The Sectoral and Regional Peer Influences on Heavy-Pollution Corporate Environmental, Social, and Governance Performance

Abstract

1. Introduction

2. Theoretical Framework and Hypotheses Development

2.1. Theoretical Framework

2.1.1. Stakeholder Theory

2.1.2. Signaling Theory

2.1.3. Imitation Strategy Theory

2.2. The Peer Effect of Corporate ESG Performance in Different Peer Groups

2.3. The Impacts of the Peer Effects of Media Coverage, Regulatory Pressure, and Green Innovation on Corporate ESG Performance

2.4. The Peer Effect of Corporate ESG Performance in Different ESG Level Changing Statuses

3. Methodology and Data

3.1. The Spatial Econometric Methodology

3.1.1. The Spatial Autoregressive Model and Spatial Durbin Model

3.1.2. The Spatial Autoregressive Probit Model

3.1.3. The Construction of Spatial Weight Matrix

3.2. Research Design

3.2.1. Data and Variables Selection

3.2.2. Regression Models

4. The Empirical Results of Peer Effect of Corporate ESG Performance and Mechanism Analysis

4.1. The Baseline Panel Model of Corporate ESG Performance

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| (5) | (6) | (7) | (8) | (9) | (10) | |

|---|---|---|---|---|---|---|

| SAR_W1 | SAR_W1 | SAR_W2 | SAR_W2 | SAR_W3 | SAR_W3 | |

| W × ESG_perform | 0.151 *** (0.000) | 0.143 *** (0.000) | 0.223 *** (0.000) | 0.212 *** (0.000) | 0.090 *** (0.000) | 0.087 *** (0.000) |

| Neg_news | −0.026 *** (0.000) | −0.025 *** (0.000) | −0.026 *** (0.000) | −0.025 *** (0.000) | −0.026 *** (0.000) | −0.025 *** (0.000) |

| Env_punish | −0.124 *** (0.000) | −0.122 *** (0.000) | −0.125 *** (0.000) | −0.123 *** (0.000) | −0.123 *** (0.000) | −0.122 *** (0.000) |

| Green_patent | 0.007 ** (0.022) | 0.005 ** (0.041) | 0.006 ** (0.040) | 0.005 * (0.069) | 0.006 ** (0.035) | 0.005 * (0.060) |

| ROA | 0.002 *** (0.001) | 0.002 *** (0.001) | 0.002 *** (0.001) | |||

| Lev | −0.004 (0.665) | −0.005 (0.622) | −0.005 (0.639) | |||

| Growth | −0.001 (0.445) | −0.002 (0.445) | −0.001 (0.446) | |||

| First | 0.180 *** (0.000) | 0.180 *** (0.000) | 0.181 *** (0.000) | |||

| Indp | 0.282 *** (0.001) | 0.282 *** (0.001) | 0.288 *** (0.001) | |||

| Firm | Control | Control | Control | Control | Control | Control |

| Year | Control | Control | Control | Control | Control | Control |

| R_squared | 0.143 | 0.506 | 0.134 | 0.451 | 0.151 | 0.469 |

| Hausman’s | 75.900 *** (0.000) | 121.180 *** (0.000) | 73.250 *** (0.000) | 120.180 *** (0.000) | 73.580 *** (0.000) | 118.010 *** (0.000) |

| Loglikelihood | 2007.246 | 2056.800 | 2013.341 | 2062.251 | 2002.982 | 2053.057 |

