Impact of Revenue Generated via Composting and Recycling of Wastes Produced in the Greenhouse Tomato Supply Chain on Reducing Income Inequality: A Case Study of Türkiye

Abstract

:1. Introduction

2. Materials and Methods

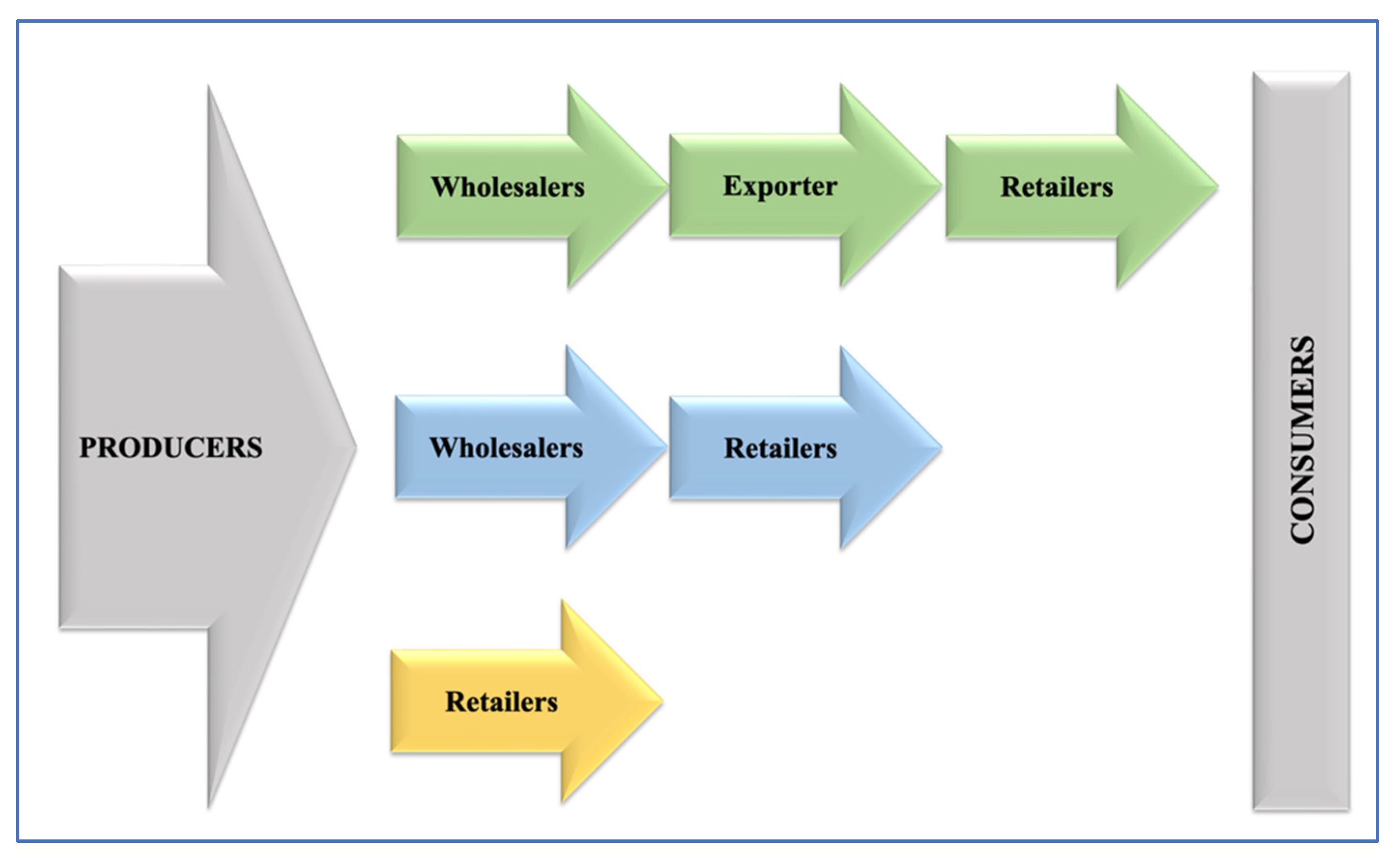

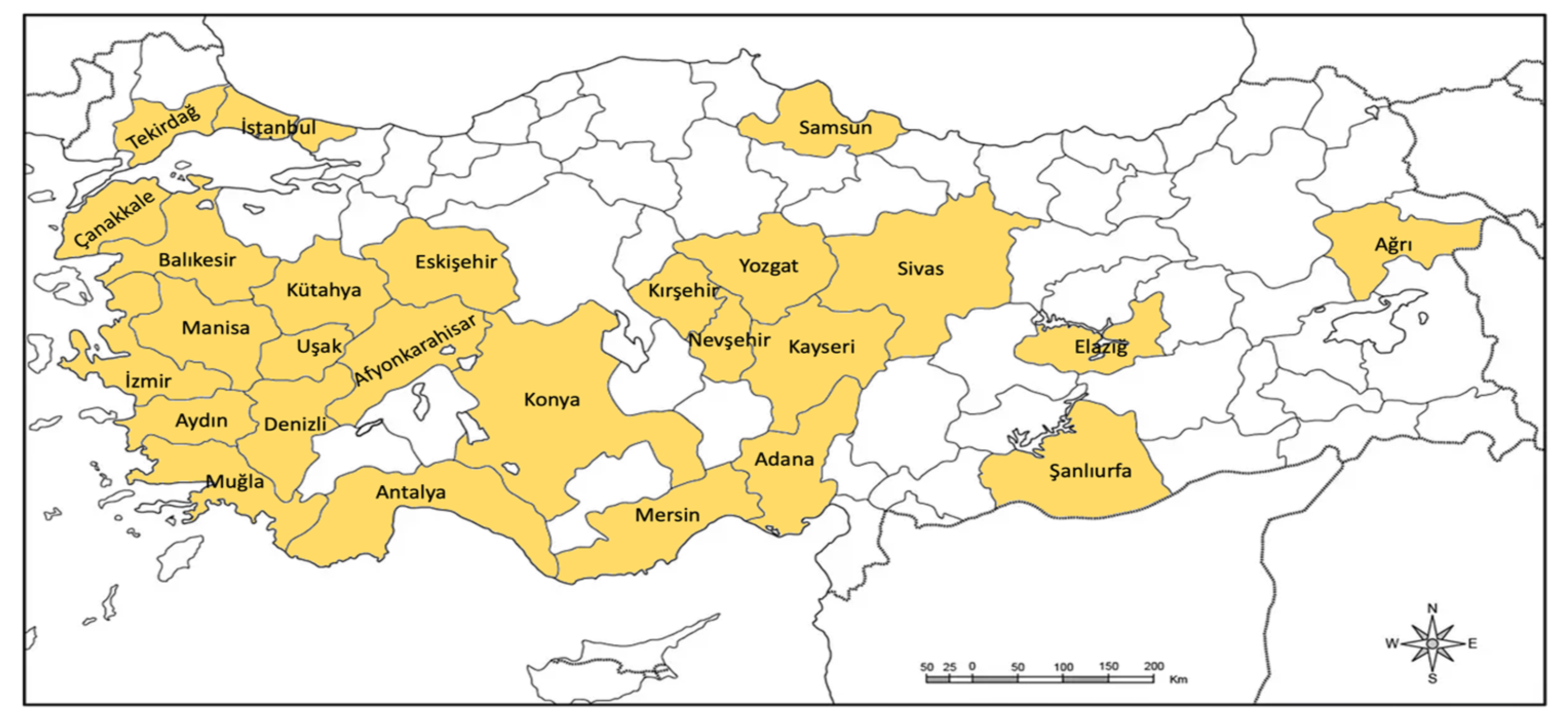

2.1. Study Area and Data Collection

