Counterparty Risk Contagion Model of Carbon Quota Based on Asset Price Reduction

Abstract

:1. Introduction

2. Interfirm Debt Network Model

2.1. Corporate Balance Sheets

2.2. Interfirm Debt Network

3. Construction of a Counterparty Risk Contagion Model for Carbon Quota Trading among Firms

3.1. Fire Sale of Firm Assets

3.2. Construction of the Relationship of Carbon Quota Debt among Firms

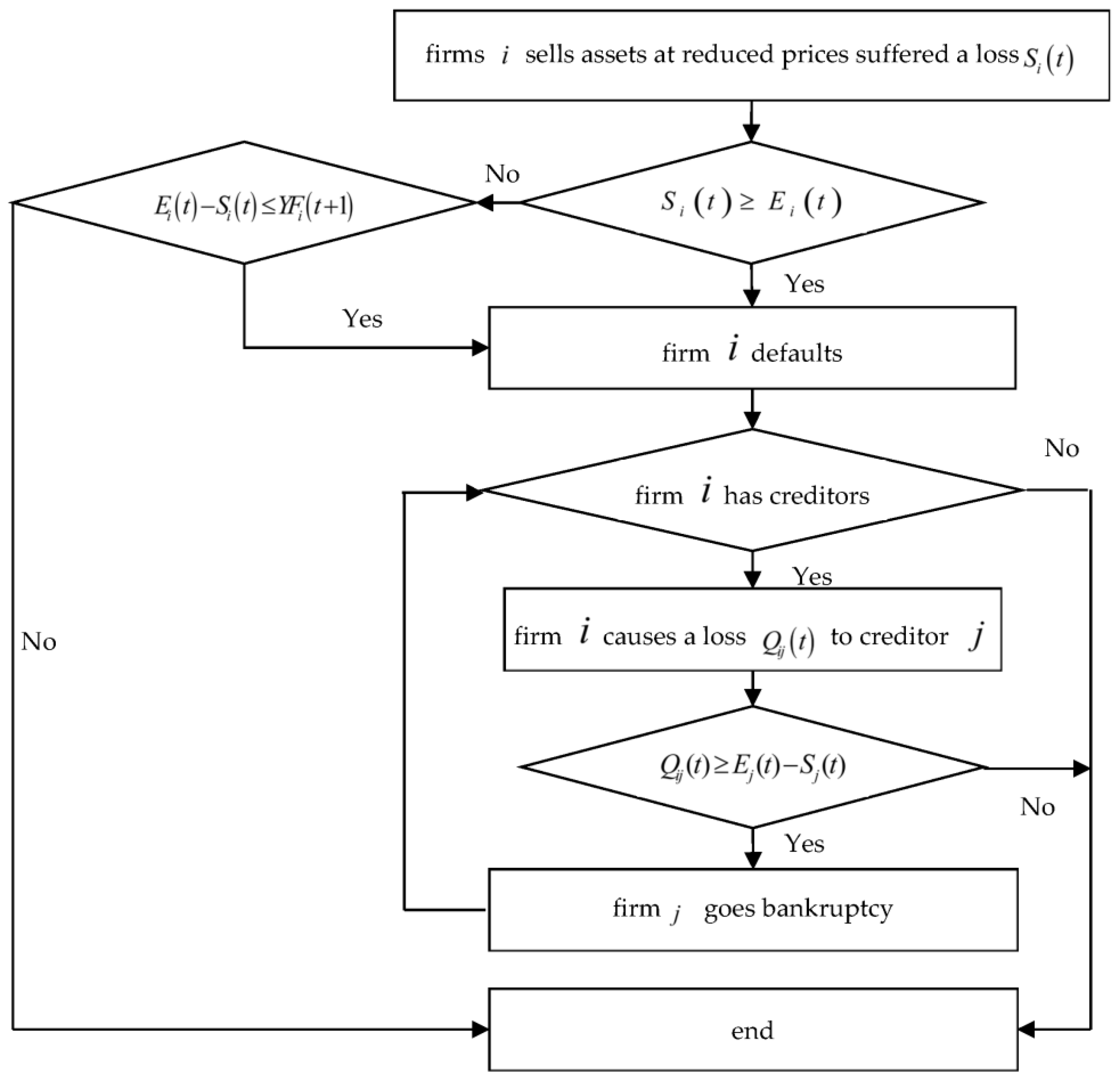

3.3. Risk Contagion Process of Carbon Quota Counterparties