| AIC | −4004.492 | −4093.600 | −4016.681 | −4104.502 | −3995.964 | −4086.114 |

| BIC | −3970.361 | −4025.338 | −3982.551 | −4036.241 | −3961.833 | −4017.853 |

| Observations | 6810 | 6810 | 6810 | 6810 | 6810 | 6810 |

4.2. The Peer Effect of Corporate ESG Performance Based on the SAR Model

4.3. The Mechanism Analysis of Peer Effect of Corporate ESG Performance Based on the SDM Model

5. The Further Empirical Analysis of Peer-Pulling Effect and Peer-Dragging Effect of Corporate ESG Level Change

5.1. The Peer-Pulling Effect of Corporate ESG Level Increases Based on the SAR Probit Model

5.2. The Peer-Dragging Effect of Corporate ESG Level Decreases Based on the SAR Probit Model

6. Robustness and Heterogeneity Tests

6.1. The Corporate ESG Performance Peer Effect Based on the SEM Model

6.2. The Endogenous Tests of Peer Effect of Corporate ESG Performance

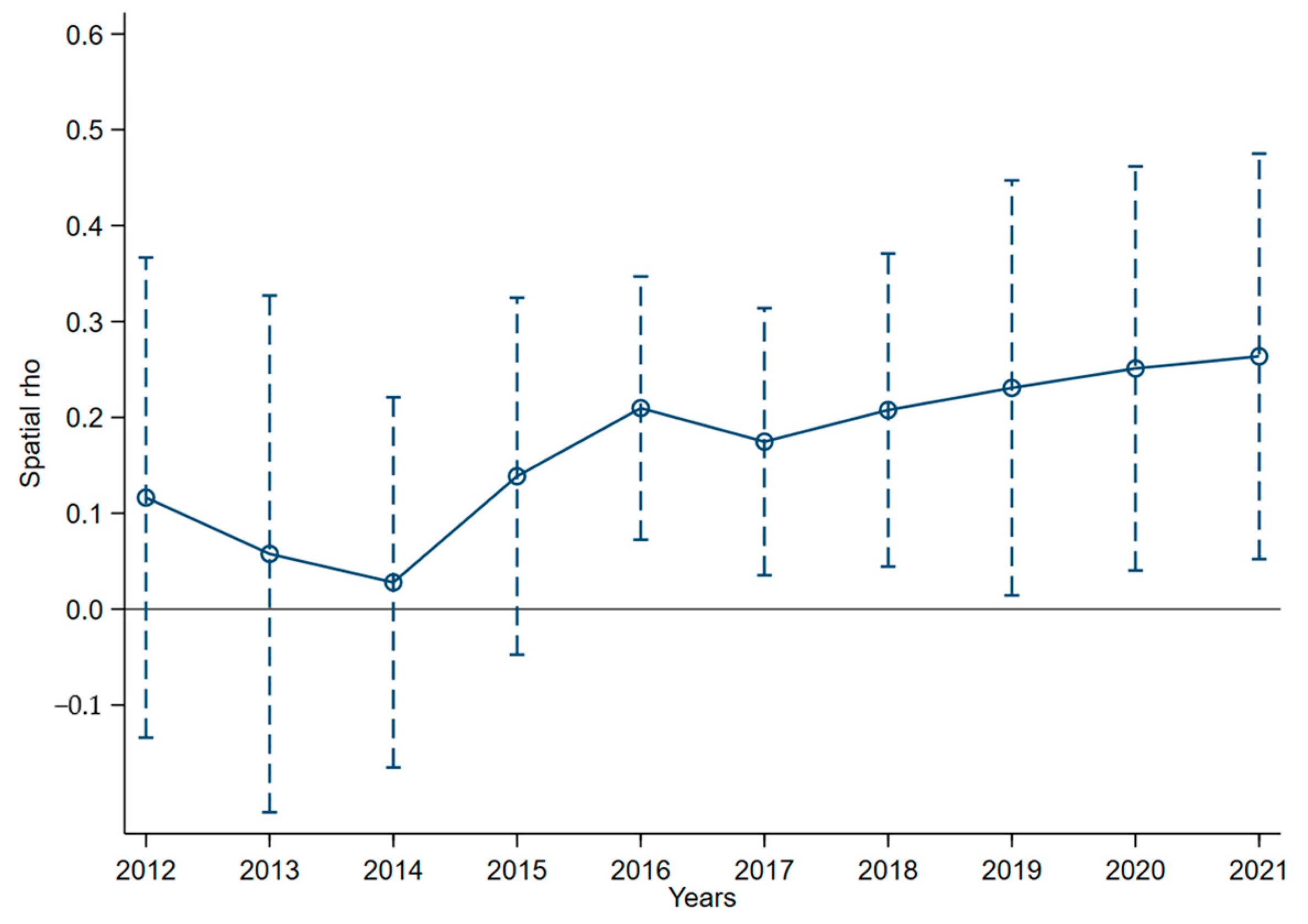

6.3. The Cross-Section Analysis of the Peer Effect of Corporate ESG Performance on Different Years

6.4. The Peer Pulling Effect of Corporate ESG Level Based on the Ordered SAR Probit Model

7. Discussions

8. Conclusions and Implications

8.1. Main Conclusions

8.2. Management Implications

8.3. Limitations and Future Research

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

| Variable | Symbol | Observation | Mean | S.D. | Min. | Max. |

|---|---|---|---|---|---|---|

| ESG performance | ESG_perfomi,t | 6810 | 1.592 | 0.265 | 0.693 | 2.197 |

| ESG level increase | ESG_levelupi,t | 6810 | 0.233 | 0.423 | 0 | 1 |

| ESG level decrease | ESG_leveldowni,t | 6810 | 0.215 | 0.411 | 0 | 1 |

| ESG level | ESG_leveli,t | 6810 | 5.072 | 1.163 | 2 | 9 |

| Negative web news | Neg_newsi,t | 6810 | 4.049 | 1.106 | 0 | 8.925 |

| Environmental punishment | Env_punishi,t | 6810 | 0.007 | 0.085 | 0 | 1 |

| Green patent | Green_patenti,t | 6810 | 1.160 | 1.409 | 0 | 8.080 |

| Return on assets | ROAi,t | 6810 | 4.034 | 7.841 | −105.165 | 119.277 |

| Book leverage ratio | Levi,t | 6810 | 1.480 | 5.079 | −182.279 | 128.343 |

| Profit growth ratio | Growthi,t | 6810 | −0.970 | 25.005 | −119.163 | 22.042 |

| The large shareholders’ ratio | Firsti,t | 6810 | 0.564 | 0.154 | 0 | 0.986 |

| The strength of independent director | Indpi,t | 6810 | 0.369 | 0.052 | 0 | 0.750 |

| Geography spatial weight matrix | W1 | 463,761 | 0.051 | 0.220 | 0 | 1 |

| Industry spatial weight matrix | W2 | 463,761 | 0.101 | 0.301 | 0 | 1 |

| Product spatial weight matrix | W3 | 463,761 | 0.049 | 0.218 | 0 | 1 |

| OLS_W1 | OLS_W2 | OLS_W3 | ||||

|---|---|---|---|---|---|---|

| Model (1) | Model (2) | Model (1) | Model (2) | Model (1) | Model (2) | |

| Residual Moran test | 0.165 *** (0.000) | 0.033 *** (0.000) | 0.248 *** (0.000) | 0.039 *** (0.000) | 0.249 *** (0.000) | 0.027 *** (0.000) |

| LM_SAR test | 23.431 *** (0.000) | 21.343 *** (0.000) | 41.769 *** (0.000) | 37.667 *** (0.000) | 12.485 *** (0.000) | 11.645 *** (0.000) |

| Robust LM_SAR test | 45.191 *** (0.000) | 17.117 *** (0.000) | 42.105 *** (0.000) | 53.186 *** (0.000) | 27.963 *** (0.000) | 10.707 *** (0.000) |

| (14) | (15) | (16) | (17) | |

|---|---|---|---|---|

| Probit | Probit | OLS_FE | OLS_FE | |

| Neg_news | −0.118 *** (0.000) | −0.112 *** (0.000) | −0.035 *** (0.000) | −0.034 *** (0.000) |

| Env_punish | −0.417 * (0.091) | −0.422 * (0.089) | −0.117 ** (0.015) | −0.119 ** (0.011) |

| Green_patent | 0.046 ** (0.029) | 0.043 ** (0.039) | 0.014 ** (0.041) | 0.013 * (0.055) |

| ROA | 0.011 *** (0.004) | 0.003 *** (0.006) | ||

| Lev | 0.005 (0.194) | 0.001 (0.208) | ||

| Growth | −0.001 (0.141) | −0.001 (0.173) | ||

| First | 0.104 * (0.098) | 0.044 * (0.066) | ||

| Indp | 0.140 ** (0.013) | 0.427 ** (0.015) | ||

| Firm | Control | Control | Control | Control |

| Year | Control | Control | Control | Control |

| R_squared | 0.083 | 0.088 | 0.055 | 0.085 |

| Loglikelihood | −3215.061 | −3198.185 | −3367.883 | −3358.452 |

| AIC | 7798.123 | 7776.371 | 6743.767 | 6734.904 |

| BIC | 12,395.140 | 12,413.710 | 6770.655 | 6795.391 |

| Observations | 6129 | 6129 | 6129 | 6129 |

| (24) | (25) | (26) | (27) | |

|---|---|---|---|---|

| Probit | Probit | OLS_FE | OLS_FE | |

| Neg_news | 0.136 *** (0.000) | 0.120 *** (0.000) | 0.039 *** (0.000) | 0.035 *** (0.000) |

| Env_punish | 0.705 *** (0.002) | 0.714 *** (0.002) | 0.214 *** (0.002) | 0.215 *** (0.002) |

| Green_patent | −0.062 *** (0.005) | −0.060 *** (0.006) | −0.018 *** (0.007) | −0.017 *** (0.009) |

| ROA | −0.017 *** (0.000) | −0.005 *** (0.000) | ||

| Lev | −0.002 (0.708) | −0.001 (0.582) | ||

| Growth | 0.002 (0.112) | 0.001 (0.167) | ||

| First | −0.394 ** (0.049) | −0.116 * (0.058) | ||

| Indp | −0.150 *** (0.009) | −0.419 ** (0.015) | ||

| Firm | Control | Control | Control | Control |

| Year | Control | Control | Control | Control |

| R_squared | 0.081 | 0.087 | 0.084 | 0.104 |

| Loglikelihood | −3094.515 | −3074.293 | −3215.813 | −3194.724 |

| AIC | 7557.032 | 7526.587 | 6439.626 | 6407.449 |

| BIC | 12,154.050 | 12,157.210 | 6466.509 | 6467.936 |

| Observations | 6129 | 6129 | 6129 | 6129 |

| (43) | (44) | (45) | (46) | |

|---|---|---|---|---|

| Ordered_Probit | Ordered_Probit | OLS_FE | OLS_FE | |

| Neg_news | −0.180 *** (0.000) | −0.172 *** (0.000) | −0.122 *** (0.000) | −0.116 *** (0.000) |

| Env_punish | −0.869 *** (0.000) | −0.871 *** (0.000) | −0.585 *** (0.000) | −0.580 *** (0.000) |

| Green_patent | 0.056 ** (0.000) | 0.052 *** (0.001) | 0.357 *** (0.002) | 0.032 *** (0.004) |

| ROA | 0.011 *** (0.000) | 0.008 *** (0.000) | ||

| Lev | −0.001 (0.872) | −0.001 (0.661) | ||

| Growth | −0.001 (0.128) | −0.001 (0.143) | ||

| First | 0.876 *** (0.000) | 0.688 *** (0.000) | ||

| Indp | 0.218 *** (0.000) | 0.143 *** (0.000) | ||

| Firm | Control | Control | Control | Control |

| Year | Control | Control | Control | Control |

| R_squared | 0.275 | 0.280 | 0.195 | 0.334 |

| Loglikelihood | −7614.105 | −7569.915 | −7866.441 | −7933.429 |

| AIC | 16,608.210 | 16,529.834 | 15,740.880 | 15,653.600 |

| BIC | 21,318.250 | 21,274.148 | 15,768.190 | 15,715.030 |

| Observations | 6810 | 6810 | 6810 | 6810 |

References

- Huber, B.; Comstock, M. ESG reports and ratings: What they are, why they matter. Harvard Law School Forum Corporate Governance 2017. Available online: https://corpgov.law.harvard.edu/2017/07/27/esg-reports-and-ratings-what-they-are-why-they-matter/ (accessed on 28 May 2023).