2.2. Assessing Income Distribution along the Tomato Supply Chain

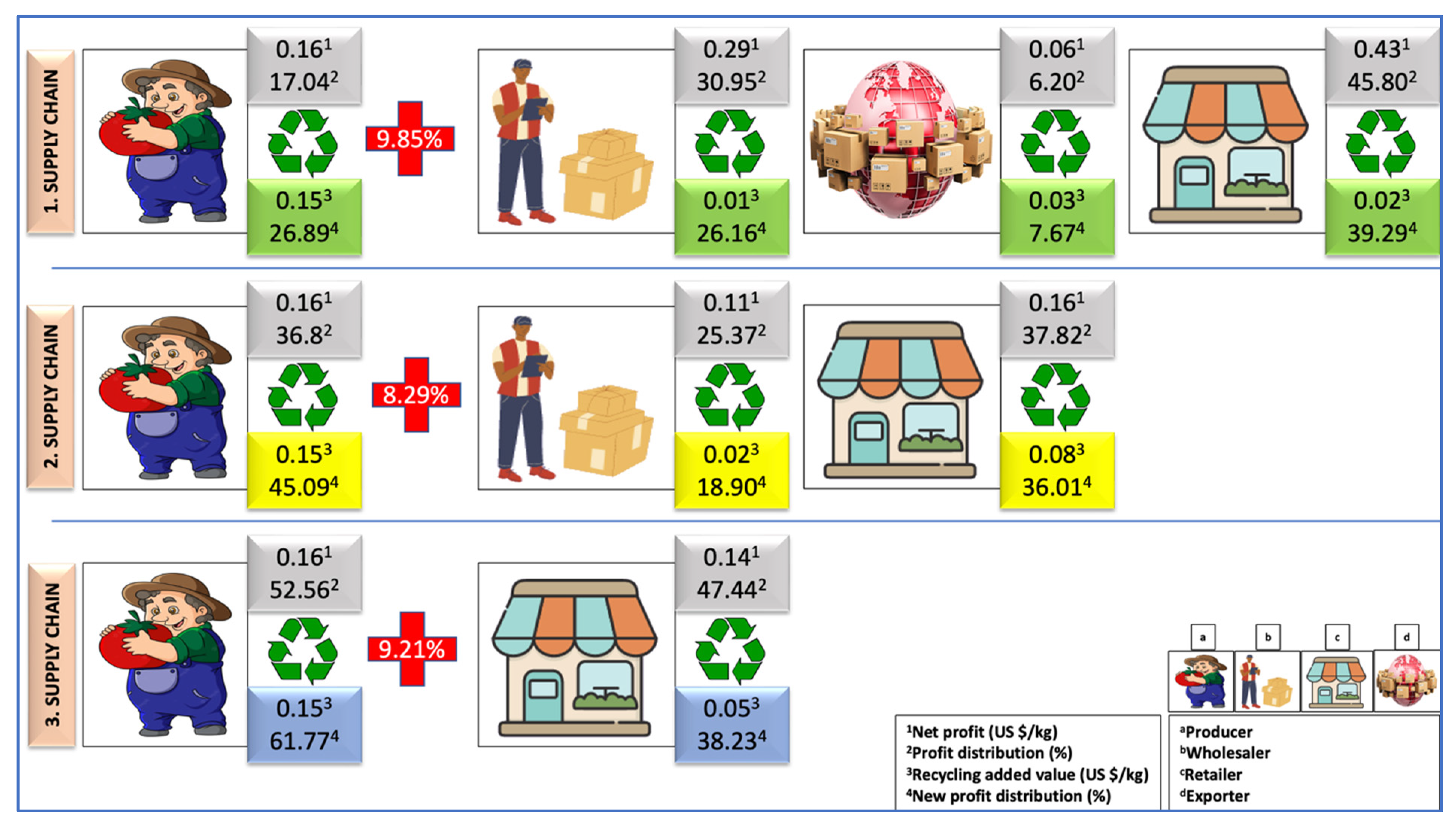

2.3. Exploring the Effect of Revenue Generated from Recycling of Tomato Waste on Income Distribution

3. Research Findings and Discussion

4. Conclusions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Anastasiadis, F.; Apostolidou, I.; Michailidis, A. Mapping sustainable tomato supply chain in Greece: A framework for research. Foods 2020, 9, 539. [Google Scholar] [CrossRef] [PubMed]

- Sharma, M.; Shah, J.K.; Joshi, S. Modeling enablers of supply chain decarbonisation to achieve zero carbon emissions: An environment, social and governance (ESG) perspective. Environ. Sci. Pollut. Res. 2023, 30, 76718–76734. [Google Scholar] [CrossRef] [PubMed]