4. Analysis of the Mechanism of Carbon Quota Counterparty Risks

4.1. Analysis of the Mechanism of Risk Formation of Carbon Quota Counterparty Risks

4.2. Analysis of the Mechanism of Risk Contagion of Carbon Quota Counterparties

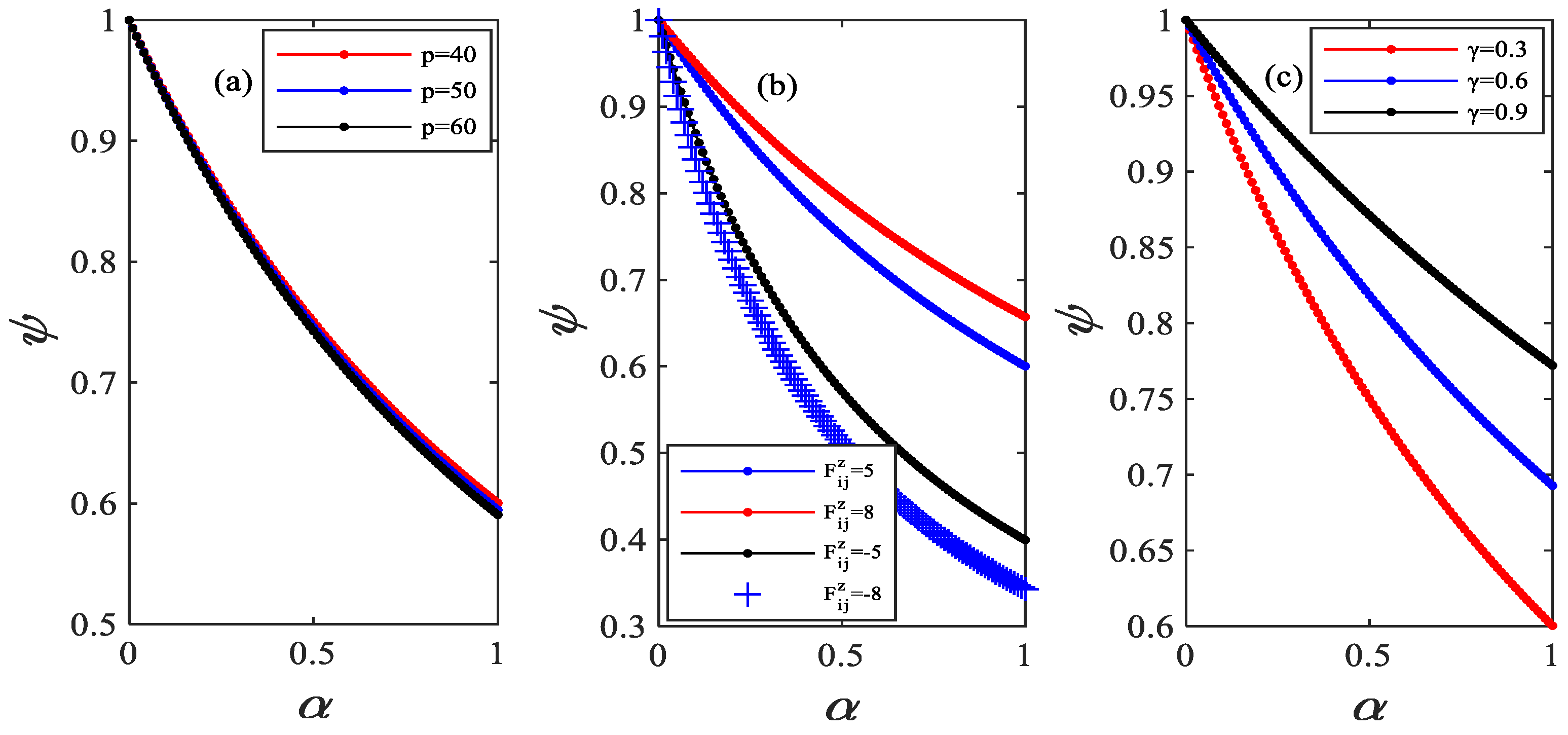

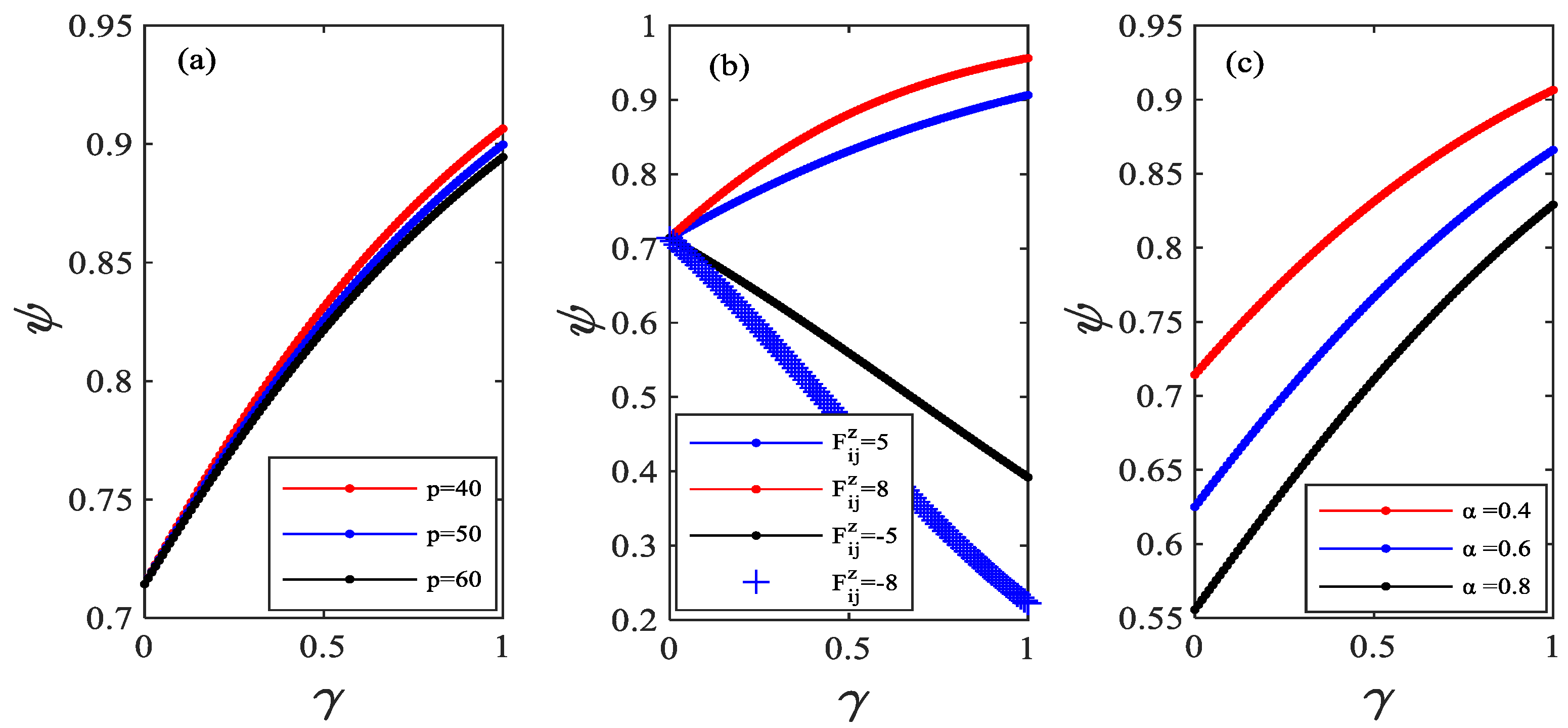

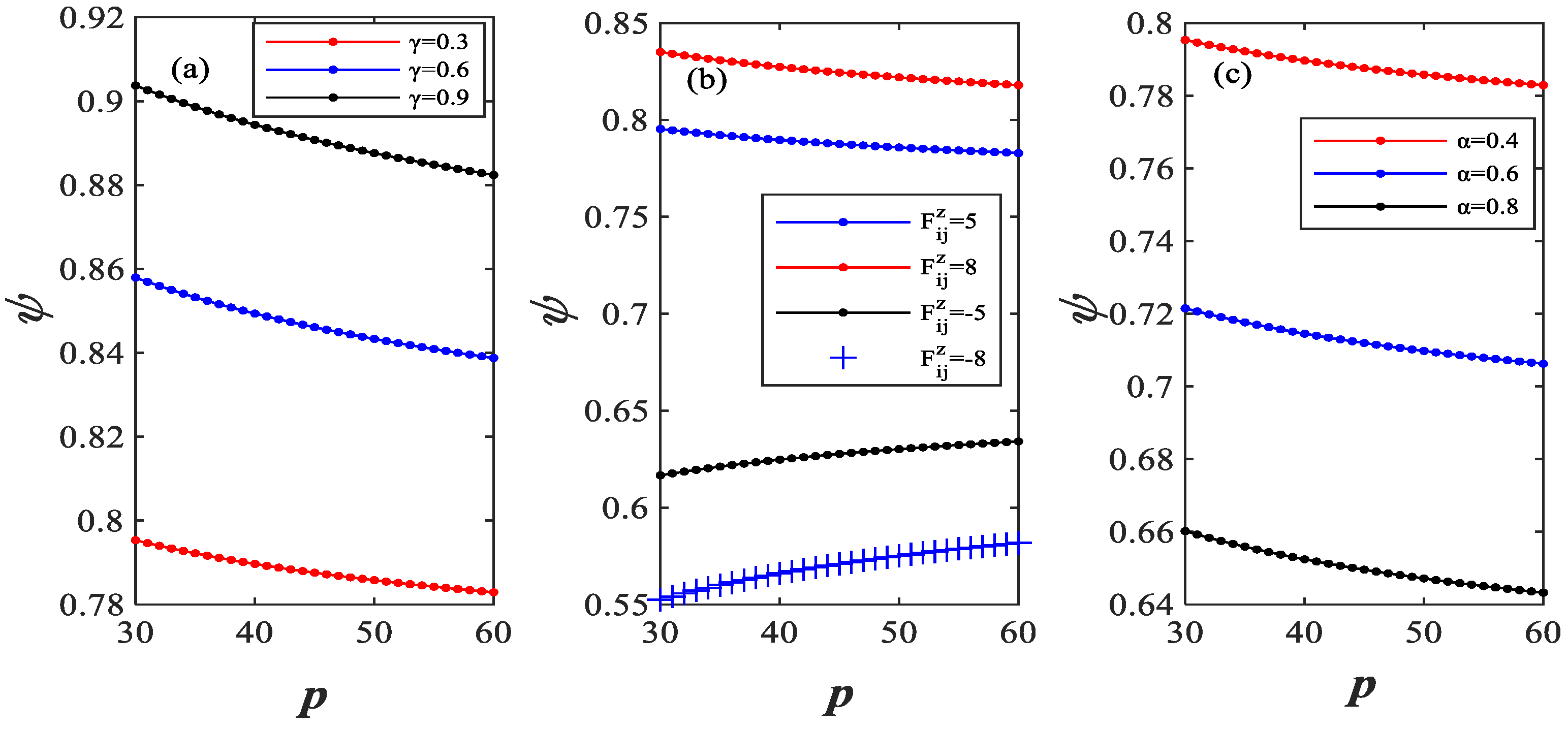

5. Simulation Analysis

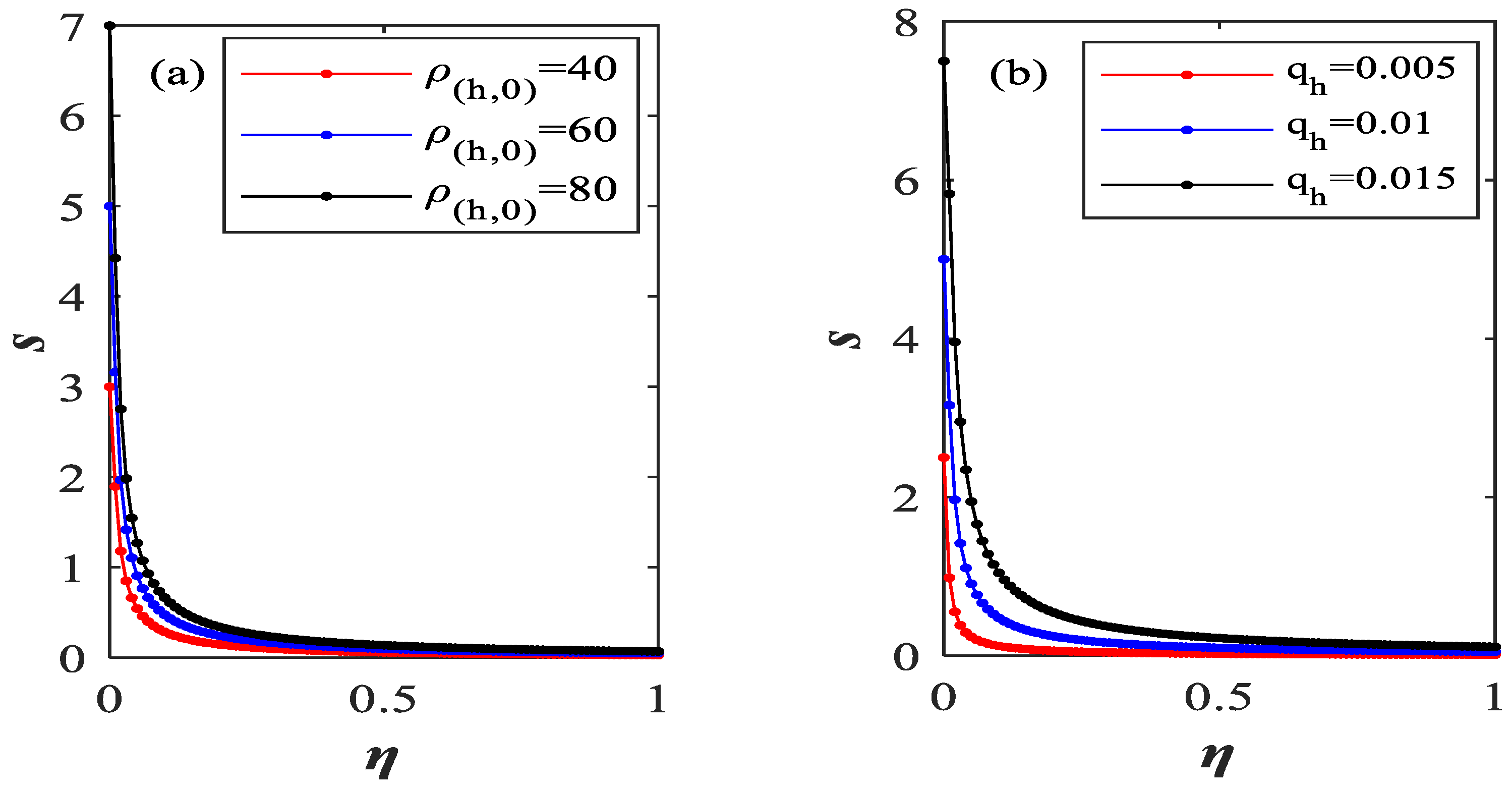

5.1. Formation Effect of Carbon Quota Counterparty Risk

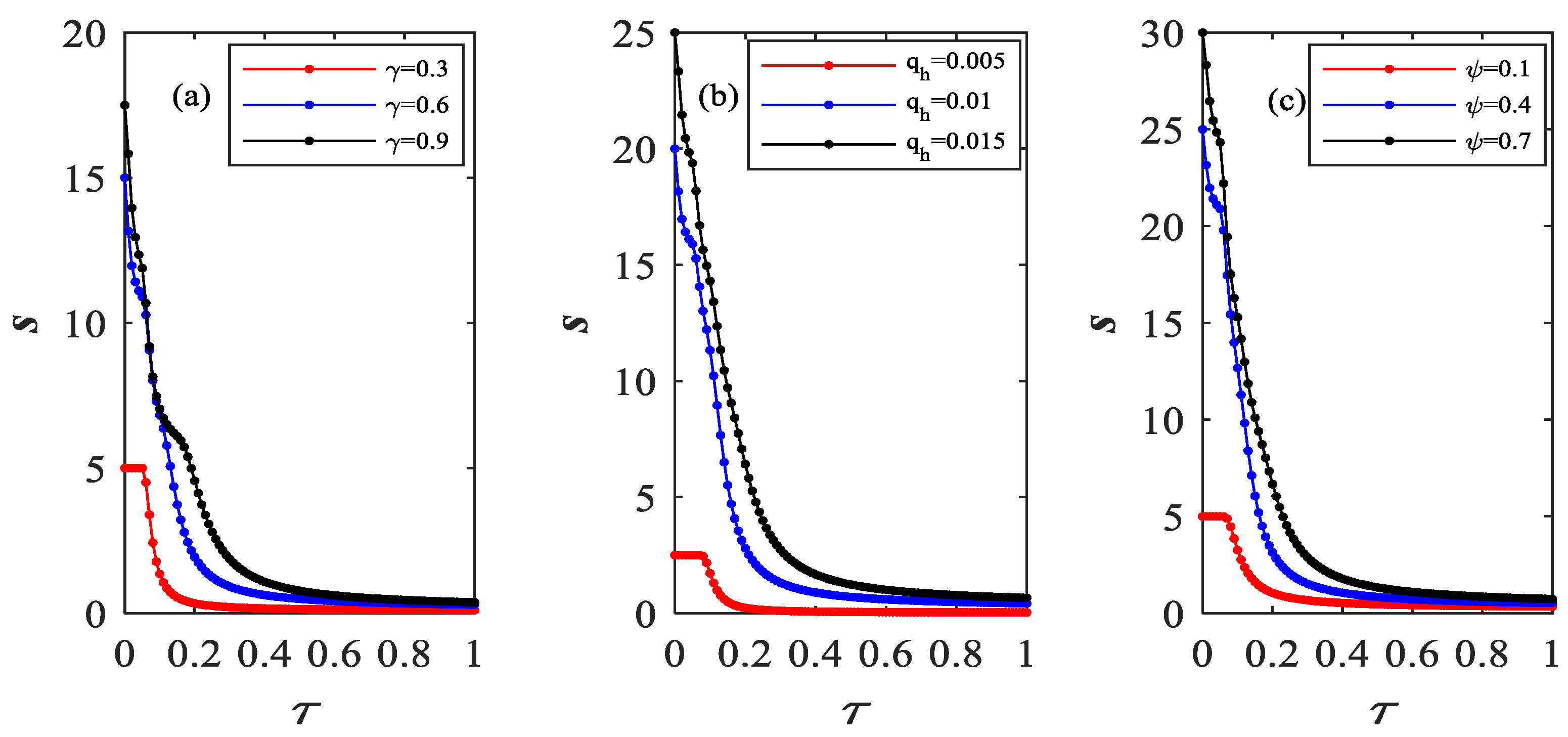

5.2. Risk Contagion Effect of Carbon Quota Counterparties

