The Path to Green Development: The Impact of a Carbon Emissions Trading Scheme on Enterprises’ Environmental Protection Investments

Abstract

:1. Introduction

2. Literature Review

3. Theoretical Analysis and Research Hypotheses

4. Research Design

4.1. Econometrics Model

4.2. Variables

4.2.1. Independent Variables

4.2.2. Dependent Variables

4.2.3. Control Variables

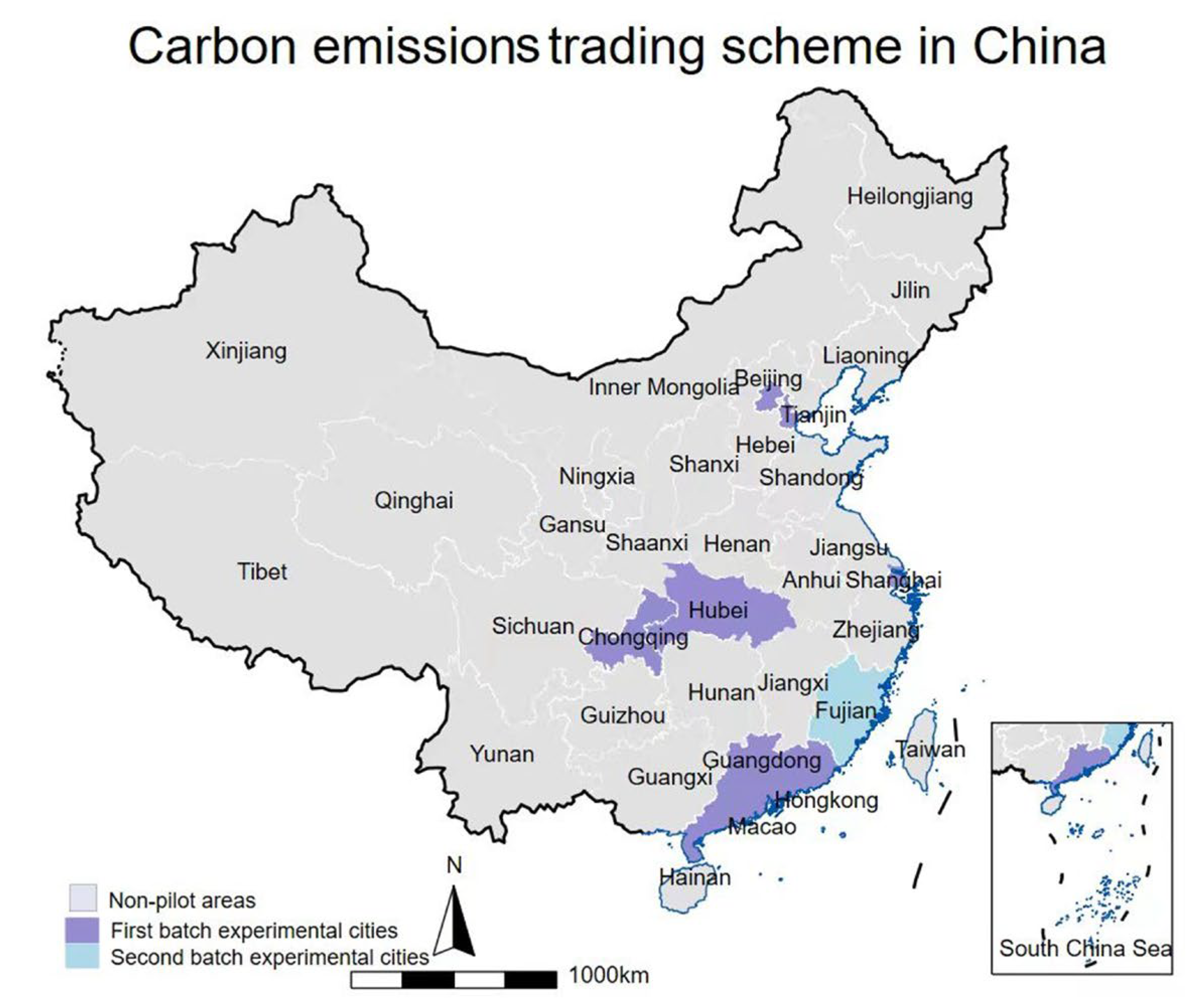

4.3. Data Sources

5. Empirical Results

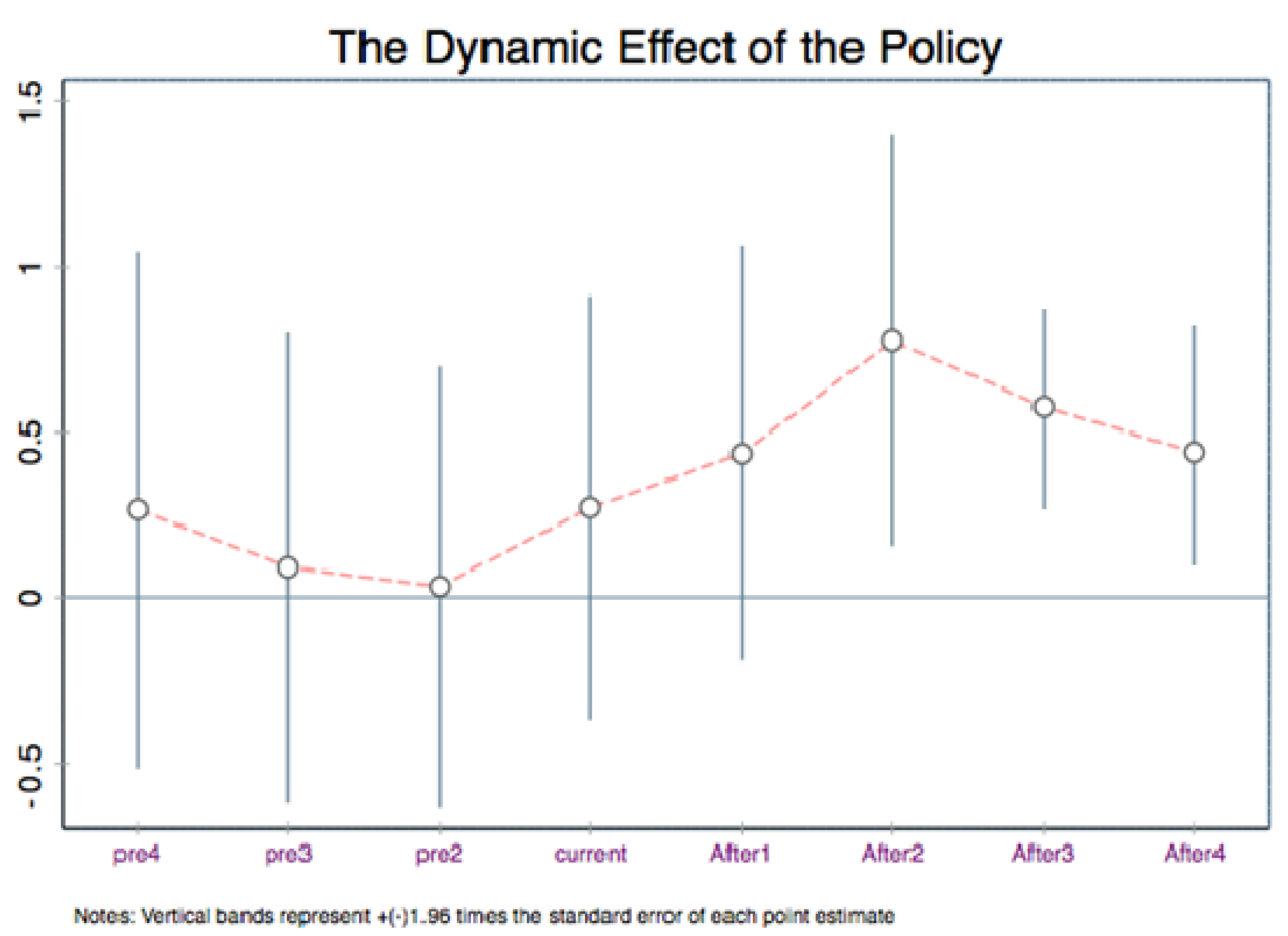

5.1. Parallel Trend Test

5.2. The Results of Benchmark Regression

5.3. Robustness Test

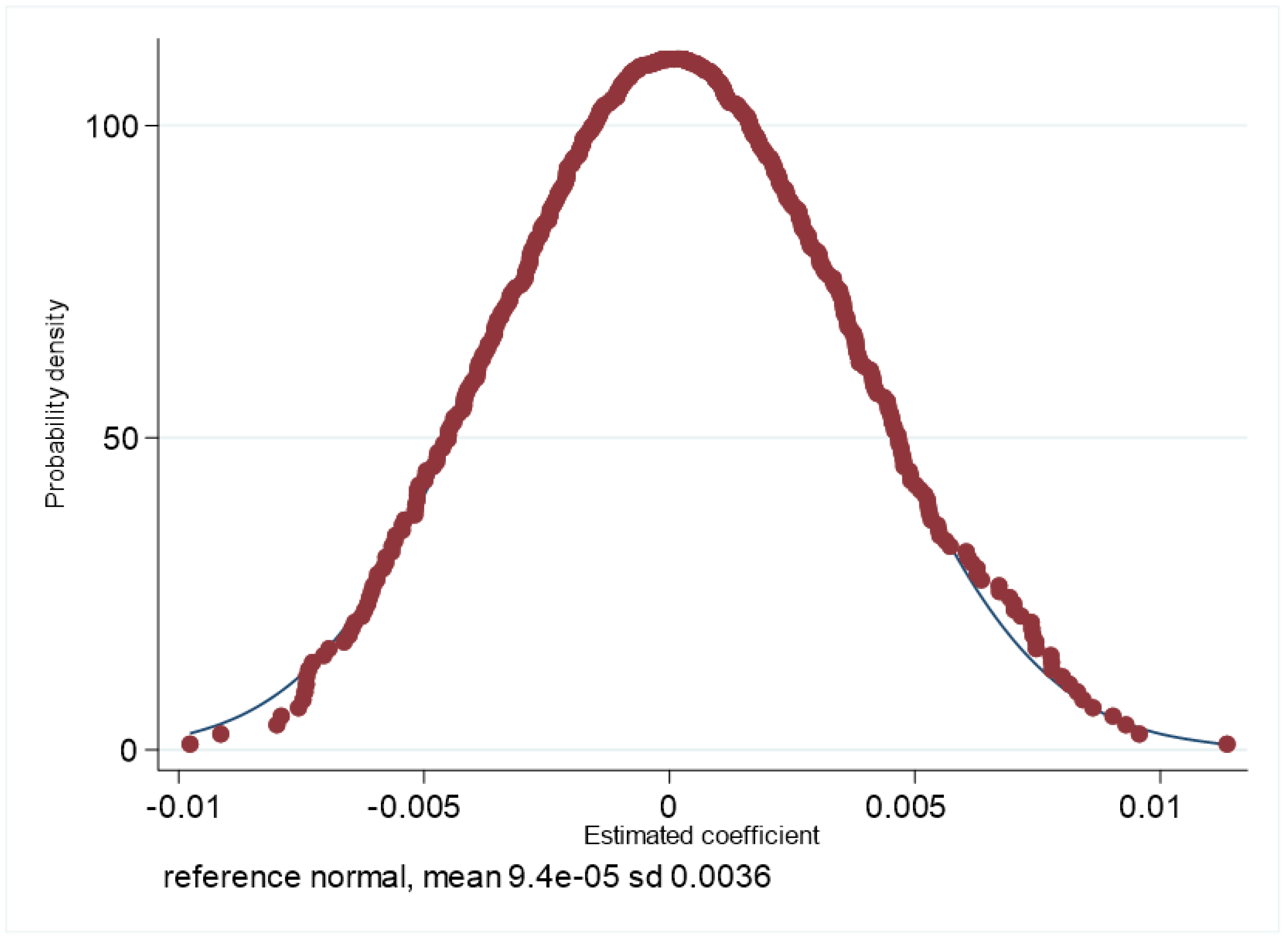

5.3.1. Placebo Test

5.3.2. PSM-DID

6. Further Analysis

6.1. The Mechanism Analysis

6.2. Heterogeneity Analysis

7. Conclusions and Policy Implications