- Liu, W.; Wang, Z. The effects of climate policy on corporate technological upgrading in energy intensive industries: Evidence from China. J. Clean. Prod. 2017, 142, 3748–3758. [Google Scholar] [CrossRef]

- Cheng, J.; Liu, Y. The effects of public attention on the environmental performance of high-polluting firms: Based on big data from web search in China. J. Clean. Prod. 2018, 186, 335–341. [Google Scholar] [CrossRef]

- Adhikari, B.K.; Agrawal, A. Peer influence on payout policies. J. Corp. Financ. 2018, 48, 615–637. [Google Scholar] [CrossRef]

- Grennan, J. Dividend payments as a response to peer influence. J. Financ. Econ. 2019, 131, 549–570. [Google Scholar] [CrossRef]

- Leary, M.T.; Roberts, M.R. Do peer firms affect corporate financial policy? J. Financ. 2014, 69, 139–178. [Google Scholar] [CrossRef]

- Kaustia, M.; Rantala, V. Social learning and corporate peer effects. J. Financ. Econ. 2015, 117, 653–669. [Google Scholar] [CrossRef]

- Joo, C.; Yang, I.; Yang, T. Peer group effect in firm cash holding policy: Evidence from Korean manufacturing firms. Asia-Pac. J. Financ. Stud. 2016, 45, 535–573. [Google Scholar] [CrossRef]

- Chen, Y.; Chan, K.; Chang, Y. Peer effects on corporate cash holdings. Int. Rev. Econ. Financ. 2019, 61, 213–227. [Google Scholar] [CrossRef]

- Bustamante, M.C.; Frésard, L. Does firm investment respond to peers’ investment? Manag. Sci. 2021, 67, 4703–4724. [Google Scholar] [CrossRef]

- Li, J.; Yao, F.K. The role of reference groups in international investment decisions by firms from emerging economies. J. Int. Manag. 2010, 16, 143–153. [Google Scholar] [CrossRef]

- Lin, X. Utilizing spatial autoregressive models to identify peer effects among adolescents. Empir. Econ. 2015, 49, 929–960. [Google Scholar] [CrossRef]

- Liu, Z.; Zhang, T.; Li, W.; Kuang, X. The neighborhood effects of provincial-level stock market participation in China. Physica A 2018, 509, 459–468. [Google Scholar] [CrossRef]

- Li, Y.; Zhang, X.; Yao, T.; Sake, A.; Liu, X.; Peng, N. The developing trends and driving factors of environmental information disclosure in China. J. Environ. Manag. 2021, 288, 112386. [Google Scholar] [CrossRef] [PubMed]

- Grieser, W.; Hadlock, C.; Lesage, J.; Zekhnini, M. Network effects in corporate financial policies. J. Financ. Econ. 2022, 144, 247–272. [Google Scholar] [CrossRef]

- Pan, X.; Xu, G.; Zhu, N. Spatial peer effect of enterprises’ digital transformation: Empirical evidence from spatial autoregressive models. Sustainability 2022, 14, 12576. [Google Scholar] [CrossRef]

- Zhao, Y.; Lin, F. Peer effects in management forecast precision decision: Evidence from a novel text-based network. Appl. Econ. Lett. 2023, 30, 1671–1675. [Google Scholar] [CrossRef]

- Zheng, H.; Ye, A. Direct imitation or indirect reference?-Research on peer effects of enterprises’ green innovation. Environ. Sci. Pollut. Res. 2023, 30, 41028–41044. [Google Scholar] [CrossRef] [PubMed]

- Yang, S.; Zhang, H.; Zhang, Q.; Liu, T. Peer effects of enterprise green financing behavior: Evidence from China. Front. Environ. Sci. 2022, 10, 1033868. [Google Scholar] [CrossRef]

- Siedschlag, I.; Yan, W. Firms’ green investments: What factors matter? J. Clean. Prod. 2021, 310, 127554. [Google Scholar] [CrossRef]

- Liu, S.; Wu, D. Competing by conducting good deeds: The peer effect of corporate social responsibility. Financ. Res. Lett. 2016, 16, 47–54. [Google Scholar] [CrossRef]

- Li, C.; Wang, X. Local peer effects of corporate social responsibility. J. Corp. Financ. 2022, 73, 102187. [Google Scholar] [CrossRef]

- Dong, Y.; Chen, S.; Wu, Y. Keeping up with the Joneses: The role of investee peers corporate environmental responsibility. Corp. Soc. Responsib. Environ. Manag. 2023, 30, 1841–1855. [Google Scholar] [CrossRef]

- Brasington, D.M.; Parent, O. Public school consolidation: A partial observability spatial bivariate probit approach. J. R. Stat. Soc. Ser. A-Stat. Soc. 2017, 180, 633–656. [Google Scholar] [CrossRef]

- Skevas, T.; Skevas, I.; Kalaitzandonakes, N. The role of peer effects on farmers’ decision to adopt unmanned aerial vehicles: Evidence from Missouri. Appl. Econ. 2022, 54, 1366–1376. [Google Scholar] [CrossRef]

- Long, W.; Li, S.; Wu, H.; Song, X. Corporate social responsibility and financial performance: The roles of government intervention and market competition. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 525–541. [Google Scholar] [CrossRef]

- Tan, X.; Yan, Y.; Dong, Y. Peer effect in green credit induced green innovation: An empirical study from China’s Green Credit Guidelines. Resour. Policy 2022, 76, 102619. [Google Scholar] [CrossRef]

- Martins, H.C. Competition and ESG practices in emerging markets: Evidence from a difference-in-differences model. Financ. Res. Lett. 2022, 46, 102371. [Google Scholar] [CrossRef]

- Cao, J.; Liang, H.; Zhan, X. Peer effects of corporate social responsibility. Manag. Sci. 2019, 65, 5487–5503. [Google Scholar] [CrossRef]

- Chen, C.; Jiang, D.; Li, W. Keeping up with the CSR Joneses: The impact of industry peers on focal firms’ CSR performance. Hum. Soc. Sci. Commun. 2023, 10, 106. [Google Scholar] [CrossRef]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Cambridge University Press: New York, NY, USA, 2010. [Google Scholar]

- Benlemlih, M. Corporate social responsibility and dividend policy. Res. Int. Bus. Financ. 2019, 47, 114–138. [Google Scholar] [CrossRef]