- Gautam, S.; Acedo, A.L.; Schreinemachers, P.; Subedi, B.P. Volume and value of postharvest losses: The case of tomatoes in Nepal. Br. Food J. 2017, 119, 2547–2558. [Google Scholar] [CrossRef]

- Secondi, L.; Principato, L.; Ruini, L.; Guidi, M. Reusing food waste in food manufacturing companies: The case of the tomato-sauce supply Chain. Sustainability 2019, 11, 2154. [Google Scholar] [CrossRef]

- Chaboud, G.; Moustier, P. The role of diverse distribution channels in reducing food loss and waste: The case of the Cali tomato supply chain in Colombia. Food Policy 2021, 98, 101881. [Google Scholar] [CrossRef]

- Mohan, A.; Krishnan, R.; Arshinder, K.; Vandore, J.; Ramanathan, U. Management of postharvest losses and wastages in the Indian tomato supply chain—A temperature-controlled storage perspective. Sustainability 2023, 15, 1331. [Google Scholar] [CrossRef]

- Imtiyaz, H.; Soni, P. Evaluation of marketing supply chain performance of fresh vegetables in Allahabad district, India. Int. J. Manag. Sci. Bus. Res. 2014, 3, 72–83. [Google Scholar]

- Traub, L.N.; Jayne, T. The effects of price deregulation on maize marketing margins in South Africa. Food Policy 2008, 33, 224–236. [Google Scholar] [CrossRef]

- Quintana, A.A.; Chong, M.; Cordova, M.L.; Camaro, P.J. The impact of logistics on marketing margin in the Philippine agricultural sector. J. Econ. Financ. Account. Stud. 2021, 3, 300–318. [Google Scholar] [CrossRef]

- FAO. FAOSTAT—FAO Database for Food and Agriculture; FAO FAOSTAT, from Food and agriculture Organisation of United Nations (FAO): Rome, Italy, 2021. [Google Scholar]

- Tatlıdil, F.F.; Dellal, İ.; Bayramoğlu, Z. Food Losses and Waste in Turkey; Food and Agriculture Organization of the United Nations Country Report; FAO: Rome, Italy, 2013. [Google Scholar]

- Karthick, K.; Boris Ajit, A.; Subramanaian, V.; Anbuudayasankar, S.P.; Narassima, M.S.; Hariharan, D. Maximising profit by waste reduction in postharvest Supply Chain of tomato. Br. Food J. 2023, 125, 626–644. [Google Scholar] [CrossRef]

- Kumar, S.; Underhill, S.; Kumar, S. Postharvest physical risk factors along the tomato supply chain: A case study in Fiji. In Proceedings of the Crawford Fund 2016 Annual Conference, Canberra, Australia, 29–30 August 2016; Volume 941, pp. 1867–2017. [Google Scholar]

- Mashau, M.E.; Moyane, J.N.; Jideani, I.A. Assessment of post-harvest losses of fruits at Tshakhuma fruit market in Limpopo Province, South Africa. Afr. J. Agric. Res. Acad. J. 2012, 7, 4145–4150. [Google Scholar]

- Anil, K.; Arora. Post-harvest management of vegetables in Uttar Pradesh hills. Indian J. Agric. Mark. 1999, 13, 6–14. [Google Scholar]

- Gupta, S.P.; Rathore, N.S. Disposal pattern and constraints in vegetable market: A case study of Raipur District of Madhya Pradesh. Agric. Mark. 1999, 42, 52–59. [Google Scholar]

- More, S.S. Economics of Production and Marketing of Banana in Maharashtra State. Master’s Thesis, University of Agricultural Science, Dharwad, India, 1999. [Google Scholar]

- Begum, A.; Raha, S.K. Marketing of Banana in selected areas of Bangladesh. Econ. Aff. Kolkata 2002, 47, 158–166. [Google Scholar]

- Sudha, M.; Gajanana, T.M.; Murthy, S.D.; Dakshinamoorthy, V. Marketing practices and post-harvest loss assessment of pineapple in Kerala. Indian J. Agric. Mark. 2002, 16, 56–65. [Google Scholar]

- Murthy, S.D.; Gajanana, T.M.; Sudha, M. Marketing practices and post-harvest loss estimated in Mango var. Baganpalli at different stages of marketing—A methodological perspective. Agric. Econ. Res. Rev. 2002, 15, 188–200. [Google Scholar]