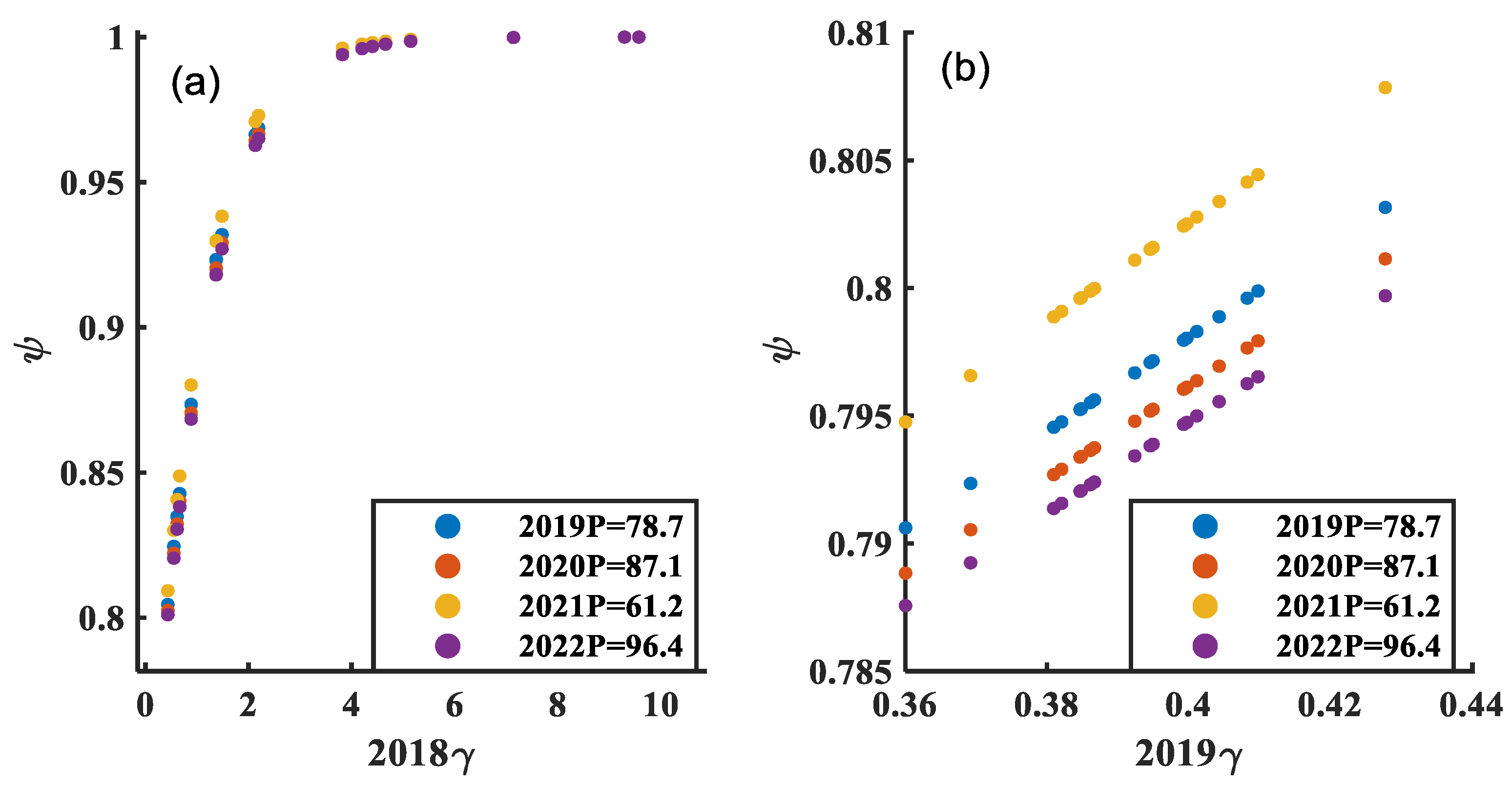

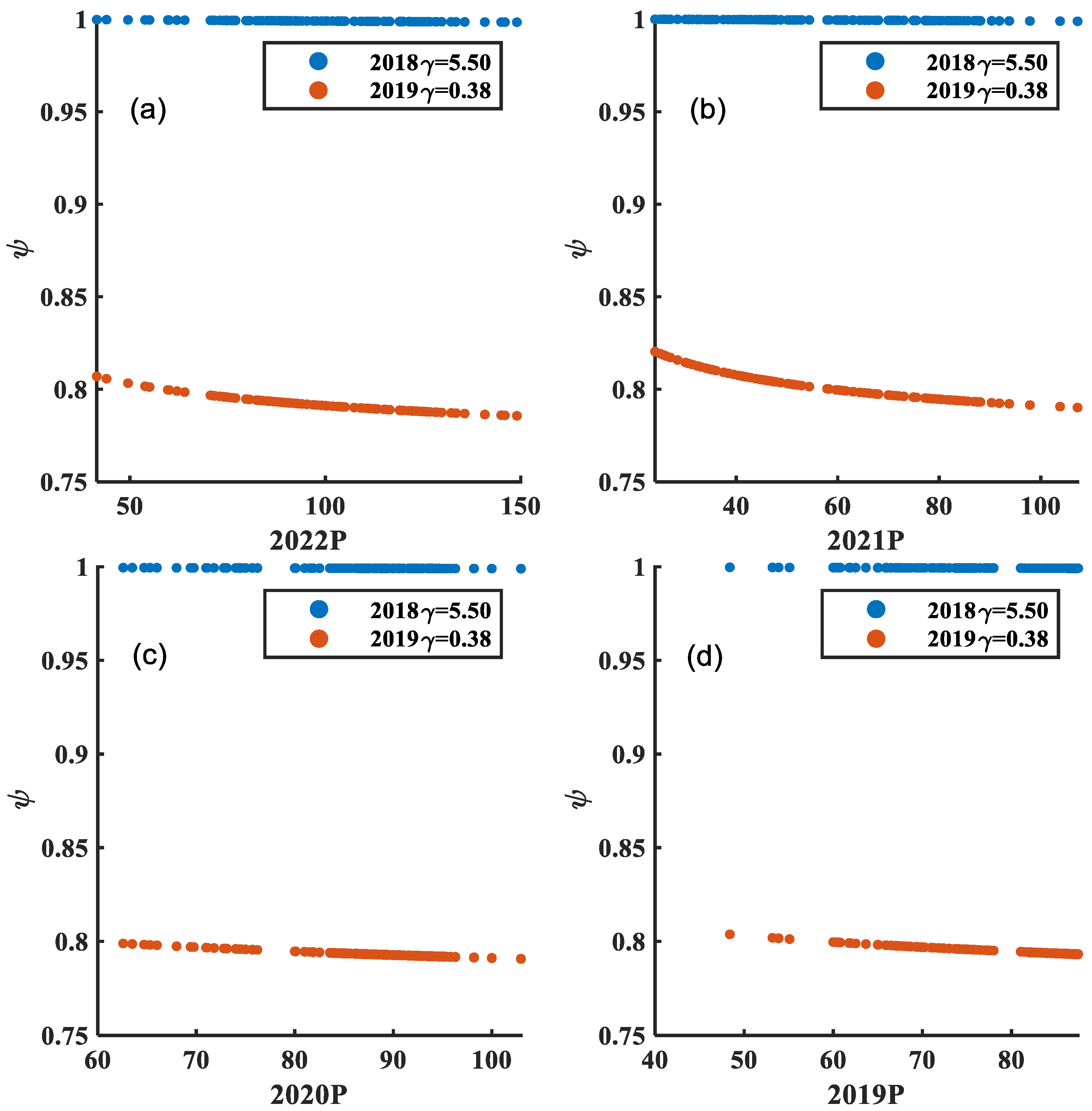

5.3. Carbon Quota Counterparty Risk Contagion Effect Based on Carbon Trading Data and Corporate Carbon Emission Intensity

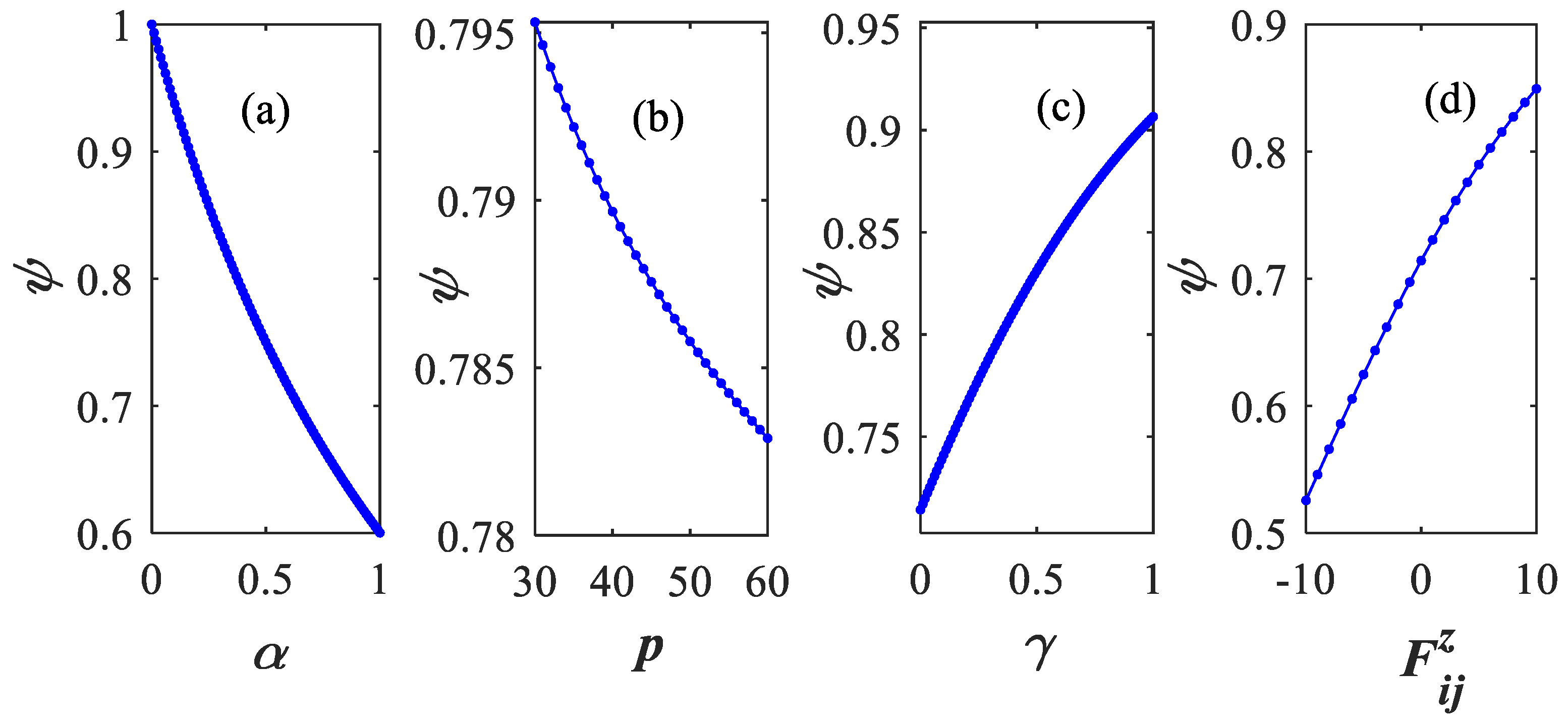

5.4. Robustness Analysis

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Wu, M.; Li, K.; Xiao, Y.; Yuen, K. Carbon Emission Trading Scheme in the shipping sector: Drivers, Challenges, and Impacts. Mar. Policy 2022, 138, 140989. [Google Scholar]