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Duan, K.; Ren, X.; Wen, F.; Chen, J. Evolution of the information transmission between Chinese and international oil markets: A quantile-based framework. J. Commod. Mark. 2023, 29, 100304. [Google Scholar] [CrossRef]

- Duanmu, J.L.; Bu, M.L.; Pittman, R. Does market competition dampenenvironmental performance: Evidence from China. Strat. Manag. J. 2018, 39, 3006–3030. [Google Scholar] [CrossRef]

- Huang, L.; Lei, Z. How environmental regulation affect corporate green investment: Evidence from China. J. Clean. Prod. 2021, 279, 123560. [Google Scholar] [CrossRef]

- Chen, L.; Dong, T.; Nan, G.; Xiao, Q.; Xu, M.; Ming, J. Impact of the introduction of marketplace channel on e-tailer’s logistics service strategy. Manag. Decis. Econ. 2023, 44, 2835–2855. [Google Scholar] [CrossRef]

- Wang, Q.; Dou, J.S.; Jia, S.H. A meta-analytic review of corporate social responsibility and corporate financial performance: The moderating effect of contextual factors. Bus. Soc. 2015, 4, 1083–1121. [Google Scholar] [CrossRef]

- Gao, D.; Yan, Z.; Zhou, X.; Mo, X. Smarter and Prosperous: Digital Transformation and Enterprise Performance. Systems 2023, 11, 329. [Google Scholar] [CrossRef]

- Jiang, J.; Xie, D.; Ye, B.; Shen, B.; Chen, Z. Research on China’s cap-and-trade carbon emission trading scheme: Overview and outlook. Appl. Energy 2016, 178, 902–917. [Google Scholar] [CrossRef]

- Ren, X.; Li, W.; Duan, K.; Zhang, X. Does climate policy uncertainty really affect corporate financialization? Environ. Dev. Sustain. 2023, 1–19. [Google Scholar] [CrossRef]

- Gao, D.; Li, Y.; Tan, L. Can environmental regulation break the political resource curse: Evidence from heavy polluting private listed companies in China. J. Environ. Plan. Manag. 2023, 1–27. [Google Scholar] [CrossRef]

- Teixidó, J.; Verde, S.F.; Nicolli, F. The impact of the EU Emissions Trading System on low-carbon technological change: The empirical evidence. Ecol. Econ. 2019, 164, 106347. [Google Scholar] [CrossRef]

- Huang, Y.; Duan, K.; Urquhart, A. Time-varying dependence between Bitcoin and green financial assets: A comparison between pre-and post-COVID-19 periods. J. Int. Financ. Mark. Inst. Money 2023, 82, 101687. [Google Scholar] [CrossRef]

- Dai, S.L.; Qian, Y.W.; He, W.J.; Wang, C.; Shi, T.Y. The spatial spillover effect of China’s carbon emissions trading policy on industrial carbon intensity: Evidence from a spatial difference-in-difference method. Struct. Change Econ. Dyn. 2022, 63, 139–149. [Google Scholar] [CrossRef]