- Singh, S.; Chauhan, S.K. Marketing of Vegetables in Himachal Pradesh. Agric. Mark. 2004, 44, 5–10. [Google Scholar]

- Bala, B. Marketing system of apple in hills problems and prospects (A case of Kullu district, Himachal Pradesh). Indian J. Agric. Mark. 2006, 8, 285–293. [Google Scholar]

- Murthy, D.S.; Gajanana, T.M.; Sudha, M.; Dakshinamoorthy. Marketing Losses and their impact on marketing margins: A case study of banana in Karnataka. Agric. Econ. Res. Rev. 2007, 20, 47–60. [Google Scholar]

- Adeoye, I.B.; Odeleye, O.M.O.; Babalola, S.O.; Afolayan, S.O. Economic Analysis of Tomato Losses in Ibadan Metropolis, Oyo State, Nigeria. Afr. J. Basic Appl. Sci. 2009, 1, 87–92. [Google Scholar]

- Rupali, P.; Gyan, P. Marketable Surplus and marketing efficiency of Vegetables in Indore District: A Micro Level Study. IUP J. Agric. Econ. 2010, 7, 84–93. [Google Scholar]

- Barakade, A.J.; Lokhande, T.N.; Todkari, G.U. Economics of onion cultivation and its marketing pattern in Satara district of Maharastra. Int. J. Agric. Sci. 2011, 3, 110–117. [Google Scholar]

- Chauhan, C. India Wastes More Farm Food than China: UN. Hindustan Times, 12 September 2013. [Google Scholar]

- Biswas, A.K.; Tortajada, C. India Must Tackle Food Waste. 2014. Available online: https://www.weforum.org/agenda/2014/08/india-perishable-food-waste-population-growth/ (accessed on 5 May 2021).

- Ghezavati, V.R.; Hooshyar, S.; Tavakkoli-Moghaddam, R. A Benders’ decomposition algorithm for optimizing distribution of perishable products considering postharvest biological behavior in agri-food supply chain: A case study of tomato. Cent. Eur. J. Oper. Res. 2017, 25, 29–54. [Google Scholar] [CrossRef]

- Handayati, Y.; Simatupang, T.M.; Perdana, T. Agri-food supply chain coordination: The state-of-the-art and recent developments. Logist. Res. 2015, 8, 1–15. [Google Scholar] [CrossRef]

- Emana, B.; Afari-Sefa, V.; Nenguwo, N.; Ayana, A.; Kebede, D.; Mohammed, H. Characterization of pre- and postharvest losses of tomato supply chain in Ethiopia. Agric. Food Secur. 2017, 6, 1–11. [Google Scholar] [CrossRef]

- Laroche, M.; Bergeron, J.; Barbaro-Forleo, G. Targeting consumers who are willing to pay more for environmentally friendly products. J. Consum. Mark. 2001, 18, 503–520. [Google Scholar] [CrossRef]

- TURKSTAT. 2022. Available online: http://www.tuik.gov.tr (accessed on 10 April 2023).

- Trade Map. 2023. Available online: trademap.org (accessed on 10 April 2023).

- Underhill, S.J.R.; Kumar, S. Quantifying postharvest losses along a commercial tomato supply chain in Fiji: A case study. J. Appl. Hortic. 2015, 17, 199–204. [Google Scholar] [CrossRef]

- McKenzie, T.J.; Singh-Peterson, L.; Underhill, S.J.R. Quantifying postharvest loss and the implication of market-based decisions: A case study of two commercial domestic tomato supply chains in Queensland, Australia. Horticulturae 2017, 3, 44. [Google Scholar] [CrossRef]

- Asrat, F.; Ayalew, A.; Degu, A. Food science and technology postharvest loss assessment of tomato (Solanum lycopersicum L.) in Fogera. Turk. J. Agric. 2019, 7, 1146–1155. [Google Scholar]

- Özdemir, I.S.; Semizer, H. Effect of good and poor postharvest handling practices on the losses in lettuce and tomato supply chains. Gida/J. Food 2021, 46, 859–871. [Google Scholar] [CrossRef]

