lifetime greenhouse gas emissions from offshore hydrogen production. Energy Rep. 2023, 10, 1538–1554. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Hydrogen Type | Production Method | Carbon Footprint | Cost, USD/ kg | % * |

|---|---|---|---|---|

| Subproduct | Subproduct in chemical (ammonia production), oil and other industries without CCS | High | 1.5–3 | 20–21 |

| Gray | Steam methane conversion without CCS | 1.5–3 | 58–60 | |

| Brown | Coal gasification | 2–3 | 14–15 | |

| Blue | Methane conversion (reforming) with CCS | Low emission | 4–5 | 1–2.5 |

| Coal gasification with CCS | 4–6 | 1–1.5 | ||

| Turquoise | Methane pyrolysis | 5–7.5 | 0.2 | |

| Yellow ** | Water electrolysis using nuclear energy | 1.5–9 | 0.3 | |

| Orange | Water electrolysis using “ordinary” electricity | 7–12 | 2–2.5 | |

| Green | Water electrolysis using renewable energy sources | Close to zero | 12–17 | 0.5 |

| Using biomass energy, biogas conversion | 10–15 | 0.2 | ||

| Gold | Natural, from the bowels of Earth | >100 | - |

| Country | 2017 | 2019 | 2020 | 2021 | 2022 |

|---|---|---|---|---|---|

| South Korea | 0.10 | 5.08 | 10.09 | 18.55 | 27.85 |

| USA | 3.53 | 8.04 | 9.25 | 12.50 | 14.00 |

| China | 0.00 | 6.18 | 8.44 | 9.65 | 12.10 |

| Japan | 2.30 | 3.63 | 4.20 | 7.50 | 9.60 |

| Europe | 1.19 | 2.18 | 2.67 | 3.60 | 5.10 |

| Other countries | 0.00 | 0.10 | 0.15 | 0.50 | 0.70 |

| Total | 7.12 | 25.21 | 34.80 | 52.30 | 69.35 |

| Country/Period | 2010–2020 | 2021–2023 | 2024–2030 | |||

|---|---|---|---|---|---|---|

| Bln Euros | % | Bln Euros | % | Bln Euros | % | |

| Russia | 0.5 | 1.7% | 0.5 | 1.4% | 10.0 | 3.2% |

| India | 0.0 | 0.0% | 1.0 | 2.7% | 92.5 | 29.4% |

| Germany | 5.0 | 16.7% | 10.0 | 27.0% | 30.0 | 9.5% |

| EU, except Germany | 3.0 | 10.0% | 7.0 | 18.9% | 45.0 | 14.3% |

| South Korea | 6.0 | 20.0% | 8.0 | 21.6% | 35.0 | 11.1% |

| Japan | 5.0 | 16.7% | 2.0 | 5.4% | 15.0 | 4.8% |

| China | 1.0 | 3.3% | 2.0 | 5.4% | 25.0 | 7.9% |

| USA | 7.0 | 23.3% | 2.5 | 6.8% | 12.5 | 4.0% |

| Other countries | 2.5 | 8.3% | 4.0 | 10.8% | 50.0 | 15.9% |

| Total | 30.0 | 100.0 | 37.0 | 100.0 | 315.0 | 100.0 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Radoushinsky, D.; Gogolinskiy, K.; Dellal, Y.; Sytko, I.; Joshi, A. Actual Quality Changes in Natural Resource and Gas Grid Use in Prospective Hydrogen Technology Roll-Out in the World and Russia. Sustainability 2023, 15, 15059. https://doi.org/10.3390/su152015059

Radoushinsky D, Gogolinskiy K, Dellal Y, Sytko I, Joshi A. Actual Quality Changes in Natural Resource and Gas Grid Use in Prospective Hydrogen Technology Roll-Out in the World and Russia. Sustainability. 2023; 15(20):15059. https://doi.org/10.3390/su152015059

Chicago/Turabian StyleRadoushinsky, Dmitry, Kirill Gogolinskiy, Yousef Dellal, Ivan Sytko, and Abhishek Joshi. 2023. "Actual Quality Changes in Natural Resource and Gas Grid Use in Prospective Hydrogen Technology Roll-Out in the World and Russia" Sustainability 15, no. 20: 15059. https://doi.org/10.3390/su152015059

APA StyleRadoushinsky, D., Gogolinskiy, K., Dellal, Y., Sytko, I., & Joshi, A. (2023). Actual Quality Changes in Natural Resource and Gas Grid Use in Prospective Hydrogen Technology Roll-Out in the World and Russia. Sustainability, 15(20), 15059. https://doi.org/10.3390/su152015059