- Zahid, R.M.A.; Taran, A.; Khan, M.K.; Chersan, I.-C. ESG, dividend payout policy and the moderating role of audit quality: Empirical evidence from Western Europe. Borsa Istanb. Rev. 2023, 23, 350–367. [Google Scholar] [CrossRef]

- Zahid, R.M.A.; Khan, M.K.; Anwar, W.; Maqsood, U.S. The role of audit quality in the ESG-corporate financial performance nexus: Empirical evidence from Western Euro-pean companies. Borsa Istanb. Rev. 2022, 22, S200–S212. [Google Scholar] [CrossRef]

- Ambarish, R.; John, K.; Williams, J. Efficient signalling with dividends and investments. J. Financ. 1987, 42, 321–343. [Google Scholar] [CrossRef]

- Spence, M. Signaling in retrospect and the informational structure of markets. Am. Econ. Rev. 2002, 92, 434–459. [Google Scholar] [CrossRef]

- Banerjee, A.V. A simple model of herd behavior. Q. J. Econ. 1992, 107, 797–817. [Google Scholar] [CrossRef]

- Hisrich, R.D.; Peters, M.P.; Shepherd, D.A. Entrepreneurship; Irwin: Burr Ridge, IL, USA, 1998. [Google Scholar]

- Chen, M.-J.; MacMillan, I.C. Nonresponse and delayed response to competitive moves: The roles of competitor dependence and action irreversibility. Acad. Manag. J. 1992, 35, 539–570. [Google Scholar] [CrossRef]

- DiMaggio, P.J.; Powell, W.W. The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. Am. Sociol. Rev. 1983, 48, 147–160. [Google Scholar] [CrossRef]

- Haunschild, P.R.; Miner, A.S. Modes of interorganizational imitation: The effects of outcome salience and uncertainty. Adm. Sci. Q. 1997, 42, 472–500. [Google Scholar] [CrossRef]

- Li, B.; Pan, A.; Xu, L.; Liu, X.; Qin, S. Imprinting and peer effects in acquiring state ownership: Evidence from private firms in China. Pac.-Basin Financ. J. 2020, 61, 101337. [Google Scholar] [CrossRef]

- Wu, X.; Li, Y.; Feng, C. Green innovation peer effects in common institutional ownership networks. Corp. Soc. Responsib. Environ. Manag. 2023, 30, 641–660. [Google Scholar] [CrossRef]

- Park, K.; Yang, I.; Yang, T. The peer-firm effect on firm’s investment decisions. N. Am. Econ. Financ. 2017, 40, 178–199. [Google Scholar] [CrossRef]

- Li, W.; Wang, F.; Liu, T.; Xue, Q.; Liu, N. Peer effects of digital innovation behavior: An external environment perspective. Manag. Decis. 2023, 61, 2173–2200. [Google Scholar] [CrossRef]

- Yuan, D.; Shang, D.; Ma, Y.; Li, D. The spillover effects of peer annual report tone for firm innovation investment: Evidence from China. Technol. Forecast. Soc. Chang. 2022, 177, 121518. [Google Scholar] [CrossRef]

- Liu, Q.; Wang, J.; Chi, W. The spillover effects of innovation content disclosure in MD&A. Pac.-Basin Financ. J. 2022, 76, 101879. [Google Scholar] [CrossRef]

- Haller, S.A.; Siedschlag, I. Determinants of ICT adoption: Evidence from firm-level data. Appl. Econ. 2011, 43, 3775–3788. [Google Scholar] [CrossRef]

- Capelle-Blancard, G.; Petit, A. Every little helps? ESG news and stock market reaction. J. Bus. Ethics 2019, 157, 543–565. [Google Scholar] [CrossRef]

- Zahid, R.M.A.; Saleem, A.; Maqsood, U.S. ESG performance, capital financing decisions, and audit quality: Empirical evidence from Chinese state-owned enterprises. Environ. Sci. Pollut. Res. 2023, 30, 44086–44099. [Google Scholar] [CrossRef]

- Bhandari, A.; Javakhadze, D. Corporate social responsibility and capital allocation efficiency. J. Corp. Financ. 2017, 43, 354–377. [Google Scholar] [CrossRef]

- Stanaland, A.J.S.; Lwin, M.O.; Murphy, P.E. Consumer perceptions of the antecedents and consequences of corporate social responsibility. J. Bus. Ethics 2011, 102, 47–55. [Google Scholar] [CrossRef]

- Hur, W.-M.; Kim, H.; Woo, J. How CSR leads to corporate brand equity: Mediating mechanisms of corporate brand credibility and reputation. J. Bus. Ethics 2014, 125, 75–86. [Google Scholar] [CrossRef]

- Lin-Hi, N.; Blumberg, I. The link between (not) practicing CSR and corporate reputation: Psychological foundations and managerial implications. J. Bus. Ethics 2018, 150, 185–198. [Google Scholar] [CrossRef]

- Salmones, M.D.M.G.; Perez, A. Effectiveness of CSR advertising: The role of reputation, consumer attributions, and emotions. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 194–208. [Google Scholar] [CrossRef]

- Zhang, L.; Shan, Y.G.; Chang, M. Can CSR disclosure protect firm reputation during financial restatements? J. Bus. Ethics 2021, 173, 157–184. [Google Scholar] [CrossRef]

- Brammer, S.; Pavelin, S. Voluntary environmental disclosures by large UK companies. J. Bus. Finan. Account. 2006, 33, 1168–1188. [Google Scholar] [CrossRef]

- Boiral, O. Sustainability reports as simulacra? A counter-account of A and A plus GRI reports. Account. Audit. Account. 2013, 26, 1036–1071. [Google Scholar] [CrossRef]

- Luo, L.; Lan, Y.-C.; Tang, Q. Corporate incentives to disclose carbon information: Evidence from the CDP global 500 report. J. Int. Financ. Manag. Account. 2012, 23, 93–120. [Google Scholar] [CrossRef]

- Braam, G.J.M.; de Weerd, L.U.; Hauck, M.; Huijbregts, M.A.J. Determinants of corporate environmental reporting: The importance of environmental performance and assurance. J. Clean. Prod. 2016, 129, 724–734. [Google Scholar] [CrossRef]

- Wu, R.; Lin, B. Environmental regulation and its influence on energy-environmental performance: Evidence on the Porter Hypothesis from China’s iron and steel industry. Resour. Conserv. Recycl. 2022, 176, 105954. [Google Scholar] [CrossRef]

- You, D.; Zhang, Y.; Yuan, B. Environmental regulation and firm eco-innovation: Evidence of moderating effects of fiscal decentralization and political competition from listed Chinese industrial companies. J. Clean. Prod. 2019, 207, 1072–1083. [Google Scholar] [CrossRef]

- Zhang, J.; Zhang, W.; Song, Q.; Li, X.; Ye, X.; Liu, Y.; Xue, Y. Can energy saving policies drive firm innovation behaviors?-Evidence from China. Technol. Forecast. Soc. Chang. 2020, 154, 119953. [Google Scholar] [CrossRef]

- Zhao, X.; Liu, C.; Yang, M. The effects of environmental regulation on China’s total factor productivity: An empirical study of carbon-intensive industries. J. Clean. Prod. 2018, 179, 325–334. [Google Scholar] [CrossRef]

- Wang, Y.; Sun, X.; Guo, X. Environmental regulation and green productivity growth: Empirical evidence on the Porter Hypothesis from OECD industrial sectors. Energy Policy 2019, 132, 611–619. [Google Scholar] [CrossRef]