- Mwagike, L. The Effect of social networks on performance of fresh tomato supply chain in Kilolo District, Tanzania. Int. J. Bus. Econ. Res. 2015, 4, 238–243. [Google Scholar] [CrossRef]

- Sarma, P.K. Postharvest losses of tomato: A value chain context of Bangladesh. Int. J. Agric. Educ. Ext. 2018, 4, 085–092. [Google Scholar]

- Maige, L.S. Analysis on The Factors for Tomato Supply Chain Performance: A Case of Kilosa District; College of Business Education: Dar es Salaam, Tanzania, 2022. [Google Scholar]

- Türkten, H. Environmental Efficiency of Tomato Growing Farms Having Soilless Culture System and Economic Analysis of Waste Utilization Methods. Ph.D. Thesis, Ondokuz Mayıs University, Samsun, Turkey, 2021. [Google Scholar]

- Chen, Y.-T. A cost analysis of food waste composting in Taiwan. Sustainability 2016, 8, 1210. [Google Scholar] [CrossRef]

- Pandyaswargo, A.H.; Premakumara, D.G.J. Financial sustainability of modern composting: The economically optimal scale for municipal waste composting plant in developing Asia. Int. J. Recycl. Org. Waste Agric. 2014, 3, 1–14. [Google Scholar] [CrossRef]

- Zulkepli, N.E.; Muis, Z.A.; Mahmood, N.A.N.; Hashim, H.; Ho, W.S. Cost benefit analysis of composting and anaerobic digestion in a community: A review. Chem. Eng. Trans. 2017, 56, 1777–1782. [Google Scholar]

- Montero, J.I.; Antón, M.A.; Torrellas, M.; Ruijs, M.; Vermeulen, P. EUPHOROS Deliverable 5. Report on Environmental and Economic Profile of Present Greenhouse Production Systems in Europe. European Commission FP7 RDT Project Euphoros (Reducing the Need for External Inputs in High Value Protected Horticultural and Ornamental Crops). 2009. Available online: http://www.euphoros.wur.nl/UK (accessed on 11 September 2023).

- Boldrin, A.; Hartling, K.R.; Laugen, M.; Christensen, T.H. Environmental in- ventory modelling of the use of compost and peat in growth media preparation. Resour. Conserv. Recycl. 2010, 54, 1250–1260. [Google Scholar] [CrossRef]

- Gruda, N.S. Increasing sustainability of growing media constituents and stand-alone substrates in soilless culture systems. Agronomy 2019, 9, 298. [Google Scholar] [CrossRef]

- Mielcarek, A.; Rodziewicz, J.; Janczukowicz, W.; Dobrowolski, A. Analysis of wastewater generated in greenhouse soilless tomato cultivation in central Europe. Water 2019, 11, 2538. [Google Scholar] [CrossRef]

- Chaudhary, K.R. Analysis of Tomato Marketing System in Lalitpur District, Nepal. Master’s Thesis, Van Hall Larenstein University of Applied Sciences, Leeuwarden, the Netherlands, 2010. [Google Scholar]

- Singh, K.; Asress, F.C. Determining working capital solvency level and its effect on profitability in selected Indian manufacturing firms. 2010. Available online: http://repository.kln.ac.lk/handle/123456789/4511 (accessed on 11 September 2023).

- Kaveri Gosavi, D.H.; Ratnaparkhe, A.N. Price spread, market margin and marketing efficiency in cauliflower marketing in Maharashtra. Pharma Innov. J. 2021, SP-10, 400–403. [Google Scholar]

- Pipera, D.; Pagria, I.; Musabelliu, B. Alternatives for improving management of the value chain for greenhouse tomato production in Albania. In Proceedings of the KONFERENCA E KATËRT, Pristina, Kosovo, 1 February 2022; pp. 235–251. [Google Scholar]

- Eltahir, M.E.S.; Fadl, K.E.M.; Hamad, M.A.A.; Safi, A.I.A.; Elamin, H.M.A.; Abutaba, Y.I.M.; Musa, F.I.; Mahmoud, T.E.; Alemeu, A.; Abdelrhman, H.A.; et al. Tapping Tools for Gum Arabic and Resins Production: A Review Paper. Am. J. Eng. Technol. Manag. 2023, 8, 33–40. [Google Scholar]