- Arora, N.; Gandhi, P.; Longstaff, F.A. Counterparty credit risk and the credit default swap market. J. Financ. Econ. 2012, 103, 280–293. [Google Scholar]

- Li, G.; Zhang, C. Counterparty credit risk and derivatives pricing. J. Financ. Econ. 2019, 134, 647–668. [Google Scholar]

- Wang, L.; Li, S.; Chen, T. Investor behavior, information disclosure strategy and counterparty credit risk contagion. Chaos Solitons Fractals 2019, 119, 37–49. [Google Scholar]

- Chen, T.; Yang, Q.; Wang, Y.; Wang, S. Double-layer network model of bank-enterprise counterparty credit risk contagion. Complexity 2020, 2020, 1–25. [Google Scholar]

- Liu, Y.; Cui, Y.; Yu, B. Threshold of Credit Risk Contagion within Firm Groups. J. Coast. Res. 2020, 104, 198–202. [Google Scholar]

- Cao, Y.; Wu, D.; Li, L. Debt risk analysis of non-financial corporates using two-tier networks. Ind. Manag. Data Syst. 2020, 120, 1287–1307. [Google Scholar]

- Sui, X.; Li, L.; Chen, X. Risk contagion caused by interactions between credit and guarantee networks. Phys. A Stat. Mech. Appl. 2020, 539, 122867. [Google Scholar]

- Chen, T.; Wang, S. Incomplete Information Model of Credit Default of Micro and Small Firms. Int. J. Financ. Econ. 2023, 28, 2956–2974. [Google Scholar] [CrossRef]

- Pan, H.; Hong, F. The Stability of Banking System with Shadow Banking on Different Interbank Network Structures. Discrete Dyn. Nat. Soc. 2021, 2021, 665037. [Google Scholar]

- Qian, Q.; Feng, H.; Gu, J. The influence of Risk Attitude on credit risk contagion-Perspective of Information Dissemination. Phys. A Stat. Mech. Appl. 2021, 582, 126226. [Google Scholar]

- Mu, P.; Chen, T.; Pan, K.; Liu, M. A Network Evolution Model of Credit Risk Contagion between Banks and Firms Based on Agent-Based Model. J. Math. 2021, 2021, 6593218. [Google Scholar]

- Zhang, Y. How Economic Performance of OECD economies influences through Green Finance and Renewable Energy Investment Resources? J. Resour. Policy 2022, 79, 102925. [Google Scholar]

- Ling, X.; Yan, L.; Dai, D. Green Credit Policy and Investment Decisions: Evidence from China. Sustainability 2022, 14, 7088. [Google Scholar]

- Zhou, X.; Caldecott, B.; Hoepner, A.; Wang, Y. Bank green lending and credit risk: An Empirical analysis of China’s Green Credit Policy. Bus. Strategy Environ. 2022, 31, 1623–1640. [Google Scholar]

- Song, M.; Zheng, H.; Shen, Z. Whether the carbon emissions trading system improves energy efficiency—Empirical testing based on China’s provincial panel data. Energy 2023, 275, 127456. [Google Scholar]

- Wang, Y.; Liu, J.; Zhao, Z.; Ren, J.; Chen, X. Research on carbon emission reduction effect of China’s regional digital trade under the “double carbon” target—Combination of the regulatory role of industrial agglomeration and carbon emissions trading mechanism. J. Clean. Prod. 2023, 405, 137049. [Google Scholar]

- Zhou, Y. Influencing Factors and Forecast of Carbon Emission Trading Price in Beijing. J. Glob. Econ. Bus. Financ. 2023, 5, 137668. [Google Scholar]

- Dong, Q.; Huo, D.; Wang, K. Risk measurement and application of the international carbon market in the era of global conflict: A data-driven study using FCM. J. Environ. Manag. 2023, 342, 118251. [Google Scholar]

- Nier, E.; Yang, J.; Yorulmazer, T. Network models and financial stability. J. Econ. Dyn. Control 2007, 31, 2033–2060. [Google Scholar]

- Ding, D.; Han, L.; Yin, L. Systemic risk and dynamics of contagion: A duplex inter-bank network. Quant. Financ. 2017, 17, 1435–1445. [Google Scholar]

- Chen, T.; He, J. A network model of credit risk contagion. Discret. Dyn. Nat. Soc. 2012, 2012, 327–337. [Google Scholar]

- Chen, T.; Wang, J.; Liu, H.; He, Y. Contagion model on counterparty credit risk in the CRT market by considering the heterogeneity of counterparties and preferential—Random mixing attachment. Phys. A Stat. Mech. Appl. 2019, 520, 458–480. [Google Scholar]

- Mizuno, T.; Ohnishi, T.; Watanabe, T. Structure of global buyer-supplier networks and its implications for conflict minerals regulations. EPJ Data Sci. 2016, 5, 1–15. [Google Scholar]

- Ohsung, K.; Sung, Y.; Hun, H.S.; Hon, C.Y.; Hee, L.D. Network Topology and Systemically Important Firms in the Interfirm Credit Network. Comput. Econ. 2018, 51, 847–864. [Google Scholar]

- Pi, X.; Tang, L.; Chen, X. A directed weighted scale-free network model with an adaptive evolution mechanism. Phys. A Stat. Mech. Appl. 2021, 572, 125897. [Google Scholar]

- Peng, D.; Peng, B.; Wang, T. Reconfiguring IVHF-TOPSIS decision making method with parameterized reference solutions and a novel distance for Corporate Carbon Performance Evaluation. J. Ambient Intell. Humaniz. Comput. 2020, 11, 3811–3832. [Google Scholar]

- Chen, T.; Wang, Y.; Zeng, Q.; Luo, J. Network model of credit risk contagion in the interbank market by considering bank runs and the fire sale of External assets. Phys. A Stat. Mech. Appl. 2020, 542, 123006. [Google Scholar]

- Yang, C.; Li, J. Investor sentiment, information and asset pricing model. Econ. Model. 2013, 35, 436–442. [Google Scholar]

- Su, C.; Cai, X.; Tao, R. Can Stock Investor Sentiment Be Contagious in China? J. Sustain. 2020, 12, 1571. [Google Scholar]

- Song, Z.; Yu, C. Investor sentiment indices based on k-step PLS algorithm: A Group of Powerful predictors of Stock Market Returns. Int. Rev. Financ. Anal. 2022, 83, 102321. [Google Scholar]

- Tang, H.; Liu, J.; Wu, J. The impact of command-and-control environmental regulation on firm total factor productivity: A quasi-natural experiment-based on China’s “the Two Control zones” policy. J. Clean. Prod. 2020, 254, 120011. [Google Scholar]

- Cai, W.; Ye, P. How does environmental regulation influence firms’ total factor productivity? A quasi-natural experiment based on China’s new environmental protection law. J. Clean. Prod. 2020, 276, 124105. [Google Scholar]

- Luo, W.; Guo, X.; Zhong, S.; Wang, J. Environmental information disclosure quality, media attention and debt financing costs: Evidence from Chinese heavy polluting listed companies. J. Clean. Prod. 2019, 231, 268–277. [Google Scholar]

- Siddique, M.; Akhtaruzzaman, M.; Afzalur, R.; Helmi, H. Carbon disclosure, carbon performance and financial performance. Int. Rev. Financ. Anal. 2021, 75, 101734. [Google Scholar]

- Jia, Z.; Lin, B. Rethinking the choice of carbon tax and carbon trading in China. Technol. Forecast. Soc. Chang. 2020, 159, 120187. [Google Scholar]

- Hu, X.; Yang, Z.; Sun, J.; Zhang, Y. Carbon tax or cap-and-trade: Which is more viable for Chinese remanufacturing industry? J. Clean. Prod. 2020, 243, 118606. [Google Scholar]

- Jung, J.; Herbohn, K.; Clarkson, P. Carbon Risk, Carbon Risk Awareness and the Cost of Debt Financing. J. Bus. Ethics 2018, 150, 1151–1171. [Google Scholar]

- Chen, Y.; Xu, Z.; Zhang, Z.; Ye, W.; Yang, Y.; Gong, Z. Does the carbon emission trading scheme boost corporate environmental and financial performance in China? J. Clean. Prod. 2022, 368, 133151. [Google Scholar]

- Liu, A.; Paddrik, M.; Steve, Y.; Zhang, X. Interbank contagion: An agent-based model approach to endogenously formed networks. J. Bank. Financ. 2020, 112, 105191. [Google Scholar]

- Danai, L.; Nopadon, K.; Karawan, W.; Chakrin, P. The Accuracy of Risk Measurement Models on Bitcoin Market during COVID-19 Pandemic. Risks 2021, 9, 222. [Google Scholar]

- Cifuentes, R.; Ferrucci, G.; Shin, H. Liquidity and Contagion. J. Eur. Econ. Assoc. 2005, 3, 556–566. [Google Scholar]