- Lu, S.; Cheng, B. Does environmental regulation affect firms’ ESG performance? Evidence from China. Manag. Decis. Econ. 2023, 44, 2004–2009. [Google Scholar] [CrossRef]

- Jiménez-Parra, B.; Alonso-Martínez, D.; Godos-Díez, J.-L. The influence of corporate social responsibility on air pollution: Analysis of environmental regulation and eco-innovation effects. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 1363–1375. [Google Scholar] [CrossRef]

- Zeng, J.; Ren, J.; Ning, Z. Mediating effect of corporate social responsibility-based entrepreneurship on environmental improvement: Evidence from 475 heavy-polluting enterprises. J. Bus. Res. 2022, 149, 506–517. [Google Scholar] [CrossRef]

- Zheng, J.; Khurram, M.U.; Chen, L. Can green innovation affect ESG ratings and financial performance? Evidence from Chinese GEM listed companies. Sustainability 2022, 14, 8677. [Google Scholar] [CrossRef]

- Wang, W.; Sun, Z.; Wang, W.; Hua, Q.; Wu, F. The impact of environmental uncertainty on ESG performance: Emotional vs. rational. J. Clean. Prod. 2023, 397, 136528. [Google Scholar] [CrossRef]

- Zheng, M.; Feng, G.-F.; Jiang, R.-A.; Chang, C.-P. Does environmental, social, and governance performance move together with corporate green innovation in China? Bus. Strateg. Environ. 2023, 32, 1670–1679. [Google Scholar] [CrossRef]

- Coad, A.; Teruel, M. Inter-firm rivalry and firm growth: Is there any evidence of direct competition between firms? Ind. Corp. Change 2013, 22, 397–425. [Google Scholar] [CrossRef][Green Version]

- Shroff, N.; Verdi, R.S.; Yost, B.P. When does the peer information environment matter? J. Account. Econ. 2017, 64, 183–214. [Google Scholar] [CrossRef]

- Schettini, D.; Azzoni, C.R.; Paez, A. Neighborhood and efficiency in manufacturing in Brazilian regions: A spatial Markov Chain analysis. Int. Reg. Sci. Rev. 2011, 34, 397–418. [Google Scholar] [CrossRef]

- Cho, H.; Muslu, V. How do firms change investments based on MD&A disclosures of peer firms? Account. Rev. 2021, 96, 177–204. [Google Scholar] [CrossRef]

- Fan, R.; Wang, Y.; Chen, F.; Du, K.; Wang, Y. How do government policies affect the diffusion of green innovation among peer enterprises?—An evolutionary-game model in complex networks. J. Clean. Prod. 2022, 364, 132711. [Google Scholar] [CrossRef]

- Cho, E.; Kim, J.; Kim, S. Spillover effect of regulatory accounting inspections on accounting quality of peer companies. Manag. Audit. J. 2020, 35, 685–704. [Google Scholar] [CrossRef]

- Elhorst, J.P. Spatial Econometrics: From Cross-Sectional Data to Spatial Panels; Springer: Heidelberg, Germany, 2014; pp. 26–87. [Google Scholar]

- Martinetti, D.; Geniaux, G. Approximate likelihood estimation of spatial probit models. Reg. Sci. Urban Econ. 2017, 64, 30–45. [Google Scholar] [CrossRef]

- Smith, T.E.; LeSage, J.P. A Bayesian probit model with spatial dependencies. In Spatial and Spatiotemporal Econometrics (Advances in Econometrics, Vol. 18); Lesage, J.P., Kelley Pace, R., Eds.; Emerald Group Publishing Limited: Bingley, UK, 2004; Volume 18, pp. 127–160. [Google Scholar]

- Wang, X.; Kockelman, K.M. Application of the dynamic spatial ordered probit model: Patterns of land development change in Austin, Texas. Pap. Reg. Sci. 2009, 88, 345–365. [Google Scholar] [CrossRef]

- Zhou, D.; Qiu, Y.; Wang, M. Does environmental regulation promote enterprise profitability? Evidence from the implementation of China’s newly revised Environmental Protection Law. Econ. Model. 2021, 102, 105585. [Google Scholar] [CrossRef]

- Lin, Y.; Fu, X.; Fu, X. Varieties in state capitalism and corporate innovation: Evidence from an emerging economy. J. Corp. Financ. 2021, 67, 101919. [Google Scholar] [CrossRef]

- Feng, J.; Goodell, J.W.; Shen, D. ESG rating and stock price crash risk: Evidence from China. Financ. Res. Lett. 2022, 46, 102476. [Google Scholar] [CrossRef]

- Yan, Y.; Cheng, Q.; Huang, M.; Lin, Q.; Lin, W. Government environmental regulation and corporate ESG performance: Evidence from natural resource accountability audits in China. Int. J. Environ. Res. Public Health 2023, 20, 447. [Google Scholar] [CrossRef]

- Cui, J.; Dai, J.; Wang, Z.; Zhao, X. Does environmental regulation induce green innovation? A panel study of Chinese listed firms. Technol. Forecast. Soc. Chang. 2022, 176, 121492. [Google Scholar] [CrossRef]

- Haque, F.; Ntim, C.G. Environmental policy, sustainable development, governance mechanisms and environmental performance. Bus. Strateg. Environ. 2018, 27, 415–435. [Google Scholar] [CrossRef]

- Pan, X.; Chen, X.; Yang, X. Examining the relationship between negative media coverage and corporate social responsibility. Bus. Ethics Environ. Responsib. 2022, 31, 620–633. [Google Scholar] [CrossRef]

- Gong, G.; Huang, X.; Wu, S.; Tian, H.; Li, W. Punishment by Securities Regulators, Corporate Social Responsibility and the Cost of Debt. J. Bus. Ethics 2021, 171, 337–356. [Google Scholar] [CrossRef]

- Hao, J.; He, F. Corporate social responsibility (CSR) performance and green innovation: Evidence from China. Financ. Res. Lett. 2022, 48, 102889. [Google Scholar] [CrossRef]

- Sandberg, H.; Alnoor, A.; Tiberius, V. Environmental, social, and governance ratings and financial performance: Evidence from the European food industry. Bus. Strateg. Environ. 2023, 32, 2471–2489. [Google Scholar] [CrossRef]

- Lemma, T.T.; Muttakin, M.; Mihret, D. Environmental, social, and governance performance, national cultural values and corporate financing strategy. J. Clean. Prod. 2022, 373, 133821. [Google Scholar] [CrossRef]

- Limkriangkrai, M.; Koh, S.; Durand, R.B. Environmental, social, and governance (ESG) profiles, stock returns, and financial policy: Australian evidence. Int. Rev. Financ. 2017, 17, 461–471. [Google Scholar] [CrossRef]

- Mahmood, A.N.; Arslan, H.M.; Younas, Z.I.; Komal, B.; Ali, K.; Mubeen, M. Understanding the dynamics of capital structure, corporate governance, and corporate social responsibility in high- and low-leveraged US and Chinese firms. Environ. Sci. Pollut. Res. 2023, 30, 46204–46221. [Google Scholar] [CrossRef]

- Bellandi, F. Equilibrating financially sustainable growth and environmental, social, and governance sustainable growth. Eur. Manag. Rev. 2023, in press. [Google Scholar] [CrossRef]

- Yue, L.; Huang, C.; Cao, Y. The impact of FDI technology spillover on the innovation quality of Chinese enterprises: A microperspective based on geographic proximity. Eur. J. Innov. Manag. 2022, in press. [Google Scholar] [CrossRef]