- Chen, L.; Dong, T.; Peng, J.; Ralescu, D. Uncertainty Analysis and Optimization Modeling with Application to Supply Chain Management: A Systematic Review. Mathematics 2023, 11, 2530. [Google Scholar] [CrossRef]

- Gao, D.; Tan, L.; Mo, X.; Xiong, R. Blue Sky Defense for Carbon Emission Trading Policies: A Perspective on the Spatial Spillover Effects of Total Factor Carbon Efficiency. Systems 2023, 11, 382. [Google Scholar] [CrossRef]

- Zhang, L.; Cao, C.; Tang, F.; He, J.; Li, D. Does China’s emissions trading system foster corporate green innovation? Evidence from regulating listed companies. Technol. Anal. Strategy Manag. 2019, 31, 199–212. [Google Scholar] [CrossRef]

- Li, G.; Wen, H. The low-carbon effect of pursuing the honor of civilization? A quasi-experiment in Chinese cities. Econ. Anal. Policy 2023, 78, 343–357. [Google Scholar] [CrossRef]

- Mo, J.Y. Technological innovation and its impact on carbon emissions: Evidence from Korea manufacturing firms participating emission trading scheme. Technol. Anal. Strateg. Manag. 2022, 34, 47–57. [Google Scholar] [CrossRef]

- Smale, R.; Hartley, M.; Hepburn, C.; Ward, J.; Grubb, M. The impact of CO2 emissions trading on firm profits and market prices. In Emissions Trading and Competitiveness; Routledge: Abingdon-on-Thames, UK, 2012; pp. 31–48. [Google Scholar]

- Li, G.; Gao, D.; Li, Y. Impacts of Market-based Environmental Regulation on Green Total Factor Energy Efficiency in China. China World Econ. 2023, 31, 92–114. [Google Scholar] [CrossRef]

- Hart, S.L.; Ahuja, G. Does it pay to be green? An empirical examination of the relationship between emission reduction and firm performance. Bus. Strategy Environ. 1996, 5, 30–37. [Google Scholar] [CrossRef]

- Liu, G.; Yang, Z.; Zhang, F.; Zhang, N. Environmental tax reform and environmental investment: A quasi-natural experiment based on China’s Environmental Protection Tax Law. Energy Econ. 2022, 109, 1060. [Google Scholar] [CrossRef]

- Tang, G.; Li, L.; Wu, D. Environmental regulation, industry attributes and corporate environmental investment. Account. Res. 2013, 6, 83–89, 96. [Google Scholar]

- Chen, Y.; Ma, Y. Does green investment improve energy firm performance? Energy Policy 2021, 153, 112252. [Google Scholar] [CrossRef]

- Martin, R.; Muûls, M.; Wagner, U.J. The impact of the European union emissions trading scheme on regulated firms: What is the evidence after ten years? Rev. Environ. Econ. Policy 2016, 10, 129–148. [Google Scholar] [CrossRef]

- Wei, Y.; Zhu, R.; Tan, L. Emission trading scheme, technological innovation, and competitiveness: Evidence from China’s thermal power enterprises. J. Environ. Manag. 2022, 320, 115874. [Google Scholar] [CrossRef] [PubMed]

- Hu, J.; Pan, X.; Huang, Q. Quantity or quality? The impacts of environmental regulation on firms’ innovation-Quasi-natural experiment based on China’s carbon emissions trading pilot. Technol. Forecast. Soc. Chang. 2020, 158, 120122. [Google Scholar] [CrossRef]

- Kunapatarawong, R.; Martínez-Ros, E. Towards green growth: How does green innovation affect employment? Res. Policy 2016, 45, 1218–1232. [Google Scholar] [CrossRef]

- Li, G.; Gao, D.; Shi, X.X. How does information and communication technology affect carbon efficiency? Evidence at China’s city level. Energy Environ. 2023, 0958305X231156405. [Google Scholar] [CrossRef]