- He, J.; Sui, X.; Li, S. An endogenous model of the credit network. Phys. A Stat. Mech. Appl. 2016, 441, 1–14. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Assets | Liabilities |

|---|---|

| Carbon quota accounts receivables Trading financial assets Cash | Carbon quota accounts payables Trading financial liabilities Owner’s equity |

| Parameter | Description | Benchmark Value | Range of Variation |

|---|---|---|---|

| Total number of firms | 300 | Positive integer | |

| Business degree | 5 | ||

| Memory decay function | 0.1 | ||

| Weight of the relationship scores in the overall rating system | 0.5 | ||

| Market prices of class assets at moment | 50 | ||

| Initial market price the class assets | 50 | ||

| Proportion of rational investors | 0.5 | ||

| Types of marketable financial asset | 10 | Positive integer | |

| Probability of credit risk contagion of carbon quota among firms | 0.4 | ||

| Corporate carbon performance | 0.3 | ||

| Price sensitivity of the firm to the sale of financial assets | 0.5 | ||

| Cumulative proportion of class assets sold | 0.01 | ||

| Market to class asset market capacity | 0.02 | ||

| Trading price of carbon quota | 40 | ||

| Corporate carbon risk awareness | 0.4 | ||

| Total score of interfirm assessment | 5 |

| Expectation | Variance | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | 1.0 | |||

| 40.0 | 0.098 | 0.049 | 0.033 | 0.025 | 0.020 | 0.017 | 0.014 | 0.012 | 0.011 | 0.010 | 0.029 | 0.001 |

| 43.0 | 0.105 | 0.053 | 0.036 | 0.027 | 0.021 | 0.018 | 0.015 | 0.013 | 0.012 | 0.011 | 0.031 | 0.001 |

| 46.0 | 0.112 | 0.057 | 0.038 | 0.029 | 0.023 | 0.019 | 0.016 | 0.014 | 0.013 | 0.011 | 0.033 | 0.001 |

| 49.0 | 0.119 | 0.060 | 0.040 | 0.030 | 0.024 | 0.020 | 0.017 | 0.015 | 0.014 | 0.012 | 0.035 | 0.001 |

| 52.0 | 0.127 | 0.064 | 0.043 | 0.032 | 0.026 | 0.022 | 0.019 | 0.016 | 0.014 | 0.013 | 0.038 | 0.001 |

| 55.0 | 0.134 | 0.068 | 0.045 | 0.034 | 0.027 | 0.023 | 0.020 | 0.017 | 0.015 | 0.014 | 0.040 | 0.001 |

| 58.0 | 0.141 | 0.072 | 0.048 | 0.036 | 0.029 | 0.024 | 0.021 | 0.018 | 0.016 | 0.014 | 0.042 | 0.002 |

| 61.0 | 0.149 | 0.075 | 0.050 | 0.038 | 0.030 | 0.025 | 0.022 | 0.019 | 0.017 | 0.015 | 0.044 | 0.002 |

| 64.0 | 0.156 | 0.079 | 0.053 | 0.040 | 0.032 | 0.027 | 0.023 | 0.020 | 0.018 | 0.016 | 0.046 | 0.002 |

| 67.0 | 0.163 | 0.083 | 0.055 | 0.042 | 0.033 | 0.028 | 0.024 | 0.021 | 0.019 | 0.017 | 0.048 | 0.002 |

| 70.0 | 0.171 | 0.086 | 0.058 | 0.043 | 0.035 | 0.029 | 0.025 | 0.022 | 0.019 | 0.017 | 0.051 | 0.002 |

| 73.0 | 0.178 | 0.090 | 0.060 | 0.045 | 0.036 | 0.030 | 0.026 | 0.023 | 0.020 | 0.018 | 0.053 | 0.002 |

| 76.0 | 0.185 | 0.094 | 0.063 | 0.047 | 0.038 | 0.032 | 0.027 | 0.024 | 0.021 | 0.019 | 0.055 | 0.003 |

| 79.0 | 0.193 | 0.098 | 0.065 | 0.049 | 0.039 | 0.033 | 0.028 | 0.025 | 0.022 | 0.020 | 0.057 | 0.003 |

| 82.0 | 0.200 | 0.101 | 0.068 | 0.051 | 0.041 | 0.034 | 0.029 | 0.026 | 0.023 | 0.020 | 0.059 | 0.003 |

| 85.0 | 0.207 | 0.105 | 0.070 | 0.053 | 0.042 | 0.035 | 0.030 | 0.026 | 0.024 | 0.021 | 0.061 | 0.003 |

| 88.0 | 0.215 | 0.109 | 0.073 | 0.055 | 0.044 | 0.037 | 0.031 | 0.027 | 0.024 | 0.022 | 0.064 | 0.004 |

| 91.0 | 0.222 | 0.112 | 0.075 | 0.057 | 0.045 | 0.038 | 0.032 | 0.028 | 0.025 | 0.023 | 0.066 | 0.004 |

| 94.0 | 0.229 | 0.116 | 0.078 | 0.058 | 0.047 | 0.039 | 0.033 | 0.029 | 0.026 | 0.023 | 0.068 | 0.004 |

| 97.0 | 0.237 | 0.120 | 0.080 | 0.060 | 0.048 | 0.040 | 0.035 | 0.030 | 0.027 | 0.024 | 0.070 | 0.004 |

| 100.0 | 0.244 | 0.123 | 0.083 | 0.062 | 0.050 | 0.041 | 0.036 | 0.031 | 0.028 | 0.025 | 0.072 | 0.005 |

| Expectation | 0.171 | 0.086 | 0.058 | 0.043 | 0.035 | 0.029 | 0.025 | 0.022 | 0.019 | 0.017 | ||

| Variance | 0.002 | 0.001 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | ||

| 40.0 | 0.381 | 0.195 | 0.131 | 0.099 | 0.079 | 0.066 | 0.057 | 0.050 | 0.044 | 0.040 | 0.114 | 0.011 |

| 43.0 | 0.409 | 0.210 | 0.141 | 0.106 | 0.085 | 0.071 | 0.061 | 0.053 | 0.048 | 0.043 | 0.123 | 0.013 |

| 46.0 | 0.438 | 0.224 | 0.151 | 0.114 | 0.091 | 0.076 | 0.065 | 0.057 | 0.051 | 0.046 | 0.131 | 0.015 |

| 49.0 | 0.466 | 0.239 | 0.161 | 0.121 | 0.097 | 0.081 | 0.070 | 0.061 | 0.054 | 0.049 | 0.140 | 0.017 |

| 52.0 | 0.495 | 0.254 | 0.170 | 0.128 | 0.103 | 0.086 | 0.074 | 0.065 | 0.057 | 0.052 | 0.148 | 0.019 |

| 55.0 | 0.523 | 0.268 | 0.180 | 0.136 | 0.109 | 0.091 | 0.078 | 0.068 | 0.061 | 0.055 | 0.157 | 0.021 |

| 58.0 | 0.552 | 0.283 | 0.190 | 0.143 | 0.115 | 0.096 | 0.082 | 0.072 | 0.064 | 0.058 | 0.165 | 0.023 |

| 61.0 | 0.580 | 0.298 | 0.200 | 0.151 | 0.121 | 0.101 | 0.087 | 0.076 | 0.067 | 0.061 | 0.174 | 0.026 |

| 64.0 | 0.609 | 0.312 | 0.210 | 0.158 | 0.127 | 0.106 | 0.091 | 0.080 | 0.071 | 0.064 | 0.183 | 0.028 |

| 67.0 | 0.638 | 0.327 | 0.220 | 0.165 | 0.133 | 0.111 | 0.095 | 0.083 | 0.074 | 0.067 | 0.191 | 0.031 |

| 70.0 | 0.666 | 0.341 | 0.229 | 0.173 | 0.139 | 0.116 | 0.099 | 0.087 | 0.077 | 0.070 | 0.200 | 0.034 |

| 73.0 | 0.695 | 0.356 | 0.239 | 0.180 | 0.145 | 0.121 | 0.104 | 0.091 | 0.081 | 0.073 | 0.208 | 0.037 |

| 76.0 | 0.723 | 0.371 | 0.249 | 0.188 | 0.150 | 0.126 | 0.108 | 0.094 | 0.084 | 0.076 | 0.217 | 0.040 |

| 79.0 | 0.752 | 0.385 | 0.259 | 0.195 | 0.156 | 0.131 | 0.112 | 0.098 | 0.087 | 0.079 | 0.225 | 0.043 |

| 82.0 | 0.780 | 0.400 | 0.269 | 0.202 | 0.162 | 0.136 | 0.116 | 0.102 | 0.091 | 0.082 | 0.234 | 0.046 |

| 85.0 | 0.809 | 0.415 | 0.279 | 0.210 | 0.168 | 0.140 | 0.121 | 0.106 | 0.094 | 0.085 | 0.243 | 0.050 |

| 88.0 | 0.837 | 0.429 | 0.288 | 0.217 | 0.174 | 0.145 | 0.125 | 0.109 | 0.097 | 0.088 | 0.251 | 0.054 |

| 91.0 | 0.866 | 0.444 | 0.298 | 0.225 | 0.180 | 0.150 | 0.129 | 0.113 | 0.101 | 0.091 | 0.260 | 0.057 |

| 94.0 | 0.895 | 0.458 | 0.308 | 0.232 | 0.186 | 0.155 | 0.133 | 0.117 | 0.104 | 0.094 | 0.268 | 0.061 |

| 97.0 | 0.923 | 0.473 | 0.318 | 0.239 | 0.192 | 0.160 | 0.138 | 0.120 | 0.107 | 0.097 | 0.277 | 0.065 |

| 100.0 | 0.952 | 0.488 | 0.328 | 0.247 | 0.198 | 0.165 | 0.142 | 0.124 | 0.110 | 0.100 | 0.285 | 0.069 |

| Expectation | 0.666 | 0.341 | 0.229 | 0.173 | 0.139 | 0.116 | 0.099 | 0.087 | 0.077 | 0.070 | ||

| Variance | 0.031 | 0.008 | 0.004 | 0.002 | 0.001 | 0.001 | 0.001 | 0.001 | 0.000 | 0.000 | ||

| 40.0 | 0.836 | 0.434 | 0.293 | 0.221 | 0.177 | 0.148 | 0.127 | 0.111 | 0.099 | 0.089 | 0.254 | 0.053 |

| 43.0 | 0.898 | 0.466 | 0.315 | 0.237 | 0.191 | 0.159 | 0.137 | 0.120 | 0.107 | 0.096 | 0.273 | 0.061 |

| 46.0 | 0.961 | 0.499 | 0.337 | 0.254 | 0.204 | 0.170 | 0.146 | 0.128 | 0.114 | 0.103 | 0.292 | 0.070 |

| 49.0 | 1.024 | 0.531 | 0.358 | 0.271 | 0.217 | 0.181 | 0.156 | 0.137 | 0.121 | 0.109 | 0.311 | 0.080 |

| 52.0 | 1.086 | 0.564 | 0.380 | 0.287 | 0.231 | 0.193 | 0.165 | 0.145 | 0.129 | 0.116 | 0.330 | 0.090 |

| 55.0 | 1.149 | 0.596 | 0.402 | 0.304 | 0.244 | 0.204 | 0.175 | 0.153 | 0.136 | 0.123 | 0.349 | 0.100 |

| 58.0 | 1.212 | 0.629 | 0.424 | 0.320 | 0.257 | 0.215 | 0.184 | 0.162 | 0.144 | 0.130 | 0.368 | 0.112 |

| 61.0 | 1.275 | 0.661 | 0.446 | 0.337 | 0.270 | 0.226 | 0.194 | 0.170 | 0.151 | 0.136 | 0.387 | 0.123 |

| 64.0 | 1.337 | 0.694 | 0.468 | 0.353 | 0.284 | 0.237 | 0.204 | 0.178 | 0.159 | 0.143 | 0.406 | 0.136 |

| 67.0 | 1.400 | 0.726 | 0.490 | 0.370 | 0.297 | 0.248 | 0.213 | 0.187 | 0.166 | 0.150 | 0.425 | 0.149 |

| 70.0 | 1.463 | 0.759 | 0.512 | 0.386 | 0.310 | 0.259 | 0.223 | 0.195 | 0.174 | 0.156 | 0.444 | 0.163 |