- Jiang, X.; Li, Y. The relationship between organizational learning and firms’ financial performance in strategic alliances: A contingency approach. J. World Bus. 2008, 43, 365–379. [Google Scholar] [CrossRef]

- Liu, M.; Shan, Y.; Li, Y. Heterogeneous Partners, R&D cooperation and corporate innovation capability: Evidence from Chinese manufacturing firms. Technol. Soc. 2023, 72, 102183. [Google Scholar] [CrossRef]

- Gyimah, D.; Machokoto, M.; Sikochi, A.S. Peer influence on trade credit. J. Corp. Financ. 2020, 64, 101685. [Google Scholar] [CrossRef]

- Hu, C.; Zhu, X.; Liu, R.; Teng, Z. The impact of external technology acquisition on enterprise innovation performance: The moderating effect of geographical distance. Technol. Anal. Strateg. Manag. 2023, in press. [Google Scholar] [CrossRef]

- Zhang, S.; Li, J.; Li, N. Partner technological heterogeneity and innovation performance of R&D alliances. R D Manag. 2022, 52, 3–21. [Google Scholar] [CrossRef]

- Ryou, J.W.; Tsang, A.; Wang, K.T. Product market competition and voluntary corporate social responsibility disclosures. Contemp. Account. Res. 2022, 39, 1215–1259. [Google Scholar] [CrossRef]

- Wang, H.; Cui, H.; Zhao, Q. Effect of green technology innovation on green total factor productivity in China: Evidence from spatial durbin model analysis. J. Clean. Prod. 2021, 288, 125624. [Google Scholar] [CrossRef]

- Fan, L.; Yang, K.; Liu, L. New media environment, environmental information disclosure and firm valuation: Evidence from high-polluting enterprises in China. J. Clean. Prod. 2020, 277, 123253. [Google Scholar] [CrossRef]

- Xiang, C.; van Gevelt, T. Central inspection teams and the enforcement of environmental regulations in China. Environ. Sci. Policy 2020, 112, 431–439. [Google Scholar] [CrossRef]

- Lambertini, L.; Poyago-Theotoky, J.; Tampieri, A. Cournot competition and “green” innovation: An inverted-U relationship. Energy Econ. 2017, 68, 116–123. [Google Scholar] [CrossRef]

- Zeng, H.; Li, X.; Zhou, Q.; Wang, L. Local government environmental regulatory pressures and corporate environmental strategies: Evidence from natural resource accountability audits in China. Bus. Strateg. Environ. 2022, 31, 3060–3082. [Google Scholar] [CrossRef]

| Variable | Definition | Data Source |

|---|---|---|

| Dependent variables | ||

| ESG performance | We apply the Sino-Securities ESG rating to demonstrate corporate ESG level and use the logarithm of the manually assigned number from 9 to 1 of each level as the ESG performance. | WIND database |

| ESG level increase | A binary dependent variable that equals one if the corporate ESG rating increased from the previous year, otherwise it is zero. | Calculated based on ESG performance |

| ESG level decrease | A binary dependent variable that equals one if corporate ESG rating decreased from the previous year, otherwise it is zero. | Calculated based on ESG performance |

| ESG level | An ordered dependent variable that corresponds to each ESG rating by manually assigning a number from 9 to 1. | WIND database |

| Core explanatory variables | ||

| Negative web news | Negative news is measured by the natural logarithm of the number of negative web news reports about a firm during the year. | CNRDS database |

| Environmental punishment | Environmental punishment is a dummy variable that equals one if a firm is punished due to environmental issues during the year and is zero otherwise. | CNRDS database |

| Green patent | Green patent is measured by the natural logarithm of the number of firm’s registered green patents during the year. | CNRDS database |

| Control variables | ||

| Return on assets | Return on assets is a measure of a corporation’s capital performance, which equals the fiscal year-end net income divided by total assets. | CNRDS database |

| Book leverage | Leverage is measured by a corporation’s total year-end debt divided by year-end total assets. | CNRDS database |

| Profit growth ratio | Profit growth ratio is the growth rate of the corporation’s year-end net profit. | CNRDS database |

| The large shareholders’ ratio | The total shareholding ratio of the largest ten shareholders. | CNRDS database |

| The strength of independent director | The proportion of independent directors on the board of directors. | CNRDS database |

| Spatial weight matrices | ||

| Geography spatial weight matrix | The element of geography weight matrix equals one if the two matched different corporations are located in the same province, otherwise it is zero. | Constructed based on CSRC registered information in WIND database |

| Industry spatial weight matrix | The element of industry weight matrix equals one if the two matched different corporations belong to the same industry, otherwise it is zero. | Constructed based on CSRC industry classification standard in WIND database |

| Product spatial weight matrix | The element of product weight matrix equals one if the two matched different corporations have the same main product type, otherwise it is zero. | Constructed based on CSRC listed firms’ main product information in WIND database |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| OLS_FE | OLS_FE | OLS_RE | OLS_RE | |

| Neg_news | −0.026 *** (0.000) | −0.025 *** (0.000) | −0.021 *** (0.000) | −0.020 *** (0.000) |

| Env_punish | −0.121 *** (0.000) | −0.120 *** (0.000) | −0.108 *** (0.000) | −0.104 *** (0.000) |

| Green_patent | 0.006 ** (0.019) | 0.005 ** (0.037) | 0.015 *** (0.000) | 0.014 *** (0.000) |

| ROA | 0.002 *** (0.000) | 0.003 *** (0.000) | ||

| Lev | −0.005 (0.353) | −0.001 (0.190) | ||

| Growth | −0.002 (0.117) | −0.001 (0.163) | ||

| First | 0.182 *** (0.000) | 0.179 *** (0.000) | ||

| Indp | 0.289 *** (0.000) | 0.291 *** (0.000) | ||

| _cons | 1.693 *** (0.000) | 1.472 *** (0.000) | 1.660 *** (0.000) | 1.439 *** (0.000) |