- Xaba, B.G.; Masuku, M.B. Factors affecting the productivity and profitability of vegetables production in Swaziland. J. Agric. Stud. 2013, 1, 37–52. [Google Scholar]

- Chauhan, A.; Singh, A. A hybrid multi-criteria decision making method approach for selecting a sustainable location of healthcare waste disposal facility. J. Clean. Prod. 2016, 139, 1001–1010. [Google Scholar] [CrossRef]

- Bhandari, R.; Neupane, N.; Adhikari, D.P. Climatic change and its impact on tomato (Lycopersicum esculentum L.) production in plain area of Nepal. Environ. Chall. 2021, 4, 100–129. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Price (USD/kg) (1) | Cumulative (%) (2) | Absolute Marketing Margin (USD/kg) (3) | Relative Marketing Margin (%) (4) | Cost (USD/kg) (5) | Net Profit (USD/kg) (6) | Profit Distribution (%) (7) | Net Profit Margin (%) (8) = (6)/(1) | |

|---|---|---|---|---|---|---|---|---|

| 1. Supply chain | ||||||||

| Producer | 0.81 | 21.62 | 0.81 | 21.62 | 0.66 | 0.16 | 17.04 | 0.20 |

| Wholesaler | 1.77 | 47.04 | 0.96 | 25.42 | 0.67 | 0.29 | 30.95 | 0.16 |

| Exporter | 2.40 | 63.60 | 0.62 | 16.57 | 0.57 | 0.06 | 6.20 | 0.02 |

| Retailer | 3.77 | 100.00 | 1.37 | 36.40 | 0.94 | 0.43 | 45.80 | 0.11 |

| Total | 3.77 | - | 3.77 | 100.00 | 2.83 | 0.93 | 100.00 | 0.25 |

| 2. Supply chain | ||||||||

| Producer | 0.81 | 52.19 | 0.81 | 52.19 | 0.66 | 0.16 | 36.80 | 0.20 |

| Wholesaler | 1.16 | 74.46 | 0.35 | 22.26 | 0.24 | 0.11 | 25.37 | 0.09 |

| Retailer | 1.56 | 100.00 | 0.40 | 25.54 | 0.24 | 0.16 | 37.82 | 0.10 |

| Total | 1.56 | - | 1.56 | 100.00 | 1.13 | 0.43 | 100.00 | 0.28 |

| 3. Supply chain | ||||||||

| Producer | 0.81 | 53.20 | 0.81 | 53.20 | 0.66 | 0.16 | 52.56 | 0.20 |

| Retailer | 1.53 | 100.00 | 0.72 | 46.80 | 0.57 | 0.14 | 47.44 | 0.09 |

| Total | 1.53 | - | 1.53 | 100.00 | 1.23 | 0.30 | 100.00 | 0.20 |

| Total Tomatoes Supply (Ton) | Number of Active Actors in Each Nodes | Quantity of Tomatoes Sold by FTSC Actors (Ton/Actor) | Net Profit (USD/Ton) | Total Net Income (USD) | Share in Total Net FTSC Income (%) | Rank of the Actors | |