| 73.0 | 1.525 | 0.791 | 0.534 | 0.403 | 0.324 | 0.270 | 0.232 | 0.203 | 0.181 | 0.163 | 0.463 | 0.177 |

| 76.0 | 1.588 | 0.824 | 0.556 | 0.420 | 0.337 | 0.281 | 0.242 | 0.212 | 0.188 | 0.170 | 0.482 | 0.192 |

| 79.0 | 1.651 | 0.856 | 0.578 | 0.436 | 0.350 | 0.293 | 0.251 | 0.220 | 0.196 | 0.176 | 0.501 | 0.207 |

| 82.0 | 1.713 | 0.889 | 0.600 | 0.453 | 0.364 | 0.304 | 0.261 | 0.228 | 0.203 | 0.183 | 0.520 | 0.223 |

| 85.0 | 1.776 | 0.921 | 0.622 | 0.469 | 0.377 | 0.315 | 0.270 | 0.237 | 0.211 | 0.190 | 0.539 | 0.240 |

| 88.0 | 1.839 | 0.954 | 0.644 | 0.486 | 0.390 | 0.326 | 0.280 | 0.245 | 0.218 | 0.197 | 0.558 | 0.257 |

| 91.0 | 1.901 | 0.986 | 0.666 | 0.502 | 0.403 | 0.337 | 0.289 | 0.254 | 0.226 | 0.203 | 0.577 | 0.275 |

| 94.0 | 1.964 | 1.019 | 0.688 | 0.519 | 0.417 | 0.348 | 0.299 | 0.262 | 0.233 | 0.210 | 0.596 | 0.293 |

| 97.0 | 2.027 | 1.051 | 0.710 | 0.536 | 0.430 | 0.359 | 0.308 | 0.270 | 0.240 | 0.217 | 0.615 | 0.312 |

| 100.0 | 2.089 | 1.084 | 0.732 | 0.552 | 0.443 | 0.370 | 0.318 | 0.279 | 0.248 | 0.223 | 0.634 | 0.332 |

| Expectation | 1.463 | 0.759 | 0.512 | 0.386 | 0.310 | 0.259 | 0.223 | 0.195 | 0.174 | 0.156 | ||

| Variance | 0.151 | 0.041 | 0.019 | 0.011 | 0.007 | 0.005 | 0.004 | 0.003 | 0.002 | 0.002 | ||

| Expectation | Variance | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | 1.0 | |||

| qh = 0.005 ψ = 0.4 | ||||||||||||

| 0.1 | 0.053 | 0.032 | 0.027 | 0.025 | 0.024 | 0.023 | 0.022 | 0.022 | 0.022 | 0.021 | 0.027 | 0.000 |

| 0.2 | 0.140 | 0.053 | 0.038 | 0.032 | 0.029 | 0.027 | 0.026 | 0.025 | 0.024 | 0.024 | 0.042 | 0.001 |

| 0.3 | 0.363 | 0.086 | 0.053 | 0.041 | 0.035 | 0.032 | 0.030 | 0.028 | 0.027 | 0.026 | 0.072 | 0.011 |

| 0.4 | 0.868 | 0.140 | W | 0.053 | 0.043 | 0.038 | 0.034 | 0.032 | 0.030 | 0.029 | 0.134 | 0.068 |

| 0.5 | 1.716 | 0.227 | 0.101 | 0.067 | 0.053 | 0.045 | 0.040 | 0.036 | 0.034 | 0.032 | 0.235 | 0.274 |

| 0.6 | 2.393 | 0.363 | 0.140 | 0.086 | 0.064 | 0.053 | 0.046 | 0.041 | 0.038 | 0.035 | 0.326 | 0.537 |

| 0.7 | 2.500 | 0.570 | 0.194 | 0.110 | 0.078 | 0.062 | 0.053 | 0.046 | 0.042 | 0.039 | 0.369 | 0.586 |

| 0.8 | 2.500 | 0.868 | 0.266 | 0.140 | 0.095 | 0.073 | 0.061 | 0.053 | 0.047 | 0.043 | 0.415 | 0.600 |

| 0.9 | 2.500 | 1.263 | 0.363 | 0.179 | 0.115 | 0.086 | 0.070 | 0.059 | 0.053 | 0.048 | 0.473 | 0.644 |

| 1.0 | 2.500 | 1.716 | 0.492 | 0.227 | 0.140 | 0.101 | 0.080 | 0.067 | 0.059 | 0.053 | 0.543 | 0.731 |

| Expectation | 1.553 | 0.532 | 0.175 | 0.096 | 0.068 | 0.054 | 0.046 | 0.041 | 0.038 | 0.035 | ||

| Variance | 1.161 | 0.334 | 0.024 | 0.005 | 0.002 | 0.001 | 0.000 | 0.000 | 0.000 | 0.000 | ||

| qh = 0.01 ψ = 0.4 | ||||||||||||

| 0.1 | 0.208 | 0.127 | 0.108 | 0.099 | 0.095 | 0.091 | 0.089 | 0.088 | 0.087 | 0.086 | 0.108 | 0.001 |

| 0.2 | 0.545 | 0.208 | 0.150 | 0.127 | 0.115 | 0.108 | 0.103 | 0.099 | 0.097 | 0.095 | 0.165 | 0.019 |

| 0.3 | 1.347 | 0.338 | 0.208 | 0.163 | 0.140 | 0.127 | 0.118 | 0.112 | 0.108 | 0.104 | 0.277 | 0.146 |

| 0.4 | 2.870 | 0.545 | 0.288 | 0.208 | 0.171 | 0.150 | 0.136 | 0.127 | 0.120 | 0.115 | 0.473 | 0.726 |

| 0.5 | 4.508 | 0.867 | 0.397 | 0.265 | 0.208 | 0.177 | 0.157 | 0.144 | 0.134 | 0.127 | 0.698 | 1.842 |

| 0.6 | 4.991 | 1.347 | 0.545 | 0.338 | 0.253 | 0.208 | 0.181 | 0.163 | 0.150 | 0.140 | 0.832 | 2.270 |

| 0.7 | 5.000 | 2.020 | 0.744 | 0.430 | 0.307 | 0.245 | 0.208 | 0.184 | 0.167 | 0.155 | 0.946 | 2.350 |

| 0.8 | 5.000 | 2.870 | 1.007 | 0.545 | 0.372 | 0.288 | 0.239 | 0.208 | 0.186 | 0.171 | 1.089 | 2.564 |

| 0.9 | 5.000 | 3.775 | 1.347 | 0.689 | 0.451 | 0.338 | 0.275 | 0.235 | 0.208 | 0.189 | 1.251 | 2.936 |

| 1.0 | 5.000 | 4.508 | 1.773 | 0.867 | 0.545 | 0.397 | 0.316 | 0.265 | 0.232 | 0.208 | 1.411 | 3.337 |

| Expectation | 3.447 | 1.660 | 0.657 | 0.373 | 0.266 | 0.213 | 0.182 | 0.163 | 0.149 | 0.139 | ||

| Variance | 4.090 | 2.484 | 0.314 | 0.066 | 0.023 | 0.011 | 0.006 | 0.004 | 0.002 | 0.002 | ||

| qh = 0.015 ψ = 0.4 | ||||||||||||

| 0.1 | 0.463 | 0.284 | 0.241 | 0.222 | 0.212 | 0.205 | 0.200 | 0.197 | 0.194 | 0.192 | 0.241 | 0.007 |

| 0.2 | 1.193 | 0.463 | 0.335 | 0.284 | 0.258 | 0.241 | 0.230 | 0.222 | 0.216 | 0.212 | 0.365 | 0.090 |

| 0.3 | 2.816 | 0.748 | 0.463 | 0.363 | 0.314 | 0.284 | 0.265 | 0.251 | 0.241 | 0.234 | 0.598 | 0.632 |

| 0.4 | 5.414 | 1.193 | 0.638 | 0.463 | 0.381 | 0.335 | 0.305 | 0.284 | 0.269 | 0.258 | 0.954 | 2.536 |

| 0.5 | 7.269 | 1.863 | 0.875 | 0.589 | 0.463 | 0.394 | 0.351 | 0.321 | 0.300 | 0.284 | 1.271 | 4.670 |

| 0.6 | 7.499 | 2.816 | 1.193 | 0.748 | 0.561 | 0.463 | 0.403 | 0.363 | 0.335 | 0.314 | 1.469 | 5.066 |

| 0.7 | 7.500 | 4.049 | 1.610 | 0.946 | 0.680 | 0.544 | 0.463 | 0.410 | 0.373 | 0.346 | 1.692 | 5.433 |

| 0.8 | 7.500 | 5.414 | 2.147 | 1.193 | 0.822 | 0.638 | 0.531 | 0.463 | 0.416 | 0.381 | 1.951 | 6.161 |

| 0.9 | 7.500 | 6.591 | 2.816 | 1.495 | 0.991 | 0.748 | 0.610 | 0.522 | 0.463 | 0.420 | 2.216 | 7.038 |

| 1.0 | 7.500 | 7.269 | 3.612 | 1.863 | 1.193 | 0.875 | 0.699 | 0.589 | 0.515 | 0.463 | 2.458 | 7.633 |

| Expectation | 5.465 | 3.069 | 1.393 | 0.817 | 0.587 | 0.473 | 0.406 | 0.362 | 0.332 | 0.310 | ||

| Variance | 8.250 | 6.830 | 1.306 | 0.304 | 0.109 | 0.051 | 0.028 | 0.017 | 0.012 | 0.008 | ||

| Expectation | Variance | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | 1.0 | |||

| qh = 0.01 ψ = 0.2 | ||||||||||||

| 0.1 | 0.364 | 0.224 | 0.190 | 0.175 | 0.167 | 0.161 | 0.158 | 0.155 | 0.153 | 0.151 | 0.190 | 0.004 |

| 0.2 | 0.928 | 0.364 | 0.263 | 0.224 | 0.203 | 0.190 | 0.181 | 0.175 | 0.170 | 0.167 | 0.287 | 0.054 |

| 0.3 | 2.138 | 0.585 | 0.364 | 0.286 | 0.247 | 0.224 | 0.209 | 0.198 | 0.190 | 0.184 | 0.462 | 0.361 |

| 0.4 | 3.903 | 0.928 | 0.500 | 0.364 | 0.300 | 0.263 | 0.240 | 0.224 | 0.212 | 0.203 | 0.714 | 1.304 |

| 0.5 | 4.919 | 1.435 | 0.684 | 0.462 | 0.364 | 0.310 | 0.276 | 0.253 | 0.236 | 0.224 | 0.916 | 2.113 |

| 0.6 | 5.000 | 2.138 | 0.928 | 0.585 | 0.441 | 0.364 | 0.317 | 0.286 | 0.263 | 0.247 | 1.057 | 2.249 |

| 0.7 | 5.000 | 3.007 | 1.245 | 0.739 | 0.533 | 0.427 | 0.364 | 0.322 | 0.293 | 0.272 | 1.220 | 2.457 |

| 0.8 | 5.000 | 3.903 | 1.648 | 0.928 | 0.643 | 0.500 | 0.417 | 0.364 | 0.327 | 0.300 | 1.403 | 2.810 |

| 0.9 | 5.000 | 4.590 | 2.138 | 1.158 | 0.773 | 0.585 | 0.478 | 0.410 | 0.364 | 0.330 | 1.583 | 3.168 |