- Yao, Y.; Hu, D.; Yang, C.; Tan, Y. The impact and mechanism of fintech on green total factor productivity. Green Financ. 2021, 3, 198–221. [Google Scholar] [CrossRef]

- Keohane, N.; Petsonk, A.; Hanafi, A. Toward a club of carbon markets. Clim. Chang. 2017, 144, 81–95. [Google Scholar] [CrossRef]

- Liu, M.; Li, Y. Environmental regulation and green innovation: Evidence from China’s carbon emissions trading policy. Financ. Res. Lett. 2022, 48, 103051. [Google Scholar] [CrossRef]

- Xu, W.; Wan, B.; Zhu, T.; Shao, M. CO2 emissions from China’s iron steel industry. J. Clean Prod. 2016, 139, 1504–1511. [Google Scholar] [CrossRef]

- Yang, S. Carbon emission trading policy and firm’s environmental investment. Financ. Res. Lett. 2023, 54, 103695. [Google Scholar] [CrossRef]

- Duan, K.; Zhao, Y.; Wang, Z.; Chang, Y. Asymmetric spillover from Bitcoin to green and traditional assets: A comparison with gold. Int. Rev. Econ. Financ. 2023, 88, 1397–1417. [Google Scholar] [CrossRef]

- Zhang, Q.; Yu, Z.; Kong, D. The real effect of legal institutions: Environmental courts firm environmental protection expenditure. J. Environ. Econ. Manag. 2019, 98, 102254. [Google Scholar] [CrossRef]

- Liu, L.; Zhao, Z.; Zhang, M.; Zhou, D. Green investment efficiency in the Chinese energy sector: Overinvestment or underinvestment? Energy Policy 2022, 160, 112694. [Google Scholar] [CrossRef]

- Yang, L.; Qin, H.; Gan, Q.; Su, J. Internal control quality, enterprise environmental protection investment and finance performance: An empirical study of China’s a-share heavy pollution industry. Int. J. Environ. Res. Public Health 2020, 17, 6082. [Google Scholar] [CrossRef]

- Liu, J.Y.; Zhang, Y.J. Has carbon emissions trading system promoted non-fossil energy development in China? Appl. Energy 2021, 302, 117613. [Google Scholar] [CrossRef]

- Zhou, F.; Wang, X. The carbon emissions trading scheme and green technology innovation in China: A new structural economics perspective. Econ. Anal. Policy 2022, 74, 365–381. [Google Scholar] [CrossRef]

- Jacobson, L.S.; LaLonde, R.J.; Sullivan, D.G. Earnings losses of displaced workers. Am. Econ. Rev. 1993, 83, 685–709. [Google Scholar]

- Wen, H.; Lee, C.-C.; Zhou, F. Green credit policy, credit allocation efficiency and upgrade of energy-intensive enterprises. Energy Econ. 2021, 94, 105099. [Google Scholar] [CrossRef]

- Chen, L.; Nan, G.; Li, M.; Feng, B.; Liu, Q. Manufacturer’s online selling strategies under spillovers from online to offline sales. J. Oper. Res. Soc. 2023, 74, 157–180. [Google Scholar] [CrossRef]

- Lu, F.; Yao, Y. Rule of Law, Financial Development and Economic Growth under Financial repression. Soc. Sci. China 2004, 1, 42–55. (In Chinese) [Google Scholar]

- Hamilton, B.H.; Nickerson, J.A. Correcting for endogeneity in strategic management research. Strateg. Organ. 2003, 1, 51–78. [Google Scholar] [CrossRef]

- Gu, Y.; Ho, K.C.; Yan, C.; Gozgor, G. Public environmental concern, CEO turnover, and green investment: Evidence from a quasi-natural experiment in China. Energy Econ. 2021, 100, 105379. [Google Scholar] [CrossRef]