|---|---|---|---|---|---|---|---|

| First FTSC | |||||||

| Producer | 195,992.64 | 136.00 | 1441.12 | 160.00 | 230,579.58 | 7.79 | 4 |

| Wholesaler | 194,969.20 | 60.00 | 3249.49 | 290.00 | 942,351.13 | 31.82 | 2 |

| Exporter | 186,597.82 | 18.00 | 10,366.55 | 60.00 | 621,992.73 | 21.00 | 3 |

| Retailer | 183,335.16 | 69.00 | 2657.03 | 439.00 | 1,166,436.74 | 39.39 | 1 |

| Total | 930.00 | 2,961,360.19 | 100.00 | ||||

| Second FTSC | |||||||

| Producer | 50,750.34 | 136.00 | 373.16 | 160.00 | 59,706.28 | 27.32 | 3 |

| Wholesaler | 50,674.70 | 60.00 | 844.58 | 110.00 | 92,903.62 | 42.51 | 1 |

| Retailer | 49,464.44 | 120.00 | 412.20 | 160.00 | 65,952.59 | 30.18 | 2 |

| Total | 430.00 | 218,562.49 | 100.00 | ||||

| Third FTSC | |||||||

| Producer | 76,382.66 | 136.00 | 561.64 | 160.00 | 89,861.95 | 15.96 | 2 |

| Retailer | 74,360.90 | 22.00 | 3380.04 | 140.00 | 473,205.73 | 84.04 | 1 |

| Total | 300.00 | 563,067.68 | 100.00 | ||||

| Waste Amount (Tons) | Value USD | |||

|---|---|---|---|---|

| Mean | % | Mean | % | |

| Agricultural waste | 1763.62 | 97.87 | 302.81 | 96.23 |

| Plant waste | 1520.41 | 84.37 | 261.01 | 82.95 |

| Plant waste during production | 1174.08 | 65.15 | 233.04 | 74.06 |

| Plant waste after harvesting | 346.34 | 19.22 | 27.97 | 8.89 |

| Product waste | 0.16 | 0.01 | 0.02 | 0.01 |

| Growing media waste | 164.01 | 9.10 | 13.62 | 4.33 |

| Drainage | 79.04 | 4.39 | 28.15 | 8.95 |

| Other waste | 38.43 | 2.13 | 11.85 | 3.77 |

| Viol | 0.33 | 0.02 | 0.08 | 0.03 |

| Plastic case | 14.65 | 0.81 | 5.42 | 1.72 |

| Box | 7.50 | 0.42 | 1.98 | 0.63 |

| Medicine box | 0.83 | 0.05 | 0.22 | 0.07 |

| Greenhouse glass | 4.22 | 0.23 | 0.60 | 0.19 |

| Greenhouse plastic cover | 6.02 | 0.33 | 2.82 | 0.90 |

| Rope | 4.89 | 0.27 | 0.74 | 0.24 |

| Total tomato production waste | 1802.04 | 100.00 | 314.66 | 100.00 |

| Box and Cardboard Waste | Pallet Waste | Product Loss | ||||

|---|---|---|---|---|---|---|

| Waste Amount (Tons) | Value USD | Waste Amount (Tons) | Value USD | Waste Amount (Tons) | Value USD | |

| Mean | Mean | Mean | Mean | Mean | Mean | |

| 1. Supply chain | ||||||

| Wholesalers | 86.4 | 9776.3 | 39.8 | 5551.3 | 7.5 | 937.1 |

| Exporter | 90.0 | 10,185.9 | 181.5 | 25,340.0 | 61.6 | 7665.2 |

| Retailers | 95.8 | 10,840.7 | 132.2 | 18,462.2 | 22.5 | 2806.2 |

| 2. Supply chain | ||||||

| Wholesalers | 50.9 | 5767.6 | 10.9 | 1518.2 | 0.6 | 69.3 |

| Retailers | 91.0 | 10,296.3 | 140.0 | 19,543.6 | 8.9 | 1108.2 |

| 3. Supply chain | ||||||

| Retailers | 52.0 | 5890.3 | 135.3 | 18,895.0 | 14.9 | 1851.2 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Türkten, H. Impact of Revenue Generated via Composting and Recycling of Wastes Produced in the Greenhouse Tomato Supply Chain on Reducing Income Inequality: A Case Study of Türkiye. Sustainability 2023, 15, 13801. https://doi.org/10.3390/su151813801

Türkten H. Impact of Revenue Generated via Composting and Recycling of Wastes Produced in the Greenhouse Tomato Supply Chain on Reducing Income Inequality: A Case Study of Türkiye. Sustainability. 2023; 15(18):13801. https://doi.org/10.3390/su151813801

Chicago/Turabian StyleTürkten, Hatice. 2023. "Impact of Revenue Generated via Composting and Recycling of Wastes Produced in the Greenhouse Tomato Supply Chain on Reducing Income Inequality: A Case Study of Türkiye" Sustainability 15, no. 18: 13801. https://doi.org/10.3390/su151813801

APA StyleTürkten, H. (2023). Impact of Revenue Generated via Composting and Recycling of Wastes Produced in the Greenhouse Tomato Supply Chain on Reducing Income Inequality: A Case Study of Türkiye. Sustainability, 15(18), 13801. https://doi.org/10.3390/su151813801