| 1.0 | 5.000 | 4.919 | 2.705 | 1.435 | 0.928 | 0.684 | 0.547 | 0.462 | 0.405 | 0.364 | 1.745 | 3.363 |

| Expectation | 3.725 | 2.209 | 1.066 | 0.636 | 0.460 | 0.371 | 0.319 | 0.285 | 0.261 | 0.244 | ||

| Variance | 3.470 | 3.194 | 0.733 | 0.180 | 0.065 | 0.031 | 0.017 | 0.011 | 0.007 | 0.005 | ||

| qh = 0.01 ψ = 0.4 | ||||||||||||

| 0.1 | 0.208 | 0.127 | 0.108 | 0.099 | 0.095 | 0.091 | 0.089 | 0.088 | 0.087 | 0.086 | 0.108 | 0.001 |

| 0.2 | 0.545 | 0.208 | 0.150 | 0.127 | 0.115 | 0.108 | 0.103 | 0.099 | 0.097 | 0.095 | 0.165 | 0.019 |

| 0.3 | 1.347 | 0.338 | 0.208 | 0.163 | 0.140 | 0.127 | 0.118 | 0.112 | 0.108 | 0.104 | 0.277 | 0.146 |

| 0.4 | 2.870 | 0.545 | 0.288 | 0.208 | 0.171 | 0.150 | 0.136 | 0.127 | 0.120 | 0.115 | 0.473 | 0.726 |

| 0.5 | 4.508 | 0.867 | 0.397 | 0.265 | 0.208 | 0.177 | 0.157 | 0.144 | 0.134 | 0.127 | 0.698 | 1.842 |

| 0.6 | 4.991 | 1.347 | 0.545 | 0.338 | 0.253 | 0.208 | 0.181 | 0.163 | 0.150 | 0.140 | 0.832 | 2.270 |

| 0.7 | 5.000 | 2.020 | 0.744 | 0.430 | 0.307 | 0.245 | 0.208 | 0.184 | 0.167 | 0.155 | 0.946 | 2.350 |

| 0.8 | 5.000 | 2.870 | 1.007 | 0.545 | 0.372 | 0.288 | 0.239 | 0.208 | 0.186 | 0.171 | 1.089 | 2.564 |

| 0.9 | 5.000 | 3.775 | 1.347 | 0.689 | 0.451 | 0.338 | 0.275 | 0.235 | 0.208 | 0.189 | 1.251 | 2.936 |

| 1.0 | 5.000 | 4.508 | 1.773 | 0.867 | 0.545 | 0.397 | 0.316 | 0.265 | 0.232 | 0.208 | 1.411 | 3.337 |

| Expectation | 3.447 | 1.660 | 0.657 | 0.373 | 0.266 | 0.213 | 0.182 | 0.163 | 0.149 | 0.139 | ||

| Variance | 4.090 | 2.484 | 0.314 | 0.066 | 0.023 | 0.011 | 0.006 | 0.004 | 0.002 | 0.002 | ||

| qh = 0.01 ψ = 0.6 | ||||||||||||

| 0.1 | 0.159 | 0.097 | 0.082 | 0.076 | 0.072 | 0.070 | 0.068 | 0.067 | 0.066 | 0.065 | 0.082 | 0.001 |

| 0.2 | 0.421 | 0.159 | 0.115 | 0.097 | 0.088 | 0.082 | 0.079 | 0.076 | 0.074 | 0.072 | 0.126 | 0.011 |

| 0.3 | 1.063 | 0.260 | 0.159 | 0.124 | 0.107 | 0.097 | 0.091 | 0.086 | 0.082 | 0.080 | 0.215 | 0.092 |

| 0.4 | 2.390 | 0.421 | 0.221 | 0.159 | 0.131 | 0.115 | 0.104 | 0.097 | 0.092 | 0.088 | 0.382 | 0.508 |

| 0.5 | 4.146 | 0.675 | 0.305 | 0.204 | 0.159 | 0.135 | 0.120 | 0.110 | 0.103 | 0.097 | 0.605 | 1.578 |

| 0.6 | 4.959 | 1.063 | 0.421 | 0.260 | 0.194 | 0.159 | 0.138 | 0.124 | 0.115 | 0.107 | 0.754 | 2.267 |

| 0.7 | 5.000 | 1.629 | 0.578 | 0.331 | 0.236 | 0.188 | 0.159 | 0.141 | 0.128 | 0.118 | 0.851 | 2.336 |

| 0.8 | 5.000 | 2.390 | 0.787 | 0.421 | 0.286 | 0.221 | 0.183 | 0.159 | 0.143 | 0.131 | 0.972 | 2.476 |

| 0.9 | 5.000 | 3.288 | 1.063 | 0.534 | 0.347 | 0.260 | 0.211 | 0.180 | 0.159 | 0.144 | 1.119 | 2.780 |

| 1.0 | 5.000 | 4.146 | 1.419 | 0.675 | 0.421 | 0.305 | 0.242 | 0.204 | 0.178 | 0.159 | 1.275 | 3.203 |

| Expectation | 3.314 | 1.413 | 0.515 | 0.288 | 0.204 | 0.163 | 0.140 | 0.124 | 0.114 | 0.106 | ||

| Variance | 4.334 | 2.030 | 0.201 | 0.040 | 0.014 | 0.006 | 0.003 | 0.002 | 0.001 | 0.001 | ||

| Expectation | Variance | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | 1.0 | |||

| 0.1 | 0.920 | 0.851 | 0.792 | 0.741 | 0.696 | 0.656 | 0.621 | 0.589 | 0.560 | 0.534 | 0.696 | 0.017 |

| 0.2 | 0.929 | 0.868 | 0.814 | 0.766 | 0.724 | 0.686 | 0.652 | 0.621 | 0.593 | 0.567 | 0.722 | 0.015 |

| 0.3 | 0.938 | 0.882 | 0.833 | 0.790 | 0.750 | 0.715 | 0.682 | 0.652 | 0.625 | 0.600 | 0.747 | 0.013 |

| 0.4 | 0.945 | 0.896 | 0.851 | 0.811 | 0.775 | 0.741 | 0.711 | 0.683 | 0.656 | 0.632 | 0.770 | 0.011 |

| 0.5 | 0.952 | 0.908 | 0.868 | 0.831 | 0.798 | 0.766 | 0.738 | 0.711 | 0.686 | 0.663 | 0.792 | 0.009 |

| 0.6 | 0.958 | 0.919 | 0.883 | 0.849 | 0.819 | 0.790 | 0.763 | 0.738 | 0.715 | 0.693 | 0.813 | 0.008 |

| 0.7 | 0.963 | 0.928 | 0.896 | 0.866 | 0.838 | 0.811 | 0.787 | 0.763 | 0.742 | 0.721 | 0.831 | 0.007 |

| 0.8 | 0.967 | 0.937 | 0.908 | 0.881 | 0.855 | 0.831 | 0.809 | 0.787 | 0.767 | 0.747 | 0.849 | 0.005 |

| 0.9 | 0.971 | 0.944 | 0.919 | 0.894 | 0.871 | 0.850 | 0.829 | 0.809 | 0.790 | 0.772 | 0.865 | 0.004 |

| 1.0 | 0.975 | 0.951 | 0.928 | 0.907 | 0.886 | 0.866 | 0.847 | 0.829 | 0.812 | 0.795 | 0.880 | 0.004 |

| Expectation | 0.952 | 0.908 | 0.869 | 0.834 | 0.801 | 0.771 | 0.744 | 0.718 | 0.695 | 0.673 | ||

| Variance | 0.000 | 0.001 | 0.002 | 0.003 | 0.004 | 0.005 | 0.006 | 0.007 | 0.007 | 0.008 | ||

| 0.1 | 0.919 | 0.850 | 0.791 | 0.740 | 0.694 | 0.654 | 0.619 | 0.587 | 0.558 | 0.532 | 0.694 | 0.017 |

| 0.2 | 0.928 | 0.866 | 0.811 | 0.763 | 0.721 | 0.683 | 0.648 | 0.617 | 0.589 | 0.564 | 0.719 | 0.015 |

| 0.3 | 0.936 | 0.880 | 0.830 | 0.786 | 0.746 | 0.710 | 0.677 | 0.647 | 0.620 | 0.595 | 0.743 | 0.013 |

| 0.4 | 0.943 | 0.893 | 0.848 | 0.807 | 0.769 | 0.735 | 0.704 | 0.676 | 0.649 | 0.625 | 0.765 | 0.011 |

| 0.5 | 0.950 | 0.905 | 0.863 | 0.826 | 0.791 | 0.759 | 0.730 | 0.703 | 0.678 | 0.655 | 0.786 | 0.010 |

| 0.6 | 0.956 | 0.915 | 0.878 | 0.843 | 0.812 | 0.782 | 0.755 | 0.729 | 0.705 | 0.683 | 0.806 | 0.008 |

| 0.7 | 0.961 | 0.924 | 0.891 | 0.859 | 0.830 | 0.803 | 0.778 | 0.754 | 0.731 | 0.710 | 0.824 | 0.007 |

| 0.8 | 0.965 | 0.933 | 0.903 | 0.874 | 0.848 | 0.822 | 0.799 | 0.777 | 0.755 | 0.735 | 0.841 | 0.006 |

| 0.9 | 0.969 | 0.940 | 0.913 | 0.888 | 0.863 | 0.840 | 0.819 | 0.798 | 0.778 | 0.760 | 0.857 | 0.005 |

| 1.0 | 0.973 | 0.947 | 0.923 | 0.900 | 0.878 | 0.857 | 0.837 | 0.818 | 0.800 | 0.782 | 0.871 | 0.004 |

| Expectation | 0.950 | 0.905 | 0.865 | 0.829 | 0.795 | 0.765 | 0.737 | 0.711 | 0.686 | 0.664 | ||

| Variance | 0.000 | 0.001 | 0.002 | 0.003 | 0.004 | 0.005 | 0.005 | 0.006 | 0.007 | 0.007 | ||

| 0.1 | 0.919 | 0.850 | 0.790 | 0.739 | 0.693 | 0.653 | 0.617 | 0.585 | 0.557 | 0.530 | 0.693 | 0.017 |

| 0.2 | 0.927 | 0.865 | 0.810 | 0.761 | 0.719 | 0.680 | 0.646 | 0.615 | 0.587 | 0.561 | 0.717 | 0.015 |

| 0.3 | 0.935 | 0.878 | 0.828 | 0.783 | 0.743 | 0.706 | 0.673 | 0.643 | 0.616 | 0.591 | 0.740 | 0.013 |

| 0.4 | 0.942 | 0.891 | 0.845 | 0.803 | 0.765 | 0.731 | 0.700 | 0.671 | 0.644 | 0.620 | 0.761 | 0.012 |

| 0.5 | 0.948 | 0.902 | 0.860 | 0.822 | 0.786 | 0.754 | 0.725 | 0.697 | 0.672 | 0.648 | 0.781 | 0.010 |

| 0.6 | 0.954 | 0.912 | 0.874 | 0.839 | 0.806 | 0.776 | 0.748 | 0.722 | 0.698 | 0.675 | 0.801 | 0.009 |

| 0.7 | 0.959 | 0.922 | 0.887 | 0.855 | 0.825 | 0.797 | 0.771 | 0.746 | 0.723 | 0.702 | 0.818 | 0.007 |