- Chen, J.; Geng, Y.; Liu, R. Carbon emissions trading and corporate green investment: The perspective of external pressure and internal incentive. Bus. Strategy Environ. 2022; early view. [Google Scholar] [CrossRef]

- Tian, Y.; Wan, Q.; Tan, Y. Exploration on Inter-Relation of Environmental Regulation, Economic Structure, and Economic Growth: Provincial Evidence from China. Sustainability 2022, 15, 248. [Google Scholar] [CrossRef]

- Martin, R.; Muûls, M.; De Preux, L.B.; Wagner, U.J. Industry compensation under relocation risk: A firm-level analysis of the EU emissions trading scheme. Am. Econ. Rev. 2014, 104, 2482–2508. [Google Scholar] [CrossRef]

- Ren, X.; Wang, R.; Duan, K.; Chen, J. Dynamics of the sheltering role of Bitcoin against crude oil market crash with varying severity of the COVID-19: A comparison with gold. Res. Int. Bus. Financ. 2022, 62, 101672. [Google Scholar] [CrossRef]

- Wang, X.L.; Fan, G.; Hu, L.P. Report on China’s Marketization Index by Province; Social Sciences Academic Press: Beijing, China, 2018. [Google Scholar]

- Zhang, D.; Kong, Q.; Wang, Y.; Vigne, S.A. Exquisite workmanship through net-zero emissions? The effects of carbon emission trading policy on firms’ export product quality. Energy Econ. 2023, 123, 106701. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| (1) | (2) | (3) | (4) | (5) | |

|---|---|---|---|---|---|

| Variables | N | Mean | Sd | Min | Max |

| EPI | 14,895 | 0.285 | 0.443 | 0.000 | 3.537 |

| CETS | 14,895 | 0.287 | 0.317 | 0.000 | 1.000 |

| Age | 14,895 | 17.17 | 5.810 | 1.000 | 51.00 |

| Size | 14,895 | 23.413 | 1.564 | 18.733 | 28.232 |

| Roa | 14,895 | 0.034 | 0.091 | −0.325 | 0.319 |

| Tobq | 14,895 | 2.922 | 1.317 | 0.684 | 18.972 |

| Lev | 14,895 | 0.447 | 0.205 | 0.369 | 0.949 |

| (1) | (2) | (3) | (4) | (5) | |

|---|---|---|---|---|---|

| Variables | DID | DID | DID | DID | DID |

| CETS | 0.421 ** | 0.308 * | 0.386 ** | 0.293 * | 0.314 ** |

| (2.51) | (1.88) | (2.38) | (1.84) | (1.97) | |

| Size | 0.039 * | 0.047 ** | 0.058 *** | 0.041 ** | 0.035 *** |

| (1.78) | (2.14) | (3.08) | (2.05) | (3.28) | |

| Age | −0.034 ** | −0.019 * | −0.035 | −0.022 | −0.047 |

| (−2.24) | (−1.69) | (−1.35) | (−1.24) | (−1.56) | |

| Roa | 0.077 *** | 0.092 *** | 0.082 *** | 0.087 *** | 0.072 ** |

| (2.98) | (3.85) | (3.88) | (3.54) | (2.39) | |

| Tobq | 0.005 *** | 0.006 *** | 0.005 *** | 0.005 *** | 0.007 ** |

| (4.21) | (3.84) | (3.25) | (4.18) | (2.28) | |

| Lev | −0.033 ** | −0.028 ** | −0.025 | −0.024 | −0.031 * |

| (−2.13) | (−2.08) | (−1.54) | (−1.07) | (−1.84) | |

| Constant | −0.195 | −0.834 * | 0.033 | −0.399 | 0.145 * |

| (−0.62) | (−1.67) | (0.16) | (−1.06) | (1.86) | |

| Firm FE | N | N | Y | Y | Y |

| Industry FE | N | N | N | N | Y |

| City FE | N | Y | N | Y | Y |

| Year FE | N | Y | Y | Y | Y |

| Observations | 14,895 | 14,895 | 14,895 | 14,895 | 14,895 |

| R-squared | 0.430 | 0.582 | 0.603 | 0.717 | 0.726 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Variables | PSM-DID | PSM-DID | PSM-DID | PSM-DID |