| Firm | Control | Control | ||

| Year | Control | Control | ||

| R_squared | 0.159 | 0.304 | 0.140 | 0.284 |

| Hausman’s | 71.240 *** (0.000) | 171.410 *** (0.000) | ||

| Loglikelihood | 1997.349 | 2047.792 | ||

| AIC | −3986.698 | −4077.584 | ||

| BIC | −3959.394 | −4016.148 | ||

| Observations | 6810 | 6810 | 6810 | 6810 |

| (11) | (12) | (13) | |

|---|---|---|---|

| SDM_W1 | SDM_W2 | SDM_W3 | |

| W × ESG_perform | 0.136 *** (0.000) | 0.217 *** (0.000) | 0.094 *** (0.000) |

| Neg_news | −0.035 *** (0.000) | −0.037 *** (0.000) | −0.034 *** (0.000) |

| Env_punish | −0.121 *** (0.000) | −0.122 *** (0.000) | −0.120 *** (0.000) |

| Green_patent | 0.011 *** (0.000) | 0.009 ** (0.010) | 0.008 ** (0.010) |

| W × Neg_news | 0.021 ** (0.015) | 0.034 *** (0.000) | 0.024 *** (0.005) |

| W × Env_punish | 0.216 (0.191) | 0.297 * (0.060) | 0.214 * (0.093) |

| W × Green_patent | −0.033 *** (0.000) | −0.005 (0.531) | −0.008 (0.278) |

| ROA | 0.002 *** (0.001) | 0.002 ** (0.010) | 0.002 *** (0.001) |

| Lev | −0.005 (0.638) | −0.005 (0.630) | −0.005 (0.637) |

| Growth | −0.001 (0.452) | −0.001 (0.477) | −0.001 (0.474) |

| First | 0.156 *** (0.001) | 0.158 *** (0.001) | 0.167 *** (0.001) |

| Indp | 0.293 *** (0.000) | 0.296 *** (0.000) | 0.296 *** (0.000) |

| Firm | Control | Control | Control |

| Year | Control | Control | Control |

| R_squared | 0.382 | 0.362 | 0.339 |

| Hausman | 125.610 *** (0.000) | 132.360 *** (0.000) | 129.140 *** (0.000) |

| Wald_sar | 21.050 *** (0.000) | 16.250 *** (0.001) | 12.010 *** (0.007) |

| Wald_sem | 17.760 *** (0.000) | 11.240 ** (0.011) | 10.030 ** (0.018) |

| Loglikelihood | 2082.289 | 2081.761 | 2065.833 |

| AIC | −4138.580 | −4137.523 | −4105.666 |

| BIC | −4049.848 | −4048.783 | −4016.926 |

| Observations | 6810 | 6810 | 6810 |

| SDM_W1 | SDM_W2 | SDM_W3 | ||

|---|---|---|---|---|

| Neg_news | −0.016 * (0.051) | −0.003 (0.733) | −0.010 (0.164) | |

| Total _effect | Env_punish | 0.121 (0.535) | 0.236 (0.249) | 0.109 (0.455) |

| Green_patent | −0.025 ** (0.012) | 0.004 (0.693) | 0.001 (0.919) | |

| Neg_news | −0.035 *** (0.000) | −0.037 *** (0.000) | −0.034 *** (0.000) | |

| Direct _effect | Env_punish | −0.121 *** (0.000) | −0.121 *** (0.000) | −0.119 *** (0.000) |

| Green_patent | 0.011 *** (0.000) | 0.009 *** (0.005) | 0.008 *** (0.006) | |

| Neg_news | 0.019 ** (0.040) | 0.034 ** (0.003) | 0.023 *** (0.009) | |

| Indirect _effect | Env_punish | 0.242 (0.196) | 0.357 * (0.074) | 0.229 * (0.069) |

| Green_patent | −0.037 *** (0.000) | −0.005 (0.634) | −0.008 (0.279) |

| (18) | (19) | (20) | (21) | (22) | (23) | |

|---|---|---|---|---|---|---|

| SAR_ Probit_W1 | SAR_ Probit_W1 | SAR_ Probit_W2 | SAR_ Probit_W2 | SAR_ Probit_W3 | SAR_ Probit_W3 | |

| W × ESG_levelup | 0.615 *** (0.000) | 0.615 *** (0.000) | 0.639 *** (0.002) | 0.621 *** (0.003) | 0.325 ** (0.014) | 0.317 ** (0.018) |

| Neg_news | −0.105 *** (0.000) | −0.099 *** (0.000) | −0.106 *** (0.000) | −0.101 *** (0.000) | −0.111 *** (0.000) | −0.106 *** (0.000) |

| Env_punish | −0.469 * (0.059) | −0.475 * (0.057) | −0.431 * (0.082) | −0.435 * (0.080) | −0.424 * (0.086) | −0.428 * (0.084) |

| Green_patent | 0.039 * (0.061) | 0.038 * (0.079) | 0.041 * (0.052) | 0.039 * (0.067) | 0.043 ** (0.041) | 0.041 * (0.053) |

| ROA | 0.009 *** (0.004) | 0.010 *** (0.006) | 0.011 *** (0.005) | |||

| Lev | 0.006 (0.175) | 0.005 (0.193) | 0.005 (0.200) | |||

| Growth | −0.001 (0.138) | −0.001 (0.144) | −0.001 (0.340) | |||

| First | 0.104 * (0.068) | 0.118* (0.058) | 0.109 * (0.083) | |||

| Indp | 0.140 ** (0.013) | 0.143 ** (0.011) | 0.143 ** (0.011) | |||

| Firm | Control | Control | Control | Control | Control | Control |

| Year | Control | Control | Control | Control | Control | Control |

| R_squared | 0.085 | 0.088 | 0.085 | 0.087 | 0.084 | 0.086 |

| Loglikelihood | −3207.518 | −3198.185 | −3210.464 | −3201.380 | −3212.080 | −3202.884 |

| AIC | 7785.037 | 7776.371 | 7790.929 | 7782.761 | 7794.161 | 7785.768 |

| BIC | 12,388.781 | 12,413.716 | 12,394.672 | 12,420.173 | 12,397.934 | 12,423.113 |

| Observations | 6129 | 6129 | 6129 | 6129 | 6129 | 6129 |

| (28) | (29) | (30) | (31) | (32) | (33) | |

|---|---|---|---|---|---|---|

| SAR_ Probit_W1 | SAR_ Probit_W1 | SAR_ Probit_W2 | SAR_ Probit_W2 | SAR_ Probit_W3 | SAR_ Probit_W3 | |

| W × ESG _leveldown | 0.622 *** (0.001) | 0.620 *** (0.001) | 0.697 *** (0.002) | 0.682 *** (0.002) | 0.073 (0.603) | 0.064 (0.651) |

| Neg_news | 0.129 *** (0.000) | 0.114 *** (0.000) | 0.129 *** (0.000) | 0.114 *** (0.000) | 0.134 *** (0.000) | 0.119 *** (0.000) |

| Env_punish | 0.718 *** (0.001) | 0.727 *** (0.001) | 0.714 *** (0.001) | 0.724 *** (0.001) | 0.706 *** (0.002) | 0.715 *** (0.001) |

| Green_patent | −0.059 * (0.061) | −0.057 *** (0.009) | −0.056 ** (0.011) | −0.054 ** (0.014) | −0.061 *** (0.005) | −0.059 *** (0.007) |

| ROA | −0.017 *** (0.000) | −0.017 *** (0.000) | −0.017 *** (0.000) | |||

| Lev | −0.002 (0.639) | −0.001 (0.757) | −0.002 (0.713) | |||

| Growth | 0.002 (0.123) | 0.001 (0.111) | 0.002 (0.111) | |||

| First | −0.399 ** (0.043) | −0.413 ** (0.031) | −0.398 ** (0.045) | |||

| Indp | −0.151 *** (0.009) | −0.154 *** (0.008) | −0.150 *** (0.009) | |||

| Firm | Control | Control | Control | Control | Control | Control |

| Year | Control | Control | Control | Control | Control | Control |

| R_squared | 0.083 | 0.088 | 0.085 | 0.088 | 0.081 | 0.086 |

| Loglikelihood | −3088.502 | −3068.556 | −3089.567 | −3069.605 | −3094.381 | −3074.191 |

| AIC | 7547.004 | 7517.112 | 7549.134 | 7519.216 | 7558.761 | 7528.381 |

| BIC | 12,150.741 | 12,154.455 | 12,152.872 | 12,156.553 | 12,162.545 | 12,165.723 |

| Observations | 6129 | 6129 | 6129 | 6129 | 6129 | 6129 |

| (34) | (35) | (36) | (37) | (38) | (39) | |

|---|---|---|---|---|---|---|

| SEM_W1 | SEM_W1 | SEM_W2 | SEM_W2 | SEM_W3 | SEM_W3 | |

| W × Residual | 0.190 *** (0.000) | 0.173 *** (0.000) | 0.270 *** (0.000) | 0.250 *** (0.000) | 0.111 *** (0.000) | 0.087 *** (0.000) |