| 0.8 | 0.964 | 0.930 | 0.899 | 0.869 | 0.842 | 0.816 | 0.791 | 0.769 | 0.747 | 0.727 | 0.835 | 0.006 |

| 0.9 | 0.968 | 0.938 | 0.909 | 0.882 | 0.857 | 0.833 | 0.811 | 0.790 | 0.769 | 0.750 | 0.851 | 0.005 |

| 1.0 | 0.971 | 0.944 | 0.919 | 0.894 | 0.872 | 0.850 | 0.829 | 0.809 | 0.790 | 0.772 | 0.865 | 0.004 |

| Expectation | 0.949 | 0.903 | 0.862 | 0.825 | 0.791 | 0.760 | 0.731 | 0.705 | 0.680 | 0.658 | ||

| Variance | 0.000 | 0.001 | 0.002 | 0.003 | 0.004 | 0.004 | 0.005 | 0.006 | 0.006 | 0.007 | ||

| Expectation | Variance | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | 1.0 | |||

| 0.1 | 0.890 | 0.801 | 0.729 | 0.668 | 0.617 | 0.573 | 0.535 | 0.502 | 0.472 | 0.446 | 0.623 | 0.020 |

| 0.2 | 0.866 | 0.764 | 0.684 | 0.618 | 0.564 | 0.519 | 0.481 | 0.448 | 0.419 | 0.393 | 0.576 | 0.022 |

| 0.3 | 0.839 | 0.723 | 0.635 | 0.566 | 0.511 | 0.465 | 0.427 | 0.395 | 0.367 | 0.343 | 0.527 | 0.024 |

| 0.4 | 0.808 | 0.677 | 0.583 | 0.512 | 0.457 | 0.412 | 0.375 | 0.344 | 0.318 | 0.296 | 0.478 | 0.025 |

| 0.5 | 0.772 | 0.628 | 0.530 | 0.458 | 0.403 | 0.360 | 0.326 | 0.297 | 0.273 | 0.253 | 0.430 | 0.026 |

| 0.6 | 0.731 | 0.576 | 0.476 | 0.405 | 0.353 | 0.312 | 0.280 | 0.254 | 0.232 | 0.214 | 0.383 | 0.025 |

| 0.7 | 0.687 | 0.523 | 0.422 | 0.354 | 0.305 | 0.268 | 0.238 | 0.215 | 0.196 | 0.180 | 0.339 | 0.024 |

| 0.8 | 0.638 | 0.469 | 0.370 | 0.306 | 0.261 | 0.227 | 0.201 | 0.181 | 0.164 | 0.150 | 0.297 | 0.022 |

| 0.9 | 0.587 | 0.415 | 0.321 | 0.262 | 0.221 | 0.191 | 0.169 | 0.151 | 0.136 | 0.124 | 0.258 | 0.019 |

| 1.0 | 0.533 | 0.364 | 0.276 | 0.222 | 0.186 | 0.160 | 0.140 | 0.125 | 0.113 | 0.103 | 0.222 | 0.017 |

| Expectation | 0.735 | 0.594 | 0.503 | 0.437 | 0.388 | 0.349 | 0.317 | 0.291 | 0.269 | 0.250 | ||

| Variance | 0.015 | 0.023 | 0.024 | 0.023 | 0.022 | 0.020 | 0.018 | 0.017 | 0.015 | 0.014 | ||

| 0.1 | 0.897 | 0.814 | 0.744 | 0.686 | 0.636 | 0.593 | 0.593 | 0.522 | 0.492 | 0.466 | 0.644 | 0.018 |

| 0.2 | 0.884 | 0.792 | 0.718 | 0.656 | 0.604 | 0.560 | 0.560 | 0.488 | 0.459 | 0.433 | 0.615 | 0.020 |

| 0.3 | 0.869 | 0.769 | 0.689 | 0.625 | 0.571 | 0.526 | 0.526 | 0.454 | 0.425 | 0.400 | 0.586 | 0.021 |

| 0.4 | 0.853 | 0.744 | 0.660 | 0.592 | 0.538 | 0.492 | 0.492 | 0.421 | 0.393 | 0.368 | 0.555 | 0.022 |

| 0.5 | 0.835 | 0.717 | 0.629 | 0.559 | 0.504 | 0.458 | 0.458 | 0.388 | 0.361 | 0.337 | 0.525 | 0.024 |

| 0.6 | 0.816 | 0.689 | 0.596 | 0.526 | 0.470 | 0.425 | 0.425 | 0.357 | 0.330 | 0.307 | 0.494 | 0.024 |

| 0.7 | 0.795 | 0.659 | 0.563 | 0.492 | 0.436 | 0.392 | 0.392 | 0.326 | 0.301 | 0.279 | 0.464 | 0.025 |

| 0.8 | 0.772 | 0.628 | 0.530 | 0.458 | 0.403 | 0.360 | 0.360 | 0.297 | 0.273 | 0.253 | 0.434 | 0.025 |

| 0.9 | 0.747 | 0.596 | 0.496 | 0.425 | 0.371 | 0.330 | 0.330 | 0.270 | 0.247 | 0.228 | 0.404 | 0.025 |

| 1.0 | 0.721 | 0.563 | 0.462 | 0.392 | 0.340 | 0.301 | 0.301 | 0.244 | 0.223 | 0.205 | 0.375 | 0.024 |

| Expectation | 0.819 | 0.697 | 0.609 | 0.541 | 0.487 | 0.444 | 0.444 | 0.377 | 0.350 | 0.327 | ||

| Variance | 0.004 | 0.007 | 0.009 | 0.010 | 0.010 | 0.010 | 0.010 | 0.009 | 0.008 | 0.008 | ||

| 0.1 | 0.920 | 0.851 | 0.792 | 0.741 | 0.696 | 0.656 | 0.621 | 0.589 | 0.560 | 0.534 | 0.696 | 0.015 |

| 0.2 | 0.929 | 0.868 | 0.814 | 0.766 | 0.724 | 0.686 | 0.652 | 0.621 | 0.593 | 0.567 | 0.722 | 0.013 |

| 0.3 | 0.938 | 0.882 | 0.833 | 0.790 | 0.750 | 0.715 | 0.682 | 0.652 | 0.625 | 0.600 | 0.747 | 0.011 |

| 0.4 | 0.945 | 0.896 | 0.851 | 0.811 | 0.775 | 0.741 | 0.711 | 0.683 | 0.656 | 0.632 | 0.770 | 0.010 |

| 0.5 | 0.952 | 0.908 | 0.868 | 0.831 | 0.798 | 0.766 | 0.738 | 0.711 | 0.686 | 0.663 | 0.792 | 0.008 |

| 0.6 | 0.958 | 0.919 | 0.883 | 0.849 | 0.819 | 0.790 | 0.763 | 0.738 | 0.715 | 0.693 | 0.813 | 0.007 |

| 0.7 | 0.963 | 0.928 | 0.896 | 0.866 | 0.838 | 0.811 | 0.787 | 0.763 | 0.742 | 0.721 | 0.831 | 0.006 |

| 0.8 | 0.967 | 0.937 | 0.908 | 0.881 | 0.855 | 0.831 | 0.809 | 0.787 | 0.767 | 0.747 | 0.849 | 0.005 |

| 0.9 | 0.971 | 0.944 | 0.919 | 0.894 | 0.871 | 0.850 | 0.829 | 0.809 | 0.790 | 0.772 | 0.865 | 0.004 |

| 1.0 | 0.975 | 0.951 | 0.928 | 0.907 | 0.886 | 0.866 | 0.847 | 0.829 | 0.812 | 0.795 | 0.880 | 0.003 |

| Expectation | 0.952 | 0.908 | 0.869 | 0.834 | 0.801 | 0.771 | 0.744 | 0.718 | 0.695 | 0.673 | ||

| Variance | 0.000 | 0.001 | 0.002 | 0.003 | 0.004 | 0.005 | 0.006 | 0.007 | 0.007 | 0.008 | ||

| 0.1 | 0.925 | 0.861 | 0.805 | 0.756 | 0.713 | 0.674 | 0.640 | 0.608 | 0.580 | 0.554 | 0.712 | 0.014 |

| 0.2 | 0.939 | 0.885 | 0.837 | 0.794 | 0.755 | 0.720 | 0.688 | 0.659 | 0.632 | 0.607 | 0.752 | 0.011 |

| 0.3 | 0.950 | 0.906 | 0.865 | 0.827 | 0.793 | 0.762 | 0.732 | 0.706 | 0.680 | 0.657 | 0.788 | 0.009 |

| 0.4 | 0.960 | 0.923 | 0.888 | 0.856 | 0.826 | 0.799 | 0.773 | 0.748 | 0.726 | 0.704 | 0.820 | 0.007 |

| 0.5 | 0.967 | 0.937 | 0.908 | 0.881 | 0.855 | 0.831 | 0.809 | 0.787 | 0.767 | 0.747 | 0.849 | 0.005 |

| 0.6 | 0.974 | 0.948 | 0.925 | 0.902 | 0.880 | 0.860 | 0.840 | 0.821 | 0.803 | 0.786 | 0.874 | 0.004 |

| 0.7 | 0.979 | 0.958 | 0.938 | 0.919 | 0.901 | 0.884 | 0.867 | 0.851 | 0.835 | 0.820 | 0.895 | 0.003 |

| 0.8 | 0.983 | 0.966 | 0.950 | 0.934 | 0.919 | 0.904 | 0.890 | 0.876 | 0.863 | 0.850 | 0.914 | 0.002 |

| 0.9 | 0.986 | 0.972 | 0.959 | 0.946 | 0.934 | 0.921 | 0.910 | 0.898 | 0.887 | 0.876 | 0.929 | 0.001 |

| 1.0 | 0.989 | 0.978 | 0.967 | 0.956 | 0.946 | 0.936 | 0.926 | 0.916 | 0.907 | 0.897 | 0.942 | 0.001 |

| Expectation | 0.965 | 0.933 | 0.904 | 0.877 | 0.852 | 0.829 | 0.807 | 0.787 | 0.768 | 0.750 | ||

| Variance | 0.000 | 0.002 | 0.003 | 0.005 | 0.006 | 0.008 | 0.009 | 0.011 | 0.012 | 0.014 | ||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chen, T.; Hou, Y.; Wang, L.; Li, Z. Counterparty Risk Contagion Model of Carbon Quota Based on Asset Price Reduction. Sustainability 2023, 15, 11377. https://doi.org/10.3390/su151411377

Chen T, Hou Y, Wang L, Li Z. Counterparty Risk Contagion Model of Carbon Quota Based on Asset Price Reduction. Sustainability. 2023; 15(14):11377. https://doi.org/10.3390/su151411377

Chicago/Turabian StyleChen, Tingqiang, Yuejuan Hou, Lei Wang, and Zeyu Li. 2023. "Counterparty Risk Contagion Model of Carbon Quota Based on Asset Price Reduction" Sustainability 15, no. 14: 11377. https://doi.org/10.3390/su151411377

APA StyleChen, T., Hou, Y., Wang, L., & Li, Z. (2023). Counterparty Risk Contagion Model of Carbon Quota Based on Asset Price Reduction. Sustainability, 15(14), 11377. https://doi.org/10.3390/su151411377