| CETS | 0.501 * | 0.442 ** | 0.370 ** | 0.393 * |

| (1.71) | (2.08) | (2.48) | (1.69) | |

| Constant | 0.645 | 0.834 * | 0.033 ** | 0.399 * |

| (0.64) | (1.67) | (2.16) | (1.86) | |

| Control | Y | Y | Y | Y |

| Firm FE | N | N | Y | Y |

| City FE | N | N | N | Y |

| Year FE | N | Y | Y | Y |

| Observations | 13,818 | 13,818 | 13,818 | 13,818 |

| R-squared | 0.332 | 0.381 | 0.431 | 0.473 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Variables | Discharge Cost | Discharge Cost | Law Enforcement Rigidity | Law Enforcement Rigidity |

| Cost × DID | 0.065 * | 0.060 ** | ||

| (1.692) | (1.970) | |||

| Law × DID | 0.025 ** | 0.022 ** | ||

| (2.265) | (1.972) | |||

| Constant | −1.808 *** | −1.893 *** | 7.284 *** | 5.499 *** |

| (−72.054) | (−12.322) | (36.504) | (9.904) | |

| Control | N | Y | N | Y |

| Firm FE | N | Y | N | Y |

| Year FE | Y | Y | Y | Y |

| City FE | Y | Y | Y | Y |

| Observations | 14,895 | 14,895 | 14,895 | 14,895 |

| R-squared | 0.373 | 0.553 | 0.561 | 0.607 |

| (1) | (2) | (3) | |

|---|---|---|---|

| Enterprise Scale | Enterprise Property | Enterprises Pollution Level | |

| CETS | 0.244 *** | 0.117 *** | 0.307 ** |

| (2.935) | (4.114) | (2.437) | |

| CETS × Scale | 0.042 *** | ||

| (3.760) | |||

| CETS × Property | 0.127 *** | ||

| (2.917) | |||

| CETS × Heavy Pollution | 0.101 *** | ||

| (3.018) | |||

| Constant | 1.021 *** | 2.193 *** | 1.588 *** |

| (2.955) | (3.651) | (2.639) | |

| Control | Yes | Yes | Yes |

| Firms FE | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes |

| City FE | Yes | Yes | Yes |

| N | 14,895 | 14,895 | 14,895 |

| R2 | 0.542 | 0.681 | 0.484 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lv, S.; Lv, Y.; Gao, D.; Liu, L. The Path to Green Development: The Impact of a Carbon Emissions Trading Scheme on Enterprises’ Environmental Protection Investments. Sustainability 2023, 15, 12551. https://doi.org/10.3390/su151612551

Lv S, Lv Y, Gao D, Liu L. The Path to Green Development: The Impact of a Carbon Emissions Trading Scheme on Enterprises’ Environmental Protection Investments. Sustainability. 2023; 15(16):12551. https://doi.org/10.3390/su151612551

Chicago/Turabian StyleLv, Shigong, Yanying Lv, Da Gao, and Lulu Liu. 2023. "The Path to Green Development: The Impact of a Carbon Emissions Trading Scheme on Enterprises’ Environmental Protection Investments" Sustainability 15, no. 16: 12551. https://doi.org/10.3390/su151612551

APA StyleLv, S., Lv, Y., Gao, D., & Liu, L. (2023). The Path to Green Development: The Impact of a Carbon Emissions Trading Scheme on Enterprises’ Environmental Protection Investments. Sustainability, 15(16), 12551. https://doi.org/10.3390/su151612551