| Neg_news | −0.030 *** (0.000) | −0.027 *** (0.000) | −0.032 *** (0.000) | −0.029 *** (0.000) | −0.028 *** (0.000) | −0.027 *** (0.000) |

| Env_punish | −0.125 *** (0.000) | −0.124 *** (0.000) | −0.127 *** (0.000) | −0.125 *** (0.000) | −0.124 *** (0.000) | −0.122 *** (0.000) |

| Green_patent | 0.008 *** (0.006) | 0.007 ** (0.014) | 0.007 ** (0.017) | 0.006 ** (0.035) | 0.007 ** (0.024) | 0.006 ** (0.045) |

| ROA | 0.002 *** (0.001) | 0.002 *** (0.002) | 0.002 *** (0.001) | |||

| Lev | −0.005 (0.664) | −0.006 (0.595) | −0.005 (0.616) | |||

| Growth | −0.001 (0.452) | −0.001 (0.475) | −0.002 (0.452) | |||

| First | 0.174 *** (0.000) | 0.169 *** (0.001) | 0.179 *** (0.000) | |||

| Indp | 0.274 *** (0.001) | 0.296 *** (0.000) | 0.289 *** (0.001) | |||

| Firm | Control | Control | Control | Control | Control | Control |

| Year | Control | Control | Control | Control | Control | Control |

| R_squared | 0.159 | 0.302 | 0.159 | 0.301 | 0.159 | 0.304 |

| Loglikelihood | 2013.224 | 2056.800 | 2021.567 | 2067.764 | 2005.879 | 2055.106 |

| AIC | −4016.449 | −4101.404 | −4033.136 | −4115.529 | −4001.758 | −4090.212 |

| BIC | −3982.318 | −4033.143 | −3999.005 | −4047.268 | −3967.627 | −4090.212 |

| Observations | 6810 | 6810 | 6810 | 6810 | 6810 | 6810 |

| Panel A: IV-2SLS First Stage (Dependent Variable: ) | |||

|---|---|---|---|

| (40) | (41) | (42) | |

| W1 | W2 | W3 | |

| IVs | 0.439 *** (0.000) | 0.502 *** (0.000) | 0.382 *** (0.000) |

| Controls | Yes | Yes | Yes |

| Firm | Control | Control | Control |

| Year | Control | Control | Control |

| Stock–Yogo weak ID F-test 10% critical value | 16.380 | 16.380 | 16.380 |

| Cragg–Donald–Wald F-statistic | 1195.290 | 1734.160 | 873.440 |

| Kleibergen–Paap–Wald rk F-statistic | 851.800 | 445.100 | 165.220 |

| Kleibergen–Paap rk LM-statistic | 204.560 *** (0.000) | 259.900 *** (0.000) | 70.780 *** (0.000) |

| Observations | 6129 | 6129 | 6129 |

| Panel B: IV-2SLS Second stage (Dependent variable: ) | |||

| IVs | 0.513 *** (0.001) | 0.754 *** (0.000) | 0.434 *** (0.001) |

| Neg_news | −0.025 *** (0.000) | −0.025 *** (0.000) | −0.025 *** (0.000) |

| Env_punish | −0.136 *** (0.000) | −0.139 *** (0.000) | −0.135 *** (0.000) |

| Green_patent | 0.008 ** (0.011) | 0.005 * (0.096) | 0.006 * (0.051) |

| ROA | 0.002 *** (0.001) | 0.002 *** (0.001) | 0.002 *** (0.001) |

| Lev | −0.003 (0.803) | −0.005 (0.628) | −0.004 (0.654) |

| Growth | −0.002 (0.412) | −0.002 (0.448) | −0.002 (0.411) |

| First | 0.166 *** (0.003) | 0.162 *** (0.004) | 0.170 *** (0.003) |

| Indp | 0.267 *** (0.004) | 0.302 *** (0.001) | 0.287 *** (0.002) |

| Firm | Control | Control | Control |

| Year | Control | Control | Control |

| Adj R_squared | 0.321 | 0.332 | 0.273 |

| Observations | 6129 | 6129 | 6129 |

| (47) | (48) | (49) | (50) | (51) | (52) | |

|---|---|---|---|---|---|---|

| SAR_ Probit_W1 | SAR_ Probit_W1 | SAR_ Probit_W2 | SAR_ Probit_W2 | SAR_ Probit_W3 | SAR_ Probit_W3 | |

| W × ESG_level | 0.388 *** (0.000) | 0.376 *** (0.000) | 0.640 *** (0.000) | 0.627 *** (0.000) | 0.333 *** (0.000) | 0.330 *** (0.000) |

| Neg_news | −0.169 *** (0.000) | −0.162 *** (0.000) | −0.163 *** (0.000) | −0.156 *** (0.000) | −0.169 *** (0.000) | −0.161 *** (0.000) |

| Env_punish | −0.901 *** (0.000) | −0.902 *** (0.000) | −0.915 *** (0.000) | −0.915 *** (0.000) | −0.896 *** (0.000) | −0.898 *** (0.000) |

| Green_patent | 0.059 *** (0.000) | 0.055 *** (0.000) | 0.050 *** (0.001) | 0.046 *** (0.003) | 0.054 *** (0.000) | 0.050 *** (0.001) |

| ROA | 0.011 *** (0.000) | 0.010 *** (0.000) | 0.011 *** (0.000) | |||

| Lev | 0.001 (0.981) | −0.006 (0.837) | −0.005 (0.845) | |||

| Growth | −0.001 (0.127) | −0.001 (0.228) | −0.001 (0.423) | |||

| First | 0.878 *** (0.000) | 0.881 *** (0.000) | 0.894 *** (0.000) | |||

| Indp | 0.209 *** (0.000) | 0.221 *** (0.000) | 0.216 *** (0.000) | |||

| Firm | Control | Control | Control | Control | Control | Control |

| Year | Control | Control | Control | Control | Control | Control |

| R_squared | 0.277 | 0.281 | 0.279 | 0.283 | 0.278 | 0.282 |

| Loglikelihood | −7597.089 | −7553.970 | −7575.630 | −7533.117 | −7592.841 | −7549.018 |

| AIC | 16,576.180 | 16,499.947 | 16,533.260 | 16,458.242 | 16,567.684 | 16,490.044 |

| BIC | 21,293.051 | 21,250.946 | 21,250.132 | 21,209.231 | 21,284.553 | 21,241.043 |

| Observations | 6810 | 6810 | 6810 | 6810 | 6810 | 6810 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhao, H.; Lei, A.; Li, Y.; Hong, D. The Sectoral and Regional Peer Influences on Heavy-Pollution Corporate Environmental, Social, and Governance Performance. Sustainability 2023, 15, 12925. https://doi.org/10.3390/su151712925

Zhao H, Lei A, Li Y, Hong D. The Sectoral and Regional Peer Influences on Heavy-Pollution Corporate Environmental, Social, and Governance Performance. Sustainability. 2023; 15(17):12925. https://doi.org/10.3390/su151712925

Chicago/Turabian StyleZhao, Hui, Ao Lei, Yuhui Li, and Dingjun Hong. 2023. "The Sectoral and Regional Peer Influences on Heavy-Pollution Corporate Environmental, Social, and Governance Performance" Sustainability 15, no. 17: 12925. https://doi.org/10.3390/su151712925

APA StyleZhao, H., Lei, A., Li, Y., & Hong, D. (2023). The Sectoral and Regional Peer Influences on Heavy-Pollution Corporate Environmental, Social, and Governance Performance. Sustainability, 15(17), 12925. https://doi.org/10.3390/su151712925